|

May ITL Focus: Customer Experience

ITL FOCUS is a monthly initiative featuring topics related to innovation in risk management and insurance.

Discover 'The Future of Risk™': Innovation, Tech, & Disruption Insights from Industry Leaders!

ITL FOCUS is a monthly initiative featuring topics related to innovation in risk management and insurance.

|

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

The instant grades, based on completely inadequate data, illustrate the dangers of false precision that show up in lots of projections about insurance.

As soon as the NFL draft ended Saturday night, we all waited anxiously to see how the various pundits would grade our teams' selections. But if you step back even a little bit, you see how ridiculous those grades are — and that they are symptomatic of an issue that can skew the judgment of lots of executives, including in insurance. The issue is false precision.

It's certainly fair to judge the players and the teams drafting them. How big, fast, strong, etc. is a player? What does the tape show about how they fared against competition in college? How well do they fit a team's needs? And so on. But that sort of general analysis isn't enough for the analysts — or for us as fans. All the attributes of a player get boiled down to a grade. Some player is an A- pick, while another is a B or a C+. The same sorts of ultra-precise ratings are rendered for teams.

Yet the data doesn't come close to supporting such precision. As the saying goes, those being drafted have to this point faced a lot of college players who are now headed off to become accountants, and not a one of the players has yet faced a pro team. Who knows how a quarterback will react when he realizes that TJ Watt is going to hit him all game?

And there's so much uncertainty about how players will last physically playing a brutal game. My Steelers used a third-round pick on a linebacker who won awards last season as the best in college football and has all the physical attributes to be a great pro, but he has a history of injuries and is reportedly lacking an ACL in one knee after tearing it twice. The data tells me he warrants a grade somewhere between F and A+. Ask me in a year or five, and I'll have a better idea.

The way the data is turned into grades raises questions, too, about how precise the analysis actually is. Just about anybody can hang out a shingle as a draft analyst, and even the well-funded operation at ESPN doesn't have the resources that are trained on the pool of talent by teams that are each spending a quarter of a billion dollars on player salaries each year.

Besides, think about who's doing the grading vs. who's doing the drafting. Any of the pundits doing the grading would kill to be one of the general managers making the actual selections. The reason they're on TV and not in the draft room? It's because their opinions aren't as respected by those who control those $250 million annual payrolls.

If those of us watching the draft just take the grading for its entertainment value, then we have the right perspective. We can still get excited as fans (and trust me, my Steelers had a GREAT draft... I think) while understanding that all those mock drafts and lists that rank players out through the end of the sixth round are really only accurate for the first five or six picks, are a rough guide for the rest of the first round and then amount to just about nothing for the remaining 200-some players chosen.

But the human tendency is to grasp on to the grade and forget how poor the data is that underlies it. And that sort of tendency can be dangerous in business.

Let's look at a few examples of false precision in insurance.

Here are the sorts of studies I see quoted all the time in articles that are sent to me for publication:

My first problem with these sorts of claims is that the terminology is so vague. At least with the projection on cyber, we can be pretty sure the measuring stick for the size of the market is premiums. And we all have a pretty good handle on what fraud looks like. But what is the "blockchain in insurance market"? Is that strictly revenue generated by those selling blockchain services? Does it include the value of, say, claims that are coordinated on a blockchain? Likewise, what does the "AI in insurance market" entail? Revenue generated from AI services? Savings from AI? Or what?

My bigger problem is the false precision. The global cyber insurance market is going to grow 22.3% a year? You're sure about that? Not 22% a year? Not 20% to 25%? Not "really fast, with our current best estimate being 20% to 25% a year"?

Blockchain in insurance will grow 52.4% a year? That ".4" kills me, just like the pluses and minuses do on the made-up letter grades for those selected in the NFL draft. So do the ".7" in the 32.7% CAGR projected for AI and the ".6" in the $308.6 billion that the U.S. supposedly loses to insurance fraud every year.

Some of the false precision feels accidental. Give someone a calculator, and they're tempted to report a precise percentage as though it's meaningful to three digits, forgetting that the inputs are really just an educated guess. Give someone a spreadsheet that automatically adds up columns, and they're tempted to report that the guesses on fraud total precisely $308.6 billion.

Some of the false precision feels deliberate, though. The people producing these studies want you to think they can be far more precise than they can, and $308.6 billion sounds a lot more definitive than, say, $250 billion to $350 billion, which is probably a more accurate expression of the conclusion even if you accept the analysts' methodology and definitions.

As with the draft grades, these studies are fine if you treat them as merely general guideposts. As John Maynard Keynes said, "It is better to be roughly right than precisely wrong."

But executives sometimes get trapped by precise forecasts.

In the mid-1980s, AT&T famously asked McKinsey to forecast how many cellphones would be in use in the U.S. in 2000 and was told the number would be only 900,000. On that basis, AT&T dropped out of the market for years and ceded territory to others. The actual number in use by 2000 was about a factor of 1,000 more than McKinsey estimated.

Similarly, IBM's market researchers decided back in 1980 that the entire demand over the lifetime of the PC it was to introduce in 1981 would be 200,000 units. As a result, IBM rushed a product to market even though that meant relying on Intel for the processor and Microsoft for the operating system. In the 1990s, more than 200,000 units of IBM-compatible computers were selling EVERY DAY, and Intel and Microsoft got rich while IBM languished because it had underestimated the power of the PC.

Both the AT&T and IBM blunders are complicated. The companies didn't just fall for some random forecast. They had internal issues that inclined them to think in terms of landlines, not cellphones, and mainframes and minicomputers (so-called Big Iron), not PCs. But they still illustrate the need to be on guard about the kind of false precision that the NFL draft demonstrated in spades and that shows up in projections about insurance lines and technologies all the time.

Go, Steelers!

Paul

Savvy insurance marketers can wow customers and prospects with near-real-time, precisely targeted, relevant messaging thanks to an abundance of data.

Many marketers in the insurance industry are feeling the pressure of operating in a highly competitive business environment where huge marketing and branding budgets are essential. While the industry is focused on building brand dominance through broadcast, online and print media marketing, savvy insurance marketers can wow customers and prospects with near-real-time, precisely targeted, relevant messaging thanks to an abundance of trigger and life event data.

While the availability of trigger data is immense, actually leveraging it internally, or with a partner, to obtain the greatest value can be a challenge for even the most experienced marketer. How one navigates this virtual sea of information can be the difference between success and failure.

Let’s take a look at some of the best practices that can help insurance companies build and deploy smarter, more effective trigger-marketing campaigns.

