Culture is often cited to explain why innovation does not work in insurance. We start by defining what culture is before delving into how a culture is born, why it matters and finally how to create a culture of innovation.

Culture: A Definition

Alfred Kroeber, together with Clyde Kluckhohn, conducted a comprehensive review of the concept of culture in their influential 1952 work, Culture: A Critical Review of Concepts and Definitions (Exhibit 1). In this opus, they identified and analyzed 164 different definitions of culture from various academic sources up to that time.

Culture proves to be an elusive concept if it takes 164 definitions to delineate it.

My favorite, a 165th one: Culture is what is left once we have forgotten everything else. It is the way we are hardwired, our values, the way we behave, how we define right from wrong without even thinking about it.

In Japanese, Atarimae (obvious, evident) would be the closest to that notion of culture. Atarimae explains why we can see Japanese fans cleaning up after themselves (and helping others) in a sporting arena, without being invited, asked, provided incentives or coerced (Exhibit 2). It is just a habit, what they do.

Exhibit 1: 164 definitions of Culture

Exhibit 2: Atarimae in action

How a Culture is Born

Culture comes from the agency we have in deciding how we adapt to our environment.

For instance, the Inuit, living north of the Arctic Circle, adapted to polar living conditions by building igloos (ice houses), have multiple words to describe snow based on its different qualities, and hunt and eat food in a way suitable to surviving and thriving in subzero temperatures. In a word, they developed a culture. They could have chosen to move south and would have developed a different culture.

In a corporate environment, culture is the agency we have in the way we choose to adapt to our environment. And our environment is the sum of processes, behaviors, rules, and values we see in action. It is not what we say. It is only what we do. And what we witness others doing. That makes the culture, the norm. Therefore, a culture is born from a structure and the way we choose and see others adapt to it.

Culture is not to be found in a mission statement, and the best proof of that is most mission statements of most corporations look alike and promise a wonderful world where we all respect each other, our customers and of course the planet. If so, why global warming? Why is insurance not more innovative despite all insurance companies professing they are?

Culture is what we do, not what we say.

Doing innovation therefore is not a matter of culture; it is only a matter of structure, until it becomes second nature, atarimae, then it becomes culture. To create a culture of innovation, we simply need to focus on the structure, on how we work and how we get things done.

Why Culture Matters

As inferred in our favorite definition of culture, it underpins what we do, how we do it, why we do it without thinking—in short, a habit. Culture is the single most powerful way to get a group of people to behave, pursue a common goal and succeed in the process. Exhibit 3 underlines how important culture is. It may not "eat" strategy as they both cohere. Technology is the enabler.

Then why does innovation matter?

