Policies that insure a person in spite of the absence of bodily harm, that exist because of the threat of reputational harm—these policies are hard to find.

Life insurance policies abound, but policies that insure a person in spite of the absence of bodily harm, that exist because of the threat of reputational harm, that ease the degree of harm—these policies are hard to find. These policies are also expensive, regardless of whether a person is rich and famous, or more famous than rich, or famous but not rich. These policies are a necessity for people at the commanding heights of society, because no one has total command of what anyone can do to a person’s reputation. Captives of chance, we have the chance to benefit from captive insurance; we have recourse from the infliction of harm.

As an alternative to traditional commercial insurance, captives participate in the alternative risk transfer (ART) market. Because of this alternative, captives risk their own capital; they accept the risks of forming their own insurance companies, of having parent groups create these companies for them, so they may avoid volatile pricing and difficulties in purchasing the policies they want.

By developing bespoke policies, captives can reduce costs, increase cash flow, write policies, set premiums and return or reinvest unused funds. As a specific type of insurance, representing the thoughts of people in positions of leadership, as an example of insurance thought leadership, captive insurance makes sense. (Please note: These policies are rare, which is not to say these policies do not exist. Insofar as these policies are available, they tend to originate from offshore insurers. More common are deductible reimbursement policies, where companies increase deductibles with their respective carriers. Captives assume the risk of paying deductibles when they file a claim with traditional carriers.)

As history proves and as a footnote to history confirms, vandals would replace a life of service with headlines from a person’s time as a public servant. The death of Raymond J. Donovan, labor secretary in the Reagan administration, underscores this point: that vindication in a court of law is no shield from vilification via the court of public opinion, that an acquittal is no guarantee of absolution from the influencers of public opinion, that these facts beg the question; that Donovan asked the question himself, “Which office do I go to to get my reputation back?”

Donovan’s question was rhetorical then, but it need not be—it should not be—now. Not when anonymous forces can harm a person’s reputation in seconds. Not when the slings and arrows of outrageous lies can exhaust a person’s fortune. Not when it can be a person’s misfortune to see his life’s work collapse in real time.

Insurance from reputational harm may be the only way to ensure loss of livelihood does not lead to loss of life, that character assassination does not lead to self-harm, that a leader does not commit suicide. Unless a public figure has this insurance, or knows that captive insurance is a means of buying this insurance, reputational harm can be hurtful indeed; so hurtful as to be harmful to the survival of the body politic and the success of the nation.

If first-rate leaders choose not to put their country first, if the choice is not theirs to make in the first place, if they are not free to choose because of what they may lose, because of what the enemies of freedom want them to lose, their sacred honor, then America loses.

We must not lose.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Jason G. Mandel has spent over 25 years at the intersection of Wall Street and the insurance industry. Mandel founded ESG Insurance Solutions (www.esginsurancesolutions.com) in 2020 to help better integrate these two, often conflicting worlds Having a strong belief in ESG concepts (Environmental, Social and Governance), Mandel found a way of incorporating his beliefs in his business.

Representing only insurance carriers and products that he believes offer compelling risk management solutions and maintaining business practices that he can support, Mandel has led the industry in this ESG initiative. ESG Insurance Solutions serves some of the wealthiest families internationally, and their business entities, by providing asset protection, advanced tax minimization vehicles, principal protected tax-free income structures, employee retention strategies, key person coverage and tax-free enhanced retirement plans for their essential employees.

Do you have time to observe and process what's happening beyond your "must do" list? How often do you stop to look twice at details that just don't seem "normal" -- that may even seem outlandish or inappropriate? Do you dismiss these as trivial, or as mistakes, or do you ever consider whether they foreshadow something bigger?

Of the many truths reinforced by events of the past 18 months, one is certainly that evolutionary change can unexpectedly become revolutionary.

That's why improving the capacity to spot, assess and sort the weak signals -- the earliest leading indicators of disruptive change -- is an imperative.

Weak signals are easy to miss, for good reason

Weak signals are all around us, all the time. The challenge in recognizing them is precisely that they are weak.

Weak signals:

Are out of place versus norms.

Show up as crude, implausible renditions.

Get blocked by groupthink.

An example of a discounted weak signal

In the early 2000s, Citi Cards' digital transformation team exposed cardholders to the idea of "tap and go" RFID technology as a means of payment with a small device attached to a keyring that would replace physical plastic credit cards. The first use case: paying fares in urban transit systems.

The weak signal that stimulated this experiment was emotional and qualitative: Users' intense, enthusiastic reaction to how they would feel commuting without having to pull out their wallet and fumble with malfunctioning "swipe" cards in crowded subway stations.

Banking traditionalists were quick to dismiss the possibilities. They were attached to the primacy of the card as the form factor, and retailers resisted funding nominal technology upgrades.

The prevailing attitude was, "if it's not broken, don't fix it." After all, why change, when magnetic stripe-based cards performed virtually 100% of the time?

The result? Within a decade, contactless payments became ubiquitous, with the pandemic acting as an accelerant.

How to read weak signals of change

You don't need a crystal ball to see weak signals. But you do need to value and reward curiosity and commit to a process that more closely resembles an anthropological journey than a traditional strategic analysis.

