In 2026, investment decision-making is being shaped by a combination of cautious confidence and meaningful structural change. Firms are balancing heightened risk awareness with the need to adapt to shifting market conditions, evolving interest rate dynamics, and the expanding role of private markets. Conning's 2025 Investment Risk Survey provides insight into how U.S. insurers are responding—positioning portfolios, reassessing risk appetite, and aligning investment strategies with long-term objectives.

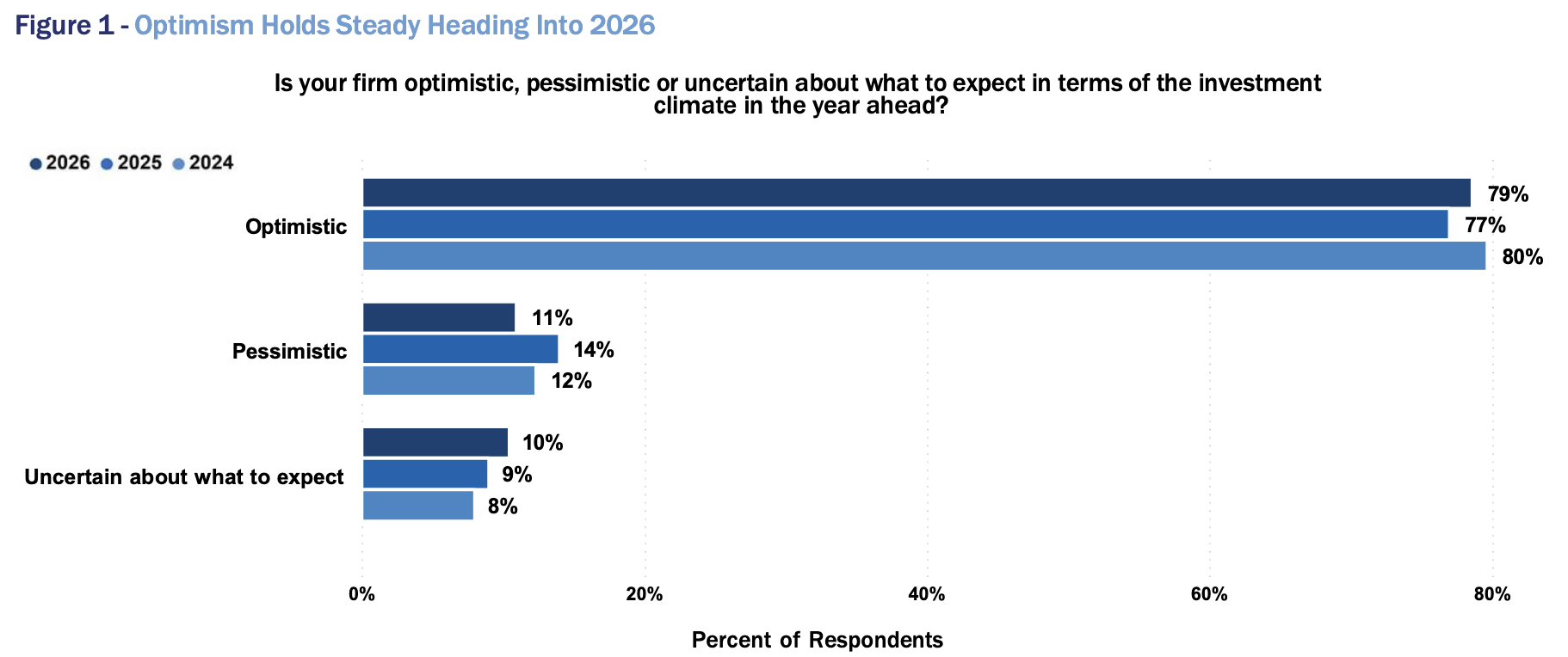

U.S. insurers remain optimistic about investment conditions for 2026 (Figure 1), with a majority expecting to take on additional investment risk. While uncertainty has increased, carriers continue to see meaningful opportunities to improve their portfolio outcomes. These findings are based on Conning's annual survey of 201 investment decision-makers in the U.S. insurance industry.

