|

March ITL Focus: Underwriting

ITL FOCUS is a monthly initiative featuring topics related to innovation in risk management and insurance.

Discover 'The Future of Risk™': Innovation, Tech, & Disruption Insights from Industry Leaders!

ITL FOCUS is a monthly initiative featuring topics related to innovation in risk management and insurance.

|

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

In this month's ITL Focus, Paul Carroll interviews Jess Keeney, Duck Creek's Chief Product & Technology Officer, exploring the game-changing role of generative AI in underwriting and its implications for insurance technology and customer engagement.

|

|

As Chief Product & Technology Officer (CPTO), Jess leads Duck Creek's product vision to drive value for customers, partners and system integrators. She is a champion of improving the customer experience and leads with a forward-thinking attitude toward deepening the connection between products. Jess has more than 15 years of experience delivering B2B products at an enterprise scale across multiple industries. |

You’ve written for us about the need for personalization in insurance. Could you start us off there?

At Duck Creek, one of our missions is to humanize insurance technology. We're in the business of providing protection for people and businesses, and you can't do that without personalization. It's key to understanding buying patterns, making sure we meet the customers where they are, reducing the burden by making it easier to understand what that protection is, and understanding what coverages we can provide and what the risk factors are for the buyer and for insurance carriers.

Personalization also leads to increased efficiency and what I like to call “higher-reward work” for human workers. It also improves accuracy for insurance companies.

How does generative AI fit improve that personalization?

With its natural language processing, Gen AI can communicate in human form and at a much larger scale than we've seen before — and in real time. It’s going to help in lots of great ways.

One of the areas is in summarization or categorization of information -- at scale and faster than a normal human pace, also making it more digestible for the people who are consuming the information, while making sure it’s presented within the normal workflow without adding a delay.

That improvement can show up in anything from how we're assessing and processing claims, to how we're underwriting policies, to how we're collecting premiums, and ultimately making better-informed decisions.

It seems to me that there are two main ways that Gen AI will contribute to personalizing underwriting. You’ve briefly mentioned both of them. First, the underwriter gets more information faster. Could you talk a bit about how that plays out?

You can incorporate more data sources without going through manual processes. You can improve the thought process of risk analysis, how you look at historical risks, and incorporate new risks from any new dataset. And those datasets are prolific and pervasive across the ecosystem, whether it's the Internet of Things (IoT), including telematics, or really anything that can allow insurers to adjust a premium based on actual behaviors.

Obviously, the prime example of what we can now track is driving patterns. But more and more, we're seeing computers interpreting visual information, satellite information, wildfire information, anything in the geo- or economic-political climate that would have an impact.

Another use case is how insurance carriers are evaluating and prioritizing new business. They have the ability to set the right priorities. What should we be processing first because it might have a greater impact on our profitability? What is a faster detection of fraudulent activities to reduce the risk of financial losses?

The second piece I wanted to ask you about is what you refer to as the higher-reward work: the idea that if you take a lot of the manual stuff off my plate then I can do other things that would personalize the underwriting and lead to better decisions.

That change allows you to have a better understanding of the business and what's going to give you a competitive edge. You get a better understanding of the market trends, of what's coming. You have more time for understanding changing customer behavior and can test to see what’s going to result in a different buying pattern. You can inform product development and provide insights into pricing strategies because you're not sitting there doing manual repetitive tasks.

You’re looking at better engagement with the underwriter, better job enjoyment, reduction of repetitive costs, also potentially reduction of human error. You’re removing operational cost, and people enjoy working more on strategic application of their thought process and how they can help the business.

Anything that can be automated should be automated. And that gives us a lot more time to focus on the newer complexities that we should be getting ahead of.

Insurers worry a lot about the talent gap, but people who are enjoying the work more are more likely to stay, and it becomes easier to recruit people, right?

If you talk to people graduating from college and say, “Hey, do you want a job where you're doing the same set of manual tasks over and over again?” not a lot of people are going to jump at that opportunity. But if you go to that same group and say, “Hey, do you want to use artificial intelligence to really understand how to do customer segmentation and understand new buying patterns for people of your generation?” that's a far more enticing job offer.

GenAI can help new talent and the new generation enjoy work because it spurs more meaningful and creative work for everyone. Also, if used properly, it can help enable more fulfillment and lead to a more engaged workforce that has opportunities for all.

I’ve asked you about two areas. Are there others where you see Gen AI playing out in underwriting?

The other obvious one is better customer support and feedback. If you give underwriters more time, they can see where they might be losing people out of the funnel, where people are not concluding with a purchase. You can also use a chatbot or do something in human language form at the spot in the cycle where people are dropping and ask, “Do you need more explanation? Do you understand what this means for you? Do you understand the risks? Do you need more protection?” Even if you don’t have an actual human asking those questions, you’re creating an avenue to offer additional products and services if they're in the wrong one. You also create cross-sell or upsell opportunities because you understand the customer better.

That's interesting. Somebody a while ago told me that the interesting thing to her about generative AI is that, while AI always had a brain, it now has a mouth. If an underwriter decides, let’s say, to turn down a risk, they might want to offer some explanation that could create another opportunity, whether then or down the road. But that takes time, and there are usually more pressing priorities. With Gen AI, you can have it generate an explanation that can give you a pretty good starting point and greatly reduce the time the underwriter spends on that explanation.

Exactly. I think of this like something that has probably happened to all of us in our online shopping. You get to checkout and decide you don’t want something. Two days later, you get prompted: “You left something in your cart.” When you return to the site to look, you maybe buy that product or purchase something else while you’re there.

I think that is where we're going with insurance products, as well. If you're in the wrong area, you're not going to complete that funnel. So, what can the insurer offer instead, because you have a better understanding, based on customer segmentation and understanding the personalization that you've offered them? What are the other products that they might be willing to work with you on?

Any final thoughts on how AI can improve underwriting?

The only other thing we really haven’t focused on is just making more informed, better decisions.

It seems like this is a time when that message resonates even more than usual, because underwriting results have been so bad in so many parts of the industry in recent years, especially in homeowners and auto.

Agreed.

Any Final Thoughts?

We are here all day every day because we want to serve people in businesses, and underwriting is obviously core to that. The best thing we can do with a new technology like Gen AI is to embrace it and figure out how to leverage it in the best way possible. Usually, new technology is met with fear. But the faster we can understand the best use cases for generative AI and implications for underwriting, the better.

