In the 1970s and 1980s, the issue was the liability crisis in the U.S. insurance market; today, it is strained capacity in directors and officers (D&O), cyber and business interruption. Many companies are looking at ways to retain risk to reduce their exposure to rate increases and capacity constraints in the insurance market. The silver bullet of retention is a captive: Growth in the number of captives gained momentum in 2020, with 100 new formations, and is continuing at a similar rate in 2021, according to a recent report from Marsh. Those who already operate a captive – around 7,000 are active globally – are expanding their volume or taking on new risks.

Captives come with challenges

However, not every company can or wants to act as an insurer itself. The company must be able to set aside large amounts of equity/capital as reserves. The risk manager must not only convince the CFO with a business case but also satisfy the requirements of insurance supervision as well as complex criteria for accounting and balance-sheet management. Operational risk management must also meet the highest standards for analyzing and evaluating risks. In addition, there are administrative costs for the captive to take into account.A captive is always a long-term play over various market cycles.

An innovative third way

But what if a captive is not an option for a business? In those cases, a virtual captive offers an innovative solution that combines the advantages of a classic insurance product with those of risk financing.

This solution is essentially a hybrid solution of risk transfer and self-retention. In the current market environment, companies can take on more risk themselves, getting coverage for risks that are difficult to insure or uninsurable.

Other advantages include better planning for corporate finances and full cost transparency. Unlike cell captives, which allow companies to rent a share in a captive operated by a third party, there is no connection to offshore financial centers, which can be subject to critical scrutiny.

Put simply, a virtual captive is a multi-year rolling insurance program that leaves a portion of the risks with the policyholder but reduces the results volatility from major loss events. The company pays an annual premium to provide for the risk of owning claims with a bonus-malus system. The contract is renewed for a further year if the cumulative loss ratio does not exceed an aggregated level; if it does, negotiations between the parties are required to adjust the terms, or the contract is terminated. Both the financial commitment (a single-digit-million amount) and the time commitment (usually up to five years) are kept within manageable limits.

What are the advantages of a virtual captive?

No need for equity capital

Easy establishment and expansion of self-retention capacities

Increased predictability of results due to lower or partially transferred volatility on the income statement

Cost transparency and more cost-effective than a fully fledged captive

Inclusion of tailor-made cover for difficult or uninsurable risks

Suitability for all risks; multi-line solutions also possible

A virtual captive is a useful option for those businesses that find it difficult to achieve the desired cover and capacities in the current environment. These are likely to be companies in critical, loss-prone sectors that have a very good risk management performance and are therefore confident they can take on more risks themselves. To develop and structure such a solution, and gain backing for it within the company, the risk manager needs solid technical underwriting know-how and financial acumen.

In principle, all risks that are insurable from a legal perspective can be included in a virtual captive, even D&O and cyber risks, for which capacities are scarce in the current market. Multi-line solutions are also possible.

For many insurers, traditional property and casualty (P&C) insurance products on the one hand and alternative risk transfer on the other are complementary and to the benefit of their clients. Virtual captives can offer businesses a tailor-made solution that aligns with their approach to risk management.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Grant Maxwell is global head of Alternative Risk Transfer (ART) at Allianz Global Corporate & Specialty (AGCS). The ART line of business provides structured (re)insurance solutions, including fronting solutions tailored to companies’ specific needs.

Technology is changing the way we think about the distribution of insurance — from adoption of digital technologies to integrated ecosystems and from intelligent automation to artificial intelligence. The rise of insurtechs and the acceleration of digitization have forced carriers and agents to reexamine each step of the customer journey and all interactions associated with it, whether it’s identifying prospects, delivering a quote, issuing a policy or servicing existing clients.

In the past, agents have viewed alternative distribution systems with a jaundiced eye. But agencies are finding they can coexist and thrive in a new world where technology truly complements their offering, becomes a true enabler and enhances the value they bring to the customer.

While digital transformation has occurred much faster in personal lines and is now a staple and a core offering, commercial lines carriers are starting to move in that direction, as well. As new technologies become more readily available and costs continue to decrease, all lines of insurance will benefit greatly from these new platform offerings, robust data and analytics capabilities and more sophisticated and efficient fulfillment processes.

New levels of digital dexterity

The pandemic demonstrated that our industry is capable of rising to new levels of digital dexterity. COVID-19 may end up serving as a technology tipping point for many carriers, and based on early indications many of the business models across different industries may have been transformed forever. Prior to COVID-19, how many agents used Zoom for agency interactions with customers or carriers? How many of our employees worked remotely 100% of the time? Almost overnight, we adopted new methods of customer, agent and employee engagements. Productivity and connectivity are at an all-time high. Our customers and distribution partners are much more comfortable with digital technologies and new interaction methods than ever before. The pandemic has created significant opportunities for insurers and agencies to benefit from this accelerated digital shift.

We’ve learned a lot about being nimble in a short time. As we move forward and seek new ways of using digital technologies, here are six guidelines to keep in mind:

Start at the beginning. We must always strive to know our customers, understand their needs and engage with them in the ways they choose to engage with us. We need to be able to respond to customers in the way they prefer to do business and when they want to do business. Ease of use, personalization, interactivity, connectivity and digital platform choice are some of the technology “must-haves” that we should build into the customer experience from the very beginning.

Recognize that agents are a critical part of the value chain. The need for advice, consultation and continued guidance is here to stay. At its highest level, the insurance transaction consists of two activities: value creation and fulfillment. Value creation is when you are connecting with the customer and providing consultation. The rest is gathering information, inputting it, creating a proposal, getting a quote and issuing the policy. As an industry, we spend the majority of our time on fulfillment activity. It’s time to start using data, analytics and digital technologies to flip that equation, so we can spend more time on value creation. In other words, agents should be empowered to leverage data and technology to do what they do best — build relationships with their clients.

Extend the omnichannel model to commercial lines. Until just a few years ago, few commercial insurance customers would start the buying process outside of a face-to-face meeting with an agent. Today, I’d say more than half of commercial customers begin the process online and know something about the product before they talk to an agent. Agents need to learn how to plug into these digital platforms at the right time and turn a prospect into a customer. Agencies must create a seamless bridge between channels, integrating online portals, chat and even mobile apps. Once the customer starts a journey with you, they want to be connected to all parts of the experience that follow. They don’t want a breakage or have to start over.

View insurtechs as enablers, not competitors. They no longer operate as disruptors. Insurtechs need an ecosystem to be relevant, and they have come to that realization. Most are moving toward an enabler model to create value for themselves and their partners. Agents need to understand this and figure out how to make insurtechs part of their ecosystem. Which ones do they want to partner with? Which ones offer complementary capabilities and competencies to achieve the outcomes they want?