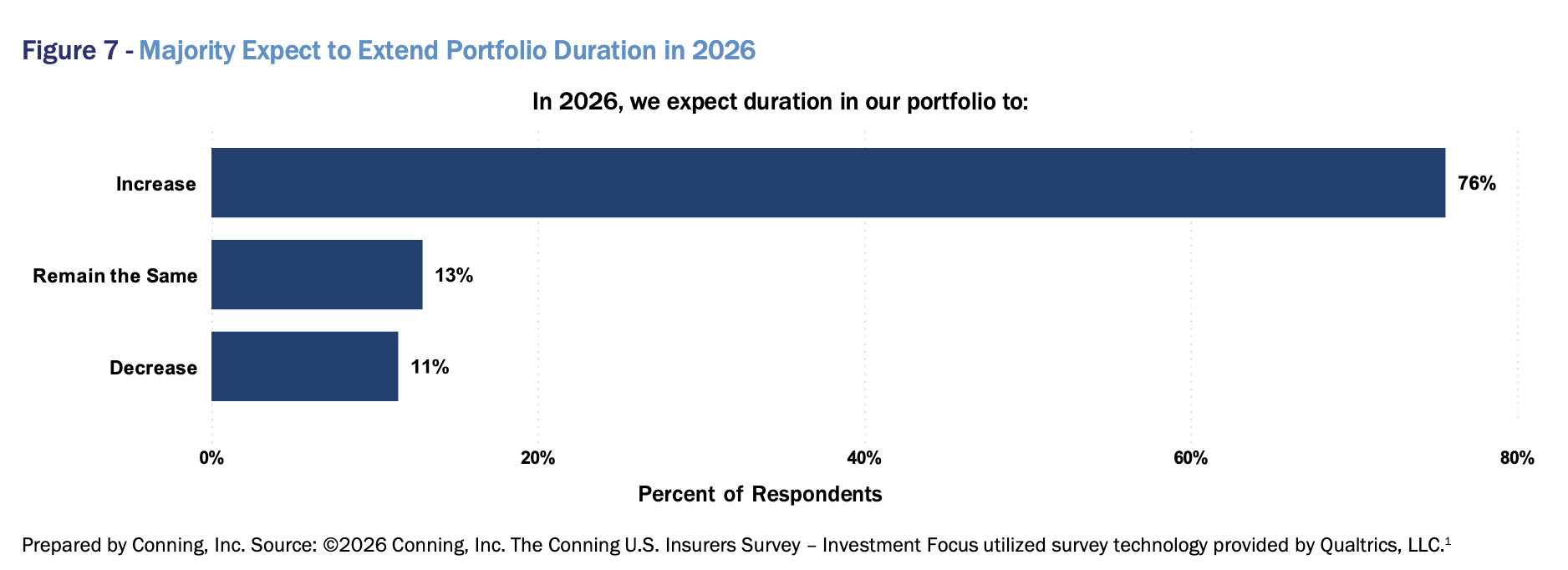

Prepared by Conning, Inc. Source: ©2026 Conning, Inc. The Conning U.S. Insurers Survey – Investment Focus utilized survey technology provided by Qualtrics, LLC.