Nothing has ever seen this sort of pace of adoption. It's going to be amazing.

Thanks, Jess.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

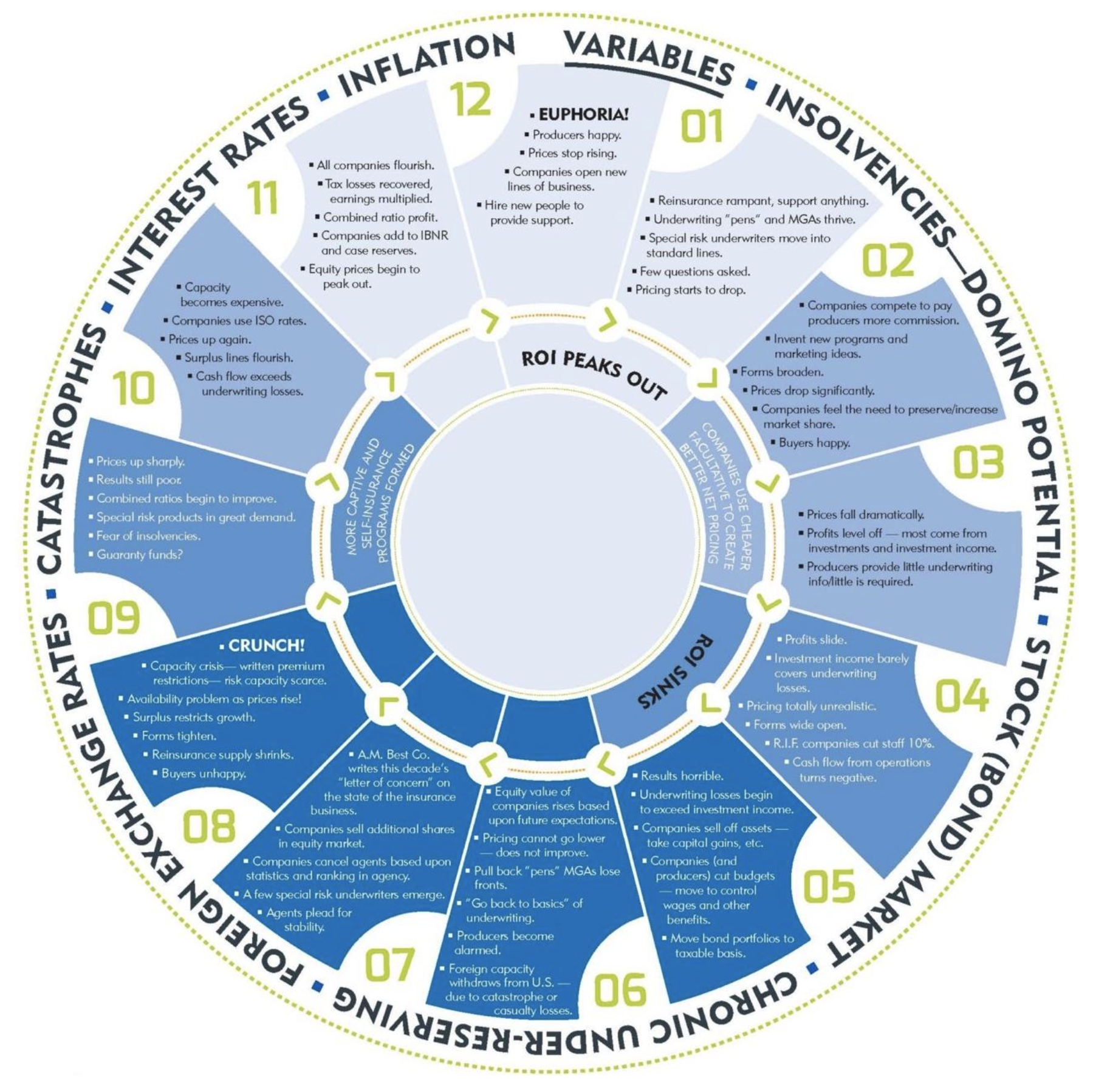

The hard market/soft market cycle has reigned for decades, but COVID shocks and a host of new technologies may be ending it.

Today’s world is confusing, replete with mixed and conflicting signals. Reports of low unemployment and high inflation have muddied forecasting for a recovery or a looming recession and leaves us unsure of what to expect: traditional economic cycles or permanent change. Either way, such signals foster uncertainty and test our objectivity on a daily and even hourly basis.

The P&C insurance market is displaying its own mixed signals, making it difficult for insurance business leaders to plan and adjust, not to mention the tremendous disruption to agents and customers. Large and persistent rate increases contrast with the most recent improvements in combined ratios and net income. Tighter underwriting actions and lack of insurance availability is creating challenges in navigating the complex landscape by all stakeholders.

See also: How to Respond at Inflection Points

The Insurance Clock

Back to the question: cycle or permanent change? Despite P&C’s desired state of steady, profitable growth, the reality is a constant tension and cycle of writing new business followed by turning the dials for profitability. In just the last 25 years, major shockwaves from 9/11 terror attacks, wars and the housing and financial market collapse have tested industry cycles, yet the clock still ticks ahead, perhaps with more elongated recoveries after these shockwaves.

The Insurance Clock best illustrates these cycles and was introduced by Paul Ingrey, former Arch Capital Group director and board chairman, and still applies today. It is a sophisticated view beyond the simplified hard market, soft market labels. For instance:

Source: Paul Ingrey, Arch Capital, 1985

Underlying this turbulence is the age-old question: Is this simply a cycle, or are we witnessing lasting changes driven by new technologies, altered consumer expectations, post-pandemic inflation and weather changes? To understand the current state of the P&C insurance market, it is necessary to delve into these key factors.

Rate Increases

One of the most noticeable trends in the P&C insurance market has been the steady increase in insurance rates. The drivers behind these rate increases are multifaceted. Post-pandemic inflation has led to higher costs across the board, from materials to labor. Additionally, the frequency and severity of natural disasters and extreme weather events have been on the rise, leading to increased claims payouts. Insurers are responding by adjusting their pricing models to reflect these new realities, which has resulted in higher premiums for policyholders.

Emerging and growing cost factors are real and may not yet be fully reflected in today’s rates. Namely, social inflation, nuclear verdicts, aging drivers and related auto injury costs, new car technology and repair/replacement costs and auto repair technician shortages are obscured by the two obvious culprits: inflation and weather losses.