Design systems with customers in mind, not internal efficiency. Digital transformation shouldn’t be just about cost reduction and efficiency alone. If that’s what digitization is for you, then you’re missing a huge opportunity in the marketplace. You may reduce some of your costs, but that will not translate into a sustainable, competitive advantage for your organization. To accomplish that, you need to have an outside-in view, and you need to transform your business with the customer and your distribution partners in mind — not with you in mind.

Embed intelligence into workflows. We hear a lot of talk about artificial intelligence and machine learning. Data analytics are powerful, but they become much more powerful and effective when you integrate them into your workflow. If you harness information and analyze it after the fact, you’re managing to a lagging indicator. Instead, think about how you can turn data into actionable insights and manage to the leading indicators by embedding intelligence at the point of sale or service. Rather than starting fresh at key points in the journey and chasing the same information over and over — at the time of endorsement, renewal or policy changes — use that embedded data to forge a true partnership with your customers.

In short, this is not your father’s alternative distribution system. This is a new way of thinking about the customer and adding value where it’s most beneficial and advantageous to the client. It’s using the power of embedded intelligence and digital technologies to enhance the overall customer experience and the decisions associated with it. By putting the customer first, you’ll be able to offer your clients a richer, more rewarding journey. This is how you’ll stay competitive, unlock the potential in the marketplace and grow your business into the future.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Amir Farid is chief operating officer and chief transformation officer for commercial lines at Westfield. A leading property-casualty carrier founded in 1848, Westfield provides personal insurance in 10 states, commercial insurance in 21 states and surety products in all 50 states.

News channels and insurance distribution have something in common. Both have been undergoing two decades of disruptive change. Both have had to re-examine their role in the life of the customer. Both are facing the dilemma of how to reach customers in the face of information overload. And… it may be that both are finding their way back into the customer mind through new technologies, data and analytics and a personalized touch that is fostered through digital means.

In the last two decades, we have seen a dramatic decline in the tangible newspaper. Most of us no longer walk outside to pick it up. If we read a paper, it has lost its heft. We gather our news through online sources. Of course, much of the support of newspapers – ads — has been pushed into the online realm, where, instead of three lines for $20, someone selling their car can show images, location and as many lines of text as they want for free until they sell. Craigslist and Facebook Marketplace and a thousand other sites have hastened the push of news into digital models. Though many of us pine for the glory days of the newspaper, the average reader probably feels less guilt over the paper they consume… and they don’t miss all of those pages of ads.

This is where every insurer needs to begin. We need to examine the insurer relationship to distributors in light of the customer mindset. What is changing with the customer and how they take in information? How do insurers and distributors adapt?

As customers, we don’t want ads. We want access to information on products. We don’t want to be sold insurance. We want access to the insurance products we need with tailored expertise across a wider array of channels.

Insurers need to work to use distributors to their advantage through the lens of the customer. Done properly, this means a better experience for the distributor, the insurer and the customer. Insurers need to help customers with an experience that will be enhanced by synchronized and seamless distributor/digital channels. People and businesses that interact with their agents feel more comfortable with their insurance products when they understand their insurance products. This is why the broker/agent channel isn’t in danger of disruptive demise but instead is ripe for digital development.

In Touch With Agents/In Touch With Customers

Insurers that are interested in serving customers will keep tabs on what customers are needing and what agencies need to serve them. In August 2021, Majesco asked Celent to give us a status report. What’s going on in the distributor/insurer relationship? Celent surveyed 231 agents, analyzed their responses and published them in a report, Reshaping the Distributor Insurer Relationship: A Survey of Independent Insurance Agents. Today, we are looking at one portion of that report: digital service and the balance that needs to be created for effective customer experiences. We’ll look at what the brokers/agents have to tell us and how it is affecting insurers.

The Insurer/Distributor Conundrum — Policyholder Self-Service

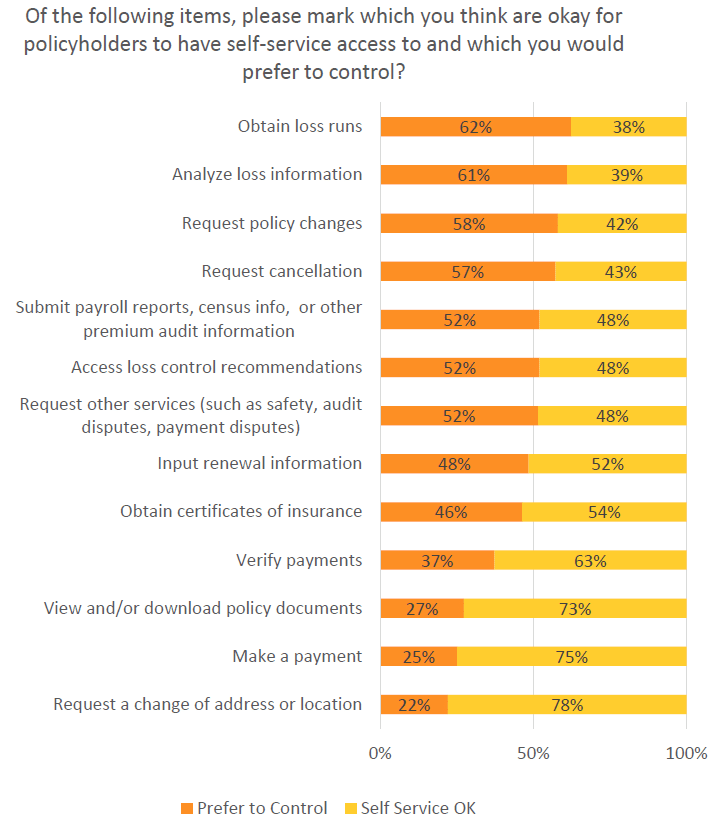

In most “retail” industries, customer digital enablement is just a matter of “give them what they want.” When it comes to insurance, however, total access can mean that the customer loses out on business wisdom when making big decisions, and the agent may lose out on customer business by not staying in touch. We were curious: Which transactions aren’t threatening to the agent/customer relationship? Which transactions release the agent from work he or she would rather not be doing? There’s a fine line. (See Fig. 1.)

“While most agents are generally okay with allowing self-service for transactions associated with maintaining an existing contract," the report found, "they would prefer to maintain control over activities associated with changing the policy or signaling a potential change (e.g., requesting loss runs). Some of their concern is around the potential for disintermediation.”

