The property and casualty insurance industry is turning to artificial intelligence (AI) to solve its most pressing issues. Record catastrophe losses created a demand for AI-driven climate models to better predict and manage risk. The pandemic accelerated investment in touchless consumer-facing technology like AI claims processing and remote inspections.

This past August, our team at Policygenius ran a survey to gauge consumer comfort around new tech being deployed by some insurance companies. The survey found that, despite faster claims turnaround times, the potential for lower rates and other AI-enabled transformations, customers still value a human touch.

A few other key findings from the survey include:

83% of consumers wouldn’t feel comfortable if their home, auto, or renters insurance claim was reviewed exclusively by artificial intelligence.

Around two in three consumers are resistant to the idea of purchasing insurance or filing claims on a website or app without speaking to a human being.

58% of drivers said they wouldn’t use an app that collects data about their driving behavior and location, even if this resulted in significant savings.

55% of homeowners said they wouldn’t install smart home devices that collect personal data, even if doing so earned them lower home insurance rates.

After a loss, around 43% of homeowners would agree to let a drone evaluate their property rather than a human.

Despite the increasing shift toward digitized insurance, customers in all age ranges still prefer the human element when it comes to purchasing coverage and filing claims.

The survey found that 72% of consumers wouldn’t be comfortable purchasing insurance online without ever speaking to a real person, and 64% wouldn’t feel comfortable filing a claim on a website or app without human interaction.

Claims reviews by artificial intelligence have skyrocketed in recent years as a means of cutting down on fraud and expediting the process. But just 17% of consumers said they’d feel comfortable if AI reviewed their claim from start to finish. Almost 60% said they were so uncomfortable with this scenario that they’d take the additional step of switching insurance companies to avoid start-to-finish AI claims.

Privacy concerns outweigh financial savings

Telematics and smart home tech can lead to lower premiums and risk reduction. But our survey found consumers haven’t fully embraced these products.

Around 43% of drivers said they’d use an app that tracks their driving behavior and location if they were offered a discount. But 74% of those drivers said they’d only use such an app if it lowered their rates by more than half.

These privacy concerns extend to homeowners and renters. Just 32% said they'd install a smart home device that collects personal data, even if doing so reduced their home or renters insurance rates by more than half. And 67% said that no home or renters insurance discount would be worth installing a smart doorbell camera that shares facial recognition data with third parties.

Consumers not ready for big tech to insure their home or car

Consumers are also wary of the possibility of a major tech company expanding into P&C insurance. Two in three consumers said they wouldn’t be comfortable with a company like Amazon insuring their home or car, with 40% saying it would make them very uncomfortable.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Pat Howard is a managing editor and licensed home insurance agent at Policygenius, where he specializes in homeowners insurance. His work and expertise has been featured in MarketWatch, Real Simple, Fox Business, VentureBeat, This Old House, Investopedia, Fatherly, Lifehacker, Better Homes & Garden, Property Casualty 360, and elsewhere.

Building a strong client base is the goal of every business, and providing good customer service is key to accomplishing it. The insurance industry has traditionally believed that good service means providing the human touch, with agents and office staff readily available to answer questions, make policy changes and process payments. But is this what your clients want and need?

As stated in Parature’s 2015 Global State of Multichannel Customer Service Report, 90% of consumers expect a brand or an organization to offer a self-service consumer support portal. In fact, according to Gartner Predicts, today’s customers manage 85% of the relationship with an enterprise without interacting with a human.How does this compare with your organization? If you aren’t providing your clients top-quality digital service, here’s why you need to do it now.

Saving Customers Time

Nearly three-quarters (73%) of all consumers say that valuing their time is the most important thing companies can do to provide them with good customer service, as reported by Forrester.Why? Because people are busy, and small business owners are no exception. That’s why they look for and expect the ability to manage their policy when it’s convenient for them. This means they always want easy access to their policy and billing documents and from any place. Business owners’ needs don’t stop at 5 p.m. when your office closes. Customers expect and want to be able to manage their policy, obtain proof of insurance, make payments and more, 24/7. With digital service, they can.

Promoting Customer Satisfaction

Clients who feelin control of theirpolicies tend to be more satisfied with their purchases, which can improve retention.

When you save your clients time and effort and give them the information and easy access to their accounts when they want and need it, you reinforce your value to them, as well as differentiate yourself from the competition. That’s good customer service!

But we all know that not all digital experiences are the same. At Insureon, for instance, we aim to partner with carriers with digital service centers to reinforce value and increase ROI.

When your clients use a digital app to manage their policies and make payments, you have more time to spend on activities that can help you build your business or work on more complex service needs. So, digital services are a win for you, too.

Changes in technology affect the way we live, and the buyers of insurance are no different than anyone else. As business owners, we need to meet our customers where they are and give them what they want.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Policyholders faced innumerable challenges within the past two years, resulting in unprecedented changes to their consumer behavior. Personal lines insurers responded swiftly to meet insureds’ new and evolving needs. They went all-in on digital self-servicing capabilities for customers, agents and employees, but recent market activity suggests that insurers’ top technology priorities of the past year may be different in 2022.

New research from SMA shows that the plans and progress of some transformational technologies are accelerating as others have hit the brakes. The “Transformational Technologies in P&C Personal Lines: Insurer Progress, Plans and Predictions for 2022 and Beyond” report offers a glimpse into which technologies have the most activity in the industry, where insurers are investing and what insurance executives think about the potential of the technology to transform their businesses.

Of the 13 technologies deemed transformational in the report, including AI-related innovations and others that fall outside of the AI family, six are seen as having a short-term impact on personal lines, yielding significant changes to business operations and the customer experience. The report also examines technologies in the mid-term horizon that are expected to become more mainstream in the industry in the next two to three years and long-term horizon technologies.

Personal lines insurers are currently reprioritizing their plans with a blend of investment activity and maturity levels. Research shows insurers currently favor digital capabilities that replace face-to-face interactions – continuing a trend that emerged early in the pandemic. One example of a technology under rapid development is virtual payments. Nearly seven in 10 personal lines insurers report investing in digital payment technologies during the pandemic, including mainstream services like Venmo and Zelle and insurance-specific vendors. While the initial focus has been on inbound payment solutions, SMA observes that piloting and implementation of outbound claims payment solutions are already beginning to expand.

When looking at long-term transformational technologies, 5G/edge computing shows increased promise in personal lines, with more insurers reporting interest in the technology now than in previous studies. Many of the possibilities related to the Internet of Things, autonomous vehicles and new user interaction technologies, and others will depend highly on the widespread availability and adoption of 5G. As the technology becomes more widely adopted, it is likely to move to the mid-term horizon before becoming a short-term technology.

