AI is transforming the way platforms are built. Open integration, flexible data structures, and meeting partners where they are will define the next market leaders.

The insurance agencies capturing disproportionate value from using AI are restructuring their workflows. Here are some ways that leading agencies operate differently by leveraging AI.

Insurers are deploying AI to combat increasingly sophisticated fraud schemes, but detection still hinges on fundamental prevention and deterrence strategies.

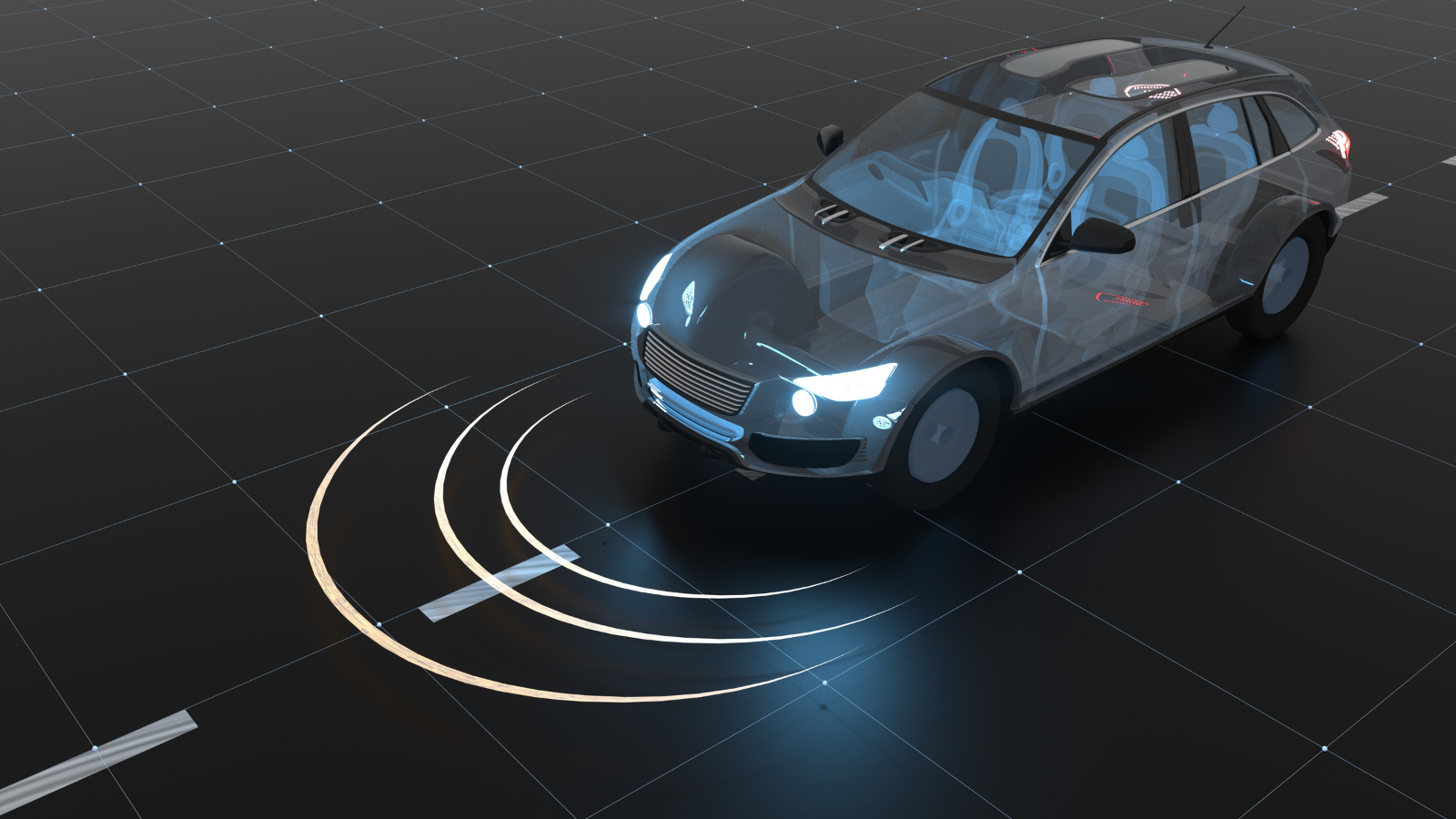

Autonomous and electric vehicles are shifting liability from drivers to manufacturers, reshaping commercial auto insurance underwriting's fundamentals.

AI-driven discovery of software vulnerabilities at machine speed challenges cyber underwriting models designed for environments where threats evolved gradually.

As AI shifts from advisory tool to autonomous decision-maker, insurers face new risk categories that traditional frameworks weren't designed to address.

As agencies embrace multi-line distribution, fragmented operational systems increasingly constrain their ability to scale and deliver integrated value.

Insurers are turning to scenario-based machine learning for portfolio optimization as traditional methods falter under regulatory and economic complexity.

Routing commercial trucking claims through general adjusting operations costs carriers millions in preventable loss ratio leakage that specialty programs consistently avoid.

As generating traffic becomes a commodity capability, competitive advantage shifts from managing customer relationships to participating in their decisions.

AI penetration testing transforms annual compliance snapshots into continuous security assurance without sacrificing the depth of manual expert testing.

The shift is from advisory systems to delegated systems. A chatbot may suggest. An agent may act. That single difference changes the risk model entirely.

Regulators aren't asking if your AI works—they're asking which named human was accountable when it didn't. If there isn't one, the person on the hook may be you.

Life insurers are advancing from AI experimentation to execution, prioritizing ecosystem integration to address escalating retirement security demands.

Commercial buildings lose their documented history through ownership transfers, creating costly underwriting and claims exposure for property insurers.

Unlike traditional property claims, wildfire losses function as multi-year community rebuilding projects governed by regulatory complexity and shared constraints.

The difference between catching fraud before payment and spending weeks recovering funds typically comes down to whether data is handled in real time or in batches.

Three converging trends—private machine learning systems, vendor large language models, and market expansion—push reinsurers toward integration over replacement.

Inadequate documentation turns routine forklift accidents into nuclear verdicts as social inflation drives claim severity to multimillion-dollar levels.

The call center isn't a cost center. It's the moment of truth. And, despite investing billions in technology, insurers still fail customers when it matters most.

AI enables overwhelmed workers' comp brokers to shift from transactional quoting to strategic risk advisory relationships that employers increasingly demand.

Fraud networks exploit multiple digital identities across accounts and websites, making digital entity resolution critical for preventing fraudulent payments.

Gen Z is driving insurtech innovation by demanding mobile experiences, personalized pricing, and transparency in an industry traditionally resistant to change.

AI isn't just allowing for efficiencies in underwriting, it's letting carriers make much faster, smarter decisions on how to manage their whole portfolio.

Deceased policyholders' digital accounts remain accessible to fraudsters but locked to legitimate beneficiaries, creating costly exposure for life insurers.

While claims technology has improved for decades, too little has been done to leverage it. It's time to move beyond document storage and into effective decision-making.

Insurance standardization has quietly shifted workforce behavior from critical thinking to process execution, a dangerous trend that AI will accelerate.

Making healthcare affordable requires rethinking system design through financial protection, cost discipline and shared digital infrastructure, not just pricing fixes.

Developers who automated other industries now face AI displacement themselves, as technical certifications prove less valuable than human judgment and accountability.

As carrier appetites shift and underwriting tightens, independent agencies turn to AI automation to streamline workflows and boost operational efficiency.

For decades, insurance professionals could lean on muscle memory. But the environment has changed. Decisions must now be documented, explainable, and consistent over time.

Platform consolidation among carriers usually promises modernization, but group benefits relies on "frankenstacks," so merging may deliver rigidity when adaptability matters most.

Sophisticated fraud thrives in fragmented data. Entity resolution, knowledge graphs, and geospatial analytics can unite disparate records and expose hidden networks.

Insurers must replace fragmented legacy systems with unified, 360-degree customer views to meet heightened digital expectations and competitive pressures.

The insurance industry is at a pivotal moment. While automation has streamlined repetitive tasks, the next wave of transformation is here: AI agents that don't just execute—they think, learn, and adapt.

Hybrid fronting carriers retain some underwriting risk to tighten alignment with reinsurers and capital partners, resulting in more disciplined underwriting and oversight.

Cybersecurity regulations are increasing nationwide, primarily through enhanced MFA requirements. Using SignOn Once helps with compliance and make workflows easier, improving productivity and customer satisfaction.)

Rather than inferring exposure solely from historical outcomes, commercial auto underwriters can now access leading indicators of attentiveness, distraction, and behavioral discipline.

Ukrainian insurers are transforming war risk from theoretical construct into operational reality, handling claims complexity most markets only simulate.

