One of my first articles having broad visibility at the international level was, "Will fintech newcomers disrupt health and home insurance?". Well, there is an insurtech that has tried. It is listed on the New York Stock Exchange, has a market cap of around $1 billion and has burned $628 million of cash since its foundation in 2015. (For reference, Lemonade has burned through $562 million).

How it started

How it's going

The distribution storytelling has evolved into a more pragmatic omnichannel approach, where "strongest growth is coming through partnerships, with attachment rates greater than 70% for embedded homeowners products offered through major developers"

I've posted in the past about their connected home approach and the embedded component [I like both these elements] and the bloody technical results of their book of business [I don't like them].

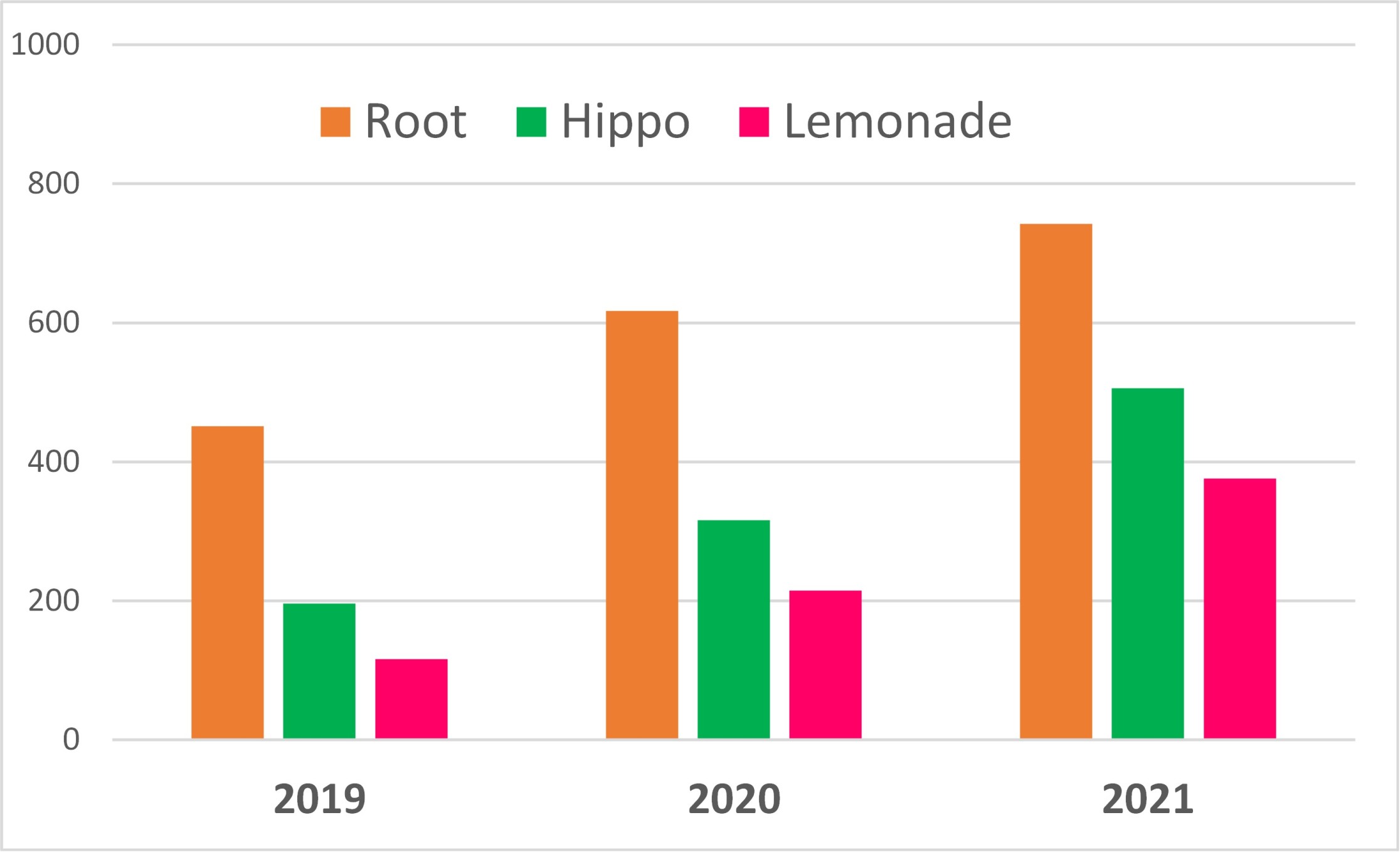

Hippo has recorded premiums of more than $600 million at the end of 2021. However, part of them comes from non-Hippo programs underwritten by Hippo's subsidiary Spinnaker. The size of the Hippo homeowners portfolio should be slightly above $500 million, compared with more than $300 million in 2020.