As the pandemic continues to play out and a post-COVID era emerges, personal lines insurers will continually need to review and revise their technology strategies and plans. The move toward broad-based digital capabilities will require insurers to understand how specific technologies contribute to digital transformation and how priorities and road maps are changing in the current environment.

Heather Turner is the lead research analyst at Strategy Meets Action.

Turner supports SMA's advisory and consulting engagements through rich written content, quantitative and qualitative primary research, market and technology trend analysis and the management of SMA IP materials.

Prior to SMA, Turner was managing editor of the NU Property & Casualty Group at ALM, which includes the insurance industry publications PropertyCasualty360.com and NU P&C and claims magazines. She started her career as a journalist reporting on the property and casualty insurance industry at Insurance Business America and its sister publications in Canada and the U.K.

In response to COVID-19, the hospitality industry has stepped up its tech investment to facilitate safer guest interactions and cut costs. For example, some hotels have swapped out front desks for check-in kiosks as smart phones increasingly drive contactless guest interactions.

But keeping hotel guests and restaurant and bar patrons safe is just one part of how the hospitality industry can move toward full recovery. There remains a huge shortage of workers, and employers must keep their existing employees safe from the remaining threat of COVID-19.

And perhaps the most troubling risks have been linked to technology — cybercrime in particular.

Cyber risk skyrockets

Two of the worst data breaches of 2020 were at hotel chains: Marriott (the personal information of 5.2 million guests) and MGM Resorts (compromising the records of 10.6 million guests).

Cyber insurance premiums are rising as much as 30%, so hotels having strong cyber security can benefit with reduced premiums.

To start, hotels need basic protections like firewalls, antivirus software and regular system backups, with dual authentication and virtual private networks providing additional layers of protection. For these measures to be effective, employers must train staff on cyber security.

Regular outside system audits will spot holes in a security plan. And because vendor lapses may cause breaches, checking and auditing vendors’ cyber security practices should be part of a cybersecurity plan.

Cybercrime is not the only risk hospitality operations must confront, and training and educating staff on how to recognize reemerging risks is critical to keep any hospitality operation functioning.

Keeping workers and patrons safe from COVID-19 remains paramount. Vaccinations cannot fully protect individuals, as evidenced by breakthrough cases of the virus infecting those who are vaccinated. One well-documented outbreak occurred in a vacation spot with high vaccination rates. Keeping workers masked is important to protect employees and patrons.

There are other risks, as well. For instance, any establishment serving alcohol must remember that, in many states, they are held responsible for the actions of those who become intoxicated at their establishment. In some states, general liability policies do not cover this liability, but it is covered under separate liquor liability insurance.

As patrons may overindulge at times — especially as many haven’t been to bars and restaurants or taken vacations for more than a year — it’s important to update policies about serving alcohol and help servers learn how to minimize the risks. Part of this includes coaching staff on common signs of inebriation and on their right to refuse service.

Another risk in hospitality: the labor shortage. However, offering benefits, especially health insurance, can be an enormous advantage to attract and retain employees in hospitality.

As the hospitality industry continues to come back from a long, hard pandemic year, it’s important to keep in mind that the work is far from done. "Prevention" and "training" are the operative words to offset risks.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

In this webinar, ITL Editor-in-Chief Paul Carroll sits down with Jim McKenney, chief strategy officer and products business head at Intellect SEEC, and Sandeep Tandon, CTO of Intellect SEEC.

In this webinar, ITL Editor-in-Chief Paul Carroll sits down with Jim McKenney, chief strategy officer and products business head at Intellect SEEC, and Sandeep Tandon, CTO of Intellect SEEC. They discuss how companies can lay the groundwork for modernization and innovation by reconfiguring their approach to core systems.

You will learn:

--Why changes in the business environment require a modernized approach to underwriting

--How you can vastly increase the speed at which you deliver capabilities and new systems - cutting deployment times to hours or days, from weeks or months, while delivering a clear ROI

--Why you should think in terms of microservices and application programming interfaces (APIs), decoupling capabilities from core systems so they can be deployed flexibly across the whole enterprise

Sandeep is passionate about technology with strong capabilities in architecting solutions for banking and insurance. He has been recognized for delivering top-level technology experiences across business segments and consistently delivering customer focused solutions. He is experienced in visualizing and capturing the transformational potential of emerging technologies.

In his 30+ years of experience working with global banks and insurance companies, Sandeep has demonstrated success in delivery of large-scale projects through the initial specification, design, development and implementation phases. His understanding and knowledge of the industry and technology has allowed him to successfully provide thought leadership to customers through innovative solutioning/consulting. Sandeep brings an extensive ability to connect business and technology to create solutions that result in value creation.

Jim McKenney

Intellect SEEC, Chief Strategy Officer and Products Business Head

Jim McKenney is Chief Strategy Officer and Products Business Head at Intellect SEEC. Jim is an experienced insurance executive, spending 18 plus years in various roles for Liberty Mutual Insurance. Most recently, Jim led Liberty's Product and Underwriting organization for the mid and large commercial segment. Prior roles include experience in small commercial underwriting segments and in various finance roles. Jim is a certified public accountant and graduated from the University of MA Amherst.

Paul Carroll

Editor-in-Chief, Insurance Thought Leadership

Paul is the co-author of “The New Killer Apps: How Large Companies Can Out-Innovate Start-Ups” and “Billion Dollar Lessons: What You Can Learn From the Most Inexcusable Business Failures of the Last 25 Years” and the author of “Big Blues: The Unmaking of IBM”, a major best-seller published in 1993. Paul spent 17 years at the Wall Street Journal as an editor and reporter. The paper nominated him twice for Pulitzer Prizes. In 1996, he founded Context, a thought-leadership magazine on the strategic importance of information technology that was a finalist for the National Magazine Award for General Excellence. He is a co-founder of the Devil’s Advocate Group consulting firm.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Coming soon... A three-digit hotline for mental health emergencies

Crisis services use has increased year after year as accessibility improves and people are more aware of their benefits. Established in 2005, the National Suicide Prevention Lifeline has answered over 12 million calls. The Crisis Text Line, founded in 2013, has responded to over 5 million conversations. Given the ever-emerging technology and science surrounding crisis intervention, these services are continually evolving. Training and accreditation processes improve standards, professionalism and quality assurance.

What is the New Movement to 988 Crisis Hotline?