Entity resolution and digital domain mapping bridge the physical and digital divide, transforming fragmented data into comprehensive risk intelligence.

Despite $10 billion in AI investment, only 7% of carriers achieve scale. It's time to decide if you must take the stairs, can find an escalator or, in the best case, can catch an elevator.

Digital skills expire faster than training programs can replace them, forcing enterprises to prioritize adaptability over traditional reskilling approaches.

Sedgwick's annual study finds Fortune 500 executives identify resilience as 2026's defining business challenge amid AI uncertainty, catastrophe risks, and cyber threats.

(Re)insurers must watch out for AI-related risks, geoeconomic confrontation, unsettled regulatory and legal environments, technological acceleration, and global inflation shocks.

Hyper-personalization is revolutionizing life insurance as carriers tailor applications, products and pricing to individual customer and agent preferences.

While insurance has for centuries run on an annual cycle of risk assessment and policy renewals, advances in technology now make it possible to assess and underwrite risk in real time.

Join Paul Carroll, Editor-in-Chief at Insurance Thought Leadership, along with industry experts Taylor Smith, President of Suite 200, and Rose Hall, CEO of RH Business Ventures, as they tackle the challenges facing claims management today.

The government shutdown crisis spotlights transparent health reinsurance as an emerging, nonpartisan solution aligning corporate and consumer interests.

Embedded insurance is transforming from a distribution tactic to a customer experience strategy as insurers prioritize seamless, friction-free protection.

Exploring how Generative AI could transform workers’ compensation — from smarter claims management and cost control to worker-centric care models and next-gen risk oversight.

Nancy Watkins and Francis Bouchard join ITL Editor-in-Chief Paul Carroll to explore how the insurance industry needs to expand its conversation about resilience beyond traditional boundaries.

MGAs are rapidly reshaping insurance with specialization, speed, and innovation, but need modern, AI-enabled foundations to stay competitive. Read the full report to explore what’s next.

Paul Hill and Marty Ellingsworth explain how a data source can predict financial health, going beyond the backward-looking credit reports that insurers use.

AI adoption is evolving and moving faster than ever making a bigger mark in insurance claims, but with innovation comes new risks and responsibilities.

AI can transform trust from an abstract idea into measurable, actionable frameworks—reshaping customer relationships and redefining the future of insurance.

In this webinar, Bolt will highlight how agencies are using conversational and workflow AI to simplify quoting, binding, and renewals while giving teams more time to focus on customers.

Cyber claim severity has dropped 50% for large insureds as ransomware attackers shift focus to less resilient, smaller companies, but the scope of potential losses is broadening for everyone.

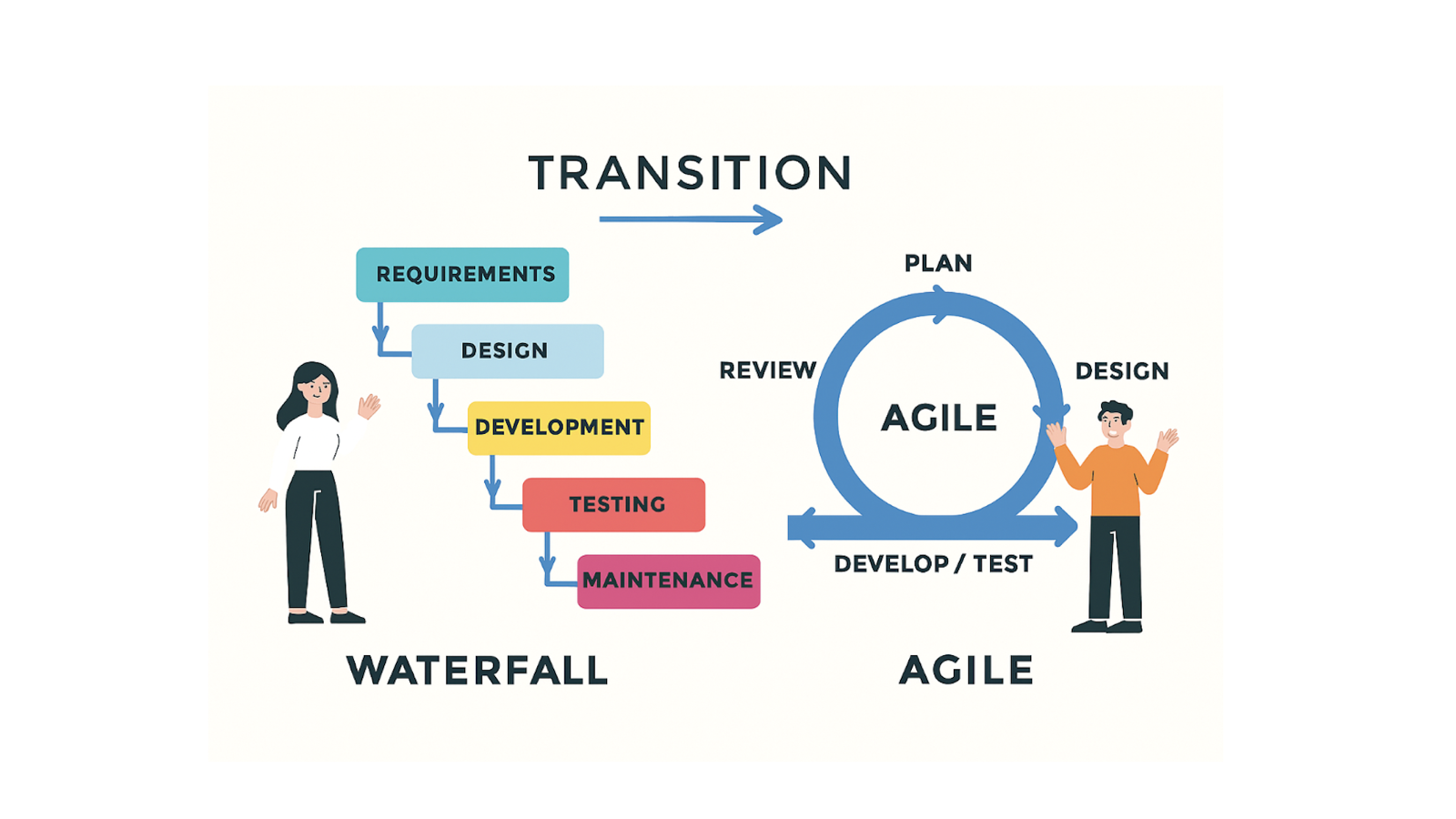

Workers' compensation insurers must shift from inflexible waterfall development to agile frameworks, which promise enhanced collaboration and responsiveness.

Insurers chase flashy AI experiments while missing practical applications in underwriting, claims processing, and customer engagement that deliver real results.

Insurers face a critical 18-month window to transform by embracing AI, data-driven innovation, capital flexibility, digital ecosystems, and data-driven decision-making.

Still, Michel Léonard, chief economist for the Triple-I, says the economy and thus the insurance industry will end the year in a better place than expected.

Every insurance organization and risk management firm is somewhere on the AI journey – but most don't know exactly where they stand or what comes next.

P&C insurers are embracing AI despite regulatory headwinds, potentially letting the technology blast through the intermediate stages of the Gartner Hype Cycle timeline.

Explore how GenAI and Agentic AI are transforming insurance, driving financial gains, operational efficiency, and customer value across the entire insurance value chain. Download now.

Munich Re’s alitheia platform helps life insurance carriers automate underwriting with patented AI and natural language processing—delivering faster, more accurate decisions through flexible, modular integration.

Rising stop-loss costs and the transparency advantages of self-funded arrangements are creating a fundamental shift in how smart employers approach healthcare benefits.

Trust, not technology, blocks AI adoption as insurance underwriters hesitate to rely on automated scoring and claims managers are reluctant to influence decisions.

Cyber risks hide in invisible digital neighborhoods, but breakthrough analytics now reveal organizational vulnerabilities across complex network connections.

While carriers rely on conventional detection methods, fraudsters increasingly leverage AI to orchestrate sophisticated, undetectable insurance schemes.

Adnan Haque, founder of Munich Re’s alitheia rapid risk assessment platform, discusses how tech and digital data are reshaping life insurance underwriting.

