Mid-market insurers today are under intense pressure to modernize. They need to build digital experiences, add AI capabilities, and upgrade legacy systems, but many are still relying on platforms built two decades ago. A recent industry report found that 74% of insurers still use outdated or legacy technology for vital processes such as underwriting, pricing, and claims.

The problem is less about the tools and more about how technology is organized and operated. Many carriers pursue three familiar paths: buy more software as a service (SaaS), hire contractors, or outsource big projects. Each may produce tactical gain, but none deliver an operating model that truly supports continuous innovation. What mid-market insurers need is a model that combines the speed of SaaS, the depth of full-time tech teams, and the accountability of managed services. That model is Technology Department-as-a-Service, or TDaasS.

Why Innovation Keeps Getting Pushed Aside

For many mid-sized carriers, the bottlenecks are technical and organizational. They may still rely on legacy policy or claims systems that cannot support rapid change. A recent survey by Gartner revealed that many insurers ranked application modernization, including replacing or upgrading legacy assets, as a top priority.

At the same time, insurers know they need AI, cloud and new digital platforms, but those need a foundation that often simply does not exist. In a survey of EU insurance undertakings, only 52% reported they already have a dedicated digital-transformation strategy in place, while 25% had none or were only developing one.

The managers and boardrooms of these firms often hear: "We need faster products" or "We need more automation." But the IT function remains focused on uptime, cost and delivery of features rather than business outcomes. Without a unified tech department that sits beside the business rather than behind it, innovation stalls.

Why Traditional Options Fall Short

Buying SaaS tools seems like a fast path to modernization. Yet every new tool still needs integration, configuration, and management. It may solve one narrow problem but it rarely changes the architecture, culture or operating model. You end up with a patchwork stack and increasing complexity.

Staff augmentation fills skills gaps. But contractors require onboarding, ramp-up time, and oversight. Once their contract ends, that knowledge often walks out the door. The organization is left with systems built by someone else, and little enduring capability.

Outsourcing large projects to system integrators is another choice. But this often shifts the burden rather than eliminates it. The vendor may build the solution, but the carrier still has to operate it and evolve it afterward. That leaves the carrier dependent, and often still without the internal structure to change rapidly.

In short, none of those models create the consistent, flexible, outcome-oriented tech team a growth-oriented insurance carrier needs.

Enter TDaasS

Technology Department-as-a-Service offers a different approach. Imagine you subscribe to a full technology department: developers, QA, UX designers, cloud engineers, security specialists, and compliance experts, all aligned with your strategy, working as your team. You don't hire them; you access them on a flexible basis. You scale up or down depending on phase, project, or business objective.