In many ways, I am encouraged by moving our mental health crisis support to the 988 call system. First, 988 is much easier to remember than 800-273-8255, so access to qualified mental health crisis supports should increase significantly. Second, with the appropriate infrastructure and funding support required to make this successful, the shift to 988 symbolizes the importance of mental health crisis support. 911 responses to community safety will be on equal footing in importance to the 988 mental health crisis responses. Third, I hope that this shift to 988 also means a shift in the way crisis services are delivered:

Less reliance on a law enforcement response and increased engagement with peer support

Less fear and more compassion

Finally, the development of 988 will bring a much-needed coordination of services similar to air traffic control. So, people will have a better chance of getting matched to the right level of service.

In late 2019, a law to create a three-digit number for mental health emergencies came into effect. It will pave the way for more support, implementation and adoption of the 988 number many call centers already use, and make it easier for people in distress to get the support they need.

More Accessible

A simple three-digit number is easier to remember and dial during mental health emergencies. In addition, the branding of the new crisis response will go beyond just support for people experiencing suicidal despair and will include all psychological emergencies and even emerging mental health hardships. The design of the new system is intended to help facilitate a warm-handoff connection to qualified supports and to follow up to make sure those referrals are a good fit.

To work, funding and infrastructure support need to be commensurate with the scope of the shift to 988. This will resolve the funding issues that make it hard for local crisis centers to respond to callers through the current line.

Taking the National Suicide Prevention Lifeline as an example, there is a general misperception in the community about how the Lifeline works. While the leaders of the Lifeline call center system are under one umbrella, each call center is responsible for its own funding and operation. As the calls to the Lifeline have swelled each year, the call centers have been left to manage the load with minimal margins. The increased support required by the shift to 988 will give the call centers a fighting chance to be sustainable.

Less Fear, More Care

The 988 line will significantly reduce the numerous problems arising from calling 911 during mental health crises and help people get the assistance they need.

911 usually activates a law enforcement response. Law enforcement is best-suited to take control of chaotic and life-threatening situations. The skills and mental abilities of law enforcement under these circumstances are NOT best when responding to someone having a mental health crisis. Many police officers can feel out of their element when responding to people who are despondent, grieving, traumatized or highly anxious.

Additionally, for communities of color or for transgender people, a 911 call can often escalate to violence, regardless of the nature of the call. People of color living with mental health conditions are much more likely to be detained than white people. Thus, they are highly reluctant to call 911.

988 will link people to crisis responders trained to help them cope with and feel supported and understood during suicidal intensity and other mental health challenges. They’ll get the assistance and care they need instead of becoming embroiled in aggressive altercations with the law or ending up in institutions ill-equipped to help them recover. So, calling for help will connect them to people trained to listen empathically and provide accurate information and referrals instead of worsening their situations.

Help During the Transition

The line won't be available for another year. Given the mental health crisis caused by the pandemic, that's disheartening and distressing. Policy and funding changes that could help significantly during this transition include:

Establishing LOSS teams in every community for suicide “post-vention” support

Establishing peer respite centers in more regions for people experiencing mental health challenges who do not need urgent care

Encourage the continued development and evaluation of technology (e.g., virtual peer support, apps for peer support)

Looking Forward: Additional Advancements

988 call centers need to not only be prepared to support people experiencing suicidal intensity but also people affected by suicide death. Many crisis call centers would benefit from specialized services addressing the complicated trauma and grief suicide brings.

Integrating more people with lived experience with suicide and mental health crises will be essential in 988's effectiveness. The voices of people who have been there give us tremendous insight into what works and what doesn’t – when the focus is on helping people. What the wisdom of people with “lived expertise” tell us is that we will all be better off moving away from a fear-based approach and toward one built on upholding dignity, collaboration and compassion.

The new law is a significant and positive development. It promises an opportunity to reduce the bias of mental health issues and people fighting through them. Three simple numbers—988—send an unspoken message that these emergencies are legitimate and require a different kind of care and vigilance.

Sally Spencer-Thomas is a clinical psychologist, inspirational international speaker and impact entrepreneur. Dr. Spencer-Thomas was moved to work in suicide prevention after her younger brother, a Denver entrepreneur, died of suicide after a battle with bipolar condition.

It is difficult to imagine where digital business operations would be today if it wasn’t for the catalyst that is the pandemic. For nearly two years, businesses across industries, and especially within insurance, accelerated digital transformation plans to adapt to remote access for customers and employees. Insurers prioritized many self-service capabilities, such as virtual inspections, digital payments and automated workflows, while also focusing on investing in artificial intelligence (AI), the Internet of Things (IoT), new user interaction tech and other advanced technologies. However, as the effects of the pandemic continue to play out, market activity indicates commercial lines insurers are reprioritizing their tech-oriented projects, with some plans continuing to move forward while others have slowed down.

Today, there are 13 “transformational” technologies working with foundational technologies, such as core systems, portals and CRM systems, to move the insurance industry into the new digital-connected era. A new SMA research report, “Transformational Technologies in P&C Commercial Lines: Insurer Progress, Plans and Predictions,” examines these technologies and how they will affect commercial lines insurers now and in the future.

Commercial lines insurers are approaching both AI-related and non-AI-related transformational technologies at varying levels of investment and rates of adoption. Over the years, SMA has monitored these technologies, organizing them into three strategic planning horizons: short-term, mid-term and long-term.

In 2022, computer vision, IoT, machine learning (ML), natural language processing, robotic process automation, user interaction tech and virtual payments will continue to garner significant activity and yield a high impact on commercial lines. However, some insurers indicate they are decelerating their plans for certain short-term technologies. Last year, 51% of commercial insurers said they were in the midst of new implementations of ML solutions, but the plans through 2022 show only 45% implementing, primarily among Tier 3 and 4 companies. This pullback in building ML capabilities for smaller insurers is mainly due to the events surrounding the COVID health crisis.

When looking further into the future, 5G/edge computing, blockchain, AR/VR and autonomous vehicles are expected to have a transformational impact on the industry. Compared with a year ago, more commercial lines executives recognize their potential in certain business segments. For example, the potential for 5G/edge computing increases as the major wireless networks expand coverage and more devices accommodate the technologies. In a 2021 SMA survey, 24% of commercial lines insurers reported that they are monitoring and developing initial strategies around 5G/edge computing, up from just 18% in 2020. A range of areas within commercial insurance can be transformed by 5G, including IoT, autonomous vehicles and new UI technologies. So as the technology becomes more widely adopted, it will likely become a short-term technology for insurers’ planning purposes.