Positive Insurer Profitability Picture

Despite these challenges, several insurers are beginning to see positive signals in profitability, particularly looking at Q4 of 2023. This improvement can be attributed to several factors, namely higher rates and fewer storms during the end of 2023. Additionally, more rigorous underwriting standards are leading to healthier books of business.

Net income and combined ratios among several leading carriers are making what looks to be an impressive rebound, with Progressive, Chubb, Travelers and GEICO among the most vibrant, to name a few. Progressive’s most recent combined ratio dropped to 87.3. Allstate’s combined ratio for homeowners’ insurance during Q4 was down 30.8 points to 62, and their auto line fell to 98.9 in Q4. Allstate CEO Tom Wilson said “improved auto profitability and mild weather” drove the fourth quarter turnaround. However, “rate increases will continue to be implemented to keep pace with loss trends and improve margins in states where we have not yet achieved rate adequacy.”

The improving profitability picture in Q4 2023 is a welcome development for insurers, as it indicates that efforts to adapt to changing market conditions are bearing fruit. However, it remains to be seen whether this trend will continue in the face of inflation and weather wild cards.

See also: 5 Key Mistakes in Long-Term Planning

Lack of Insurance Availability

Insurers are becoming more selective about the risks they underwrite, creating a lack of insurance availability in high-risk regions, leaving homeowners and businesses vulnerable. Higher deductibles, less coverage, push toward wind pools and flat participation in NFIP’s flood insurance program despite more flooding is becoming the norm. The widening protection gap, underinsured and uninsured are highly concerning and defy the risk-transfer proposition of insurance.

The lack of insurance availability is a complex issue with no easy solutions. Insurers are caught between the need to manage their risk exposure and the desire to provide coverage to those in need. Finding the right balance between is crucial to ensuring the long-term sustainability of the insurance market.

Recurring Cycle or Permanent Change?

According to the Insurance Clock, there is little need for panic, in fact, good reason for optimism. Although one might interpret the return of a stable market not so far away, just two to three hours, according to the clock, that does not seem remotely possible. Yes, raising rates has always served as the ultimate relief valve and the fastest way to recovery. Bolt on some re-underwriting actions, and the combination becomes the fixer of all underpriced or unfavorable risk selections. Once rates become adequate, risk appetite increases, and carriers revert to a growth mindset in what compares to financial yoyo dieting. At least, this is how it has worked in the past.

Things are different now as inflation is proving persistent and as catastrophic weather exposure is accepted as here to stay -- more frequent and more severe. Certainly, things are vastly different from 1985 when the Insurance Clock was invented. Still, there are continuing shockwaves from COVID-19, which reshaped the economy and changed the workforce in terms of participation and shortages. Population migration to CAT-exposed Southern states and away from cities like San Francisco and New York are shifting exposure in real time. Changing social attitudes and risks are happening at a quicker pace. Massive rate increases and pull-out from markets and whole states is widespread. Although it is difficult to forecast all future COVID-related impacts, those identified are more pronounced and longer-lasting, bringing the cycle into question.

Arguably the most significant changes since the Insurance Clock was introduced in 1985 are those resulting from new technologies. These include: cell phones, World Wide Web, notebook computers, the personal digital assistant, VOIP, Amazon, eBay, WebEx, WiFi, Google, Blackberry, Bluetooth, Apple iPod, Wikipedia, wireless internet, application programming interfaces (APIs), wireless high-speed internet access, Facebook, YouTube, Twitter, social media, Apple iPhone, Apple iPad, Skype video conferencing, tablet computers, Amazon Echo, VR headsets, facial recognition, IoT, AI, 5G, cloud computing, blockchain, quantum computing, virtual meeting software and virtual hybrid events. The combined impact of these advances is unprecedented in how deeply and widely it has permanently changed almost every aspect of the insurance industry, leaving one to consider how new technology might ballast current trends or how much worse would today’s results be without all these advances.

We believe that the traditional insurance cycle is no longer as relevant as it once was, primarily because underlying market conditions have permanently changed – and will continue to change. In this environment, insurance leaders must become more entrepreneurial, encourage and embrace innovation and reshape their organizational cultures to be the same.

Carriers should seek to develop strategic partnerships and alliances with more nimble technology-enabled partners. Recruiting, hiring, training and upskilling strategies should be revisited to ensure appropriate alignment of required skills today and tomorrow. And diversification of product and even business focus could be appropriate as a means of spreading the risks presented by changing and unpredictable future conditions.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Alan Demers is founder of InsurTech Consulting, with 30 years of P&C insurance claims experience, providing consultative services focused on innovating claims.

Stephen Applebaum, managing partner, Insurance Solutions Group, is a subject matter expert and thought leader providing consulting, advisory, research and strategic M&A services to participants across the entire North American property/casualty insurance ecosystem.

Tony Kuczinski, an insurtech pioneer at Munich Re, explains what went wrong in the early days – and what is now going right.

|

Anthony (Tony) Kuczinski is a highly regarded executive leader with over 38 years of (re)insurance experience, 34 years of which were with Munich Re in numerous senior roles, including 15 years as President and Chief Executive Officer of Munich Reinsurance US Holdings. He also served as Executive Advisor to the Munich Re Board of Management for MR US Holding (MRUS), the NA Property and Casualty operations of Munich Re (DAXI: MUV2). Prior to Munich Re, Mr. Kuczinski was Chief Operating Officer of NY Marine and General Insurance Company (NYM), a publicly traded insurance group now part of Pro-Sight Insurance Group, and he worked in the audit practice for the public accounting firm of Coopers & Lybrand (now PWC). |

How would you characterize the evolution of insurtech over the last decade?

At Munich Re's U.S. business, we were early participants in the insurtech wave. I never believed insurtech would disrupt the insurance industry, and in retrospect, it didn’t. However, I firmly believed we needed to be involved in this space. Over the last decade, innovation has changed dramatically. While insurtech hasn't disrupted the industry, it has changed the industry for the better, specifically for the more forward-leaning companies and those focused on strong underwriting fundamentals and those keenly focused on their clients. Insurtech has made us faster, more nimble and more technologically savvy. It has also made us more client-focused.