Close the back door

In a hyper-competitive market like the insurance industry, retaining existing customers is job number one! While many consumers don’t realize they can terminate policies without waiting for a renewal date, insurance marketers know they need to be watching diligently to identify customers who may be looking to exit, regardless of where they may be in a defined coverage period.

Many companies, across all industries, use first-party data, like website traffic, demographic and CRM data, to stay on top of customers who may be shopping for new products/providers.

Savvier marketers will take that first-party data and pair it with third-party life event triggers, as life events are often a strong motivator for consumers to upgrade existing policies or seek new insurance providers altogether. For example, consumers may increase the value of life insurance after having a baby or getting married, add a vehicle to a policy after relocating or buying or selling a home or combine policies of two individuals into one after getting married. The combination of first-party data and life event triggers offers valuable insights into customers' activities and allows identification of risks associated with these events at critical inflection points so marketers can reengage customers with a series of timely and pertinent marketing messages geared toward retaining business.

See also: The Promise of Continuous Underwriting

Triage the triggers

No two triggers are quite the same, so neither should your marketing outreach strategies. First and foremost, it is important to understand which triggers are the most immediately actionable for certain products and which triggers may have a longer marketing curve. For instance, an expectant parent trigger might be a more long-term nurturing opportunity to sell a life policy for the child or to take out a larger policy for one or both soon-to-be parents. Meanwhile, someone planning to move will have a much more urgent need that demands a much more aggressive approach. That is a bottom-of-the-funnel, top-of-the-priority-list situation. Treat the most pressing triggers immediately.

Prioritize your channels

Much like assessing the value and urgency of triggers, it’s important to do the same across multiple channels. For instance, consumers conducting early-stage product shopping may be best nurtured via programmatic display and paid social, while those indicating greater intent could be effectively reached by direct mail with the support of email and other digital media. Of course, these aren’t hard and fast rules, but assessing the mix is vital to delivering an effective, efficient omnichannel strategy.

Leverage “FOMO” in your messaging

The fear of missing out, or “FOMO,” as it applies to trigger marketing, can instill in customers a sense that perhaps they may not have made the best choice or that there is a better option. A misstep in insurance can translate into tangible – and costly – consequences for consumers, so the motivation is there to find the right partner. Marketers can develop creative ad messaging that encourages customers to question their current insurance policies and wonder ... Are they getting the best rate? Do they have the right amount of coverage? Have they engaged with a company that will support them when disaster strikes?

One word of caution as it relates to messaging around life event triggers; make your messaging targeted but not intrusive. Getting too specific can make consumers feel “Big Brother” is looking over their shoulder. Aim for relevance; We’re here for you through life’s stages. Avoid creepiness; Congratulations on your pregnancy!

Drive alignment

A strong brand is built through years of messaging. The insurance industry has some of the strongest and best-known brands and messaging in advertising and the best trigger marketing touchpoints consistently ladder up to a provider’s core principles and mission. It’s vital for insurance marketers to make sure campaign messaging lives up to a company’s bold brand identity and hits the mark with consumers’ current needs.

Team alignment matters, too. The speed and responsiveness of trigger campaigns require marketing, outside vendors and sales teammates to work in parallel to build a process that keeps communications on brand and compliant, delivering effective marketing outreach at the earliest possible opportunity to reach consumers first!

See also: 2-Speed Strategy: Optimize and Innovate

Monitor your metrics

Not only does trigger marketing provide valuable insights into consumer behaviors and trends, it’s far more quantifiable and provides faster reads than most other campaign types, making it a darling of CMOs and CFOs. The ability to drill down into conversions and revenue metrics based on consumer triggers in near real time allows marketers to make quick adjustments and finetune strategies on the fly, which enhances the likelihood of a strong ROI.

For more information, download a free copy of The Insurance Marketer’s Guide to Life Event Marketing.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Kristopher Lazzaretti is president of data solutions at Deluxe, a full-service data driven marketing solutions company.

A broad survey found that 77% of senior executives said they are in some stage of adopting AI, up 16 percentage points from a year ago.

Insurance companies often struggle against the perception of being conservative institutions that are slow to change. Nothing could be further from the truth.

Since the 1960s, the insurance industry has embraced so many new technologies, from punch cards and mainframes to tablets and mobile phones. Technology is the backbone of the modern insurance industry.

Here’s an example of the industry’s technology commitment. In 2002, the life-annuity sector spent $1.4 billion on IT, and the P&C sector spent just under $3 billion. In 2022, those expenses were $5.7 billion for life and $9.3 billion for P&C. In our view, this investment is about industry transformation and platform modernization, not just administering business growth.

In 2024, insurers are embracing AI (artificial intelligence) to manage data, uncover opportunities and improve productivity.

AI Deployed Across the Value Chain

At Conning, understanding what’s driving insurer profitability is a crucial part of helping our clients develop effective investment strategies. Given 2023’s media storm around generative AI, we wanted to understand the state of AI within the industry. In addition to engaging in numerous conversations with insurers, AI experts, and technology firms, we conducted a survey in the fall of 2023 that looked at AI deployment across the insurance value chain.

This is the second year of our annual survey on AI and technology adoption in the insurance industry. We surveyed senior insurance chief technology officers, chief operational officers and chief innovation officers, along with a select few senior insurance technology vendor executives.

Three Parts of the Value Chain

Our survey focused on three broad areas of the value chain in which AI is already showing some promise.

Sales and Underwriting: By analyzing vast amounts of data, including customer information and external factors, AI is helping insurers make better-informed decisions when assessing underwriting risks, speeding up the underwriting process and reducing the likelihood of human error.

Operations (Claims Processing and Fraud Detection): AI-powered systems are improving claims processing by automating mundane tasks and streamlining the workflow, analyzing claim documents, assessing damage and even calculating payouts, all with minimal human intervention. AI is playing a crucial role in fraud detection by flagging suspicious claims and patterns that may indicate fraud.

Risk Control and Pricing: AI tools are improving insurers' ability to assess risks accurately and set prices accordingly. By analyzing historical data and real-time information, AI algorithms can predict trends and potential losses more effectively, enabling insurers to offer more competitive rates while maintaining profitability.

