|

Six Things Newsletter | July 20, 2021

In this week's Six Things, Paul Carroll explores the sensor revolution. Plus, aviation risk trends post-COVID; true evolution in insurance? not yet; the past, present, future of telematics, UBI; and more.

Discover 'The Future of Risk™': Innovation, Tech, & Disruption Insights from Industry Leaders!

In this week's Six Things, Paul Carroll explores the sensor revolution. Plus, aviation risk trends post-COVID; true evolution in insurance? not yet; the past, present, future of telematics, UBI; and more.

|

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Sensors will not only let insurers price risk more accurately but will help them counsel clients on how to avoid those risks in the first place.

An announcement by Google and insurtech BlueZoo last week signals the next level of deployment of sensors, a development that will not only let insurers price risk more accurately but will help them counsel clients on how to avoid those risks in the first place.

The announcement involves BlueZoo installing sensors in buildings that detect cellphones looking for WiFi signals. At the moment, rules of thumb tend to be used to generate estimates for the occupancy for restaurants, bars, ballrooms, etc. The BlueZoo approach, essentially counting cellphones, will be much more accurate. Unlike with traditional methods for estimating, the BlueZoo sensors will also be able to monitor constantly, letting insurers and building owners know about issues such as surges in occupancy.

Those surges can be correlated with risk and even used to alert the manager of, say, a bar that everyone should be alert to the possibility of a slip and fall in the bathrooms.

As intriguing as the Google-BlueZoo announcement could be for the insurance industry, it's actually just the latest in a series of developments that will make essentially all information available on any issue at zero marginal cost. That's because sensors can -- and will be -- everywhere. Sensors won't need to be connected to the electric grid or to the WiFi networks that BlueZoo is using. They'll be able to draw power even in remote locations, from tiny solar panels and batteries, and to connect to the cloud via cellular networks or satellites. Nowhere will be out of reach.

Lots of information will increasingly become available just because we're all carrying sensors with us, in the form of our smartphones. Those sensors have been informing traffic management for decades now -- when you see red show up on the route in front of you, you aren't actually seeing cars slowing down, you're seeing the phones in the cars slowing down. They'll generate all kinds of other useful information, too, far beyond what BlueZoo and Google are using.

Other sensors will increasingly envelope us and map our world. While the recent fuss about space travel has been jaunts by billionaires, the far more consequential story is that SpaceX has carried nearly 900 satellites to space already this year. Those satellites will augment the world's communication network while also providing continual updates with more more detailed images of the Earth than are now available. Those images will let insurers -- among many others, including governments -- track vulnerabilities to natural disasters, spot erosion and other developing risks and generally have a map of the entire Earth that they can monitor every day.

Cameras will continue to spread on Earth, too. We've all seen what the adoption of body cams by police officers has meant, and are now surprised when some public event isn't caught on some camera somewhere. These days, cameras are just a lens plus a bit of battery and some memory, so they can be put just about anywhere at almost no cost and be connected to the cloud via WiFi or satellite. Even just the increased use of cameras on cars will capture massive amounts of new information as they drive around, and that information can be put to good use. (To bad use, too, but I'll focus on the good for the moment.) Other types of sensors, notably lidar, will also be mounted increasingly on cars, especially as autonomous vehicles spread, and will generate huge amounts of new data, not just on traffic but on everything they pass.

Sensors will be built into just about every device, so they can warn owners before they break down, can sense water leaks and can provide any other sort of warning or information that might be useful. Sensors will increasingly even move into our bodies. Having them on our wrists has been helpful, but we're not far away from being able to swallow sensors the size of a grain of rice that would provide real-time information on blood pressure, blood sugar and other measures that matter much more than how many steps we take in a day.

Add up all the ways that sensors, including cameras, will spread, and you have a full-on revolution in the information available to all of us, including insurers, to better monitor and manage our world.

You'll note that I haven't said when I think all this magic will happen. That's both because it won't be a single event -- it's already been happening for decades -- and because a firm prediction is hard. I can tell you that two colleagues and I have written a book coming out this fall that refers to the infinite availability of information at no marginal cost as a Law of Zero that we argue will be firmly in place by 2050, with many of the benefits appearing well before then.

I'll tell you more about the book as we get closer to the publishing date and, thus, more about the Laws of Zero, including the one on ubiquitous information. For now, it's enough to start pondering where sensors can go in the short to medium term, how to harvest the information from the new sensors and from existing ones such as smartphones and how to analyze information in ways that improve decisions by insurers and many others.

There will be a ton of work involved -- but profound improvements will result.

Cheers,

Paul

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Paul Carroll is the editor-in-chief of Insurance Thought Leadership.

He is also co-author of A Brief History of a Perfect Future: Inventing the Future We Can Proudly Leave Our Kids by 2050 and Billion Dollar Lessons: What You Can Learn From the Most Inexcusable Business Failures of the Last 25 Years and the author of a best-seller on IBM, published in 1993.

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

As part of this month’s ITL FOCUS on customer experience, we spoke with Scott McArthur, chief revenue officer, Statflo, about the impact of digitization on customer interactions.

McArthur: Over a lot of different verticals, this whole concept of digital transformation, which has been a theme for the last four or five years, just accelerated over the last 14 months. Insurance brokers and bank and telco representatives had to find different ways to communicate with customers as long as they couldn’t meet face-to-face.

There’s a stat: 70% of consumers want to have the ability to securely text or message with their insurance company. And I think insurance companies are finally starting to take notice. They are introducing other means of communication, other channels, to interact with customers. 71% of customers want to be able to fill out documents and send documents digitally rather than go old school and have to sign a piece of paper, then bring it back to the office.

Companies need to maintain local customer interaction but do it through different forms of communication.

McArthur: I think it is. When Statflo started out four or five years ago, we had to educate the market around the value of having one-to-one, local interactions with customers through text, and volume has accelerated tenfold in the last couple of years. People crave one-to-one interactions. They crave simplicity and efficiency.

Increasingly, insurance customers prefer using digital channels when they're looking for product information or are updating their data. Instead of having to call the broker to say, “I just moved, or whatever,” customers can go online and update as they see fit. If you need to do something quickly, you message the broker, maybe do an online chat or just do something through the broker’s website.

McArthur: It’s really across the whole customer journey: when you’re engaging them because they've recently signed up for something new, when you’re sending documents on their insurance plan for the year or when you’re letting customers know about new products and services or reaching out to them when their insurance is up for renewal.

McArthur: I think we can start to know what customers want before they want it. We can be where customers are shopping and looking and surface the right information for them at the right time.