The early insurtech players believed they had a different model that would make the industry dinosaurs obsolete. This turned out to be a misconception on their part. Many insurtechs stumbled over the years. Others realized early on that the risk-sharing model they wanted to disrupt wasn't what they thought and shifted more toward being MGA-oriented or distribution-oriented.

Insurtech isn't gone. It just didn't materialize as initially anticipated. Valuations were high in the early days, then stumbled, and there was a back-and-forth kind of situation for some time. And the jury is still out for the risk takers among them. However, I think they made the industry better in the long run.

If you invested in insurtech, and collaborated with them, you probably learned some lessons about being nimble and agile. You probably learned to deploy technology differently than you did in the past. You also likely became more intensely focused on the customer and the service elements you bring to them.

Looking forward, I still think there's a role for insurtech, but I think it's going to take a different form. It's going to be more about getting better at what we do. How do we help to mitigate risk? How do we get better at identifying risk? The industry will evolve into a predict-and-prevent model as well as a financial reimbursement model. How do we get better at servicing the client and at providing this service more efficiently? And how do we deploy effectively artificial intelligence in the insurance space today?

Why do you think the big tech companies didn't jump in and disrupt the insurance industry?

Early on, I think there was a lack of appreciation for two things in the industry: capital and regulation. There is a big capital need to be a strong player in the industry, and it's a highly regulated industry. Even the non-standard businesses aren't free from regulation. I think there was a recognition after a while that this is a difficult model to emulate. There was also a realization that the long-term-return proposition would dilute the hefty returns many of the big tech companies enjoy today.

The tech players dabbled a lot and are still dabbling in this space. However, I think they're looking at how to impact the insurance space more as a service provider or as an enabler, not as an insurance entity. I still think that's possible. It's clear to me that AI could absolutely help, whether it's robotic processing or better analytics. It could be a game changer.

So the companies that improve insurers, rather than trying to replace them, are the ones thriving at this point?

I think that's an accurate statement. I think there's a new phase of this. Those that took the new business model into places like cyber technology and cyber coverage have done pretty well. They focused not only on the risk element but the predict-and-prevent aspect. They're fairly new players, and you could call them insurtech firms. They've taken the distribution model and enhanced it with good technology to help with mitigation, identifying the risks and making us more aware of what the risk could be and how we mitigate those risks going forward.

On the enabling side, every industry is looking at AI in a very different way today. They're using enhanced technology to make information much more usable to the industry. I think that's a place where the industry is more likely to partner as opposed to just build themselves.

Could you tell me more about how the new model works in cyberspace?

On the cyber side, the cyber MGAs [managing general agencies] that exist today weren't around 10 years ago. They all came into existence with the entry of insurtech. Most of them came into the industry with some underwriting know-how, but more importantly, they came with technology know-how and tools as well as loss-control features that help provide not just an insurable product but also ways of mitigating the insurance exposure that's out there.

Could you talk about the biggest successes that you witnessed or were involved in, and why you think they worked?

So far, the cyber entrants are a success story. They're more of a success than the beginning days of some of the risk takers that jumped into this space that just didn't get it right. There are very few players that started out as insurtech that made a big impact in the marketplace. I would say there were several failures, more on the full-stack side. When you get to the MGA space, I would say there were more successes. And when you get to the very focused enabling aspect, there were or will be more yet.

You said something that resonated with me partly because my mantra for 25 years, since I started writing about innovation, is: Think big, start small, learn fast. And you talked about how you got involved, at least to dabble, and become aware and participate and learn. How would you recommend people think about innovating now?

The phrase that you used about think big, start small, learn fast resonates with me. But I would say to quit fast, too. If it's not working, you need to pivot or change. Here's where I think insurtech has helped and where legacy companies get it wrong: I think innovation is here to stay. Over these last 10 years, incumbents went all in on innovation, then, little by little, people backed away. When I say back away, I don't mean they're walking away from innovation. Instead, I think their approach changes to let's just use innovation as a constant theme and a constant way of improving the way we deliver our products or service, how we connect with a client, how we underwrite our business, how we mitigate the losses that could affect the business.

Could you tell me more about your vision of prevention?

Predict-and-prevent is a great term. We're in the risk business. We know the current risks. And those current risks are continuing to get more and more complicated and bigger. But we don't know all the risks yet to come. So we need tools that will help us to navigate both are the things that we should be focusing on as an industry and predict those things that could go wrong and build tools or resiliency to mitigate or eliminate them. This is the most important part of the insurance industry’s value proposition.

Any final thoughts?

We are in one of the best underwriting environments that we have seen in the insurance industry for quite some time. And there's still some legs to the strength of this hard market.

This is also one of the times when most traditional companies will spend the least amount of time on innovation and the future. My warning to the industry is, you should always be focusing on the future. Maybe a little bit less or a little bit more in certain markets or cycles, but you should never lose sight of the focus on the future and how you need to deal with what's coming, as opposed to where you are now.

In the end, we are a noble industry that brings people, businesses and communities from harmed to whole because of what we do. No industry plays this role better. But this carries an obligation to continue to look into the future and work on the strategies we will need in place to continue to deliver strong, positive outcomes.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

With drivers concerned about rising premiums, there is a prime opportunity to win them over to telematics.

With car insurance rates rising sharply in the last few years, providers of all sizes will likely be looking for ways to build loyalty and improve customer experiences in 2024.

But that’s a difficult trick to pull off with prices rising across the board. Customers will be looking for competitive prices and discounts, which aren’t easy to offer in our current landscape.

This somewhat concerning trend has also coincided with a more promising one: the rise of telematics devices, which offer a distinct opportunity for providers. However, these opportunities also have their skeptics, as some drivers cite privacy concerns as a reason they’re skeptical about giving telematics insurance a try.

Still, it seems like the tide is turning, and telematics has a chance to make a real difference in the marketplace. Below, we’ve outlined the biggest advantages — and how providers can best communicate those advantages to their customers.

See also: How Better Data Can Turn Auto Insurance Around

The state of telematics insurance

A recent survey found that more than three in 10 policyholders were hesitant to put a tracking device in their car, citing privacy concerns.

Simultaneously, though, a recent study from Mordor Intelligence predicts that the telematics industry will nearly double in market size by the end of the decade.

As the technology and infrastructure around telematics improve, these devices will continually become a more beneficial option for both providers and their customers. However, it’s up to the providers to emphasize those benefits and quell any concerns.

