The creator economy was once seen as a new form of independence. Individuals could publish articles, videos, courses, communities, or other forms of content, build their own audiences, and turn that relationship into income and influence. They no longer had to rely entirely on publishers, media organizations, academic institutions, or large companies. They could face the market directly, build their own voice, establish trust, and create their own business model.

But that promise has changed.

Today, much of the creator economy looks less like an ecosystem that supports genuine creativity and professional expertise, and more like a content production machine driven by platforms, algorithms, and monetization mechanisms. It encourages creators to chase exposure, trigger emotion, manufacture anxiety, and convert content into traffic and income as quickly as possible. More and more content is no longer built around understanding, knowledge, judgment, aesthetics, or responsibility. It is built around clicks, engagement, conversion rates, and repeatable monetization routines.

So, when people say the creator economy is becoming a "junk economy," the statement should not be dismissed as an emotional complaint. It is a criticism of the platform economy on which the creator economy depends, especially its traffic mechanisms and monetization structure.

The creator economy is not an isolated phenomenon. It is a visible sample of a broader platform economy. It deserves attention not only because creators are being shaped by algorithms, traffic, and monetization rules, but also because this process reveals a common structure across many platform-based industries.

Whether we are looking at e-commerce, food delivery, ride-hailing, short-form video, financial services, or insurance distribution, platforms do more than provide connection. They use connection as a means to redistribute visibility, trust, and value.

This is why the issue is not that creation itself has lost value, nor that all creators are becoming low-quality producers. The deeper issue is that platforms control traffic and use distribution rules to establish evaluation standards that benefit themselves. Content, products, and services are forced to adapt to algorithmic preferences. The participants on the platform are gradually reduced to suppliers of traffic, data, or transaction opportunities.

In this structure, people with real experience, expertise, and responsibility may not be the ones most easily seen. Instead, those who are skilled at stirring emotion, amplifying anxiety, copying and pasting content, and selling shortcuts often receive greater platform rewards. The original ideal of the creator economy is then swallowed by platforms, traffic, and arbitrage.

This is not merely a moral question about whether platforms are "good" or "bad." It is a question of concentrated power, market-driven dependence, distorted business models, and long-term sustainability.

Platforms Are Rule-Makers, Not Neutral Infrastructure

When discussing platforms, a common, soft explanation is that platforms do not necessarily intend to do harm; their business models simply lead to certain negative outcomes.

But this explanation weakens platform responsibility.

Platforms are not innocent carriers of rules. They are designers, modifiers, and primary beneficiaries of those rules. They decide which content is recommended, which voices are suppressed, which formats receive traffic, and which participants are easier to monetize. Platforms use seemingly neutral language such as algorithms, customer preference, and market efficiency to package their power. But such language does not make the power neutral.

When platforms control visibility, creators no longer truly own their audiences. When platforms dominate distribution paths, content value becomes a measurable traffic resource. When platforms define monetization rules, creators' income and survival depend on the platform's decisions.

The same logic applies beyond creators. A merchant may believe it owns customer relationships, when it owns access granted by a marketplace. A service provider may believe it is competing on quality, when visibility is determined by ranking rules. A financial or insurance intermediary may believe it is managing customer relationships, when leads, timing, evaluation, and conversion tools are increasingly shaped by the platform.

Therefore, platforms do not merely control entry points. They reshape the entire relationship structure through which participants and customers meet, trust, and transact.

The key question is not whether platforms intend to do harm. The real question is this: when a platform controls the rules, profits from those rules, and refuses to take responsibility for the degradation of content quality, professional expertise, and trust that results from them, then harm is no longer just an unintended side effect. It becomes part of the structure.

