The insurance industry is renowned for its ability to remain emotionally unaffected by hype and respond cautiously to it. With trading in risk as the core business, the insurance industry has evolved through several centuries, catering to the risk needs of the changing geopolitical, economic and technological landscapes. This inherent risk mindset has made the industry immune to being excited about any trigger or responding to it without a qualified assessment. However, a technology-driven startup boom in the last decade is changing the paradigm. These startups strive to gain attention by trumpeting their capabilities and offerings. For example, propositions such as on-demand, parametric and embedded insurance have been grabbing enormous column inches of insurance literature.

We are here to discuss embedded insurance. In the past, only large insurance companies and third-party brands had the privilege of partnering to sell embedded insurance policies. The simultaneous growth and adoption of several technologies has democratized the eligibility criteria and made it easier for anyone to partner, thus ushering in the new era of embedded insurance 2.0 (EI 2.0).

Now, we can seamlessly integrate granularized and tailor-made insurance coverage into the primary purchase process of a product or service, positioning it as an add-on component or an integrated feature, rather than treating it as a discretionary choice that follows a primary purchase. Embedding helps to prevent traditional decision fatigue and hesitation when purchasing insurance coverage.

Every piece of literature on EI 2.0 raves about how it is beneficial for the insurer, third parties and customers. This article aims to temper hype with words of caution, without intending to spoil the enthusiasm.

On the hype

The core concept of embedded insurance, which is to sell insurance coverage when a customer purchases a different product or service, is not new. Insurance companies have experience selling their policies through affinity relationships, trade associations and other partnerships. They sell insurance policies when a customer buys a car, mobile phone or a flight ticket or obtains a mortgage loan from their authorized partners.

However, the old process was fraught with manual handovers and friction points; it did not work as seamlessly as customers wanted.

The world is a different place now. The growth and proliferation of a constellation of technologies, such as application programming interfaces (APIs), cloud computing, infrastructure platforms, mobile wallets, security technologies and payment applications, has led to broader industry movements like open insurance. This has catalyzed the supply-side development of EI 2.0.

The demand side is empowered by the generational shift in consumer demography, changing consumption dynamics and increasing technologically savvy consumers. This near synchrony between supply and demand allowed insurers to experiment with product innovation by granularizing the coverage and innovatively integrating it within the purchase process of a third-party product or service. The outcome is the unobtrusive positioning of tailored insurance coverage at the right moment in the customer journey of the primary product or service.

There are two prominent indicators of hype in any technology or concept that can be identified with plain eyes: the mushrooming of many startups concentrating on a space in the short term, and the volumes of literature proselytizing its virtues as the best thing since sliced bread. A cursory search of EI 2.0's benefit glossary will leave both checkboxes marked in bold. The results you might get will be replete with phrases like brand expansion, convenience purchase, enhanced experience, financial inclusion, market development, new revenue stream, personalized coverage, protection gap and reduced acquisition cost. Whether you are an insurance company or a consumer thinking about experimenting with EI 2.0, you must ignore the din and exercise caution.

If you are an insurer

The earlier version of embedded insurance achieved two significant things for you: completing the sales process of already commoditized products and facilitating lead generation and early application processing for non-commoditized products that needed individual risk assessment. With EI 2.0, you could achieve much more, but it depends on how you prioritize the overall new proposition.