See also: AI: Beyond Cost-Cutting, to Top-Line Growth

More Than Just LLMs

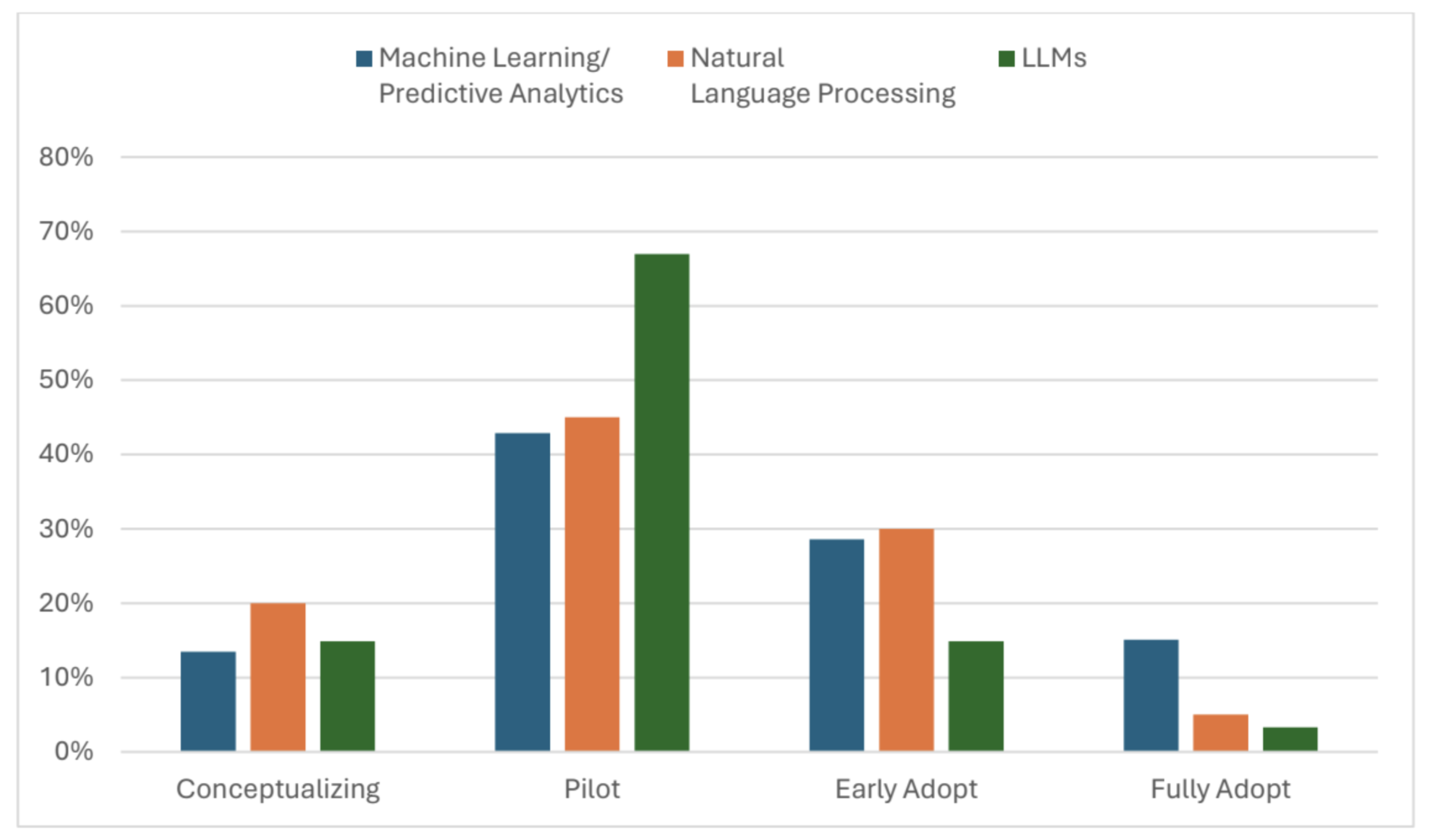

Since 2023, AI, or more specifically generative AI, has been a significant focus of insurance management teams, but AI encompasses a variety of technologies. Understanding the differences is crucial to thinking through where and when their impact is likely to be felt. Our latest survey looked at three specific types of AI.

Large language models (LLMs) are advanced AI systems designed to understand and generate human language. LLMs are the foundational technology supporting generative AI.

Machine Learning/Predictive Analytics (ML/PA) are quantitative, statistical models using algorithms to make predictions or decisions learning from inputted data, are updated in real time and can improve performance from feedback from objective functions.

Natural Language Processing (NLP) extracts meaning from speech or text. This enables insurers to efficiently process unstructured data from agent and customer phone calls to reports.

Older AI Technologies More Widely Adopted

In this survey, we asked how AI is reshaping the insurance industry and the opportunities and challenges that come with this technological transformation. At a high level, we found that, while there were varying degrees of adoption for all three technologies across the value chain, ML/PA and NLP had higher rates of adoption and deployment. Survey results suggest, however, that LLMs show great potential.

This year’s survey results show 77% of the respondents indicated that they are in some stage of adopting AI, a 16-percentage-point increase from our 2023 survey.

The survey found that 67% reported they were already piloting LLMs, which was the largest technology in the piloting stage. Given the relatively recent awareness of generative AI, this high percentage of piloting the underlying technology is a strong indicator of future adoption.

Across the overall value chain, ML/PA was either in the early stages of adoption or had been fully adopted by 44% of responding firms. Sales and underwriting reported the highest adoption among components, at 54% of respondents.

Our report, “Transformative AI Technology: Insights from Conning’s Executive Survey” provides a deeper analysis of the three technologies’ use within each part of the value chain.

See also: Can AI Solve Underlying Data Problems?

Outlook and Challenges

The surveys and discussions we’ve had strongly indicate that AI is helping insurers manage complexity and data diversity. We see its deployment increasing, and management teams will be spending time figuring out the best AI solutions for their company.

However, regulations will significantly influence the speed of adoption. Already state regulators are restricting the types of data insurers can use in their AI systems. Additional regulations are being proposed and enacted at the national and international levels. Beyond regulations, insurers need to be mindful of potential litigation surrounding the use of generative AI.

While regulation and litigation may slow AI’s continued adoption within the insurance industry, they are unlikely to stop it. If history has proven anything, when it comes to new technology, insurance is an industry where embracing new technology never stops. In 2024, nothing suggests to us that will change.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Scott Hawkins is a managing director and head of insurance research at Conning, responsible for producing research and strategic studies related to the insurance industry.

Previously, he was senior research fellow for Networks Financial Institute at Indiana State University. He spent 16 years at Skandia Insurance Group in the U.S. and Sweden as an analyst and senior researcher.

He studied history at Yale, has a certificate in information management systems from Columbia University and was a board member of the J. M. Huber Institute for Learning in Organizations at Teacher’s College.

In this Future of Risk Forecast, Adam Rimmer of FloodFlash explains how parametric insurance is closing the protection gap in flood insurance.

|

Adam Rimmer first saw the potential of parametric insurance while working at RMS, the world’s largest catastrophe modeling firm, since acquired by Moody’s. While there, he and his FloodFlash co-founder Ian Bartholomew structured and modeled triggers on over $2 billion of parametric insurance products and catastrophe bonds to protect governments and large corporations in the U.S. and around the world. They are now using those same principles at FloodFlash, a sensor-based, parametric flood product.

|

What gaps do you see in the traditional insurance market that FloodFlash is trying to fill?

