The life insurance industry has long grappled with closing the insurance gap by reaching underserved populations – those who have traditionally not owned life insurance, particularly in the middle market.

As insurers explore new approaches to access these previously untapped segments, they face a hurdle: a lack of familiarity with these markets. Reinsurance Group of America (RGA) conducted an analysis to help address this shortcoming.

Beyond underwriting: Market matters

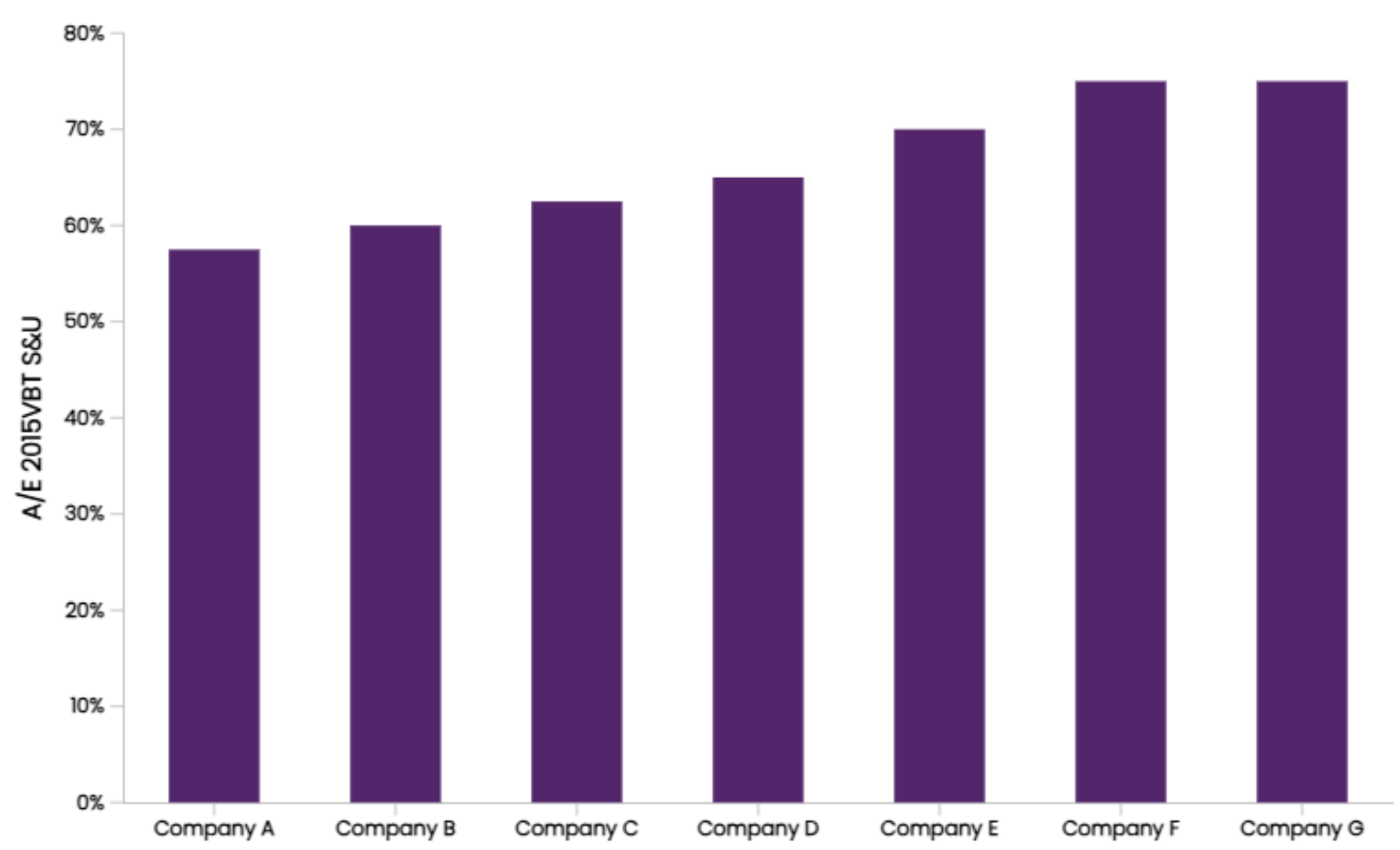

RGA has long understood that there is more to mortality outcomes than underwriting alone can explain. To demonstrate this, we compared fully insured lives across various carriers to determine the degree to which mortality could vary based on factors other than underwriting. The analysis focused on the best preferred class available at similar ages, policy amounts, and product types, and limited to carriers that had very similar preferred criteria. In other words, we examined policies with the same level of underwriting rigor. The results showed the differential across carriers ranged as high as 1.3 times.