How telematics can help

It’s clear that car insurance customers, already weary from years of rate increases, will be looking for discounts in 2024.

As ValuePenguin’s annual State of Auto Insurance report shows, car insurance rates in the U.S. are expected to rise by nearly 13% this year. Drivers are currently paying $1,984 a year on average — or $165 a month — and those averages will grow by 2025, largely due to extreme weather damage and rising repair costs.

According to a report from Analytics IQ, a majority of drivers considering dropping their provider cite high rates as the main reason.

In this shifting landscape, price comparisons will likely influence consumer behavior more than ever, which is all the more reason that providers need to attract customers with potentially discount-offering policies like telematics insurance.

While not every driver saves money with a telematics device, all drivers have the potential to do so. Plus, these devices can offer drivers the ability to track their own driving and make improvements — simultaneously building loyalty and lowering their accident risk.

Highlighting the benefits

The simplest way to quell any concern is, of course, to highlight the benefits over the costs. Telematics should be presented as an opportunity for customers — a chance to be rewarded for being a good, safe driver.

One of the biggest points of emphasis here is customer control. With telematics, drivers have an enormous say in how much they pay for insurance, which is not true with many other coverage types.

It’s also worth leaning into the gamification of this benefit. Not only can drivers use telematics to lower their rates and improve their driving, but they can track that information in real time — often through something as simple as a mobile app.

A 2023 report from J.D. Power found that digital service satisfaction is the lowest among insurance customers when they can’t find the information they need on an insurer’s app or website. Telematics offers an opportunity for providers to beef up their digital presence, as well as a plethora of easy-to-access information for customers.

Above all, providers should also let the savings do the talking. In addition to emphasizing that telematics lets drivers “control” their rates, it’s also worth detailing the high, high upside for the safest drivers. Including testimonials or examples of especially low customer rates on your website can demonstrate just how beneficial telematics insurance can be.

Leading with transparency

That said, it’s a mistake to address the positives and pretend that the negatives don’t exist. With research showing that privacy is the biggest concern for drivers who are skeptical of telematics, it’s crucial that providers get ahead of these worries by addressing them head-on.

This can be as simple as disclosing exactly what your telematics devices are tracking and what customer data is being used for.

It’s also essential to make sure that disclosure is easily available for customers — shown right below the long list of benefits — and that your employees are briefed on explaining these details in full.

See also: Oops! The Futurologists Were Wrong

Accepting the skepticism

The reality is that some people will likely remain skeptical of telematics for a long time. That’s OK — there are more than 230 million licensed drivers in the U.S., and the majority will gladly accept the freedom and potential discounts over privacy concerns.

But pushing too hard could turn some customers off completely. Ultimately, it’s better to lead with the benefits, address the skepticism and let the cards fall where they may. Telematics doesn’t seem to be going anywhere, and you don’t have to win everyone over in a day.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Divya Sangameshwar is an insurance expert and spokesperson at ValuePenguin by LendingTree and has been telling stories about insurance since 2014.

Her work has been featured on USA Today, Reuters, CNBC, MarketWatch, MSN, Yahoo, Consumer Reports, Consumer Affairs and several other media outlets around the country.

Insurers are funneling $100 billion annually through their litigation departments--and the extent of litigation challenges has yet to fully manifest.

KEY TAKEAWAY:

--The rapid surge in litigation exposure has rendered the term "nuclear verdicts" --typically those exceeding $1 million — obsolete, with "thermonuclear verdicts," exceeding $10 million, emerging as the new benchmark.

----------

Litigation stands as the foremost challenge within the P&C industry. From 2018 to 2023, litigation management costs for the combined P&C sector surged 19%. As detailed in AM Best Financial reports, this escalation is reflected in an approximate $24 billion loss adjustment expense (LAE). According to alternate assessments, the top 50 carriers in the U.S. individually allocated an average of $500 million toward litigation expenses. If we conservatively estimate that litigation expenses represent only a quarter of the total litigation spending, accounting for expense and indemnity, the industry is funneling approximately $100 billion annually through its litigation departments.

However, litigation experts contend that the true extent of litigation challenges has yet to fully manifest. A prominent trade organization has identified combatting legal system abuse as the primary focus for the P&C sector in 2024. In many markets, lawyers have emerged as the dominant advertisers, often yielding substantial rewards in nuclear verdicts, which have now escalated to thermonuclear proportions. The rapid surge in litigation exposure has rendered the term "nuclear verdicts" --typically those exceeding $1 million — obsolete, with "thermonuclear verdicts," exceeding $10 million, emerging as the new benchmark. The consequences of unfettered litigation are exemplified by events such as the world's largest personal injury firm filing an astonishing 25,000 lawsuits in a single week in 2023.

Big tech and Wall Street have taken notice. One software company raised $50 million to use AI to draft demand letters for plaintiffs’ attorneys, and business is so good that one $30 billion technology investment fund just purchased another litigation tech company. Wall Street is deploying hundreds of millions of dollars to remove any obstacles to plaintiff attorneys acquiring as many claimants as possible.

If this continues through 2024, insurers could pump an additional $40 billion directly to their courtroom opponent – plaintiffs’ personal injury attorneys.

What’s next? What’s at stake?

See also: Attorney Involvement Keeps Claims Soaring

Insurance Litigation Today: A System Poised for Disruption

Over the past decade, insurers have increasingly delegated litigation responsibilities, first to attorneys and subsequently to external bill reviewers. The introduction of bill reviewers has since shaped today's industry standard, emphasizing the measurement of adjusters and law firms based on expense rather than value.

While insurers and insurance defense attorneys have grappled with the challenges posed by bill reviews for years, viable alternatives have only recently emerged. At the heart of this issue lies the need for a universally accepted standard for assessing value, with insurers predominantly focusing on cost metrics. Initially, bill reviewers provided a valuable service by scrutinizing expenses, yet insurers have failed to progress to the critical stage of controlling actual outcomes, particularly settlements.

Meanwhile, plaintiffs’ attorneys measure their value by one thing and one thing only: their bank accounts. Plaintiffs’ attorneys are typically paid a percentage of the settlements they obtain.

After decades of rising litigation expenses and little innovation, insurers named this dynamic social inflation. Insurers were able to predict the decreasing performance well enough to stay profitable. So long as insurers could predict the decline in claims litigation and insurance defense quality, they could price it into the premium.