The great irony in property insurance is that those who most need coverage are the ones who can't buy it. If you operate in a high-risk area like the coastline, or if you are a class of business that is difficult for traditional underwriters to tackle, such as auto dealerships or specialist manufacturing facilities, the rates can be incredibly high. So you opt to self-insure. The same is true of some coverage types within flood: Business interruption loss is notoriously difficult to price, for example, so businesses in higher-risk areas frequently end up with no coverage at all.

That leads to a big coverage gap. Less than 20% of the $70 billion of loss that is caused by catastrophic floods annually is insured. And that gap is disproportionately among those at high risk.

I consider the flood insurance gap in the U.S. to have two sides: One is a demand-driven gap, caused by homeowners and businesses deciding that it’s not worth purchasing because they consider themselves at lower risk. Companies like Neptune Flood are doing an amazing job at addressing this gap, creating flood insurance that is so efficient and so easy that more people take it up.

The other side is a supply-driven gap: This is among homeowners and businesses that know themselves to be at high risk and want to buy protection. But no supplier is willing to sell it to them at a reasonable rate. Those customers will use the National Flood Insurance Program (NFIP) to cover the first $250,000 (homeowners) or $500,000 (businesses). For bigger losses, they are forced to self-insure.

FloodFlash is focused on that second, supply-driven gap. Its customers are too risky/uncertain for the private flood market and too large for the NFIP alone.

The reason this apparent alchemy is possible — to insure the highest-risk customers and for it to still be profitable — lies not only in FloodFlash’s underwriting algorithms but also in a fundamental property of parametric insurance: Exposing the underwriter to only one variable (the parameter that’s being measured) removes sufficient uncertainty that the underwriter can actuarially justify charging more affordable rates for the first time. Parametric insurance creates a new market.

I don't see any way other than a paradigm shift in approach, like parametric coverage, for the insurance industry to materially close that gap.

What are the biggest challenges in convincing customers, regulators and insurers about the benefits of parametric insurance?

The challenge is different for each of those groups. Insurers and reinsurers have been fantastic at grasping the science behind the underwriting and the analysis that means this type of coverage allows them to profitably access risk that they had previously been unable to touch. FloodFlash policies are placed at Lloyd’s of London with Munich Re, the largest reinsurer in the world, and Hiscox, the leading writer of U.S. flood risk in that market. We collaborate closely to ensure that FloodFlash is providing value for customers while simultaneously being a profit center for those underwriters. They believe in the opportunity here. Indeed, Munich Re’s VC arm has now taken on an equity stake in FloodFlash.

Regulators want to protect consumers, and FloodFlash's approach of using site-specific IoT sensors as the triggering mechanism has been important. The difference between a good parametric policy and a bad one is “basis risk,” i.e., How much does your payout under the parametric policy correlate with the loss you experience? The parameter that correlates most tightly with majority of property and property-adjacent flood losses is flood depth at the client site (as opposed to, say, a satellite image, a rainfall index or a nearby river/coastal gauge). FloodFlash originally launched in the U.K., and the team spent time with the Financial Conduct Authority (FCA) through their regulatory sandbox program to make sure the FCA were comfortable that the tight coupling between financial losses and readings from the FloodFlash sensor meant there were likely to be good outcomes for consumers.

For customers — and often their agents — the biggest challenge is perhaps making people comfortable that this new technology and new type of insurance can save their livelihood. That's tougher in insurance than other industries because buyers index on trust and familiarity in insurance. We have overcome that through our growing library of success stories and testimonials and through FloodFlash’s association with those big and trusted names like Munich Re and Lloyd's.

Is parametric a complement or alternative to traditional insurance coverage?

Both. It can be a different answer for each client because the biggest factor is what other coverage options are available to them. In the U.K., 75% of customers use FloodFlash as their entire flood program, and the others use FloodFlash to expand their existing coverage -- most often as deductible infill.

In the U.S., the majority of customers use a FloodFlash policy as excess coverage above an NFIP policy. Our team works with agents to structure policies so the parametric trigger points correspond with the exhaustion of the NFIP limits. I also frequently see FloodFlash being used as standalone business interruption coverage. Standalone BI is almost impossible to buy in the traditional flood market if you're in a high-risk zone, but it's simple for FloodFlash, hence our recent launch of the specific Flood BI product. It can be viewed as a complement to their underlying property coverage, or equally as an alternative to traditional BI.

How is climate change affecting the flood insurance landscape?

Every year, not just climate change but also population growth and urbanization are increasing flood risk in the U.S. As it gets worse, the traditional market retreats, which is creating more of a gap. Almost every dollar of risk that FloodFlash protects is not risk that was previously covered by a traditional provider. It was previously part of the gap, and FloodFlash solved that problem.

FloodFlash first paid parametric claims when Storm Ciara hit the U.K. in 2020. It was an emotional moment. Our customers were business owners who previously were uninsured and didn't want to be. After the event, FloodFlash experienced incredible gratitude from customers whose businesses would otherwise have not survived.

What are some other trends you’ve observed in the global insurance market related to flood losses and parametric cover?

In 2023, the U.S. experienced 26 flood and storm events that each caused over $1 billion in damage. That's the most ever in a single year, even after adjusting for inflation. The increased prevalence of storms and severe losses in a time of wider economic turmoil has led to a very hard insurance market, which in turn is putting parametric coverage on the table for an increasingly wide area of the market. That's a trend that's been particularly strong: customers considering parametric flood options for the first time.

People have been pointing out to me the parallels between parametric nat cat and where cyber insurance was maybe eight to 10 years ago. In both cases, you have this large and growing insurance gap that exists because the risk is very difficult to price. Product and technology developments mean the risk can now be insured for the first time. However, it's not something that happens overnight: Customers and their agents have to be educated not just on the solution but sometimes even on the problem, too. Today, of course, cyber cover is mainstream.

What has been different about the U.S. market compared with the U.K. one? Any surprises?

Many differences, many of which I learned the hard way. I've found that wholesale brokers are an incredibly important part of the ecosystem in the U.S. They aren't anywhere near as prevalent in the U.K. And given that wholesalers disproportionately see hard-to-place risks, i.e., the customers where FloodFlash is most competitive, wholesalers have become very important to us.

