Prevention in Modern Underwriting: How to Shift from Reactive to Proactive Risk Management

Traditional underwriting still relies heavily on historical claims data. As a result, risk management can only be reactive, acting “after the fact”. As we face an industry where margins are tightening and climate-related risks are growing, this reactivity is no longer enough. Proactive risk management, which heads off these losses before they occur, rather than responding after the fact, is critical.

Below, we look at how prevention technology is transforming underwriting and how using a service like bolt’s Prevention Technology helps reduce loss frequency before it happens.

Traditional Reactive Models: Challenges We Need to Escape

In the insurance industry, traditional underwriting models rely mostly on historical claims data to predict future risk. While this retroactive approach served us well for many years, it no longer addresses some critical modern realities. Underwriting innovation, especially in prevention technology, is essential to reinvent how we think about doing business in insurance.

The reality is that many losses are preventable – if consumers are using the right technology to alert of potential risk. Data-driven underwriting and predictive insights in insurance open up many new possibilities.

Consider these sobering statistics:

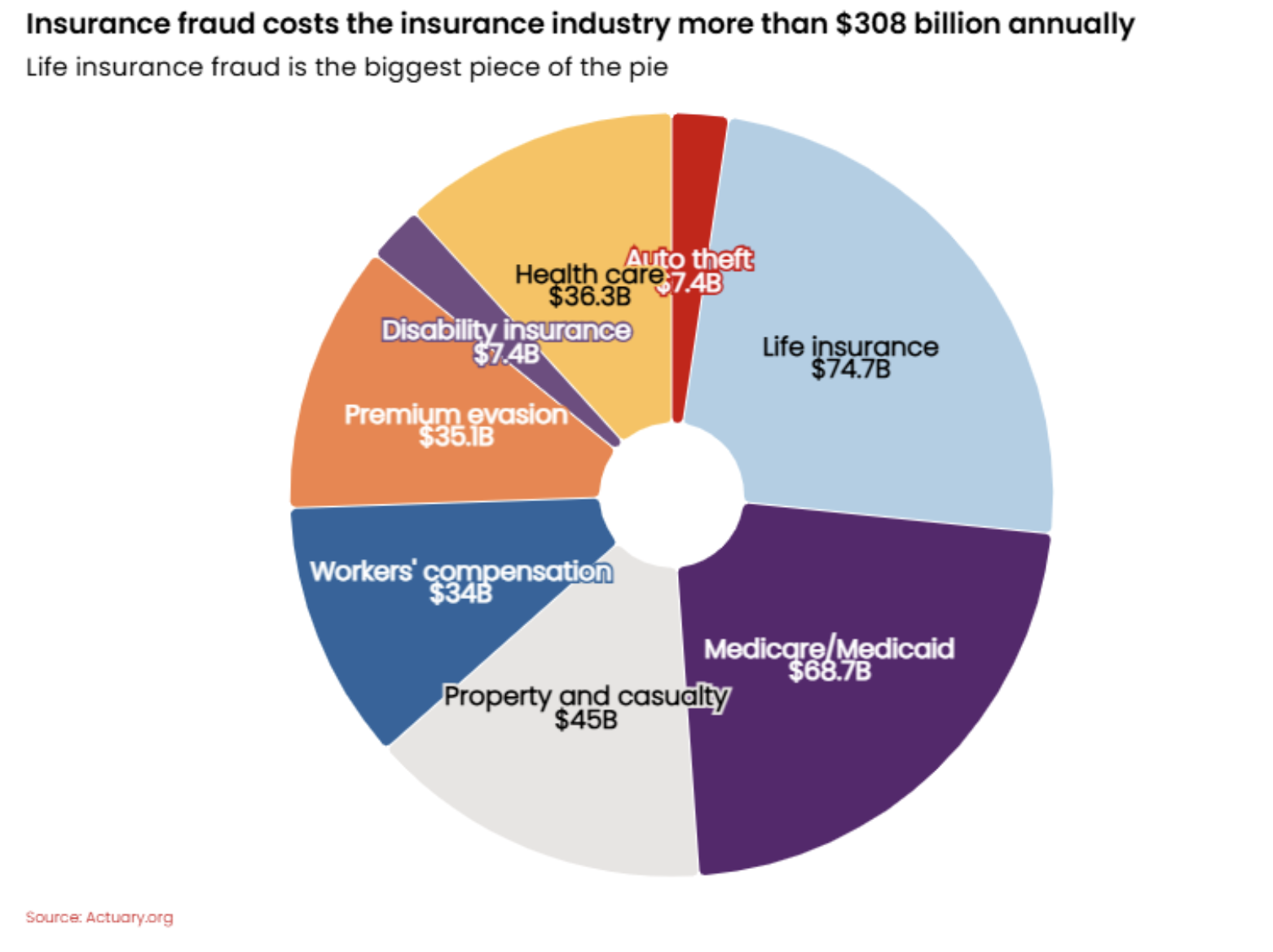

- Water damage comprised close to 24% of all US homeowners’ insurance claims, with 32% noting they’ve experienced an “adverse weather event” over the last five years.

- On average, these damage claims exceed $12,500 per event, costing insurance companies more than $13 billion annually.

- Water/freezing damage is the second most frequent claim after wind and hail damage.

Then there’s the real kicker: weather-related catastrophes where damages cross the billion-dollar mark have risen from 3.3 events per year to more than 17 annually since the 1980s.

There’s a pressing need for underwriting innovation, as this escalation exposes the weaknesses in traditional insurance risk selection processes. The missing key? Real-time visibility as risk conditions evolve. If underwriters are confined to assessing risk at only a single point in time – such as when policies are taken out or renewed – they have no chance to influence risk outcomes over the policy lifecycle.

New Proactive Risk Management: The Solution to Traditional Underwriting Weaknesses

Proactive risk management is a key facet in modern underwriting innovation. And it’s being driven by new technology offerings. Traditional underwriting and its dependence on historical claims data fails to address preventable losses, driving up claim severity and frequency.