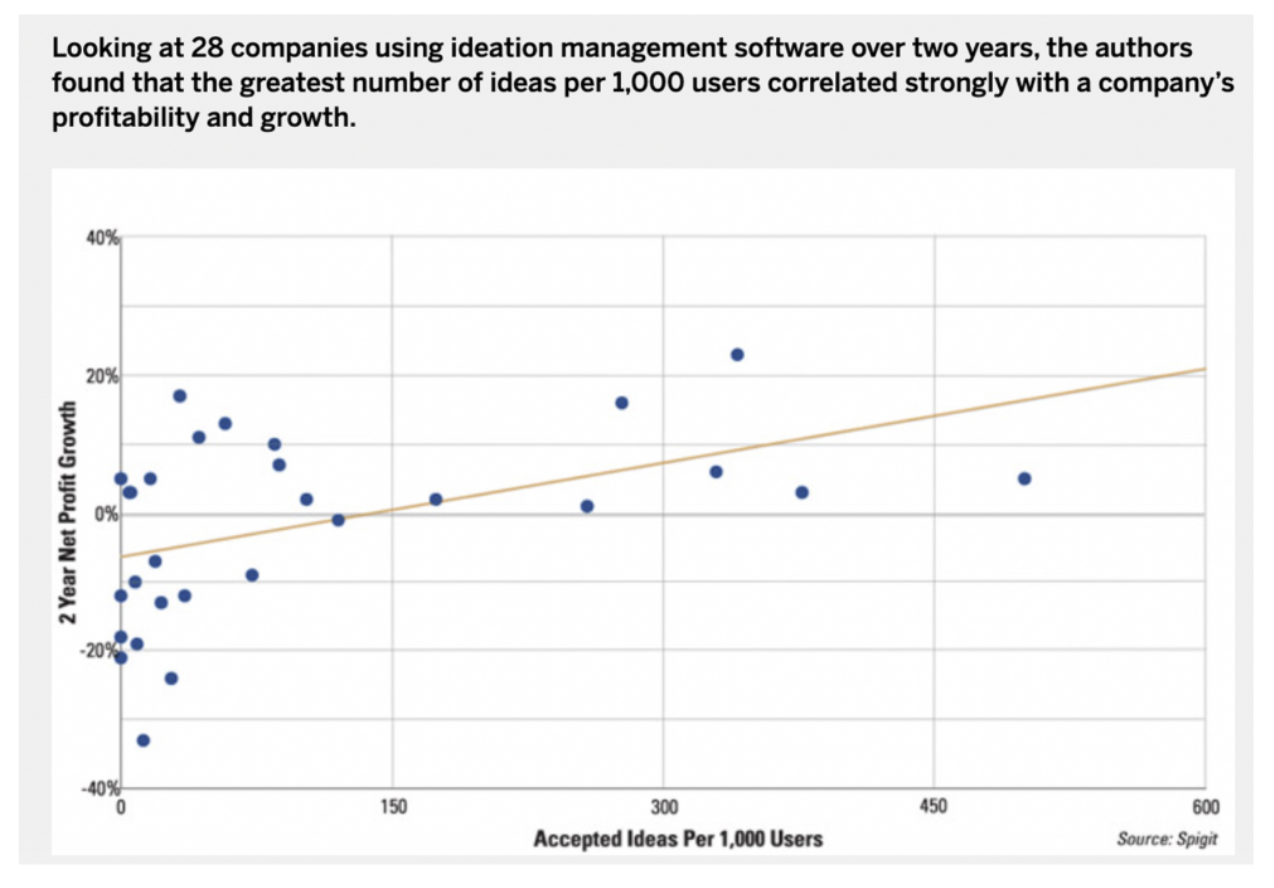

Research demonstrated a correlation between the highest numbers of accepted ideas and profit and growth (Exhibit 4).