Companies can do the sort of thing that Amazon or Google does, keying off searches, and tailor messaging or curate products and services that are useful to their customer base. If you do that, customers will be more likely to interact with you. They’ll think, “Wow, ABC Insurance Company really gets me and understands what my needs are.”

McArthur: We look at the different industries we work in. And, as much as a lot of people have pain and suffering with their mobile providers, some are providing customers the right information at the right time about the right products and services. That is not the spray-and-pray of blasting out messages to everybody. The carriers focus on specific products and services that a customer might want. A handful of Canadian carriers are doing a great job.

Nordstrom is another example. We've hired a few folks from Nordstrom, where associates keep “black books” on their customers about their preferences on makeup, clothing or sunglasses, whatever it might be. Associates are empowered to reach out to those customers to let them know about some sale that may be coming up or about a new shipment from a favorite brand.

I'm a big Nike guy. I love Nike shoes. Over the last 14 or 15 months, Nike has done a great job at kind of reinventing how they go to market. They've created this level of exclusivity in sneakers with an app that provides “members” the ability to see the latest and greatest with limited edition shoes. They’ve done a great job at creating curated content.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

COVID and its digital pressures have compressed previous time assumptions. Even if you didn't respond, your competitors surely did.

The pandemic led to a burst of home remodeling, and some insurers have likewise found themselves in the middle of a dramatic remodeling project. Choices must be made. Which remodeling projects will modernize and optimize the business, and which ones will create a whole new business next door? COVID and its digital pressures have compressed previous time assumptions. Many initiatives and investments that were set for a three - to five-year path are now moved to 18 months or less.

For decades, the creation and evolution of insurance markets and products unfolded at a slow and steady pace. Insurers’ technology, data and processes were adapted to take advantage of these opportunities – sometimes through technology updates, extensive customization or through new technology. The result of this approach was highly customized and costly systems that did not adapt quickly to market changes. They became increasingly unresponsive to market shifts or opportunities. Companies managed and lived with slow transformation because everyone was in a similar position — new products took 9 -18 months or more to build and launch. Adding new distribution channels could take 6-12 months. These long timeframes slowed and limited market, revenue and growth opportunities because not only were they long but expensive.

But the market is much different now. The pace is significantly different. The types of change have expanded. The constantly changing risks, customer behaviors and expectations, technology-driven capabilities, new sources of data, and blurring market boundaries have increased insurance market demands for new products and services that the old technology cannot support. Today, insurers must be able to launch new products in weeks, new capabilities in days, new channels in weeks or days, and new rates or rules in hours.

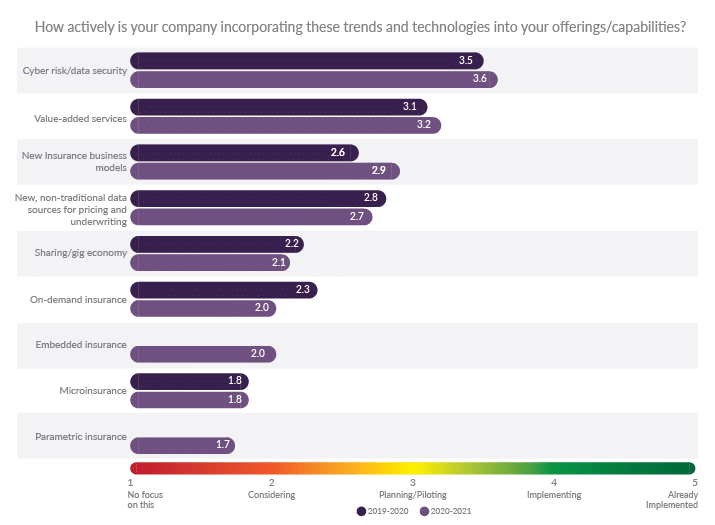

Majesco’s recent Strategic Priorities 2021 report looked at both “traditional” market trends and new and emerging market trends. Insurers continue to show the highest levels of action in the “traditional” market trends, where Cyber risk/data security and Creating value-added services moved past the Planning/Piloting stage and into implementation. Most continue to plan and pilot the use of New data sources for pricing and underwriting, something insurance customers, especially Gen Z and Millennials, want based on our consumer and SMB research.

Encouragingly, strong advances in Creating new insurance business models were made in the Planning/Piloting stage with the strongest year-over-year jump of all the trends (see Figure 1).

Lower Activity Among Emerging Trends

Within the newer or emerging trends, insurers continue to consider offerings for the Sharing/gig economy, Embedded insurance, and On-demand insurance, maintaining similar levels of activity as last year. Microinsurance and Parametric insurance show the lowest levels of interest. While low this year, we suspect that parametric insurance will see a rise next year due to an increased interest in UBI insurance as a result of changed behaviors and less driving.

Figure 1: Insurers’ responses to opportunities created by technology and market trends

The concern with these low levels of activity is that they represent blind spots for insurers as compared to the market potential and customer demand.

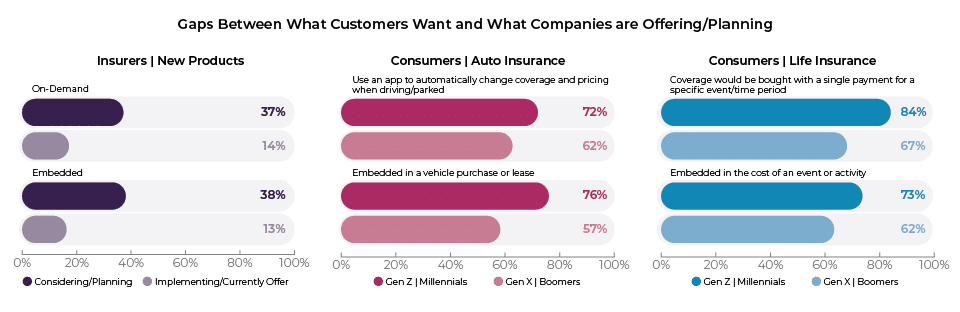

Embedded insurance, which is estimated to account for 25% of the worldwide market by 2030 with $700B in GWP, shows significant gaps between customers and insurers. (See Figure 2.) Only 13% of insurers offer or are implementing embedded insurance and only 38% are considering or planning/piloting it. The 60% gap between customer demand and insurer offering for Gen Z and Millennials reflects a major blind spot and market opportunity for those who can respond quickly. Offering what their parents bought and have is not necessarily what they want or need!

