Driver fatigue is one of the most consequential risks in commercial auto, and one of the least measurable. When dashcam footage is used as evidence in litigation, SambaSafety's 2026 Driver Risk Report highlights that fatigue is named in 9% of crashes, nearly eight times higher than what is reported in police reports.

With no agreed-upon definition, no field test to confirm it, and no reliable way to attribute it after a crash, driver fatigue has remained on the periphery of underwriting conversations—even as the claims it contributes to quietly shape loss ratios across the industry.

SambaSafety's report indicates that the industry is beginning to shift. As telematics and camera technology mature, insurers are using new tools to detect behavioral signals associated with fatigue. However, to interpret these signals and act on them, insurers need to understand why fatigue has been so difficult to measure in the first place.

Why Fatigue Is So Hard to Pin Down

Kyla Hagan-Haynes, principal researcher at SambaSafety, spent years researching this challenge.

"Historically, researchers have had to rely on self-reports and proxy measures—lack of skid marks, unexpected lane departures," she explained. "There's no breathalyzer equivalent. The variability in how prevalence is estimated is a direct result of that."

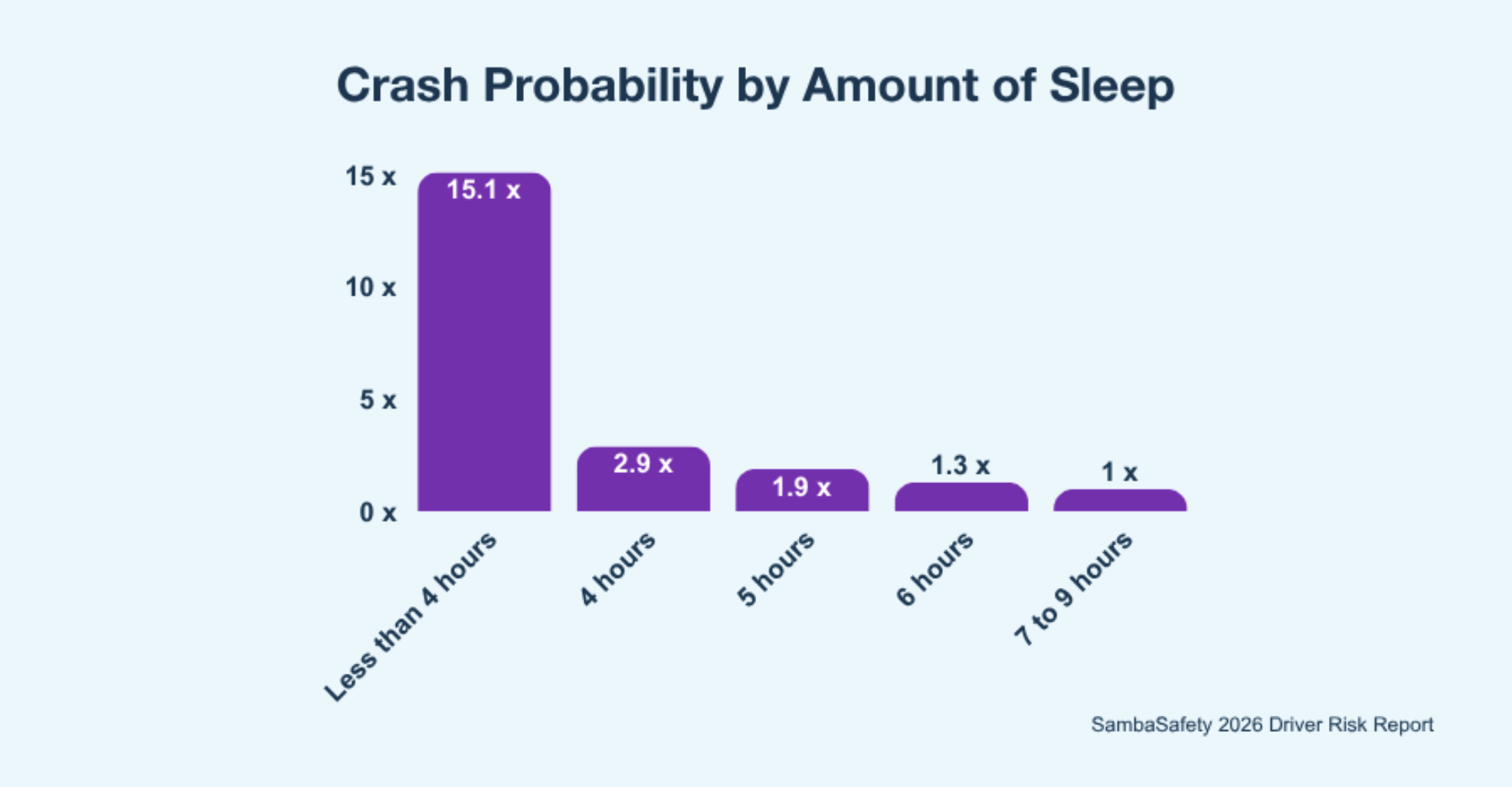

What's captured in loss data understates not only how often fatigue contributes to crashes but also how severe those crashes tend to be. More than 17% of fatal crashes involve fatigue, and one in three crashes involving a drowsy driver result in injury, according to SambaSafety's 2026 Driver Risk Report. For insurers, that severity gap has direct implications for loss ratios, litigation exposure, and how fatigue risk is, or isn't, priced.