However, by integrating real-time monitoring, IoT sensors, and better use of predictive data, underwriters can help prevent claims – before they occur. This proactive risk management helps to return profitability to underwriting, reducing claims costs and allowing more accuracy in pricing strategies.

IoT Sensors in Underwriting

Until now, we’ve only had historical data to rely on. With the growth of the Internet of Things, or IoT, underwriters can now benefit from continuous and real-time information about insured assets or properties.

Smart sensors, for example, detect early warning signs of potential damage, such as water leaks or frozen pipes. They can even detect subtle issues, like electrical anomalies and structural weaknesses. This helps facilitate intervention before minor issues become major claims.

There’s significant interest in using IoT sensors in underwriting, alongside other AI-powered solutions. Even in 2019, 44% of the Top 100 insurers had already introduced this kind of intelligence into their operations, with 39% piloting it actively. Large residential property insurers indicated a massive 70% were interested in these solutions. However, while 42.8% of those using machine learning have already implemented it for auto insurance, there are only 8.6% who can say the same in home insurance.

However, real-time sensor data can improve damage assessment accuracy by up to 40%, reduce fraud by roughly 35%, and cut claims processing time by up to 50% while improving response times by as much as 70%.

But this level of impact is only achieved in an actively managed program. Otherwise, the carrier is reliant on self-selection by engaged policyholders, which limits results. Bolt has found that with managed engagement and rapid response it is possible to meaningfully lower non-weather water risk. In fact, our revised rate filings show a three to eight times increase in effectiveness compared to passive approaches.

Data-Driven Underwriting

Data is king for effective underwriting. Being able to bring data from connected devices alone has value, as we noted above. Now add the ability to crunch data on weather patterns, analyze building specifications, and even introduce data on behavioral indicators.

Together, this gives underwriters embracing underwriting innovation almost unprecedented insights into risk profiles. With these predictive insights in insurance, carriers can more accurately segment customers by:

- Identifying high-risk properties that may appear deceptively “normal.”