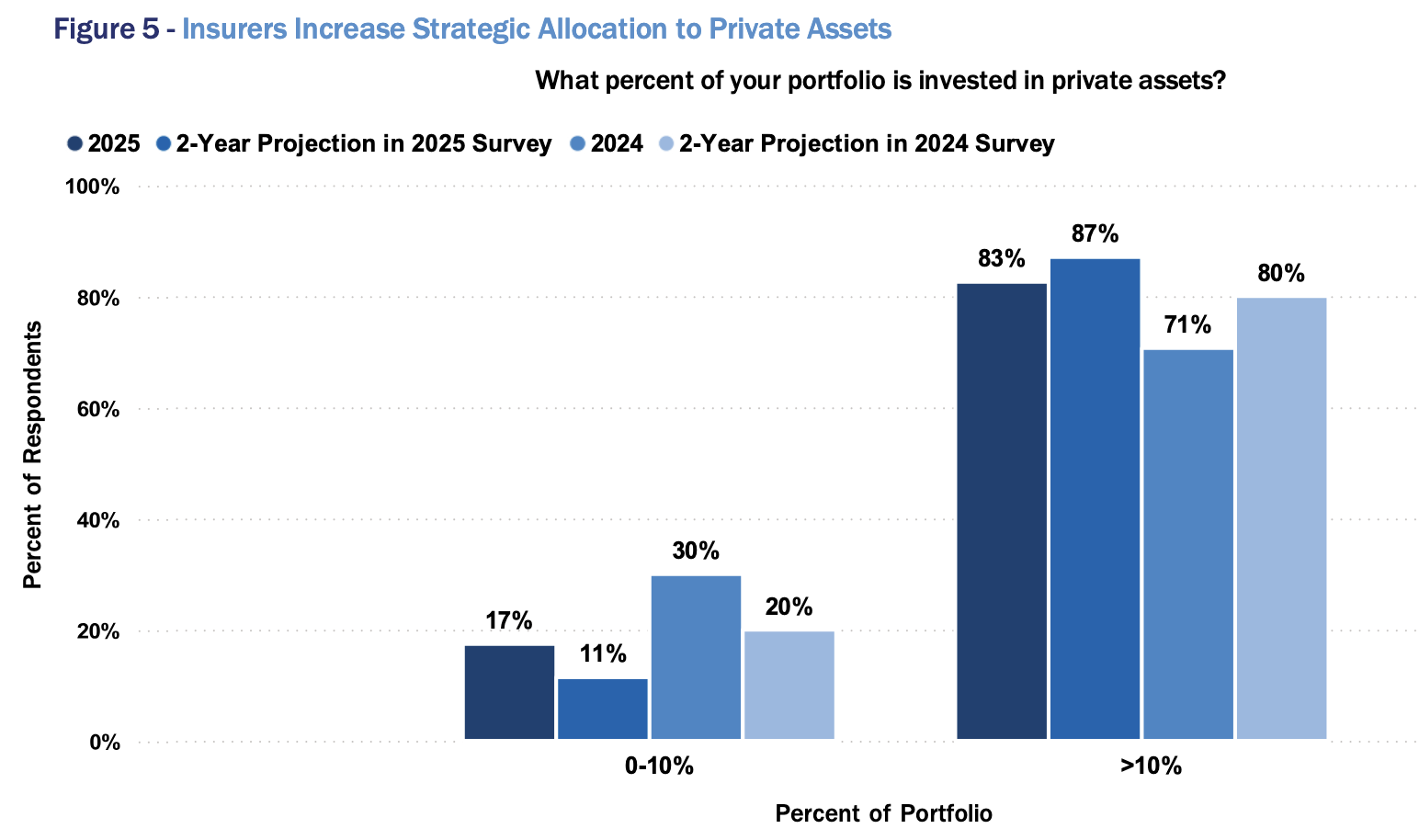

Private assets remain a key focus of insurance company investment strategy. The majority of respondents (83%) currently have private asset allocations in excess of 10% of their portfolios. Respondents expect growth in their overall private asset allocations, accompanied by broader diversification across private investment strategies.

Uncertainty about the future of interest rates is drawing increased attention among insurers. After several years of elevated yields, there is a renewed focus on Federal Reserve policy and expectations for lower interest rates in 2026. Against this backdrop, survey results provide additional insight into how insurers are responding to a more complex investment environment.

