Warren Buffett recently paraphrased the thoughts of an unnamed insurtech: “'We are not an insurance company. We’re a tech company.'" He added: "Well, they’re an insurance company…A dozen people or so have raised a lot of money. They just don’t pay any attention to the fact that [they] sell insurance…. In the end, they wrote insurance and overwhelmingly lost a lot of money.”

Let's see if he's right. Let's look at the Q1 financials of these insurtechs to see how they're doing.

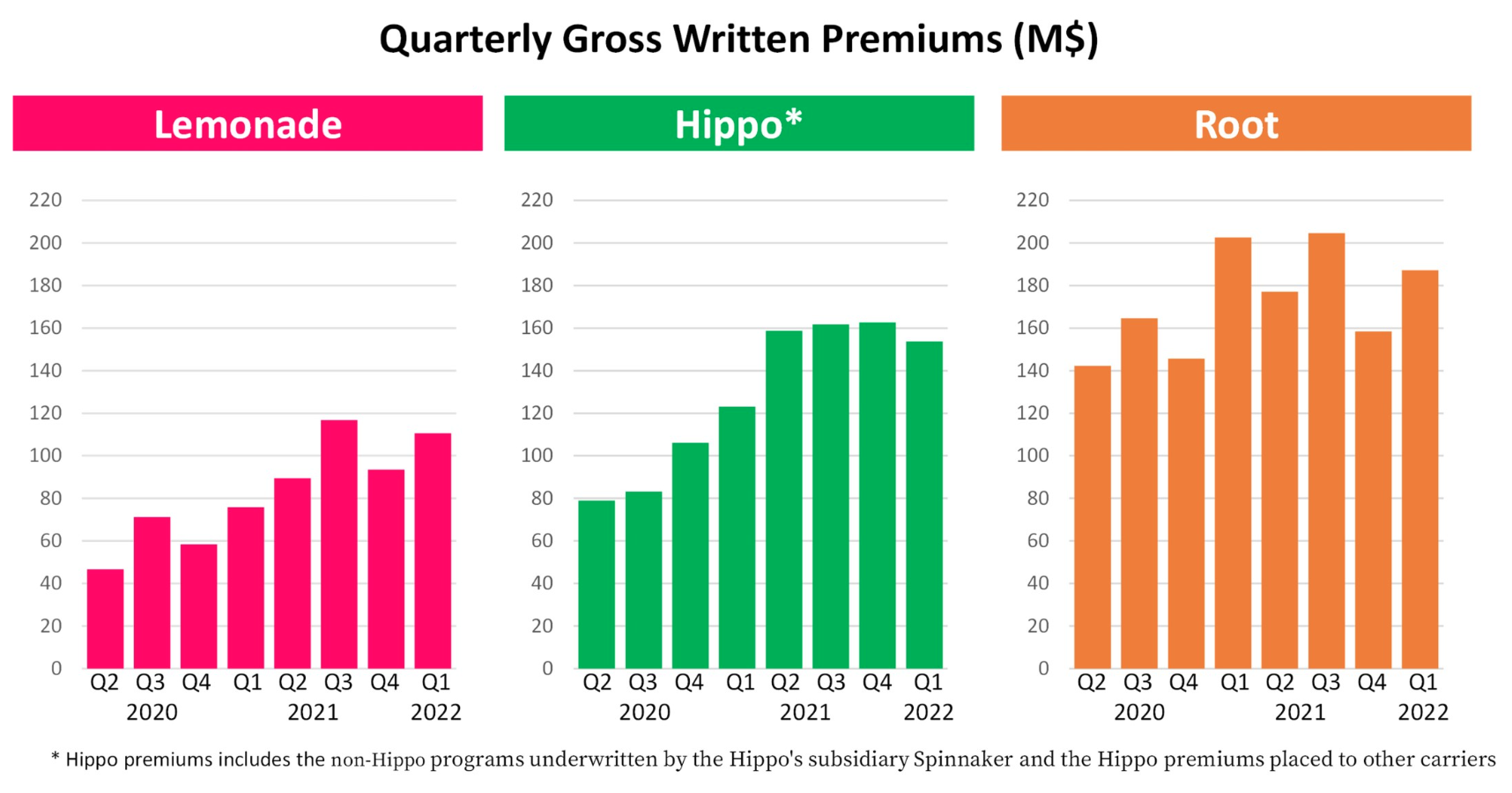

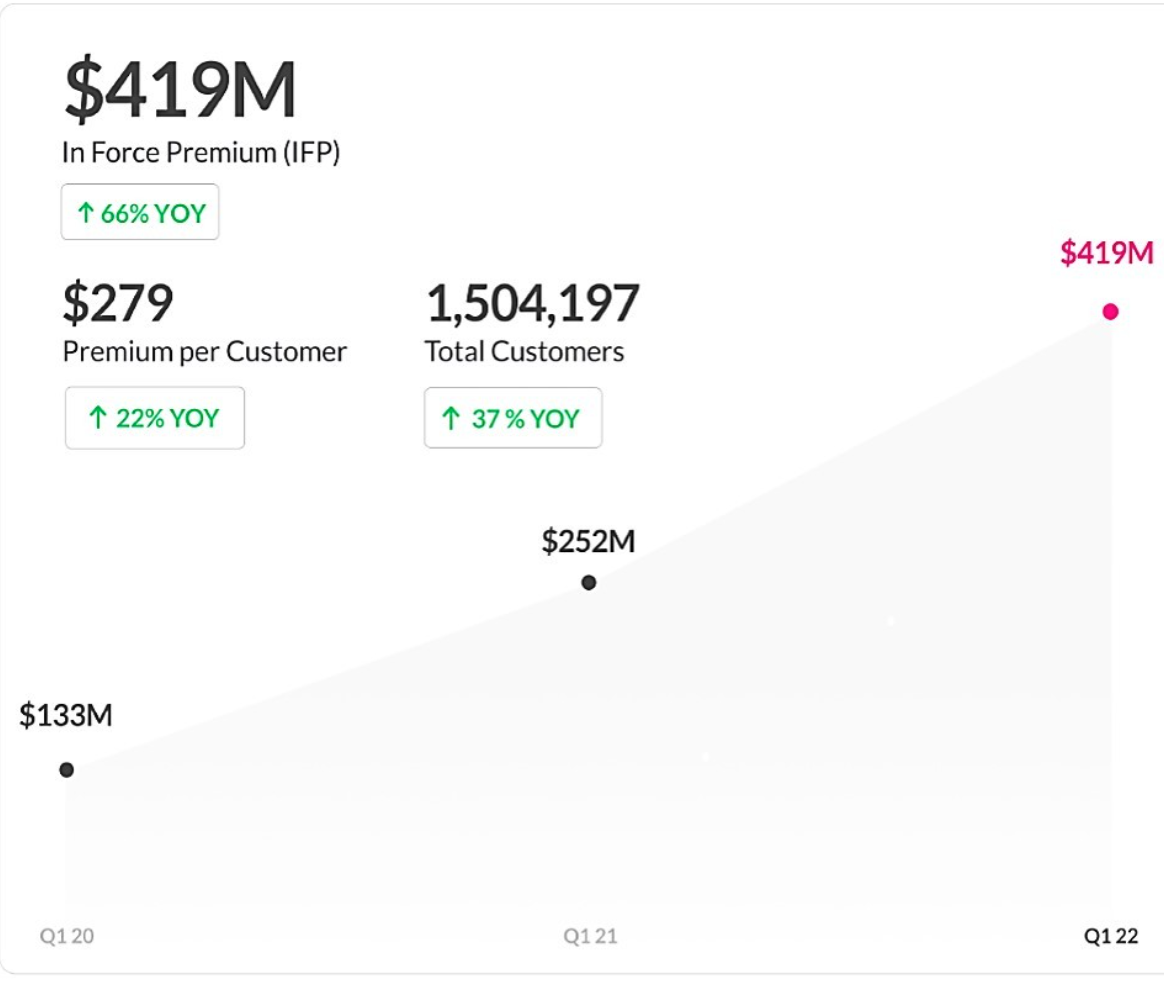

Lemonade

- Loss ratio: 90% gross loss ratio in Q1 '22 (in line with the 90% loss ratio that led to a 167% COR for 2021)

- Burned cash: $59 million in Q1 '22

- Short interest: 34% of float (MarketBeat data at May 15)

