While technology-enabled disruption of the automotive ecosystem was already well underway prior to 2020, the global pandemic caused even greater disruption, and many of the changes will continue to affect every corner of society and industry well into the future. We have identified deceleration in some areas but acceleration in others. Our intent here is to put as much of this into context as is possible and to offer a view of the “new” future as we see it, following what we are calling “The Great Reset”

Auto Safety

Early Traffic and Driver Safety

Traffic safety has been a concern since the first U.S. gasoline-powered car was introduced in 1896. In fact, the first seat belt patent was granted in 1858. Massachusetts introduced the nation’s first statewide traffic laws in 1901, limiting speeds to 12 mph in cities and 15 mph on country roads. New York introduced a drunk driving law in 1910. And in 1930 the nation’s first three-way traffic light was introduced.

Before there were lane departure warning systems, blind spot monitoring and rearview cameras, the automotive world saw one of the most important safety technologies to ever be invented—brake lights. The first brake lamps appeared as early as 1905, though the requirements for brake lamps took a bit longer to catch on. For many drivers, hand signals were enough of a warning to other drivers of their intent to stop or turn. This reliance on hand signals made it difficult for many drivers to enjoy their automobiles at night, though, making the brake light a necessity.

By 1928, 11 states in the U.S. had made brake lights a requirement on cars. But the most important brake light of all is the third brake light, introduced in 1974. The third brake light reduced rear-end collisions more than 60%. It quickly became a requirement on all automobiles.

Later in this article, we describe more recent driver safety technologies, introduced in 1950, and collectively referred to today as ADAS (Advanced Driving Assistance Systems).

Rising Traffic Deaths

In spite of all of the many driver safety technologies and the many impaired and distracted driver laws, U.S. traffic deaths have continued to rise. One of the many unexpected consequences of COVID was the increase in driving speed on much-less-congested roadways, which resulted in higher accident severity, including more fatal crashes. The number of U.S. traffic deaths surged in the first nine months of 2021 to 31,720. The estimated number of people dying in motor vehicle crashes from January to September 2021 was 12% higher than in the same period in 2020. That represents the highest percentage increase over a nine-month period since the U.S. Department of Transportation (DOT) began recording fatal crash data in 1975.

This February, DOT announced an ambitious safety plan with the goal of zero roadway deaths. Calling the status quo “unacceptable,” Secretary of Transportation Pete Buttigieg unveiled a plan that will be implemented over the next three years. He noted that nearly 95% of U.S. transportation deaths occur on streets, roads and highways. Buttigieg cited National Highway Traffic Safety Administration (NHTSA) data that found an estimated 38,680 people died in motor vehicle crashes in 2020 and 20,160 died in the first half of 2021. That’s an 18% increase compared with the first six months of 2020 and is the largest number for January through June since 2006.

Collision Repair Industry Consolidation

For the last 15 years, we have seen the influence of financial institutions, investment banking and private equity targeting industry consolidation through multi-shop pperators (MSOs). Today, small to medium-size MSOs are now partnering with private equity companies to help accelerate their growth. These aggressive consolidators, known as multi-location operators (MLOs), such as Crash Champions, Classic and CollisionRight, are building regional and super-regional platforms to compete with the larger legacy consolidator MSOs like Caliber and Boyd/Gerber.

The collision repair space has long-term, proven economics and insurance-industry-driven demand dynamics that create relatively strong cash flow stability. A very high percentage of the repairable vehicles come from direct repair program (DRP) relationships with top 10 insurance carrier partners with ever-increasing market share. Repairers that provide consistent, high-quality repairs and service can depend on receiving a steady stream of vehicles. The quid pro quo revolves around managed performance metrics and agreed revenue/expense models between the repairer and insurer. The better the performance metrics, the more reliable volume the carrier will continue to influence to the MSO; carriers will rescind flow if performance and customer satisfaction deviates much from agreements.