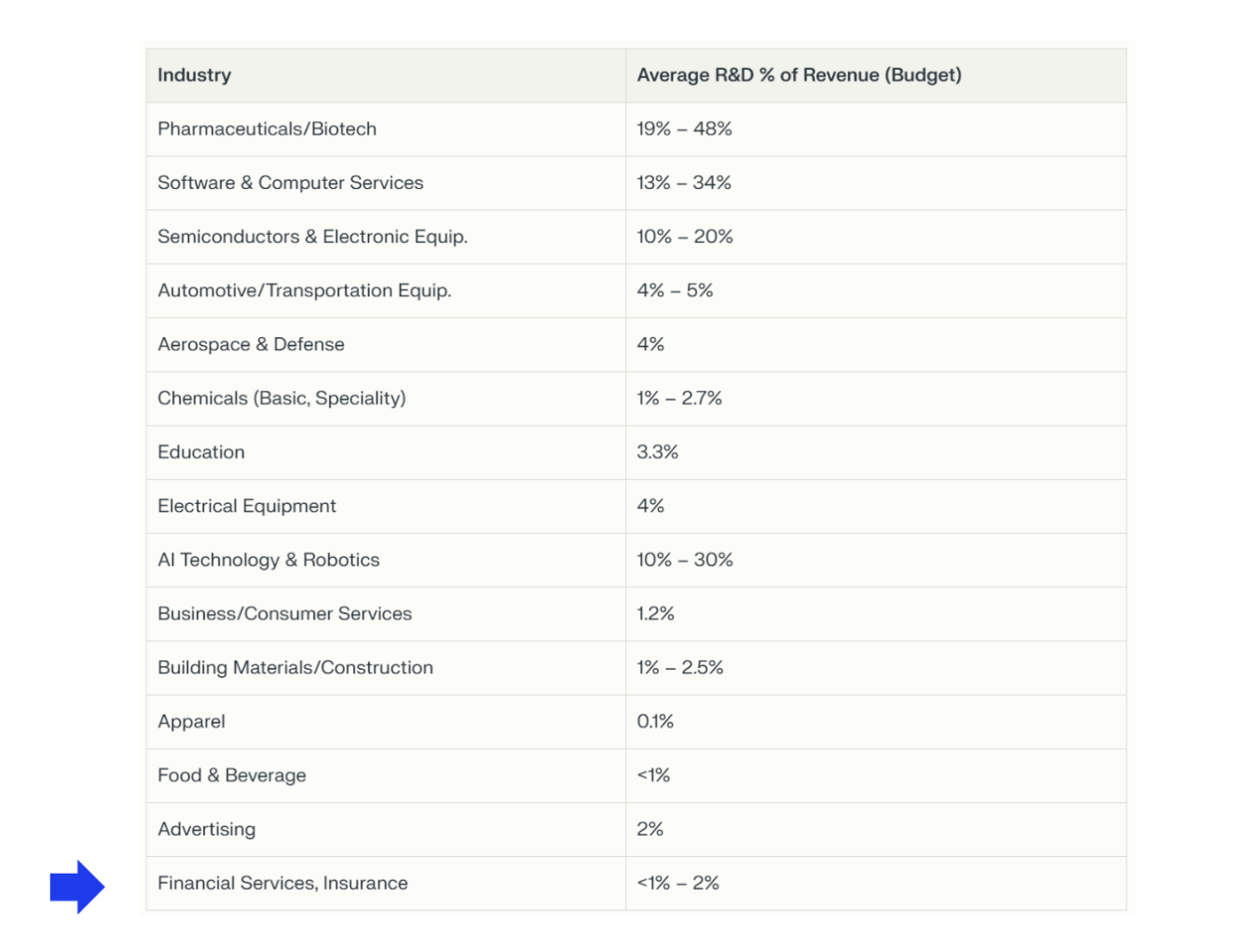

And looking at the percentage of revenue invested in innovation, insurance comes among the last compared to other industries. Of course, selling a product versus a service does not entail the same magnitude of budget. The point is some industries are built and judged by the market based on their future products and therefore their innovation as a sign for future earnings. Innovation makes tomorrow's profit.

To be noted, MAPFRE made a public commitment to dedicate 1 percent of its revenue to innovation in 2018.

Exhibit 3: Why culture matters

Exhibit 4: Profit & Growth is correlated with more accepted ideas

Exhibit 5: Insurance among the last industry in percent of revenue dedicated to innovation

How to Create a Culture/Structure of Innovation

First, innovation may be the job of a few (innovation team), but it is the work of every employee.

What good does it do to give an innovation team innovation objectives if everyone else in the company does not have the same objective? To be innovative, everyone in the company must be innovative.

It means everyone must be held accountable for innovation objectives. How is that usually done in a corporate environment? Through performance reviews, constant feedback, coaching enforced through rewards and correction, carrot and stick.

Absolutely everyone. Not just underwriters, sales, claims, operations. But also legal, compliance, governance. Gatekeepers must be held accountable for innovation; otherwise, every endeavor will end at their door. We would have only pushed the buck from innovation teams to business teams if we do not include governance. Now the job of governance is also to innovate, to balance profit and loss, risk and opportunity.

Balance is the key word in regulated industries. The more we sell, the more risk we take. It needs to be balanced. But it is not putting innovators against gatekeepers. Everyone is an innovator and a gatekeeper.

Start small. What have you done this year to be more efficient (transformation) and improve our relevance in the market (innovation)? Count initiatives first, then count their impact in dollars as innovative measures mature. Just that for everyone would promote innovation when rewarded and corrected. There are no rules without enforcing them.