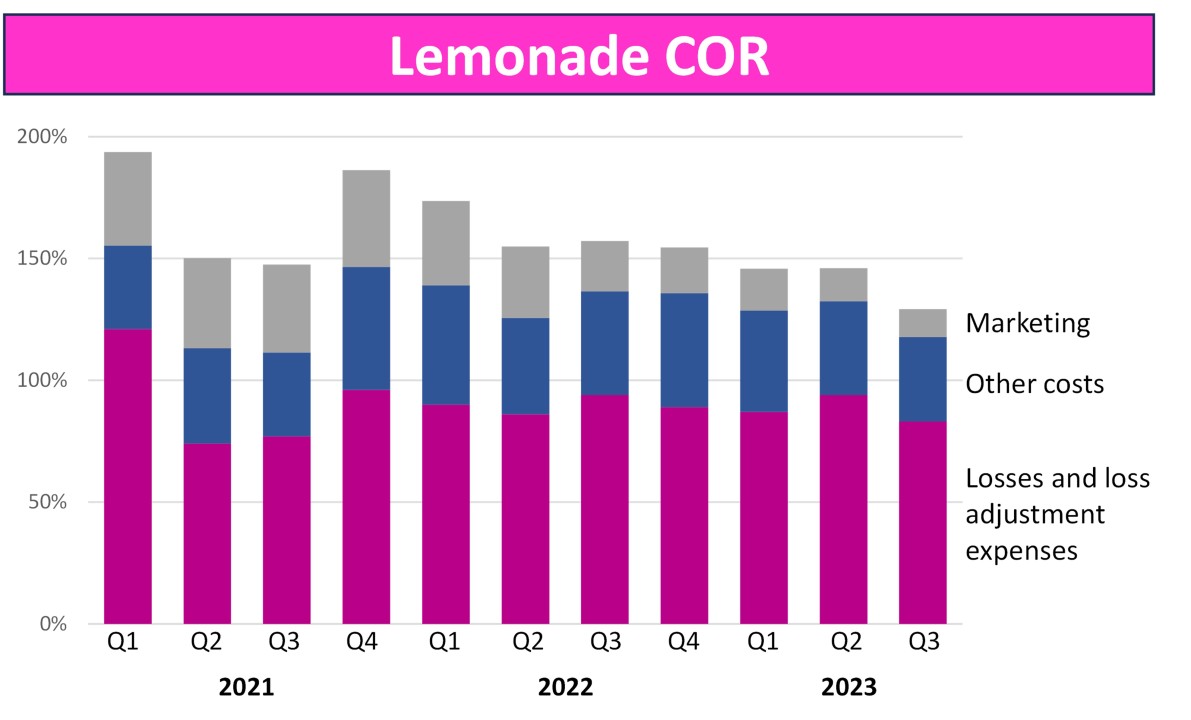

Turns out radical honesty, black-and-pink cartoons, and frictionless UX are more disruptive than massive ad spending. Lemonade made “boring” brilliant.

Proactive risk management through IoT sensors and real-time data is reshaping insurance underwriting. With bolt, carriers reduce claims severity and deliver better value to policyholders.

In this Future of Risk interview, Oliver Wyman’s Mick Moloney delves into the implications of the model that private equity is imposing on life insurance.

Executive personal devices become primary attack vectors as cybercriminals exploit the home-office security gap. Digital executive protection (DEP) is needed.

By deploying AI-powered multimodal technologies to sniff out fraudulent behaviors, insurers can help vanquish a multibillion-dollar drain on consumers.

Discover why now is the time for insurers to embrace tech-driven transformation. Learn how modern operating models unlock efficiency, innovation, and long-term profitable growth.

Integrating drones with AI and machine learning offers an unprecedented opportunity to rethink how property inspections and claims evaluations are conducted.

All players in the property insurance ecosystem must help clients and communities harness property insurance as a tool for climate adaptation - or risk irrelevance.

Baby Boomers are suffering from a catastrophic shift of pension risks from institutions to individuals, because of a misunderstanding of behavioral steering.

Automated data ingestion transforms commercial insurance operations, driving efficiency and revenue growth while laying the groundwork for AI advancement.

Analysis of trends from Q4 2024 suggest property and worker's comp rates will remain stable, while general liability and excess/umbrella markets are softening.

In this Future of Risk interview, Praedicat founder Dr. Robert Reville explains how it combs the scientific literature to spot risks like talcum powder years before mass litigation happens.

Michel Léonard, the Triple-I's chief economist, remains an optimist on the U.S. economy but warns that "we're in an environment of extraordinary uncertainty."

The insurance industry is shifting from traditional actuarial models to incorporate behavioral data in risk assessment practices. The implications are enormous.

The insurance industry has a pivotal opportunity to redefine itself. By prioritizing transparency, insurers can address premium leakage while restoring trust.

Don’t miss Majesco’s latest research report that highlights insurer’s top strategic priorities for 2025 and how they plan to compete in today’s changing market landscape.

In this Future of Risk interview, Gallagher Bassett's chief digital officer, Joe Powell, details how far AI has come in insurance and where it goes next (carefully).

In today's fast-paced risk environment, traditional roles in claims, insurance management, safety, and GRC are evolving into strategic positions crucial for organizational decision-making. Discover the four key ways to elevate your approach to risk by downloading the eBook.

"Generative AI isn’t just regurgitating pre-programmed responses anymore; it’s starting to think. Sort of....It’s not perfect, but it’s getting there—fast."

In this Future of Risk interview, Amy Radin says the traditional, top-down approach to change management no longer works. In the age of AI, she recommends the approaches revolutionaries use.

An analysis of 11,000 P&C verdicts shows the power of granular data to make judgments fairer--shaping all the settlements that are based on those damage amounts.

AI revolutionizes insurance operations while maintaining the human touch that builds customer trust and loyalty and allowing for hyper-personalized customer experiences.

Rather than use communications merely to satisfy operational and compliance requirements, insurers should leverage them to build trust and stand apart from competitors.

As extreme weather events increase in frequency and intensity, they don't just affect the environment but also the operational viability of businesses.

The lingering effects of rising premiums, coverage restrictions and evolving client expectations are making retaining business and maintaining strong relationships paramount.

Download Majesco’s new research report to better understand current industry challenges, the evolution of past trends, and the accelerating forces shaping the future of insurance through 2025.

Rising repair costs and climate disasters force insurers to push auto premiums to historic height, especially in Maryland, South Carolina, New York and seven other states.

Leveraging advanced analytics, AI, IoT sensors and telematics, insurers can now dynamically adjust premiums based on market conditions and behavioral patterns.

Insurers face critical choices between modern legacy systems and true cloud-native solutions for digital transformation. Five myths can lead to bad decisions.

It's time to move past small-scale, cautious pilot projects focused on efficiency and to start testing how generative AI can let us reinvent processes, governance, and structures.

In the face of ever-increasing premiums, auto owners are foregoing coverage, taking higher deductibles and not filing claims. This marks a profound change.

Dive into a new Majesco report that reveals strategies for insurers to engage tech-savvy, value-driven Millennials and Gen Z by addressing their expectations, leveraging technology, and building trust amid rising costs.

Security service edge (SSE) solutions are crucial for protecting data, but as the market has evolved and expanded to over 30 vendors, some cracks are beginning to show.

Discover how Integrated Risk Management (IRM) can unify your risk and safety efforts, boost visibility, and drive smarter decisions across your organization.

AI is transforming insurance by enhancing fraud detection, optimizing claims, and improving customer service. Success depends on ethical, accountable, and strategic implementation.

Think of agencies as a relay team: Connecting all systems, people, and stages of the client journey and policy lifecycle makes the baton handoffs much easier.

Embedded insurance promises to disrupt insurance distribution as well as product and help close the “protection gap”--the 50% of all economic losses not covered by insurance.

As the industry keeps making progress on reducing injuries, Bill Zachry describes how AI and other technologies can take workers' comp to a whole new level.

As carriers and agencies adapt to hybrid work models, AI-powered tools are becoming increasingly crucial for maintaining efficiency and quality of service.

The recent CrowdStrike outage and disruption to businesses of all sizes has refocused attention on the value of cyber insurance for non-malicious losses.

Choosing the right insurance carrier is crucial for brokers and agencies—and the issues go well beyond financial strength and products. Join us for a webinar that explores the often-overlooked elements that can take your carrier partnerships to the next level.

As insurers grapple with legacy systems and fragmented data, no-code predictive modeling tools provide a practical solution for unlocking insights into future risks and staying competitive in a rapidly changing market.

The on-demand economy is exploding, but building suitable auto insurance products and services for the drivers fueling this economy is taking far too long.

In this Future of Risk interview, Quizzify CEO Al Lewis lays out an unconventional, bottoms-up approach to healthcare: He educates consumers to only pursue care that will likely benefit them and not expose them to harm.

After four decades of running my own business, I’ve developed a set of tips to help strengthen client acquisition and retention efforts–-even in difficult circumstances.

Next-generation distribution management can be key to fostering growth, delivering exceptional agent experiences, and advancing the agency into its next evolutionary stage.

Current insurance types don't protect small businesses from trolls abusing the Americans with Disabilities Act. A new endorsement could address the problem.