The transformational technologies underway in the industry today will only become more critical as virtual and digital interactions become the norm. Regardless of where commercial insurers are on their digital transformation journey, their strategies must be continually reviewed and revised in today’s ever-evolving technology landscape.

Heather Turner is the lead research analyst at Strategy Meets Action.

Turner supports SMA's advisory and consulting engagements through rich written content, quantitative and qualitative primary research, market and technology trend analysis and the management of SMA IP materials.

Prior to SMA, Turner was managing editor of the NU Property & Casualty Group at ALM, which includes the insurance industry publications PropertyCasualty360.com and NU P&C and claims magazines. She started her career as a journalist reporting on the property and casualty insurance industry at Insurance Business America and its sister publications in Canada and the U.K.

The Future of Work. Plus, 2022 resolutions to foster innovation; building a digital field of dreams; 3 keys to enhancing the customer experience; and more.

Some 20 years ago, I collaborated on a white paper with Bill Gates and other senior leaders at Microsoft on the future of work, to be the centerpiece of the annual gathering he held in those days for Fortune 500 CEOs at his home.

He framed a problem in a way that has stuck with me. It has yet to be solved — but that’s where you and your companies come in, as you take advantage of what we’ve all learned during the pandemic and map out new ways of working as we scope out a new normal.

The problem concerns focus — and how to get a lot more of it in our work lives.

Register now for a "crystal ball" view into 2022 to understand where your customers, martkets, technology and competitors are heading so that you can adapt to capture these opportunities.

With conversational AI, insurance companies can deliver easier and more convenient digital support to customers, improve agent experience and productivity, and reduce contact center traffic.

Paul Carroll Editor-in-Chief and Dr. Michel Leonard, CBE, head of the Triple-I’s Economics and Analytics Department, discuss the Triple-I’s latest Insurance Economics Outlook for Q4 2021 focusing on this year’s unusually wide range of growth and inflation forecasts and key performance indicators for the P&C industry in 2021

"Even before a commercial version of the internet browser was invented in the early 1990s, the rich, geeky types I dealt with in my travels at the Wall Street Journal were figuring out ways to wire their homes to ward off possible intruders."

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

An agency partner in Ohio recently submitted a California-based residential plumbing contractor for underwriting consideration, needing expedited review to avoid project delays. Using virtual tools, a Nationwide loss control services expert in Texas quickly contacted the contractor in California for a virtual survey and jobsite assessment, helping us accurately price the account while also providing valuable risk management expertise from his extensive experience working with residential plumbing contractors.

Just two years ago, this scenario might have posed a challenge for many carriers as they tried to accurately understand and price the risks, but in today’s age of historic digital adoption, it was an opportunity to showcase Nationwide’s tech-driven, customer-focused protection, which allowed us to put the right associate on the right risk.

Today’s business owners are working hard to continue serving customers while navigating extended supply chain disruptions and labor shortages. When it comes to insurance, they need their carrier and agent to work just as hard for them to prepare and protect their business for risks that lie ahead.

Nationwide’s latest Agency Forward survey found many business owners are missing openings to use risk management planning to help defend their business from costly disruptions and accidents – presenting an opportunity for agents and carriers to advise commercial clients about the importance of understanding and mitigating their business’s risks and the considerable impacts these efforts can have on their company’s bottom line.

The business owner survey revealed three key themes for agents to consider as they prepare for annual check-ins with clients:

Business owners want easy claims processes and industry expertise from their agents and carriers.

Risk management planning can help prevent costly disruptions or claims.

Agents can help clients mitigate risk and navigate claims.

Speed, ease and industry expertise top business owner needs when filing a claim

Eighty-five percent of the anonymous business owners surveyed who filed a claim in the past 12 months report being satisfied with their experience, yet some owners still struggle with navigating the claims process with their carriers. In fact, a quarter were dissatisfied with their claims experience, saying it was difficult (25%) or slow (24%), while another one in five say it was challenging to track the progress of their claim (22%) or that their insurance agent wasn’t helpful (21%).

Carriers who lean into quick claims handling when possible, clear communication and strong industry-specific expertise in claims can deliver a smoother experience for business owners, giving them confidence they’ll be back up and running quickly.

Nationwide has reduced average claim cycle times for business owners with easy filing online or by phone, digital payments and dedicated claims experts with deep knowledge in clients’ industries and the challenges they face. Customers also have access to solutions like the Nurse Triage Hotline to get qualified medical professional advice after an accident to help determine an effective course of action.

Risk management planning can help prevent costly disruptions or claims

Across the board, business owners believe risk management plays a significant role in protecting their business, employees and customers. However, owners’ risk management actions greatly differ based on their business’ size.

More than a quarter (27%) of small business owners say they have no risk management practices in place at all for their company, compared with just 4% of middle market business owners who don’t have practices in place to mitigate risk.

Further, middle market business owners are much more likely than their small business owner counterparts to be using carrier-offered risk management services. Business owners report using in-person/on-site services, safety program development and review and online resources most often. Just four in 10 middle market business owners, and about a quarter or less of small business owners, say they leverage digital risk management tools or virtual/teleconference services.

As business owners reconsider the locations of their offices and how they will be doing business in the future, in-person or virtual safety resources such as Nationwide’s virtual risk management consultations offer industry experts to review client programs, identify potential risks and provide solutions to keep their businesses running smoothly – no matter where they’re located or how they’re doing business.

Agents can help business owners mitigate risk and navigate claims

The survey found agents have opportunities to help clients better understand how adequate business planning and risk management programs can bolster their company’s performance, workforce retention and preparation for coming challenges.

Timely claims reporting is critical to getting your company back to work quickly. On average, commercial lines claims are reported 20 days after the event of loss, adding as much as 15% to the life cycle of a claim.

Many business disruptions are preventable. Taking time to ensure proper housekeeping, maintenance and business continuity planning is in place can reduce costly disturbances and decrease recovery time.

With the average cost of a fleet accident at approximately $70,000 and auto accidents being the leading cause of work-related fatalities in the U.S., for many organizations their fleet operations pose their greatest liability and workers’ compensation risk. It is important that organizations establish a formal fleet safety program to protect employees and reduce accident risk.

Agents who are able to deliver this counsel in the moment, while understanding the carrier-supplied solutions to benefit their clients, can open doors to deeper relationships and smoother experiences for clients leading into the year ahead.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

The biggest myth in healthcare is that better care costs more. The city of Fort Worth, Texas busted that myth. Using advanced analytics to establish and monitor a provider network, the city got its injured employees better care while driving its workers’ compensation costs down, not up.