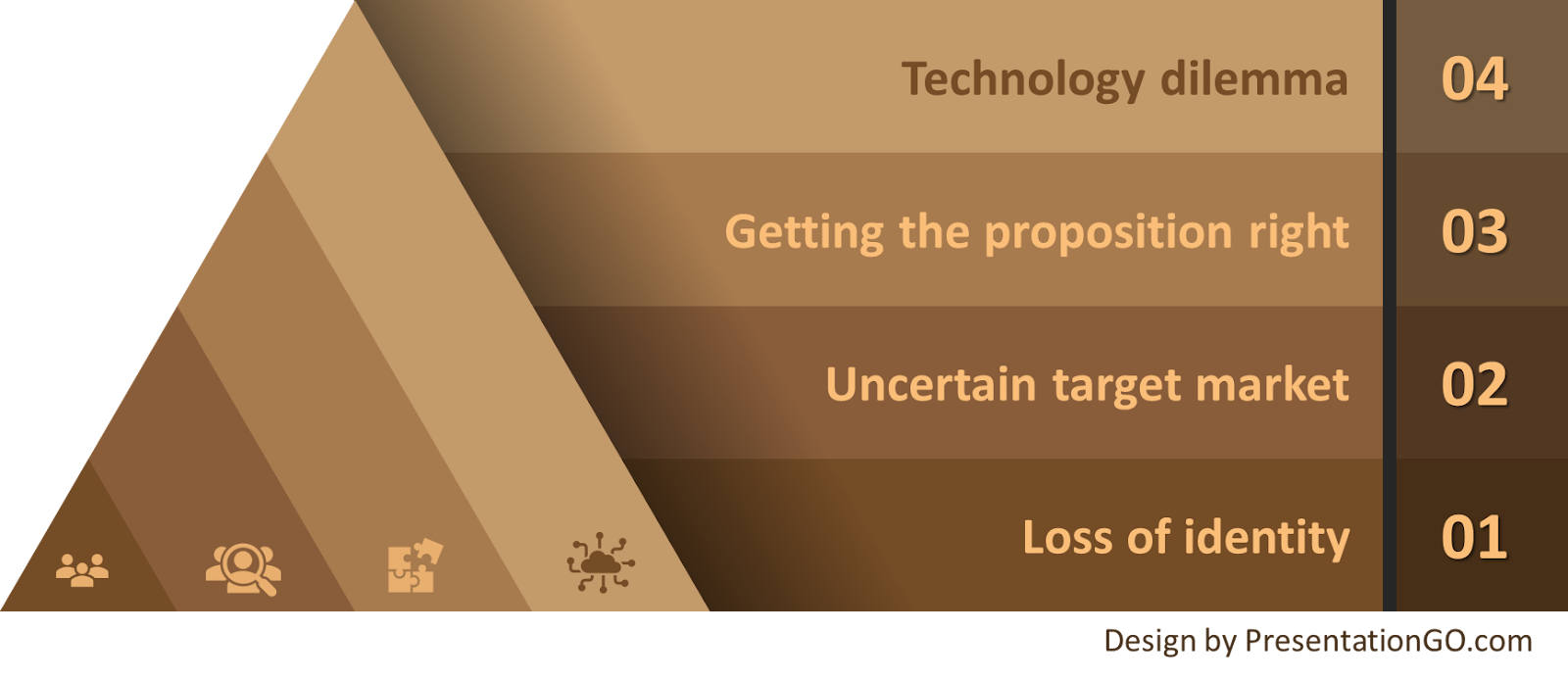

Figure 1: What you should contemplate as an insurer

See also: What's Next for Embedded Insurance?

Loss of identity

The product or service that customers buy is the primary transaction on which insurance piggybacks. The customer does the research to choose the third-party brand from various options, and the brand in turn owns the customer. You are merely leveraging the third-party brand to secure a share of their customer base. You are dependent on your partner, not the other way around. The third-party distributor holds an undeniable dominant position in this relationship and captures the maximum eye-share, mindshare and wallet-share.

It is likely that your partner may dictate the service standards you should provide to their customers. This puts you in a servile and vulnerable position, susceptible to replacement based on the partner's convenience. It is also possible that all your good work, rather than improving your brand or recall value, enriches your partner's goodwill.

EI 2.0 abstracts the insurance coverage selection as a checkbox on the screen, or worse, as an invisible or inbuilt feature of the primary product or service. If you are a startup seeking to establish a presence in the insurance industry, you may be able to adapt to this inconspicuous existence. If you are an established player, you may tolerate it when embedded insurance holds an insignificant percentage of your portfolio, or if you are using it as the tip of the spear to attract customers. On the other hand, if you want to establish a strong presence in the embedded space, indistinct positioning could result in a significant dilution of your brand and a loss of identity.

This deconstructs the insurance product beyond its commoditization and converts it into a transaction. Such "transactionalization" eliminates the buyer's decision-making process and exposes insurance purchases to third-party behavior steering.

Uncertain target market

The hype period projections for the total addressable market (TAM), serviceable addressable market (SAM) and serviceable obtainable market (SOM) for any technology or concept are exaggerated. The realistic values will always be much lower.

Digitalization, the foundation on which the premise of EI 2.0 rests, has lowered the entry barrier for participants, birthed new substitutes, changed consumer preferences and increased their bargaining power. This has led to a reduction in profits, and in a partnership where you are only a secondary player, you may find yourself with less money on the table. Furthermore, given that EI 2.0 represents contextualization, personalization and granularity in risk cover, the premium for these bite-sized products is likely to be lower.

The early technology-led startups have so far focused only on experience-driven topline growth. Operating on thin margins will deprive you of any opportunity to face adverse claim experiences. Consecutive years of underwriting losses could derail your determination to stay on track with your EI 2.0 journey.