Optimism While Reducing Risk

Overall, respondents remain optimistic about the investment climate in 2026, with sentiment rebounding from a slight dip in the prior year's survey (Figure 1). Levels of pessimism remain muted. Optimism varies by insurer balance sheet size, with optimism highest among smaller insurers: 83% of respondents at firms with invested assets of under $1 billion reported a positive outlook.

While overall optimism reflects many considerations, investment opportunity is a key driver. Seventy-six percent of respondents indicate that investment opportunities for insurers are improving. Reasons for optimism include:

- Higher yields for high-quality fixed income securities

- Attractive investment opportunities across a variety of private markets

- Growing investment opportunities in sectors, including both traditional and digital infrastructure

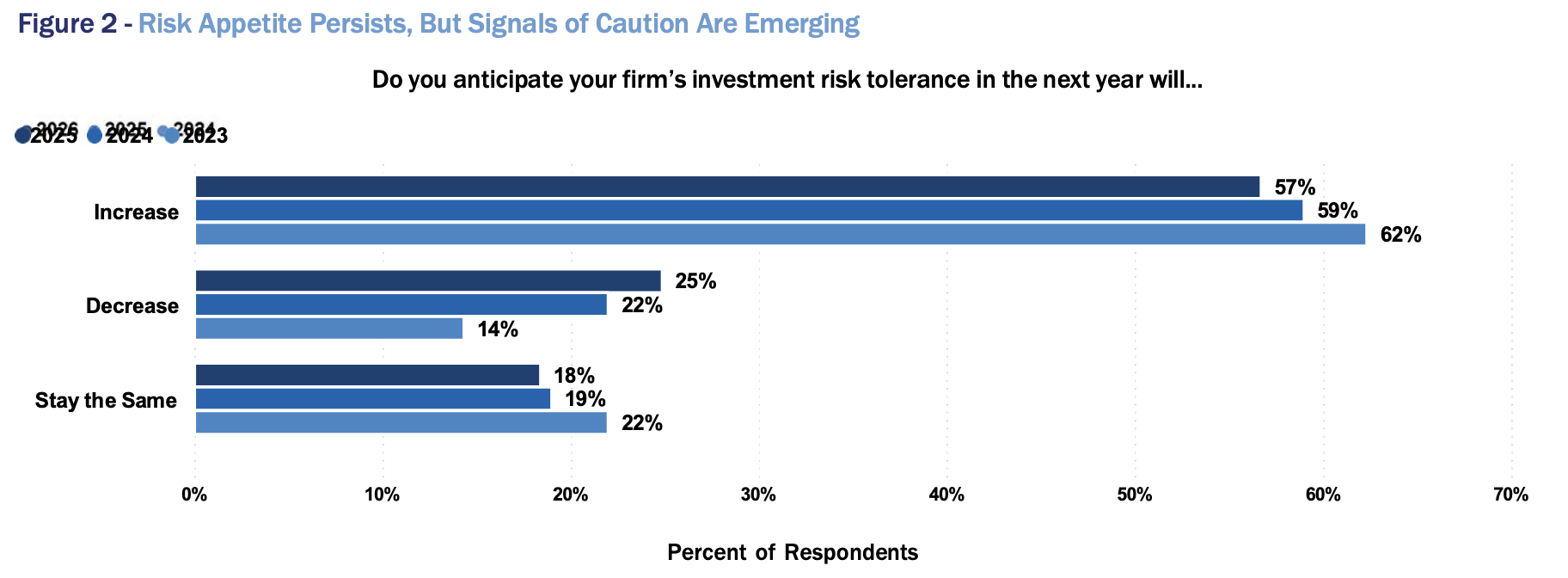

For the fourth consecutive year, most respondents expect to increase their investment risk in the year ahead (see Figure 2), although the sentiment has moderated since 2022, declining from 65% to 57%. Respondents from larger firms were more likely to indicate an expectation to reduce risk. This trend is also evident among property & casualty carriers, where 28% report a likelihood of decreasing investment risk in 2026. Part of this may reflect strong equity market performance over the past several years, which has elevated risk assets—including equities—within overall portfolio allocations.

