Now is the winter of our discontent. With this famous line, Shakespeare voiced the frustration of a prince with kingly ambitions, but the sentiment is familiar to modern homeowners, agents and insurers. Winter is notorious for plumbing failures. Frozen pipes and related issues account for a growing share of water-damage claims, and losses add up quickly.

Home issues compound this time of year, from burst pipes and ice dams to heating system failures and holiday fire hazards. Property insurers know that many of these incidents are preventable. Most can be avoided with routine maintenance and better visibility into smart protection systems. And it's up to insurers to help homeowners understand the risks before they turn into losses.

Winter Woes & Tech Solutions

Plumbing failures remain one of the biggest drivers of non-weather water loss. Aging infrastructure, temperature volatility and unmonitored second homes create the perfect storm that leads to high-severity claims. Close to 23% of U.S. home insurance claims are categorized as "water damage or freezing," which includes pipe freezes and burst-pipe losses. It's second only to wind or hail, with average claims costing more than $15,000. Homeowners often don't realize pipes are vulnerable until after they burst, especially in attics, garages, exterior walls, pool houses and crawl spaces.

As winter plumbing failures escalate with more volatile weather swings, the need to adopt technology becomes clearer. Modern shutoff valves can prevent or reduce the severity of water damage by stopping the flow before a leak spreads, but a device that's incorrectly installed, unplugged or offline offers no protection.

Devices installed in cold-exposed areas or crawl spaces often fail because they're placed in vulnerable spots, leading to flooded boxes and power shutoffs. Industry monitoring data shows that 30–50% of insurer-credited shutoff systems are offline or not functioning properly, meaning homeowners believe they're protected when they're not.

Reducing Risk Through Seasonal Checklists

Risk management experts recognize the scenarios where homeowners consistently discover gaps in coverage. Some learn too late that losses tied to neglected maintenance are excluded, such as frozen pipes in unheated areas or long-term leaks. High-net-worth property owners in particular may assume "everything is covered," but policy sublimits for water damage vary widely. Secondary and vacation properties are also disproportionately exposed due to extended vacancy and delayed monitoring.

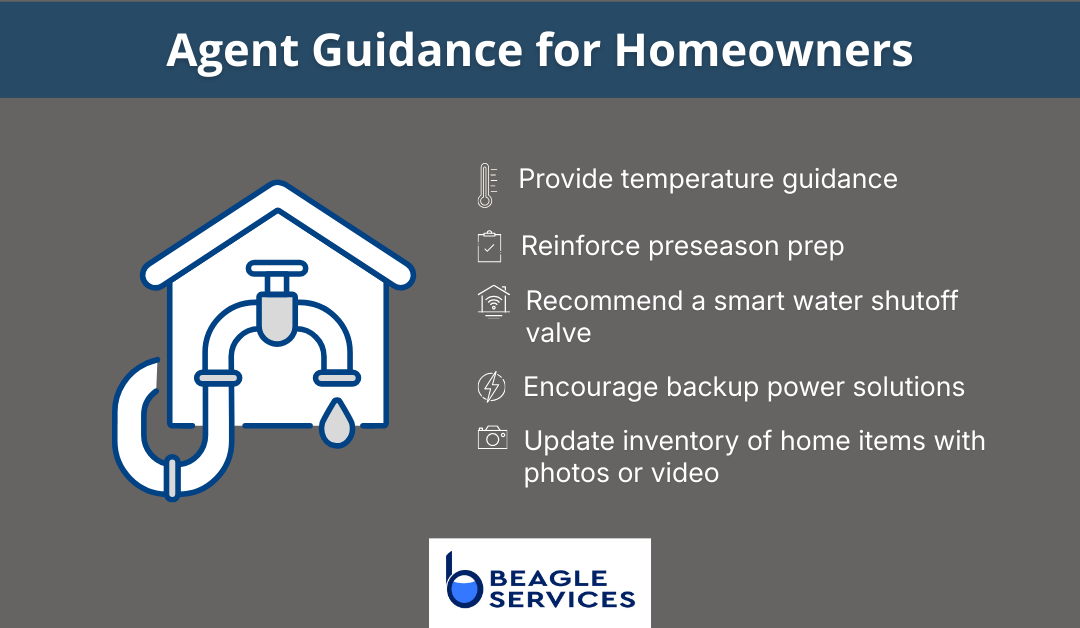

Carriers and agents can give clients clearer guidance on avoiding winter damage by reinforcing these steps:

- Providing temperature guidance — reminding customers to keep thermostats at 65°F or above, especially while traveling. Lower settings may save money, but temperatures that drop too low can cause pipes to freeze and expand, putting faucets and plumbing at risk of cracking or bursting.

- Reinforcing preseason prep — advising homeowners to shut off and drain exterior spigots and irrigation lines before the first freeze and to cover them with a pool noodle, a towel, or covers purchased from a hardware store.

- Promoting smart devices — encouraging customers to install automatic shutoff devices and to verify monthly that they are online; many losses occur because devices are installed incorrectly or are offline.

- Emphasizing backup power — recommending battery or power backup so leak-detection and shutoff devices stay active during outages.

- Making claims easier if something does go wrong — encouraging homeowners to maintain an updated inventory and a brief photo/video walkthrough documenting the items in their home.

At the end of the day, insurers provide something more than coverage; they provide peace of mind. And agents play an equally critical role as trusted advisors who help homeowners understand risks, make informed decisions and stay ahead of preventable losses.

Helping Homeowners Stay Educated

Beyond plumbing, carriers and agents should leverage their communication channels – email, social media, mailers and seasonal checklists – to highlight other winter risks. Unattended holiday candles and overloaded electrical circuits can quickly escalate into fire-related claims. Downed trees and ice-related roof damage are more common after early freezes followed by rain. And temporary residents, from visiting family to short-term renters, add risk that homeowners may overlook.

Insurer education remains essential to reducing loss severity and strengthening client relationships. Making this outreach before cold-weather events ensures homeowners are equipped with the right knowledge and coverage. Technology can help, but protecting a home still requires attention and involvement.

As the Bard wrote, our remedies oft in ourselves do lie.