But this incentive structure is powerful enough to end an insurance market – even before the ensuing exponential impact of litigation finance and AI. Over time, plaintiffs’ attorneys push settlements higher and higher and higher. They take 40% of the settlement and reinvest those settlements into more advertising.

Next, plaintiffs’ attorneys leverage the increased income to invest in staff to prolong litigation instead of settling. Armed with an increasing amount of money and people, insurers reinforce this behavior by paying more and more, especially on the courtroom steps. Left unchecked, insurance becomes unaffordable or unavailable, as evidenced by the Florida property market. By the time legislators try to fix everything, the markets could be gone forever.

Within the four walls of a claims litigation department or law firm, you can see with your own eyes how litigation became such a drain on the industry. Defense attorneys are paid by the hour to send emails to adjusters, and adjusters have to copy and paste those emails into claims systems to satisfy regular quality audits.

The average adjuster routinely prioritizes work by email. The insurance defense attorney is paid the same hourly rate, whether productive or passive. For defense attorneys who go rogue and try to win, the external bill reviewers delete significant portions of their income.

As a result, the average insurance defense attorney and plaintiff attorney often do not even begin exchanging serious settlement offers until after a substantial expense is incurred. Insurers typically can use billing data to watch this happen but do not have any other data or tools to control it. Ultimately, some event forces the attorneys to prioritize the case, and they call each other and settle … finally.

Insurance Litigation Tomorrow: Starting With Simplification

In 2023, the national P&C industry was compelled to confront the unfolding situation in Florida, which served as a harbinger of broader challenges emerging nationwide. This prompted a decisive response, with insurers initially turning to AI and predictive analytics to address the burgeoning crisis. However, they swiftly realized that such technological solutions were not the immediate panacea.

The unique nature of litigation, wherein insurers navigate a complex network of numerous lawyers from diverse law firms, with plaintiffs' attorneys often holding sway as the ultimate decision-makers, posed a formidable obstacle to innovation. Any transformative efforts needed to be rooted within the existing system, focusing on optimization from within.

See also: Role of NLP in Claims Management

While the innovation opportunities are complex from a people standpoint, they tend to be simple from a process standpoint:

The Industry Tipping Point: Will P&C Stop Legal System Abuse Before It's Too Late?

Insurance typically undergoes incremental change, not rapid transformation. Yet insurers now find themselves directly confronting the plaintiffs' bar in courtrooms, bolstered by support from Big Tech and Wall Street.

This litigation tipping point isn't your typical insurance issue. While inertia might lead insurers to attempt to predict this crisis rather than prevent it, this level of change isn't easily foreseeable.

Fortunately, insurers confront this challenge in the age of cloud technology. Core systems providers have equipped them with the necessary tools to combat legal system abuse should they choose to do so.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Wesley Todd is the CEO and founder of CaseGlide.

An attorney by trade, Todd has litigated hundreds of cases for some of the largest insurance companies in the world, including USAA, Fireman's Fund, Allstate and Farm Bureau.

Generative AI offers unparalleled opportunities for insurers to enhance efficiency, improve customer experiences and stay ahead.

In the rapidly evolving landscape of the insurance industry, the integration of cutting-edge technologies is reshaping the way companies operate and serve their clients. One such groundbreaking advancement that is set to revolutionize the insurance sector in 2024 is generative artificial intelligence. This sophisticated technology is poised to significantly improve various aspects of insurance, from underwriting processes to claims management.

Generative AI operates on the principle of generating new content, such as images, text or even entire datasets, based on patterns and information it has learned from vast amounts of existing data. This capability has the potential to redefine how insurers assess risks, personalize coverage and streamline operations for enhanced efficiency.

1. Precision Underwriting:

Generative AI enables insurers to conduct more precise underwriting by analyzing extensive datasets to identify nuanced patterns and correlations. This leads to a more accurate evaluation of risks, allowing insurers to tailor coverage to individual policyholders based on their unique circumstances, ultimately optimizing pricing strategies.

2. Enhanced Customer Experience:

The integration of generative AI enhances the overall customer experience by enabling insurers to provide personalized services. From crafting customized policies to offering targeted recommendations, this technology allows insurers to understand and meet the evolving needs of their clients, fostering stronger relationships.

See also: What Generative AI Offers the Insurance Industry

3. Fraud Detection and Prevention:

The insurance industry has long grappled with fraudulent claims. Generative AI's ability to analyze vast datasets and identify anomalies facilitates robust fraud detection and prevention mechanisms. Insurers can identify suspicious patterns, flag potential fraud and mitigate risks before processing claims.

4. Efficient Claims Processing:

Generative AI streamlines the claims processing workflow, reducing the time and resources required for manual assessment. By automating mundane tasks and leveraging predictive analytics, insurers can expedite the claims settlement process, leading to faster and more accurate payouts for policyholders.

5. Data Security and Privacy:

As insurers handle sensitive customer information, data security and privacy are paramount. Generative AI algorithms are designed with advanced security features, ensuring the protection of confidential data. This technology assists insurers in maintaining compliance with evolving data protection regulations and safeguarding the trust of their policyholders.

6. Predictive Analytics for Risk Management:

Generative AI's predictive analytics capabilities empower insurers to anticipate and mitigate potential risks more effectively. By analyzing historical data and identifying emerging trends, insurers can adjust their strategies, minimizing losses and optimizing risk management protocols.

7. Product Innovation:

Generative AI facilitates product innovation. Insurers can leverage this technology to develop new, tailored insurance products that align with changing consumer preferences and market demands. This adaptability ensures that insurance offerings remain relevant and competitive in a dynamic marketplace.

See also: 4 Key Questions to Ask About Generative AI

8. Regulatory Compliance:

Staying compliant with regulatory requirements is a critical aspect of the insurance industry. Generative AI assists insurers in navigating complex regulatory landscapes by automating compliance checks and ensuring adherence to evolving legal frameworks, reducing the risk of penalties and legal complications.

9. Cost Efficiency:

By automating routine tasks and optimizing processes, generative AI contributes to cost efficiency. Insurers can allocate resources more strategically, reducing operational expenses.

10. Industry-wide Collaboration:

The adoption of generative AI encourages collaboration within the insurance ecosystem. Insurers, insurtech startups and technology providers can work together to harness the full potential of this technology, fostering innovation and driving transformations across the industry.