Insurers rely on the MSO repair organization to expand to new locations in insurer-targeted markets while the repairer looks to benefit from incremental cash flow through the working relationship and referrals from the insurance partner. This relationship allows the repair organization to leverage its insurer referrals without investing heavily in consumer direct marketing.

There is no evidence of a slowdown, especially for private equity investors, as they continue to see opportunity in consolidating the collision repair industry, even during a worldwide black swan event like the COVID-19 pandemic. Currently, there are 12 MSOs in the U. S. that have a total of 15 private equity or strategic investors or are publicly held.

See also: Reflections on Insurtech, Pandemic

Caliber and Boyd/Gerber, by far the two largest consolidators, have continued to be consistent, prolific buyers of MLOs throughout the last two years. Service King continues its acquisition hiatus, which now spans almost four years. Two of the largest acquisitions in 2020 were of the U.S. Fix Auto network by Driven Brands and of Pacific Elite by Crash Champions.

Because of these and many other transactions and despite COVID’s impact, 2020 and 2021 ranked as very active years for MLO transactions, with 676 MLO locations acquired, representing revenue of $1.8 billion. Since 2012, when we initiated coverage of MLO transactions, 2,271 MLO locations have been acquired, reflecting over $6.5 billion of revenue transfer while averaging $2.9 million per location.

The Advent and Future Impact of ADAS

Adoption and Impact on Collision Repairs

ADAS were being used as early as the 1950s with the adoption of the anti-lock braking system (ABS). Early ADAS include electronic stability control (ESC), anti-lock brakes, blind spot information systems, lane departure warning, adaptive cruise control and traction control.

The adoption of ADAS features on newer vehicles is having a growing impact on all aspects of collision repair and paint consumption, along with material changes and consequences within the auto physical damage landscape. Below, we have quantified through the current decade those changes most important to the number of collision repairable vehicles, PBE and paint company refinish revenue and expected changes across related distribution channels.

A new American Automobile Association study on the effectiveness of driver monitoring systems in vehicles equipped with ADAS found that direct systems with driver-facing cameras to detect driver distraction or disengagement are more effective than those that only monitor steering wheel use. On average, the percent of time drivers were engaged was approximately five times greater for direct systems compared with indirect systems.

The U.S. government’s annual safety ratings of cars may soon give them credit for having driver-assistance systems, the latest indication that the once-futuristic technology is becoming mainstream. DOT proposed on Thursday that lane-keeping support, automatic emergency braking, blind spot detection and blind spot intervention be incorporated into its Five-Star Safety Ratings program for new cars.

ADAS Features

While there is not industrywide agreement on the nomenclature and features composing ADAS, there is general agreement that ADAS today may include any or all of the following 16 safety features:

● Reverse Camera

● Rear Collision Warning

● Rear Collision Mitigation

● Adaptive Cruise Control

● Automatic Emergency Braking (AEB) or Collision Avoidance

● Brake Assistance (sensors determine when driver is making emergency stop and applies full

braking force)

● Blind Spot Warning

● Blind Spot Mitigation

● Lane Departure Warning/Lane Keeping Assistant (LKA)

● Lane Departure Mitigation

● Cross Traffic Warning (blind spot alert using long range radar)

● Forward Collision Warning

● Forward Collision Mitigation

● Pedestrian Detection

● Adaptive Headlights

● Driver Monitoring

ADAS Impact on Claims Frequency and Severity

While there is not yet enough data to forecast the long-term impact of ADAS on accident frequency, existing data and opinion indicate that overall accident frequency is likely to decrease as ADAS features proliferate, but the nature of accidents will shift until all vehicles are similarly equipped. (Currently, for instance, there is an increase in the percentage of front-rear collisions as Automatic Emergency Braking and Collision Avoidance technology reacts more quickly than do the drivers of unequipped vehicles). Offsetting this decrease in accident frequency is the sharply increasing severity of accidents due to the higher costs of ADAS technology replacement and the necessary associated repair procedures required.