Automating repetitive tasks can streamline workflows and allow for data-driven decisions with greater accuracy and speed.--but getting to scale can be tricky.

The Mediterranean shines the spotlight on the vulnerability of food supply chains to droughts, which are predicted to become more prevalent under climate change.

Historical data offers outdated information. Real-time data keeps you informed of changes to a policyholder’s risk profile, letting you adjust premiums.

Triple-I Chief Economist Dr. Michel Leonard discusses key geopolitical risk scenarios and their impact on the insurance industry in his latest quarterly interview with ITL.

New product technology are addressing the traditional pain points of data analysis, model development, and risk assessment for life insurance actuaries.

Here are six strategic steps carriers can take to better prepare for handling auto claims following severe weather, such as the recent Hurricane Helene.

If an insurer is evaluating risk for properties along a Florida coastline, a discrepancy of as little as 50 to 100 feet matters during hurricane season.

AI in pricing represents a breakthrough, with some insurers already shifting to automated solutions that promise more accurate risk assessment and increased profitability.

Although a life or AD&D claim involving one or both substances could seem straightforward, far too often carriers encounter complications during the process.

Parametric reinsurance offers a new approach to managing the increasing threat of secondary perils, providing much-needed financial protection for insurers.

Facing increasingly unpredictable and destructive wildfires, insurers grapple with complex challenges in risk assessment, coverage, and claims response.

The U.S. P&C insurance industry faces challenges. AI-based behavioral insights improve risk prediction, helping insurers stay competitive and profitable.

Learn more about the immense pressure the insurance industry is facing, forcing insurers to rethink operational models and update outdated technology to stay competitive and relevant.

This webinar will discuss the findings of an independent survey sponsored by insured.io on the importance of digital channels when customers are selecting an insurance carrier.

By embracing personalization, technology, prevention, ethical considerations, and collaboration, insurers can position themselves for long-term success.

Data visualization tools are empowering agencies with role-specific insights, enhancing decision-making and operational efficiency across the organization.

There are hopeful signs that insurers are finally embracing the benefits of technological innovation, as technology vendors are providing them with what they want.

While increased life expectancy benefits individuals and society, it presents business challenges, particularly in managing workers' compensation claims.

While the general outlook for the industry is positive, there are still lots of challenges to tackle, including soaring repair costs and a lack of mechanics.

By automating routine tasks, AI can free adjusters to focus on the human aspects of their work that require empathy, nuanced judgment and creative problem-solving.

Large language models will let insurers onboard, renew and service risks at close to zero marginal cost, underpinned with consistent control over risk selection.

The elections could affect Medicaid expansion, Obamacare's future, long-term funding of Medicare, strategies for negotiating drug prices and reproductive care.

Insurance agencies use generative AI to communicate but must integrate it into more sophisticated processes: policy analysis, document comparison -- and more.

The future is looking bright thanks to AI and business rules engines, which greatly reduce menial tasks and let underwriters take on more strategic issues.

Life insurance carriers need to be able to quickly and easily make product changes or develop new products, independent of their policy admin system vendor.

The crisis calls for collaboration on some combination of state-run plans, offerings from surplus lines insurers, litigation reform and risk mitigation.

37% of insurance companies acknowledge their resilience and agility are weak -- and firms that exhibit strong adaptability outperform competitors by up to 50%.

Four years on from COVID-19, life insurers have a key opportunity to assess the accuracy of their risk models and better prepare for the next global pandemic.

Skills-based hiring and skills-based salary levels can mean better results and access to a wider pool of talent at a time when AI is increasing the pace of change.

The insurance industry can no longer rely on current strategies and responses to this threat, nor can it continue to absorb and pass along the associated costs to policyholders.

AI requires using guardrails to account for technical limitations, leveraging GenAI’s strength at hyper-personalized interaction and ensuring human agents remain in the service flow.

Litigation risk looms large over the insurance industry, driven by digital transformation, more complex insurance products and heightened regulatory scrutiny.

In workers’ comp, generative AI can transform claims management by improving accuracy, enhancing documentation and, freeing adjusters to focus more on the injured workers.

Insurers that decide they can handle claims with young, inexpensive, inexperienced and untrained claims handlers should be accosted by angry stockholders.

Companies should revisit their risk exposures and ensure there are proper protections in place for the business as well as employees on trips that combine business and leisure. .

Mainframe modernization can let incumbents turn the tables on newcomers by taking full advantage of new approaches while leveraging their historical strengths.

Paul Carroll, editor-in-chief of Insurance Thought Leadership, recently sat down with Scott Frisch, EVP and chief operating officer at AARP, to discuss the power of what AARP has labeled the longevity economy.

Today's insurance CRM solutions capture customer data, likes, dislikes, preferences and more so insurers can finally realize their personalization goals.

Proponents rave that embedded insurance benefits the insurer, third parties and customers, but we should temper the hype--without spoiling the enthusiasm.

The future of the annuity business lies in leveraging digital technologies to enhance regulatory compliance, streamline operations and deliver superior customer experiences.

Risk mitigation is no longer just a nice bonus but instead a critical aspect of a strong insurance application, and crucial to limiting premium increases.

Dr. Michel Léonard of the Insurance Information Institute discusses the current economic landscape and its impact on the insurance industry for the rest of 2024 and beyond.

In this Future of Risk conversation, insurtech veteran Callie Thomas explores how the industry can ditch some very bad habits and pursue 10X improvement.

In this month's ITL Focus, we look at how a generational transfer of wealth will transform life insurance and at how to align incentives in health insurance.

A recent discussion revealed a global car insurance fraud exploiting lax verification to insure cars online and then steal them. This has led insurers to adopt stricter measures like multi-factor authentication.

Insurance carriers facing profitability challenges and shrinking market options turn to behavioral deep learning for sustainable solutions, managing risks effectively while serving stakeholders.

Insurance carriers stand on the verge of a transformative era fueled by AI's promises of personalized services, predictive analytics, and enhanced productivity, aligning with evolving customer expectations.

The State of Online Payments report reveals that 60% of respondents encounter monthly digital payment issues, emphasizing the need for streamlined solutions to enhance efficiency.

Imagine an application programming interface that retrieves weather records or property information instantly, eliminating the need for manual data entry.

Just as Underwriters Laboratory was set up to make electricity safe for the world, insurers have a huge opportunity (and responsibility) with climate change.

Imagine being able to access data all in one place, any time and to have the power to fulfill endless business needs. Technology is making that goal possible.

Selecting the right deployment model for insurance management software is crucial for optimizing operations, ensuring data security and maintaining resilience.

With stock market valuations for some big-name insurtechs taking such a hit, the public perception seems to be that innovation in insurance has paused.

Emerging tech like generative AI poses new fraud risks for insurers. They must adapt with improved security, detection tools, and data management to stay ahead.

Data security is no longer a simple IT task and can't be solved with one tool. It's a strategic imperative that touches every level of an organization.

In this month's ITL Focus, Paul Carroll interviews Jess Keeney, Duck Creek's Chief Product & Technology Officer, exploring the game-changing role of generative AI in underwriting and its implications for insurance technology and customer engagement.

Generative AI is all the rage in the world of business, including insurance, but is it everything it's cracked up to be? Deepak Dastrala, Chief Technology Officer of IntellectAI, says Gen AI may disappoint ... unless it's combined effectively with traditional AI.

AI-driven automation transforms insurance fraud detection, enhancing speed and accuracy while minimizing financial losses for a more customer-centric approach.

Paul Carroll, ITL Editor-in-Chief, and Allister Yu, Senior VP Operations at Rhoads Online Institute, discuss the transformative impact of automation in the insurance industry.

This webinar stretches the bounds of what seems possible with the Internet of Things – including provocative examples such as parametric insurance that is based on factors inside homes and factories, not just on the weather, and such as insurance for AI.

In this webinar, ITL's Future of Risk series looks at the excitement around generative AI and sorts out where the real opportunities are--and where they aren't... at least not yet.

In advance of next week's Town Hall (register here), ITL sat down with Triple-I CEO Sean Kevelighan to talk about how the insurance industry can tackle climate risks.

AI and ML tools enhance insurance agents' careers, boosting retention and performance while making insurance careers more attractive to millennials and Gen Z.

In this Future of Risk conversation, Nauto CEO Stefan Heck explains how his AI- and camera-based system routinely reduces vehicle fleets' losses from accidents by 60% -- and says he has his eye on the broader consumer market.

In this Future of Risk Forecast, Jim Jones shares his view of how technology is transforming insurance, and how he prepares students to succeed in this new landscape.

In this webinar, ITL's Future of Risk series explores the growing impact of natural disasters, discussing resilience, political challenges, innovation, and a call to action.