Two lessons emerged:

- Insured mortality outcomes are driven by more than the traditional questions and data collected.

- All risk cannot be underwritten away in an underlying market, as there are other considerations (i.e., who is buying it, who is selling it, etc.).

Figure 1: Term mortality by company with similar best class underwriting

Given this disparity can exist for business that is known and understood – this type of insurance has been sold by the industry for nearly three decades – it piques the interest in results that may exist for less familiar markets.

Three questions arise:

- Is there a difference in mortality between the historical insured population and the prospective insured population?

- If yes, how big is the difference?

- Can medical underwriting resolve the issue?

(Definitions: Historical insureds are those identified as having had at least one policy reinsured with RGA at any time between 2007 and 2022. Prospective insureds are those identified as not having had any policies reinsured with RGA at any time between 2007 and 2022.)

The mortality divide

Historically, there have been material mortality differences between the insured population and the general population. The insured population has consistently demonstrated better mortality outcomes. This leaves the uninsured portion of the general population – the prospective insureds – as a group with potentially higher mortality risk.

To explore these differences, RGA conducted a comprehensive study comparing mortality outcomes between the historical insured population and the prospective insured population. The study leveraged unique data that allowed for the examination of mortality outcomes and risk profiles across a broad spectrum of the U.S. population.

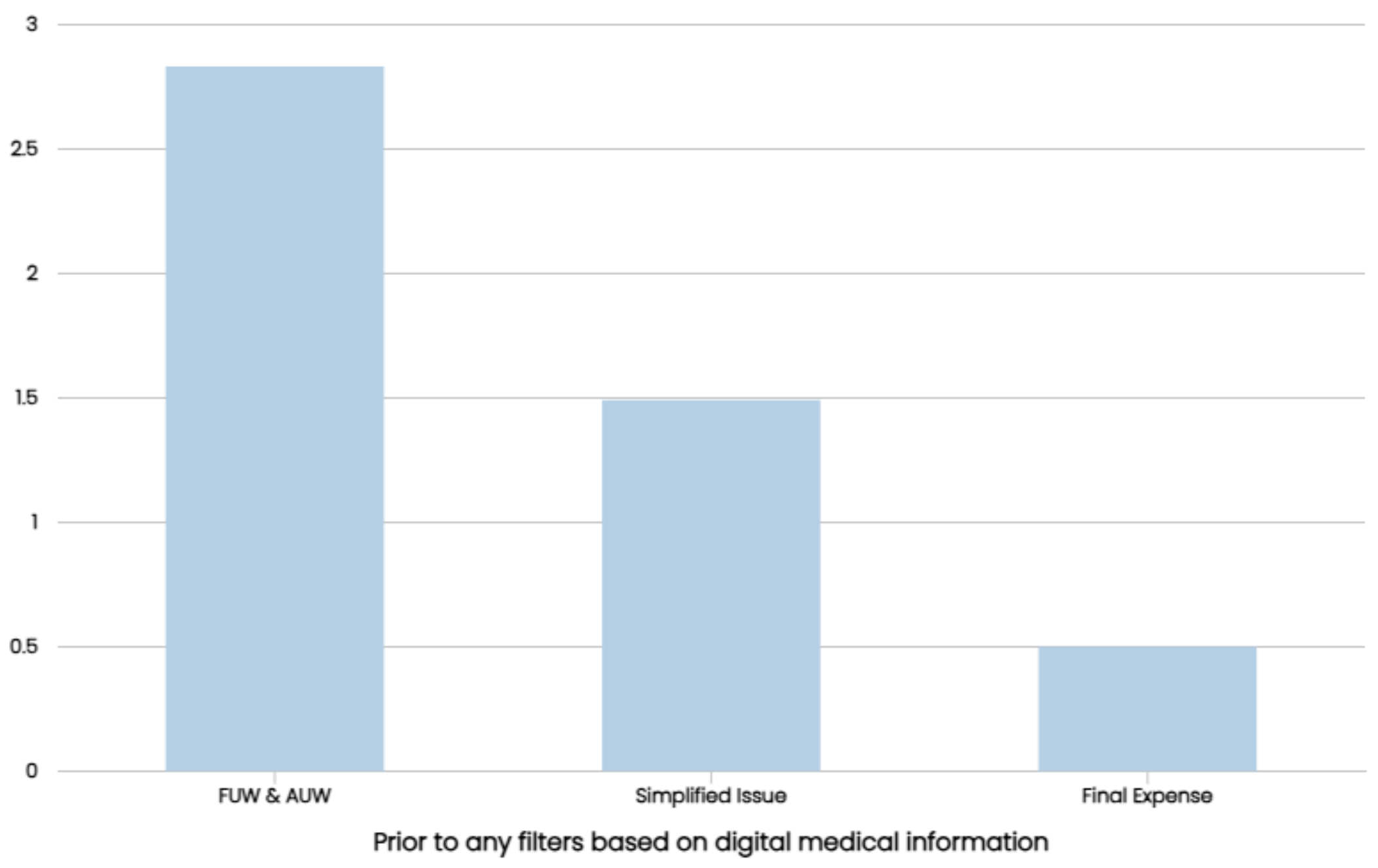

The study's findings revealed significant mortality differences between the two. When compared with fully underwritten (FUW) policies, the prospective insured population showed mortality rates more than 2.5 times higher. Even when compared with simplified issue policies, the prospective insureds still exhibited about 50% higher mortality.

Interestingly, final expense insurance – typically associated with higher-risk individuals and simplified underwriting that allows for more impairments – was the only segment where the prospective insured population showed lower mortality, at about half the rate of the insured group. These stark contrasts underscore the complexity of the mortality landscape when considering underserved markets.

Figure 2: Prospective insured mortality relative to historical insured by underwriting category

What can medical underwriting accomplish?