Generative AI is poised to reshape the insurance industry in 2024, offering unparalleled opportunities for insurers to enhance efficiency, improve customer experiences and stay ahead in an ever-evolving landscape. Embracing this transformative technology will be crucial for insurers seeking to thrive in the dynamic and competitive insurance market of the future

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Abhishek Peter is an assistant manager at Fecund Software Services.

Peter possesses a master's degree in marketing.

Navigating these challenges requires strategic foresight, technological agility and a commitment to meet evolving customer needs.

The insurance industry, a cornerstone of financial stability, is confronted with an array of challenges in 2024 that demand innovative solutions and strategic adaptation. As insurers navigate this dynamic landscape, they encounter complexities ranging from technological disruptions to evolving consumer expectations. In this article, we delve into the 10 major challenges poised to shape the trajectory of insurers in 2024.

1. Technological Integration:

Embracing and integrating cutting-edge technologies, such as artificial intelligence and blockchain, remains a top challenge for insurers. Adapting legacy systems to meet the demands of a digital era requires significant investments and a robust change management strategy.

2. Cybersecurity Threats:

With the increasing digitization of operations, insurers face heightened cybersecurity risks. Protecting sensitive customer data from cyber threats and ensuring compliance with stringent data protection regulations are paramount challenges in safeguarding the industry's reputation and maintaining customer trust.

See also: Risks, Trends, Challenges for Cyber Insurance

3. Regulatory Compliance Complexity:

The regulatory landscape is ever-evolving, with changes in data protection laws, financial regulations and environmental standards. Navigating these complexities demands continuous vigilance, adaptation and investment in compliance management systems.

4. Climate Change Impact:

The escalating impact of climate change introduces a new dimension of risk for insurers. From more frequent and severe natural disasters to changing patterns in health and life expectancy, insurers must reassess and adapt their risk models to stay ahead of the curve.

5. Shifting Consumer Expectations:

Changing consumer expectations, influenced by advancements in technology and a demand for personalized experiences, pose a challenge for insurers to stay relevant. Meeting these evolving expectations requires the development of innovative, customer-centric products and services.

6. Talent Acquisition and Retention:

Attracting and retaining top talent remains a persistent challenge for insurers. As the industry undergoes digital transformation, there is a growing need for skilled professionals in data analytics, cybersecurity and emerging technologies, creating intense competition for qualified personnel.

7. Economic Uncertainty:

Global economic uncertainties, exacerbated by geopolitical tensions and unexpected events, pose challenges for insurers in predicting and managing financial risks. Navigating economic fluctuations while maintaining profitability requires agility and strategic risk management.

See also: 20 Issues to Watch in 2024

8. Pandemic Preparedness:

The continuing impact of the COVID-19 pandemic and the potential for future health crises underscore the need for insurers to enhance their pandemic preparedness. Developing resilient business continuity plans and adapting to remote work dynamics are critical aspects of this challenge.

9. Ethical Use of Data:

As insurers leverage vast amounts of data for decision-making, the ethical use of this information becomes a focal point. Balancing the benefits of data-driven insights with privacy concerns and ethical considerations poses a challenge in maintaining trust with policyholders and the broader public.

10. Competition from Insurtech:

The rise of insurtech disruptors presents a significant challenge for traditional insurers. These agile startups leverage technology to offer streamlined, customer-friendly experiences, forcing established insurers to innovate, adapt and explore strategic partnerships to remain competitive.

In conclusion, the insurance industry faces a complex and rapidly changing landscape in 2024. Successfully navigating these challenges requires a combination of strategic foresight, technological agility and a commitment to meet evolving customer needs. By addressing these challenges, insurers can position themselves for long-term success in an industry marked by resilience and adaptability

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Abhishek Peter is an assistant manager at Fecund Software Services.

Peter possesses a master's degree in marketing.

Automated processes, AI-driven solutions and digital platforms enhance efficiency while placing customer satisfaction at the forefront.

In the dynamic landscape of insurance, the claims process stands as a pivotal point where customer satisfaction is either strengthened or compromised. As technology continues to evolve, insurers are leveraging innovative solutions to reshape the claims experience. In this article, we explore 10 groundbreaking ways technology is revolutionizing the claims journey, ensuring efficiency, accuracy and enhanced customer satisfaction.

1. Automated Claims Processing:

One of the key advancements in reshaping the claims experience is the implementation of automated claims processing systems. Using artificial intelligence (AI) and machine learning, insurers can reduce processing times and minimize manual errors.

2. AI-Powered Fraud Detection:

Technological advancements enable the integration of AI algorithms for sophisticated fraud detection. By analyzing patterns and anomalies in claim data, insurers can identify potentially fraudulent activities, safeguarding against financial losses and maintaining the integrity of the claims process.

See also: 5 Ways Generative AI Will Transform Claims

3. Digital Documentation and Imaging:

The shift toward digital documentation and imaging has significantly enhanced the efficiency of claims processing. Mobile apps and digital platforms allow policyholders to submit photos and documents related to their claims, expediting the assessment process and providing a seamless user experience.

4. Blockchain for Transparency:

Blockchain technology is making waves by providing a secure and transparent platform for claims processing. With distributed ledger technology, insurers can create an immutable record of claims, reducing disputes and enhancing trust between insurers and policyholders.

5. Telematics for Accurate Assessments:

Incorporating telematics data from connected devices, such as IoT-enabled vehicles, enables insurers to obtain real-time information for more accurate claims assessments. This data-driven approach ensures precise evaluations, leading to fair and prompt settlements.

6. Chatbots for Instant Support:

The integration of chatbots in the claims process offers policyholders instant support and information. By leveraging natural language processing, chatbots can answer queries, guide users through the claims submission process and provide timely updates, enhancing overall customer satisfaction.

7. Predictive Analytics for Risk Assessment:

Technology enables insurers to employ predictive analytics models for more accurate risk assessments. By analyzing historical data and patterns, insurers can identify potential risks, allowing for informed decision-making and risk mitigation strategies.

See also: Making the Claims Process More Efficient

8. Mobile Claims Tracking Apps:

Mobile apps dedicated to claims tracking empower policyholders to monitor the status of their claims in real time. Providing transparency and accessibility, these apps enhance communication between insurers and customers, fostering a more collaborative and responsive claims experience.