Fatigued drivers rarely brake before impact, making fatigue-related crashes disproportionately severe, leading to higher rates of bodily injury claims and more total losses—events that push verdicts into nuclear territory. As Matteo Carbone, founder of the IoT Insurance Observatory, noted in the report, "Sleep is not a wellness topic. It is a road risk variable." With thermonuclear verdicts exceeding $100 million, up 81% year over year in 2024, the litigation landscape has become an amplifier of poorly documented risks.

Hagan-Haynes highlighted a dimension of this risk that doesn't get enough attention, noting that hours-of-service compliance doesn't ensure a driver is rested. Plaintiff attorneys use ELD logs not just to examine the day of a crash, but also to reconstruct weeks of scheduling patterns, building a picture of the pressure placed on a driver to consistently work up to the maximum limits allowed by regulation.

A fleet that's technically compliant can still face a compelling fatigue argument in litigation if its schedule practices don't reflect genuine fatigue risk management.

"When I talk to customers, I also see so many fleets that are not regulated drivers—they don't have CDLs, they have no hours-of-service requirement," Hagan-Haynes said. "There are no rules around how long a non-CDL driver can drive. And companies can be held liable even for a commute. I've seen it happen, where a driver worked two weeks straight, got in a vehicle to drive home, and fell asleep [at the wheel]."

It's a blind spot most commercial auto insurers aren't accounting for.

