Insurance is a data-driven industry, and underwriting is its heart. It’s an uncomfortable fact, then, that data from the only longitudinal study of North American P&C underwriters reveals that many important parts of underwriting seem to be mired in decline.

It is no overstatement to describe the results of the most recent Accenture and The Institute’s underwriting survey as alarming. Underwriting may be in crisis.

In my previous post, we looked at the survey results from a high level. Today, we’re going to zoom in on the findings about underwriting quality specifically.

Underwriters seem to be losing faith in their craft

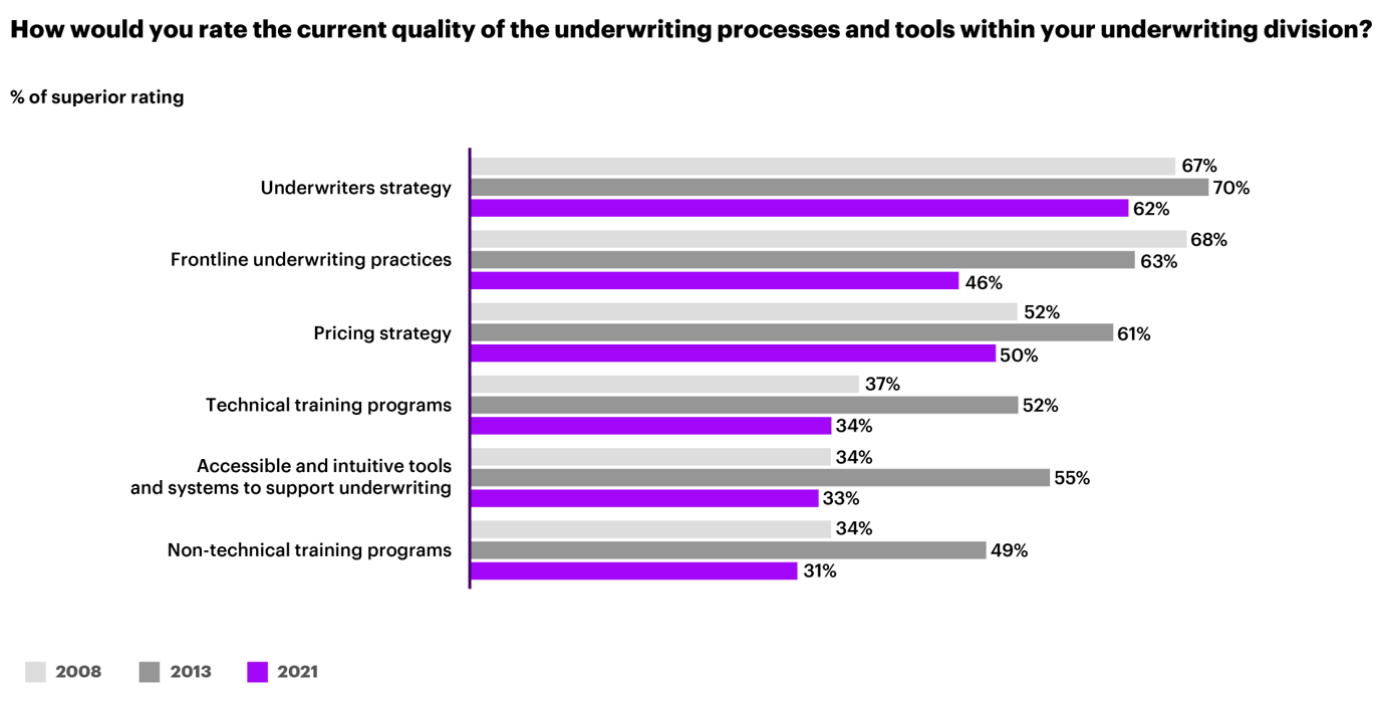

In 2008, 2013 and most recently 2021, we asked underwriters to rate the quality of the processes and tools they use to do their jobs. The scores for 2021 were the lowest we’ve seen—though, interestingly, the decline has not been uniform.

For example, 62% of underwriters in 2021 told us they’d rate their organization’s underwriting strategy as superior—down eight percentage points from 2013. Likewise, confidence that their organization employed a superior pricing strategy fell 11 points, from 61% in 2013 to 50% in 2021.

These are substantial declines, but they are far from the biggest ones in our most recent data. That dubious honor goes to confidence in the accessibility and ease of use of the tools used to support underwriting, which shrank from 55% in 2013 to 33% in 2021. Perhaps more concerning, confidence in both technical and non-technical training declined along similar lines.

We also asked underwriters to rate the importance of different areas of potential improvement for underwriting. The top four issues identified were, in order of the portion of underwriters highlighting them as important:

- Improving the quality and accuracy of data around underwriting submissions (95%)

- Improving training and talent development (91%)

- Improving tools for rating and pricing risks (90%)

- Eliminating non-core tasks to allow more time for risk analysis (88%)

See also: The Future of Underwriting

Change is needed—but where?

My view is that these findings are a clear indication that many underwriting leaders, amid the industry’s growing focus on expenses, growth and analytics, have taken their eye off the ball of traditional underwriting quality.

This has created a tremendous challenge for the industry, made more urgent as many markets are softening and the risks insurers cover grow more complicated. Do today’s underwriters have the skills they need to drive profitable business?

It’s not at all clear that they do—but neither is it a foregone conclusion that they do not.

In recent years underwriters have been equipped with many powerful new tools to help them measure risk and write policies more quickly. Our survey suggests that these tools have not had the hoped-for impact (and in some cases have actually made underwriting less efficient).

But the power of digital tools to take underwriting to new heights is still undeniable. To reverse the decline suggested by our survey, underwriters and carriers need to close the gap between the potential of these new tools and their actual impact on underwriting. This will require changing the carrier’s internal structure to let underwriters focus on underwriting.

It will also require making these modern underwriting tools truly accessible and intuitive. A good example of this is how underwriting guidelines are handled in the industry today. In general, these guidelines are more concerned with containing every piece of information that could possibly be useful than they are with helping underwriters quickly, accurately write the risk.

Guidelines instead should be broken up into pieces and made fit for purpose so that underwriters can quickly and easily find the information they need when writing policies. Ideally, a guideline system should “push” information to underwriters at the moment of need instead of requiring the underwriter to “pull” it from a lengthy document or database.

The digital tools to make all this happen, of course, are widely available in the industry today. This survey suggests that carriers that seize the initiative and implement changes along these lines will see a significant bump in underwriting performance.

In my next post, we’ll look at what the survey revealed about tech investment in underwriting.