In 2015, Fort Worth had 6,250 employees, and its total workers’ compensation costs ‒ claims plus indemnity payments ‒ were $9.7 million. After implementing the provider network, the city’s costs in 2016 fell to $9.1 million, and they’ve fallen every year since. In 2019, the costs were only $8.2 million, despite the city’s number of employees increasing to 6,900.

How?

How did Fort Worth do it? The city created a physician panel under Chapter 504 of the Texas Labor Code that would be available to its employees only. To identify the providers to include, the city applied the outcome algorithms described below to two juxtaposed data sets and found the providers achieving the best outcomes for each injury type ‒ who cost the city less, not more.

Healthcare is not a commodity. We all think that our doctor is the best ‒ or at least above average ‒ but we don’t live in Lake Wobegon, where all the children are above average. Exactly half of all children are above average, and exactly half are below. It’s the same with doctors ‒ and the specialists and surgeons that they refer us to, and the hospitals that they put us in.

Although counter-intuitive, going to a good doctor costs less overall than going to a bad one. 30% of healthcare costs are unnecessary, the result of poor or ineffective care. Good doctors don’t incur those excess costs because they:

Make fewer errors;

Perform fewer unnecessary procedures;

Experience fewer patient complications; and

Get their patients better faster.

So how can you do what Fort Worth did? First, you need access to the two data sets on which to run the analytics ‒ your medical and pharmacy claims and your employee absence records. If you’ve self-insured your workers’ compensation program, like Fort Worth does, then you own the medical and pharmacy claims. You still engage a third party administrator (TPA) to process those claims for you, but you are at actuarial risk for them, and therefore you own the claims. If, on the other hand, you’re fully insured ‒ you pay the insurance company a premium, and the insurance company bears the risk ‒ then you won’t own the claims and won’t be able to perform these analytics, although your insurance company could.

If you have the claims, then you match them against the absence records to identify the time that the employee missed from work because of the injury. You can do so in two ways. First, juxtapose the claim dates against your Human Resources (HR) Department’s time and attendance records to find the days missed because of the injury and value that time off at the employee’s pay rate or a normalized rate. Alternatively, you can use the indemnity payments to the employee as a proxy for the absence costs. When a TPA or insurance company uses these analytics, this is the route that they take because they don’t have access to the employer’s HR records.

Next, you must be able to direct care ‒ tell the employee which provider to go to. Every state has its own rules. In Texas, an employer can do so. This can include establishing referral protocols and criteria for medical procedures that don’t require pre-authorization ‒ decreasing the wait times to obtain care and thereby driving down lost days and indemnity payments.

If you meet these three criteria ‒ you own the claims, can direct care and have absence data ‒ read on and learn how you, too, can drive down your workers’ compensation costs while improving the care for your injured employees.

Quantifying Outcomes

We begin with the premise that a “good outcome” is getting an employee back to work and keeping them there. We therefore accumulate all the costs to do so and then rank the providers based on the outcomes that they achieve.

