In the U.S. financial services sector, the rising costs of traditional B2C customer acquisition are self-evident. A 2023 report indicates that the B2C customer acquisition cost (CAC) has surged by 60% during the past few years.

Turning to a B2B2C growth model through partnerships, also known as alternative distribution channels, provides an avenue for organic growth, aligning with modern consumer preferences for simplicity, digital accessibility, and trust through brand loyalty. Partnerships not only offer startups an economical path to scale but also enable legacy incumbents to enter adjacent markets quickly, as trying to do it all in a vertically integrated model is becoming increasingly challenging.

Without executing a robust partnership strategy, startups like Trust & Will may not be able to amass 400,000 users, and Oscar Health might have been nipped in the bud. Likewise, legacy firms such as State Farm and USAA could have faced much more challenges in surpassing their competition, had they opted to go solo in tackling the market.

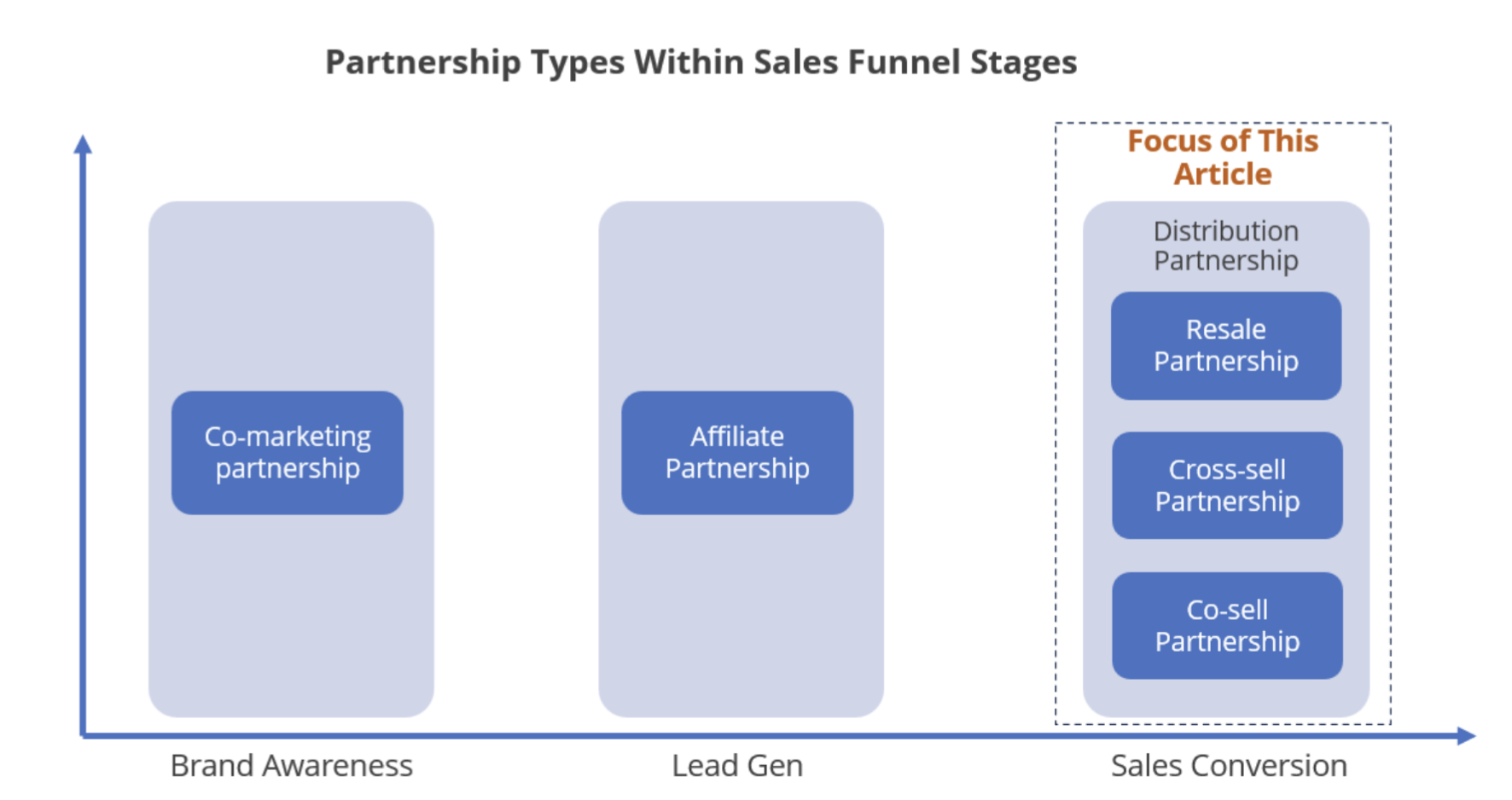

Of the various partnership models, the distribution partnership stands out due to its complexity and the absence of a definitive playbook. It is a collaboration where one sells another's financial products, with a primary focus on expanding sales reach rather than boosting operational or technological capabilities.

The advantages of a successful distribution partnership are manifold. Such partnerships not only ensure a cost-effective go-to-market approach but also create a competitive moat as a successful partnership typically requires three to 12 months to procure, unlike B2C counterparts, which can be established much more rapidly. There is no shortage of examples of a three-person marketing team putting out more quality content daily than $100MM companies put out in a month. A competitive moat, established through distribution partnerships, is critical for ensuring longevity in a highly competitive market, especially one where startups can iterate quickly.

However, this landscape has been changing. In recent years, the introduction of new technology and data has transformed the distribution partnership model within the financial services industry. Yet, the outcomes have been mixed at best.

While distribution partnerships are common in the tech and legacy financial service spaces, emerging financial service companies have grappled with leveraging the potential of B2B2C channels. Many high-profile partnerships have fizzled out prematurely, while others remain lackluster. A significant proportion of fintech or insurtech firms that embraced the B2B2C strategy have either floundered or pivoted.

