As we live in an era of technological boom, it is increasingly difficult to separate hype from reality. With so many breakthroughs in medicine, space exploration and even autonomous driving, it is not advisable to bet against even the boldest of efforts. So, perhaps humans will indeed live on Mars one day. In recent times, the naysaying against hype is generally about the when it will happen, less about the if it will happen.

The P&C insurance space has seen its share of hyped concepts like blockchain and virtual reality but none as much as the recent exuberance for AI. And for good reason. Insurance practices are largely about information gathering and validation, whether for underwriting, claims or risk management. Actuarial mathematical sciences are applied for trending and pricing. Internal functions and external processes are just a few ways to describe insurance at-a-glance. All of which may benefit from AI tools and agents near-term and into the future. Insurance talent shortages, high costs of insurance for consumers and businesses, changing risks, demand for loss prediction and prevention are just some of the bigger challenges in which AI may come to the rescue.

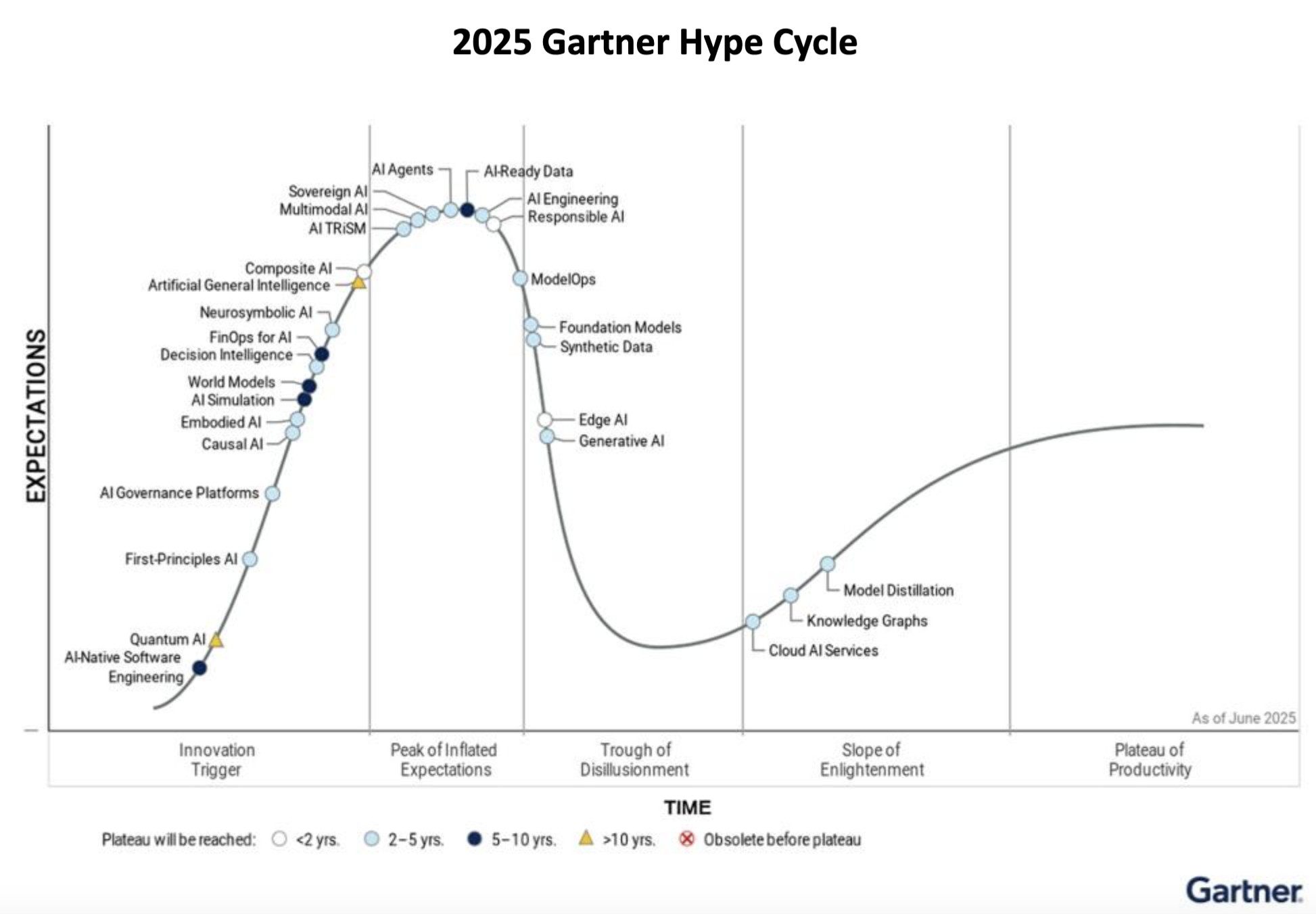

The Gartner Hype Cycle

Most of us are familiar with the Gartner Hype Cycle, a visual model that illustrates the maturity, adoption, and social application of a new technology, charting its progression through five key phases. It provides a framework to guide technology investments by showing when a technology's actual value becomes clearer, helping organizations reduce risks and make informed decisions about when to adopt emerging technologies. As valuable as it has been, the arrival of AI technologies may challenge its relevancy.

References to AI and related application are impossible to avoid, which could lead many of us to conclude that we have moved from the Peak of Inflated Expectations and are approaching the dreaded Trough of Disillusionment in the Gartner Hype Cycle (see below).

Indeed, edge AI and generative AI have just barely entered this phase in Gartner's 2025 report.