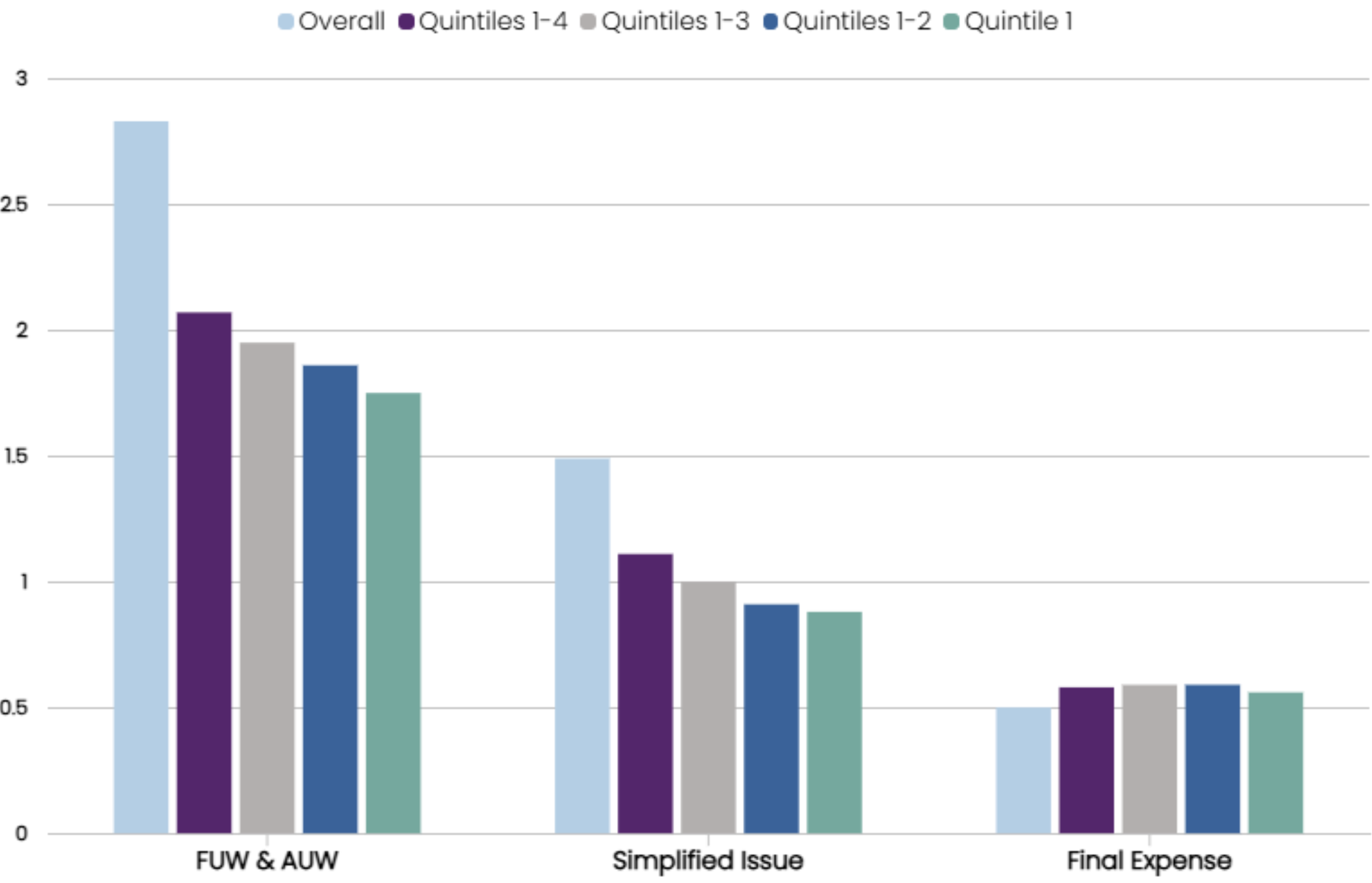

Rigorous medical underwriting could presumably bridge this mortality gap; however, the study's results suggest otherwise. After applying the same risk assessment standards using a proxy for medical underwriting (i.e., prescription and medical claims history) to both populations, mortality differences persisted between the prospective and historical insured populations.

For fully underwritten policies, even when comparing only the lowest-risk quintiles of both populations, the mortality ratio remained materially greater than one. This suggests there may be inherent differences between these populations that extend beyond what traditional medical underwriting can capture.

The simplified issue category showed the most similarity between historical insured and prospective insured populations. As underwriting restrictions tightened, the mortality ratio crossed below the 1.0 threshold for the best risk quintiles, indicating prospective insureds might be well-suited for simplified issue products in today's market. Also, the prospective insured population consistently had lower mortality outcomes than final expense insureds.

Figure 3: Prospective insured mortality relative to historical insured by risk profile