Follow these four steps to get started:

Embrace the mindset. Cultivate curiosity as a habit. A simple step? Start by recognizing and accepting that we filter what we see based on what we know. Have an open mind, challenge preconceptions and stop to explore for more when you come upon the unusual.

Cast a wide and decentralized net to gather signals. Go far to the edge of your networks for observations, paying special attention to things that stand out as strange or curious.

Create a mechanism to interpret and understand the signals. Keep a database or a journal -- narrative, images and other stimuli -- of signals, including what is interesting and what each suggests.

Channel the signals for monitoring and further action. Begin to organize the signals -- perhaps a few key trends are emerging that suggest logical groupings, e.g., which should be set aside, monitored more intensively or moved toward brainstorming?

For more tips...

Spotting the weak signals depends on active sensing of the environment. For more on listening, take a look at my Fast Company article.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Amy Radin is a strategic advisor, keynote speaker, and Columbia University lecturer focused on why transformation succeeds or stalls in large, complex organizations.

Drawing on senior leadership roles at Citi, American Express, and AXA, including one of the world’s first corporate chief innovation officer roles, she helps leaders build the capabilities required to absorb, scale, and sustain change.

For maybe the first 15 years of the personal computer revolution, business and even government leaders talked a lot about the need for computer literacy. We were told that the very competitiveness of our nations depended on educating the populace to prepare for the digital age. Then Steve Jobs came along.

It turned out the problem wasn't our lack of education. The problem was that computers were just too hard to use. Once Jobs and Apple brought the graphical user interface to computers, and once processors became powerful enough to handle the demands of GUIs, the talk of computer literacy faded. Then came the iPad and iPhone, making an intuitive experience available on almost any device. If you asked a teenager to define "computer literacy" today, he or she would likely say, "Hey, Siri...."

The insurance industry is trying hard to move into a "Hey, Siri" phase, as companies focus on drastically improving the customer experience. Companies are finding that they have to reinvent chunks of their businesses to really get the experience right. Yes, they have to focus on the ways that they touch customers, through agents and brokers, through call centers, through adjusters and through an increasingly broad array of electronic means. But a customer doesn't just experience a company through a direct communication. Customers also experience, for instance, how long and painful an underwriting process or a claim is.

And here's the thing: This emphasis on customer experience requires a revolution for companies but merely an evolution for customers. Insurers have to move heaven and earth to add computing power, to deal with new kinds of data, to come up with new analytical models, to design new processes and so on. Consumers just have to add an app or a phone number so they can text a company, have to e-sign documents rather than printing and mailing them, etc. -- and consumers have already been doing these sorts of things with other companies in other industries.

So, customers may understand at some level all the effort that has to go into changing how they experience an insurance company -- but they don't really care.

As you'll see from this month's interview, from the appended articles and from a host of articles throughout the website, lots of noble efforts are underway, and companies are making progress, but improving customer experience is a marathon, not a sprint. Every January, I publish articles about how this is the year that the industry will figure out the customer experience. Then I publish more of those articles the following January... and the January after that. Despite the undeniable progress, I don't expect to stop publishing those pieces any time soon.

- Paul Carroll, ITL's Editor-in-Chief

ITL FOCUS INTERVIEW

An Interview with Scott McArthur, CRO, Statflo

We spoke with Scott McArthur, chief revenue officer, Statflo, about the impact of digitization on customer interactions.

WHAT TO WATCH

3 Tips for Increasing Customer Engagement

Even before the pandemic, insurance customers were moving to digital channels and demanding the kind of smooth experience they get with Google and Amazon. With customers demanding new types of interactions and agencies and companies needing to increase leads in a world that’s gone from face-to-face to zoom, technology doesn’t have to be intimidating.

WHAT TO READ

Key to Better CX: Think Like NTSB

Airlines are rarely held up as exemplars of customer experience, but in one important respect the industry deserves such recognition.

Why CX Must Trump Efficiency

Companies talk about improving customer experience but focus too much on saving money. Customer process automation does both.

Providing a Better Claims Experience

It’s important to consider the communication preferences of five different generations when building a better claims process.

Self-Service Portals Improve CX

81% of companies expect customer experience to be a key battleground. Self-service portals are a great place to start.

3 Ways to Optimize Customer Experience

Even in a heated marketplace, a superior customer contact center can let life insurers grow.

Millennials Demand Modern Experience

To address the life insurance gap among millennials and create more financial security, the industry needs to move quickly.

How to Increase Profits With Connected CX

Fostering connected experiences is vital to meeting customer expectations and succeeding in a technology-centric world.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Until the arrival of COVID-19, Americans had, for decades, been more concerned with outliving their savings than the prospect of premature death. With that in mind, it’s not surprising that life insurance policy sales dropped 45% during the 1980s and have remained flat ever since, according to LIMRA. Today, only half (52%) of Americans own life insurance, either bought individually or through employee benefit programs.

But COVID-19 may have reordered priorities. The pandemic has served as a reminder that life can be shortened unexpectedly. Eleven percent more life insurance policies were sold in the first quarter of 2021 as compared with early 2020, when employment was down and employee-based life policies lagged. This increase represents the biggest gain since 1983 and the first break after a long decline in life insurance sales. In addition, a greater percentage of policies were sold to households with more modest incomes.