By 2030, 75%, or 211 million vehicles, of the 281 million cars registered in the U.S. are anticipated to have some number of ADAS features.

Compared with similar vehicles without any core ADAS features, vehicles with at least one core ADAS feature resulted in:

- 1% lower Bodily Injury claim severity

- 1% lower Property Damage claims severity

- 4% lower Property Damage claim severity

(Source: LexisNexis Risk Solutions, November 2021)

COVID and the Great Reset

COVID Cuts Into Collision Repair Production

The lack of production based on technician shortage has been real since the beginning of COVID. This is due to not only COVID but is also based on changing cultural work norms and mores reflecting less interest in being a repair technician. Fewer available techs = less production = more time to repair = fewer cars being repaired = less collision repair revenue produced = lower paint sales for suppliers and distributors.

A half-dozen collision repair companies in different regions of the country that were contacted last week all reported having staff out during the first half of January with COVID-19. A seven-location MSO in the Northeast reported having as many as 15 people home sick at the same time. A shop in the Midwest had 10 of its 16 employees on sick leave.

“This is the worst we’ve seen it since the pandemic began,” a West Coast shop owner said. “Customers and even most insurers have been pretty understanding about the delays, but customers are back to asking a lot more about how we’re cleaning their vehicle before they pick it up – more like they were doing the first few months of the pandemic. One lady paid us to deliver her car and park it in her garage with all the windows open, saying she’d look it over the next day.”

Post-Pandemic: What Stays, What Reverts?

The global pandemic had a broad range of impacts, many of which were expected, a few of which were totally unexpected and some of which continue and are likely to leave the world permanently changed.

Driving Behavior and Deaths

Initially, pandemic lockdowns and work-from-home (WFH) models took the majority of private passenger vehicles off the roads, almost instantly cutting car accidents and repair volumes, and caused most auto insurers to reduce/refund auto premiums in one way or another. A noticeable uptick in usage-based insurance program adoption quickly followed, reflecting consumers’ interest in more closely matching auto premiums to the new realities of risk. It remains to be seen whether this adoption will continue once the pandemic recedes.

Touchless Everything

Out of consumer concerns about infection, touchless everything became pervasive, and digital claims solutions, including auto photo accident claim self-service, absolutely spiked. As COVID fears began to recede in late 2021 and into 2022, miles driven returned to almost pre-pandemic levels, as did accident frequency, but the average severity of each accident and repair has increased due to higher speeds on more open roads, which drivers became used to, and the higher cost of onboard technologies.

Crashes — and deaths — began surging in the summer of 2020, surprising traffic experts, who had hoped that relatively empty roads would cause accidents to decline. Instead, an increase in aggressive driving more than made up for the decline in driving. And crashes continued to increase when people returned to the roads.

Now, the U.S. is enduring its most severe increase in traffic deaths since the 1940s. Deaths from vehicle crashes have generally been falling since the late 1960s, thanks to vehicle improvements, lower speed limits and declines in drunken driving, among other factors. By 2019, the annual death rate from crashes was near its lowest level since cars became a mass item in the 1920s. But then came the COVID-19 pandemic.

And virtual claims inspection continues to gain traction as the preferred method of inspection (MOI) for insurance claims of many kinds, led by personal lines auto, with personal property close behind. There appears to be no going back to historical levels of staff or independent appraisal methods.

Work From Home and the Great Resignation

Many of us initially assumed that working from home would be temporary and that a return to pre-pandemic working models was only a matter of time. We now know that to be wrong. A majority of the workforce, if given the choice, would now prefer some form of WFH, either hybrid or complete, to a full-time return to the workplace.

A lack of work-life balance and declining job satisfaction are among the greatest factors contributing to mass employee departures, referred to as the Great Resignation. Owing to the trend of working from home, the lines between work and leisure often get blurred, making professionals work beyond their dedicated hours. Working remotely for almost two years has gotten many employees used to the new trend. Some employees will inevitably quit their existing jobs and search for new opportunities if their employers leave them with no option but to work on-premise.