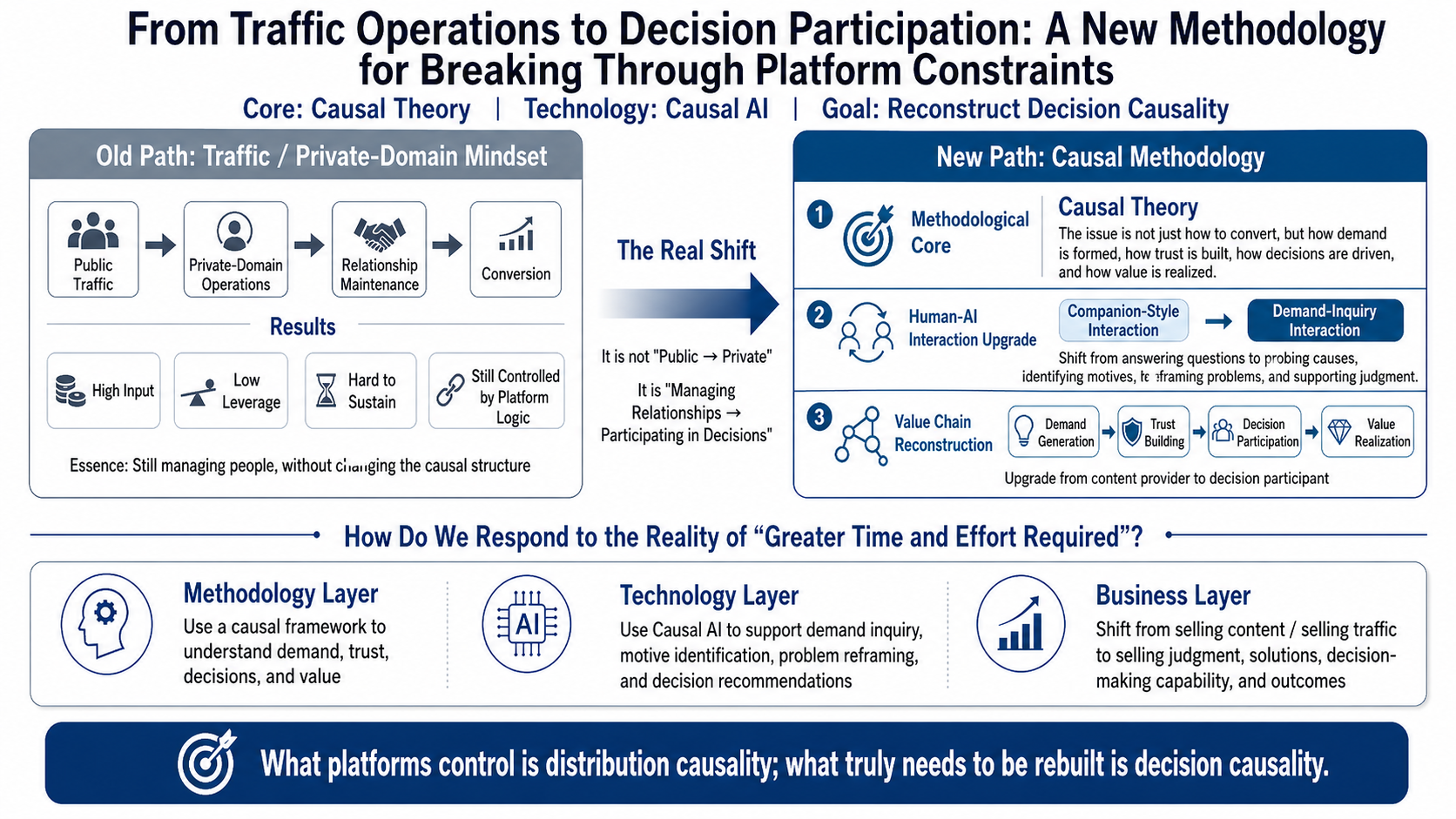

Why Moving from Public Traffic to Private Relationships Is Not Enough

A common response to platform dependence is to move from public traffic to private-domain operations. The idea is to reduce dependence on platform algorithms by building more direct relationships through communities, email lists, membership systems, subscription content, messaging tools, or other private channels.

This approach has value. But it does not fundamentally change the logic of the traffic economy.

In many cases, private-domain operations simply move people from a large traffic pool into a smaller one. On the surface, creators or companies appear to regain some direct access to users. In practice, however, the logic often remains focused on retention, activity, conversion, repurchase, and referral. The relationship structure between the participant and the customer has not been fundamentally changed.

This is one reason many private-domain strategies fail to deliver lasting results. They require long-term investment, continuous content supply, frequent interaction, manpower, funding, and management capacity. Even when they work in the short term, they often struggle to become a high-leverage, sustainable, and replicable system of value creation.

More importantly, private-domain operations are still mainly relationship maintenance. They can increase familiarity, strengthen trust, and improve conversion probability. But unless they help the company understand the customer's real needs and enter the customer's decision process when opportunities arise, they remain a low-efficiency form of relationship management.

The real shift is not from public traffic to private traffic. It is from managing relationships to understanding needs and participating in decisions.

This distinction is particularly important for insurance.