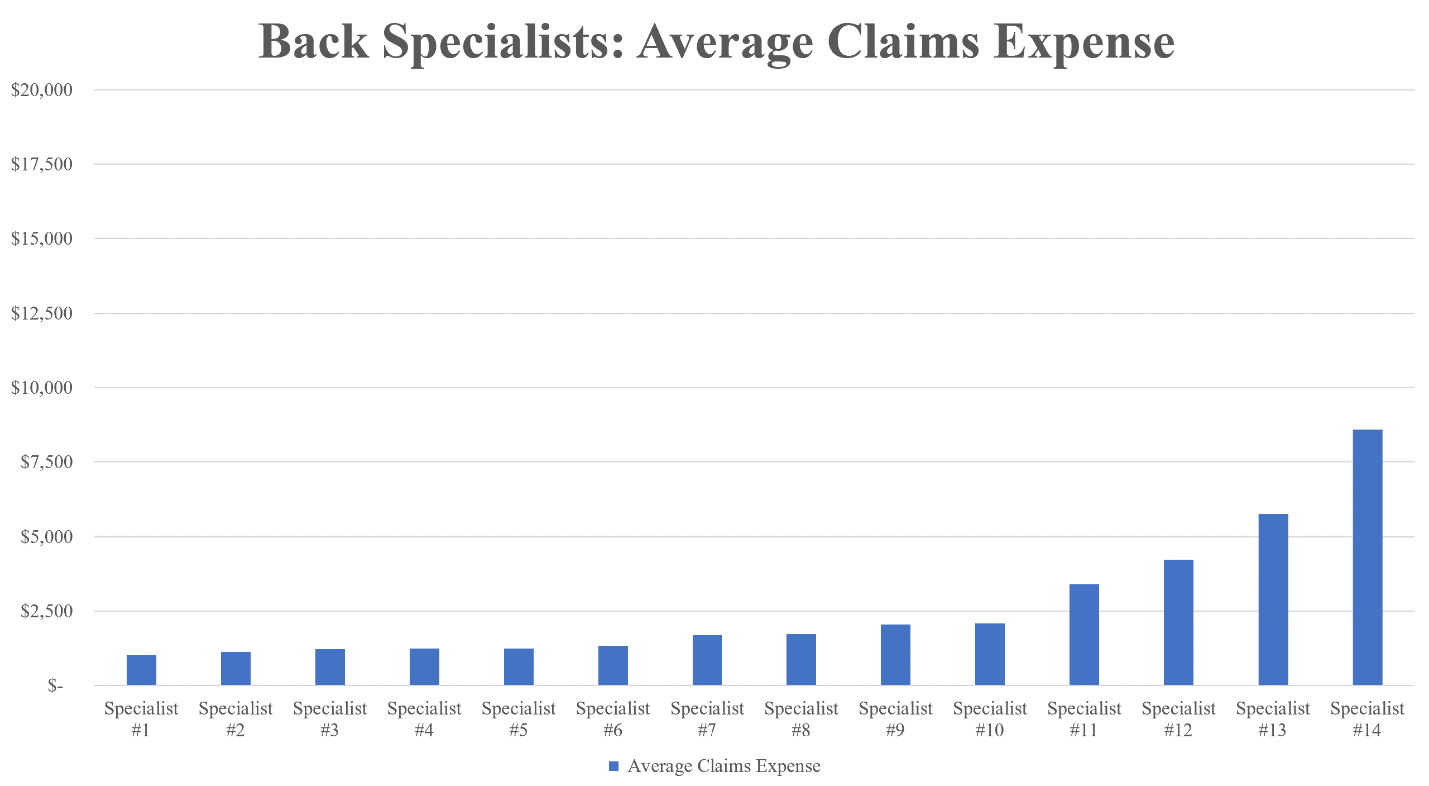

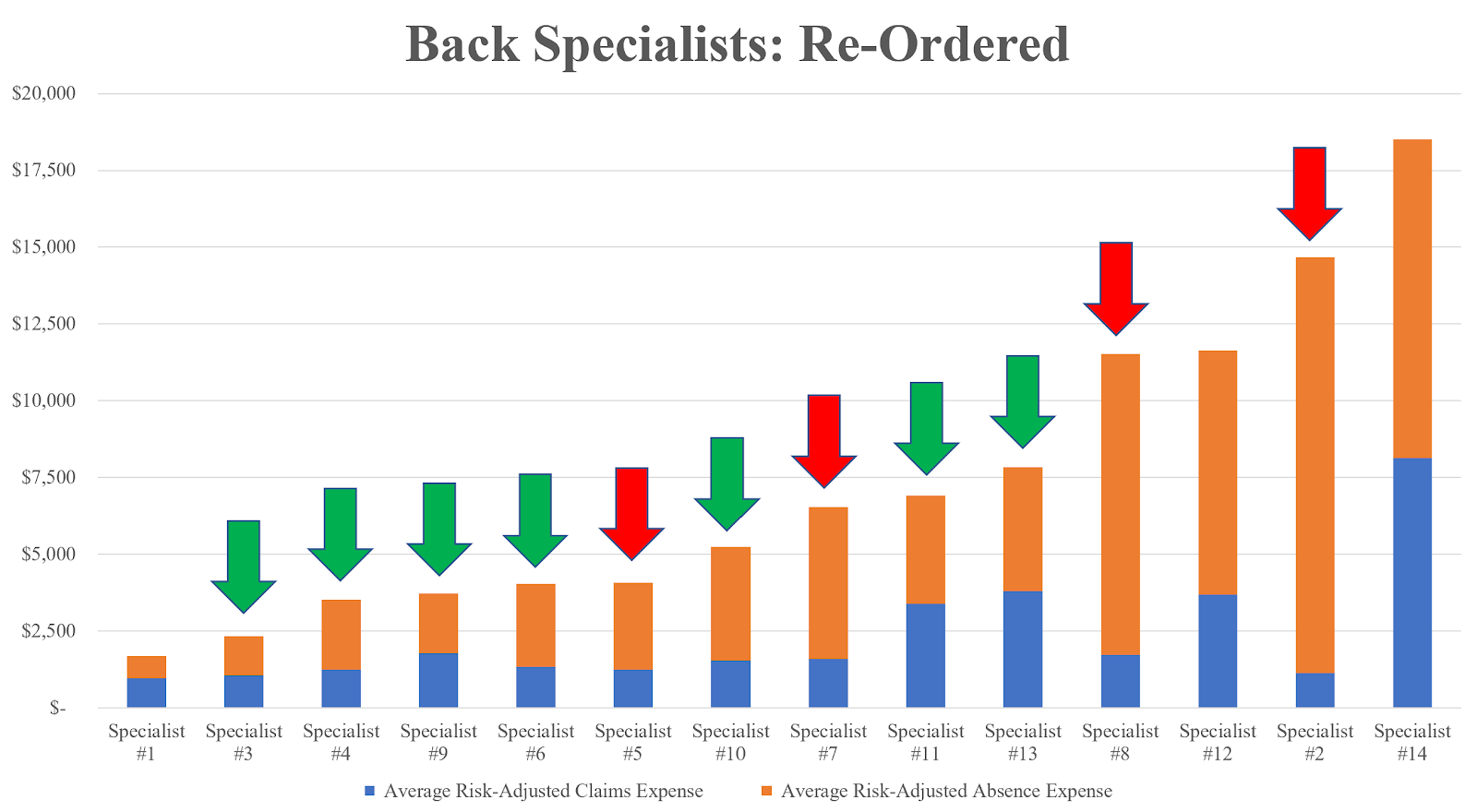

First, let’s look at the claims. The chart below shows the average claims costs for 14 specialists treating back injuries. Specialist #1 on the far left is the best, with average claims costs of $1,000, while Specialist #14 on the far right is the worst, at $8,600.

The claims, however, are only half of it ‒ sometimes less than half. You have to add the absence costs, the amounts that the employer paid the employee while out with their injury. Not only are these absence costs a real cost to the employer, but they double as an indication of the effectiveness of the care. The quicker the doctor got the employee better and back to work, the more effective the doctor was. This chart adds each specialist’s average absence costs on top of their claims.

Now Specialist #2 goes from being second best to second worst; and Specialist #9 is doing a better job than we originally thought because that doctor is getting their patients better and back to work faster.

There’s one more step. If you ask any doctor why their costs are more than another doctor’s, they’ll always give the same answer: “Because my patients are sicker.” And sometimes they’re right.

Sicker patients cost more and take longer to get better. If you have two employees with the same back injury, one of them young and otherwise healthy, while the other is older, overweight and diabetic, the older employee is going to cost more. So we adjust for comorbidities by assigning each employee a risk score. That way our rankings are based solely on the provider performances, not the patients that they treated.

There are a number of risk-scoring systems. One that is open-source is the Chronic Illness and Disability Payment System (CDPS). CDPS was designed by the University of California, San Diego and is employed by many Medicaid programs around the country. Accordingly, it is demographically appropriate for a working age population.

