Let’s face it, insurance is not an industry known for the quality of its customer experience. Rather, it’s an industry known more for its complexity, its lack of transparency and its stubborn adherence to old-fashioned ways of doing business.

Granted, some insurance providers are trying to counter this reputation -- a few have even been so bold as to appoint chief customer officers (yes, sadly, that qualifies as “bold” in the staid insurance industry).

Still, the idea of investing in a better customer experience is often met with skepticism in the insurance C-Suite. Those occupying the corner office may publicly affirm the importance of the customer experience, but, privately, they question the value of customer experience differentiation, unsure of the financial return it really delivers.

In an industry where actuaries are kings and numbers rule the day, the seemingly “soft” benefits of a great customer experience don’t carry much weight when it comes to allocating capital.

In reality, those benefits are far from soft -- it’s just that many firms aren’t well-versed in the economic calculus of customer experience, which requires a holistic, cross-silo view of financial impacts. (For example, the benefits of a plain-language policy summary from an underwriter may only manifest themselves downstream -- by reducing customer confusion, and preempting phone calls, to a service center.)

What many numbers-oriented insurance executives seem to crave is quantifiable evidence that, at least at a macro level, a great customer experience really does pay dividends.

And now they have that evidence.

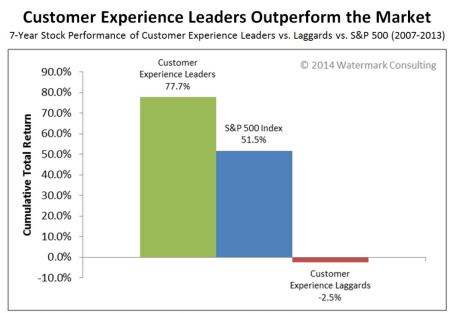

The graphic below illustrates the results of Watermark Consulting’s “2014 Customer Experience ROI Study.” The Watermark analysis sought to determine the long-term value of customer experience differentiation using a language that most any CEO would understand – shareholder value.

The study calculated the cumulative total stock returns for two model portfolios -- composed of the Top 10 (“leaders”) and Bottom 10 (“laggards”) publicly traded companies in Forrester Research’s annual Customer Experience Index rankings.

For the seven-year period ending in 2013, the Customer Experience Leader portfolio outperformed the S&P 500 market index by an astounding 26 percentage points. Perhaps even more striking was the performance of the Customer Experience Laggard portfolio, which posted a 2.5% decline in value, despite a big rally in the broader market.

The results underscore the benefits enjoyed by companies that invest in, and effectively execute on, a customer-experience strategy: higher revenues (because of better retention, less price sensitivity, greater wallet share and positive word-of-mouth) and lower expenses (because of reduced acquisition costs, fewer complaints and the less intense service requirements of happy, loyal customers).

Conversely, the study also provides a sober reminder of how customer dissatisfaction saps business value, by depressing revenues and inflating expenses.

Whether your firm is a public or private entity, the lesson here is clear: The market believes that companies that deliver a great customer experience over the long-term are simply more valuable than those that do not.

And that’s a message that insurance traditionalists should take to heart, because a great policyholder experience really is good for business.

Note: A complimentary report describing the 2014 Customer Experience ROI Study, including commentary on how the leading firms differentiate themselves, is available from Watermark Consulting.

The study calculated the cumulative total stock returns for two model portfolios -- composed of the Top 10 (“leaders”) and Bottom 10 (“laggards”) publicly traded companies in Forrester Research’s annual Customer Experience Index rankings.

For the seven-year period ending in 2013, the Customer Experience Leader portfolio outperformed the S&P 500 market index by an astounding 26 percentage points. Perhaps even more striking was the performance of the Customer Experience Laggard portfolio, which posted a 2.5% decline in value, despite a big rally in the broader market.

The results underscore the benefits enjoyed by companies that invest in, and effectively execute on, a customer-experience strategy: higher revenues (because of better retention, less price sensitivity, greater wallet share and positive word-of-mouth) and lower expenses (because of reduced acquisition costs, fewer complaints and the less intense service requirements of happy, loyal customers).

Conversely, the study also provides a sober reminder of how customer dissatisfaction saps business value, by depressing revenues and inflating expenses.

Whether your firm is a public or private entity, the lesson here is clear: The market believes that companies that deliver a great customer experience over the long-term are simply more valuable than those that do not.

And that’s a message that insurance traditionalists should take to heart, because a great policyholder experience really is good for business.

Note: A complimentary report describing the 2014 Customer Experience ROI Study, including commentary on how the leading firms differentiate themselves, is available from Watermark Consulting.

The study calculated the cumulative total stock returns for two model portfolios -- composed of the Top 10 (“leaders”) and Bottom 10 (“laggards”) publicly traded companies in Forrester Research’s annual Customer Experience Index rankings.

For the seven-year period ending in 2013, the Customer Experience Leader portfolio outperformed the S&P 500 market index by an astounding 26 percentage points. Perhaps even more striking was the performance of the Customer Experience Laggard portfolio, which posted a 2.5% decline in value, despite a big rally in the broader market.

The results underscore the benefits enjoyed by companies that invest in, and effectively execute on, a customer-experience strategy: higher revenues (because of better retention, less price sensitivity, greater wallet share and positive word-of-mouth) and lower expenses (because of reduced acquisition costs, fewer complaints and the less intense service requirements of happy, loyal customers).

Conversely, the study also provides a sober reminder of how customer dissatisfaction saps business value, by depressing revenues and inflating expenses.

Whether your firm is a public or private entity, the lesson here is clear: The market believes that companies that deliver a great customer experience over the long-term are simply more valuable than those that do not.

And that’s a message that insurance traditionalists should take to heart, because a great policyholder experience really is good for business.

Note: A complimentary report describing the 2014 Customer Experience ROI Study, including commentary on how the leading firms differentiate themselves, is available from Watermark Consulting.