Key Takeaways

- Direct buyers invest heavily in consumer-facing marketing with a single objective: acquire policies at the lowest cost possible.

- The vast majority of policyholders who sell their life insurance never receive a competing offer, creating a structural information asymmetry in the market.

- Fiduciary brokerage representation introduces competition into the transaction and shifts the incentive structure in favor of the seller.

- The life settlement industry needs to prioritize brokerage advocacy as a consumer protection standard, not treat it as optional.

The life settlement market has grown significantly over the past two decades. More policyholders are becoming aware that selling a life insurance policy is a legal, regulated option. More institutional capital is flowing into the space. And more technology platforms are making the process faster and more accessible than it was even five years ago.

But there is a structural problem sitting at the center of this growth that the industry has been slow to address. The players with the largest marketing budgets and the most aggressive consumer outreach are the ones whose financial incentive is to pay sellers as little as possible.

The Asymmetry Problem

When a senior decides to explore selling their life insurance policy, the first point of contact almost always determines the outcome. And in the current market, that first point of contact is overwhelmingly a direct buyer.

Direct buyers, also known as life settlement providers, are institutional investors or companies backed by institutional capital. Their business model is straightforward: acquire life insurance policies from policyholders at the steepest discount possible. Some hold those policies to maturity, collecting the death benefit when the insured passes away. But many do not hold the policy at all. Instead, they turn around and resell it, often immediately, to institutional investors, hedge funds, or bundled portfolio buyers at a significant markup. They are functioning as middlemen, buying low from an uninformed seller and selling high into the institutional market. The policyholder takes the discounted payout while the direct buyer captures the spread.

This is the part of the life settlement market that rarely gets discussed publicly. A direct buyer who purchases a $500,000 policy from a senior for $80,000 and resells it into the institutional market for $160,000 has just made a substantial profit without ever holding the policy as a long-term investment. The senior, meanwhile, accepted what felt like a windfall without ever knowing their policy was worth twice what they received.

None of this is illegal. But it reveals a structural imbalance that the industry has been slow to address. Direct buyers are spending millions of dollars on television ads, direct mail campaigns, digital advertising, and call center operations designed to reach policyholders before anyone else does. Their goal is to be the only offer on the table.

And it works. A significant number of policyholders who sell their life insurance in the United States receive only one offer. They have no basis for comparison, no competitive tension in the process, and no independent representation looking out for their financial interest.

The Marketing Budget Gap

Consider the economics. A direct buyer who acquires a $500,000 policy for $80,000 instead of $150,000 has just improved their return by a significant margin. That $70,000 difference is real money, and it came directly out of the seller's pocket. This means every dollar a direct buyer spends on marketing to reach that seller first is a high-ROI investment, because the payoff is a cheaper acquisition.

Brokerages, by contrast, earn a commission on the transaction. Their fee is a percentage of the sale price. They have an incentive to maximize the payout, but their marketing budgets are a fraction of what direct buyers spend. The result is a market where the loudest voice in the room belongs to the party with the least alignment to the seller's financial interest.

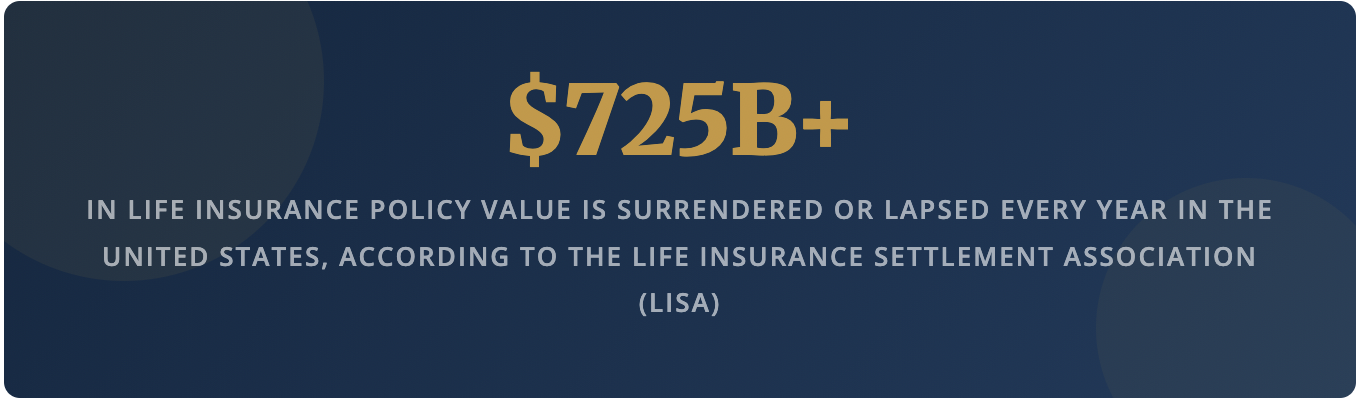

This is not a niche issue. According to the Life Insurance Settlement Association (LISA), the life settlement market processes billions of dollars in face value annually. But the gap between what sellers actually receive and what their policies are worth on the open competitive market remains significant. That gap is the direct consequence of a market where most transactions happen without competitive bidding.