Insurance has always been a business that depends on trust, timing, context, and decision support. Yet many digital strategies still treat insurance customers as traffic to be acquired, segmented, nurtured, and converted. The problem is that buying insurance is rarely a simple transaction. It often involves family responsibility, health anxiety, risk perception, financial constraints, and a person's willingness to face uncertainty.

If insurers continue to look at customers only through the old lens of leads, conversion, product matching, and campaign response, they may miss the deeper question: why does a person decide to think about protection now, and what kind of support does that person need before making a decision?

Sometimes, the insurance industry cannot solve new problems by staying entirely inside its old mental framework. Looking at creator platforms, e-commerce, and other platform economies may help insurers see their own problem more clearly: the challenge is not only how to get more traffic, but how to enter the customer's decision moment with understanding, trust, and responsibility.

From Relationship Management to Decision Participation

There is a fundamental difference between managing relationships and participating in decisions.

Relationship management asks: how do we keep the customer, increase interaction, maintain contact, build trust, and improve conversion?

Decision participation asks a different set of questions: why does the customer have this need? What situation is the customer really facing? What problem is the customer trying to solve? Which factors are shaping judgment? What is causing hesitation? Is the customer looking for a product, or looking for a reason to make a difficult decision?

From a methodological perspective, relationship management deals with how to move along a path. Decision participation asks why the path exists, and whether it is the right one.

This means a new methodology cannot be centered only on traffic, private-domain operations, content frequency, or community activity. It must be centered on causality.

The question is no longer simply how to convert customers. The question is how customer needs and decisions arise. How is a need formed? How is trust established? How is a decision triggered? How is value realized?

The focus is not messaging or content. The focus is understanding the causal structure behind customer decisions.

A person does not buy insurance simply because they understand policy terms. They may be responding to family responsibility, health anxiety, risk imagination, or a life event. A company does not adopt AI simply because its leaders understand the technology. It may be responding to competitive pressure, management anxiety, cost reduction needs, strategic signaling, or a transformation challenge. A reader does not follow a creator simply because the content is good. The reader may be looking for a framework to understand the world, a way to judge problems, or language to clarify confusion that has not yet been expressed.

The true value, therefore, lies in the insurance adviser's insight into customer needs, the executive's understanding of organizational pain points, and the creator's ability to help readers reconstruct problems and form judgment.

What these roles share is not merely that they are good at managing relationships. It is that they can enter the process through which needs are formed and decisions are made.

That is what decision participation really means.

In this diagram, "distribution causality" refers to how platforms shape visibility and distribution rules, while "decision causality" refers to how customer needs, trust, judgment, and choices are formed.

Figure 1: The shift from traffic operations to decision participation.

From Companionship to Demand Inquiry

If the core of this new methodology is causal thinking, then the supporting technology cannot stop at generative AI in the usual sense. It must move toward causal AI.

Generative AI is powerful at producing content, organizing information, answering questions, and simulating conversation. But if it relies only on correlation-based generation, it is not enough to support true decision scenarios. In decision scenarios, the key is not only how to answer or what to answer. The key is why a need has appeared, which factors are influencing judgment, and what conditions might change the decision.

This also means the human-AI relationship must change.

In the past, AI often functioned like a companion, assistant, or customer service representative. It answered questions and provided information. Its interaction model was mainly responsive.

But in decision scenarios, AI cannot only respond. It must be able to ask follow-up questions based on causal logic. It should help people see problems they cannot yet clearly express, identify the motives behind stated needs, uncover causal factors beneath surface answers, and, when necessary, reframe the problem itself.

Companion-style interaction makes people feel heard. It is closer to emotional support and information provision.

Demand-inquiry interaction helps people better understand their own problems. It is closer to causal analysis and decision support.

This is not simply an improvement in customer experience. It is a change in role.

For AI to move from a content tool to a decision-support capability, it cannot rely on the model alone. It needs a causal methodology as an analytical framework, concrete business scenarios as sources of problems, contextual data that can support judgment, and human experts who can correct, interpret, and take responsibility for the results.

Only in such an environment can AI truly participate in need formation and decision construction.

Decision Participation Is Harder Than Relationship Management

There is an unavoidable reality: participating in decisions is harder than managing relationships.

Relationship management already requires substantial investment. Without effective automation, many participants eventually fail because they cannot sustain the required content, interaction, and service effort. Decision participation is more demanding. It requires understanding context, identifying needs, interpreting motives, reframing problems, offering recommendations, and, to some extent, taking responsibility for the consequences of advice.