Second, how to actually create something new or work better. This is where the innovation team would help connect goals and pain points with solutions from an ecosystem of innovative partners.

There is no build, partner or buy in open innovation. It is partner first, buy or build next. Only partnering ensures quick development, cheaper cost and provides a benchmark to emulate to build later on or buy.

Business teams are transactional in nature, whereas innovation would require total commitment from vision to execution, working in an agile fashion with a deadline. As a result, business teams have a hard time building and dedicating resources to innovating. But they can eventually take on a dynamic partner to help them achieve their goals, rather than accruing IT legacy debt. For instance, as a chief underwriting officer, I wanted to pilot my portfolio of business effectively across 50 countries. IT suggested launching a 250-page RFP. I opted instead to work with a nimbler company then, QlikView, to design the portfolio features I needed without having to change the IT infrastructure. In less than a year I could make portfolio decisions at the click of a button that would have otherwise required three days of manual work. Quick, cheap, no legacy debt to amortize and effective (one click vs. three days per request).

Partnering is still work, but instead of building from scratch what already exists, teams can focus on the personalization layer with a partner, truly making a solution their own.

Third, any initiative needs to be aligned with strategy and with a senior sponsor signing off on it. Commitment from the business is required. Therefore, an innovation budget shall never fully fund any initiatives, only 30 percent at the most. The rest comes from the business.

Fourth, innovation is unprecedented change. Change is hard. Unprecedented change is harder. Innovation is also iterative. Thomas Edison indicated that he found 10,000 ways that did not work to create the light bulb. So failure at launching an innovation is still learning if we keep going and learn from it.

The point is quick learning matters, and the lines between success and failure have to be redrawn for innovative endeavors. The assessment therefore is on the learning and next steps more than on the failure to launch. The failure is on not starting and on not finishing.

Fifth, people can be trained on innovation. Many tools exist to uncover ideas: job to get done, extreme user analysis, ethnography, persona, user journey, assumption checker, value proposition canvas, etc. Lack of skills can be remediated. Lack of will and commitment may not, unless innovation is enforced through the structure. Freedom to explore tends to be a challenge for business teams that innovation teams can answer.

Sixth, innovation is a portfolio to articulate between horizon one, two, three. If horizon one and two require a good connection between innovation and business teams, horizon three can be the prerogative of innovation teams, projecting future activity in new business models, distribution and new ways to define the corporation. In a life environment, I call that the "meaning of life" or how to be a life player rather than a mere life insurer. After all, Daiichi is called the Daiichi Life Group, not Life Insurance Group. And a life, as defined by policyholders, has multiple dimensions not addressed by a life insurance policy: caregiving to ascendants, descendants and pets, grief management including of pets, prevention, early detection, longevity as a service, wealth building as a service in a tax-efficient manner. It is also our digital lives—we all have one with its cyber risks, cyberbullying, disinformation and misinformation.

Horizon three is often connected to development in adjacent industries, notably biotech, digital health, cybersecurity, fintech, consumer services, climate and nature.

Seventh, a portfolio of innovation can be articulated two ways: through partnership and/or investment.

Eighth, champions. Any innovation requires a network of believers, champions. Individuals empowered to go above and beyond to think and execute on innovation. They are typically younger people, not yet disillusioned. They can be paired with a senior sponsor to get support and guidance.

Ninth, influence is the alternative to authority, to structure that makes the culture. It eventually leads to the same result. But it takes much, much, much longer as it relies on the goodwill of a few good people with no incentive.