Insurers are adjusting to meet millennials' digital preferences and tackling workforce attrition by incorporating technology and enhancing work-life balance measures.

In this Future of Risk Conversation, John Sviokla discusses the game-changing impact of generative AI and advises executives on how to harness its potential for a competitive edge.

Paul Carroll, Editor-in-Chief of ITL, and Taruja Deshmukh, InsurTech Solutions Manager at Conner Strong & Buckelew, discuss strategies for advancing innovation and operational efficiency.

In this webinar, ITL's Future of Risk series explores the transition from reactive to proactive risk management through Predict & Prevent, highlighting technology and resilience.

The evolving role of CRM systems, cloud-based tools, and the transformative impact of AI and ML will have a profound impact on insurance sales strategies and operations.

In our quarterly interview with Dr. Michel Leonard, the chief economist at the Insurance Information Institute provides insights into the factors behind the current inflation trends.

ITL Editor-in-Chief Paul Carroll engaged in a discussion with Dan Swift, CEO of Numentum, about strategies for enhancing the effectiveness of insurance agents and brokers.

The future of fraud is here, but so is the future of fraud protection. Decision intelligence saves thousands of hours of manually searching through risk anomalies.

PURE Insurance and OneShield share strategies for future-proofing insurance technology in their eBook resulting from a 17-year partnership. From Startup to Market Leader offers guidance for insurance startups and carriers seeking growth and transformation.

Sixty $1 billion natural disasters hit the U.S. in the last three years, already nearly half the total in the entire previous decade. Something has to give.

Majesco’s new research delivers a roadmap for leaders to better understand, invest and act on new ways to stay competitive, relevant and grow their business for the future.

Only 11% of policyholders think their insurer is among the best in providing a good experience when compared with other companies they do business with.

Here is a three-step plan to bring together the generations, with all their inherent capabilities, to increase capacity and capabilities in underwriting.

Watch OneShield's panel of industry experts for a dynamic discussion of ways to enhance your advisory role, reduce risk in your portfolio and address inflationary economic conditions with a greater understanding of the commercial properties you insure.

Intelligent Document Processing can record information from every channel and standardize it seamlessly, creating a much-needed layer of centralization.

Generative AI third wave tools portend to expand creativity and eventually, to enhance predictive modelling. The implications of this paradigm shift on financial services, moving from a algorithmic to a data driven approach, have the potential to turbocharge service providers’ ability to provide trusted advice and planning on the full range of financial services.

Exceptional product designers harness emotions that serve as the basis for purchase decisions. What if insurance specialists were included in this process?

Insurers will be relied on to help clients identify and alleviate risks, particularly those caused by climate, and other environmental and social factors.

AI-based data governance solutions let financial firms benefit from powerful deep learning technology that improves data access and activity governance.

Participation in a group captive can help companies save on insurance costs and provide access to extensive risk management resources, including industry-specific expertise.

Despite the severity of the problem, agent gaming has been difficult to detect and mitigate. Fortunately, insurers have new technology that can help them.

As customisation and embedded services shape a new era for insurance, companies in Ohio are looking to build partnerships like never before. JobsOhio’s Ron Rock spoke to four of them.

With change as the only constant, what should CEOs prioritize in 2023? Oliver Wyman shares 10 actions CEOs should take to Reinvent Insurance and fuel growth in 2023.

The future is multichannel. Are you? OZ Global Insurance Practice President Mark Smith provides insurers actionable guidance to navigate the CX cutting-edge.

Laws against using forced labor is creating risks for importers without complete visibility down their supply chains—while presenting an opportunity to insurers.

The next generation of insurers must look beyond traditional attributes and embrace new forms of data and analytics, including contextual, behavioral and motivational data.

In developing technology solutions, one of the most overlooked and critical elements of delivering value to end users is empathy -- truly understanding their pain points.

Employers are more aware than ever that employee caregivers represent a large portion of their workforce and require more assistance to stay on the job.

Insurers are becoming more adept at using telematics to differentiate their products, reduce risks and expenses and continue improving the policyholder experience.

Underwriters face hyper endorsement, misrepresentation from known fraudsters, as well as criminal networks and the schemes they perpetuate, such as Ghost Broking.

While being protected by insurance provides peace of mind to numerous individuals and businesses, insurance companies themselves are at increased risk of fraud.

Incredible as it may seem, the average underwriter today spends seventy percent of their valuable, limited time on tasks unrelated to underwriting. But does it have to be this way? Mark Smith, President of the Global Insurance Practice at OZ Digital Consulting, reveals how advances in intelligent automation can not only remedy that disparity, but open up entirely new avenues to opportunity, productivity, and profitability.

Self-service automation is the next step in the insurance industry. The right solution can be a win-win for insurers and customers, while the wrong solution can irritate customers and ruin a carrier’s reputation.

Personal lines executives see the potential for new user interaction technology to transform core business areas, primarily policy servicing and claims.

AI's capabilities have surged so much that it has the potential in 2023 to dramatically raise the quality of claims handling and underwriting in workers’ compensation.

In this webinar from Equisoft, learn how taking a Greenfield approach as a first step in policy administration system modernization can reduce risk, accelerate innovation and help carriers stay ahead of the digital transformation curve.

Instead of asking how ethical a firm’s AI is, we should ask how far ethics is taken into account by those who design the AI, feed it data and use it to make decisions.

Ohio is committed to business development and innovation across the financial industry. Ron Rock, Senior Director of Insurance and Insurtech at JobsOhio, explains how state enterprise is targeting this increasingly important part of it

Insurers started 2022 in a position of strength and still are in a good spot to drive down costs and increase demand, unless rising claims costs and market volatility continue.

To help industry players orient themselves, compete more effectively and better serve customers in an increasingly volatile world, here are trends to watch for.

In workers' comp, a patient-focused, early intervention claims management model has demonstrated many key improvements over traditional case management.

At a time when few answer a call from an unknown number, insurers can identify themselves as a legitimate caller by displaying logos and a reason for the call on the recipient’s device.

Insurance companies store large amounts of information about their policyholders, and attacks are expected to grow in frequency and severity in the coming years.

Survey responses from 1,000-plus subjects very much confirmed that gig work is here to stay. 59 million Americans—36%of the workforce—are classified as gig workers.

The application of advanced analytics is already well ingrained in underwriting. It has only more recently begun to exert more influence in claims operations.

Geopolitical conditions, specifically those related to Ukraine, have increased risks as nation-states orchestrate prolific cyberattacks against other countries.

Winter Storm Elliott highlights the importance of preparedness and provides fundamental lessons to better manage winter risks and advance business resilience.

Prepayment reviews can save money and increase an organization’s efficiency by reducing the workload and friction of concluding retrospective payment reviews.

Discover an integrated suite of solutions that detect fraud, automate claims processing, and underwrite risk - delivering incremental value and verifiable financial results.

The Federal Insurance Office's proposal on collecting more data to improve understanding of the impacts of climate change is a great start -- but can be improved.

While there are certainly more than 20 issues to discuss, here are high-impact matters relating to workers’ comp, healthcare and risk management that need more attention.

Some 2,300 business interruption suits have been filed related to COVID-19, and a massive cyber-attack would surely produce even more--and more confusing--suits.

The employee-oriented job market is putting a strain on insurance IT departments, because over half are having difficulty hiring and retaining tech staffers.

People who choose interim or contract work are often highly skilled, mission-oriented and project-based individuals who assimilate quickly into new environments.

Younger generations want jobs in which technology reduces frustrations, increases productivity and enables quick successes. In insurance, too many obstacles still exist.

Humanized experiences are the only way insurance can successfully digitally transform to serve its purpose. Let’s look at our future through this lens.

With the rise of SaaS solutions propelling insurers to adopt emerging technologies faster than ever, ensuring security requirements can keep pace with technology adoption is imperative.

We had expected the U.S. economy to muddle through 2022 to a soft landing with modest inflation, but we find ourselves with skittish markets and possibly a downturn in 2023.

The latest results still show major problems, but they have some digital assets that could be of great help to an incumbent insurer, and for a modest price.

Investments in digital, AI and connected world technologies remain top priorities for insurers, but they are being strategic about how they accelerate certain technologies.

Lead by example and embody positivity, confidence, humility and gratitude. You will have a significant impact on the success of your team or organization.

In today’s complex risk landscape, spreadsheets can no longer carry their weight. They create administrative burdens and introduce the possibility of human error.

Most insurers focus too much on the technical issues related to data and too little on the more strategic aspects, especially on embedding analytics into workflows.

One challenge is recognizing this might be the greatest time ever to recruit people, because 70% of employed individuals say they need a second income to make ends meet.

Anyone who has purchased insurance by phone and a series of back-and-forth emails knows how slow and difficult that process can be. But it doesn't have to be that way.