Timing of insurance purchasing, particularly for hurricane-exposed commercial property, is much more seasonal in the U.S. than in the U.K. In general, there is a much more sophisticated flood insurance market in the U.S.: in the U.K., flood is a default inclusion in both homeowners and commercial policies, so the market for standalone policies only exists when the main carrier is actively excluding flood coverage.

The most surprising element is the difference in policy size. I always expected U.S. policies to be bigger — median revenue, a reasonable predictor of insurance spending, is 2x in the U.S. what it is in the U.K. — but our average policy size is around 20 times bigger in the U.S. than the U.K. And that's just one of the reasons why I'm so excited about what FloodFlash is doing in the U.S. It’s going to be big.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Insurers must navigate high-frequency losses post-disaster, where fraudsters capitalize on overwhelmed systems.

Fraud opportunists often make waves following natural disasters and catastrophes.

The times during and immediately after a catastrophic event are some of the most important — and challenging — for the insurance industry. Helping people through catastrophes and natural disasters by providing financial assistance during the crisis and when it is time to rebuild is what insurance companies are designed for. This is the time when insurers fulfill their promise to policyholders to be there during times of need.

But natural disasters also create significant challenges for insurers to manage. Adjusters are working longer hours on cat duty and the high volume of losses makes it difficult to keep up with the administration and handling of claims. These conditions create the perfect environment for potential fraud attempts by bad actors who want to take advantage of the challenges exacerbated by natural disasters.

While most insureds and claimants are honest, some decide to commit fraud by exaggerating their loss or making up a claim. The Coalition Against Insurance Fraud reports insurance fraud costs consumers $308.6 billion annually and estimates 10% of P&C claims contain an element of fraud. These costs add up, making the fight against fraud an important priority for insurers worldwide.

Disaster Fraud Becomes Big Business

The insurance industry has seen examples of fraud attempts during natural disasters across all lines of business, from life insurance and workers’ compensation to property and liability losses. Disaster fraud, as it has become known in the industry, happens after all kinds of losses.

After Hurricane Katrina, the FBI investigated over 900 people for fraudulent activity, including identity theft, which allowed fraudsters to gain access to funds earmarked for recovery efforts. Scammers have used cyberattacks to divert FEMA funds following catastrophes like Hurricane Ian that struck Florida in 2022.

The NICB warns homeowners to use caution with contractors who offer to repair damage from natural disasters, estimating about $10 billion was lost to contractor fraud in 2022. Following the 9/11 tragedy, many fraudsters emerged to take advantage of the disaster, including a woman sentenced to prison for collecting disaster relief money for a fictitious husband she claimed perished in the attack.

FRISS recently released its 2024 Fraud Report examining global beliefs about fraud and actions taken to detect and prevent fraud in the insurance industry. The survey asked respondents about fraud following natural disasters and catastrophes in their regions. The responses seemed to confirm the phenomenon of disaster fraud around the world.

A majority of respondents, 62.84%, believed bad actors took advantage of catastrophic events to commit insurance fraud. But some of the responses were regional, as the report found respondents from LatAm and Europe felt the impact from natural disasters and other catastrophes on fraud was low. Respondents around the world agreed that new fraud schemes tended to develop following catastrophic events, however.

How Insurers Can Manage Disaster Fraud

Insurers can take action against disaster fraud by making improvements in a few key areas. Bad actors often take advantage of the low severity/high frequency losses that follow in the wake of a catastrophe to file exagerated or made-up claims. These claims for losses like vandalism, theft, or food spoilage are often handled quickly to make time for the more complex, large dollar losses. Fraudsters count on the fact that insurers will be too busy to spend much time adjudicating a small dollar loss when they have hundreds of other claims to review.

Some of these smaller claims do get routinely paid when they should be investigated further. Instead of being overwhelmed by volume, insurers that invest in fraud detection tools can sort through the high frequency losses to find the ones needing more investigation. Insurers should also invest in fraud awareness and prevention training for their employees — and refresh the training as often as needed.

82% of the respondents to the FRISS survey said their firms invested in fraud awareness training programs and about half of respondents used other tools to help detect and prevent fraud, like behavior analysis and social mining. Empowering employees to educate consumers may also help reduce the occurrence of fraud following catastrophes, especially when it comes to contractor fraud.

The survey found some insurers had a fraud detection and prevention platform in place, with 35% of respondents reporting having an external solution and 28% used a homegrown platform. Having a platform in place to help detect, prevent, and manage fraud is one significant way insurers can fight back against disaster fraud.

Detecting and mitigating fraud within high frequency losses is a challenge for humans to take on alone, but with the right platform in place, technology acts as a partner and first line of defense.

To learn more, read the full 2024 Fraud Report

External Links:

1. https://insurancefraud.org/fraud-stats/

2. https://www.thomasdamico.com/blog/2023/07/how-did-relief-fraud-occur-after-hurricane-

ded%20identity%20theft,brought%20charges%20against%20those%20involved

3. https://therecord.media/cybercriminals-use-hurricane-ian-as-lure-for-scams-theft-of-fema-funds

5. https://www.nytimes.com/2002/12/31/nyregion/separating-fakes-from-9-11-victims.html

Sponsored by ITL Partner: FRISS

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

FRISS is the leading provider of Trust Automation for P&C insurers. Real-time, data-driven scores and insights prevent fraud and give instant confidence and understanding of the inherent risks of all customers and interactions.

Based on next generation technology, the Trust Automation Platform allows you to confidently manage trust throughout the insurance value chain – from the first quote all the way through claims and investigations when needed.

Thanks to FRISS, trust is normalized throughout the organization, enabling consistent processes to flag high risks in real time.

While autonomous cars have made real progress lately, there's no reason to pay any attention to Musk's tease for a robotaxi announcement in August.

The auto insurance market is in turmoil. Insurers are not only dealing with soaring repair costs and pushback about rising rates but are facing core uncertainties about how quickly electric vehicles will gain share and when autonomous vehicles will really take hold. That last is an existential issue for personal auto insurance, because drivers don't need insurance if they aren't driving; liability will lie with the makers and operators of the autonomous vehicles.

In this kind of tumult, it can be hard to separate the signal from the noise.

I'm here to tell you that Elon Musk's recent promise of a major announcement on robotaxis in August is just noise.

There are two reasons I can make such a blunt statement: Musk's long history of overpromising on the autonomous capabilities of Teslas and the state of his technology. Let's start with the simple one: his history of overpromising.

When Musk says he'll unveil his robotaxi design on Aug. 8, it's important to step back and look at what else he's said over the (many) years.