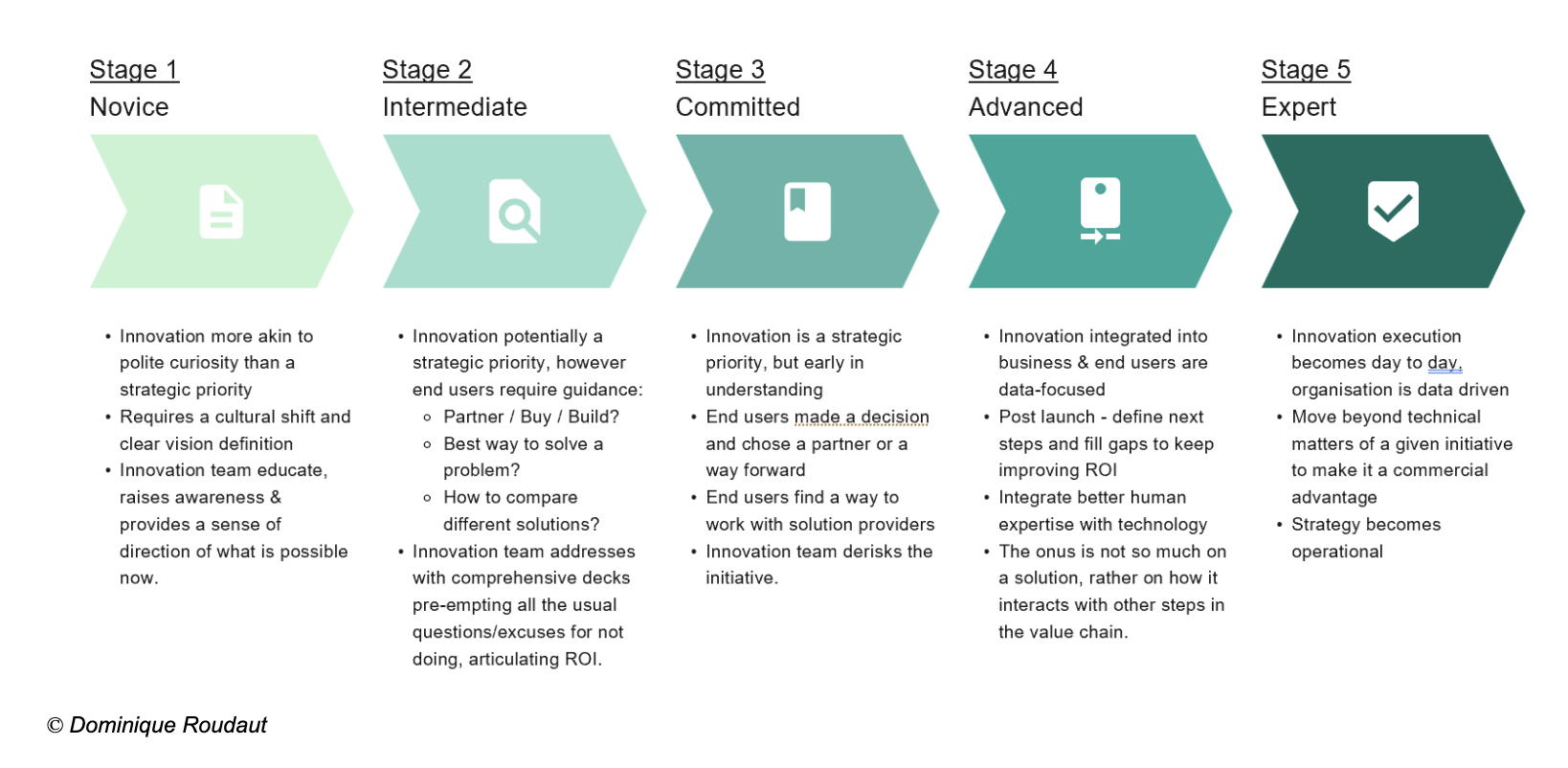

Tenth, innovation is akin to a grieving process. Denial first. Innovators need to work the problem and do it in a quantified way since the second step of a grieving process is minimization (I may have a problem, but it is not that important). The third step of a grieving process is negotiation (if I had resources, I could). So that needs to be sorted through strategic alignment ahead of time. Fourth step, depression. Innovation is hard, as aforementioned. Made easier through partnership rather than in-house building. Fifth step, finally getting one thing done with acceptance/deployment, which gets us to define the level of readiness of an insurance company toward innovation through another five-step process (Exhibit 6).

Exhibit 6: Corporate innovation journey