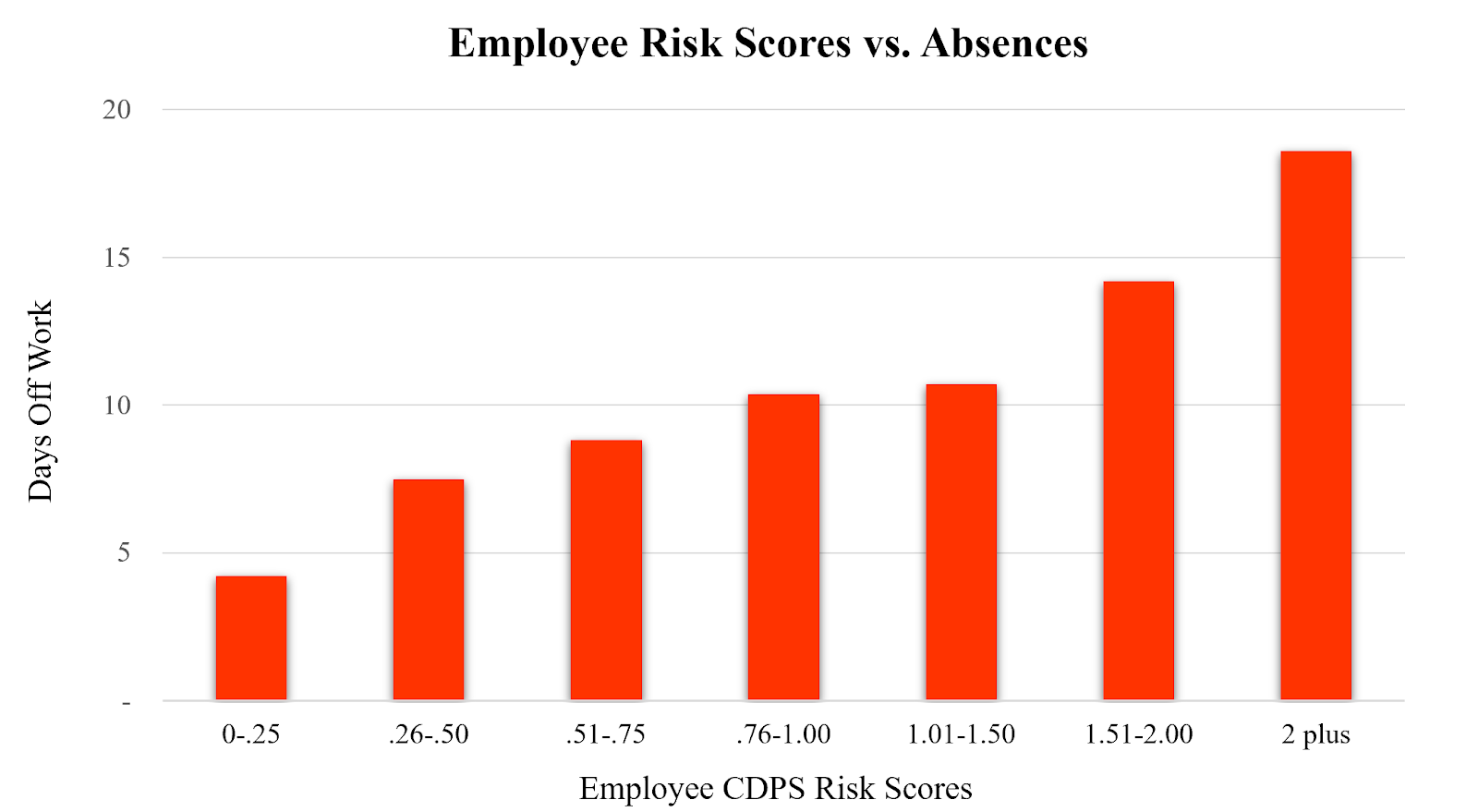

The CDPS system looks at various demographic and clinical data, including age, gender, diagnoses and the prescription drugs that a patient is taking and assigns the patient a score: 1.00 being an individual of average health, below 1.00 healthier than normal (the lower the score, the healthier) and above 1.00 sicker (the higher the score, the sicker).

The chart below shows the relationship between an employee’s risk score and the number of days that they miss from work. As you would expect, the higher the risk score ‒ the less healthy the employee ‒ the more time that they miss.

Going back to our back specialists, when we risk-adjust their patients and level the playing field the results change again.

Now the doctors’ total costs and rankings are based on their performances, not the patients that they treated. Doing this, we see that Specialist #13 was doing a better job than we initially thought. This doctor would now be ranked 10th, not 13th.

When we re-order the doctors based on their average risk-adjusted total costs, Specialist #1 is still the best, and Specialist #14 is still the worst. But other than Specialist #12, the order has completely changed. The green arrows show the doctors who moved up, and the red arrows show the ones who moved down.

We can also show this on a quadrant graph. Along the horizontal axis, we graph each provider based on their average claims costs relative to the group average, and along the vertical axis we do the same for the absence costs. The best providers are in the upper right quadrant ‒ low claims costs and low time off ‒ and the worst providers are in the lower left quadrant, with high claims costs and high time off.

Fort Worth’s Provider Network

Fort Worth used these analytics to identify the best providers by injury type and then placed them in its own workers’ compensation provider network. An injured employee must stay within this panel when seeking treatment.

But Fort Worth didn’t just look at its workers’ compensation claims and rank the doctors handing its current cases. Instead, it threw in its health plan claims, too. That way, it identified great doctors not currently handling workers’ compensation cases, but whom the city wanted to in the future.

By sending injured employees to the best doctors, Fort Worth achieved fantastic results ‒ a decrease of 23% in its costs while getting its employees better care!

Benchmarking and Predictive Analytics

Fort Worth didn’t stop there, but incorporated the Official Disability Guidelines (ODG) for benchmarking and predictive analytics, too. ODG is a nationwide database of workers’ compensation and occupational health injuries owned by the Hearst Health Network.

Using these guidelines, Fort Worth not only compares the providers in its network against one another but benchmarks them against national and regional best practices and averages for claims, time off work and other metrics. These other metrics include whether the doctor is seeing the employee more often than usual for a particular type of injury, or whether the doctor is billing unusual procedure codes (which could be either good or bad but bears investigating). In addition, comparing claims against the database allows Fort Worth to categorize them as being within the normal range for that injury type ‒ which the city can pay without further scrutiny ‒ or outside those norms, in which case the city flags the claims for investigation.