In 2015, he promised Tesla shareholders that cars would be fully autonomous within three years. In January 2016, he doubled down via tweet: "In ~2 years, summon should work anywhere connected by land & not blocked by borders, eg you're in LA and the car is in NY." In other words, by roughly the beginning of 2018, you would be able to tell a car to drive to you in Los Angeles from New York City, and it would do so entirely on its own. In April 2017, during a TED talk, he confirmed that claim: “November or December of this year," he said, "we should be able to go from a parking lot in California to a parking lot in New York, no controls touched at any point during the entire journey.”

2018 came and went without any Teslas crossing the country on their own, but he was back at it in 2019, saying on a podcast: "I think we will be feature complete — full self-driving — this year. Meaning the car will be able to find you in a parking lot, pick you up and take you all the way to your destination without an intervention, this year." He told investors in April that year that "by the middle of next year, we’ll have over a million Tesla cars on the road with full self-driving hardware,” so reliable that the driver “could go to sleep.” He has said that owners of fully autonomous Teslas could just hit a button and make their cars available to others for a fee, so he was basically promising to have a one-million-vehicle fleet of Tesla robotaxis on the road ... by mid-2020.

You see where this is going.

Musk has toned down some of his promises in recent years, in the face of regulatory scrutiny and lawsuits by families of people who were killed while their Teslas were in Full Self-Driving mode. But if the old saying is, "Fooled me once, shame on you; fooled me twice, shame on me," then what would you say about people who let Musk fool them repeatedly for a decade?

You can decide Musk is for real this time on autonomy, if you like. I'll wait for proof.

And his general lack of credibility on the issue is only half the problem. The other is that his technology just doesn't measure up.

As far back as 2013, when I published a book on driverless cars with Chunka Mui, we argued that Tesla was taking too limited an approach to the technology. It was using radar and cameras to track what was happening around the vehicle but wasn't using lidar (essentially a laser-based form of radar), as Google and others were. The Tesla approach was economical, because radar and cameras were inexpensive while lidar cost tens of thousands of dollars per vehicle. But the benefits of lidar seemed clear--it detects objects that can be hidden from radar and cameras by weather. And Chunka and I argued that lidar costs would follow the same curve that all electronics follow, as described by Moore's law (essentially, that costs drop 50% every two years or so). Sure enough, lidar now costs maybe $1,000 per vehicle, and prices are steadily dropping--but Tesla's AI isn't designed to incorporate information from lidar.

In fact, Tesla has headed in the other direction. In May 2021, Musk announced (against the advice of senior engineers) that he would stop using radar in his self-driving technology. His reasoning was that human drivers just rely on their eyes and their brains, so why did his AI need anything more than cameras? For good measure, he also stopped using sensors that detect objects within inches of a vehicle.

But think about how much trouble you have seeing well enough to drive in a rainstorm or snowstorm or perhaps at night, Wouldn't it be much safer to have inputs from radar and lidar, as well as your eyes (assuming your brain were wired to make instant sense of those inputs, as an AI can be trained to be).

Self-driving technology is really hard. How hard? Even Apple recently gave up after spending $10 billion on an autonomous vehicle project. But Musk is doing himself no favors by limiting the sensors in his vehicles. I'm not sure he ever gets to reliable self-driving of the kind he has been promising if he just uses cameras.

He's also kidding himself if he thinks he can quickly stand up a robotaxi operation. Think of all the intelligence that has to be built into a system that dispatches robotaxis--and that complexity increases by an order of magnitude if, as Musk has discussed, he wants Tesla owners to be able to volunteer their vehicles as robotaxis when not using them.

And the dispatch system is just the start of the complexities. Who is responsible for cleaning the car when kids are transported back from the beach all covered in sand? And how do you make sure that cleaning gets done before the car is sent to its next passengers? Who is liable if a car is used in a drug deal? Who plugs the car in if it runs out of charge before being returned to its owner?

I did some consulting for a major company on robotaxis in 2017-18 and can tell you that the list of complexities is extremely long.

Investors in Tesla are going to make whatever decisions they make, but I wanted to be sure that the hype about this robotaxi announcement didn't bleed into anyone's thinking in insurance. Yes, auto insurance is in turmoil, and, yes, autonomous vehicles are an existential threat to personal auto insurance (years from now), but whatever Musk says in August about robotaxis won't even cause a ripple. Ignore it.

Cheers,

Paul

P.S. As you think about what WILL have an effect on auto insurance, here is a smart piece from two McKinsey partners.

While 70% of retirement-age Americans will need continuing care at some point, merely 14% are very confident they’ll be able to afford it.

America’s long-term care crisis warning signs are mounting. The latest red flag is the rising cost of long-term care services across all provider types, with increases up to 10% over the past year, according to the 2023 Genworth Cost of Care Survey.

Clients are already facing the convergence of major trends that pose a potentially devastating dilemma that can compromise their aspiration to age in place and enjoy a happy, healthy retirement.

The retirement crisis remains a menacing presence. Overall, 80%—or 47 million households— with older adults are financially struggling or at risk of economic insecurity as they age. Recent research also shows a short-sighted attitude regarding long-term care services. While 70% of retirement-age Americans will need continuing care at some point, merely 14% of retirees are very confident they’ll be able to afford it. Lastly, our country’s health is bleak, having the lowest life expectancy among high-income countries.

As the population ages, the threats promises to intensify. Older generations will look to their trusted advisers to weather the storm, providing an opportunity to help heighten clients’ long-term care readiness while bolstering agents’ profitability.

See also: Using Data Science to End Surprise Billing

Become a Partner in Health

Today’s rapidly aging society must prompt a paradigm shift within the insurance industry marked by fundamental change in the attitudes of professionals and how they perceive and service their clients.

The inherent nature of the agent-client relationship has been somewhat fractured amid carrier business directives to increase rates and decrease payouts or claims. This longstanding approach must evolve into one centered on a “Best Alignment of Interests” model that creates a mutually beneficial partnership among carriers, agents and policyholders.

The critical topic of long-term care is often ignored due to a lack of awareness. One of the most common, and perilous, misconceptions among agents and policyholders is that Medicare covers long-term care. Medicare only covers basic medical needs, and not long-term care services.

This is a highly underserved market where agents can lend their vital support and promote extended quality of life. Formulate a plan to help clients live the best possible versions of their lives.

Embrace Innovation for Aging Boomers

The Baby Boomer explosion means professionals will experience a surge in clients who are painfully unprepared, and whose specific needs must be addressed.

Despite the population’s urgent need, long-term care insurance purchases are declining, with 2022 marking the lowest sales volume in over two decades. This trend is understandable due to heritage issues like inaccurate assumptions, which led to significant rate increases, lack of product innovation, agents and carriers dropping out of the market and overall unfavorable consumer perception of the segment.