- Recognizing low-risk properties that conventional underwriting may misclassify.

- Developing dynamic pricing strategies, reflecting real-time risk conditions.

- Incentivizing (and rewarding) risk-reducing behaviors among policyholders.

Prevention Technology in Action with bolt

This growing need for proactive risk management and smarter underwriting innovation was one of the key drivers behind bolt Prevention Technology, which integrates seamlessly into underwriting, claims, and even policy workflows, offering actionable risk insight to reduce water-related losses at every step.

bolt Prevention Technology has been proven to decrease water loss claim frequency by 39% and severity by 12%, helping insurers cut costs and improve profitability. As bolt CEO, Jon Walheim, notes, many sensor programs fail to drive policyholder engagement or integrate risk insights directly into carrier workflows.

Historically, it has been challenging to unite sensor adoption and policyholder engagement for sensor providers alongside carriers. What sets bolt Prevention Technology apart is the ability to leverage bolt’s integration to carrier systems create our unique and effective loss mitigation experience. We help insurers bridge that gap, ensuring actionable prevention data, targeted follow-ups, and better compliance, leading to lower risk and measurable claim reduction for better underwriting performance.

Additionally, bolt Prevention Technology provides automated notifications and guidance, ensuring sensors are used properly to minimize non-compliance and remove inactive devices. Carriers can also work with a range of sensor partners, allowing insurers to customize and scale as needed by different risk profiles.

With simple integration into existing underwriting workflows, there’s no need to overhaul operations. bolt’s Prevention Technology will fit into current processes, offering new prevention capabilities through:

- Stronger Risk Selection: Identify optimal candidates for prevention programs, using property characteristics and risk algorithms.

- Dynamic Risk Assessment: During the policy lifecycle, real-time data allows carriers to update risk profiles continuously, for more precise policy administration.

- Pricing Optimization: Using relevant and specific data for each property or asset helps keep pricing optimized and realistic.

- Risk Intervention Opportunities: Education and adoption change the fundamental risk profile as sensors increase awareness and can detect policy impacting concerns, then automatically alert policyholders so minor issues don’t escalate.

- Claims Integration: In the event of a loss despite these preventative measures, data history offers adjusters the insights they need to streamline the claims process and carriers insight to future prevention.

Using tools like bolt Prevention Technology to foster proactive risk reduction alongside underwriting innovation helps insurers deliver value throughout the insurance lifecycle. The result? Improved outcomes for both carriers and customers.

Implementing Proactive Risk Management in Your Underwriting Strategy: Actionable Steps

For carriers looking to improve their proactive risk management, the path can seem overwhelming. However, with the help of bolt’s Prevention Technology, implementing predictive insights in insurance needn’t be a headache.

We suggest that carriers start by assessing their portfolio to identify where the highest loss ratios or more preventable claims occur. For many, that will be water damage in residential properties, as we’ve examined, and also specific commercial risk segments.

From here, carriers can launch targeted pilot programs, establishing clear data metrics to track success across financial and customer experiences. Next, look at working with a prevention partner like bolt, with the experience to integrate our technology with existing policy management or underwriting systems.

Lastly, make sure underwriters are equipped to incorporate this prevention data into their existing decision-making, and look to developing pricing structures to incentivize and reward policyholders for participating in prevention programs and keeping their risk low.

Embrace a Preventative Future with Proactive Risk Management and Data-Driven Underwriting

The shift to proactive risk management is set to transform how the industry thinks about underwriting. Reducing loss frequency isn’t just about carrier profitability, although that’s always a compelling side effect.

When carriers embrace predictive insights in insurance, they shift from being a “pay platform” that only reacts after disasters to being active partners in risk mitigation.

As claims escalate in severity and climate risk intensifies, carriers who wish to thrive need to move past reactive models and embrace the power of prevention through underwriting innovation.

If you’re ready to take your underwriting from reactive to proactive, bolt can help you integrate prevention technology into your workflows hassle-free. Learn more about bolt Prevention Technology, or contact us for a demo today.

Sponsored by ITL Partner: bolt