This heightened awareness has given life insurers a chance to prove their value for the first time in decades. But they will only succeed if they are able to meet the needs of the largest group of adults in the workforce: millennials, the oldest of whom are now approaching 40. Representing 25% of the population and numbering approximately 73 million, according to Pew Research, millennials are the generation life insurers will need to reach most urgently if they are to revive their fortunes.

It won’t be easy.

This is a generation that has a lot going on. It is the most educated generation of Americans, with 39% holding a B.A., but millennials are also preoccupied with competing financial priorities, including paying off student loans, managing healthcare costs, finding jobs that pay well, establishing home ownership, starting families and dealing with the cost of supporting aging parents.

JungleScout notes that millennials also constitute the majority (58%) of U.S. mobile shoppers. These are consumers who think nothing of ordering a latte or a pizza through a smartphone. Siegel & Gale found that 64% of all consumers are willing to pay for a simpler experience, but millennials are particularly used to quick and easy digital solutions. It’s no wonder a KPMG study notes that 46% of millennials cite confusion as the biggest barrier to purchasing life insurance. After all, life insurance has been a highly regulated industry loaded with jargon and legalese, and life insurers have lagged P&C counterparts such as Lemonade, which offer P&C insurance on a smartphone app powered by AI and machine learning that can onboard digital customers in less than a minute and pay claims in a matter of seconds.

How Life Insurers Can Reach Millennials

Millennials already understand the need for car and home insurance. Now that the pandemic has gotten their attention, life insurers must speak to them in a language they understand, or risk being ignored. Here are a few factors life carriers should keep in mind as they seek deeper connections with this key demographic:

Use Rewards to Drive Loyalty: According to a KPMG study, 81% of millennial consumers say being a member of a rewards program encourages them to spend more money with a brand.With this in mind, life insurers should consider rewarding policyholders with discounts and better rates as they commit to healthy lifestyle choices through partnerships with third-party wellness programs and insurtechs. From a technology perspective, this means life insurers will need to create platforms based on application programming interfaces (APIs) that can integrate data from a multitude of sources.

Make it Easy: According to an IBM study, almost half of all millennials say that buying life insurance is too confusing. Whether an interaction takes place through an app, web browser or face-to-face with an agent, millennial customers expect simplified explanations and options, price tiers and bulleted lists of specifics. Policy applications should include only the most relevant questions and, where possible, avoid medical exams. Insurers that do the best job of shielding shoppers from unnecessary complexity will win.

Prioritize Mobile Apps: Given millennials’ digital-first lifestyles,to stay relevant, incumbent life insurers must offer intuitive mobile apps that are both technologically sophisticated and intuitive, leveraging capabilities such as Face ID for quick login and providing smooth integrations with other financial products.

Develop a Subscription Model: A massive 92% of millennials have active monthly subscription services, from razors to clothing to music to food. These services are automatized, tailored, simple and easy to manage. The subscription model could work well for life insurers, which, like other insurers, collect monthly premiums. What’s required is packing additional value into a more personalized monthly subscription.

It’s not too late for traditional life carriers to reach millennials. Although insurtechs and startups unencumbered by legacy infrastructure have gained some traction, their success has been modest. Larger life insurers still have the lion’s share of customers, highly recognizable brands and the resources to scale quickly. But they need to couple these advantages with a broader re-think of their core technologies if they are to regain a competitive advantage and create the kind of seamless user experiences that will engender millennial loyalty.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Samantha Chow is the global market lead for life, annuity and health with Capgemini.

She has over 20 years of experience in the life insurance, annuity and benefits industry. She has deep expertise in product development, pricing strategies, competitive intelligence, operational process improvement, underwriting, claims, policy administration and change management. Chow is focused on growing enterprise-wide capabilities for facilitating transformational and cultural change, digital transformation, improving the customer experience, innovation and competitive advancement.

Six Things Newsletter | June 29, 2021

In this week's Six Things, Paul Carroll wonders if we will see an avalanche of M&A. Plus, Looking to the future of insurance and insurtech; from risk transfer to risk prevention; better models for the next pandemic; and more.

In this week's Six Things, Paul Carroll wonders if we will see an avalanche of M&A. Plus, Looking to the future of insurance and insurtech; from risk transfer to risk prevention; better models for the next pandemic; and more.

A financial adviser friend likes to say that “taxes are on sale” at the moment. He’s focusing on the possibility of higher income-tax rates for his well-to-do clients and for the corporations whose shares are in their portfolios, and trying to get clients to reduce or liquidate certain holdings before the increases hit. But this idea of taxes on sale should have effects that ripple far beyond my friend’s client base, possibly including a spate of consolidation in the insurance industry.

Tune in as industry experts from Deloitte join Denise Garth, Chief Strategy Expert at Majesco to discuss new innovative products that are supporting changing demographics in a post-covid world.

As the world starts to emerge from the pandemic, ITL Editor-in-Chief Paul Carroll sat down to discuss the new normal for workers’ comp with two of ITL’s most widely read contributors: Mark Walls, VP of communications and strategic analysis at Safety National, and Kimberly George, global head of innovation and product development at Sedgwick.

The world of work turned upside-down and inside-out beginning 15 months ago, as the pandemic shut down offices and forced so very many of us to work from home.

Now that we're beginning to reverse this process, insurers will have to sort through all sorts of new issues. Here's one: When is the place where a worker works a "workplace," and when is it not?