In recent years, many new business models, such as platform-based ecosystems, collaborative consumption models, q-commerce platforms and gig-working models, have emerged. The protection requirements of these customer segments are unique. To meet their needs, you must be creative and astute in designing protection covers, even in the absence of any reliable claim experience history.

Every EI 2.0 proposition revolves around catering to the tech-savvy younger generations and tailoring risk cover to their purchase patterns, preferences and financial means. However, the younger generation faces challenges, such as income disparities, education debt, the cost-of-living crisis and lofty intergenerational inequality. This economic trend could upend your strategy of using embedded propositions to catch them young and position high-value conventional products as they grow and stabilize.

By catering to this socio-economic group, you are targeting the bottom of the pyramid, recognized for its low price and low margin. To make sustainable profits in this market, you may need your partners to sell insurance coverage in large volumes, which could be beyond their capacity. If selling insurance coverage in large volumes proves to be unfeasible, you may need to increase the margins by either increasing the rate per unit of risk or implementing the widely debated price optimization practices, the success of which is difficult to calculate.

Insurance is considered a normal good in economics, whose demand increases as consumers’ incomes rise and decreases as consumers’ incomes fall. However, it exhibits varying degrees of income elasticity depending on the type of insurance. Some products, such as health, auto and home insurance, are income-inelastic, whereas others, such as life and travel insurance, are income-elastic. Broadly speaking, when income levels increase, customers may start looking for value and may prefer fewer iterative insurance purchases. They could stop buying granular coverage pieces and opt for comprehensive coverage.

Your inconspicuous presence in the EI 2.0 partnership does not provide you with any recall value among your target customer segment: the less affluent younger generations. As these customers progress in their lives, your previous acquaintances will not be valuable if you wish to leverage them for the sale of other conventional policies.

See also: A New Approach to Embedded Insurance

Getting the proposition right

Before delving into identifying the right proposition, you need to gauge your commitment quotient. Ask yourself if your plan is merely to play with the concept of EI 2.0 for the short term, to reenact your current, manually intensive embedded insurance onboarding process in the digital landscape, or to consider it with all seriousness for the long term.

If you are serious, you must develop a well-thought-out philosophy on how you are going to pursue EI 2.0. Do you want to test with a small number of partners and products, or do you want to embark on a long-term strategy to broaden your reach across multiple partners and products? Are you going to embed products from your existing portfolio or create innovative ones that cater to the needs of each customer segment? Do you want to take the traditional rigid approach or a fluid approach for product creation?

A rigid approach is where you work with your partner to identify their requirements, create products from scratch and freeze them. A fluid approach is where you already have the coverage deconstructed, unbundled and granularized. For the launch, you can either adopt a template-based approach, which involves creating pre-configured coverage bundles designed for predefined customer segments, or you can adopt an à la carte approach, which allows partners to customize the coverage to their unique requirements, thereby reducing the design-to-deployment time.

For innovative product creation, the most important thing you need is a fresh pair of eyes to see across the spectrum of interactions that a consumer might have with a product or service to find opportunities. While developing your proposition, you need to check if, by any means, you are disrupting your current product-distribution-customer equilibrium.

Creating an innovative coverage is just one part of the success equation of EI 2.0. You should also consider other factors, such as how the cover is positioned in the purchase process, how customers are onboarded, including risk underwriting, the cost at which the coverage is offered and the smoothness of all post-sale services.

Insurance policies that are simple, pre-underwritten, meant for risks related to fortuitous losses, providing episodic or short-term covers and necessitating just a single payment of premium would follow an optimal pathway to onboarding as they could be sold as part of the primary purchase transaction itself. In contrast, if the products require individual risk underwriting, they may need to follow the traditional approach by integrating the insurance purchase process into the primary purchase journey and enticing interested consumers to reach out for completion. Given the way insurance is bundled and the limited time for completing the purchase, you should aim to ask fewer questions to assess the risk.

You must be aware that, in the past, there have been several instances where third parties and intermediaries have been involved in the mis-sale of insurance policies, driven by the urge to increase their revenue. This could lead to the suppression of material information and exacerbate information asymmetry. To prevent any such eventuality, it is essential that you exercise utmost caution while choosing your partner, designing the embedded risk coverage and implementing the risk selection process.

Traditionally, embedded insurance propositions focused only on lead generation and customer acquisition. With EI 2.0, the insurance purchase and customer acquisition processes become frictionless. As customers get used to this convenience, their logical expectation is for you to make other services, including claims, resonate at the same level of ease and comfort.

For simple monoline policies with a single trigger for insurance coverage, you may also explore designing parametric contracts for claim settlement. Parametric contracts will be well-suited for faster resolution of low-value embedded policy claims because they do not require a lot of evidence for a complicated adjudication and approval process.

