The mobility landscape is evolving rapidly – once defined by individual vehicle ownership and predictable risk models, mobility now includes electric vehicle (EV) fleets, autonomous driving systems, shared mobility platforms and micromobility solutions. Driven by technological innovation, sustainability mandates and shifting consumer behavior, this transformation is reshaping transportation risk across industries and geographies.

For commercial insurers, these changes demand a rethink of traditional commercial auto insurance, spanning underwriting, pricing, liability allocation and risk management while increasing the need for data-driven decision-making.

Mobility Market Transformation

Modern mobility models are redefining how risk is created and transferred. Liability is shifting from human drivers to manufacturers, software developers, fleet operators, and platform providers. EV adoption is driving higher claim severity, while shared and usage-based mobility introduces fluctuating exposure that challenges static rating models.

Regulation is evolving alongside these market changes. States such as California, Arizona and Texas are establishing autonomous vehicle (AV)-specific operational and liability requirements, requiring insurers to adapt underwriting frameworks quickly to remain compliant and competitive.

Autonomous Vehicles: Fewer Crashes, More Complexity

Autonomous technology is moving from pilot programs to commercial deployment across logistics, delivery, and passenger transportation. According to a Goldman Sachs forecast, by 2040 autonomous liability and risk will shift to reduce the underlying cost per mile by over 50%, from $0.50 to $0.23.

We think that is more likely to underestimate, rather than overestimate, the cost reduction, and related societal benefits.

AVs are expected to deliver substantial safety improvements: Research from Deloitte found that human error causes 94% of crashes, while autonomous technology could reduce collisions by up to 90%. However, while AVs may lower collision frequency, they also introduce more complex loss scenarios when incidents occur.

In an AV accident, liability may rest with the vehicle manufacturer, software provider or fleet operator rather than the driver. This shift elevates the importance of product liability, technology errors and omissions (E&O) and contractual risk transfer. In California, commercial AV operations must hold $5 million liability per vehicle, signaling a long-term structural shift in commercial auto insurance.

Shared Mobility and Usage-Based Exposure

Shared mobility platforms, including ridesharing, carsharing and subscription fleets, scale rapidly, particularly in urban markets. These models generate highly variable exposure driven by multiple drivers, high usage rates and short-term vehicle use.

For insurers, shared mobility accelerates the move toward usage-based insurance (UBI) and telematics-driven pricing, enabling premiums to better align with real-world risk rather than fixed assumptions.

Electrification and Fleet Risk

Electrification is one of the most material forces reshaping commercial auto risk, with the IEA's Global EV Outlook 2025 underscoring the rapid growth in EV adoption.

According to published reports, EV fleets introduce higher average claim severity due to expensive battery systems, specialized repair requirements and longer repair cycles. Additional exposures include charging infrastructure liability, fire risk and business interruption related to extended downtime. EV fleets present opportunities for insurers to support environmental, social and governance (ESG) objectives through green underwriting incentives.

Micromobility and Last Mile Risk

Micromobility solutions such as e-scooters and e-bikes are increasingly used for last mile transportation and urban delivery. While they support congestion reduction and sustainability goals, they also create risk and new exposures and operate within inconsistent regulatory frameworks, particularly for commercial operators and municipalities.

These lightweight vehicles are redefining last mile connectivity. According to the Micro-Mobility Market Size, Share and Industry Growth Report 2025, the global micromobility market was valued at $63 billion in 2024 and is expected to grow to $162 billion by 2029.

KEY MOBILITY RISKS FOR COMMERCIAL INSURERS

- Shifting liability from human drivers to original equipment manufacturers (OEMs), technology providers and platform providers

- Higher EV repair costs and claim severity

- Charging infrastructure and fleet hub property exposure

- Regulatory uncertainty across jurisdictions

COMMERCIAL INSURANCE IN A NEW RISK LANDSCAPE

The mobility transformation creates significant opportunities for insurers:

- Embedded Insurance Partnerships: Collaboration with OEMs, telematics providers and mobility platforms enables insurers to integrate coverage directly into fleet operations.

- Usage-Based and EV-Specific Products: UBI and EV-focused coverage align pricing with exposure while addressing battery and infrastructure risk.

- Advanced Analytics and Telematics: Artificial intelligence (AI)-driven underwriting and real-time monitoring improve pricing accuracy and loss prevention.

- ESG-Aligned Insurance Solutions: Incentives tied to electrification and emissions reduction position insurers as sustainability partners, not just risk carriers.

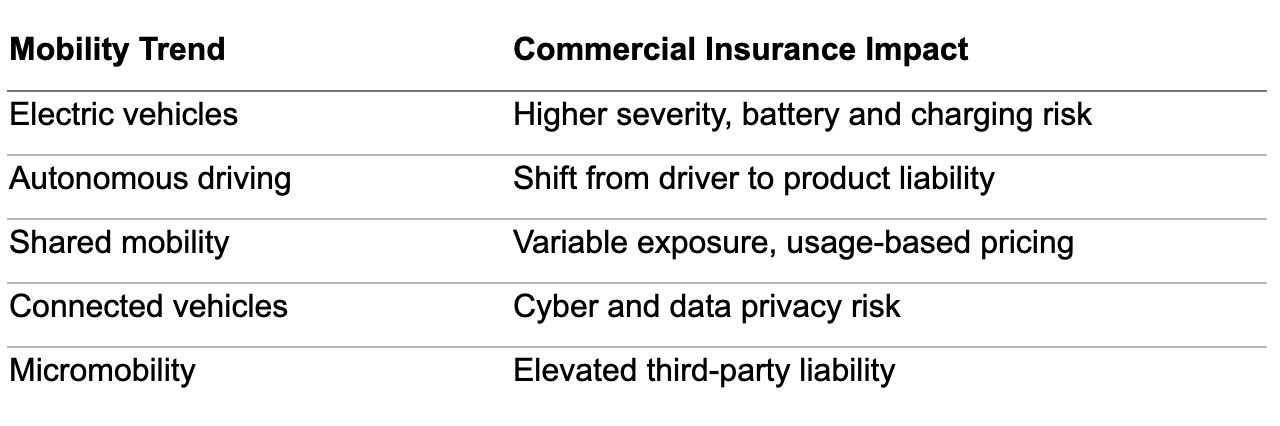

MOBILITY TRENDS AND THEIR INSURANCE IMPACT

STRATEGIC CONSIDERATIONS FOR INSURERS

To remain competitive, commercial insurers should:

- Invest in digital underwriting, telematics and AI

- Develop flexible, modular underwriting models

- Expand expertise in product liability and technology risk

- Engage proactively with regulators

- Build ecosystem partnerships across mobility value chains

INSURANCE AS AN ENABLER OF FUTURE MOBILITY

The evolution of mobility is redefining transportation and insurance. Electrification, autonomy, shared platforms and micromobility are reshaping liability, increasing loss severity in some segments and introducing new risk dimensions. They also offer insurers an opportunity to lead through innovation and collaboration.

Commercial insurers that embrace data-driven underwriting, embedded partnerships and sustainability-aligned solutions will move beyond traditional risk transfer to become enablers of the future mobility ecosystem. As mobility becomes a service, insurance must evolve with it to support safer, more sustainable transportation systems.