See also: The Rules of Digital Transformation

These blind spots reflect the challenge for insurers to respond to a new generation of buyers who want different products via different channels to meet a new era of customer needs and expectations.

Figure 2: Customer-Insurer gaps in embedded and on-demand insurance

Fortunately, some insurers are actively taking advantage of these opportunities. While likely offering traditional products as well, insurers offering new products lead significantly over others who are not. The only trend that is aligned between traditional and new is Cyber risk/data security and it isthe only trend where those who only offer P&C products do not come in last or second to last compared to those who offer new products, L&A/Group products, or multiline products.

This highlights the risk for the P&C-only segment. If they remain focused on only traditional products they will lose out on new and rapidly growing market opportunities.

Platform Technologies

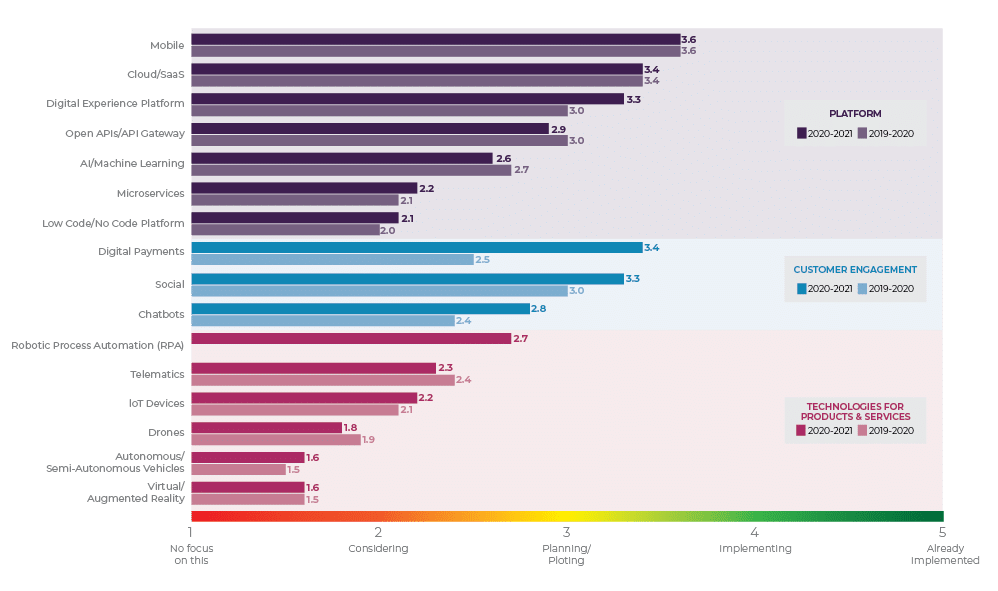

When it comes to the specific technologies that power the insurance platform, we’re seeing the strongest and most consistent adoption of mobile and Cloud/SaaS, while Digital Experience Platforms made a sizable jump year-over-year (see Figure 3). The results we’ve seen for Cloud/SaaS in our research are consistent with the trend SMA has also found: in their 2019 P&C Core Systems Purchasing Trends report, they noted that 84% of core system deals were deployed in the Cloud, and 32% of these cloud deployments were multi-tenant SaaS.

APIs and AI/Machine Learning are entering the Planning/Piloting phase, the tipping point for more widespread implementation and adoption. Microservices and Low Code/No Code Platforms are still in the early stage of adoption. These two critical components give the insurance platform its unique ability to adapt quickly to new market opportunities by making changes to components of insurance processes (microservices), rather than having to change an entire siloed process, and by opening up configurations to a wider audience of citizen developers (low code/no code).

Figure 3: Insurers’ levels of activity in adding platform technologies

All three Customer Engagement technologies – Digital Payments, Social and Chatbots – saw significant year-over-year increases in activity, driven by the sudden need to implement effective self-service capabilities in response to COVID. In particular, the increase in digital payments highlights the acceleration to open banking and innovative payment technology companies.

In a recent InsurTech Forum article, it was noted that open banking has encouraged competition and innovation by requiring banks to share data with third parties such as payment technology companies and by creating customized payment methods through new apps and data streams that will be difficult for companies (sellers like insurance) to ignore. The interest in advanced data-supported digital payments comes from customers’ increased comfort with online banking and shopping during COVID.

Knowing how and why this concerns insurers is of vital importance.

Not surprisingly, companies in the New Products line of business segment lead all others in 11 of the 16 technologies covered by the survey, including the key platform technologies of Cloud/SaaS, APIs, AI/Machine Learning and Microservices. These same companies are in lock step with the Multiline Products segment for two other platform technologies, Digital Experience Platform and Low Code/No Code Platform.

Most importantly, those companies making the strategic decision to adopt these key platform technologies that outpace others are innovating with new products and services and adopting the viewpoint that they are “technology companies providing insurance” as opposed to “insurance companies using technology.”

Digital Capabilities

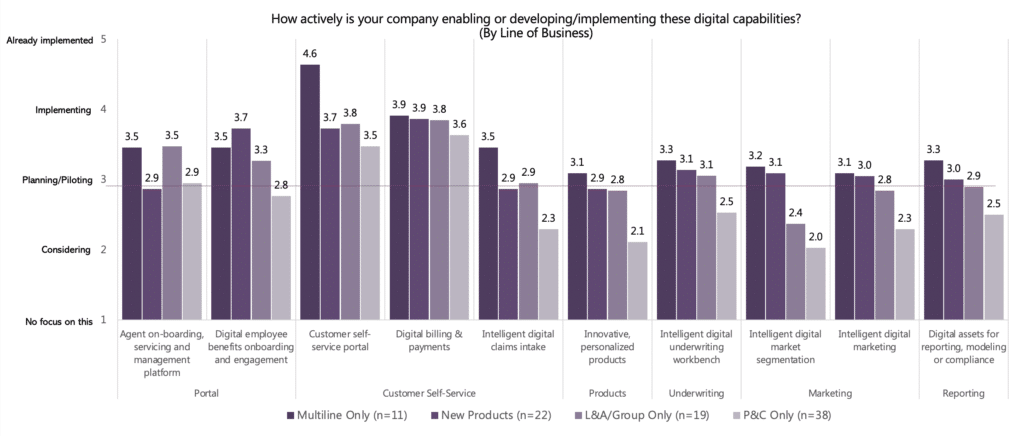

Insurers’ digital transformation is underpinned by increasing customer expectations for new experiences. In their response, insurers are heavily focused on customer self-service applications and portals, with 41% to 61% of companies saying they are implementing or have already implemented these.