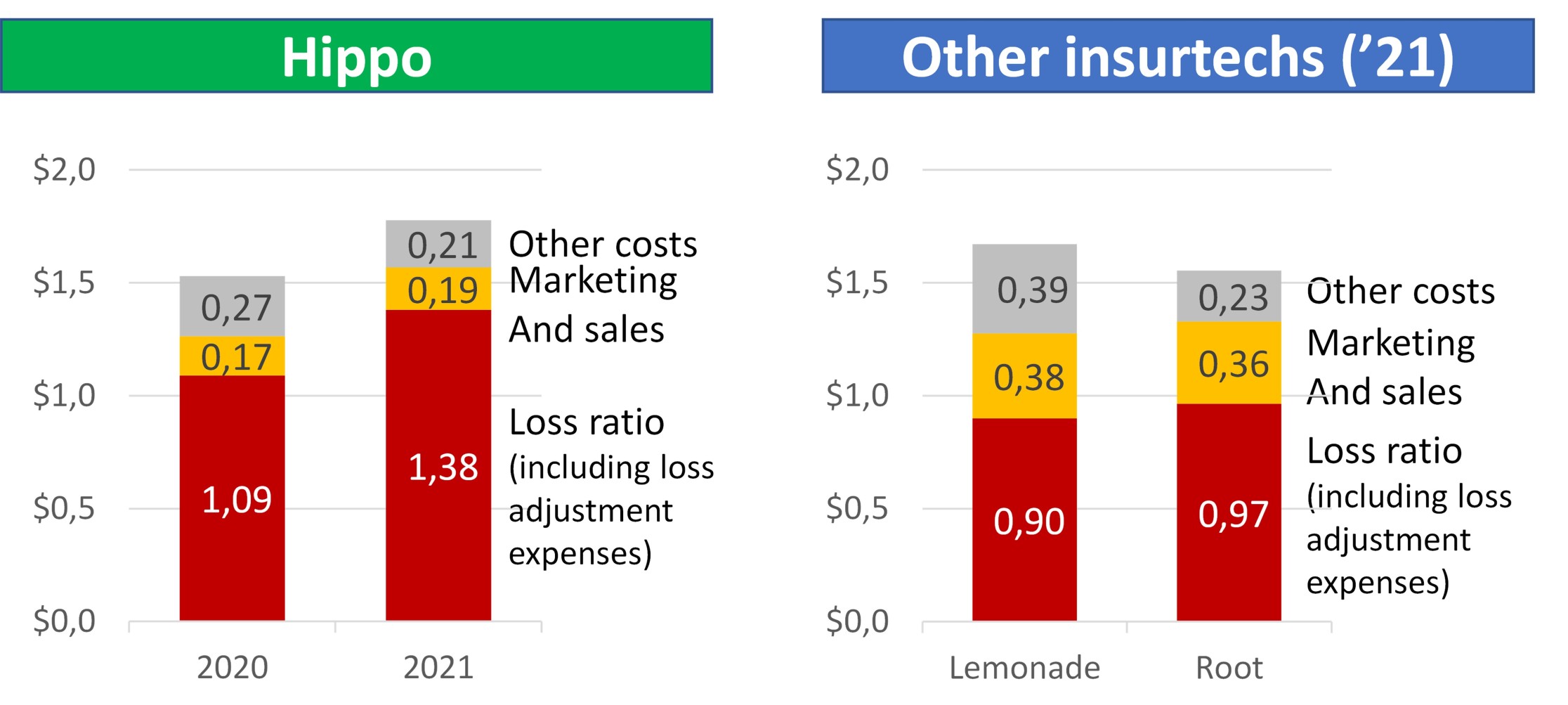

Each of these dollars of homeowner premiums written has cost Hippo more than $1.50.

It seems that the main problem - even worse than what we discussed about Lemonade and Root - is the loss ratio. The amount to be paid for claims is even higher than the premiums charged to clients.