However, it is our contention that many other uses of AI – including AI agents and decision intelligence, in insurance and beyond – could defy the history of new technologies and collapse the model, skipping right over or compressing the trough and moving straight on to the Slope of Enlightenment and the Plateau of Productivity.

This is not to say that AI adoption – we could call it commercialization at scale – is not without plenty of headwinds. Regulators and lawmakers are expressing ethical and data privacy concerns. Labor unions, service, and information workers are concerned about employment security. Insurance carrier adoption for all new technology is often quite slow, and AI is demonstrating the highest scrutiny ever. Data privacy, legal exposure and brand protection are front of mind among insurers. As legitimate as these concerns may be, collectively, they underscore the huge potential for disruption that these technologies represent.

The insurance industry is among the earliest adopters of AI, although the use cases are still somewhat basic and not yet delivering material returns. But we caution carriers not to allow these early experiences to discourage greater investment and research – the potential returns cannot be ignored, and moreover neither can the competitive market advantages.

International Insurance Society Report Identifies the Rapid Rise of AI

The International Insurance Society, which is affiliated with The Institutes, collaborated with The Institutes along with several affiliates, including the Insurance Information Institute, Insurance Thought Leadership, and Pacific Insurance Conference, on this survey.

According to their just released report, in 2025, artificial intelligence (AI) has emerged as the single most important priority among industry executives, surpassing inflation for the first time in recent years. Two-thirds of executives now place AI at the top of their technology and innovation agendas, representing a steady climb from just 17% in 2021. This accelerated focus is driven by the growing realization that AI can streamline operations, enhance data analytics, and open avenues for product innovation, all of which are seen as critical for staying competitive in an evolving business landscape.

One executive described the benefits of AI to their bottom line: "These tools enhance forecasting capabilities by allowing for deeper insights into trends and potential future risks. By empowering themselves with robust analytics, organizations can improve their strategic planning and risk management efforts, ultimately driving better business outcomes."

P&C Observations on AI Adoption

The following is a snapshot of what we are seeing and hearing from carriers and others:

• Insurers are embracing the concepts of AI to benefit in several areas, including risk selection, underwriting, operational efficiency, and cost management. Claims and underwriting tend to be the most often cited insurance use areas

• C-suites are promoting and setting mandates to advance AI agendas with a "let's not get left behind" mantra

• The variety and number of use cases for nearly every insurance function from product development to distribution and service are remarkable and optimistic

• Internal insurance carrier governance panels tend to narrow, halt and perhaps appropriately stall expansion of use cases due to data security and privacy, legal, and reputational harm risks, along with anticipated future regulatory controls

• AI for insurance encompasses a wide range of types and usage, including computer vision, generative, conversational (chatbots), agentic, and predictive

• Document review and summarization is a particular and popular use, e.g., medical records, demand packages, and legal documents

• Other areas of use include risk section, CAT modeling, claim case escalation, visual damage evaluation tools, reserving, insurance sales, and numerous internal processing functions

• Carriers are mixed in terms of buy vs. build, with most doing both by partnering with AI solutions firms and building proprietary solutions

• There is an abundance of "AI solution" providers with .ai in their URL or otherwise in marketing material, making it extremely difficult to distinguish

• Insurers are highly protective when contracting with vendors and providers, focused on data security and privacy and buckle down on AI usage, data access and related items

• Demands on people, including AI knowledge, skills and capabilities, are understated when it comes to change management

Regulators and AI

The National Association of Insurance Commissioners (NAIC) has introduced model guidance and regulations for the use of artificial intelligence systems by insurers, which have been adopted by 24 states (see NAIC Model and NAIC Model Adoption Map).

The April 2025 Genpact Consumer AI Study reveals that a majority (55%) of U.S. adult respondents feel neutral about their insurance companies using AI, and 25% view it negatively. However, when AI delivers tangible benefits – such as faster and more accurate claims processing, customized quotes, and improved customer service – customer acceptance increases significantly. The findings emphasize an opportunity for insurers to shift perception and build preference and trust with their customers.

"As insurers embrace AI to enhance operations or customer experience, they must ensure that every interaction – whether human-led or AI-powered – meets or exceeds customer expectations," said Adil Ilyas, global business leader for insurance at Genpact. "This research highlights AI's potential to transform insurance, but also the need for insurers to close experience gaps and communicate transparently to build trust and loyalty."

Recommendations for P&C Industry Leaders

Prioritize governance and model risk management now. Regulators and plaintiffs are focused here — being proactive protects both customers and the balance sheet.

Focus first on high-value, low-risk gen-AI deployments (internal productivity, document summarization, FNOL assistance) while building the data and MLOps backbone.

Treat vendors and foundation models as concentration risk — strengthen contractual, privacy and incident response clauses.

Measure outcomes, not just outputs — track bias metrics, appeal reversal rates, customer satisfaction and financial key performance indicators (KPIs)

Plan for regulatory change — assume more granular supervisory questions and state/federal enforcement in the short term.

Disclosure and Transparency

We employed ChatGPT to gather some of the facts for this article, which itself is validation of our premise that AI is becoming pervasive and is too valuable to ignore for certain tasks. We believe that any published work should include an AI disclosure statement. When used in conjunction with the author's own experience, informed insights, common sense, and ethical judgement, it feels like AI could help make it an exciting future.

Even though insurance AI hype exceeds measurable uplift at the moment, it is our view that AI is not just another technology bubble. AI in insurance holds tremendous potential to ultimately solve the many worsening gaps and challenges in the insurance model.

Waiting for regulatory clarity or delaying to completely de-risk AI may prove to be a detrimental path with first movers having an insurmountable advantage.