Self-service tools and portals have been around for some time, but they do not meet the shift in the desire for personalized, holistic experiences because “out of the box” portals are functionally focused … i.e. a claims app or quote app. In contrast, digital insurance platforms transform these older approaches from siloed, separate transactions into more satisfying, holistic experiences for customers, channel partners and employees as we noted in our life and auto customer research.

Encouragingly, about a third of insurers are implementing or have implemented digital capabilities for intelligent claims intake, intelligent underwriting, intelligent digital marketing and market segmentation, and for reporting, modeling or compliance, with over 40% planning or piloting these, highlighting the acceleration of their digital capabilities.

While the overall high interest in these digital capabilities is encouraging, some very significant differences between business and IT must be resolved to maintain and accelerate momentum.

Business’ ratings were higher than IT for:

See also: Culture Side of Digital Transformation

Finally, multiline carriers are very active in establishing digital capabilities. Driven by the complexity of multiple products, they want to digitalize, simplify processes, and provide self-service capabilities for customers, employees and agents (see Figure 4).

Figure 4: Insurers’ levels of activity in adding digital capabilities by lines of business

So the question for each insurer is: What are you doing with your idle time during COVID? We can tell you the competition is taking advantage of this idle time!

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

Mobile-based data collection has vastly increased the reach of telematics programs by simplifying the sign-up.

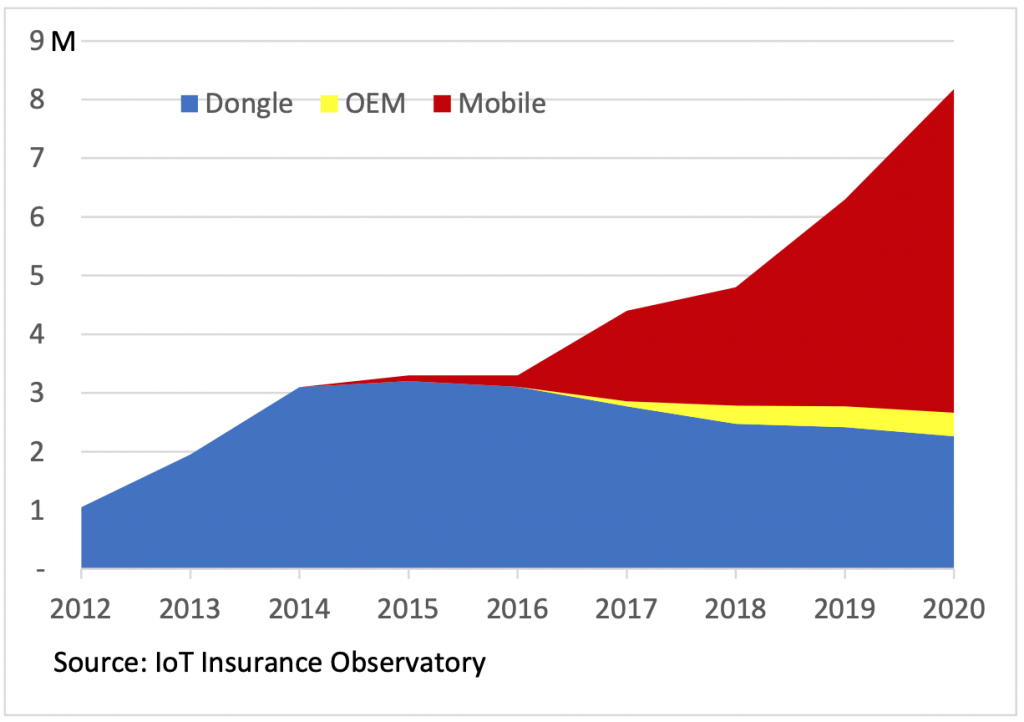

Insurers have spent the last 20 years exploring the potential of telematics with alternating curiosity, commitment and disillusionment. Last year, 8.2 million U.S. auto policyholders shared their driving data with an insurer, according to the IoT Insurance Observatory, a global think tank.

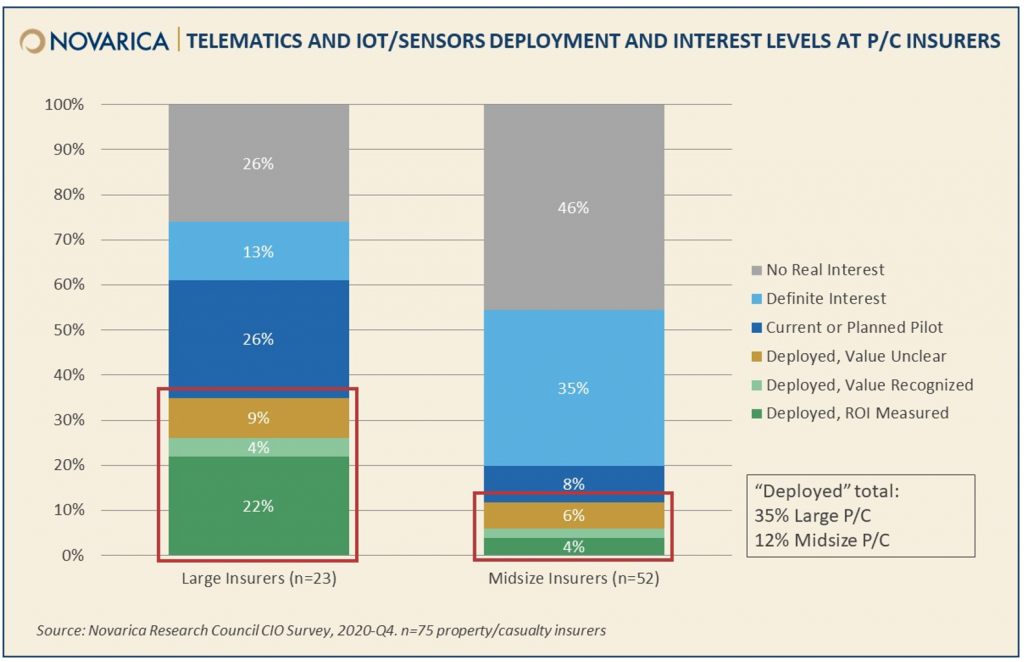

Insurer participation in the telematics space has been consistent for the past several years, according to annual surveys of insurer CIO members of the Novarica Research Council. Insurers that have deployed telematics generally indicate positive experiences; this includes a majority of larger insurers (more than $1 billion in annual written premium), 63% of which have measured positive ROI from their telematics programs. This is fairly rare for emerging technologies, where insurers are more likely to generally recognize value than formally measure it; the ROI places telematics alongside technologies like machine learning and robotic process automation in terms of the value created for insurers that have deployed it.