What the Data Is Starting to Reveal

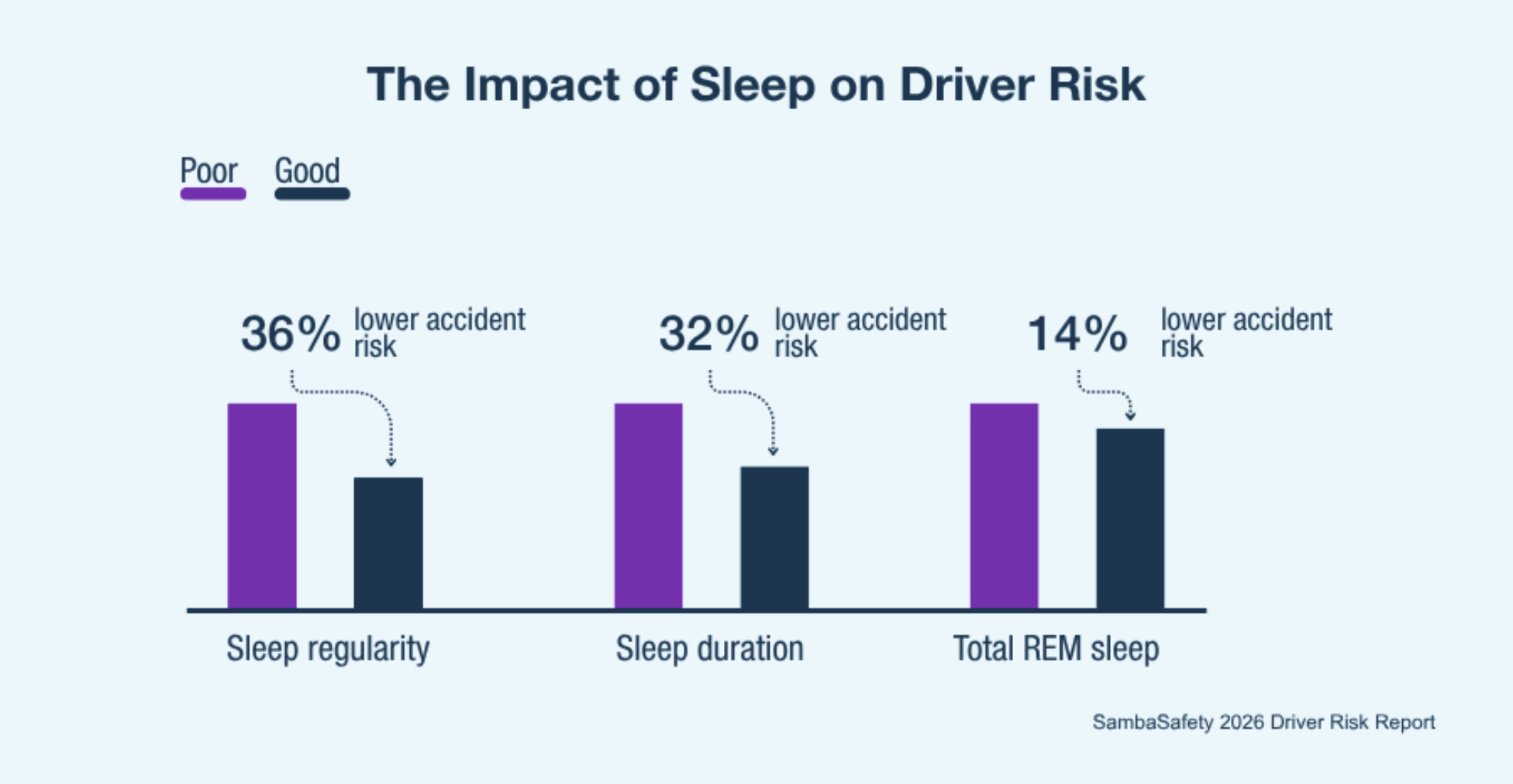

A Discovery Vitality study referenced in SambaSafety's report found that sleep regularity is associated with a 36% lower crash risk, sleep duration with a 32% reduction, and total REM sleep with a 14% reduction. For underwriters, that data suggests that off-duty hour patterns in telematics aren't just operational—they're a risk signal worth accounting for in underwriting.

For Hagan-Haynes, the most important underwriting variable is almost straightforward. "The most significant factor when it comes to driver fatigue is whether a driver is getting sufficient sleep—for most people, seven to eight hours," she said. "Telematics data on working hours and off-duty windows is going to be an important piece of data to consider."

Whether a fleet has a fatigue management policy at all is another signal. Not just the existence of one, but whether it's enforced, communicated to drivers and managers, and addresses scheduling, medical examinations, and rest opportunity—not just regulatory minimums. "If they don't have anything to share with insurers other than their ELD logs, that's informative," noted Hagan-Haynes.

In-cab cameras that detect eye closure or lane deviation are valuable, and their adoption among commercial fleets is growing. But Hagan-Haynes was direct about where they sit in the risk management chain. "That's far downstream. By the time a camera is flagging eyelid closures, you're really late in the game."

Real fatigue management happens in scheduling practices, sleep education, medical screening, and a culture that empowers drivers to take rest when they need it. For insurers, these factors matter in most jury trials, not only in responding to what happened at the moment of a crash, but also to the whole pattern of what didn't happen—the interventions that could have occurred but didn't.

When telematics data shows fatigue signals despite a fleet's stated policy, Hagan-Haynes framed it as a root cause question, not just a pricing adjustment. Is the risk concentrated in a single driver, suggesting an individual issue with a medical component? Or spread across many drivers, pointing to something systemic in scheduling or culture? The answer shapes what comes next and what a productive conversation between insurer and fleet looks like.

The Role Insurers Play in Closing the Fatigue Risk Gap

Renewal conversations are among the most effective moments insurers have to influence how policyholders think about risk. A fleet with a genuine fatigue risk management program that goes beyond regulatory compliance represents a meaningfully different risk—one that should be reflected in how a book is evaluated throughout the policy term, not just at renewal.

The industry has spent years absorbing losses it couldn't fully explain. Fatigue is part of that story. The insurers that move first to build it into their risk frameworks won't just improve their own outcomes; they'll help define what responsible commercial auto underwriting looks like going forward.

To explore the full findings from SambaSafety's 2026 Driver Risk Report, visit http://sambasafety.com "