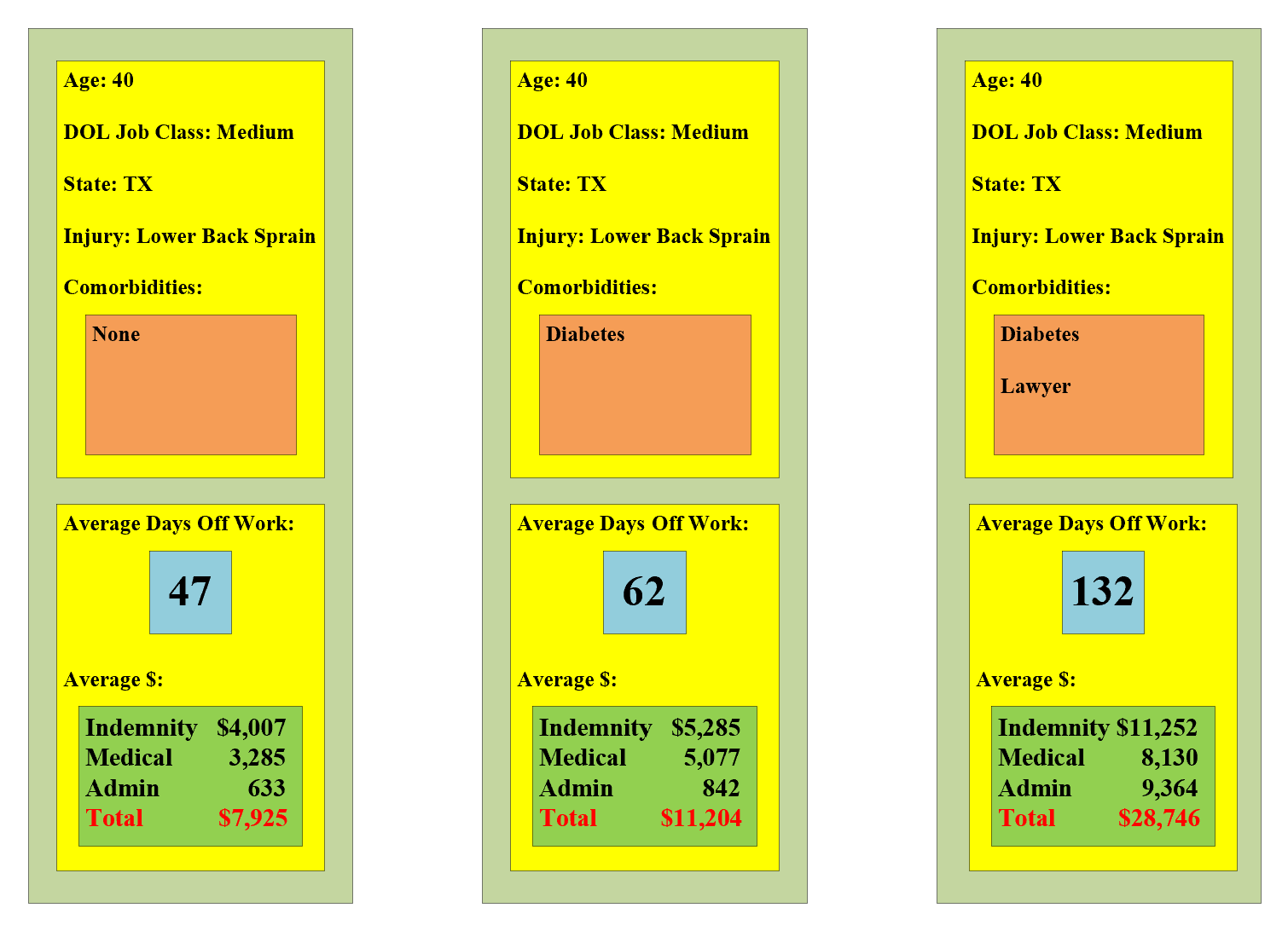

Fort Worth also uses the guidelines to perform predictive analytics. When an injury occurs, the city predicts the claims and lost time based on specific factors and then monitors the case and intervenes early when the actual results begin to stray from the predicted ones. For example, using ODG, the table on the left predicts 47 days off and $7,925 in total expenses for an employee suffering a lower back sprain with the following particulars:

40 years old

Living in Texas

Job involves “medium” physical demands (not sedentary, like an office worker, or heavy, like a construction worker)

No risk factors or comorbidities

Case involves some time off work, so it is more severe (80% of all workers’ compensation cases involve only medical expenses, no lost time)

The table in the middle shows that keeping everything the same, except adding that the employee has diabetes, increases the prediction to 62 days off and $11,204 in total expenses. And the table on the right shows that, if the employee hires a lawyer ‒ not a comorbidity for an employee, but definitely a risk factor for an employer ‒ everything more than doubles!

Health Plans

You can use these analytics for your health plan, too. When doing so, there are two differences.

As discussed above, in workers’ compensation, many states permit the employer to direct care. In most health plan settings, however, you can’t do that. You can only encourage someone to go to the best doctor. They can go to whomever they want.

So how do you get your employees and their dependents ‒ your health plan members ‒ to the best doctors for what they need? You could ask your TPA to include only the best doctors in the provider network, or at least eliminate the worst ones, but your TPA usually won’t do that. In fact, many of the contracts that TPAs sign with health systems preclude the TPAs from excluding any of the health system’s providers from the network or steering patients away from them.

Although you won’t be able to set the network, you can stratify it. Tier the network and decrease or eliminate co-pays and out-of-pocket costs when members go to the best doctors. If you have an HDHP (High Deductible Health Plan) married with HSAs (Health Savings Accounts), you can even pay employees to go to the top-ranked doctors by contributing to their HSAs when they do so.

You can also give a list of the best providers for each root diagnosis to:

The case managers handling your high-cost and chronically ill members so that those case managers can suggest the best providers to them;

The primary care physicians (PCPs) in your network to use when referring your members to specialists and surgeons; and

The employees themselves so that they and their dependents can look up the best providers for what they need.

The second difference is that your health plan will have not only employees in it but their dependents, too. You won’t be able to use the algorithms above on the dependents because you won’t have any absence data to match against their claims.

Instead, you can use a different algorithm on the dependents that uses only the claims data. For the employees, we combine the claims and absence data and ask how much it cost and how long it took to get the employee back to work and keep them there. For the dependents, we flip the question and ask how much it cost in claims to keep them well.

We define being well in terms of healthy days, which we can see in the claims. Healthy days are days that the person does not spend in the healthcare system (e.g., hospital stays, doctor’s visits, etc.) or at home in a non-functional state (e.g., recuperating or otherwise unable to carry out their normal activities).

We put this information in a fraction. The numerator is the patient’s risk-adjusted claims for a particular root diagnosis during the year, and the denominator is the patient’s healthy days during that year. We then rank each provider by root diagnosis, from the best with the lowest average risk-adjusted claims per healthy day when treating patients with that condition, to the worst with the highest.

Not only can you rank providers based on their claims per health day, but you can rank wellness programs and just about anything else, too. The chart below compares the risk-adjusted claims per healthy day to keep employees with behavioral health issues at work (instead of out sick) against the claims per healthy day to keep employees without those issues at work (almost everyone has some claims and absences during a year). The risk-adjusted claims per healthy day for a person without any issues is $10, while the claims per day for a person with headaches is double that at $21 per day, and the claims per day for a person with drug and alcohol problems is double that again at $44.

Better Care at Lower Costs

,Fort Worth busted the myth that better care costs more. By sending injured employees to the best doctors the city drove down its costs, while getting its employees better care.

This article originally appeared in the March/April 2021 issue of Public Risk, the member magazine of the Public Risk Management Association (PRIMA).

Get Involved

Our authors are what set Insurance Thought Leadership apart.