The quotes from agents reflect that they also wrestle with a desire to give customers great self-service, yet keep them from some of the stressful situations that can arise when they are allowed to make certain moves without the agent knowing. Here are examples from two agents:

“I prefer that the customer not be able to log on and make changes to their coverages without us….It puts us in an E&O spot. You get this change—where did this come from? Who requested that?”

“It’stheir information, so I don’t personally have any issues with it. I would have an issue with the loss runs. That’s a red flag that they're shopping, and we want to be ahead of that. A copy of their policy? CSR24 all the way. But notify us if there is any activity making changes.”

The Insurer Imperative — View Digital Service Through Two Lenses

As insurers decide what they need to do to facilitate business through independent agents, it might be good for them to visualize the customer and the agent at a virtual table, with the insurer present, acting on behalf of both. What does the customer want in the way of communication and self-access? What does the agent need to place the business, to maintain it and report on it, etc.? What is needed to facilitate communication between the two?

The answer to what is needed can be determined by the tools that the insurer brings to the table. There is a wide variance in capabilities. In general, agents are pleased with their primary insurers (see our blog on insurer/distributor bonding), but they are also expecting those insurers to “up their game” with relevant tech improvements across a wide range of capabilities. Celent’s data from a separate study indicated that 76% of agents agreed that they would send more business to the carriers that catered to them by improving the technologies that would make working with the insurer easier.

inThis means that insurers need to be thinking of technology improvement from both the agency and customer perspectives. How will improved processes fill agency communication and transaction gaps in ways that streamline and improve end-customer experience? Nearly all answers to this question end in the need for carrier system change.

Two Perspectives With One Shared Answer to Modernization

The only way to improve broad-level and detailed capabilities and to rewrite customer engagement processes is to design and implement a system where innovation and flexibility naturally occur in a “native” environment. Both the agent and the end-customer share the need for personalization, relationship development and data-driven policy management. This requires that carriers prepare for digitally infused automation and capabilities that move way beyond transactions. There are implications in terms of the vast differences you see currently between carriers.

The report found: “There is wide variation in insurers’ abilities to deliver on the needs of an agent. For many, only critical business processes have been automated…even many of the 'modern systems' commercially available today are not as open or flexible as needed. Even those that have updated their core systems often have legacy systems in place for distribution management. Many still use spreadsheets to manage bonuses, and many insurers only provide PDFs of production reports and commission statements.

“Contrast this with the insurers on the other end of the capability scale. These insurers are heavily automated, using predictive analytics and AI in their workflow automation. A robust integration layer allows the orchestration of third-party data and additional digital processes to become part of the delivery of customer-centric services. A high level of routine business is handled without touch… Some insurers use analytics to manage the distribution channel at a very granular level. Policy, claims and commission data has been well-organized in a logical and physical model, making it easier to utilize extremely complex segmentation and compensation programs and manage agents in a more sophisticated fashion.”

Everyone recognizes that technology isn’t an end unto itself, but that it must be supported by the processes and methodologies that match. Real innovation and advancement happens when the organization can approach both from a high level and integrate tech design and new processes. The hurdle, of course, is usually the traditional processes used by insurers. Old implementation methodologies will also stand in the way of real innovation.

Celent adds, “Old methods to create products that provide transaction efficiency, maximize features and deliver scale will not deliver digital customer experiences. Step-by-step implementations take too long and are overly rigid. Sending books of requirements to a coding factory and receiving deliverables at some time in the distant future does not allow for responsive, iterative adjustments. To move down this path, insurers need to invest in two major workstreams simultaneously—designing their future information technology architecture and shifting their implementation methods.”

The suggestion?

“Select high-value business functions and rebuild these using an API and microservice architecture approach. If you’re not able to rebuild, consider wrapping your existing technology with a digital platform as the base to create the agent experience across core transactions. Include agency management functions such as access to commission statements, production reports, marketing information, training and other capabilities to support an agent’s full set of needs.”

Many agencies are adapting as quickly as they can to digital needs, and they are making the kinds of changes that they need to make to provide digital service with a personal touch. But for them to truly grow and adapt, they need carrier partners that are willing to advance their own technology agendas in a manner that supports the agents in their efforts to touch customers and manage their businesses.

The report says: “Agents select their carrier of choice based on their alignment to key capabilities that support them in promptly selling business…. To compete and grow, insurers must enable future-ready distribution models that support multi-channel engagement; embrace platform technologies including cloud and APIs to support increased real-time integration; use advanced digital and data analytics to rethink distribution optimization; embrace ecosystems for access to data, distribution channels and digital capabilities from a growing array of partners; and implement digital experience platforms to build next-gen customer and distributor experiences.”

Is your organization ready to adapt and improve the agent and customer experience? Are you preparing for the next generation of agent-led customers who are both digitally savvy and interested in a deeper understanding of their insurance coverage?

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

The era of low – and even negative – interest rates does not seem likely to end any time soon. Banks across the globe are responding by looking for new fee-based growth pockets to partially offset the declining margins on their balance sheets. The current European insurance market accounts for roughly EUR 1,300 billion, including an estimated EUR 250 billion involving bancassurance. Growing the bancassurance business can thus generate substantial fee-based or commission-based income for banks. In a world with soaring customer expectations and exponential growth of new digital ecosystems, innovation is imperative to secure a foothold in this market.

Open APIs Provide New Opportunities for Insurance and Usher in the Next Phase of Bancassurance

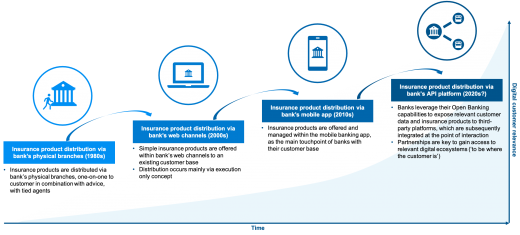

Banks have long relied on their own physical and digital channels as the main distribution point for insurance products and as the key touchpoint for engaging with their clients. Nowadays, however, insurance product offerings and insights can increasingly be found at the point of interaction within third-party channels. Digital channels have gained further importance since the outbreak of COVID-19, and this trend is expected to accelerate. Two-thirds of bank executives across the globe believe that the bank branch model will be dead within five years as a result of digitalization. Therefore, the logical step for bancassurance is to play a role within new digital ecosystems based on open application programming interfaces (APIs), thereby ushering in the next phase of the bancassurance distribution model (see Figure 1). By pursuing an open API strategy, banks can create customer relevance, leverage their presence in new digital ecosystems, drive innovation and create revenue streams.