Partnerships undoubtedly present numerous advantages, such as reduced customer acquisition costs, improved customer experiences, and mutual revenue opportunities. These advantages are clear in theory, but what are the underlying causes of the notable failures in practice? Let's explore some of the frequently overlooked challenges.

Challenge 1. Confusion Over Sales Strategies

One of the primary challenges that partnership leaders face in the financial services sector is the ambiguity in distinguishing among various distribution partnership strategies.

In the scope of distribution partnerships, terms like co-selling, cross-selling, and reselling often lead to confusion due to their subtly different interpretations arising from a lack of consensus on their exact definitions.

Consider co-selling, a strategy that has recently garnered attention for its advantages for complex products or services. In essence, co-selling unlocks value via synergistic collaboration between partners, working together to meet a common customer need throughout the sales process, a challenge beyond the capabilities of a single partner alone.

Reselling is generally traditional, standard, and straightforward, mirroring a vendor-buyer relationship. Co-selling, in contrast, involves a deeper, more integrated partnership that extends beyond conventional frameworks.

Cross-selling is another common form of distribution partnership, where complementary products are offered to an existing customer base. An example of this is the bundling of travel insurance with travel bookings, a notable success in cross-selling. However, most successful cross-selling today is confined to simple and commoditized products that have short sales cycles with low contract value, which yield lower margins for both parties involved.

Additionally, it's critical to differentiate co-selling from cross-selling. Cross-selling primarily involves offering supplementary products through the existing delivery mechanism, while co-selling is about two companies working together to cater to their shared customer base through innovative, previously non-existent delivery mechanisms.

The partnership between Lemonade and SoFi also serves as an instructive example. Despite their seemingly complementary products – mortgage and homeowner's insurance – the anticipated cross-selling actually requires a co-selling approach due to the significant gaps in education, experience, and customer expectations to purchase insurance versus mortgage. Both products are complex and require a longer sales cycle. A simple embedded insurance solution could not fill such a gap. This became evident when the partnership unwound in 2023 after two years of underperformance.