Recent research reveals that:

- The recent rise of COVID-19 cases resulted in 71% of respondents’ companies delaying plans to return to the workplace or reverting to remote/hybrid work.

- 30% were back in the workplace and reverted to remote/hybrid work.

- 41% rescheduled or canceled plans to return.

- Nearly half (48%) have not determined a date to return to the physical workplace.

Auto Claims, Current State of Collision Repair and Projections Through 2030

Within the collision repair industry, 2019 was the pinnacle for opportunity and success. Repair facilities were flush with repairable vehicles, and the relevant total addressable market (TAM) reached its historical high of $38.3 billion.

Then with very little warning, in March 2020, the scourge of the COVID-19 pandemic emerged and persisted through 2020, 2021 and, while the spread of the omicron variant seems to be slowing, through the beginning of 2022. 2020 will forever be seen as a year of significant disruption and structural change with far-reaching economic, social and political implications.

It clearly has not been a short-term experience. Following are some of the 2020-2021 collision repair industry’s confluences of trends and constructs affecting the entire auto physical damage ecosystem.

- Consolidation remained well underway and was intensified by the numerous private equity investors and their MSO buyers. M&A activity remained extremely active in 2020 and throughout 2021, continuing within the collision repair segment and throughout the broader auto physical damage landscape, including the many segments within its orbit: insurance, parts, technology, dealers, glass and paint, body and equipment, etc.

- We estimate that 2020 repairable claims were down around 22% nationally when compared with 2019. We have seen some recovery in 2021 and estimate the year to end up 10% to 13%, with repairable claims reaching 2019 levels by late 2022 to early 2023, barring some external events like COVID continuation.

- Technician labor and skill shortages continue to hurt revenue and production opportunities while increasing costs.

- Increasing parts costs, coupled with sourcing and delivery delays, are adding to the increase in total repair cycle time.

- Digital transformation of the repair process, well underway in 2019, was aggressively stepped up in 2020 by the insurance industry and supported by technology and information services companies. The virtual repair process model was becoming ubiquitous through the use of self-service photo estimating, artificial intelligence, AI and human intervention as a way to co-manage estimating vehicle damage. This model morphed into an auto-generated image capture of vehicle damage supported by adjuster exception-based estimating. Video estimating supported by AI, machine learning and computer vision, is inevitable and has already surfaced within many areas of claims processing.

- A gap continues to exist between insurers and OEMs regarding the OEM vehicle repair standard and its growing adoption and implementation and how to balance and resolve keeping the repairer out of the middle regarding repair procedures completed and payment for same. Despite the insurer/OEM repair standard gap, forward-thinking repairers took the opportunity to diversify their businesses by leaning into their relationships with OEMs through participating in OEM certification programs.

- As of November 2021, year-over-year inflation was at 6.1% and growing. Inflation jumped to 7.5% in January 2022.

- According to Enterprise Holdings, the average length of rental is now just over 17 days, an increase of 3.9 days from the fourth quarter one year earlier.

- Despite improvement in front-end claims repair process reduction, primarily due to a decrease in cycle time at first notice of loss (FNOL) assisted by telematics and AI, the middle to back-end of the repair process has been increasing due to many of the constructs mentioned above.

- We expect vehicle repair costs to rise moderately, but steadily, in the future due to several factors:

- A shortage of qualified and dedicated technicians, which is fueling the need for increasingly competitive employee acquisition and retention compensation programs.

- Increased vehicle repair complexity and embedded ADAS technology.

- Expense of participating in OEM certification programs, including training, equipment and tools.

- Increased use of OEM parts and additional line-item repairs due to OEM certification program participation requirements and growing acceptance of OEM repair standards.

- Growing long-term risk of existing and proposed country-of-origin tariffs raising the cost of automobiles manufactured outside the U.S.

- Short to medium-term Inflation.