Technology dilemma

You must be aware that the growth and proliferation of new technologies drive EI 2.0. However, how you respond to this fact depends on whether you are a startup or an incumbent. If you are a startup, having zero-legacy technology burden is a big advantage. In contrast, if you are an incumbent working on legacy infrastructure with disparate systems and technologies, you might be wondering how to meet EI 2.0 requirements. Will a temporary fix do the trick, or is an expensive, broad-based approach that involves modernizing your legacy baggage required?

You know well that embracing new technologies, digitalization and giving your application landscape a total makeover are no longer options that you can ignore. These have become prerequisites for engaging with your customers, whether you choose to pursue the embedded insurance road or not. However, you still need to conduct a cost-benefit analysis, considering the expenses for EI 2.0 deployments relative to your philosophy toward them. Given that most embedded contracts are small-ticket items, the revenue stream and profits are likely to be limited. Your calculations should determine whether short-term experiments can justify the cost, or if several long-term engagements are required to recover it.

To launch EI 2.0 propositions, you must invest in a policy administration system that is adaptable, robust, cloud-based and built on open standards and that supports microservices. Low-code platforms will provide you with the flexibility to quickly adapt to the changing needs of the market and configure products rapidly. It would be ideal if your policy administration system was capable of handling claims functions.

If you fail to sustain your initial enthusiasm for launching embedded insurance, your technology investments may turn into shelfware or abandoned software, thereby contributing to your growing technology debt. To avoid "sitting on the shelf," you must engage in prior soul-searching to measure your commitment quotient and conduct a realistic market assessment.

See also: Embedded Insurance Is Made for SMBs

If you are a consumer

When compared with the process friction you might have faced while purchasing conventional insurance, the ease of buying insurance through embedded arrangements could be enticing. However, you must be aware that the insurance policy sales process is historically known for mis-selling practices such as misrepresentation, non-disclosure, pressure selling, churning, unsuitable recommendations, overstating benefits and undisclosed fees.

The terms and conditions of insurance policies are full of jargon and are notorious for being difficult to understand. Currently, the technology-dominated EI 2.0 environment lacks a clear definition of the permissible types of insurance coverage unbundling and rebundling. You must consciously avoid being beguiled and clearly understand the nature of the coverage you are purchasing.

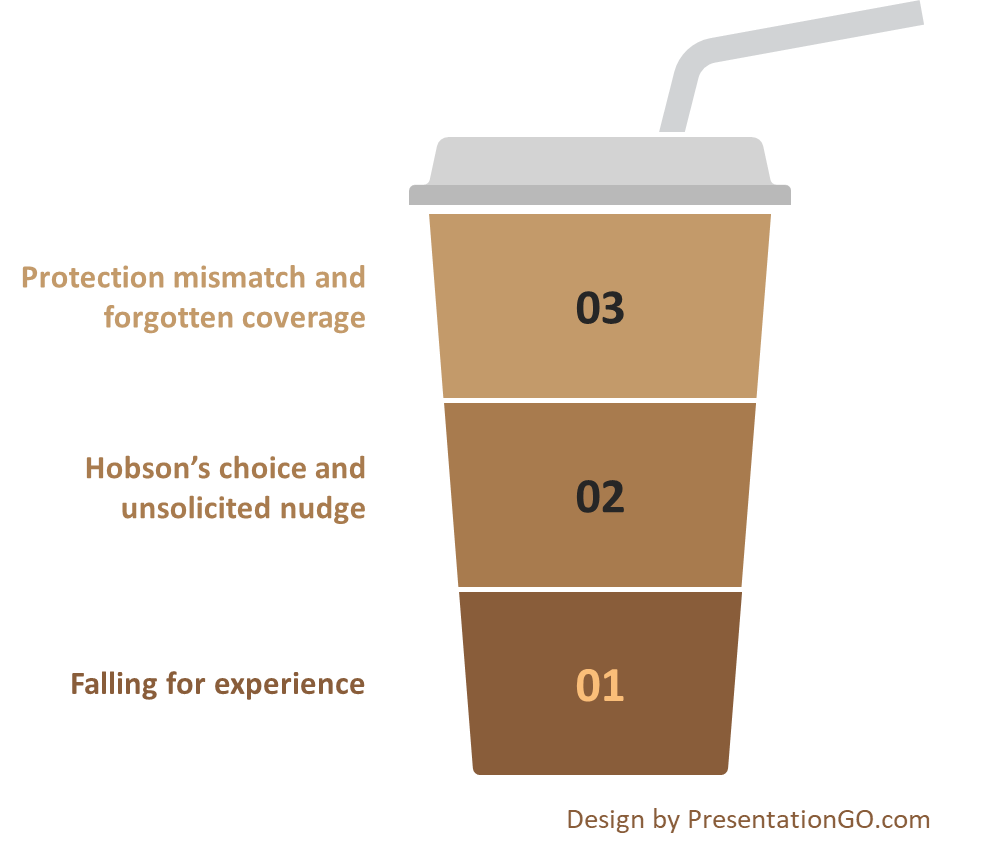

Figure 2: What you must watch out for as a consumer.