Given this activity, it’s useful to example the past, present and future of insurers’ use of telematics in personal auto lines, contextualizing current activity in light of insurers’ past approaches and speculating on future developments based on insurers’ present actions. As the article profiles the stages of telematics adoption, the focus will be on what is changing and why.

The Past (1998-2016)

Insurers in this phase were exploring telematics and the insights it could provide. Progressive’s Snapshot program has been the pioneer in OBD/dongle telematics-backed programs. The company's journey has motivated other tier-1 insurers to engage with usage-based insurance (UBI). Several other top-10 insurers had introduced similar programs by the end of 2012, at least in some states.

These programs went out of their way to avoid scaring off initial adopters. They offered discounts to opt in and monitored driving behavior only temporarily, and many even didn’t impose surcharges on poor drivers. The value for insurers largely came from self-selection: only good drivers were interested in enrolling. However, insurers that were better able to effectively manage the usage of telematics data for pricing not only obtained better economic results thanks to surcharging the worst risks but were also able to keep an average retention rate above 94%.

The number of policyholders sharing data with an insurer grew to 3 million in 2014 but then leveled off. Insurers’ commitment subsequently vanished, and market sentiment about UBI became pessimistic. After almost 20 years and relevant investments, only about 1.5% of U.S. drivers were sharing telematics data with their insurers.

Number of policies sending data to an insurer by year in the U.S.

The Present (2017-2021)

While many market analysts with a little literacy about telematics data were speculating whether UBI would die before its potential was realized, in 2016 forward-looking insurer Allstate created Arity, a company dedicated to telematics and focused on the usage of the smartphone as a sensor.

Mobile-based data collection has vastly increased the reach of telematics programs by simplifying sign-up. The market has grown at 30% per year in 2019 and 2020. The COVID-19 pandemic has further increased awareness of UBI among the media, agents and customers – especially about pay-per-mile mechanisms – and is likely to support even more robust growth in 2021, as presaged by new mileage-based programs like that from American Family Insurance (MilesMyWay).

At first, it wasn’t clear mobile was a suitable source for telematics data: A leading telematics conference in 2016 included a session titled “Royal Rumble: Dongle vs. Mobile vs. Embedded Data Collection.” But mobile-based solutions have been the growth engine for telematics over the last few years, and quality of OEM data hasn’t yet met expectations. All the new successful approaches rely instead on the sensors present in the phone – sometimes paired with a tag positioned in the vehicle – and monitor the policyholder for the full duration of the coverage, rather than using a dongle for a single initial monitoring period.

See also: From Risk Transfer to Risk Prevention

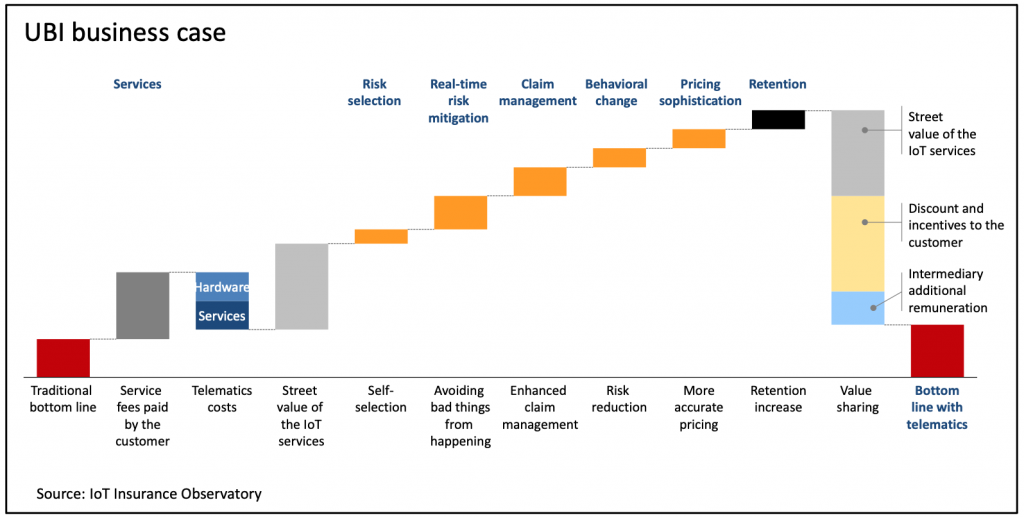

Continual monitoring has allowed many of the top insurers to expand the way they use telematics data. In recent years, U.S. insurers have:

Additional use cases like these allow insurers to build more robust UBI business cases, creating value on insurance profit and loss. This, in turn, allows insurers to create more attractive value propositions for customers: The more value created, the more there is to share with policyholders in the form of discounts, rewards and cash back. These incentives in turn attract new customers, driving further adoption.

Forward-looking insurers investing in these innovations today are progressively building the set of competencies necessary for mastering the usage of telematics data in the insurance business. This will not only create faster-growing and more profitable UBI portfolios but also address the transition to future mobility, as suggested by the story of Avail, the car-sharing service created by Allstate.