Understanding these nuances is fundamental to nurturing successful partnerships in the financial services industry.

Challenge 2: Absence of a Robust B2B2C Partnership Framework

The success of a B2B2C partnership strategy is often jeopardized from the onset by misaligned expectations. Partnership leaders regularly confront frustration when stakeholders perceive the process as a simple "plug and play," rather than recognizing it as the complex collaboration process it is. Success thus hinges on developing a shared understanding and strategic alignment among all stakeholders, such as partners' leadership team, operation team, and internal teams, to ensure commitments are made and resources are effectively optimized from the get-go.

To navigate these challenges effectively, a comprehensive framework is required, one that not only addresses the overarching issues but also tackles specific problems such as:

Partnering with companies that have little customer profile or needs overlap, leading to little gains beyond initial excitement.

Engaging with channels lacking authentic sales or marketing incentives, which proves futile, despite surface-level compatibility.

Over-reliance on revenue sharing without adapting it to distinct distribution partnership models might not adequately motivate partners seeking more support for their unique challenges. Moreover, those without experience in selling specific products may not see the projected benefits as tangible. Generally, revenue sharing tends to be more effective in reselling scenarios than in other contexts.

Lack of incentive alignment, risking half-hearted commitment internally and externally, causing project delays or directional chaos.

An aligned strategic partnership framework is essential. Without it, pinpointing the root causes of B2B2C challenges becomes nearly impossible. Teams may struggle to determine if issues arise from inadequate marketing, product issues, business development missteps, or fundamentally unviable channels. Blame games may start, often leading to the partnership's dissolution.

Take the SoFi and Lemonade partnership as an example: Despite their status as fintech and insurtech leaders in the B2C space with exceptional growth at the time, the absence of a solid partnership framework left the insurtech's business model misaligned and interests unmet, rendering the partnership a victory only on paper.

Challenge 3: Not Establishing Clear Expectations and Full Commitment

An internally aligned partnership framework and a solid business case are essential, but setting clear expectations and ensuring full commitment from motivated partners are equally important. As the saying goes, "it takes two to tango." A partnership, much like a marriage, aims to collaboratively create innovative solutions with lasting motivation. The distribution of contributions and benefits in these agreements is rarely quantitatively symmetrical, and results typically emerge over time.

Commitment and trust are the cornerstones of lasting partnerships. It's worth mentioning that partnerships differ fundamentally from typical sales interactions; there isn't a pre-packaged product awaiting a purchaser. Instead, the partnership involves a process of continuing, collaborative execution. Clear expectation setting, coupled with fostering deep commitment not just from executives but also from those stakeholders on the ground, is essential for effective execution and aligning both long-term goals and short-term resource investments.

"Reflecting on our journey, I've seen a recurring challenge," stated Ara Agopian, CEO of SolarInsure. "While our channel partners' executives often share our excitement about the partnership, that enthusiasm doesn't always reach the teams on the ground. This mismatch is typically rooted in external market pressures and a shortfall in product knowledge and training. Historically, this misalignment of commitment has led to several failed partnerships, stemming from our own miscalculated expectations and a lack of engagement from our partners. We've since refined our partnership strategy, now ensuring the commitment requirements are clear from the outset in our contracts."

Partnerships marked by transparency, collaboration, effective communication, and robust commitment stand a much greater chance of success. Conversely, concerns over intellectual property, methods or similar trust-related issues can almost completely undermine such endeavors. Effectively, setting expectations is a critical process for both assessing and motivating partners, a step without which true commitment is rarely attainable.

The collaboration between Allstate and Nationwide is an excellent example of this. The misalignment of expectations among top executives and the underestimation of the technological integration effort contributed to its failure, highlighting how such discrepancies can threaten the success of even the most established brands.