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Several long-established industries are considered “legacy” — having little motivation to change and slow to adopt new, critical technologies. Large, stable industries that provide essential or compulsory goods and services--like insurance--often fit squarely within this realm. But in 2020, the COVID-19 pandemic forced business leaders in legacy verticals to quickly adapt their technological infrastructure to support the long-term remote workforce.

In the insurance industry, organizations already considering digital transformation sped up their plans. Some started nearly from scratch. , Leaders focused on innovations in areas like personalization, IoT, process digitization and even artificial intelligence. However, one essential area that is still frequently overlooked is the adoption of hybrid cloud models.

The ability to undergo agile digital transformation while maintaining the same customer service levels and keeping up with shifting markets is possible--if the underlying infrastructure can adapt rapidly to changing needs. Cloud technologies, and specifically hybrid cloud models, enable smoother digital transitions for traditional industries because they can easily operate their existing on-premise infrastructure during the transition process.

What are the advantages of implementing a hybrid cloud model for insurance companies? Here’s a closer look.

What is the hybrid cloud model?

A hybrid model in its most basic form is a computing environment that shares data with both a private and public cloud. Private clouds are dedicated specifically to an organization while a public cloud is delivered via the internet and shared across an organization. Less critical workloads can move to the public cloud without opening public access to data, while more sensitive information is kept in a more secure private cloud. Hybrid is an accommodating approach, especially for insurance businesses, which often store sensitive or protected customer information.

Many industries cycle through short periods of increased demand. For example, insurance companies are busier when home and real estate sales are higher in the spring and summer and slower in January-February. Instead of investing millions of dollars to accommodate increased data and information during a small window of time, a hybrid cloud model scales seamlessly to accommodate evolving needs. Organizations may have the flexibility to only pay for services they use when needed.

The hybrid cloud model affords many other advantages:

Improved data security and privacy

Data security and privacy is an ever-growing concern for IT and business leaders, especially in industries like insurance that house sensitive or legally protected customer information. For this reason, moving to the cloud can seem like a risky option. However, a hybrid cloud model can alleviate some of these concerns as doing so can reduce the risk of data loss or exposure.

In a hybrid model, companies may opt to store their most sensitive data on-premise and shift functions like accounting or other operational processes to the cloud, all of which drives process optimization and cost savings.

Some business leaders in the industry have been hesitant about making the jump to the cloud due to concerns that they won’t achieve the same performance as that of on-premise infrastructure. However, the most important aspect of this transition is deciding which parts of the workflow must stay on-premise and which can be shifted over. This is a process that actually provides IT teams more flexibility and control within the overall system.

The teams also can strategically use more of their budget through hybrid models because pay-as-you-go plans with no upfront costs are available. Cloud-only solutions can be costly upfront and disrupt workflows through complete lift and shift, but hybrid allows internal teams to define where multi-tenancy is needed. And, of course, any operations moved to the cloud will also benefit from automatic application fixes and updates--so they’ll always be using the latest technology.

Better disaster recovery measures

Disruption, data breaches and physical infrastructure damage were prevalent in 2020 and early 2021. Insurance leaders must keep these concerns top of mind when making decisions about where and how to house varying types of data.

A totally on-premise solution presents risks in disaster recovery. Contrarily, hybrid models can scale noncritical workloads while allowing IT teams to secure the most sensitive data and act quickly in the event of a disaster.

Legacy industries don’t have to get stuck in the past or be forced to lift and shift all workloads into a full-scale cloud migration. Instead, organizations with critical infrastructure like insurance should implement a hybrid cloud model to reduce costs, improve security and enhance overall operations and productivity during peak seasons.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Gary R. Kay serves as Excellarate's chief operating officer, with responsibility for several key enterprise functions, including leading the insurtech business, North American delivery, integration, alliances/ partnerships, analysts and internal IT operations.

The insurance industry has steadily been digitizing in recent years. It is taking advantage of technological developments in automation, offering apps to clients and introducing things like electronic proof of auto insurance.

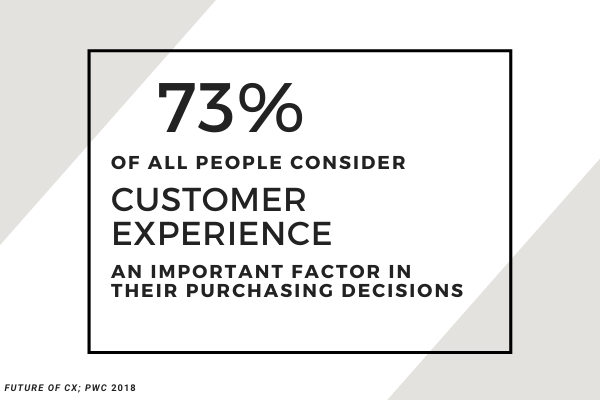

PwC’s Annual Global CEO Survey in 2020 identified customer experience (CX) and core tech transformation as the top two opportunities for companies to set themselves apart, with CX significantly ahead. When customers are communicating with their insurance company, they are usually dealing with an awful experience (a car accident, a medical issue, a home invasion, a roof leak or a full-on natural disaster). Hitting any snags when it comes to getting the service they need is a big factor in driving them to a competitor.

Artificial intelligence (AI) addresses both customer experience and tech transformation and has helped insurance companies improve their services and stay competitive in a tough industry. AI enables many services and processes to be automated, resulting in both cost and time savings. But AI deployment also benefits customer experience, in three specific areas.