Figure 1: Evolution of bancassurance.

Banks Are Ideally Positioned to Capitalize on This Opportunity

As part of their strategic Open Banking initiatives, banks already provide third-party platforms with access to banking products and data. Numerous banks have recognized the potential of API-enabled distribution. Some banks expose lending products via APIs to accounting platforms, for instance, enabling their users to apply for a loan directly from within the accounting platform.

The Open Banking journey has put banks in the hot seat for insurance product distribution due to a strong set of capabilities they have acquired along the way:

Banks have a large client base, relevant data assets and frequent digital client interaction. Banks have built a large customer base with frequent digital interaction and have consequently developed trusted relationships. As a result, banks possess a wide range of financial and non-financial customer data (e.g. payments data, investments, insurance policies, etc.). Banking clients are comfortable with managing their finances online, making banks a logical and trusted party to be involved in their digital journeys and transactions on third-party platforms. This large client base also makes banks an attractive partner for third parties.

Banks have a licensed, secure and regulated infrastructure. Due to their PSD2 compliance and Open Banking efforts, banks can offer licensed third-party platforms safe access to their API environment (including developer portal). This enables trusted and shared use of the bank’s products, services and data, and easy, scalable and secure integration with third-party platforms. Banks therefore have a significant head start on other parties (e.g. insurers) that are still several years away from developing this crucial capability.

Banks have well-established digital identities of their customers and authentication/authorization capabilities in place. Having established digital identity of customers is key for personalized API-driven insurance. Strong customer authentication and authorization capabilities are required to participate in open digital ecosystems to interact with others, provide access to account data and digitally engage in legal agreements such as insurance policies. Banks already have these capabilities due to their thorough know your customer (KYC) processes in combination with authentication and authorization mechanisms derived from Open Banking. This gives banks a clear competitive edge over insurance companies, insurtechs and BigTechs.

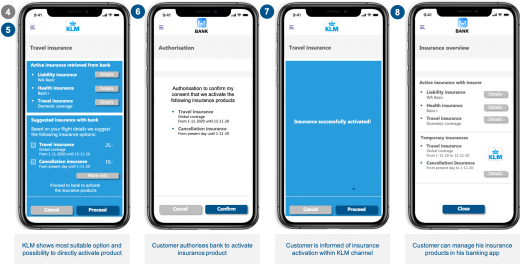

How Could It Look for the Customer?

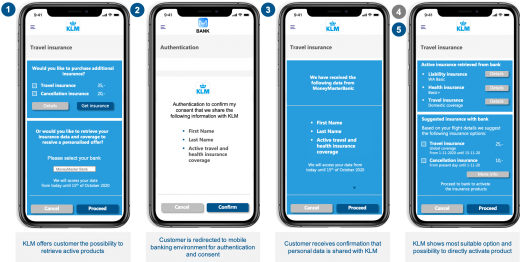

So banks have a unique opportunity to develop new open API propositions. But how can the propositions create value for customers? At INNOPAY, we regularly explain this to our clients using a bancassurance case from the travel sector (as illustrated in Figures 2 and 3). In this example from airline KLM, when booking a flight passengers can check their existing insurance coverage in real time. Based on that personalized insight, they can then decide to buy extra coverage for that trip. Once the personalized coverage is activated, clients can see and manage their coverage in the banking app. Customers thus gain an integrated and personalized digital experience tailored to their specific needs with all the necessary information in one place.

Figure 2: Use case part 1 – Client authenticates their consent for the sharing of their personal data with the airline.Figure 3: Use case part 2 – Client receives a personalized insurance offer and authorizes purchase.

According to the market insights from our Open Insurance Monitor and interviews with key industry players (banks, insurers, insurtechs), some front-running banks are already moving into this space in a bid to stay ahead of their competition. Banks that limit themselves to distribution via their current channels will see their share of wallet decline as their competitors are taking part in new digital ecosystems. Most importantly, they will miss out on the opportunity to increase the resilience of their business model and to become more relevant for their clients.

Three must-do actions for banks that want to seize this emerging opportunity within bancassurance:

Define the right strategy and business model. Banks need to define their open API strategy, business model and use cases for distributing insurance products

Engage in digital ecosystem partnerships. Banks need to engage in new partnerships to gain access to the ecosystems they want to be part of to meet new customers’ needs

Prepare the operating model. Banks need to review their current operating model and define how they can integrate key open API insurance distribution initiatives into the daily operations

Prepare for the Next Phase of Bancassurance

Digitalization is shifting insurance product distribution from the organization’s own channels to the point of interaction within open digital ecosystems. Banks that fail to position themselves at the forefront will not only see their share of wallet decrease but will also miss out on the opportunity to increase their relevance and build a more resilient business model during these uncertain times.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

It’s well-known in workers’ compensation that 20% of cases account for 80% of costs. It’s been a mystery why four out of five cases progress fairly routinely, and why that fifth one is an outlier. Struggling to find the answer, we’ve continued to do versions of the same things over and over again for these patients, without success – the very definition of frustration and insanity. If it were easy to define who the 20% of patients were, we would have done it years ago, but the problem has essentially eluded us.

As an industry, we have spent countless hours and dollars looking for extrinsic causes to the problem. Could we build a better healthcare delivery network? Perhaps we need to change our drug formulary. Maybe the problem lay with the individual adjusters approving or denying care. All of these are viable and appropriate question, but they place the locus of control for the problem on the world around the patient. I submit that the reason 20% of patients struggle and fail with recovery is purely an intrinsic problem and the solution to the problem is easily fixable once it is identified.

The Real Reason Why That 20% Languishes

The core problem is twofold: Patients do not respond the same way to treatment, and they experience trauma and suffering in very different ways.

A one-size-fits-all approach simply does not work for everyone, because their symptoms and suffering are different.

The nature of an injury is not just a broken bone or a laceration. While the physical manifestation of trauma is easy to see and treat, trauma expresses itself in emotional ways, as well. So far, our approach to treating injured workers has been primarily biologic – and pharmaceutical. Only recently have we begun to identify the ramifications of mental and emotional health on an injured worker’s recovery and ability to return to work.

These emotional wounds and physical suffering express themselves differently in different individuals. We need to recognize these variations and develop customized and innovative ways to treat them on an individual level that are cost-effective and long-lasting and can provide patients with a truly positive experience.

Why Are the Psychosocial Factors So Powerful?