Prepared by Conning, Inc. Source: ©2026 Conning, Inc. The Conning U.S. Insurers Survey – Investment Focus utilized survey technology provided by Qualtrics, LLC.

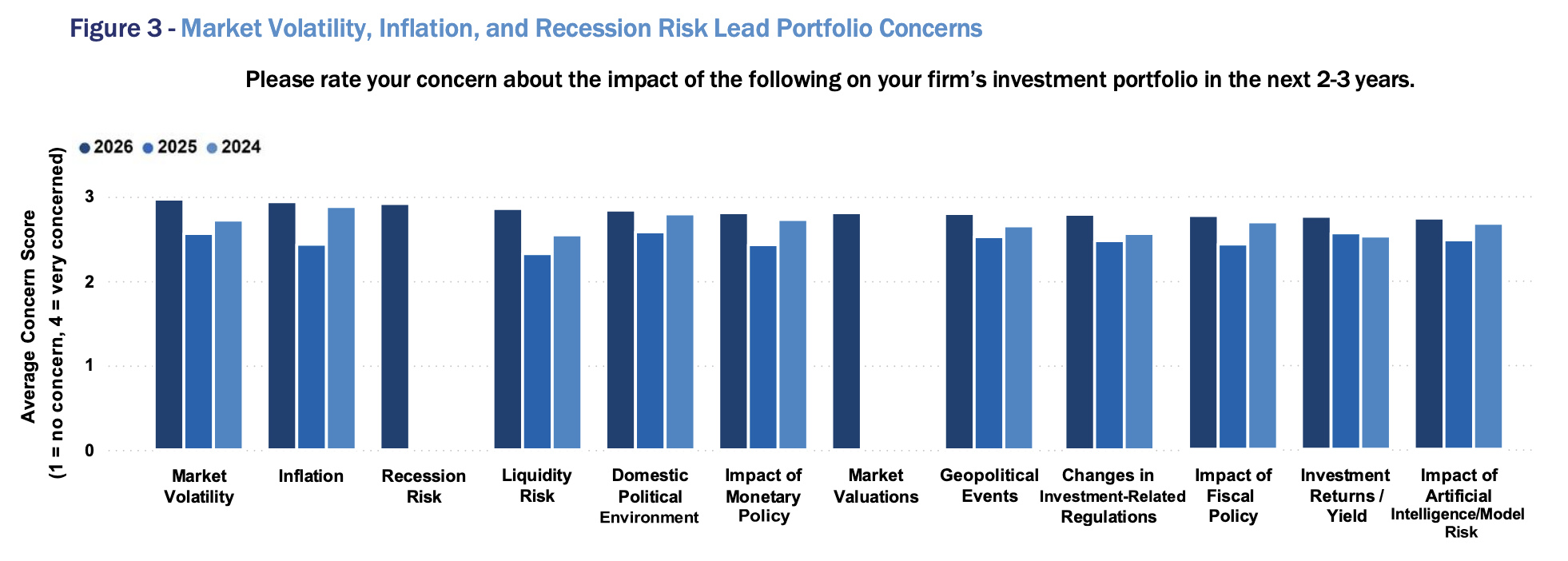

While market and asset price volatility was cited as the top portfolio risk, the reemergence of inflation as a leading concern for insurers is notable. Inflation ranked as the top concern in the first three years of this survey and fell to seventh in last year's iteration. While inflation did not reclaim the top spot, it ranked a close second. Rounding out the top three risks was the risk of recession, which was a new option respondents could select in this year's survey (Figure 3). Overall, the level of concern across risks is elevated compared with recent years, suggesting insurers may be approaching 2026 and 2027 with increased caution.

Prepared by Conning, Inc. Source: ©2026 Conning, Inc. The Conning U.S. Insurers Survey – Investment Focus utilized survey technology provided by Qualtrics, LLC.

