This is part two of a series of five on the topic of risk appetite and its associated FAQs.

The author believes that enterprise risk management (ERM) will remain locked in organizational silos until boards are mobilized in terms of their comprehension of the links between risk and strategy. This is achieved either through painful and expensive crises or through the less expensive development of a risk appetite framework (RAF). Understanding risk appetite is very much a work in progress for many organizations. The first article made a number of observations of a general nature based on experience in working with a wide variety of companies. This article describes the risk landscape, measurable and unmeasurable uncertainties and the evolution of risk management.

The Risk Landscape

Lessons learned following the great financial crisis (GFC) include the importance of establishing an effective risk governance framework at the board level. In essence, two key questions must now be addressed by boards.

First, do boards express clearly and comprehensively the extent of their willingness to take risk to meet their strategic and business objectives? Second, do they explicitly articulate risks that have the potential to threaten their operations, business model and reputation?

To be in a position to provide credible answers to these fundamental questions, we must first seek to understand the relationship between risk and strategy.

It is RMI’s experience that risk and strategy are intertwined. One does not exist without the other, and they must be considered together. Such consideration needs to take place throughout the execution of strategy. Consequently, it is vital that due regard is given to risk appetite when strategy is being formulated1

Crucially, risk is now defined as "the effect of uncertainty on objectives."2

It is clear, therefore, that effective corporate governance is strategy- and objective-setting on the one hand, and superior execution with due regard for risks on the other. This particular landscape is what we in RMI refer to as the interpolation of risk and strategy. For this reason, RMI describes board risk assurance as assurance that strategy, objectives and execution are aligned. Alignment is achieved through operationalization of the links between risk and strategy, which will be described in the final article in this series.

Before further discussion, however, we would like to draw attention to observations based on our practical experience that give cause for concern, namely:

1. Risk appetite: While we now have a globally accepted risk management standard3 and sharper regulatory definition of effective risk management for regulated organizations, there is as yet much confusion, and neither a consensus nor an internationally accepted guidance, as to the attributes of an effective risk appetite framework.

2. Risk reporting: In relation to risk reporting, two significant matters arise:

Risk registers that are primarily generated on the basis of a compliance-centric requirement, as distinct from an objectives-centric4 approach, tend to contain lists of risks that are not explicitly associated with objectives. As such, they offer little value in terms of reporting on risk performance.

Note: RMI supports the adoption of a board-driven, objectives-centric approach5 to reporting and monitoring risks to operations, the business model and reputation.

Risk registers and other reporting tools detail known risks and what we know we know. They tend not to detail emerging or high-velocity risks that have the potential to threaten the business model. As such they tend to be of limited value in terms of reporting or monitoring either unknown knowns6, or unknown unknown7 risks. This is a matter that should give boards cause for concern given pace of change, hyper-connectivity and the disruptive nature of new technologies.

3. Risk data governance: The quality, rigor and consistency in application of accounting data that is present in well-managed organizations does not equally exist in those same organizations in the risk domain.

The responsibility of directors to use reliable accounting information and apply controls over assets, etc. (internal controls) as part of their legally mandated role extends equally to information pertaining to risks that threaten financial performance. The latter is not, however, treated in an equivalent fashion to accounting data. Whereas the integrity of accounting data is assured through the use of proven and accepted accounting systems subject to audit, information pertaining to risks typically relies on the use of disparate Excel spreadsheets, word documents and Power Points with weak controls over the efficacy of copying and pasting of data from one level of report to another.

Weaknesses and failings in risk data governance can be addressed in much the same way as for other governance requirements.

For example:

a. Comprehensive training for business line managers and supervisors on:

It is also interesting to observe the diversity in understanding of emerging risk definitions. For example:

It is also interesting to observe the diversity in understanding of emerging risk definitions. For example:

- (Risk) Management Processes,

- (Risk) Vocabulary,

- (Risk) Reporting,

- Board (Risk) Assurance Requirements

- The quality, timing, accessibility and auditability of risk performance data is as rigorously and consistently applied as that for accounting data,

- Dynamic management of risk data (including risk appetite/tolerance/criteria) can be tracked at the pace of change

- Tests can be applied to the aggregation of risks to objectives at the pace of change and prompt interdictions applied when required,

- Reports, or notification, of significant risks are escalated without delay, and without risk to the originator of information.

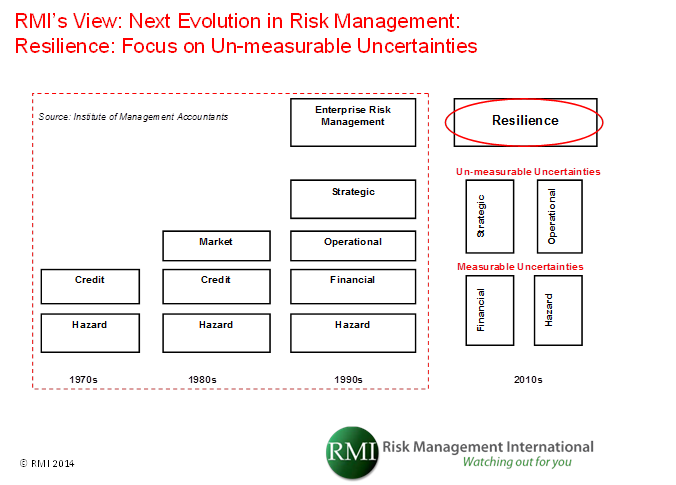

Figure 1: Evolution of risk and the emergence of “resilience” as the current era in the evolution of 21st century understanding of risk

Resilience was the theme that ran through the World Economic Forum: Global Risks 2013, Eight Edition Report. Resilience was described as capability to- Adapt to changing contexts,

- Withstand sudden shocks, and

- Recover to a desired equilibrium, either the previous one or a new one, while preserving the continuity of operations.

- Lloyds: An issue that is perceived to be potentially significant but that may not be fully understood or allowed for in insurance terms and conditions, pricing, reserving or capital setting,

- PWC: Those large-scale events or circumstances beyond one’s direct capacity to control, that have impact in ways difficult to imagine today,

- S&P: Risks that do not currently exist,

- Financial volatility (24% of respondents)

- Cyber security/interconnectedness of infrastructure (14%)

- Liability regimes/regulatory framework (10%)

- Blowup in asset prices (8%)

- Chinese economic hard landing (6%)