Aimee Kilpatrick, chief operating officer at Cadence Insurance, describes how the Cadence Bank-owned insurance agency is tackling the industry-wide talent shortage, and how it is meeting clients' evolving needs,

Haphazard marketing may result in a decent amount of web traffic. But if those prospects do not convert into customers, you've wasted your time, effort and money.

Drawing on our national franchise, we set up an "insurance village" after Hurricane Ian. Here are three lessons we learned that can help agents make an impact after a natural disaster.

Across the sales value chain, insurer executives generally have low satisfaction with digital capabilities, particularly in early stages of the sales process.

Carriers can bundle products, enable direct mobile sales channel distribution and offer relevant, affordable and flexible coverage to the underserved market of gig workers.

If, instead of being paralyzed, you use fear to motivate you to check out every factor that could go wrong and mitigate that negative potential, your odds of succeeding skyrocket.

With increased adoption of APIs (application programming interfaces), embedded insurance products can seamlessly integrate into third-party buying processes.

Any company that still relies solely on governmental property records instead of using AI-derived property databases is significantly increasing its risks.

Haven Life's second annual Q4 survey highlights a large gap in knowledge surrounding life insurance and its role in building a financially secure household.

Combining artificial intelligence with aerial imagery can allow for the creation of 3D property insights and make risk identification quicker and more efficient.

In this webinar with ITL Editor-in-Chief Paul Carroll, Michel Leonard, head of the Insurance Information Institute's Economics and Analytics Department, discusses the prospects for P&C growth in the face of fiscal and geopolitical risks.

Robotic process automation is giving way to E2E (end-to-end), the only acronym that matters. Here are three guiding trends for the new automation platforms.

Previously inaccessible data on customer insights, producer management and renewal optimization can improve a carrier's or MGA’s topline growth by up to 30%.

Unfortunately, this time of year frequently sees an increase in workplace injuries, because of added responsibilities, stress, tighter deadlines and a decreased workforce.

Aging has evolved, and there is no longer enough good information about the populations being insured, so every policy issued has more risk than it needs to.

The corporate world is now so connected and complex that underwriters need to understand accumulations of exposures within corporate distribution and value chains.

I asked an audience how long it takes a new underwriter to go from zero to productive: The majority voted for 24 to 36 months. This is a ludicrous proposition in the age of AI.

Within the fleet industry, the most common cause of crashes is distracted driving, which injured more than 420,000 drivers and killed 3,142 people in the U.S. in 2020 alone.

EVs bring to light some potentially interesting implications on auto insurance. They could represent a prime use case for a new type of embedded usage-based insurance policy.

Insurtech 2.0 recognizes the innovators who came before but takes a more nuanced and collaborative approach, recognizing the structural issues inherent in insurance.

96% of insurer executives see personal lines underwriting undergoing significant changes within five years – remarkable given the shifts that have already occurred.

The legacy of Insurtech 1.0 may be more enduring than the actual companies. They forced incumbents to recognize their intransigence, producing a new focus on customer experience.

Auto insurers have a strategic imperative to not be left behind in the race to monetize connected car data, and there are several ways insurers can do this.

Rising costs, general anxiety about the economy and a surge in relocation that began during the pandemic are driving insurance shoppers to seek more options.

Wearable devices paired with artificial intelligence can significantly reduce workers' comp costs for businesses and the insurance providers that protect them.

More than six in 10 people don’t think that any discount is worth letting insurance companies collect more information about their driving habits and homes.

Based on two decades as a consultant, executive and entrepreneur, I see three patterns that get in the way: Spinning Plates Syndrome, the Department of No and Zombie Resurrection.

When organizations do not complete a detailed cyber evaluation of target companies before a merger or acquisition, they risk significant financial and legal challenges.

By bolstering confidence in the integrity of carbon offset transactions, insurers can ultimately enable greater capital flows to areas where investment is most critical.

Ron Rock, senior director, insurance/insurtech, JobsOhio, and Andrew Daniels, founder and managing director, InsurTech Ohio, talk about what comes next for the insurtech market.

We talk with Bryan Davis, a HUB International executive and head of its digital platform, VIU by HUB, about its new hybrid business model that includes digital and its broader implications for brokers.

A robust ecosystem of risk-reduction mechanisms can result in far better health outcomes while conservatively reducing total health spending by 25% or more.

What does it take to be a successful leader? How can you lead change effectively? Here are 10 tips that can help you lead change in the insurance industry.

While ransomware still dominates among cyber threats, business email compromise incidents are on the rise, and geopolitical hostilities could spill over into cyberspace.

While several high-profile insurtechs have had a rough year in public market valuations, there are still many bright spots for startups in this marketplace.

Fraud accounted for $6 billion in losses to insurers and government agencies after Hurricane Katrina, but AI-based verification has come a long way since 2005.

Small businesses often seek providers offering them the most affordable policy quickly and efficiently. Any delay, and they will likely go to a competitor.

Faced with new challenges, including changing customer expectations and increased competition, MGAs know relationships are no longer enough to stand out.

Solutions can address brokers’ administrative risks from within, in a way that focuses on the customer/risk manager experience and leads to vastly improved alignment.

Most property risk models rely heavily on ZIP code. Yet, technology and data exist today to evaluate more than 1,000 risk data points for every single property in the U.S.

No one is happy with the current, cumbersome approach to auto claims -- and a key technology has finally arrived that will digitize and speed the whole process.

How one carrier (the Hartford) rolled out MFA to its agents. What was measured, what was learned and how this shapes the future of the industry’s data security.

In this webinar, we explore a different way of looking at how to improve underwriting; focusing on the needs of the underwriter, not just on the process.

Over this five-part series, hear from insurance industry leaders about the cascading challenges wrought by the pandemic and other social and environmental issues -- and enormous opportunities to rethink the old ways of doing business and plan a better path forward.

Though blockchain has vast potential due to security and trust, some of its benefits, such as decentralization and distributed processing, can turn into limitations.

Instead of experiencing a blizzard of statements and notices, employees get a single, simple statement summarizing all their care, regardless of where they received it.

Shifting distribution tactics, focusing on more personalized coverage, designing new products and partnering across industry lines can all narrow the gap.

Discrimination and historical trauma have shaped the mental health of our BIPOC and AAPI communities and the treatment they receive. How can we do better?

Based on technological advances, a hybrid approach lets the injured worker get in-person care while doing carefully monitored, supplementary activities at home.

By removing data silos and creating a unified, contextual understanding, each department will gain a more complete picture of how best to improve overall performance.

As the North Atlantic hurricane season typically has a secondary peak around mid-October, businesses need to remain vigilant about protecting their premises and people.

When we step outside the confines of either/or thinking and embrace a "both/and" mindset, we can achieve great things in our work and home lives and in our businesses.

Insurers need partnerships with fully integrated national providers with deep expertise in medical, record and investigation management, bolstered by new technologies.

Demand for commercial insurance is on the rise, but profitability remains elusive. Algorithmic data is the key to greater, granular insight into risks and prices.

One in four Americans is caring for a loved one with a debilitating illness or other special needs. COVID-19 amplified the problem, and it will continue to grow.

Loss control teams at insurance brokers and carriers desperately need new ways to de-risk day-to-day operations of high-value shippers that have had troubling losses.

By improving weather modeling and assessing past catastrophes, insurers can use predictive analytics to provide better support to customers during difficult times.

Understanding your dark data can reveal insights into customers and employees, the quality of your assets and manufacturing and the risks your brand faces on social media.

Solutions that help explain the process and catch and correct errors before they happen increase productivity and improve the applications' success rate.

We now have the ability to look at data differently, leveraging innovations to identify risk, extrapolate insights and see the bigger picture big data offers.

Given the difficulties involved with suppressing battery fires, particularly at sea, loss prevention measures are crucial, whether batteries are transported within EVs or as standalone cargo.

From tuition insurance to life, health, auto or renter’s insurance, parents and their students should get ready for the risks a school year has in store.

Many underwriting leaders, amid the industry’s growing focus on expenses, growth and analytics, have taken their eye off the ball of traditional underwriting quality.

Insurance companies pursue digital transformation and customer experience optimization but overlook some of the fundamentals. This is exemplified by payments.

In this webinar with ITL Editor-in-Chief Paul Carroll, Dr. Michel Leonard, head of the Insurance Information Institute's Economics and Analytics Department, lays out the Triple-I's latest thinking on the perplexing problem of inflation.

While many agencies decry a “race to the bottom” by states, a true analysis of workers' comp benefits over the past half-century requires a far broader context.

Read the latest report from Majesco to understand the opportunities of creating a diversified distribution ecosystem that expands the footprint of offerings and reaches new markets.