Most repairers remained open during the pandemic. With business down 50% to 60% in the early days, repairers cut costs, accepted PPP money from the government and furloughed personnel. In some cases, repairers shuttered their businesses for a time, ultimately reopening with limited work. Many of these locations are single, mom-and-pop-style shops that will struggle to make the types of investments needed as cars become more sophisticated. This scenario means that more and more work will continue to shift to larger, more sophisticated operations with brand-specific training and certifications.

The disruption caused by the pandemic will accelerate change in ways that make it difficult to find clarity around both near- and long-term effects. The expected and unintended consequences of the pandemic will accelerate what we have profiled previously as the dynamic and interactive confluence of prevailing trends and conditions throughout the broader auto physical damage ecosystem.

We expect to emerge from 2021 with stronger nascent and legacy businesses that were well-capitalized pre-COVID-19 and with emerging disrupters that happen to be at the right place and time with new solutions within the broader aftermarket.

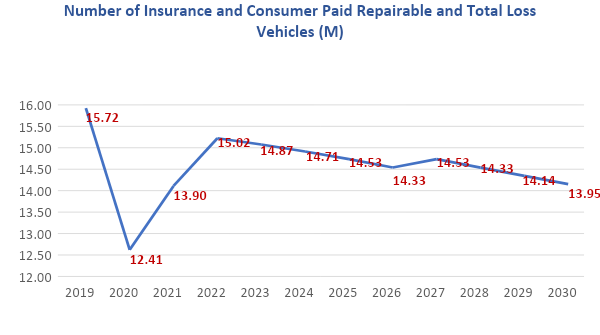

The pandemic caused a dramatic decrease in vehicle repairs and total losses from the 2019 total of 15.7 million to 12.4 million in 2020. 2021 saw a partial return to pre-pandemic levels, with 13.9 million vehicles repaired. However, our projections (see figure below) indicate that the industry is unlikely to ever return to 2019 levels as ADAS features continue to penetrate the population of registered vehicles and significantly reduce collisions. There may be some short-term anomalies in repair volume in early 2022 as the industry works to clear its record backlog as labor and parts shortages ease.

The average repair severity stood at $3,527 at June 30, 2021, up 6% compared with $3,327 for the prior 12-month period .

As shown in the chart below, the number of insurance and consumer paid repairable and total loss vehicles dropped precipitously in 2020, partially recovered over 2021 and 2022, but are unlikely to ever return to 2019 levels. The forecasted decrease between the 15.7 million repairs in 2019 and the 14 million repairs in 2030 is 12%.

Source: Romans Group and Insurance Solutions Group extensive market research informed by our understanding of the facts and trends related to ADAS adoption and its impact on repairable vehicles

See also: Insurance 2030: Implications for Today

Future View

There is no doubt that EVs (electric vehicles) and AVs (autonomous vehicles) will displace gas-powered cars – that transition has already begun. General Motors and Ford have vowed to phase out internal combustion engine (ICE) vehicles – GM by 2035 and Ford by 2030 — and some states will also ban gas-powered vehicles by 2035. Joint ventures between OEMs will also continue, such as those between BMW and Toyota on the Supra and Subaru and Toyota on an SUV. In fact, Ford just announced that it is splitting into two distinct business segments – Ford Blue managing legacy internal combustion engine (ICE) vehicles and Ford Model E for electric vehicles (EVs).

In addition, there is a related transformation emerging that will transform the future of the auto ecosystem – the new OEM strategy around the connected or software-defined vehicle (SDV), a term that describes a vehicle whose features and functions are primarily enabled through software, a result of the transformation of the automobile from a product that is mainly hardware-based to a software-centric electronic device on wheels. The implications are enormous and far-reaching. Current plans call for OEMs to earn subscription fee revenues in the tens of billions of dollars by 2030 for a wide range of travel, safety and entertainment products and services such as insurance, premium ADAS features and tailored brand and vehicle experiences that include family activities, off-roading adventures and performance-oriented outings.

The questions now are at what rate should we expect these changes and what will they mean to the many players, large and small, across the broad automotive ecosystem?