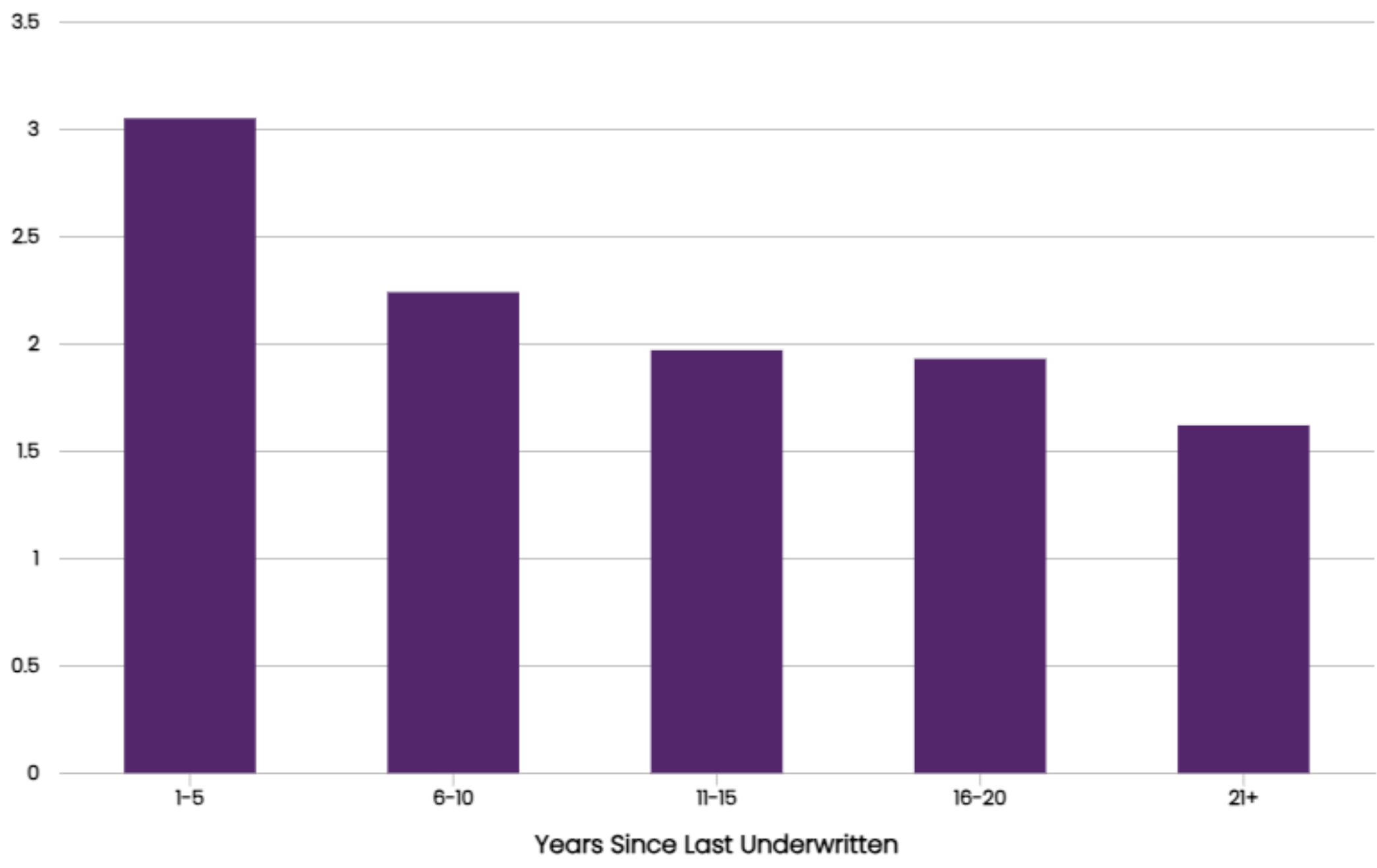

Age and duration

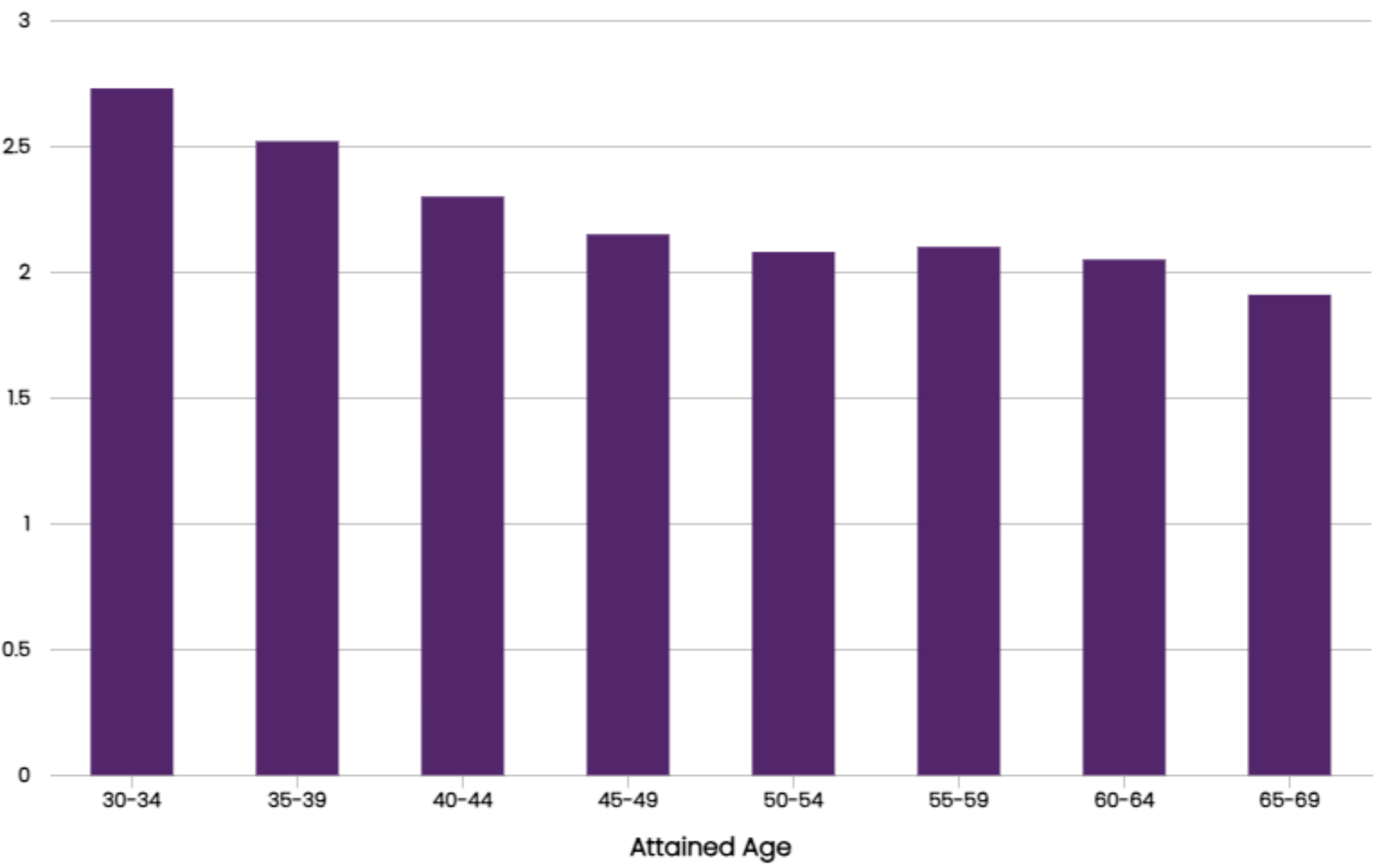

The study also revealed interesting trends when examining mortality differences by age and policy duration. For fully underwritten policies, excluding the highest-risk individuals, younger ages showed a more significant mortality ratio between historical insureds and prospective populations. This finding is particularly noteworthy as younger individuals are often a target demographic when attempting to enter the middle market.

Figure 4: Prospective insured mortality relative to FUW and AUW, quintiles 1-4

Duration analysis showed that a historical insured policy assessed more than 20 years ago had a better mortality rate – well above 1.0 – than the prospective insured population. This persistent difference suggests that factors beyond underwriting continue to have a long-lasting influence on mortality outcomes.

Figure 5: Prospective insured mortality relative to FUW and AUW, quintiles 1-4

Strategies for responsible market expansion

These findings highlight the challenges of expanding into underserved markets and underscore the need for innovative approaches to responsibly reduce the insurance gap. However, this is not to suggest that this market and its challenges should be avoided.