What Brokerage Advocacy Actually Changes

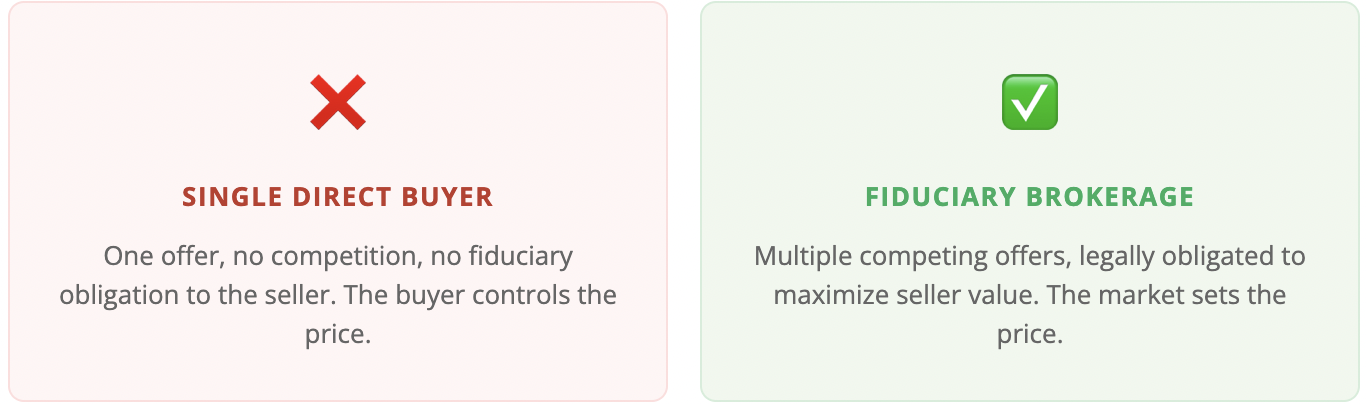

A life settlement broker is licensed by the state and, in most jurisdictions, carries a fiduciary obligation to the policyholder. The broker does not buy the policy. Instead, they take the policy to a network of competing institutional buyers and facilitate a competitive bidding process. The result is straightforward: More buyers see the policy, more offers come in, and the seller receives a higher payout.

The data supports this consistently. Policies that go through a competitive brokerage process routinely settle for multiples of what a single direct buyer initially offers. This is not because direct buyers are acting in bad faith. It is because a buyer in a non-competitive environment has no reason to offer more than the minimum a seller will accept.

Brokerage representation changes the dynamic entirely. It introduces market forces into a transaction that would otherwise be a private negotiation between an institutional buyer and an individual seller who has no leverage, no information, and no representation.

What the Industry Needs to Do

The life settlement industry has made real progress on transparency, technology, and regulatory standards over the past decade. But if the default path for most sellers is still a single offer from a direct buyer with no competing bids and no independent representation, then the market is not functioning the way it should.

There are several things that need to happen:

- Regulatory bodies should require disclosure at the point of sale informing policyholders of their right to independent brokerage representation before accepting any offer.

- Financial advisors and estate attorneys need to understand the difference between referring a client to a single buyer and referring them to a fiduciary broker who will create competitive tension.

- Industry associations should advocate for brokerage representation as a best practice standard, not a secondary option.

- Consumer education efforts need to come from sources other than the buyers themselves, who have a vested interest in keeping the process simple and non-competitive.

None of this requires new legislation or a fundamental restructuring of the market. It requires the industry to acknowledge that a market where most sellers receive exactly one offer is a market that is underserving the people it claims to protect.

The Bottom Line

The life settlement market is not short on capital, technology, or regulatory infrastructure. What it is short on is seller advocacy. The policyholders entering this market are overwhelmingly seniors on fixed incomes making one of the most consequential financial decisions of their later years. They deserve more than a single take-it-or-leave-it offer from the party with the most to gain from underpaying them.

Stronger brokerage advocacy is not about attacking direct buyers. It is about building a market where the seller has a real seat at the table, with real representation, real competition, and a real chance at receiving fair market value for their asset. Until that becomes the standard, the life settlement industry will continue to leave billions of dollars on the wrong side of the transaction.