Customers now expect exceptional service from all businesses, and low-code platforms hold great promise for businesses’ internal and external users alike. They’re capable of aggregating data from multiple administrative legacy systems and quickly bringing value to customer service functions.

Many of these platforms are rich in user interface functionality. They allow for drag-and-drop efficiency instead of burdening users with extensive lines of code. Circumstances may not be as flexible as with other technology, but the speed and integrity of low code make it a viable choice.

Additionally, integrating low code to existing IT operations provides modern tech experience to in-house system managers who, in turn, grow their expertise. For example, domain experts can immerse themselves in articulating need requirements and even build out the solution. Those who already have systems development expertise can be assets in the transformation.

See also: Thinking Big for True Transformation

Low-code platforms are rich in functionality and capable of rapidly creating enterprise-level applications, and vendors offer different solutions with varying levels of functionality. Some are robust with powerful capabilities, providing user interfaces, automated workflows, automated case-management processes, integration with many different systems and more.

These solutions often come through built-in connectors to automate processes.

IT pros in the insurance industry both influence and benefit from digital transformation. IT has significant experience with methodology and process. Pros understand and can describe business requirements in a product backlog and are familiar with testing and deployment processes. Such IT experience can be advantageous if complex integration needs arise. In turn, the platform offers significant leverage to the product team seeking an automated solution to a business problem.

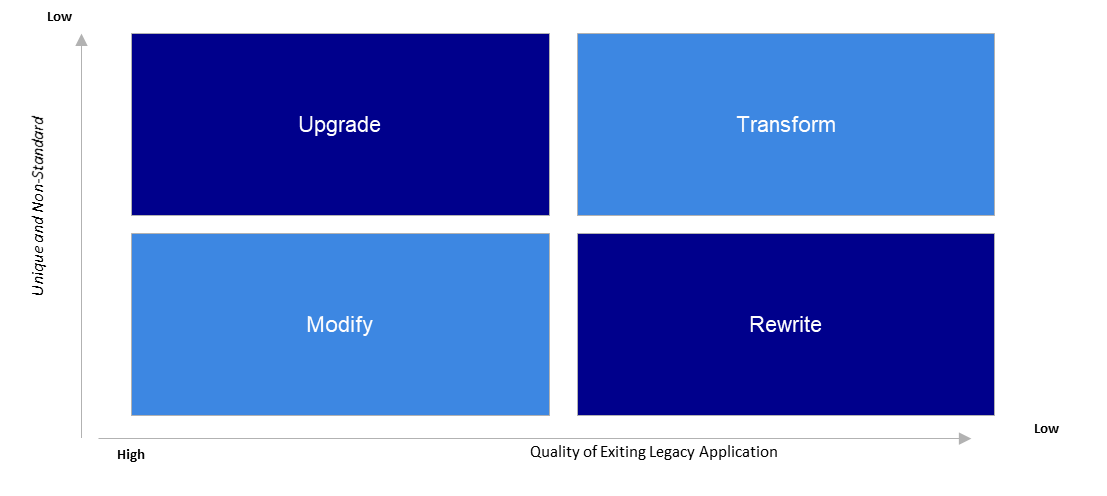

Some businesses find themselves frustrated by the functionality of commercial off-the-shelf packaged software. Those products result from requirements dictated by the larger market needs and generalized feature set, though this is now changing. These features may not apply to all and may need heavy customizations to adapt within an existing ecosystem. Such frustration is a low-code opportunity that's tailorable to a client, suits its needs, is cost-effective and is simply a better fit.

There are four ways for insurance organizations to leverage low-code:

- Build out enterprise-class applications.

A full-stack platform brings everything necessary to create a customer-facing user application. That includes a user interface, business process management, business rules, case-centric capabilities, content and document management power and third-party connectors that allow connectivity that provides for and extends legacy systems.

- Complement an existing system.

Underwriting often involves manual processes where paper notes present valuable information. However, it is hard for software systems to digest and make sense of this material. Low-code solutions with character recognition and language processing capabilities can integrate and automate gathering this vital information.

- Integrate relying upon multiple existing systems.

Low code can orchestrate leveraging these systems into modern service, whether administrative, claims, internally developed or inherited systems or multiple other varieties.

- Reduce technical debt

Low code is easy to maintain and increases user productivity by speeding the development process. It reduces several tasks to a single workflow, enabling more automation and integration of apps, ultimately reducing overhead costs.

Many legacy systems are expensive and complicated to migrate. Retaining these systems but capturing information held within them through low-code platforms makes all that intelligence available to the user. Low code simplifies. It brings efficiency and value to the business while managing costs and risks.

See also: 3 Ways to an Easier Digital Transformation

Moving to this level takes significant commitment. Insurance IT infrastructure can be well out of date. If merging old technology with new was a simple one-to-one proposition, every company would’ve done it long ago. Additionally, mergers and acquisitions among organizations that keep creating short-term demands to absorb various legacy systems steal from long-term transformation plans.

There are no indications that this fluctuation will slow any time soon. While making sense in a chaotic environment, insurers must also choose and commit to agile, modern digital solutions that address this legacy influence.

No plug-and-play solution resolves all these complicated obstacles. Demonstrated expertise in navigating technical roadblocks should be sought. Doing this will position the business to incorporate the latest technology to design a system that functions with power and features that meet the business needs and customer demands.

.png?cb=286156)