Challenge 4: Misalignment in the Commoditization of Customer Relationships

Even in the presence of a robust partnership framework, a compelling business proposal, and clear expectations and commitment, the financial service industry faces a significant challenge: aligning the commoditization potential of various customer relationship models. The concept of "commoditization potential of customer relationships" – essentially, the ability to monetize customer relationships – is influenced by various factors. These include the length of the sales cycle, the degree of product commoditization, the expected customer lifetime, the average value of contracts, and the complexity of the product. Failure to effectively navigate these aspects can often lead to partnerships that unfortunately do not yield significant outcomes.

Strategic planning and execution are critical in partnerships, especially when there are differing perspectives and strategies on commoditizing customer interactions, even for the same client base.

The effectiveness of a partnership hinges on aligning these models. Some companies focus on long-term cycles with infrequent but high-value interactions, while others prioritize more regular engagement. Additionally, approaches to client relationship management can range from tightly controlled to more relaxed. These disparities can create substantial obstacles to successful collaboration.

For example, life insurers have persistently sought to collaborate with fiduciary RIAs to cross-sell life insurance products targeting affluent clientele. Despite numerous attempts over the years, only a few have achieved significant scale. Even with products targeting the same clientele as RIAs with concrete use cases, many insurers struggle to appropriately "commoditize" advisor and client relationships and offer the support required, which fundamentally differ from life agent-customer relationships. Such misalignment can render the partnerships ineffective.

Challenge 5: Divergent Business Models

Expanding on the previous point, a sufficiently distinct customer relationship model often implies a different business model which necessitates a deliberate effort to bridge the gap. For example, a common challenge in partnerships arises when SaaS solution providers collaborate with financial product or service vendors. Theoretically, the broad customer base of SaaS companies appears to complement perfectly with the high-value contracts typical of financial products, suggesting an ideal match. However, in reality, this combination often results in complexity rather than simplicity.

Several factors contribute to these challenges. For instance:

- Many SaaS providers lack specialized expertise or an appropriate marketplace for effectively cross-selling financial products, hindering seamless integration.

- The introduction of third-party financial products involves risk, with potential liabilities that SaaS providers are often reluctant to take on.

- The differing business models of these entities imply different operational cadence: SaaS providers usually operate rapidly, while financial product or service providers need more deliberation and understanding.

- SaaS entities generally function in a less stringent regulatory environment and may be resistant to additional legal constraints.

- Additionally, SaaS companies might not fully understand the financial nuances and the commoditization possibilities inherent in their non-SaaS counterparts, leading to misaligned expectations and strategies.

Understanding and overcoming these complexities demands a nuanced and tailored approach to partnership strategies between varying business models. When executed with precision, these strategies can lead to substantial and meaningful success.

For example: Trust & Will, a SaaS solution in digital estate planning, exemplified a B2B2C partnership strategy by partnering with digital term life insurance distributors. In a highly competitive space with low entry barriers, Trust & Will distinguished itself by embracing a B2B2C approach since 2021, one of the first among its competitors. The team developed a robust partnership framework that gained internal support. This strategy was well executed in the subsequent years. By leveraging their digital capabilities and understanding of customer relationships nuance, they crafted an incentive structure perfectly aligned with the needs of term life distributors seeking differentiation. This strategic partnership with term life distributors contributed to Trust & Will's remarkable growth, further establishing its leadership in the digital estate planning domain.

The promise of B2B2C in financial services remains strong, but success requires more than ambition and alignment on paper. It demands surgical precision in partner selection, a shared commitment to execution, and a deep understanding of the underlying dynamics, from cost recovery models to business model compatibility. As the industry continues to evolve, those who approach B2B2C partnerships with discipline, clarity, and a framework rooted in operational realism will be the ones to convert potential into durable, scalable growth.

Note:

Other success cases: SasID and NAR (National Association of Realtors), IHC specialty benefits with USAA; New York Life and AVMA, Allstate's historical expansion due to partnering with Sears Roebuck & Company, Petco and Nationwide 23.