- Market cap: $1.42 billion at May 27 (-46% YTD)

See also: Lemonade: No Sign of Disruption Yet

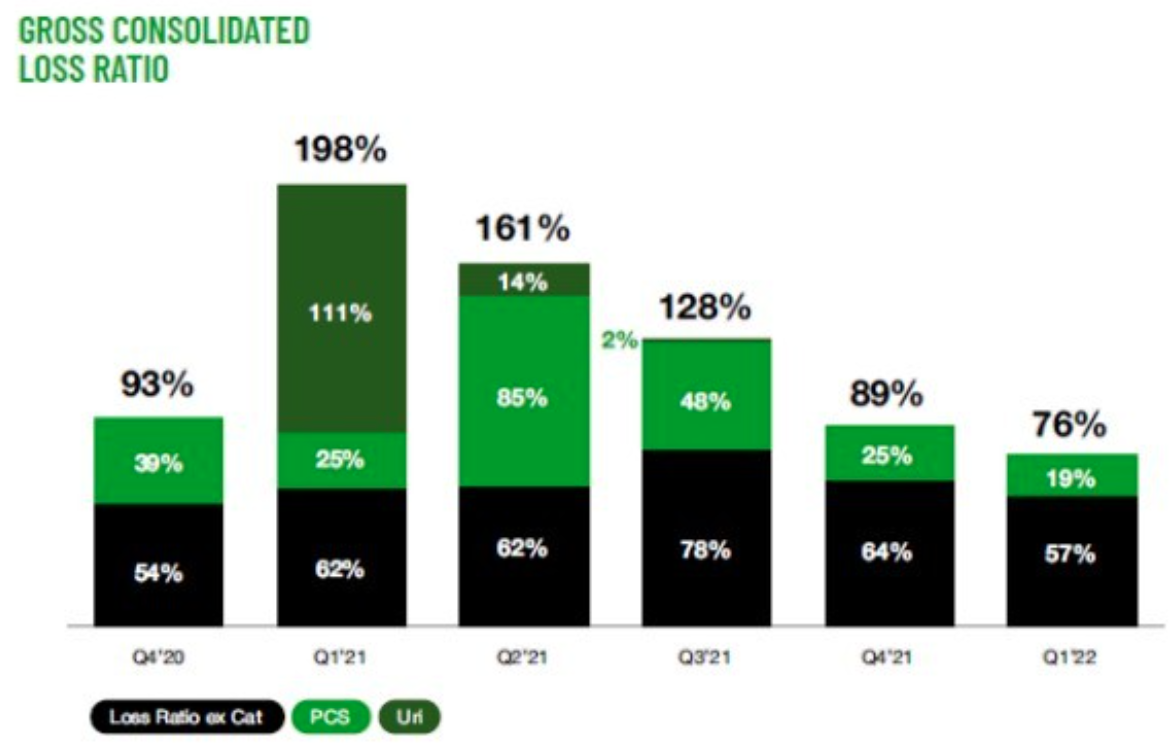

Hippo

- Loss ratio: 76% gross loss ratio in Q1 '22 (significantly improved from 138% loss ratio, which led to 178% COR for 2021)

- Burned cash: about $59 million in Q1 '22

- Short interest: 1.6% of float (MarketBeat data at May 15)

- Market cap: $800 million at May 27 (-50% YTD)