Improvement of policies, products and processes

The retail sector has capitalized on custom products and experiences, and the concept that one or two sizes will fit everyone is fading quickly in other sectors, too. The insurance industry is now also latching onto customization, as AI enables companies to leverage data to personalize a core product for an individual customer.

A company’s AI model can use a client’s historical data to calculate with a high degree of probability that a particular product or policy will be the best fit. In the eye of the customer, they get an attractive product without needing to spend a lot of time on consultations with the broker. For the insurance company, the efficiency gains are impressive, and agents don’t need to spend a lot of time finding the right product for the client.

Not only does AI improve the speed of crafting policies for customers, the technology can also speed up underwriting, as well as the claims process -- two key touchpoints where turnaround time is essential for CX. If a health insurance customer is filing a claim for an expensive prescription, they will want a simple and quick resolution. Long waiting times may drive them to a competitor known for quicker reimbursements. But AI can bring a competitive edge to an insurance company if customers know they can expect trouble-free claims processing.

Enabling rapid online assistance

The days of customers playing phone tag with agents to get the information they want are long gone. Insurance companies can leverage AI on their platforms -- both web and mobile -- to allow customers to quickly find an answer to a question. The ability to more easily respond to inquiries from policyholders is especially important following a major event, such as a tornado or hurricane, when there is sure to be a high-volume of online interactions.

AI-powered chatbots have become the first touchpoint for customers in many sectors. When done right, they can give a major boost to an insurance company’s customer experience. Organizations can also save money by automating simple and routine online customer interactions, leading to another win-win situation where customers can quickly get to the information they need.

Once an insurance provider has an AI model in place to help with the crafting of policies and settling of claims -- and the organization begins using it as an integral part of its daily routine -- it is vital that the AI model suitably addresses four risk factors: accuracy, stability, flexibility and ethics. AI can be used to test these models against those factors.

Any AI model an insurance company employs should have a high accuracy score. Smart AI model testing will ensure that the results are reliable -- with an agreed tolerance for the model, to protect a company’s profitability while appropriately managing their risk. Because data changes over time, testing will ensure that an AI model remains stable when there’s a change in the data in the ecosystem, or in the way the insurance company handles business. Such testing will also ascertain that the model is flexible enough to react to those changes while remaining accurate.

Above all, AI can be used to test whether the insurance company’s AI models are ethical -- meaning that they are not biased toward or against any specific groups of society. Even the largest dataset imaginable can be flawed or biased depending on the data that is included. Therefore, it is vital that these models be tested on a regular basis, to verify that the risk factors are being appropriately applied without bias, ensuring the company’s reputation and its brand.

Giving customers a reason to stay

As the saying goes, it’s cheaper to retain a current customer than to attract a new customer, so insurance companies need to look at technological innovations that can improve customer retention. By recognizing the value AI can bring to all aspects of the customer experience, insurance providers can deliver fast, accurate and fair service to policyholders.

Whether a business provides health, car, home or other types of insurance, there will always be a line of competitors just waiting to snatch away disappointed and frustrated customers. What’s most important is for insurance companies to focus on giving customers reasons to stay.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

A financial adviser friend likes to say that "taxes are on sale" at the moment. He's focusing on the possibility of higher income-tax rates for his well-to-do clients and for the corporations whose shares are in their portfolios, and trying to get clients to reduce or liquidate certain holdings before the increases hit. But this idea of taxes on sale should have effects that ripple far beyond my friend's client base, possibly including a spate of consolidation in the insurance industry.

That's the thesis that was advanced last week by Stephen Schwarzman, CEO of Blackstone Group, the private equity firm that as of March 31 had a staggering $650 billion of assets under management.

He says corporate leaders worry about a Biden administration proposal to tax capital gains as ordinary income for those earning more than $1 million a year, rather than let them apply the much lower rate that has long been used for profits on sales of stock, real estate and many other assets. The change would mean a tax rate of 39.6% on capital gains for those high earners, rather than 20%.

While any tax increases look to be at least months away, Schwarzman said high earners are starting to look now at selling assets and booking profits, to be safe.

Although he didn't single out insurance, I suspect his thinking applies, in particular, to many owners of insurance brokerages and agencies. We could see an acceleration of the consolidation that has been occurring in the distribution channel. Private equity has already been buying up brokerages and agencies, and having eager sellers should only increase the pace.

The continuing digitization of insurance sales, accelerated by the pandemic, may also encourage owners to continue selling. Digitizing takes capital that some don't have, so, knowing they face a steady loss of competitiveness, owners might explore selling now. Even if they have the capital, owners have to decide whether they want to manage a significant transition -- moving business online and incorporating digital technology into a host of internal processes while also figuring out how to reopen offices following the pandemic. Many may decide that they'd just as soon let some bigger entity handle the shift. For anyone contemplating an exit, now would seem to be a good time.

Beyond the effect on agencies and brokerages, the possibility of a higher tax rate on capital gains could encourage insurtechs and even some larger, established companies to consider putting themselves on the market now if they had already been considering an exit. The same for the possible increase in the corporate tax rate in the U.S. from 21% to 28% (or whatever the final proposal turns out to be): Potential sellers might hope to get a higher valuation based on the loftier net income that lower taxes allow.