Although the life insurance industry has been cautious by nature, data and technology are shifting the analysis of risk and enabling prudent underwriting without volatility.

Stressed employees are less engaged and have lower productivity - and some may even left their job. Here is how to promote a low-stress work environment.

You are passing up maybe $1,000 in commissions per client if you aren't cross-selling instant-issue term life insurance policies that don't require a medical checkup.

The idea that financial transformation can help insurers better serve their customers even as they position their businesses for rough seas is no longer theoretical.

The most important contact center metrics are: satisfaction, customer experience, quality assurance and revenue growth -- but the most measured is “call handle time.” Hmmm.

New research shows how COVID has moved insurance from seeing change on the horizon to feeling the impact of customer change in the decision-making process.

Employee benefits carriers can differentiate themselves and shield themselves from disruption by harnessing predictive models to optimize pricing and radically improve profitability.

Cloud-based platforms will let auto insurers make a critical pivot away from purely reactive claims response and processing to claims minimization and avoidance.

A cross-disciplinary study using digital health data may have serious implications for mortality from sleep apnea -- and for insurers seeking to underwrite these risks.

As competition heats up, a simple policy add-on that costs just a few dollars each year is a hidden tool in the agent’s toolbox: the roadside assistance policy rider.

Custom health plans allow employers to shop competitively the vendors inside of their health plan, like their pharmacy benefit manager, claims manager and reinsurer.

While insurtechs are struggling, established brokerages have deep industry knowledge and solid businesses from which to build and evolve technology solutions.

Insurers can lower operational costs, improve underwriting performance, offer appropriate insurance quotes and more effectively track the facts on the ground.

The industry in aggregate is retreating from climate risk, at a time when society needs it to run toward the most severe risks that threaten us. It's time for the industry to step up.

Off-the-shelf technology packages rarely produce exactly what an organization needs; with low-code, they can configure solutions to their unique needs.

During the last five years, 89 weather and climate disasters in the U.S. caused $788 billion in damage. In 2022, nine events have exceeded $1 billion in losses.

Newly available data will be ingested into weather models to improve forecasting for carriers, reinsurance companies and even insurance linked securities.

Navigating a business' ups and downs can be as challenging as steering a ship through a storm on the high seas. I’ve done both—and lived to tell how it can be done.

Adding a layer of phone number and device intelligence can slash the risk of fraud, giving the organization and customers greater security while maintaining a positive experience.

Having a team that's adaptive is essential. Transformation needs to be top-down and bottoms-up. Everyone involved understands why we're going somewhere.

Amazon and Mark Cuban have entered the pharmaceutical industry. Will they disrupt things in a way that delivers more efficiency and value for Americans?

At what point does social inflation severely constrict the availability of certain lines of coverage and thereby give rise to legal remedies, such as tort reform?

As the industry faces mass retirements and a challenging labor market, it’s time to get down to brass tacks. Maybe the solution is simpler than we think.

How do businesses/defendants and carriers combat the effects of social inflation? It is definitely not a simple challenge, but here are three key considerations.

WeFox raised money at a valuation of $4.5 billion. My first reaction is the same one I had when Root raised funds at a valuation of $3.65 billion: This makes no sense.

Insurers with future-ready operations are 2.8 times more profitable and 1.7 times more efficient than their peers. Yet only one in 10 insurers is at that stage.

The past several years have demonstrated that the insurance industry really needs to understand the social inflation landscape so we can begin to address it.

Natural language processing can transform a burdensome process, freeing claims professionals to apply their expertise where it makes the biggest difference.

While the metaverse is still largely theoretical, providers of group and voluntary benefits might be able to capitalize on this emerging technology. Let’s speculate!

It will take more than raising premiums and putting more limits on the businesses that can qualify for cybersecurity insurance to prevent increased claims and higher costs.

As the second-largest railroad company in the U.S., they took the bold leadership move to take the pledge to make suicide prevention a health and safety priority.

High-res data sees more than a shipment of glass: It sees a load of Gorilla Glass on clear summer roads or of crystal chandeliers on a pockmarked highway in a winter storm.

Integrating a new feature, for example to provide dynamic quoting and pricing, usually takes months. Hyperautomation, such as low-code, provides robust solutions faster.

Looking at the root causes of the spate of fires -- and the root causes of the root causes -- suggests a lapse in discipline in enterprise risk management.

I hope the next wave of insurtech players will have more robust insurance fundamentals and will not pretend that insurance ignorance is a competitive advantage.

Even though agents are thriving, direct distribution will significantly increase, insurtech will play a big role in reshaping distribution and big tech companies will enter the space.

MGAs and E&S carriers are thriving, and they have lots of runway in front of them. They can continue to exploit their deep understanding of market niches, can drive efficiencies in the often-cumbersome underwriting process and can increasingly fit into insurers' processes by being at the forefront of APIs.

While the cyber market improved significantly in 2021, increases to prior-year reserves may cause a drag on earnings, and the Russian invasion of Ukraine creates uncertainty.

Billing is important enough to the business that it requires a future-focused strategy. Billing innovation and transformation strategy pays for itself.

Despite improvements in risk management and prevention, fire/explosion (excluding wildfires) is the largest single cause of corporate insurance losses (21% of total losses).

Insurers and body shops need to start thinking differently about claims and repair processes, and how they can be revolutionized through AI and VI – Visual Intelligence.

Many insurance companies have begun to reevaluate their equity investments. Is it time for them to follow John D. Rockefeller’s example and focus on dividend-paying equities?

Auto insurers should expect higher claims costs in the second half and longer wait times for damaged vehicles to be repaired and returned to their owners.

A recent SMA study shows that 41% of personal lines insurers are revisiting their digital transformation strategies in 2022, a significant jump from 19% in 2021.

At Oliver Wyman, we have been helping clients understand Web3 and what it means for insurers, and guiding strategic moves — near-term and longer-term — around this evolving ecosystem. Our latest research finds the Web3 economy is currently under-insured and has huge potential for future growth. Here, we share a practical guide for insurance executives to help separate hype from reality, including Web3 insurance opportunities and risk considerations.

When jobs are in high demand for both employers and prospective employees, it creates a hyper-competitive job market that requires a strategic approach.

Discomfort with the certainty of death leaves life insurers questioning where they can meet customers. The answer lies where almost all other industries have ventured – online.

Social unrest won't abate any time soon, given the after-shocks of COVID, the looming cost-of-living crisis and the ideological rifts that divide societies around the world.

Advancements in technology today provide the tools and resources necessary for the step change in reserving capabilities that were not previously possible.

Changes in customer behavior are creating a series of “from – to” shifts that have huge implications for billing and payments and require a quick response.

Insurers must prepare for disruptions in the availability of cash, the functionality of global supply chains, global GDP growth and various other factors.

In painting a rosy and likely unrealistic picture of what AI can and can't do, Musk has, in our view, misled the public about how far we still have to go.

Individuals are reevaluating what’s important to them, what they want for their careers and the pandemic's significant impact and financial burden on their families.

More open sources of data and common standards for models will enhance our understanding of the potential implications of climate transition decisions.

While APIs have become commonplace, we are running into the danger of creating too many point-to-point tethered connections and losing the value that we had found.

Analytics are finally catching up to the vision, letting everyday business users harness the power of data through easy-to-use tools and advanced automation.

Insurers have at their disposal incredible amounts of data, and powerful analytics can turn it into business intelligence better than traditional tools.

Insurers and their distribution partners must evolve and convert new customers where they already choose to spend their money, no matter where that is.

Personalized packages that support all aspects of an employee's physical and mental health are essential and now feasible with modern digital technology.

Research finds that insurers in small commercial lines are further along in their digital transformation journeys than their peers in mid/large commercial lines.

Traditional discussions of react, repair and replace are changing to predict, prevent and protect. Part of this transition has been supported by the IoT.

Identity management involves reconciling what you know about an individual with real-time behavioral data, specifically actions that signal purchasing intent.

Recent macroeconomic events involving supply chain slowdowns, flexible work arrangements and rising inflation have paved the way for a possible uptick in crime.

Property-casualty insurers should stress test their operations and consider ways to counter potential inflation impacts on both sides of their balance sheets.

Insurers have massive databases from simulation models and satellites when it comes to weather and climate. The problem is figuring out how to use them to their full potential.

For insurers seeking to accelerate their analytical innovation cycles and move ideas “out of the lab,” data discovery tools such as External Data Platforms are vital.

A major survey of consumer attitudes toward insurers found them... indifferent. Indifferent is not negative. Indifferent can mean a chance for great opportunity.

As much progress as the industry has seen in recent years, we can't categorize UBI participation as mainstream when only 22% of people reported being in a program.

