A false dilemma assumes an either/or choice: You are either with me, or you are against me. This kind of thinking typifies life insurance sales, with many insurers looking to digitally transform either their adviser or their direct-to-consumer channel. But does that thinking match the reality of how policies are sold today?

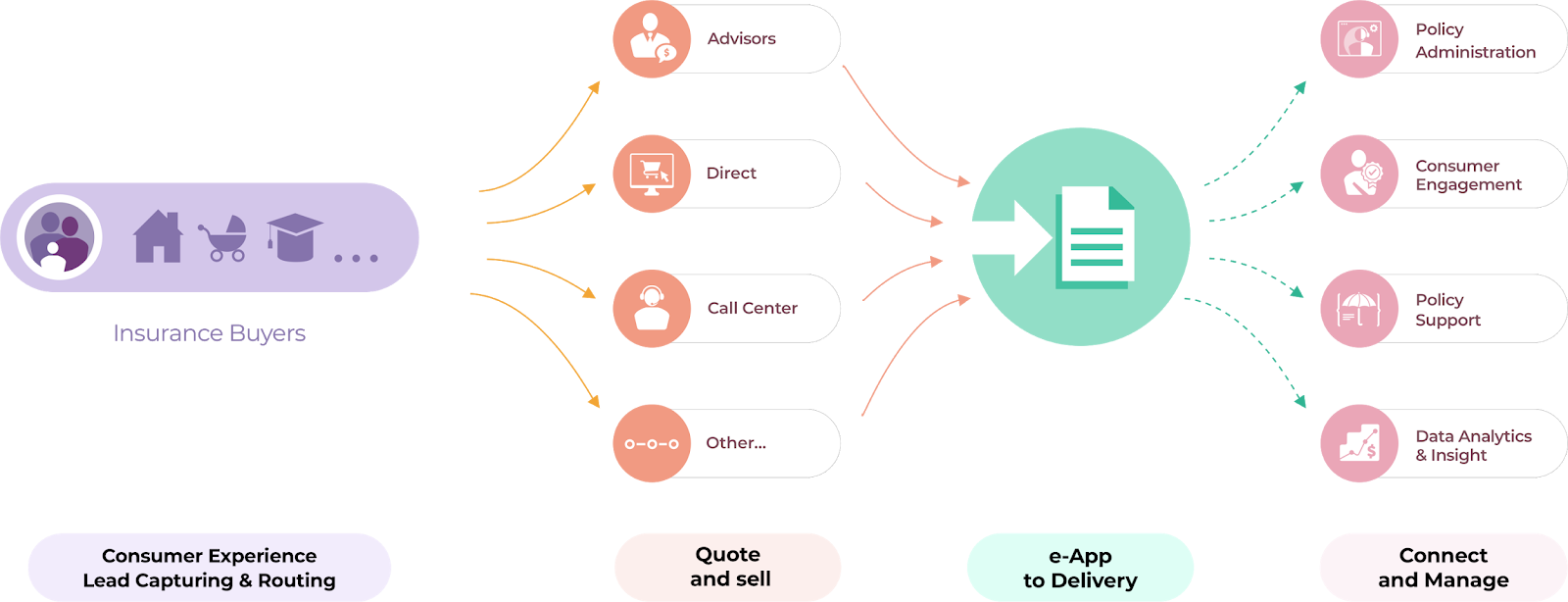

Consider the purchasing journey: research, quote comparison, application, purchase, processing, underwriting, issuance and continuing service. Some parts of the modern journey are almost entirely done online, e.g. research and quoting, while others are primarily handled by advisers, e.g. purchase and processing. Both the direct and adviser channels are engaged.

If that’s the case, can your digital transformation strategy afford to promote one sales channel at the expense of the other?

Empowering Advisers Requires Empowering Consumers (and Vice Versa)

Advisers typically sell products that are easy. So, insurers must provide the adviser a great experience via intuitive, easy-to-use digital tools for turning prospects into clients. This includes automated lead capture, data analytics for lead routing and management and a dynamic e-application. It also encompasses streamlined application processing, underwriting, approvals and payment to ensure policies are issued and claims are processed in a timely manner.

Now compare that to the traditional life insurance sales process. First, find a hot prospect and send a generic PDF quoter or application that the person needs to fill out and send back to you. Then manually confirm that all the information needed is provided and send it off to the insurance carrier. Finally, days or weeks later, the carrier approves the application or requests more information. Either way, the process is so manually cumbersome and time-consuming that it’s probably only worth the effort for really big, complex policies – i.e., expensive.

But what about everybody else? We already know that millennials, the generation of 20- to 45-year-olds our industry desperately needs to attract, has much less buying power than their Baby Boomer peers did at the same age. Can you afford to help millennials? Can you afford not to?

We know that consumers gravitate toward great experiences. It’s your job to offer them one, including dynamic, engaging and easy-to-use content on your website as prospective clients self-educate. You also must make it easy for prospective clients to ask questions and get more information from an adviser in real time, or to convert them directly when no additional help is needed. From there, consumers expect to have policies issued and claims processed in a timely manner.

See also: COVID-19 and Need for Analytical Insurers

Imagine going to the Walmart website, finding exactly the product you are looking for, then not being able to purchase it directly. Maybe you are researching products on the Walmart website and have questions, but no one is available to answer them. How long will you continue to rely on Walmart for your purchases, especially when you can buy from Amazon and receive your product the next day?

Today, you can have your cake and eat it, too, with an omnichannel approach – enabled by both people and technology -- that provides a great experience to each “user” at every point in the buying process.

Getting to Omnichannel

The key to going omnichannel is NOT blowing up your existing business model. Quite simply, it just means focusing on both processes AND experiences when you are applying technology to distribution challenges. Omnichannel must be part of your plan – really, your endgame -- even if you choose to focus on a single channel to start. Here are some ideas for how to get there:

- Start small — you don’t need to commit millions of dollars to get started. Pick a couple of products rather than digitizing the distribution of your entire portfolio. Or, start with a single process with a relatively quick time to value.

- Establish a few, reasonable key performance indicators (KPIs) — focus on quantifiables besides revenue to start, e.g. an increase in traffic, number of leads generated, number of policies sold, etc.

- Test and adjust as needed — this worked; let’s do more of it. This didn’t work; let’s not make the same mistake.

- Evaluate the experience — how does your project improve the experience for all stakeholders (present and future) who engage with it? Is there more you can do to improve?

- Add on — for example, you’ve successfully enabled D2C sales of T10 and T20 products. What’s next? Identify another product or process to tackle, establish KPIs and go for it. Do more of what works and learn as you go... just keep going.

In the past, insurance companies had to assume the full cost and risk associated with technology projects, but this is no longer the case. Subscription-based pricing and modular software platforms provide new levels of flexibility and shift the implementation risk to the technology vendors. They implement, integrate and deliver. You pay a reasonable, agreed-upon monthly fee

Don’t fall into the false dilemma trap. Life insurance, like just about everything else involving digital-native consumers, is a “both/and” world. You can do omnichannel, and frankly you have to to stay competitive. There has never been a better time to get started!

Omnichannel Life Insurance Policy Sales