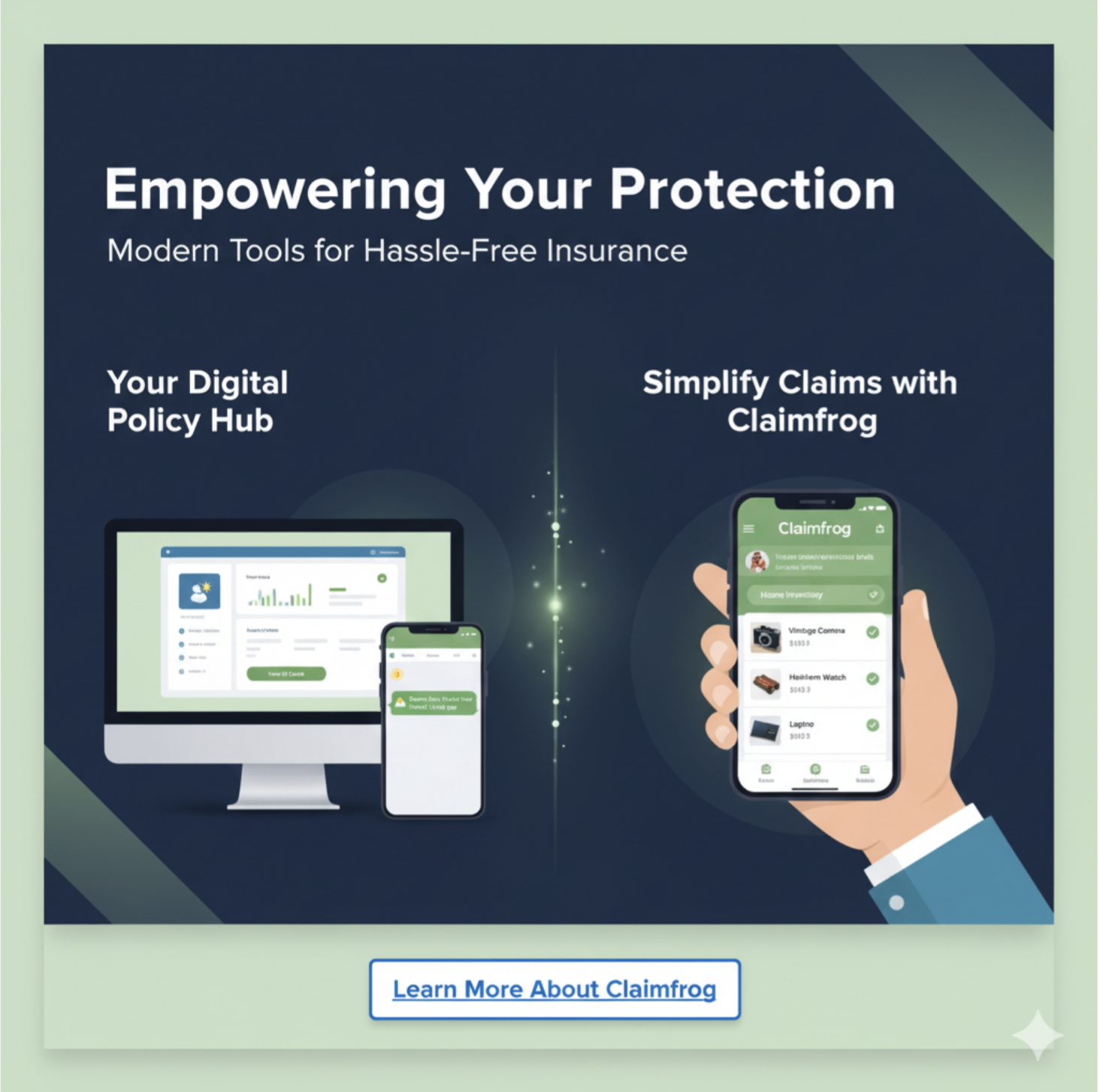

In practice, this means the carrier defines business outcomes—faster claims processing, higher customer retention, faster product launches—and the TDaasS team supports it end-to-end. They handle delivery, operations and optimization. They stay aligned with leadership rather than simply responding to tickets or vendor demands.

One regional insurer we supported had a legacy policy system and limited innovation capacity. After engaging a TDaasS model, they replatformed core applications to a cloud environment and launched an AI-driven agent portal within six months. Claims settlement improved by about 20% and IT spending dropped by roughly 15%. The tech team operated as a single entity from development to operations and compliance, accelerating value rather than fragmenting it.

Modernization Without Disruption

Replacing a legacy core is expensive, risky, and slow, and many mid-market carriers cannot afford to stop business functions while doing it. With TDaasS, you modernize in layers. You build new capabilities like microservices, APIs and front-end portals on top of your existing platform. Meanwhile, you treat the legacy core as the system of record while you gradually migrate, modernize or wrap it. Research points to this "middle-office" model for carriers unwilling or unable to perform a big-bang transformation.

Why Mid-Market Carriers Are the Ideal Fit

Large national carriers may already have big internal tech operations. Small niche insurers might rely fully on third-party stacks. Mid-market carriers live in between: complex enough to demand tailored systems, yet without the budget or scale of the largest players. TDaasS gives them enterprise-grade tech capability without enterprise overhead.

This model offers cost predictability and capacity flexibility. When you need a sprint team for a new product you scale up. When you shift to steady-state operations you scale down. You stop thinking about head-count, vendor management or internal hiring cycles. You replace that complexity with a managed function aligned with your business.

Most importantly, it alters how tech works in the enterprise. Instead of technology being a cost center measured by uptime and head-count, you start measuring it in terms of outcomes: product launch speed, customer retention, claims efficiency. That shift is what separates digital leaders from the rest.

Final Thoughts

Digital transformation in insurance is no longer optional. It is essential. Yet the path carriers adopt often determines their pace and outcome. Technology Department-as-a-Service is that model. It enables insurers to modernize their legacy platforms, integrate AI capabilities, and build digital products without being weighed down by technology debt. Over time it turns IT from a bottleneck into a growth engine. For a carrier serious about scaling innovation and doing so without paralysis, TDaasS may be the model you didn't know you needed.