Let’s start here with five major short-term trends identified by CCC Intelligent Solutions:

- The changing work landscape and its continued impact on auto sales, traffic volumes and accident severity

- The growth of ADAS and connected-vehicle technologies

- Climate change and its emergence as a significant factor in the future of insurance risk and regulations

- New customer expectations in our on-demand, need-it-now world

- A carry-over from 2021: Increasing complexity given all these factors continuing to disrupt the status quo

Technology and the Future of Collision Repair: EVs, AVs, SDVs and Computer Vision

One major industry that will continue to be heavily affected by the proliferation of EVs, AVs and SDVs is the collision and mechanical repair industry. The EV market share in the U.S. at Dec. 30, 2021, was only 3.5%, but EVs may account for up to 40% of new car sales by 2030. One industry expert predicts that dealer service volume will decline by 35% while tire replacement, glass and visibility services and length of ownership will all increase with EVs. Until autonomous vehicles are widely in use by consumers, there will be many AV fleets, robotaxis, delivery and commercial trucks and trains, especially in and near urban areas.

OEMs are catering to Millennial and Gen Z consumers who expect online and app connectivity. And shops need to have an online presence to reach them because both generations look online for everything, including where to take their cars for repairs. OEM-certified repair networks will exert growing influence over repair procedures and referrals.

Collision repairers will need to pivot from traditional body repair work to become more like computer technicians. New and different skills will be required, and the industry may begin to seem more appealing to young people as compensation rates increase. Specialized training programs will emerge to serve this new profession. Vehicle repair costs could double between now and 2030. One industry expert predicts that in five years the average repair order will be $6,000 to $7,000 due to the increase in parts and technician costs as repair complexity continues. The collision repair industry of the future will need EV charging stations and dedicated work areas or separate locations to repair EVs.

OEMs and the Connected Vehicle Economy

Self-driving vehicle companies from Tesla to General Motors’ Cruise are racing to start making money with their technology, outrunning efforts by regulators and Congress to write rules of the road for robot-driven vehicles. This month, Cruise said that SoftBank Group will invest another $1.35 billion in anticipation of Cruise launching commercial robotaxi operations. Cruise is opening up its driverless robo taxi service to the public in San Francisco as it creeps toward commercialization.

OEMs will continue to push to certify collision repair shops, which means that the repair work must be done to each OEM’s recommended repair guidelines for shops to be part of these certified networks, receive repair referrals and maintain vehicle warranty provisions. This will likely increase the average cost of repair to auto insurers, putting upward pressure on auto premiums. It will also likely disrupt the multibillion-dollar aftermarket parts and distribution markets as more OEM parts are sold to certified repair shops. More auto insurer-OEM partnerships are likely to emerge out of economic pragmatism, especially as the capability to automatically generate real-time crash notifications and triage accident and repair management improes. Fifth-generation (5G) cellular network will enable this era of more reliable connectivity that facilitates faster data throughput rates and greater network capacities, while ultra-low latency ensures fast response times between senders and receivers.

Telematics will eventually connect everything to the vehicle, the urban infrastructure, homes and other property.

One regulatory movement that could impede or slow these developments is the “right to repair” legislation that is rapidly emerging at federal and state levels. These rights are positioned as giving consumers choice, the right to their vehicle’s data and safeguarding a free and fair repair market. Most notably among these proposals is the “Right to Equitable and Professional Auto Industry Repair Act” introduced by U.S. Rep. Bobby Rush (D-Ill.)

Summary

If we’ve learned anything from COVID, it’s that the future is not easy to predict or certain to unfold based on existing trends. However, we are confident that barring another “black swan” event in the next decade, the automotive ecosystem of 2030-2035 will be virtually unrecognizable from today. Some legacy market leaders will lose ground and disappear. New market entrants possessing truly transformative technology and business models will rise. New and unprecedented inter-industry partnerships and alliances will emerge. And, above all, evolving consumer preferences and choices will dictate almost all of the change.