In an in-depth study, Weighing the Evidence, RGA has quantified the expected mortality and morbidity impacts of incretin-based drugs, including GLP-1s, approved as anti-obesity medications (AOMs) and diabetes treatments in the U.S., U.K., Canada, and Hong Kong. Results include the following key findings:

Population mortality

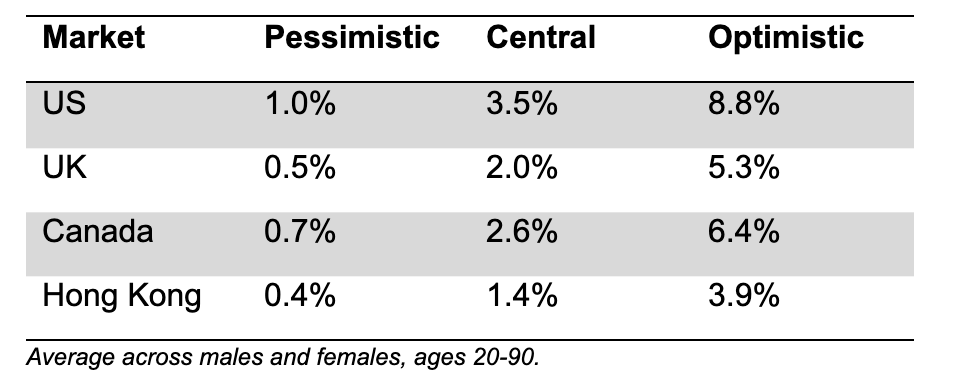

- By 2045, incretin-based drugs such as GLP-1s could reduce mortality in the U.S. by 3.5% in a central scenario, 8.8% in an optimistic scenario, and 1.0% in a pessimistic scenario.

- Under the same central scenario, mortality could decrease by 2.0% in the U.K., 2.6% in Canada, and 1.4% in Hong Kong.

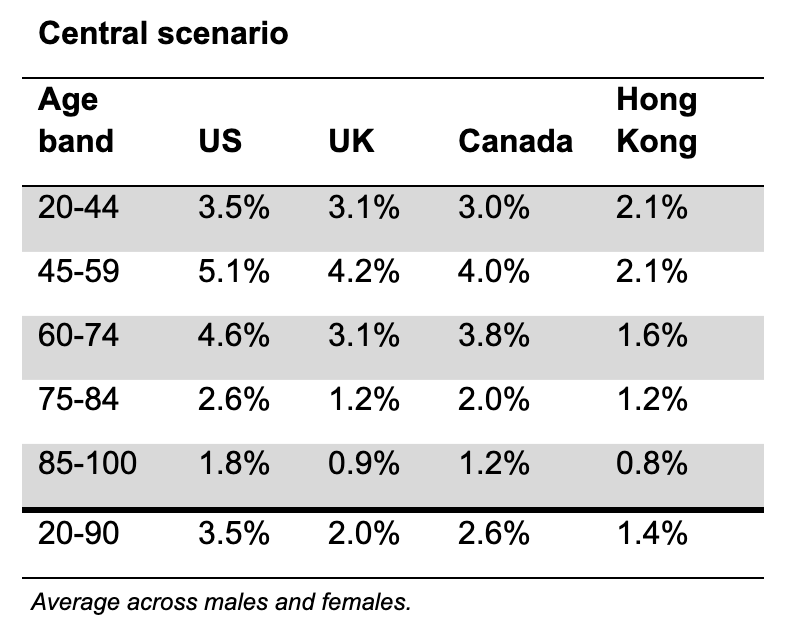

- Mortality improvements vary by age, with ages 45-59 seeing the biggest reduction and age 85+ the lowest reduction.

Population morbidity

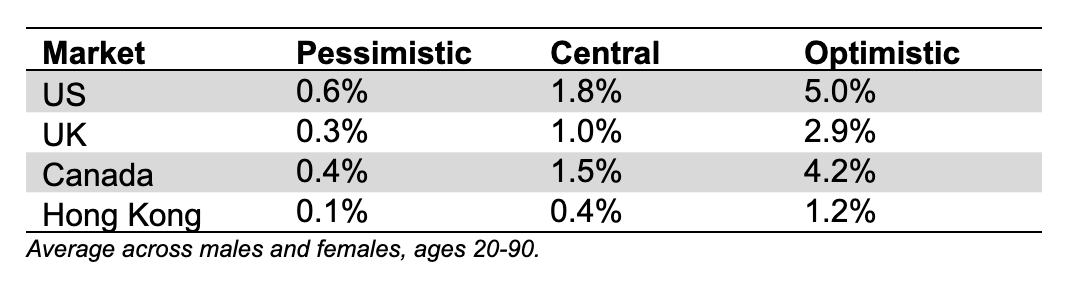

- Populations could see smaller but still positive reductions in the incidence of cancers over the same period.

Insured mortality and morbidity

- Insured groups and annuitants are likely to see somewhat lower mortality and morbidity reductions than the general population.

The report also explores how the impact of these treatments could exceed those projected in RGA's central scenario and the potential for further reductions in mortality and morbidity as the therapeutic landscape for incretin-based drugs expands beyond obesity and diabetes. The authors further outline considerations for insurers on how to incorporate the report's insights into future improvement bases and highlight implications for underwriting, claims, and policyholder behavior.

Key Takeaways

1. At the general population level, AOMs will have a meaningful impact on mortality.

This will differ by geography, largely reflecting the obesity profiles of different markets, and by age, sex, and access to the drugs.