An interesting article from Matthew Queen provided an optimistic perspective about the evolution of Hippo's loss ratio: https://seekingalpha.com/article/4493487-hippo-long-run-getting-shorter

See also: 5 Questions for Matteo Carbone on Smart Homes

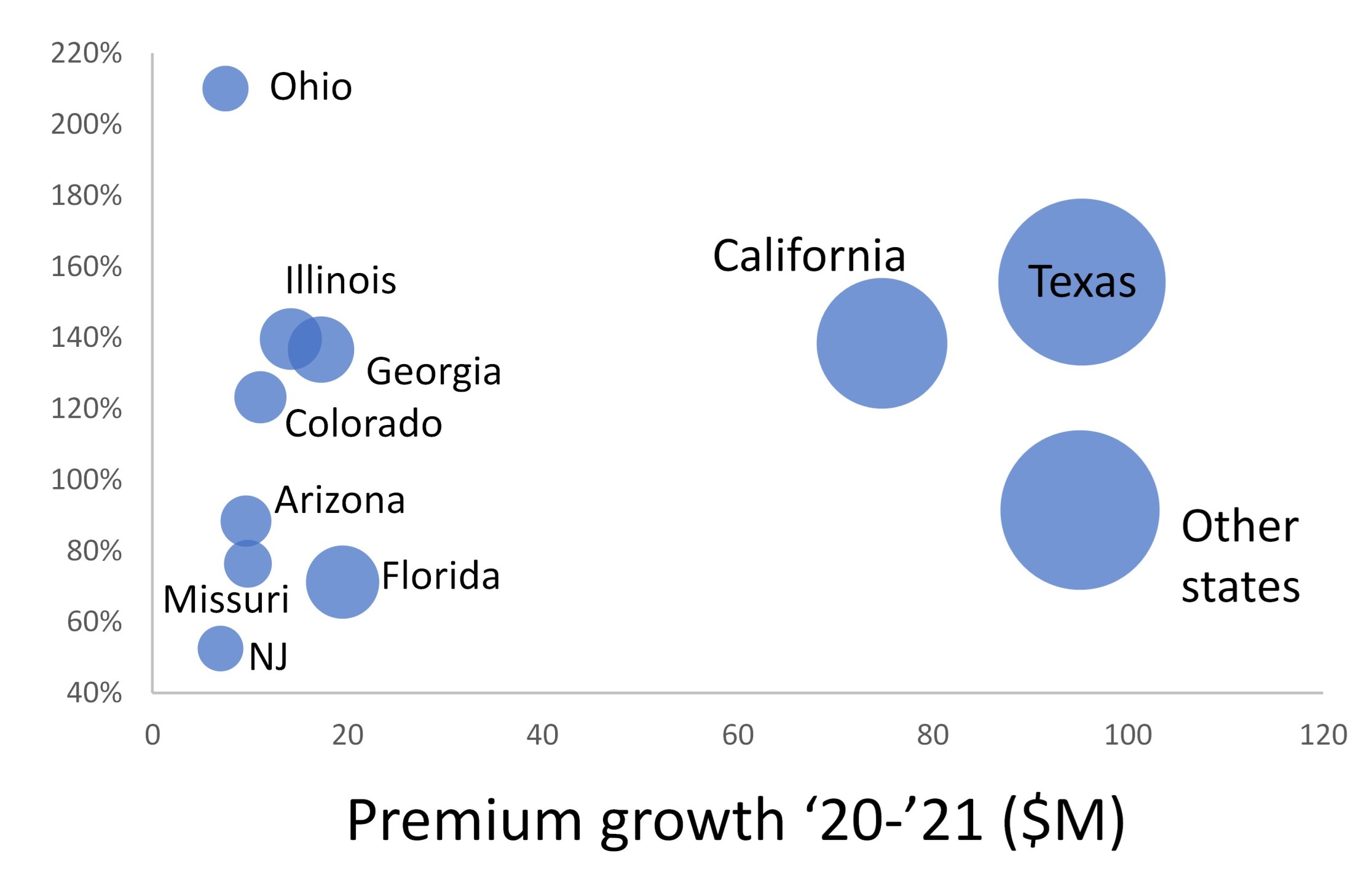

Looking at the geographical distribution on the Spinnaker annual statement. the bloody technical results seem pretty diffused.

An improvement is possible (if not probable). However, for sure there is no disruption around here, just maybe some more chances of surviving than other full-stack insurtech carriers have,

I remain positive about the potential of the smart home approaches in the U.S. homeowner insurance portfolios. I believe there are many opportunities for creating an impact using smart home data, but it is necessary to move beyond the gadget approach.