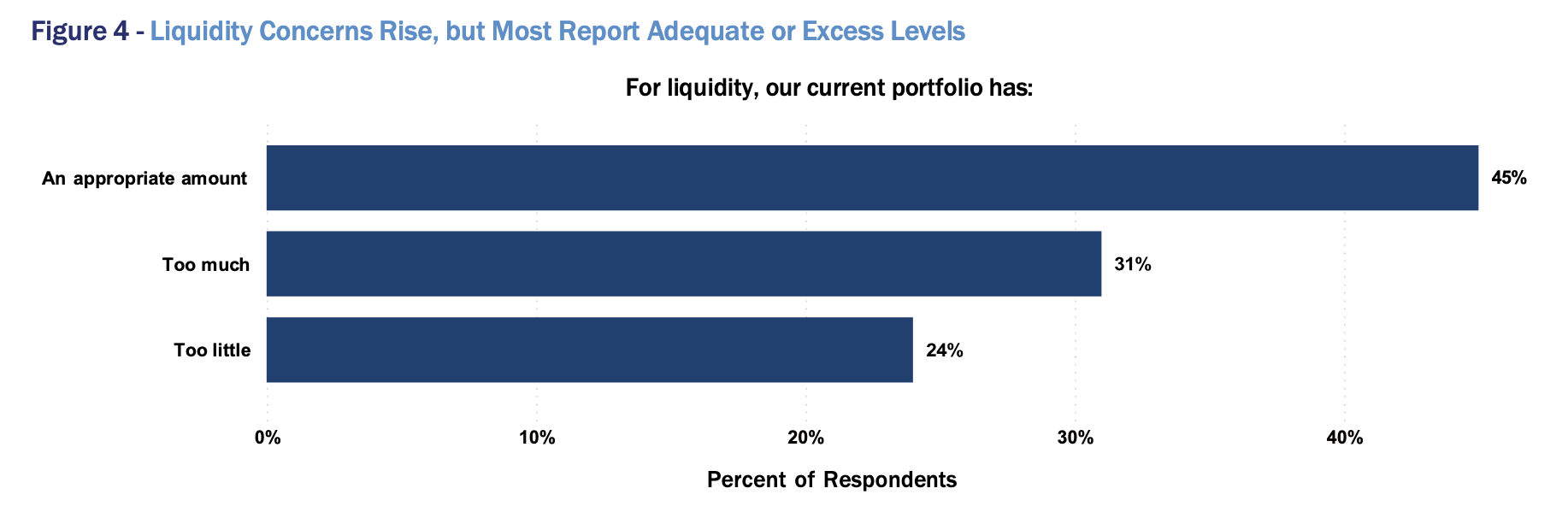

Liquidity risk has become a significantly higher priority for insurers. It ranked well below other considerations in last year's survey but has gained prominence this year, potentially reflecting the growing level of private assets in portfolios. In a separate question, 45% of respondents indicated that their portfolios have an appropriate level of liquidity. Interestingly, 31% reported having too much liquidity, which could continue to support allocations to less liquid investments, as shown in Figure 4. Risks that appear to have become less critical include investment yields and the effect of AI, potentially reflecting a shift in insurer mindset as elevated yields and AI adoption have persisted and become less novel. These views on risk and opportunity are closely reflected in insurers' approach to private assets.

Prepared by Conning, Inc. Source: ©2026 Conning, Inc. The Conning U.S. Insurers Survey – Investment Focus utilized survey technology provided by Qualtrics, LLC.

Private Assets Remain a Strategic Focus

While liquidity concerns may be increasing, insurers' appetite for private assets is expected to remain robust (Figure 5). In last year's survey, 71% of respondents reported private asset allocations between 5% and 20%; this year, that figure increased to 87%. Similarly, 63% of respondents last year expected to have between 10% and 25% allocated to private assets within two years, compared with 79% in the current survey. This trend is evident not only in the annual survey results, but also in continuing conversations with carriers. While several factors are driving this increased interest in private markets, one key contributor is the continued convergence of public and private markets, which is expanding investment opportunities for insurers.