Applications to establish businesses surged in 2021 in the insurance industry, driven by changes in behavior during the pandemic, and will likely stay strong.

The last six hurricane seasons have been characterized by above-average activity, and this trend is expected to continue in the 2022 Atlantic hurricane season.

Quantum computing, in the wrong hands, could create a multitude of digital risks, including advanced cyberattacks -- a significant problem for the insurance industry.

With the heavy focus on premium costs, the market has overlooked the very real cost of foregone economic value caused by insurance collateral requirements.

We've been talking about the topic for many years now. Aren't we done yet? Can't we move on? In fact, we are just about done -- almost all insurance operations have incorporated digital technology. So, yes, it's time to move on to the next stages of the industry's remake.

While investment slowed in the early phases of the pandemic, it rebounded strongly in 2021: Levels during the first half equaled the total for all of 2020.

There is no going back. Insurers must optimize operations for remote teams and supporting partners serving an increasingly diversified, and shifting, client base.

But Russia’s invasion of Ukraine; the move to decarbonization; crew and port congestion challenges and other issues mean there is no room for complacency,

An increase in digitization, the rise of AI and better value-tracking methodologies have paved the way for more advanced technology like "intelligent decision-making."

Read Majesco's latest research to better understand the important changes in insurer's strategic priorities which are fueled by growing customer expectations and defined by three digital eras.

One insurtech has tried, but Hippo has burned through $628 million in cash and is spending more than $1.50 for every dollar of premium it is generating.

With two-thirds of consumers reporting they base buying decisions on brand values, an increased focus on sustainability presents a huge opportunity for insurers.

While talent challenges are nothing new to insurers, new research shows they are prioritizing talent strategies more than ever in the post-pandemic era.

Here is what insurers should be aiming to achieve ahead of the UN climate summit in November to support both their own and broader net zero emissions pledges.

A key to diversity and inclusion is strong support from senior leadership. Another is naming a single leader to be responsible for the success of all your efforts.

Technology and weather science have evolved to help warn of approaching events, giving advanced notice to people to alter course and relocate to safety.

Can insurers envision the opportunities clearly enough that they are motivated to switch gears and change something right now, and tomorrow, and the next day?

The assumption about technology is that progress comes fast: Because electrons move at the speed of light, changes driven by technology must, too. But that's often not the case.

The pandemic elevated the need for companies to provide digital experiences to customers and employees, such as real-time payments and virtual claims submissions.

The majority of workplace injuries are slips, trips or falls, but there are many unexpected injuries, such as getting hit by lightning or falling overboard.

Instead of simply selling consumers products, smart companies. including insurers, market themselves as companies to believe in and make part of one’s life.

With online-only companies becoming more popular and more desirable, they’re causing the entire industry to rethink how they’re going to stay relevant.

If the proper guardrails and governance are not put into place early, insurers could face legal, regulatory, reputational, operational and strategic consequences down the road.

People want to do work that is interesting and purposeful. They value an organizational culture that places a premium on creativity, thought leadership and innovation.

Just as the U.S. spends hundreds of billions on warships and planes, it should invest in an information warfare machine focused on continually preempting disinformation.

Marie Carr, Amanda Davis, and Bhushan Sethi, along with moderator Paul Carroll, discuss creating a culture of innovation and how to attract new talent and motivate and upskill existing talent.

We often think about climate change in the long term. It's easy to forget that we already live with the consequences of unchecked climate change today.

When done correctly, technology is as transparent as it is critical. When implemented poorly, it's like begging your customers to look elsewhere for services.

The insurers that will pave the road to the future will be those that figure out to seamlessly serve customers by matching each product to the right distribution channel.

The invasion poses a complex threat to the operations of financial services companies and has enormous consequences for the financial markets in the short term.

Family offices face increasing threats to their assets, reputation and physical security, and the consequences can be severe if risk barriers are not built.

A story about monks and nuns doing electronic piecework suggests just how far the gig economy can stretch, if we think about the issues creatively enough.

At this point, we believe that the hard U.S. E&S market will not end any time soon; however, some companies will struggle with prior year reserving issues.

Existing strategies addressing medical debt, such as stopping lawsuits or removing it from credit reports, are important but do little to actually prevent debt.

As employees start to return to work after two years of mostly working remotely, smart employers are rethinking just about all aspects of how work is done to get the best of both the home and office worlds.

Insurers can create a better narrative for investors if they, like Musk, play offense, not just defense, on moving toward net-zero emissions of greenhouse gases.

Emerging threats are precursors to business crises, so all organizations should have an updated risk management plan to implement when these risks become a reality.

The litmus test for talking about suicide is to substitute the word "cancer" for the word "suicide" to see if the sentence still makes sense or if it has a negative connotation.

Putting the right product in the right place at the right time through embedded insurance has more potential than any other insurance innovation in recent memory.

Email is based on an antiquated physical model (the inbox and outbox), and better ways of communicating -- even collaborating -- with customers are emerging.

This year and beyond, agencies will fiercely focus on channel expansion and assess their current partnerships. Insurers must stay abreast of new partnership opportunities.

Social media data provides insurers with an opportunity to gain insights into a customer's risk exposure in real time. But it comes with many challenges.

Maintaining compliance requires manual, repetitive and error-prone processes, handled by small armies of well-compensated experts -- but many can be automated.

The acceptance and delivery of payments must be in real time, and capabilities must let customers create tailored digital payment experiences that fit their needs best.

ITL's latest On-Demand Webinar featuring Marie Carr, partner at PwC; Andrew Robinson, CEO at Skyward Specialty Insurance Group; and Andy Cohen, COO at Snapsheet; along with moderator Paul Carroll, editor-in-chief at Insurance Thought Leadership.

The roots of intelligent automation remain firmly established in the information technology industry, yet its influence has branched to serve a wide range of businesses.

Clients, brokers, insurers and investors have woken up to the possibilities of simpler, faster catastrophe insurance, and they are already experiencing the benefits.

Efforts will include using technology to improve the ease of doing business for agents and implementing tools and applications to increase employee productivity.

Studies show that the quantity and quality of sleep have declined steadily, and sleep loss can make it more challenging to maintain focus and vigilance.

Application forms that encourage fast thinking can lead to misdisclosure through careless mistakes, approximate answers and intuitive biases. Slowing the buyer down may help.

We need to start a discussion about underinsurance, especially after natural disasters, to determine if changes need to be made to better estimate replacement costs.

Seemingly impersonal digital transactions underscore the criticality of personalization. The key is to pinpoint the exact moment of need in the insurance buying and filing experience.

Personal lines insurers will continue to advance their digital transformation strategies in 2022, albeit with a new lens and several shifts in priorities.

In dynamic conditions like today's, strengthening existing relationships, elongating the customer lifecycle and focusing on the right prospects are all-important.

The gender gap is societally based, and change needs to happen at a core level. Not just with how men see women in the industry, but with how women see themselves.

Group and voluntary insurers have a whole new challenge: How to create products that fit each unique life and then offer them where life happens — at work.

Insurers are already familiar with adverse selection. Now, they are getting to grips with the new concept of inverse selection that arises with big data.

Commercial insurers will continue to advance with their transformation strategies in 2022. However, their focus will look a little different than it did a year ago.

New political risk insurance losses in Ukraine due to Russia's invasion will likely be material but well within the ability of private carriers to perform on their obligations.

The two most immediately relevant are "the end of passwords" (yay!) and the growing availability of "synthetic" data to train AI in situations where there isn't enough real data available.

Properly applied, AI produces better medical outcomes, gets employees back to work faster, reduces litigation risk and lowers the costs associated with claims.

If an organization does not have a well-thought-out incident response plan with trusted and tested backups in place, a cyber attack can be devastating.

Thousands of lines of insurance haven't been innovated in 30 years. With so much opportunity, it's time to think about insurtech as a permanent fixture in the larger ecosystem

While the assumption has been that higher repair costs for advanced driver assistance systems features offset ADAS loss-cost benefits, a new study finds significant benefits.

2022 will look a lot like the second half of 2021, but opportunities are emerging for auto insurers to differentiate themselves, especially through telematics.

Customers now expect exceptional service from all businesses, and low-code platforms hold great promise for businesses’ internal and external users alike.

With time, the true cost of maintaining a legacy system and its entire ecosystem tilt in favor of an upgrade. The trick is to know when that time has arrived.

Capacity-seekers and capacity-providers are starting to recognize the benefits of an organized digital marketplace with an efficient electronic infrastructure.

Home-based businesses exemplify the sort of opportunity that is arising as we start to come out of the latest wave of this awful pandemic and head toward a new normal.

Insurtechs and carriers both need to take the time and make the effort to understand one another’s needs, capabilities, constraints and strategic objectives.