The insurance industry must continue to unlock the full potential of digital evidence. As individuals' digital footprints grow, leveraging electronic health records and other unstructured data sources could pave the way for more effective and efficient underwriting. The shift toward digital applications also presents an opportunity to balance customer experience with accurate disclosures, potentially through the implementation of behavioral science principles.

It is crucial for insurers to have a deep understanding of not only who they are targeting but also who is seeking them. This may involve developing effective lead generation strategies and partnering with quality third-party providers, especially when entering the direct-to-consumer market. Starting with familiar or well-defined markets, such as affinity groups, could provide a valuable entry point into underserved segments.

For those underserved markets (and all segments), it is essential for the industry to ensure it is fulfilling a true insurance need with its product offerings, not merely seizing an opportunity. This may involve creating offerings that fill the gap between simplified issue and fully underwritten products, both in terms of underwriting rigor and pricing.

Insurers should strive to manage price sensitivity, striking a balance between adequate pricing for the risk and affordability for the target market. For example, individuals, particularly those who are younger, may have an appetite for paying a higher cost for a more palatable experience along with a product that is more understandable.

Conclusion: A cautious but committed approach

RGA's study provides valuable insights into the mortality considerations for underserved markets. While it reveals significant challenges, including higher mortality outcomes and limitations of traditional underwriting methods, it also provides a path toward innovative solutions.

As the insurance industry strives to close the protection gap, it must be cognizant of the realities of mortality differences in untapped markets. This means developing new underwriting techniques, leveraging advanced data analytics, and creating products tailored to the needs and risk profiles of underserved populations.

By approaching this challenge with a combination of caution and commitment, insurers can navigate the unknown territories of underserved markets, expanding their reach while maintaining responsible risk management practices. RGA is excited to work alongside carriers to provide solutions that will make financial protection accessible to all.