Prepared by Conning, Inc. Source: ©2026 Conning, Inc. The Conning U.S. Insurers Survey – Investment Focus utilized survey technology provided by Qualtrics, LLC.

Insurers remain risk-aware when evaluating private asset allocations. The top concern when considering an expansion of private assets is capital efficiency. Central to this discussion is investment structure: more than half of respondents reported using rated note feeders, collateralized fund obligations, or similar structures to access private investments in the past year. Other key considerations include liquidity impact, the availability of data and analytics to support private asset allocations and securing management and board approval.

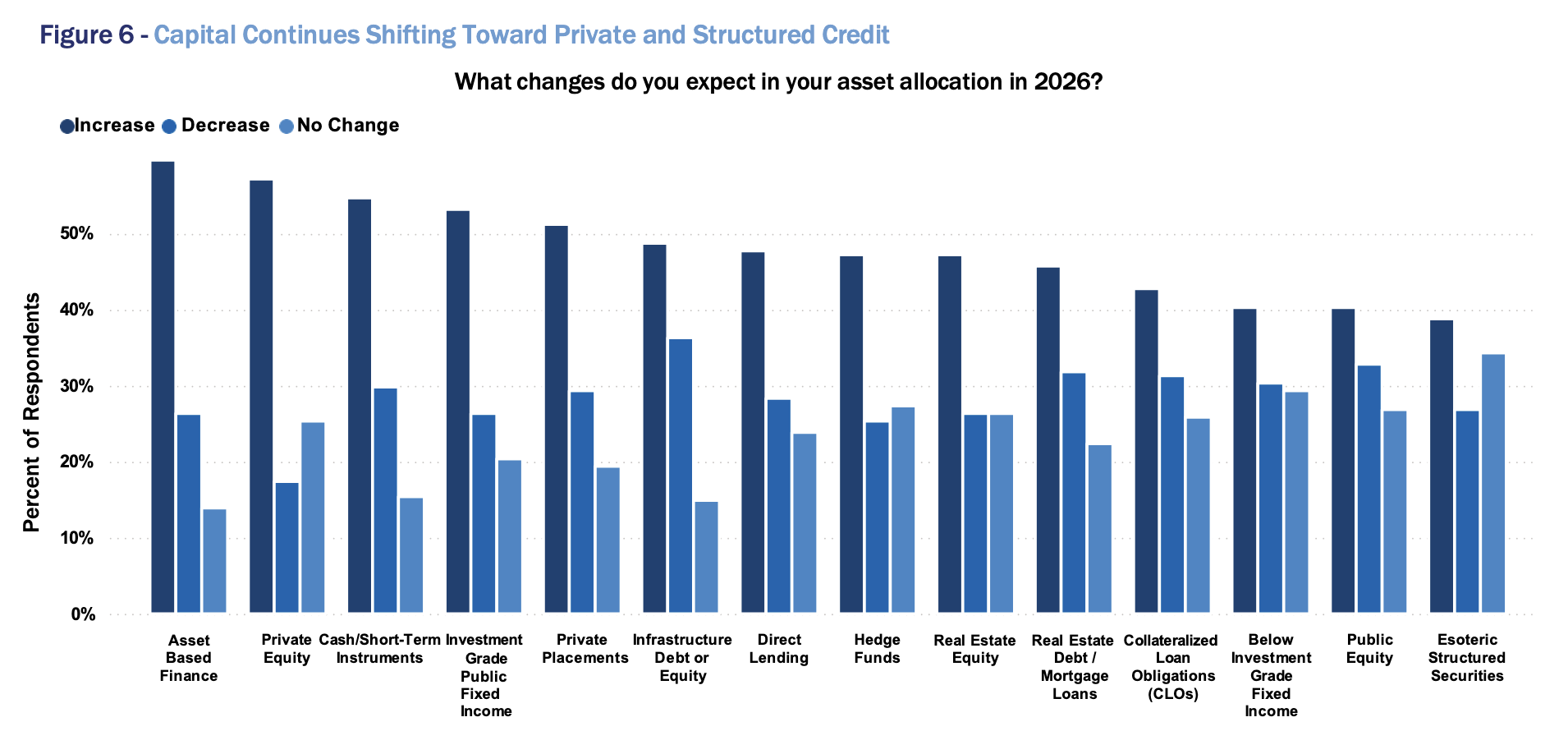

Allocation expectations for 2026 reflect clear preferences across private asset categories (Figure 6). Asset-based finance is the most cited area for increased allocation in 2026, with 60% of respondents expecting to increase exposure. Other areas expected to grow include both public and private investments. Within private markets, roughly half of respondents anticipate increasing allocations to private equity, private placements, real estate, and infrastructure. In public markets, short-term securities and investment-grade public securities continue to attract interest.

Prepared by Conning, Inc. Source: ©2026 Conning, Inc. The Conning U.S. Insurers Survey – Investment Focus utilized survey technology provided by Qualtrics, LLC.

Insurers' Outlook for 2026

Higher interest rates have been a significant tailwind for investment income; however, interest rates and prospective Federal Reserve rate cuts are now more central to investment strategy. In the survey, 47% of respondents indicated that the Federal Open Market Committee actions will be significantly important to their investment strategy in 2026, up from 38% in the prior year. Only 1% indicated that FOMC actions would have minimal impact on their strategy, compared with 12% last year.

Insurers are not focused solely on short-term rates. More than half of respondents (52%) expect the yield on the 10-year Treasury to end the year below 3.5%, while only 12% expect it to finish above 4%—levels where it has traded at the beginning of 2026. Beyond interest rates, insurers are also anticipating a return of inflationary pressures: 57% expect inflation to increase moderately over the next 12 months, and an additional 19% expect inflation to increase significantly. These expectations are translating directly into portfolio positioning decisions.