It's not clear how great the effect of the possible tax changes would be for insurtechs and larger companies. Lots of other factors come into play, the larger a company is, and tax increases aren't anywhere near a done deal. But the prospect of higher taxes might tip the scales for some.

In theory, consolidation will address one of my bugaboos -- the wild inefficiency of so many insurance processes -- through economies of scale and greater investment in digitization.

I realize that the adage says: "In theory, there is no difference between theory and practice. In practice, there is."

And, in fact, a lot of the increase in scale among agents and brokers seems to have been used to press carriers for higher commissions, rather than to drive efficiency.

But I don't give up easily. I'm holding out for scale that drives digitization and that drives costs down while simplifying life for customers.

Cheers,

Paul

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

The COVID-19 pandemic has obviously accelerated the development of the healthtech and insurtech industries. Let’s look at these changes and certain corresponding innovations in more detail and see what we can expect in 2021.

Healthtech

In general, the existing healthcare system turned to various modern and necessary digital tools to perform the following crucial tasks:

make predictions concerning the disease’s spread;

collect and analyze vast amounts of data;

diagnose and treat patients remotely.

And due to the spread of COVID-19 pandemic, the sector has developed rapidly in multiple directions. Among the most notable are:

Remote monitoring;

Telehealth;

Artificial intelligence technologies.

It’s not surprising that providers advocate for integrating more data sources and new patient matching methods, from telehealth to big data analytics, to build effective coordination concerning COVID-19 tracing and valuable testing.

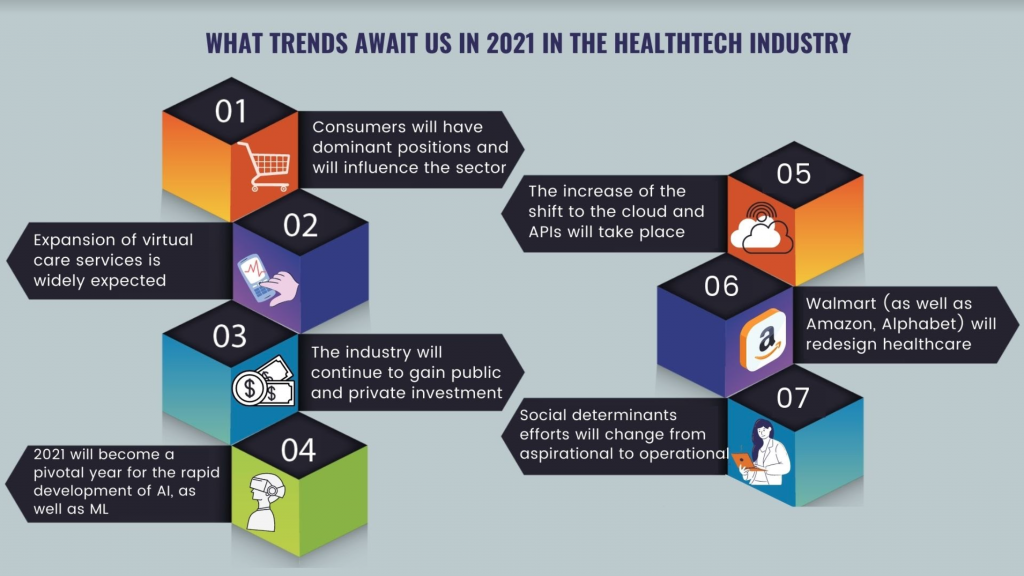

What trends await us in 2021 in healthtech?

1. Consumers will have dominant positions and will influence the sector in 2021.

Healthcare will be restructured according to patient needs and expectations. More and more healthcare providers understand the necessity and even indispensability of digital and virtual healthcare in the post-COVID world. So, healthcare organizations will have to leverage technologies to help their patients in their day-to-day life – smart devices, omnichannel communication tools, intensive machine learning and many others.

Let’s look at a concrete example. In an article for Everyday Health, Vivian Lee, the president of platforms for Verily Life Sciences, describes cooperating with the federal government in the creation of Project Baseline, a tool to screen for coronavirus risks, while also working with universities and employers to create programs that provide detailed testing, competent symptoms’ tracking and data analytics. An app lets users to check any symptoms and schedule lab tests.

Such virtual systems extend beyond COVID-19 uses. For example, Verily's technology has been used by Onduo, a virtual diabetes clinic that tries to help patients lower their A1C levels and develop vital health habits.

2. Expansion of virtual care services is widely expected.

In the same article, Deneen Vojta, the executive vice president of research and development at UnitedHealth Group, said virtual health will direct patients to more self-care. This may lead them to rely on doctor services only in more essential cases.

According to Sarahjane Sacchetti, Cleo CEO (in an article in Fierce Healthcare), in 2021 we will see increased use and efficacy of virtual services that had been seen as in-person only: postpartum, maternity, pediatric. Understanding the necessity of virtual health services, employers will offer flexible and convenient benefits to support employees (and drive productivity).

Indeed, many companies are looking to expand healthcare service.

3. The industry will continue to gain public and private investment.

Digital health has already received a surge of private and public investment during the pandemic. At the same time, modern digital health companies are going to become more comprehensive, which will attract even more.

4. 2021 will become a pivotal year for the rapid development of artificial intelligence, including machine learning.