RGA models the impact of AOMs over the next 20 years to 2045 with reference to three key groups of assumptions: effectiveness, uptake, and relative risk of mortality and morbidity. The report calculates optimistic and pessimistic scenarios by flexing these key assumptions to plausible higher and lower values. The chart below shows the expected mortality impact of these scenarios at the population level.

Table 1: Cumulative population mortality improvements over 20 years to 2045 due to AOMs under three scenarios

It is important to recognize that the impact of AOMs will vary by age, reflecting differences in obesity levels, the mortality risk associated with obesity, and differences in uptake. The table below shows the expected mortality impact in the central scenario by market and by age.

Table 2: Cumulative population mortality improvement impacts over 20 years to 2045 due to AOMs by market and age

2. AOMs will likely have a smaller impact on general population morbidity.

The report defines morbidity as the incidence of claims under a typical critical illness product. Cancer is the largest single cause of morbidity incidence in critical illness products. While reducing body mass index (BMI) does reduce the risk of cancer incidence, it is not to the extent that lowering BMI reduces mortality risk. Therefore, RGA expects morbidity impacts to be generally smaller than the corresponding mortality impacts.

Table 3: Cumulative population morbidity improvements over 20 years to 2045 due to AOMs under three scenarios

3. Insured groups are likely to see somewhat lower mortality and morbidity impacts than the general population.

Lower average BMI means less scope for improvements, even though insureds have greater access to the drugs.

Insured lives and annuitants typically come from a higher average socioeconomic group than the general population and generally are expected to have a lower average BMI. Insured lives are also typically underwritten and have a different mix of causes of mortality and morbidity than the general population. The RGA model projects that the lower average BMI for insured groups has more impact than the increased ability to access the drugs, and so the overall mortality and morbidity impact is typically lower than for the general population. The actual impact AOMs will have will reflect the characteristics of a life and health insurer's insured portfolio.

4. An insurer's current mortality trend assumptions likely include anticipated improvements from drivers such as medical advances.

It may be too early to make material adjustments to those assumptions for AOMs, but they increase confidence in future mortality and morbidity improvements.

RGA's study results described so far reflect changes to current mortality and morbidity rates. When translating to impacts on assumptions, it is important to consider that (re)insurers already assume positive improvements in the future. Anti-obesity medications are a tangible advance contributing to these future improvements.

5. This is a fast-moving space with significant uncertainty.

Model assumptions will need refining as new evidence emerges and as new indications for the drugs are approved.

The upside potential of these drugs is exciting, but challenges linked to safety, side effects, access, and adherence need to be overcome to achieve the full impacts anticipated in this report. While cost is currently a barrier to uptake, growing competition and the arrival of generic and oral formulations are expected to lower costs significantly. The next wave of incretin-based therapies is poised to offer significant advantages over the current generation for treating diabetics and for weight loss in those living with obesity. RGA's model has already anticipated some of these developments, but this is a fast-moving space that requires continual review of model assumptions.

Incretin-based therapies are under active investigation to treat a growing spectrum of medical conditions ranging from neurodegenerative disorders to substance abuse. As approved indications continue to broaden, and adoption scales in those with established disease, the cumulative impact on public health could be profound.

There is growing interest in the potential of incretin-based drugs as preventive medicines. Their systemic anti-inflammatory effects, metabolic regulation, and influence on satiety and insulin sensitivity suggest they could help prevent the onset of multiple chronic conditions. If these benefits extend to individuals without established disease, there could be a significant reduction in morbidity and mortality across the general population.

6. Insurers should consider the impact on business, including pricing and reserving assumptions, new policyholder behaviors, underwriting, and claims.

RGA's companion paper, "Evaluating Biometric Trend Drivers: How to reflect medical breakthroughs and other drivers in forward-looking assumptions," explores the practicalities for insurers in maintaining an up-to-date view on emerging biometric trend drivers such as AOMs and provides a framework for incorporating the insured mortality impacts into insured improvement bases.

The use of AOMs introduces the risk of anti-selective policyholder behavior, as individuals who have lost considerable weight may lapse their rated policies and re-enter with better terms. As such, insurers may not capture the full economic benefit of improved mortality and morbidity.

The increasing use of AOMs will significantly influence underwriting risk assessment. As evidence accumulates, underwriting approaches must evolve to recognize improvements while maintaining vigilance to validate these therapies' potential. Accurate disclosures at the underwriting stage may need to be validated at the claims stage, and claims assessors will require a deep understanding of the use of AOMs to ensure accurate interpretation of disclosures made as part of the insurance application.

Conclusion

AOMs have the potential to significantly improve population mortality and disease incidence rates.

The impact on insured groups is likely to be somewhat lower, and it may be too early to make material adjustments to insured trend assumptions, but the efficacy of AOMs to date increases confidence in future mortality and morbidity improvements.

This is a fast-moving space with significant uncertainties, so monitoring developments closely will be vital to responsible and successful insurance practices. Model assumptions will need continual refining as new evidence emerges and as new indications for incretin and hormone-based medications are approved.

To learn more, view the full study: "Weighing the Evidence: Quantifying the mortality and morbidity impacts of GLP-1 and other incretin-based drugs in the US, UK, Canada, and Hong Kong populations."

Additional Contributors: Dr. John J. Lefebre, Vice President and Senior Technical Global Medical Director, Global Medical; Matt Battersby, Senior Vice President, Head of Global R&D; Marilda Kotze, Vice President, Head of Global Underwriting & Claims