The insurance sector must foster innovation that will ignite behavioral and buying changes and safeguard elderly individuals from financial insecurity during their retirement phase of life.

Begin with an application overhaul. Innovation can streamline the LTCI application process, which has traditionally involved in-person exams and lengthy procedures that frustrate consumers and result in high rejection rates. Today’s improved risk selection and application processing techniques enable insurance products to provide decisions within an hour, leading to better risk selection and significantly improved consumer experiences.

Innovation is transforming claim handling, making the process more efficient and precise. Automated initial claims routing streamlines the process and swiftly directs claims to the appropriate department or personnel for evaluation and next steps. We must replace legacy systems with automation that saves time and resources, leading to faster response times and reducing the risk of claims getting lost or mishandled.

Additional advancement areas exist in identifying potential policyholders who might require assistance and make future claims for health challenges. Those opportunities require insurers to analyze massive data sets mapped against population health metrics.

See also: Healthcare Inflation's Impact on Auto Insurers

An Ounce of Prevention Brings Big Mutual Benefit

Preventative services play an integral role in protecting and promoting health, yet only 5% of adults 65-plus received these recommended services in 2020. By using data analytics and predictive modeling, insurance carriers can reach out to these individuals, offering assistance, guidance and resources. This preemptive approach can prevent or mitigate problems, helping policyholders maintain better health and quality of life.

There’s a difference between living well into old age and living “well” into old age. Therefore, some insurance carriers are incorporating creative wellness programs into their pre-claim processes. They offer policyholders access to targeted, personalized health and wellness services like fitness programs, nutrition counseling, mental health support and preventive screenings. One example is Assured Allies’ NeverStop, an innovative wellness rewards program that’s built right into your insurance policy. By encouraging healthier lifestyles and early intervention, these insurers reduce the chances of claims arising from preventable health issues while improving the overall customer experience, building stronger and deeper connections.

Small interventions can make a huge impact on health and wellbeing. Falls are the leading cause of injuries for older Americans, with one out of four Americans age 65-plus falling each year. Simply installing a grab bar in a bathtub can decrease fall hazards by 76%. Treating hearing loss may lower the risk of dementia, with hearing aids reducing the rate of cognitive decline in older adults at high risk by almost 50% over three year.

A Critical Wake-up Call

The inevitable reality facing insurers must be addressed to offset its accompanying, significant cost. We should be encouraged by what we are seeing, as insurtech companies are introducing innovative solutions that can revolutionize the insurance industry and fill the gap in long-term care. These efforts are powered by our social obligation to serve the needs of the growing elderly population, and by the business opportunities they present. The combined force of dynamic solutions and adaptive client service methods can drive the industry successfully into the future.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Larry Nisenson is the chief growth officer for Assured Allies.

For more than 25 years, he has held leadership roles in the insurance and financial services industry, including as chief commercial officer for Genworth's U.S. life insurance business, covering long-term care life and annuity products. Prior to that role, Nisenson held senior positions at Plymouth Rock Assurance, AXA Equitable, American General Life and Allstate. Nisenson started his career in financial services in 1995 as a financial adviser.

Nisenson received his BA from Rutgers University and attended the Global Executive Leadership Program at the Tuck School of Business at Dartmouth from 2018-2019. He serves on the board of directors for the Rutgers School of Design Thinking and is a public advocate and speaker on the caregiving dilemma that affects millions of people.

The use of generative AI for coding for in-house applications is set to be the next big thing in 2024.

Generative artificial intelligence (AI) models are 10,000 times more powerful compared with just five years ago. An increase in power on this scale creates significant opportunities for insurers.

The life insurance industry is at a turning point, with rapid transformation being driven by factors including technological innovation and changing market dynamics. AI, in particular, has the potential to redefine traditional practices and revolutionize the entire value chain, from greatly improving customer services and risk assessments to retention and policy customization.

AI for code – the next big milestone

The use of generative AI for coding for in-house applications is set to be the next big thing in 2024 as the industry realizes just how powerful the latest models have become and insurers find ways to leverage this power. In a recent conversation, a non-executive director in a major U.K. insurance firm revealed that they had already started using generative AI for a coding project to translate all the code from the insurer’s entire legacy box of business into their preferred code to sit more efficiently with their newer main block of business.

When looking at exactly how these technologies can improve our day-to-day work, the writing of computer code is a prime example of a core application of AI. For example, an AI coding system can help generate and test code, as well as assist in the debug process, which many developers struggle with. AI can also significantly help to improve documentation and adherence to coding best practice.

AI technologies can also facilitate code translation, such as transforming an Excel macro file into an open-source code like Python or R, with the endgame of fitting such applications into a better-governed process. There are many other applications of generative AI that can help the insurance industry, such as report drafting, checking the consistency of reports in large groups or compliance with group or professional standards and process automation that requires collation and large numbers of documents to be inspected.

Insurance firms are also undertaking competitions internally to see who can come up with the best generative AI use case, such as feeding generative AI an insurer’s complete collection of training and underwriting manuals to create an expert bot. This approach also benefits from avoiding the risk of any external interaction, which is sensible for insurers in 2024 that are considering how best to use generative AI, while a better understanding and a level of control are still being established.

See also: Balancing AI and the Future of Insurance

AI regulation on the rise

The opportunities of AI do not come without risks, which means implementing AI must be approached with care. As AI becomes progressively more integrated into insurance industry practices, regulatory oversight is also on the rise. This means insurers need to make sure that their AI practices comply with relevant regulations.

With such a heavy reliance on data, protecting data privacy and maintaining ethical standards are crucial. For this reason, insurers will need to comply with data protection regulations and handle personal or sensitive data ethically when using AI.

There is also the risk of bias unfairness. AI models can unintentionally learn and produce biases presented in the training data, leading to unfair outcomes. As a result, a continuous monitoring for bias is essential, alongside a commitment for transparency and fairness in their AI applications.

A key question for regulators will be the extent to which their focus is on the internal use of AI by an insurer, as opposed to concentrating on the company’s actual outputs generated by AI. With the main focus of regulators to date having been on the outputs (for instance, whether premiums are fair and non-discriminatory), the hope shared by many insurers is that this approach will persist.

A further problem arises with transparency. All model users, stakeholders and regulators ideally require their models to be transparent. But this is not possible with generative AI, which is typically based around neural networks with a hundred or more labyrinthine layers, each containing thousands of nodes (in effect, robotic neurons). So how can we learn to cope without transparency? Alternative criteria will need to be defined to allow use while retaining confidence in that use.