This is not work that individuals or companies can sustain through enthusiasm and diligence alone.

A sustainable approach requires three supports.

The first is methodology. A causal framework is needed to rethink needs, trust, decisions, and value, rather than staying within the language of traffic, retention, conversion, and repurchase.

The second is technology. Causal AI can support demand inquiry, motive identification, problem reframing, and decision recommendations, reducing excessive dependence on individual experience and manual labor.

The third is a business model. Professional judgment must be reasonably priced. Otherwise, it will be forced back into free content for attracting traffic or low-priced services for conversion.

Only when these three supports work together can decision participation move beyond a high-cost service provided by a small number of experts and become a value creation model that more individuals and companies can adopt.

For insurance, this matters because the industry often describes itself as a trust business, but still operates many customer processes as traffic and conversion systems. If AI is used only to generate scripts, summarize conversations, or automate follow-ups, it may improve efficiency but not change the underlying relationship. The more important opportunity is to use AI to help advisers and insurers understand why a customer is hesitating, what responsibility or fear is shaping the decision, and how to support the customer's decision-making process instead of reducing the conversation to a sales script.

The Real Moat Is Decision Position

In the platform environment, content alone is no longer enough to create lasting differentiation. Opinions can be rewritten, articles summarized, videos edited, courses imitated, and even personal style learned and regenerated by AI. When the threshold and cost of content generation continue to fall, low-level homogeneous competition becomes unavoidable.

For customers, the true source of irreplaceability is not whether you can produce more content. It is whether you can enter their decision position.

This is the key for the creator economy to move beyond junk content. It is also a strategic question for e-commerce merchants, insurers, enterprise service providers, professional advisers, and AI solution companies trying to break through platform dependence.

In scenarios where transactions require long-term relationship building, if we treat content push merely as a tool to collect customer tags and build customer profiles, while ignoring the essence of customer management, we are still playing a game of "guess what you like." We are competing on statistical probability, not understanding.

The essence of customer management is to enter the customer's mind and wallet at the critical moment of decision. That does not mean manipulation. It means being present with relevant understanding when the customer actually needs help.

A platform may reduce your exposure, but it cannot easily replace your position in the customer's decision process. A platform can decide what content is distributed, but it cannot bear judgment and consequences on behalf of the customer. Even the most precise algorithmic recommendation can only infer preferences from past behavior. It cannot fully understand the customer's present context, constraints, hesitation, and responsibility. Trust, especially in insurance and financial services, cannot be created for an individual customer simply by scaling traffic.

Therefore, the answer to platform dependence is not to flee platforms. Nor is it merely to move traffic into private channels. The answer is to reposition one's value role: from traffic operations to decision participation.

Conclusion: Being Present When Customers Need Help Most

In the platform economy, what individuals and companies need to build is the ability to understand customer needs and enter the customer's decision process. The purpose is simple: to be present when customers need help most.

Platforms are powerful because they control traffic, distribution, and visibility. But the key to breaking through is not to fight platforms directly. It is to build another path of value. Instead of waiting to be distributed by platforms, companies should ask how they can become truly needed by customers. Instead of chasing exposure, they should learn how to enter the process through which customers form judgment and make choices.

When platforms control the distribution of content, products, and services, individuals and companies need to build a closed loop of capability: from need formation, trust building, problem reframing, and judgment formation to value realization. Once this chain is established, participants are no longer merely units of content, products, or services to be distributed. They become structural roles in the customer's decision process.

What we should oppose is not the platform economy itself, but the junk economy that emerges when platforms use traffic and algorithms to capture value from participants across industries. The part of the platform economy worth preserving is its ability to improve connection efficiency and reduce transaction costs. If that capability helps truly valuable people and companies become visible, understood, and trusted, then it deserves to be expanded.

What we should support is not everything that platforms amplify, but the individuals and companies that sincerely provide knowledge, experience, judgment, and responsibility. By understanding causality, reconstructing needs, and participating in decisions, they are the true creators of future value.

Individuals and companies may not be able to change platforms, and they do not need to. What they need is an upgrade in customer management: to rely less on traffic and content production, and gradually build their own loop of demand inquiry and decision influence.

For B2B service providers, this is also a reminder. Customers should stay because of value, not because of lock-in. This is not easy. But it should be a basic value principle for technology companies entering enterprise scenarios.