EI 2.0 revolves around you and your desire for experience. While you are immersed in the captivating purchase experience of the primary product, insurance coverage is offered to you as a "convenience-wrapped" parcel. EI 2.0 eliminates the need for you to initiate a separate process for purchasing insurance coverage after completing the primary purchase. You will benefit from the default insurance proposition of EI 2.0 if the coverage is custom-designed with the utmost care and if the default option is optimal in terms of design and cost. If trust is not maintained, you may end up paying an experience premium for coverage that you may or may not need.

Despite prioritizing experience as the most important performance measure, you must be vigilant that transparency, suitability and ethical practices are not compromised. If you go with the flow without understanding the coverage and its suitability for you, the terms and conditions may hurt you later, and you will have only your compromised rationality to blame.

Falling for experience

An embedded insurance proposition involves an inherent contractual agreement between the primary product or service provider and the insurer whose coverage is embedded. This means that when you buy the primary product, if you opt to purchase embedded coverage, you are limited to the specific insurance company providing that coverage. You do not have the choice to compare it with other products available on the market and select better coverage from a different insurer of your choice to bundle into the primary purchase. Even if you have the freedom to opt out of the embedded coverage and purchase one from the open market, it's possible that you won't find comparable custom-made coverage. This could become Hobson’s choice for you.

Ever since behavioral economics gained global attention, nudges and behavior steering have become corporate zeitgeist. When applied ethically, the principles of nudge can significantly benefit you. However, nudging can become evil if the sole intention of the insurer or third party is to manipulate you digitally into purchasing insurance coverage without assessing your actual need or suitability for the coverage. Any method that exploits your emotional state or irrationality constitutes a violation of your autonomy. Therefore, it is crucial to persistently seek full disclosure and transparency of the terms of the insurance contract.

See also: Driving Growth Via Embedded Insurance

Protection mismatch and forgotten coverage

There is one very special aspect about EI 2.0: It bundles appropriate coverage with the product or service you are purchasing, thereby informing you of any potential risks associated with it. However, you should be aware that, in most cases, EI 2.0 bundles granularized and custom-designed coverage rather than comprehensive coverage. It will compensate you only for named perils, not all perils.

Because the insurance coverage is closely bundled with the primary purchase, any conscious effort from you to purchase the insurance coverage is muted. This disengagement may lead you to mistakenly believe that you have purchased full protection when, in fact, you have not, and thus neglect to seek alternative full protection options. This false sense of security could leave you either partially covered or uncovered.

The other side of this dilemma is the possibility of being overinsured. As a consumer purchasing various products and services, you may also choose to buy embedded insurance coverage as part of the respective purchase journeys. If these different policies include extra coverage and frills, you may wind up with overlapping protection in certain areas.

Another downside of making a disengaged insurance purchase is that when a loss occurs, you may forget that you are covered for it. While this may not be problematic for short-term episodic coverage, it could pose challenges for long-term coverage if insurance companies fail to continuously engage with and inform you.

End note

The EI 2.0 story is yet to cross the chasm, inviting active participation from the early majority. The success of EI 2.0 does not depend solely on a few enthusiastic startups celebrating it; rather, it hinges on a significant number of incumbent insurance companies joining the party. Insurance giants have so far taken a measured approach. To entice them, EI 2.0 must go beyond focusing solely on product innovation and experience, and instead emphasize equitable value for all parties involved, including insurers, third parties, and consumers.

Regulations are not explicit regarding the permitted ways in which insurance, a highly regulated financial instrument, could be integrated with a less regulated product or service in a digital setting. Regulatory guidance and oversight must adapt to accommodate all potential forms that embedded insurance could take.

Despite efforts to make it appealing, at its core, insurance remains a boring business focused on numbers, and its seriousness cannot be diluted. Amid all the excitement, insurance companies and third parties must not overlook the importance of transparency to consumers regarding embedded insurance coverage and its terms and conditions.

Insurance is a contractual agreement, and no amount of innovative packaging and positioning can make it become a candy at the payment counter.