My family recently purchased me a coffee cup with the slogan, “I’m not always sarcastic, sometimes I’m sleeping.” And I get really sarcastic about the notion that insurers put the customer first.

What do customers want from insurance?

That is a pretty broad topic, so let’s explore. Each day, we interact with products that are customary, or quite simple. We are familiar with them and therefore can make decisions with the use of minimal information and help. On the other hand, there are products that are unfamiliar and complex and even if we work with them quite frequently are still confusing. Take the purchase of my internet service vs. doing my taxes. Although there are a number of different bundles and options for the internet, I will quickly settle in on the right service for me. When I do my taxes, even though this is an annual occurrence, I still seek the advice of a professional because my circumstances may change and the array of options is confusing.

Now consider insurance. We have some products like auto insurance that act a bit more like the internet service provider. Once I am comfortable with my limits of coverage, I likely renew each year without fail unless the provider does something that I question, like increasing rates. On the other hand, if I were to purchase commercial insurance, there are more moving parts -- my business may expand, payroll may change, I may add vehicles or I ay enter into a new service or product line. Commercial insurance takes some advice and hand-holding to ensure the coverages are appropriate and aligned with my expectation.

Customers want delivery that meets their needs. That delivery is what we call distribution. Whether through an agent, directly online or via a call center, distribution must bring order to chaos.

If we are going to make a breakthrough, where do we start?

First, we need to step back and evaluate the go-to-market strategy. If you do not have a GTM strategy or it is “do what we have always done,” then now is the best time to review.

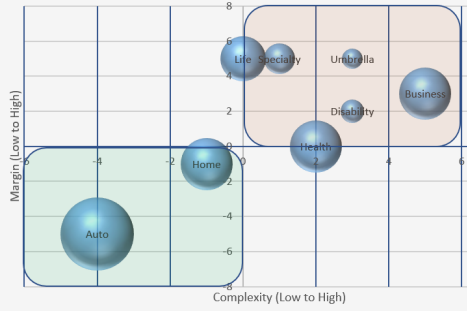

Each product in the insurance industry can be categorized based on two attributes that determine how you should take it to market:

- Product complexity

- Margin

A product that has high complexity and a high margin can and should be supported by an expert who can answer questions, customize coverages and explain the product choices. Contrast that with a product that has low complexity and low margin. This can and should be digitized.

The chart below depicts a simple view of the marketplace in terms of complexity, margin and market size. You could analyze your own offerings based on a qualitative and quantitative approach considering your own portfolio or considering the future growth opportunities facing your organization.

See also: How to Achieve Customer Ownership

Product Comparison of Margin v. Complexity by Line of Business

There is a linear path that exists in charting these products, suggesting that all lines of business fundamentally are either low-complexity and low-margin or high-complexity and high-margin. On the lower-left portion of the chart, competition keeps margins low, which means keeping complexity low. On the top right, you see products where competition may be more fragmented and where pricing advantages are not the only determining factor in taking market share.

How do you put this analysis into action?

First, plotting your own performance is key. Second, understanding your starting point and determining the important priority for each product will help you invest in the right change for the future. For instance, for a low-margin, low-complexity product like auto insurance, you may want to use agents today, call centers in the intermediate term and digital channels in the future, while high-margin, high-complexity products like commercial insurance would be taken to market by agents, whether now, in the intermediate term or in the future.

A few important points to consider:

- Agents and companies that do not perfect digital selling for low-margin/low-complexity products will suffer in the future.

- The idea that agents will disappear is false.

- Incumbent companies should evolve their distribution to obtain customers digitally and seamlessly refer these customers to professional agents to upsell and cross-sell. Insurtech companies need to consider this, as well, and the potential to partner with agents in the future.

- Companies that have agents need to support their agents in moving to more profitable products, opening new market opportunities and finding ways to compensate for the value they bring to the customer journey.

- Finally, decisions about change are guided by alignment with customer expectations first and further supported by financial success.

The road to the future will be paved by companies that understand that customers want a seamless purchasing experience for all their insurance products and are able to design a strategy that meets them where and how they expect to purchase important coverages.