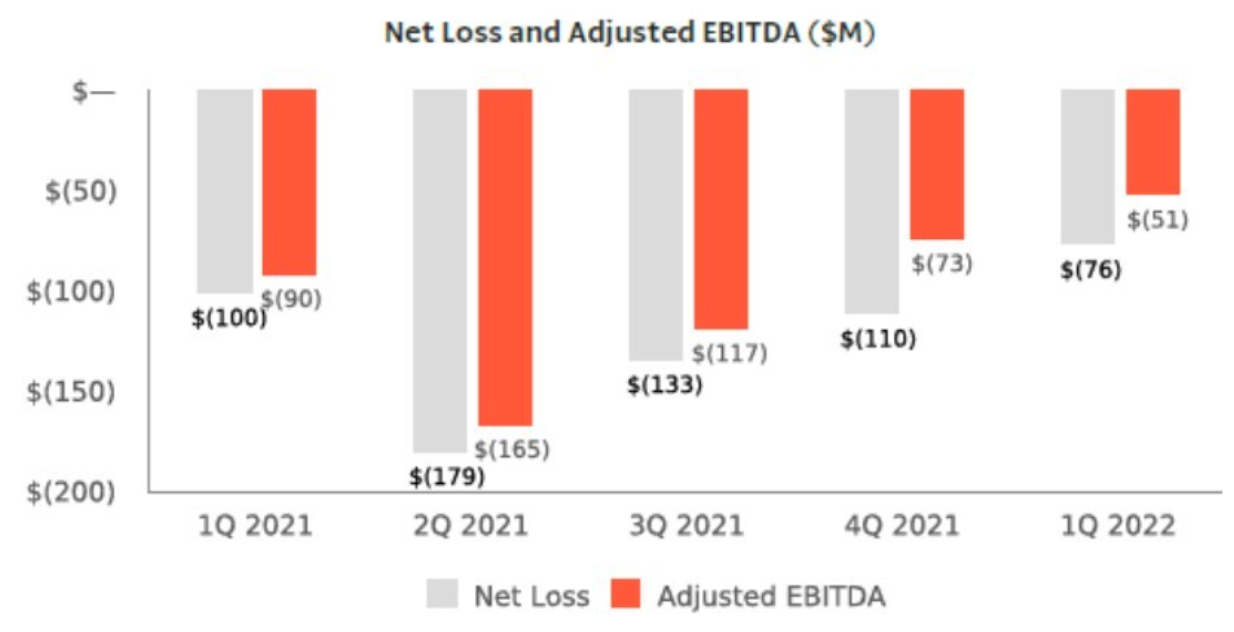

Root

- Loss ratio: 93% gross loss ratio in Q1 '22 (slightly improved from the 97% loss ratio, which led to a 157% COR for 2021)

- Burned cash: about $57 million in Q1 '22

- Short interest: 4,8% of shares (MarketBeat data at May 15)

- Market cap: $360 million at May 27 (-57% YTD)