9. Augmented Reality for Property Claims:

In property insurance, augmented reality (AR) is transforming the claims assessment process. Insurers can use AR to remotely assess damages, enabling quicker decision-making and reducing the need for on-site inspections, particularly in emergencies.

10. Personalized Communication Platforms:

Technology enables insurers to implement personalized communication platforms that cater to the individual needs of policyholders. Tailored updates, alerts and guidance throughout the claims process contribute to a more engaging and customer-centric experience.

Technology is undeniably reshaping the claims experience in the insurance industry. The integration of automated processes, AI-driven solutions, and digital platforms not only enhances efficiency but also places customer satisfaction at the forefront. As insurers continue to embrace these technological innovations, the future of claims processing promises a more streamlined, transparent and customer-friendly journey

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Abhishek Peter is an assistant manager at Fecund Software Services.

Peter possesses a master's degree in marketing.

It may require a 50X increase in processing workloads, which means P&C insurers need a modern, cloud-based infrastructure.

Over the past year, generative AI (or GenAI) has hijacked the technology agenda in every industry—including P&C insurance. Given its ability to generate virtually any form of content based on the inputs it's trained on, a potentially endless number of GenAI use cases in P&C insurance span distribution, underwriting, claims and beyond.

The enthusiasm is palpable. Today, 59% of large insurers are actively experimenting with GenAI, with most running up to 15 different proofs of concept or early-stage prototypes. The payoff could be huge: According to McKinsey, generative AI could help unlock up to $1 trillion in annual value for the insurance industry worldwide.

Yet as the transition from conceptual to operational accelerates in the months ahead, insurers will face formidable challenges. GenAI-enabled fraud, increased government scrutiny and any number of legal complications will threaten progress. Yet many carriers will discover the most significant hurdles will stem from the practical realities of supporting and leveraging generative AI to its fullest potential.

For some, these obstacles could derail their efforts to harness GenAI to their competitive advantage. For others, the hype surrounding this technology will give way to a more pragmatic approach that enables them to make full use of what is arguably the most consequential technology of the next decade.

P&C Joins the GenAI Revolution

To understand the dynamics in play, let's start with the basics. generative AI is a subset of deep learning that leverages sophisticated algorithms to digest vast amounts of structured and unstructured data, learn patterns and generate original content—including text, audio, images, video and code. If early signs are any indication, generative AI has the potential to unleash a whole new level of human productivity.

GenAI isn't new—its foundations and the large language models (LLMs) it uses trace back to at least the 1960s. The public release of OpenAI's ChatGPT in November 2022 catapulted generative AI into the popular imagination. By December 2023, a survey found that 76% of personal lines and 79% of commercial lines carriers were either studying or piloting GenAI applications in their operations. What they're learning is eye-opening.

See also: 4 Key Questions to Ask About Generative AI

Generative AI Use Cases: Unlimited

According to Celent, 84% of senior insurance executives expect to gain a sustainable competitive edge from their investments in this technology. But that's predicated on identifying the most compelling use cases for GenAI, from transforming distribution and underwriting processes to revolutionizing claims handling and more.

Coaching or "co-piloting" agents through the sales process for complex products like cyber or summarizing submission data to streamline underwriting workflows have emerged as some of the most promising applications. So has synthetic claims analysis to identify opportunities for new lines or potential enhancements to existing ones. But as many carriers are learning, identifying advantageous use cases is one thing. Implementing the requisite infrastructure and data ecosystems to support them is another. That's where the reality check comes in.

The Critical Role of Cloud-based Infrastructure

Infrastructure considerations are paramount to leveraging generative AI's full potential. For one thing, diverse and continuously refreshed datasets are required to train GenAI for use cases throughout the insurance life cycle. As Forbes reports, a single model must often span multiple servers and accelerators to execute a trained language models that may have billions of parameters.

This level of complexity requires an average 4X improvement in hardware computing performance and a 50X increase in processing workloads. Most organizations won't have the appetite for the investments and overhead needed to support that kind of performance on their own. Nor is it likely they'll be successful if they did.

According to Deloitte, a modern, cloud-based infrastructure is required to support and scale the computational demands of GenAI applications. Insurers will need one that combines core, data and digital to integrate with and interpret data from an expanding ecosystem of data partners and make it actionable.

Governance Takes Center Stage

As the industry navigates the complexities of GenAI adoption, governance will become the linchpin in ensuring effective and responsible deployment. Establishing frameworks for data privacy, security, transparency of training data and compliance with evolving regulatory mandates will be business-critical.

In view of these needs, look for more insurers to establish centers of excellence (CoE) to oversee GenAI implementations. For each use case, the CoE must define factors such as: Who is the user? What is the user experience? What data and functionality are they permitted to access—and why?

There's also another critical dimension. Making GenAI truly effective and empowering means giving the people using it—employees, customers, partners—an understanding of how it's being used and what data serves as its inputs. In coming months, look for regional insurers to learn that, like their major carrier brethren, they must tap multiple large language models simultaneously to corroborate output details and prevent AI "hallucinations" that can reinforce biases or lead to errors.

See also: 5 Ways Generative AI Will Transform Claims

Human + GenAI: The Future of the P&C Workforce

GenAI's most promising P&C use cases should showcase another reality: This technology isn't about replacing human roles. It's about empowering them. Humans with domain expertise are needed to identify use cases and develop, test and deploy GenAI-enabled applications. A human-in-the-middle must also vet AI-produced output for factual errors and bias.

According to McKinsey, leaders must take a broad view of GenAI's capabilities and deeply consider its implications for workforce needs. Training and upskilling will be required. So might new roles such as AI trainers, interpreters and ethicists.

According to a recent study published by Harvard Business School, it's well worth the investment. Designed to measure the impact of AI on knowledge work, the study found that teams using AI completed 12% more tasks on average, completed them 25% faster and produced 40%-higher-quality results than those not using AI. Better still, workers with the lowest scores before the study saw the most significant jump (43%) in performance when they could use AI—suggesting the technology works as a skills leveler.

The Road Ahead: Embracing a Pragmatic Approach

As the industry moves forward, a checklist approach can guide insurers in refining their strategies for generative AI:

The transition from irrational exuberance to reality will not be easy for some carriers. But it will be necessary. With more than $1 trillion in annual value at stake, insurers that refine approaches, focus on governance and foster human-GenAI collaboration won't just safely navigate the near term—they'll shape the future of insurance.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Laura Drabik is Guidewire's chief evangelist.