In 1997, George Engle introduced the bio-psycho-social construct for understanding the human condition as it relates to medical conditions. By identifying the fact that humans are much more complex than biologic creatures, he opened the door to detecting the underlying reasons why some people persevere in the face of grave illness or injury while others languish. To address this interplay, it is critical to understand two constructs.

First, there is a direct relationship in the brain among pain, trauma, depression and anxiety. They are inextricably tied through the neural pathways of the brain. When someone suffers from one of these issues, the others are directly correlated. In physics terms, for every action there is an equal and opposite reaction, and those reactions are not always positive.

Second, a work-related injury is a life-changing event. Consider what the patient is facing:

Anxiety about continuing in their job and being able to support themselves and their family.

A loss of sense of self – will I ever be the same again?

A loss of identity – our jobs, our professions, our roles in the family and the community are representations of who we are. With an injury, those identities may permanently change.

Fear of the unknown – success in treatment is not guaranteed to restore full function.

Time to ruminate and worry during the recovery process.

A loss of control for their own healthcare – patients are reliant on their adjuster and payer to grant access to care for their problem.

If you consider the biologic connectedness of trauma and mental health and then factor in the emotional impact of a workplace injury, it’s no wonder that anxiety, depression and other mental health problems are present in most cases that drive volatile claims cost and poor patient outcomes.

When the injured worker is in pain, as most are, the recovery is longer, discomfort persists on a daily basis and emotional problems are exacerbated. Sleep is interrupted, delaying the healing process and increasing anxiety and depression. This downward spiral is clinically referred to as the fear-avoidance cycle, and it continues, often ending in permanent disability and addiction, because patients, and oftentimes medical providers, do not know how to break this vicious cycle.

As noted, pharmacology has been the traditional answer for both pain and emotional/mental health issues. These medications were the only resource available to us clinicians, so they became the proverbial “hammer” and everyone we treated became the “nail.” We’ve seen what long-term reliance on painkillers can cost in terms of addiction, more suffering and even death. A pharmacological solution alone doesn’t work. Not only does it fail to resolve the source of the pain, but it also fails to treat the array of psychosocial symptoms that are related to pain. If anything, narcotics and pharmacology have the potential to make these problems worse.

Science Leads to a Solution

Fortunately, recent breakthroughs in technology, science and clinical care offer alternatives to effectively treat the 20% of outliers that have long stymied us for their lack of response to the current biologic treatment paradigm. The innovation is understanding that the brain has the ability to promote neuroplastic change when given the appropriate clinical cues for the right frequency and duration. This neuroplastic change promotes a biologic re-wiring of the brain to create permanent resiliency to the symptoms related to the traumatic event. It is imperative that the biologic changes be coupled with social and psychologic training and education to provide an individualized level of support for the patient. The ability for a clinician to use a single therapeutic modality to address all three of these humanistic pillars is unparalleled.

This disruptive approach consists of four components:

Virtual reality technology: This technology is used to immerse the patient and to distract from the maladaptive sensations. The brain’s ability to create new pathways (neuroplastic change) reprioritizes these signals to create resiliency in the patient. Using the immersive technology, patients report an immediate decrease in their symptoms as well as a residual, or legacy, effect. This equates to acute relief from their symptomology with continuing relief even when they have removed the VR platform. Previously, similar results could only be accomplished with prescription drugs. The results using VR are obtained in a purely non-pharmacologic and safe manner. In addition to the reduction in symptoms (pain, depression, anxiety or PTSD), patients are also reporting a dramatic increase in the quality and quantity of sleep, which is essential to healing following any traumatic event – physical or emotional.

Individualized behavioral counseling and coaching: The coupling of masters-level behavioral health specialists to coach and guide the patient through the virtual reality platform allows for an extremely customized and individual therapeutic experience. These weekly encounters help maximize the protocols within the virtual world as well as drive engagement and behavioral change skills in the real world. The coaches have been charged with helping traumatized patients return to their version of normalcy in their lives or helping them identify and adapt to a new version of normal as they move forward.

An exceptional patient experience: Digital engagement in a virtual setting means that patients don’t need to leave home to engage in therapy. Patients receive direction as to when and how to use their platform from their personal coach, and then it’s available any time of the day or night. When a person is injured at work. there is a loss of control in their life, as their daily routine is interrupted. With this unique therapy, traumatized workers have complete control of one aspect of their healthcare—this is an extraordinarily powerful tool that helps engage these patients and gives them some ownership in the treatment plan.

A time limit: The 90-day duration of treatment is designed to promote the necessary neuroplastic change, coupled with behavioral change and goal-setting education. The goal for any therapy should be to create change in a timely manner. Furthermore, a true biopsychosocial program needs to drive the patient toward a graduation event—accomplishing a series of goals promotes positive behavioral change.

Through this combination of virtual reality technology and customized behavioral counseling, we now have a solution to effectively bring relief to injured workers in a holistic and patient-centric manner. The goal is to be synergistic and complementary to other therapeutic modalities, while promoting a safer and more efficacious treatment pathway. Simply put, this treatment modality delivers on the notion of the triple AIM – better patient outcomes, lower financial burden, and exceptional patient experiences.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Medicare Secondary Payer (MSP) compliance is changing. The rapid evolution of technologies is making it possible to automate portions of the process that were previously beyond reach, empowering claims professionals and those responsible for the creation of Medicare Set-Asides (MSAs), conditional payment resolution and Section 111 reporting with new tools that increase their efficiency and vastly improve accuracy.

The stakes are higher, as well. We have seen a marked shift in policy in recent years, as the Centers for Medicare and Medicaid Services (CMS) has increased its focus on cost recovery. This has manifested itself most noticeably in the form of new MSP compliance policies and increased enforcement measures. Starting Jan. 1, responsible reporting entities (RREs) could face penalties of up to $1,000 per claim, per day, for failure to properly comply with Section 111 reporting requirements.

In addition, CMS has increased coordination between Section 111 reporting and cost-recovery programs, which will permit greater scrutiny and empower the agency to implement these increased enforcement measures. Conditional payment debt recovery measures can now be categorized as aggressive, with swift referral of unresolved debt to the U.S. Department of Treasury.

At the same time that MSP compliance is growing more stringent, though, insurers are benefiting from improvements in technology that are driving costs down, increasing accuracy and accelerating the reporting process through automation. Old-school methods are losing viability, especially in light of technology innovations that have arrived on the scene in recent years.