One great example comes from one of the members of my IoT Insurance Observatory: State Farm. They are scaling a smart home insurance portfolio. My exchange (below) with their VP, innovation and venture capital, Haden Kirkpatrick, shows the first results they are achieving.

Matteo: We have known each other for more than six years, and we have frequently exchanged thoughts about insurance incumbents' ability to innovate. State Farm is the first large carrier scaling a smart home program in the U.S., and I've been impressed by the 20,000 monthly installation rate shared by your tech partner Ting at the IoT Insurance Observatory plenary session last December. I would like to ask you to share your smart home innovation journey: "how it started" and "how it;s going."

Haden: Matteo, what a journey it has been. You and I have discussed for some time how “home telematics” is the new “mobile telematics” and will further change the game for the insurance industry.

We at State Farm have a complete innovation ecosystem, and Ting is a great example of that ecosystem at work. Ting was initially brought to us through State Farm Ventures, our corporate venture capital unit; we invested in Ting in 2019 and have been an advocate of them ever since. Throughout our time working with them, we are confident that we have saved more than 1,000 homes from electrical fires. Now, we are panning back to explore other loss types and connected home devices to see what else is possible in this exciting space. Our team is prototyping and testing with customers while we engage broadly in strategic partnership discussions and tactical go-to-market planning for a wider range of offerings, within which Ting will be central.

Matteo: This approach uses IoT data for preventing a risky situation and avoiding a claim from happening. I've always considered these smart actions an extraordinary opportunity for insurers, because they affect directly the core of the portfolio technical profitability. Could you share the results already achieved in the electrical fire risk reduction through this smart home solution?

Haden: Today, we have 132,000 customers enrolled in the program. Since launching the program, Ting has been able to detect several hazards within our customers’ homes. We’ve seen problems with main panels, faulty heating blankets, sump pumps and even old Christmas decorations. The feedback from our customers who had hazards discovered has been overwhelmingly positive.

A benefit that we didn’t expect initially was the value provided by Ting in uncovering hazards that occur outside the home. These hazards occur when there is a problem with power coming into the home from the utility provider. In these cases, the customer works with the utility company to resolve the issue. This not only benefits our customer but the utility customers in the neighborhood.

From Risk Transfer to Risk Prevention from Matteo Carbone

Matteo: I'd expect that this new State Farm service offered to the homeowner policyholder is also increasing the frequency of interaction with them. Insurance has always been something relevant but not frequent in the daily life of people. So, smart home insurance seems a great opportunity to be more present for the insurers. Would you like to share any facts and figures about the customer engagement?

Haden: Our thinking on your core comment (the relevance vs. frequency of engagement) and the challenges of “passive engagement” is shaping our future.

Customers receive an email each week that provides a summary of their Ting monitoring and any events that have occurred. In addition to that, they get a monthly email with helpful hints and tips along with real stories where Ting has saved the day.

State Farm’s mission is to help people manage the risks of everyday life, recover from the unexpected and realize their dreams. While insurance is core to how we achieve our mission, we see so many more opportunities to help people. The simple fact of the matter is that consumers overall are exposed to risks that limit their ability to live complete and fulfilled lives. State Farm has been the industry leader for decades, and we’ve always recognized our responsibility to go beyond insurance and find ways to build stronger and safer communities for customers and the communities where they live.

Beyond helping to mitigate losses in the first place, this is a way to have a more meaningful relationship with our customers and the broader market to help them be safer and better protected overall. That will be the focus of our innovation efforts going forward.

Matteo: Promotion of less risky behavior among the insured portfolio has always been part of the sector philosophy. You have just shared how State Farm is doing it in a faster, more effective and more precise way. I love it! However, I'm now curious to hear your vision for the future. What is the role that you see for the insurance sector in the (smart) houses in 10 years? What's next in your home insurance innovation journey?

Haden: More so than in most categories, our research shows that consumers expect the insurance industry to lead the way as it pertains to helping people prepare for and mitigate the risks that we see increasing in the macro environment. When customers are presented with areas of opportunity on which they care deeply (sustainability, security, etc.), they have a desire and are willing to take action, but they simply may not know what to do, and nobody is helping them to facilitate the process in a safe, trusted manner by which they can get engaged and drive change among themselves and their community.

Interestingly, these customers often reference their insurance carrier as the trusted source to help with these issues. With State Farm’s strategic assets (brand, financial strength, agency network, etc.), we are better positioned to deliver here and, by extension, help lead the industry toward a better future for our customers.

Sign up for my daily insurtech posts: https://bit.ly/RINGmyBELL