The healthcare industry will pay attention to the benefits of machine learning in highly scalable solutions. AI has a vital ability to identify trends and sequences in data gathering and analytics that human beings can’t.

Hospitals are going to become smarter, says Kimberly Powell, vice president, general manager of NVIDIA Healthcare, in the same article in Fierce Healthcare. Smart cameras and speakers will help them to automate many activities. This, in turn, will help to increase operational efficiency and to improve virtual patient monitoring.

Modern, cloud-based systems give providers the opportunity to access necessary patient’s data practically anywhere. They also enable telehealth and much better care coordination.

Application programming interfaces (APIs) will continue to play a significant role in healthcare data exchange, improving data analytics while allowing for important medical research and innovative ways to access electronic health records (EHRs).

However, on top of technological challenges there is always a challenge related to regulatory policies. Colin Anderson, lead developer at Tactuum, told our chief growth officer, Timothy Partasevitch, in an interview:

“The past year, as terrible as it has been, there are some good things that have come out of it. And that is the NHS [National Health Service] and U.K. government as a whole, realized what they are missing out on by not embracing the technology. We have got the ability to implement more streamlined healthcare through technology, and we’ve got the expertise to do it really quickly as well.”

Colin added that a new winner in healthtech could be “having patient records being available to actual patients themselves, so they can have a secure app with all their records on it that can be shared with their healthcare provider, whether that be their local [general practitioner] or a surgeon.”

6. Walmart (as well as Amazon and Alphabet) will redesign healthcare.

Andy Arends, vice president at NTT Data Services, says Walmart can establish great healthcare facilities within a reliable, low-cost and no-frills environment. As a result, Walmart could become not only a certain health plan but also the provider and create its own insurance distribution.

7. Social determinants efforts will change from aspirational to operational.

Megan Callahan, vice president of healthcare at Lyft, says there are predictable calls to action in the industry to form a more standardized approach to measuring and collecting data on social determinants of health.

Insurtech

Now let’s look at the predictions of different experts concerning how insurtech will grow and evolve in 2021.

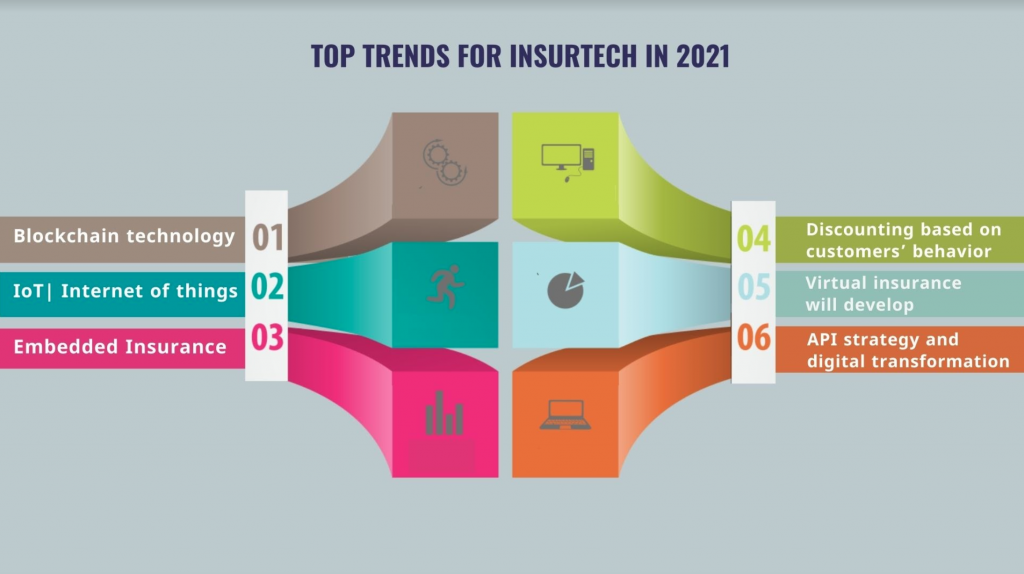

Top trends for insurtech in 2021

1. Blockchain

Many experts are confident that blockchain technology will become a leading component of insurtech. Incorporating blockchain with encryption can better protect important medical records and other sensitive information against cybertheft.

Insurers will have to calculate all long-term environmental and economic costs. And, due to lack of regulation, an opportunity for fraud and scram could appear.

2. IoT (Internet of Things)

Internet of Things devices such as Apple’s smartwatch and Amazon’s Echo are going to reach an estimated $43 billion by 2023. Integration of IoT can help not only consumers but also insurers, by accelerating and simplifying the claims and underwriting process while reducing costs and expanding business. The technology can let insurers stay in touch with their customers, strengthening the relationship, and form partnerships with other companies to cross-sell services and products.

But smart technologies can be attacked by cybercriminals and hackers and require considerable investment.

3. Embedded insurance

In 2021, more insurance products will be embedded in the purchases and experiences customers are having online. Tesla, for instance, has announced its own insurance product, so all willing can purchase a car and insurance, specifically tailored to the vehicle, in one experience.

4. Discounting based on customer behavior

Many experts say that in 2021 we will see really creative programs, with smart technologies being used to offer customers special discounts according to their individual behaviors.