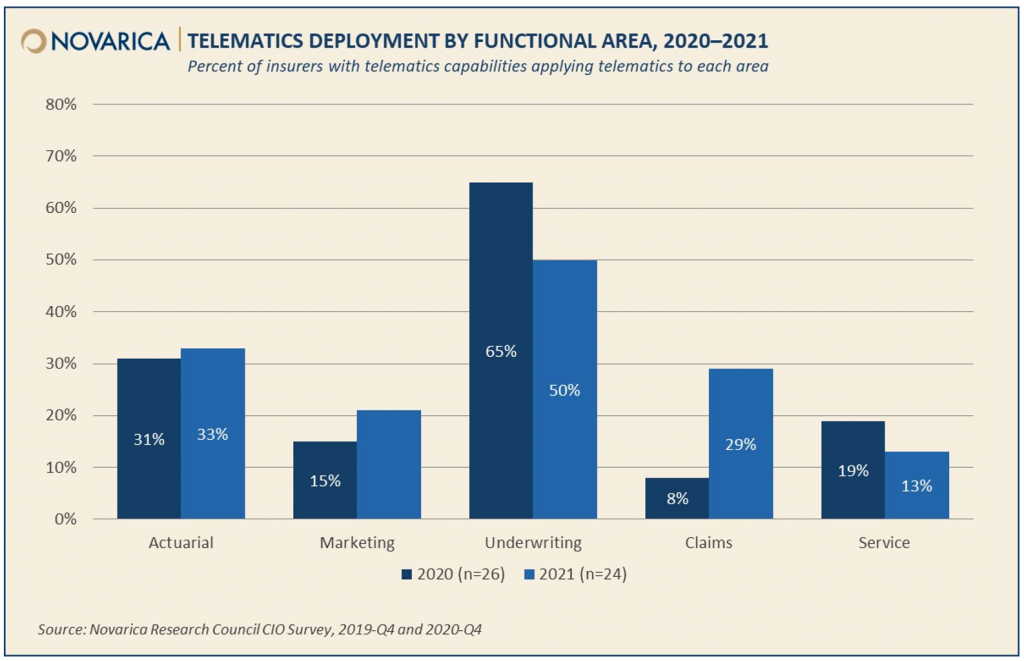

A large portion of the market hasn’t reached this level of maturity, however. Underwriting is still the most common area where insurers use telematics, although a few are beginning to explore other areas.

Many insurers are still watching the space, especially midsize insurers, which have engaged with telematics at roughly a third the rate of their larger counterparts. The percent of insurers deploying or piloting telematics has been roughly unchanged since 2018. (Insurers that are already participating, many of which have measured positive ROI, are continuing to innovate.)

Insurers whose internal technology environments are still mid-transformation may have a harder time supporting value-added telematics features; for these insurers, the value proposition for telematics as a whole is less clear. In particular, insurers need substantial data capabilities to manage UBI data at scale and innovation capabilities to transform the way business has been done for decades. As insurers continue to improve their data capabilities, and as more and more consumers adopt telematics, insurers that aren’t yet in the space may have more ability and more reasons to enter it.

The Future (2022-2030)

An insightful postcard from the future has been delivered by Tom Wilson, Allstate CEO, in a recent Bank of America Securities virtual conference: “If you're not leaning into telematics, you’re not going to be in business for very long, at least on a profitable basis.”

We believe that in 10 years it will be the norm in the U.S. personal auto market:

See also: Personalized Policies, Offered via Telematics

Forward-looking insurers are already preparing for this kind of scenario. This will in turn require transforming processes to most effectively use telematics data. It may not be enough to simply have a UBI product: The technology itself has a cost, and value-sharing (e.g., through discounts), can start at 10%. Insurers will need to use telematics data effectively to generate a return on this investment.

Insurers will have to educate both externally and internally: Not only will they need to communicate the benefits of telematics to potential customers, they’ll need each internal functional area to have a basic literacy about telematics. We expect that the next 10 years will see a tremendous degree of innovation and adoption, so telematics and the value-sharing it enables will be necessary to compete at the leading edge. This in turn should create a sense of urgency: Although simple telematics products can be replicated quickly, effectively leveraging telematics data to generate profitability can take years of iteration and concerted effort across organizations, and capability gaps will require years to be closed. After 20 years of experimentation in the U.S. personal auto market, telematics is ready to take flight.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Harry Huberty is Research Director at Datos Insights, leading the production of their reports for their insurance practice. His personal research interests include the evolution of telematics and IoT in insurance.

Matteo Carbone is founder and director of the Connected Insurance Observatory and a global insurtech thought leader. He is an author and public speaker who is internationally recognized as an insurance industry strategist with a specialization in innovation.

In April 2020, two-thirds of the global commercial aviation fleet sat idle on the tarmac. Today, the aviation industry is slowly rebounding.

The sudden halt imposed on the aviation industry by the COVID-19 crisis hit the sector hard. In April 2020, two-thirds of the global commercial aviation fleet sat idle on the tarmac, while passenger traffic was down 90% year-on-year. Today, the aviation industry is slowly rebounding, led by domestic travel. As more aircraft return to the skies, a new report from aviation insurer Allianz Global Corporate & Specialty (AGCS) highlights some of the challenges airlines and airports face as they restart operations.

1. “Rusty” pilots and the return of sightseeing flights

Earlier this year, dozens of pilots reported making mistakes, such as taking multiple attempts to land, to NASA's Aviation Safety Reporting System, with many citing rustiness as a factor on returning to the skies. Airlines (and other operators) are well aware of the potential for pilot “rustiness” and continue to take steps to manage and mitigate these risks.

Major airlines have developed different training programs for pilots re-entering service, depending on the length of absence. At a time of such unprecedented activity, it is comforting to know that the risk management processes that made airline travel safer than any form of travel prior to the pandemic will continue to drive an unparalleled travel safety environment in the post COVID-19 world.

However, the return of sightseeing flights in tourism destinations could lead to an uptick in risk for smaller leisure aircraft, including helicopters, particularly if there is an influx of new pilots unfamiliar with the routes and terrain. There have already been a number of fatal accidents involving sightseeing flights in recent years.

2. “Air rage” incidents

Unruly behavior of airplane passengers is increasingly a concern, particularly in the U.S. In a typical year, there are around 150 reports of passenger disruption on aircraft. By June 2021, there had been 3,000 just this year, according to the Federal Aviation Administration – the majority involving passengers refusing to wear a mask. The report notes that unruly passengers may later claim they were discriminated against by the airline in these cases even when in the wrong – a trend insurers need to stay on top of.

3. Perils from parked fleets

Although a large proportion of the world’s airline fleet have been – and are still – parked during COVID-19, loss exposures do not disappear. They change. Parked fleets are exposed to weather events. There have been numerous incidents of grounded aircraft being damaged by hailstorms and hurricanes.

The risk of shunting or ground incidents also increases, which can bring costly claims. There were a number of collisions at the start of the pandemic as operators transferred aircraft to storage facilities. More are likely when aircraft are moved again ahead of reuse.

Aircraft in storage typically undergo regular maintenance to ensure they are ready to return. However, never has the industry seen so many aircraft temporarily put out of service, and the report notes that smaller airlines may face significant challenges when reactivating fleets, given that it will be an unprecedented process.

See also: How COVID Alters Claims Patterns

4. Pilot shortage

Odd as it may seem given the impact of COVID-19, but the global aviation industry faces a pilot shortage in the mid- to long term. The tremendous increase in air travel pre-pandemic – annual air passenger growth in China alone was 10%-plus a year from 2011 – meant pilot demand was already outstripping supply. More than a quarter of a million are required over the coming decade.