See also: Cautionary Tales on AI

The AI takeover - redefining insurance

All too often, the insurance industry approaches risk from a one-sided perspective, only seeing the negative. While this is a natural human instinct and typical of chief risk officers concerned with everything that could possibly go wrong, real-world risks tend to be two-tailed. That is to say, insurers also need to think about the commercial risks of being slow to harness the powers that generative AI offers and hence being left behind.

Looking ahead, the insurance industry is likely to accelerate the pace at which AI and human expertise are integrated. Insurers that invest in the necessary resources and capabilities to ensure the benefits of AI are effectively harnessed, while being mindful of its limitations and potential challenges, will be best equipped to thrive in this new era of insurance innovation.

Generative AI will be profoundly transformative and far more so than analytics and machine learning were predicted to be 10 years ago. Until very recently, industry leaders were skeptical as to how such tools could safely help their business. Given the record speed at which these tools are evolving, coupled with an increasing awareness of the technology’s scope and transformative potential, we should be flipping the default question from "show me how generative AI can help in this part of the value chain" to "explain to me why you’re not using generative AI here."

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Matthew Edwards is senior director and innovation lead at WTW.

Arlen Galicia Carreon is associate director at WTW.

The widespread adoption of telehealth, catalyzed by the pandemic, reshaped the way medical services are delivered across the U.S.

In 2024, the landscape of healthcare underwent a profound transformation, marking it as the Year of Digital Health & Wellness. The widespread adoption of telehealth, catalyzed by the COVID-19 pandemic, reshaped the way medical services were delivered across the U.S.

Prior to the pandemic, telehealth usage was relatively low, with approximately 5 million users nationwide. However, as the need for remote healthcare grew, so did the use of telehealth services, skyrocketing to over 53 million participants among Medicare recipients alone. Now, in 2024, 91% of health systems report having a telehealth program.

It wasn't just the aging population that embraced telehealth. Even workers' compensation agencies, which previously provided minimal coverage for telehealth services, experienced a significant shift. Before COVID-19, only about 1.2% of all medical bills covered by workers' compensation included telehealth services. However, at the peak of the pandemic in April 2020, this figure surged to approximately 8.8%, indicating a rapid adaptation to remote healthcare solutions. Although the use of telehealth services has since stabilized, it still remains significantly higher than pre-pandemic levels, hovering around 4%.

This unprecedented surge in telehealth usage serves as a critical foundation for the transition toward Digital Health & Wellness. The widespread acceptance and integration of telehealth into mainstream healthcare delivery systems have demonstrated its efficacy and value in providing accessible, convenient and efficient medical care.

See also: Data Science Is Transforming Public Health

In today's rapidly evolving healthcare landscape, Digital Health & Wellness has emerged as a pivotal force, encompassing the integration of information and technologies to manage health risk and promote wellness. This concept represents the convergence of healthcare and technology, aiming to enhance delivery methods and improve patient outcomes. Often used interchangeably with terms like telehealth, mHealth, eHealth and health informatics, Digital Health & Wellness has gained prominence, particularly in the wake of the pandemic.

The pandemic highlighted the necessity for healthtech solutions and the convenience of receiving medical care from the comfort of one's home. This shift in patient preferences, coupled with advancements in technology, has paved the way for a transformation in healthcare delivery. With the global healthcare market projected to grow by 5.4% annually from 2022 to 2028, there exists a vast and expanding market for Digital Health & Wellness solutions.

Even the regulatory environment has become more favorable, with the Biden administration prioritizing healthcare innovation as a cornerstone of its agenda.

One focus will be on musculoskeletal conditions (MSK). MSK conditions, which encompass a range of disorders affecting the muscles, bones, joints and connective tissues, represent a significant portion of healthcare expenditures in the U.S. According to data from the Centers for Disease Control and Prevention (CDC), MSK conditions rank among the leading causes of disability and chronic pain in the U.S.

The scope of the issue is staggering, with an estimated 1.71 billion people worldwide grappling with musculoskeletal conditions, and a notable 30% of individuals over the age of 45 affected by some form of MSK issue. These conditions often coexist with other health-related issues, compounding their impact on overall wellbeing. MSK conditions account for billions of dollars in healthcare spending annually, underscoring the urgency of effective intervention strategies.

See also: How Digital Health, Insurtech Are Adapting

The surge in virtual wellness tools, particularly in the domain of digital physical therapy, offers a promising avenue for addressing MSK concerns. These innovative solutions leverage technology to deliver accessible, personalized and effective care to individuals managing MSK conditions. By providing remote access to expert guidance, monitoring and rehabilitation exercises, digital physical therapy platforms empower patients to take an active role in managing their MSK health.

The challenge lies in bridging the gap between traditional healthcare models and innovative digital solutions, ensuring that individuals receive comprehensive and integrated care for their MSK wellness needs. This necessitates a holistic approach that encompasses not only symptom management but also prevention, early intervention and continuing support.

As we navigate the complexities of MSK wellness in the digital age, collaboration between healthcare providers, technology developers, insurers and policymakers is paramount. By harnessing the power of advanced technology, data analytics and patient-centered design, we are paving the way for a future where MSK conditions are effectively managed, healthcare costs are reduced and population health is optimized.

In the rapidly evolving landscape of Digital Health & Wellness, insurance companies are adapting to meet the changing needs of consumers. Recognizing the importance of preventive care and holistic wellbeing, insurance providers have introduced in 2024 additional reimbursement codes and expanded coverage for annual wellness visits. In a significant development, Medicare Advantage programs are now extending coverage to include Digital Health & Wellness memberships, acknowledging the vital role of technology in enhancing healthcare access and outcomes.

Also, 2024 marks a turning point in the approach to employee wellness, with a sharp uptick in workplace programs focusing on digital solutions. From large corporations to small businesses, there's a concerted effort to prioritize employee health and overall wellbeing.

At the forefront of this transformation are technological innovations that empower individuals to take control of their health. Digital health platforms, wearable devices and AI-driven solutions are revolutionizing wellness programs, offering personalized insights and actionable data to users. By shifting the focus from reactive healthcare to preventive measures, these technologies are reshaping the healthcare landscape and driving a fundamental change in how we approach wellbeing.

These developments underscore the immense potential for Digital Health & Wellness to revolutionize healthcare delivery and improve patient outcomes. By leveraging new technologies and focusing on wellness, the healthcare industry has a unique opportunity to address longstanding challenges and usher in a new era of patient-centric care.

As we look to 2024 and beyond, Digital Health & Wellness is poised to play a central role in shaping the future of healthcare, driving innovation and improving access to quality care for all. So, yes, all indications mark 2024 to be the innovative year for health.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Dr. MaryRose Reaston is the co-founder and CEO of Segen-Health.

She is an expert in diagnostic techniques for the evaluation and management of soft tissue injuries.