In an article for Benzinga, Brett Jurgens, co-founder and CEO of Notion, a Comcast company, says greater discounts could be offered for clients who use devices, such as modern smart sensors, in different water-prone locations or for better coverage across the home or whole property.

Insurers are ready to leverage augmented, virtual and extended reality solutions to meet their customers’ and employees’ needs.

6. API strategy and digital transformation

With APIs, insurance companies can benefit from better internal systems and data integration, streamlining the claims management process and speeding the resolution of claims. APIs allow for flexible and powerful technology platforms, which can consume and share large volumes of data while linking insurers with a huge number of customers and partners. Insurers that fail to build valuable APIs into their platforms will not be competitive.

Bryan Falchuk, founder and managing partner at Insurance Evolution Partners, said:

“I see the data in any system as having to be available to all other systems. This is table stakes today, and, as an industry, we are still lagging here. APIs are the preferred way to enable this if each function has a different system, but the industry is still struggling. There are new solutions coming out that can ride on top of legacy platforms or newer platforms that aren’t as API-friendly to solve the problems of standardizing data and making it available to other systems. They’re often built as low-code/no-code solutions, making hesitation in adopting them even harder to justify. Yet we do. This is where I try to help carriers I work with to see a) customers increasingly will not stand for re-entry of information or you not having a complete view of them when they come to you, and b) the means to solve for this exist today.

"For example, if you use a modern [customer relationship management system], based in the cloud, it can publish and consume data from many different sources through APIs. But what if those sources aren’t built to communicate that way? Or, what if they are, but the APIs aren’t very good (as I’ve often found to be more the case than a stark inability to use APIs)? We don’t need to stop there, and can instead see if there is another path to bring the data trapped in disparate systems together without having to go through a multi-year, multiple-tens-of-millions (or hundreds or millions) of dollars effort to replace a legacy system.

"Many carriers that were resistant have started to see on the back of pandemic-driven lockdowns and remote work that they simply must change. And the speed with which the industry virtualized its workforce was a good reminder that we can change much faster than we thought we could. Luckily, we also have the tools to get there now.”

So, obvious changes have occurred in healthtech and insurtech. And they will develop further in 2021. Modern healthcare and insurance companies must adapt.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

In 2020, people flocked to purchase life insurance amid the looming fear and uncertainty brought by COVID-19. None of us had experienced a global health crisis like this, and, when mortality is at risk, the demand for security increases.

While life insurance policy sales increased 2% overall in 2020, other indicators showed just how much life insurance was brought to the forefront once again, following a decline in policies sold over the decade prior. CNBC reported a 50% spike in Google search traffic for “life insurance” between March and May 2020, while leading carrier Northwestern Mutual saw a 15% increase in policies sold between April and September compared with the year prior. On the annuity side, sales were up $58.6 billion from 2019.

You’d think these numbers would be a good thing for insurance companies and agents, but that wasn’t necessarily the case. The massive influx in applications caused insurance carriers to become increasingly bogged down; applications that once took one to two weeks to review and process were suddenly taking over one month. And thresholds for coverage became even more challenging to meet, with many premier carriers only insuring people if they met a $750,000 coverage threshold. This continues to be the case today for many major carriers.

Luckily, simplified-issue insurance let people who are generally healthy just answer a handful of questions. And, with instant-decision life insurance, many people didn’t have to get a medical exam to enroll in a policy, and a decision was made in two minutes as to whether a carrier will cover that person. Insurance companies have also found easier ways to do underwriting or attending physician reports, which are essentially a doctor's official response regarding a patient's current state of health and health history.

And yet, as the demand increased and both simplified-issue and instant-decision insurance became more prevalent, so did the need for efficient, user-friendly digital insurance quoting and sales platforms. But our industry just hasn’t kept up with the times. It has been using the same antiquated application process for decades.

On the consumer side, the process of applying for life insurance required a 15-page application, doctor’s appointment and various other qualifying factors and steps (if the person doesn’t qualify for instant decision). And, the person would be on the receiving end of many broker marketing calls, and have to pick from 20 companies on the basis of pricing and insurability.

Now, as people’s health and desire for financial security have been in jeopardy, there’s been a needed shift in how we go about buying and selling life insurance. For instance, our platform, Quote & Apply, supports agents in making the transition to digital as seamless as possible. A person can go through our entire application in under five minutes and be quoted a policy (with several coverage options dependent on the person's unique history) right on the spot. There are just six questions (age, gender, height, weight, smoking history and a rating of general health). Insurance companies can directly contact the medical information bureau and a person's doctor through a health portal and make instant decisions while offering numerous policy options.

The implications of COVID-19 spurred this heightened awareness of the importance of life insurance, and I believe that it’s every agent’s fiduciary duty to offer these policies to their clients. Life insurance gets people through the most challenging times of their lives.

We’re not going back to where we were as an industry, even post-pandemic. COVID-19 put a microscope on the issue of our mortality and how life insurance can provide an essential layer of security for people everywhere. COVID simply crystallized the demand for digital wholesale life insurance solutions.

Between the shift to a remote workforce, and the pandemic itself, we had no choice but to evolve; and we now have a chance to create widespread life insurance literacy through this experience.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Mark Tattersall is the principal of BackNine Insurance, a wholesale life insurance company formed in 2008. Tattersall and his two sons (Brett and Reid Tattersall) are the forces behind the newly released insurtech platform Quote & Apply.