Some airlines are building their own pilot pipelines by establishing flight schools. Given the nature of training, flying schools are prone to accidents, and claims are becoming more expensive with rising values of aircraft and increased activity. Landing accidents are most common, but insurers have also seen total losses.

5. New generation aircraft

A number of airlines have shrunk their fleets or retired aircraft over the past year, as the pandemic hastens a generational shift to smaller aircraft, given the anticipated reduced number of passengers on aircraft in the short-term future.

Newer-generation aircraft bring safety and efficiency benefits, but new materials such as composites, titanium and alloys are more expensive to repair, resulting in higher claims costs.

6. Robust performance by air cargo

Although passenger travel has been devastated by the pandemic, other aviation sectors have performed more robustly, such as cargo operators. In April 2021, Asia Pacific reported its best month for international air cargo since the pandemic began, thanks to rising business confidence, e-commerce and congestion at sea ports, while Latin America to North America freighter capacity grew by almost a third in May 2021 compared with the same two-week period in 2019. The report expects air cargo to continue to perform strongly.

7. Business travel – boom or bust?

Pre-COVID-19 business travel traffic amounted to $1.5 trillion a year, or around 1.7% of global GDP. With many airlines dialing back expectations in the short term, the report asks whether those days are over. New ways of collaboration, such as video calls, proved to be effective, and more companies are aiming to reduce business travel to improve their carbon footprint. Therefore, while there will be initial surge once lockdowns end, many airlines are preparing for a long-term paradigm shift in traveling, with business travel expected to be slow to pick up.

However, what speaks for a possible uptick is that some areas of business aviation have proven resilient during the pandemic. Companies that had aircraft continued to use them, while many that had never purchased or chartered an aircraft before did so for the first time. Many charter companies thrived.

8. New routes in Europe and Asia Pacific

Over 1,400 new air routes are scheduled for 2021 – more than double those added in 2016 – driven by Europe (over 600) and Asia Pacific (over 500), with regional airports set to be the main beneficiaries. Growth in China’s domestic market alone has seen over 200 routes added – almost the same as the U.S.

9. Insect infestations

There have been a number of reports of unreliable airspeed and altitude readings during the first flight(s) after some aircraft have left storage. In many cases, the problem was traced back to undetected insect nests inside the aircraft’s pitot tubes, pressure-sensitive sensors that feed data to an avionics computer. Such incidents have led to rejected takeoffs and turn-back events. Contamination risk increases if storage procedures are not followed.

See also: Pressure to Innovate Shifts Priorities

COVID-19 claims impact

The report also notes the aviation industry has seen relatively few claims directly related to the pandemic to date. In a small number of liability notifications, passengers have sued airlines for cancellations/disruptions.

AGCS analysis of more than 46,000 aviation insurance claims from 2016 to year-end 2020 worth more than EUR 14.5 billion (US$17.3 billion) shows collision/crash incidents account for over half the value of all claims. Other expensive causes of loss include faulty workmanship/maintenance and machinery breakdown.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Dave Warfel is head of aviation, North America, for global insurer Allianz Commercial.

He has two decades of aviation insurance experience. He is a graduate of the Institute of Aviation at the University of Illinois and is a licensed commercial pilot.

Disruption won’t occur until 80 cents out of every dollar in premium is given back to the policy holder, instead of the 50 or 60 cents given back now.

More insurtech startups were launched in the last two years than in the previous 10. The brightest minds are developing new ideas and forging new paths in the insurance industry, but the reality is that significant change is a little further down the line. We need structural change long before the process of buying and selling insurance can adapt to the needs of modern consumers. This will take several years, maybe even a decade.

In my 30-plus years investing in fintech and insurtech and operating both digital and legacy insurance companies, I have seen first-hand the changes required to reduce costs and create better customer experiences in the industry. Many people approach innovation with the goal of improving existing products or procedures. That’s a good start, but, in the digital world we live in today, it’s not enough. Tweaking the product isn't a significant change, and the process will be repeated within a year or two.

Innovation requires duality: You must innovate for the needs of the business while innovating for the needs of the consumer. It’s no longer solely about business processes and controlling the lion’s share of the distribution channels. It’s about figuring out how to be more consumer-centric. We must be motivated by creating a great experience that makes customers want to come back every day.

Unfortunately, this is easier said than done. Take Lemonade. They launched a few years ago with a completely different user experience, which is amazing; but because the regulatory environment in which they operate is still not very bespoke to each individual consumer, they did not really change the product—but we’ll get to that later.

We are witnessing a significant shift in consumer expectations and desires, but we must also manage the longstanding and tradition-holding customers we have today. While we wait for structural transformation in the insurance industry to come, there are a few smaller changes that will bridge the gap in the meantime.

See also: The Evolution of Telematics Programs

Embrace Digitization

Insurance is, for the most part, digital in nature: and, given that tech is more available and accessible than ever before, it’s only natural that insurtech is becoming so prominent in the industry. Technology is less expensive, easier to use and more ubiquitous than it’s ever been, and many companies want to digitize their business. This, of course, would include the user experience.

Many are missing the mark here. Though technology has advanced significantly in the last few years and we have seen rapid increases in digitization across industries, it is still a real headache to change your insurance, even though it’s been digitized. Part of the problem is the archaic nature of insurance regulation, which requires constant approvals every time you want to amend the insurance provided. Insurance company’s rules and regulations make dynamic pricing virtually impossible in their historic form, especially when you compound that by 50 state regulators within the U.S. These processes must be made easier for us to see real growth and change in the industry.

Understand the True Meaning of Disruption

Many people believe that they have the chance to be a disruptor or play a role in disruptive innovation. But why does that matter? If you can be the disruptor, you win the prize and get the 10-digit valuation. But many are missing a more simplistic way of running their business because they have not embraced innovation and are making things more complicated for themselves. They also aren’t focused on the value proposition. Disruption won’t occur until 80 cents out of every dollar in premium is given back to the policy holder, instead of the 50 or 60 cents given back now. So how do we get there? We have to focus on making it the best possible experience for the customer, in every way possible.

Tech is now more available and accessible than ever before. It’s only natural now that people have a go at it. Some of the companies that were started seven to 10 years ago, such as Oscar, Clover Health, Root Insurance, Next Insurance, Metromile, CoverHound and PolicyGenius, now have enough traction that they are becoming more widely used in the marketplace—you are hearing or reading about them even though they have been around for a while. Many companies know by now to invest in data and analytics and create more processes. But to truly disrupt things, companies will need to come up with entirely different business models than the ones that exist today. This won’t happen without embracing digitization combined with a new level of customer-centricity.