MSP Compliance the Old-School Way

To better understand how technology is changing the game, let’s look at how things have been done in the past. Traditional MSP vendors have been tasked with examining a patient’s medical records to identify the types and effectiveness of medical treatment rendered, recommending physicians for future care, scrutinizing Medicare coverage determinations, reviewing claim payment histories, consulting workers’ compensation fee schedules and researching Redbook average wholesale price (AWP) pharmacy costs, all in the name of MSA preparation. The tedious, painstaking and manual effort involved in creating an MSA involves the use of highly trained and specialized medical and, oftentimes, legal personnel.

All of the efforts of your MSP compliance vendor don’t merely drive up the vendor’s cost; it can drive internal costs higher, as well. CMS Workers’ Compensation Review Center (WCRC) policies require a 24-month lookback at active treatment records relative to a single date or multiple dates of loss, so claims adjusters or their support staff must typically pull a select subset of patient and payment records to fulfill the current MSP compliance requirements. The amount of documentation to be retrieved by the client and reviewed by the MSP compliance vendor can be voluminous in many cases, driving costs up even further.

Many MSP compliance vendors still rely on insurers to manually supply other important information, as well, including demographic data, the First Report of Injury form, covered and denied body parts, a pharmacy benefit management summary (PBM), pertinent legal documentation and more, depending on case specifics. Some of that information may require authorization to speak with a third-party vendor, which can complicate matters even further. All of this takes time, which in turn drives costs.

There is a time delay associated with this manual methodology, as well. In most cases, reports can be produced in a matter of a week to 10 days, but in some cases they may require several weeks, depending on their complexity, the volume of documentation involved and the capacity of the vendor. If the MSA is needed in a hurry, most MSP compliance vendors will impose an additional charge to expedite the process. Those rush fees can add up quickly, even doubling the total cost of producing a single report.

Given the sheer volume of information that might need to be reviewed to create an MSA, it’s no surprise that errors occur. Strong quality assurance (QA) programs ensure the accuracy of the reports before delivery to the client, but, again, QA efforts, although necessary, can increase costs and delay report delivery times.

AI Is Changing the Game for MSP Compliance

One of the key challenges associated with medical claims, generally speaking, is the abundance of unstructured and semi-structured data that might be involved. This is precisely why MSP compliance has been such a high-skill, labor-intensive process. But today, artificial intelligence and machine learning (AI/ML) have advanced to the point at which they can accurately ingest the kind of information that previously required extensive human involvement.

Today, we can read various types of documents and can use AI and machine learning to derive meaning from them. Natural language processing (NLP) can discern the subtle, but extraordinarily important, differences between phrases such as “patient reports no back pain” and “pt rpts no prior hx of back pain.” While claims and MSP compliance professionals still have an important role to play, AI gives them a distinct head start in the process, first by filtering out the right information, then by ingesting it, making sense of it and highlighting key attributes of the cases that require attention.

When claims adjusters are relieved of the problem of preparing information for an MSP compliance vendor, they can instead focus on their core responsibilities. AI can ingest everything, automatically filtering out what it needs for a particular report. AI now automates tasks that were once thought to fall outside the realm of automation.

This level of automation also makes it possible to easily develop multiple versions of an MSA report quickly, enabling adjusters and managers to assess the risk levels associated with various claims' scenarios and potential outcomes. This, in turn, gives insurers greater control over claim decisions while helping them to remain fully compliant with CMS policies and regulations.

For MSP compliance, in particular, AI applications can improve the process even further by incorporating CMS feedback into decision-making algorithms. In other words, AI/ML can learn which elements of a report rendered development requests and counter-higher approvals from Medicare’s WCRC, and AI/ML can incorporate feedback and tailor future reports to more closely conform to CMS expectations.

Lower Costs, Increased Accuracy and Efficiency

AI technology is no longer just a visionary idea; AI has arrived, and it’s transforming the way insurers do business. Innovative insurance companies are already reaping the benefits of this technology. Tom Veale, president of TRISTAR Risk Management, reports that his company has saved over 33% on compliance costs after adopting a purpose-built AI approach designed to handle MSP reporting, risk analysis and compliance.

AI and machine learning will continue to gain momentum. In the short term, that will provide competitive advantage to early adopters (as is already happening at TRISTAR and other organizations). As adoption increases, the old ways of managing MSP compliance will be rendered increasingly obsolete. CMS policies and enforcement measures will only serve to accelerate that trend.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Christine Melancon, director of regulatory compliance at CLARA Analytics, has spent her entire career working in the healthcare industry, emerging as a true leader, particularly in the areas of Medicare Secondary Payer (MSP) compliance and Medicare Set-Asides (MSAs).

This week, Paul Carroll explores the great unbundling. Plus, navigating the future of risk management; when captive agents go independent; the importance of explainable AI; and more.

General Electric’s announcement last week that it is splitting into three parts not only marks the final stage in the unbundling of the world’s most successful conglomerate but underscores a theme we’ve been sounding at ITL for years now: that the future belongs to ecosystems.

The GE announcement — and one by Johnson & Johnson, also last week, that it is splitting into two pieces — largely relates to stock market issues. GE felt that investors weren’t fully understanding a three-headed business — which manufactures equipment for healthcare, power generation and aviation — and thought the aggregate valuation of the businesses would fare better if each had its own, clean story to tell. J&J made a similar calculation when it decided to split its volatile prescription drug business from the steady-as-she-goes consumer business that sells Band-Aids and Tylenol.

But the splits also reflect that the need for specialized expertise in a business, whether that’s jet engines or over-the-counter medicines, increasingly overwhelms whatever benefits come from combining a variety of businesses in a single corporate structure — and that digital connections make it ever-easier to gain any benefits via collaboration without being under the same corporate roof.

When I was a young pup of a reporter at the Wall Street Journal, an old hand told me, “If you have a good story, you should write it every once in a while.” In that spirit, I’d like to resurface some of the many articles we’ve published on how the unbundling of businesses and capabilities can play out in insurance, benefiting businesses and customers alike.

Join Majesco’s Denise Garth for a discussion with Managing Director, Ajay Radhakrishnan and Senior Manager, Ahmed Abdul-Wali from Deloitte Consulting on the importance of taking a customer first approach and upgrading the next-gen core billing.

Even as insurers focus on innovation and the technology that will enable it, they still must maintain and operate the legacy systems that run the business.

Beam Dental, an innovative insurtech business, was growing. With the help of JobsOhio, Beam Dental moved to Ohio and found the perfect market for a growing startup.

In all my years covering all manner of technology, telematics may have caught me off-guard the most. When I first wrote about Progressive’s auto telematics program, Snapshot, in 1998, it seemed like a slam dunk. Of course, it made sense to monitor how people drove and to price their insurance accordingly.