Portfolio Positioning Reflects Rate Expectations

With expectations for falling long-term interest rates and Federal Reserve actions in 2026, it is not surprising that a growing share of insurers expect to increase portfolio duration. Last year, 64% of respondents planned to increase duration; this year, that figure has risen to 76% (Figure 7). As in last year's survey, most respondents also expect to increase exposure to floating-rate assets in 2026—57% compared with 53% last year—suggesting that an interest-rate barbell approach is likely to remain prevalent. Credit risk and equity risk were also cited as key considerations in portfolio positioning.

Prepared by Conning, Inc. Source: ©2026 Conning, Inc. The Conning U.S. Insurers Survey – Investment Focus utilized survey technology provided by Qualtrics, LLC.

Portfolio turnover was higher than in last year's survey, with 73% of respondents reporting increased turnover in 2025, compared with 50% in the prior survey. Among those reporting higher turnover, the most common reason was to pursue tactical market opportunities. Other drivers included aligning portfolios with longer-term investment targets and generating cash to support portfolio needs.

Positioning Portfolios for a More Complex Environment

Conning's 2025 Investment Risk Survey finds that insurers remain optimistic, while also recognizing meaningful challenges in the year ahead. Uncertainty around interest rates and shifting asset allocations underscores the importance of building portfolios that are resilient and capable of performing across a range of potential economic environments.

As insurers pursue greater diversification and private asset allocations continue to grow, gaining a holistic understanding of how portfolio risks and insurance risks interact will be increasingly critical. Accessing investments through insurance-friendly, capital-efficient vehicles remains a key consideration for certain strategies. As allocations to less liquid investments expand, understanding portfolio liquidity and enterprise cash-flow dynamics becomes even more important.

In an increasingly complex market environment, insurers must ensure they have the tools and partners necessary to align ALM, capital, and investment strategy in support of enterprise objectives and policyholder obligations. Differences in business goals, risk tolerance, and lines of business reinforce the need for customized solutions tailored to each insurer's unique circumstances.