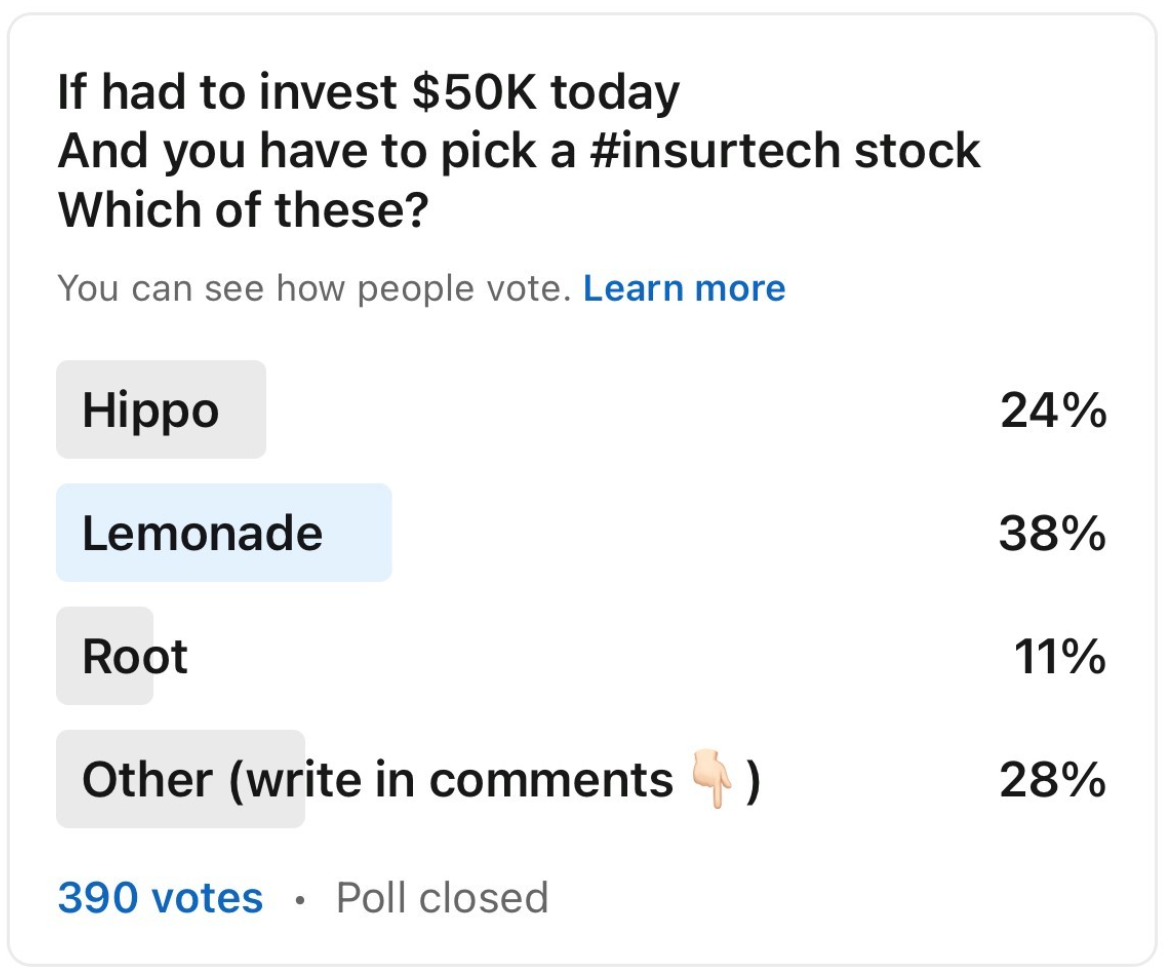

Despite the facts and figures, fascinating stories show impressive resilience. After the publication of these financials, I did a LinkedIn poll to assess my network's current mood about these stocks.

The poster child of the insurtech passionate stays on top of the ranking!

I'm a firm believer that insurtech solutions will make the insurance sector stronger, therefore more capable of achieving its strategic goal of protecting people's lives. I hope the next wave of insurtech players will have more robust insurance fundamentals than the first wave and will not pretend that insurance ignorance is a competitive advantage.

I've been lucky over the past four years to work with Andrea Battista on Archimede SPAC and -- after the acquisition of Net Insurance -- as a board member of the listed combined entity, which has overperformed the plan we designed initially. This is a concrete experience where insurtech solutions have been integrated into the insurance value chain to perform the insurance job better (to assess, manage and transfer risks). Lessons learned: tech & underwriting discipline!

We have seen hundreds of insurtech articles with click-baiting headlines claiming a coming disruption in the insurance sector for the last seven years. Now they are shifting to the underwriting discipline.

Talking about past disruption expectations and current mood, Bill Harris, chief revenue officer at Insuretech Connect, adds some color.

Matteo: ITC is at its seventh edition; you have observed the entire first insurtech wave. What is your critical review of these seven years? How has the thinking of industry leaders changed?

Bill: When we launched ITC back in 2016, it was all about disruption, and we asked, “Will insurtechs replace traditional carriers?” It’s evolved into a more symbiotic relationship. Now, carriers understand insurtechs can help enhance their offering, and especially how to be more customer-centric. When we began seven years ago, investment was everywhere, the first million was easy to get. We are now seeing a trend where it may be harder to get the early seed/Series A investments, but the investment amounts in later rounds are much bigger. To us, it indicates that the VCs and CVCs know exactly what they are looking for and are not scared to invest massive rounds in companies that can really scale.

It's been interesting to observe insurtechs that have become carriers and gone public. A few on our team might say that it’s been more interesting to see the likes of Trov, Bold Penguin and SingLife be acquired by carriers. Also, we are delighted to see how insurtechs such as Flock or Zego are evolving and expanding their lines of business. ITC is a platform where you come to see new and emerging insurtechs, plus new product launches from innovators that we’ve seen evolve over the past 7 years.

See also: Strategies to Combat Barriers to Insurtech

Matteo: What should people expect from ITC 2022?

Bill: We’ve developed a meaningful formula for ITC, so we will continue with a focus on making connections and showcasing the top thought leaders. We recently announced that McKinsey is joining us as the presenting sponsor at ITCVegas, which is a great honor for us.

One innovation to our content is that we will host 14 distinct tracks across seven stages to make it easier to plan your time. We look forward to seeing you again, Matteo!