Join Paul Carroll, editor-in-chief of Insurance Thought Leadership, as he sits down with speakers from the event to take a closer look at critical topics. Over this six-part series, hear from industry leaders about bridging the protection gap through innovation, leveraging data for success, and more.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Typically, about 80% of small businesses in Canada will survive the first three years, but only half of the 100,000 new businesses that open their doors annually will still be around eight years later.

Consider the following statistics:

Canadian businesses lost $30.4 million to fraud in 2017.

29% of cyber breach victims in 2019 were medium-sized businesses, while 18% were small businesses.

Almost one-third of small businesses fear they won’t survive 2021.

No matter their age, many organizations will struggle to survive this year. Whether an organization remains afloat or not depends on how resilient they are and how capable they are to prepare for, respond to and adapt to disruptive events.

In this pursuit, an organization needs to leverage all of the financial, technical and human resources at its disposal. It will need to develop skills and competencies in an efficient, flexible manner to manage the risks and challenges it faces.

While there is no single strategy or solution to make an organization resilient, an organization can enhance its resilience by:

Strengthening individual management disciplines of the organization that manage risk and doing so in an integrated and coordinated manner.

Building a culture that ensures the organization behaves in a healthy manner.

Increasing its adaptive capacity and ability to manage change.

The resilient company or organization uses its financial, technical and social resources to:

Develop long-term skills and competencies

Deploy resources in an efficient, reliable and flexible manner

Strong risk management practices are an important aspect of resilience. Though risk management can be challenging, the importance of building a solid foundation and program to protect your people, property and profitability is vital. Enterprise security risk management (ESRM) is a strategic, all-hazards approach that provides a framework to identify, evaluate and mitigate threats to an organization's resilience.

Emergency Action Planning: Emergency action plans are intended to protect people and property and prevent further harm during an emergency. As defined by OSHA, an EAP facilitates and organizes employer and employee actions during workplace emergencies. When there are well-developed emergency plans and employees are trained properly, there are fewer and less severe injuries and less structural damage to property. Conversely, poorly designed plans and poor training leads to disorganized evacuation and emergency response, which could lead to avoidable injuries and property damage.

Crisis Risk Management: When a crisis hits, a resilient organization will bounce back or even pivot, if necessary. Crisis risk management includes an organization’s ability to coordinate an effective response to protect people, operations, profitability and reputation. Planning may require gathering resources for outside support and partnerships to manage the issues, as well as a careful consideration of the vulnerabilities inside the organization.

Business Continuity: Business continuity plans help keep a resilient organization operational. Key to this are processes that ensure critical activities keep going during a crisis. A formal written plan notifies team members of their responsibilities and allows them to take charge when the time comes, especially if they have already practiced those tasks during drills and exercises.

Fraud Risk Management: Theft and fraud are two of the most complex risks to your organization. Indeed, they can be so costly that they threaten even the most resilient organizations. While external and insider threats are posing new and heightened risks, regulations and public scrutiny are demanding greater responsibility. Now, more than ever, organizations are looking for ways to manage the risk of fraud, especially within the ESRM context and in a way that takes industry-specific considerations into account.

Cyber Security:Developing a resilient organization means taking into account even newer and ever-evolving risks like cyber security. In fact, cyber security may be one of the least understood areas of the risk picture. Adequately managing cyber risk does not require all participants and stakeholders to be technical subject matter experts. However, it does require comprehensive awareness of cyber risk issues and strategic and appropriate mitigation efforts, especially vendor risk management and privacy laws.

Risk management can be daunting for those at the very beginning, but planning and preparing for all areas of risk is vital to an organization’s survival today.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Ray Monteith is a senior vice president with HUB International's risk services division. He leads the organizational resilience practice for the division and is the risk control services leader for the Canadian region.

GE's announcement that it is splitting into three parts underscores a theme we've been sounding at ITL for years now: that the future belongs to ecosystems.

General Electric's announcement last week that it is splitting into three parts not only marks the final stage in the unbundling of the world's most successful conglomerate but underscores a theme we've been sounding at ITL for years now: that the future belongs to ecosystems.

The GE announcement -- and one by Johnson & Johnson, also last week, that it is splitting into two pieces -- largely relates to stock market issues. GE felt that investors weren't fully understanding a three-headed business -- which manufactures equipment for healthcare, power generation and aviation -- and thought the aggregate valuation of the businesses would fare better if each had its own, clean story to tell. J&J made a similar calculation when it decided to split its volatile prescription drug business from the steady-as-she-goes consumer business that sells Band-Aids and Tylenol.

But the splits also reflect that the need for specialized expertise in a business, whether that's jet engines or over-the-counter medicines, increasingly overwhelms whatever benefits come from combining a variety of businesses in a single corporate structure -- and that digital connections make it ever-easier to gain any benefits via collaboration without being under the same corporate roof.

When I was a young pup of a reporter at the Wall Street Journal, an old hand told me, "If you have a good story, you should write it every once in a while." In that spirit, I'd like to resurface some of the many articles we've published on how the unbundling of businesses and capabilities can play out in insurance, benefiting businesses and customers alike.

In "Insurance Ecosystems: Opportunity Knocks," Marie Carr argues that, "rather than taking several years to fulfill digitization road maps, insurers will find that participating in a connected supply and demand service model offers something better, faster and cheaper.... Now that the building blocks are in place, industry leaders are increasingly engaging in ecosystems that serve broad consumer needs, often where insurance is only one offering among many. Strategic options are multiplying."

Carr then lays out four strategic considerations that can help insurers identify the right ecosystems to participate in and the right ways to participate.

In "The Intersection of IoT and Ecosystems," Matteo Carbone says, "Traditional, end-to-end business models are breaking down in every industry, including insurance. In the digital era, it is increasingly difficult for any single firm to deliver the seamless experience that customers expect. More insurers are leveraging digital ecosystems to reinvent their products and services, providing better risk management, reduced claim cost and new sources of revenue."

Carbone then describes how digital technology, especially through the Internet of Things, can be used to create a platform for coordination among numerous companies.

In "Power of Partner Ecosystems," Denise Garth focuses on distribution, where she says an "ecosystem can rapidly reach more markets, potential customers and current customers with more purchase and service options by tapping into a growing array of channels beyond the traditional agent/broker channel.... [including] direct-to-customer, other insurers (for products you want to offer your customers), marketplace exchange or platform and embedded."

Garth adds that "distribution ecosystems provide new access avenues, capabilities and services" and provides a formidable list of partnerships that involve insurers and that illustrate her point.