See also: Digital Revolution Reaches Underwriting

It is time to go beyond embracing tech and innovation and into tailoring bespoke experiences to individual consumers, especially in an industry as personal as this one. The Lemonade example teaches us the importance of this; without this balance, we aren’t achieving true optimization. A lot of companies claim that they are innovative and are disrupting the industry but have yet to embrace the actions that will get them there. We need to focus on changing the narrative to where it’s more about serving the policy holder as opposed to the product nature of the industry historically. It is time for the insurance industry to change and grow to accommodate a new generation of consumers.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Mark E. Watson is a venture capitalist, philanthropist and CEO who is fully invested in seeing companies reach their full potential. For over three decades he has led businesses to immense success. His current role is CEO at <a href="https://www.aquilacapitalpartners.com/">Aquila Capital Partners</a>.

Embedded insurance has been around for a long while in the form of affinity groups, but it still creates opportunities that smart agents will exploit.

You may have heard of all the wondrous new possibilities afforded by embedded coverage, with hints of ominous implications for insurance agents. But before any agents start polishing up their resumes, hear me out: Embedded insurance is nothing new. It’s been around for a long while in the form of affinity groups. And embedded insurance will increase opportunity for intermediaries, not eliminate it -- so long as they know how to use it to their advantage.

What exactly is an affinity group? Essentially, it is a group of people who share some trait that makes them a desirable market. An affinity relationship is symbiotic: The carrier provides discounts or other benefits to group members (conferring benefit onto the organization itself, as well, as it can boast this additional membership value). The group provides the insurer with a pool of potential customers and built-in marketing. Everybody wins.

So, is embedded insurance actually the “new affinity?” Not exactly; there are some important distinctions. In both instances, you’re targeting a specific group with a coverage offer because they share some trait that makes them desirable. The distinction is that embedded insurance is more like a tool that agents and carriers can use to be more creative about the affinity groups they target. It allows them to target adjacencies that might not have been viable in the past: For instance, by partnering with a large property rental company, carriers can offer embedded renters insurance as an applicant is about to click “submit” on their lease paperwork -- at the precise moment the risk is top of mind and the offer is most relevant to the consumer. Not so long ago, that consumer would turn in their lease documents, think to themselves that they should look into renters insurance and then get busy with moving priorities and maybe eventually forget to secure a policy at all -- and the carrier’s distribution costs in attempting to market renters insurance to the right audience were often impractical. By increasing relevance and convenience through embedded marketing, carriers have the opportunity to create massive new revenue streams. Embedded insurance comprises the tools and technology that will allow affinity to scale, and the sky’s the limit.

So what should carriers and intermediaries be doing right now to ensure that they are equipped to ride this wave, instead of being capsized by it?

See also: Building Your Digital Sales Arsenal

So next time you read about how embedded insurance is going to make you obsolete, remember that a tool can’t be used to clobber you if you’re the one wielding it. Embedded insurance will create boundless opportunities for a wide variety of businesses over the next decade, so seize them. There are a million ways to make this model work for you and not against you -- the only wrong move is to do nothing.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Bill Suneson is the co-founder and CEO of Bindable, a national leader in digital insurance and alternative distribution technology. He also co-founded and serves on the board of Next Generation Insurance Group, which operates GradGuard.

In this week's Six Things, Paul Carroll explains why customer surveys are passe. Plus, killer flying robots are here - what now?; how workplace has changed for women; AI and its impact on automotive claims; and more.

|

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

By using life insurance to create an estate plan, qualified borrowers can turn rising house prices into tax-free income.

The pinnacle of the real estate market, of any market, is hard to predict, just as the precipice of a collapse in prices is real but unpredictable. About the sea below, red with debt and white with foam, about the flotsam from those houses underwater and too deep to raise, a reminder: We must sail to port, for we cannot afford to drift or drop anchor; we must sail toward safety, in safety, with the safety insurance provides; we must sail with the tide, allowing it to lift us without having it crash against us, so we may convert a rise in valuations into a plan that delivers everlasting value.

By using life insurance to create an estate plan, and funding the plan with cash from a home equity conversion mortgage (HECM), qualified borrowers (ages 62 and older) can turn rising house prices into tax-free income. Because the appraised value of a house determines the size of a loan, and because prices have risen at the fastest rate in more than 30 years, borrowers have more money to invest. How they choose to invest this money, whether they choose to guarantee a legacy for their loved ones or better themselves without relying on their loved ones, is their choice.

More important is the fact that borrowers are free to choose, that they have the freedom to secure paper wealth with paper as secure as property. Because of what the law says, that life insurance is a form of property, and because of what life insurance offers, liquidity, borrowers are free to make real the promises of HECM: bestowing upon themselves, or bequeathing to posterity, the blessings of financial freedom.

Take, for instance, a 62-year-old woman with an average life expectancy of 84. If the appraised value of this woman’s house is $500,000, or 25% higher than a year ago, she can transfer the money from a HECM loan into a life insurance policy, safeguarding the principal while earning tax-free income from a diversified portfolio of investments. Or the beneficiaries of her estate can receive a cash payout, minus the balance and interest of the HECM loan, thanks to a life insurance policy.

See also: Where Does Life Insurance Go Now?

Thanks to the fact that life insurance is a lifeline, this woman has the power to avoid the shallows and miseries of the sea. Whether her voyage is long or short, whether her vessel is a sloop or a schooner, the sea—mysterious, wild and unrestrained—endures. To weather its storms and withstand its moods, to be like a rock of strength and prudence, able to rise from awful stirrings and right the course, to stir the course with apparent wind, requires the assurance of a wise captain.

The captain deserves insurance, too, so she may sail in peace, despite the conditions of the sea. Mindful of the direction, and peaceful because of her directives, life insurance guides this captain home. Life insurance guides her travels.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Jason G. Mandel has spent over 25 years at the intersection of Wall Street and the insurance industry. Mandel founded ESG Insurance Solutions (www.esginsurancesolutions.com) in 2020 to help better integrate these two, often conflicting worlds Having a strong belief in ESG concepts (Environmental, Social and Governance), Mandel found a way of incorporating his beliefs in his business.

Representing only insurance carriers and products that he believes offer compelling risk management solutions and maintaining business practices that he can support, Mandel has led the industry in this ESG initiative. ESG Insurance Solutions serves some of the wealthiest families internationally, and their business entities, by providing asset protection, advanced tax minimization vehicles, principal protected tax-free income structures, employee retention strategies, key person coverage and tax-free enhanced retirement plans for their essential employees.