In "Big Opportunities in Insurance Ecosystems," Stephen Applebaum offers an example of an insurance ecosystem that dates back "to 1980, when information providers built platforms linking auto insurers to collision repair facilities to streamline the repair process. These ecosystems quickly expanded to include independent appraisers and adjusters, auto glass and car rental vendors, salvage pool and towing operators, parts providers and others. Today the ecosystems are beginning to include telematics service providers and auto manufacturers and dealers."

He adds that "new property claims ecosystems are emerging to include a full suite of contractors, inspection technology, digital payments and other service providers, enabling insurers to resolve claims in hours instead of days or weeks."

In "The Word of the Year Is... 'Ecosystems,'" I took my own shot at the topic in early January of this year. Like some of the others I cited, I noted the potential for expanding the reach of sales efforts through partnerships. I also looked at "a second opportunity for ecosystems that is even more fundamental, because it allows for rethinking the whole organizing principle of major parts of a business and, eventually, the entire business.

"Historically, big insurers have been closed systems. They have their sales force, their underwriting teams, their actuaries, their claims organization, etc., all down the line, all operating within one set of walls. But what if an organization were more like a piece of software and could be organized as an open ecosystem, so the organization didn’t have to do everything itself and could incorporate a continual stream of innovations, whether from inside or outside the organization?"

Thinking of an organization as an ecosystem of businesses and capabilities would really lead to an unbundling of work.

Ronald Coase, who won the Nobel Prize in Economics for formulating the idea of transaction costs and whom I had the pleasure of interviewing once, came up with the notion because he was trying to figure out why businesses did certain things within their walls and contracted with others to do other things. He decided that the key was a measure of efficiency.

If a business wanted some legal work done, for instance, it could hire an outside attorney every time and avoid the fixed costs of having a legal staff. But then each bit of work would be a separate transaction and would carry costs -- and not just the costs of negotiating a deal. Transaction costs would include the time involved, the higher per-hour rate an outsider would charge, the uncertainty about the quality of the attorney if a business hadn't worked with the person before, etc. So, Coase theorized, businesses would hire staff attorneys and bring other work inside, to the point where those internal costs matched the cost of using external resources, including the transaction costs.

Although Coase was in his late 80s when I sat down with him (he lived to almost 103), he was as intrigued as anyone by the possibilities of the internet in the latter half of the 1990s. He thought it could drastically lower the transaction costs of doing business with other people and enterprises and thus shift work from inside corporate walls to outside them through the sorts of digital-based partnerships and ecosystems we're now, in fact, seeing.

He even put a number on how much he thought transaction costs could be cut. Figuring that about 20% of the U.S. economy was transaction costs, he speculated that the internet/digitization could take out some $4 trillion of cost per year.

But he also left me with a thought: One person's cost is another person's revenue. In other words, he warned, there would be plenty of rear guard actions to prevent costs from being eliminated.

So, I'm not saying that moving to ecosystems will be free and easy. Lots of people and companies have vested interests in the status quo. But if even the legendary GE has succumbed to the forces that have been undercutting the rationale for conglomerates, then I'm confident that resistance to ecosystems will steadily erode, too.

Cheers,

Paul

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

In this webinar, ITL Editor-in-Chief Paul Carroll interviews Anne Plese, Senior Director of Product Marketing at Rimini Street, and James Maudslay, global director of insurance at Equinix on how operational efficiency can create the room for innovation.

Even as insurers focus on innovation and the technology that will enable it, they still must maintain and operate the legacy systems that run the business. What if it’s possible to spend less time and money on those systems, freeing resources to focus on developing systems that will really move the needle for the business?

In this webinar, ITL Editor-in-Chief Paul Carroll interviews Anne Plese, Senior Director of Product Marketing at Rimini Street, and James Maudslay, global director of insurance at Equinix on how operational efficiency can create the room for innovation.

They cover:

--How outsourcing service can return massive amounts of dollars of working capital to insurers.

--How to address the skills gap as those who coded the core systems decades ago retire and are being replaced by people who aren’t even trained in the computer languages that were used.

--How to cost-effectively maintain the tens of millions of lines of custom code that aren’t covered under mainstream maintenance contracts with Oracle, SAP and the other big technology vendors.

Marketing leader and technology evangelist with 20 years of experience in product marketing and management. Powerful blend of business, leadership, technical, and communication skills. Experienced in Private Cloud, Hybrid Cloud, IoT, IaaS, PaaS, SaaS, Networking, Open Source, and Big Data. Deep background in defining customer requirements and influencing buying criteria of enterprise, mid-market, and service provider segments.

James Maudslay

Global Head, Insurance, Equinix

Joining Equinix in September 2012, James took on the subject matter expert role of the insurance vertical as part of the UK Financial Services team, enlarging that role globally in 2014. James is responsible for developing Equinix's Interconnection and Colocation solutions in the Insurance Industry in all the primary worldwide insurance centers.

James has worked in the London Insurance Market since 1989 at Centerwrite, The Euclidian Group, and Colt Communications. James holds a Master's Degree from City University, London, and has been a Fellow of the Chartered Insurance Institute (FCII) since 2000.

Joining Equinix in September 2012, James took on the subject matter expert role of the insurance vertical as part of the UK Financial Services team, enlarging that role globally in 2014. James is responsible for developing Equinix's Interconnection and Colocation solutions in the Insurance Industry in all the primary worldwide insurance centers.

James has worked in the London Insurance Market since 1989 at Centerwrite, The Euclidian Group, and Colt Communications. James holds a Master's Degree from City University, London, and has been a Fellow of the Chartered Insurance Institute (FCII) since 2000.

Paul Carroll

Editor-in-Chief, Insurance Thought Leadership

Paul is the co-author of “The New Killer Apps: How Large Companies Can Out-Innovate Start-Ups” and “Billion Dollar Lessons: What You Can Learn From the Most Inexcusable Business Failures of the Last 25 Years” and the author of “Big Blues: The Unmaking of IBM”, a major best-seller published in 1993. Paul spent 17 years at the Wall Street Journal as an editor and reporter. The paper nominated him twice for Pulitzer Prizes. In 1996, he founded Context, a thought-leadership magazine on the strategic importance of information technology that was a finalist for the National Magazine Award for General Excellence. He is a co-founder of the Devil’s Advocate Group consulting firm.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Rimini Street, Inc. (Nasdaq: RMNI) is a global provider of enterprise software support products and services, and the leading third-party support provider for Oracle and SAP software products. The Company was founded to disrupt and redefine the enterprise software support market by developing innovative new products and services, providing ultra-responsive service and delivering outstanding value to clients.