There is something far more interesting about the Amazon, Berkshire and JPMorgan Chase (let’s call them ABC) than the 1 million-plus lives they employ. There have been similar initiatives announced before along with countless business group on health coalitions that have made no meaningful dent in the wildly underperforming status quo healthcare system. The BUCAs (Blues United Cigna Aetna) have been adept at fighting off efforts like these. But this time, I predict it will be different. In this piece, I will explain why past efforts have failed. In a follow-on piece, I’ll explain why the ABC health initiative has great potential to be very unlike past employer-led efforts.

Note: I reference my book, which can be found on Amazon or downloaded for free.

See also: Open Letter to Bezos, Buffett and Dimon

10 reasons past efforts have led to failure:

Note: I reference my book, which can be found on Amazon or downloaded for free.

See also: Open Letter to Bezos, Buffett and Dimon

10 reasons past efforts have led to failure:

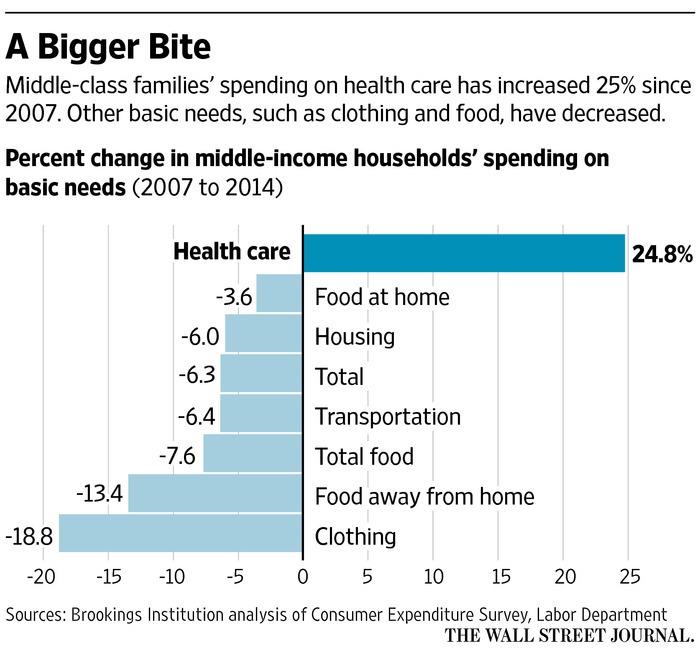

In all of the case studies in my book, the employers treated their employees like adults and explained what was going on at a macro (see the "bigger bite" graph) and micro level to explain how they wanted to ensure their teams could achieve the American Dream. Successful employers point out that healthcare is blocking the American Dream for 60% of the workforce. The math simply doesn’t work: 60% of the workforce makes less than $20 per hour, and the average family of four premiums are $26,000; in addition, greater than 50% of households have less than $1,000 in savings (largely due to healthcare costs), and more than 50% of the workforce has over a $1,000 deductible.

See also: Whiff of Market-Based Healthcare Change?

It’s no wonder that Buffett called healthcare the tapeworm on the U.S. economy. The handwriting was on the wall following the Michigan primary that showed that populism was being driven, overwhelmingly, by healthcare’s hyperinflation as was pointed out in Healthcare Drives Middle Class Economic Depression & Trump/Sanders Campaign Success.

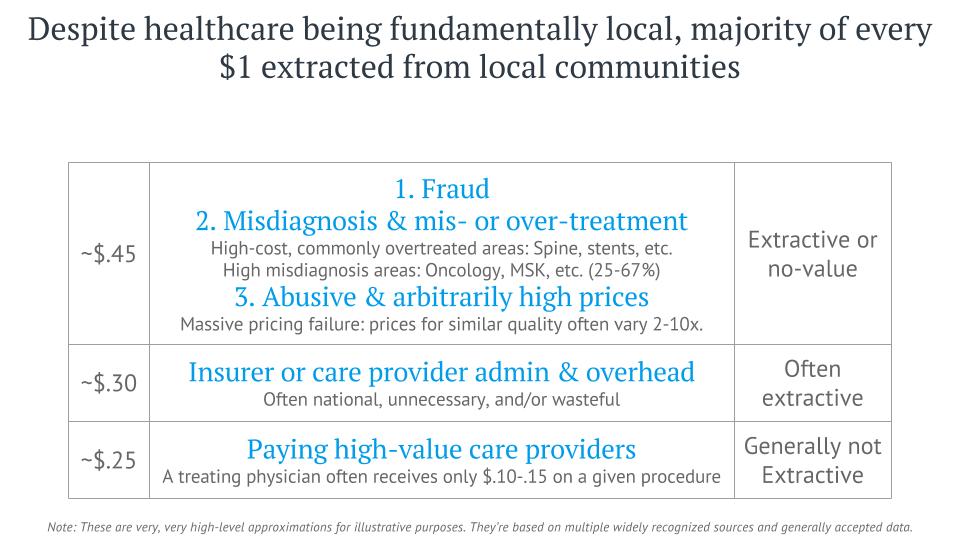

In the follow-on piece, I’ll outline how the ABC health initiative has the potential to have as big an impact on U.S. healthcare as the Affordable Care Act. I leave you with a quote and a slide from a presentation I gave recently that will give a preview of the opportunities available for this new initiative. Note how little of every dollar goes to the value creators in healthcare.

In all of the case studies in my book, the employers treated their employees like adults and explained what was going on at a macro (see the "bigger bite" graph) and micro level to explain how they wanted to ensure their teams could achieve the American Dream. Successful employers point out that healthcare is blocking the American Dream for 60% of the workforce. The math simply doesn’t work: 60% of the workforce makes less than $20 per hour, and the average family of four premiums are $26,000; in addition, greater than 50% of households have less than $1,000 in savings (largely due to healthcare costs), and more than 50% of the workforce has over a $1,000 deductible.

See also: Whiff of Market-Based Healthcare Change?

It’s no wonder that Buffett called healthcare the tapeworm on the U.S. economy. The handwriting was on the wall following the Michigan primary that showed that populism was being driven, overwhelmingly, by healthcare’s hyperinflation as was pointed out in Healthcare Drives Middle Class Economic Depression & Trump/Sanders Campaign Success.

In the follow-on piece, I’ll outline how the ABC health initiative has the potential to have as big an impact on U.S. healthcare as the Affordable Care Act. I leave you with a quote and a slide from a presentation I gave recently that will give a preview of the opportunities available for this new initiative. Note how little of every dollar goes to the value creators in healthcare.

Note: I reference my book, which can be found on Amazon or downloaded for free.

See also: Open Letter to Bezos, Buffett and Dimon

10 reasons past efforts have led to failure:

- No focus on healthcare industry business practices: As my business partner, a securities attorney with various securities licenses, often points out: Practices that are standard in healthcare would land him in jail in financial services. The staggering level of conflicts of interest and lack of disclosure is why the Health Rosetta community crowd-sourced the Plan Sponsor Bill of Rights (“plan sponsor” is a fancy term for employer/healthcare purchaser), Benefits Advisor Code of Conduct and Benefits Advisor Disclosure Form to establish new industry norms. Past efforts didn't seek to change industry norms. As long as these practices persist, there will be little change.

- No sustained CEO-level champion: This translates into a lack of organizational backbone. One analysis of a past failed employer-led effort said, “The lack of available data has long prevented employers from figuring out where their biggest expenditures were coming from.” There is no freaking way Amazon CEO Jeff Bezos would accept that. It is a common trope for the BUCAs to say that the claims data they process for self-insured employers (roughly two-thirds of the workforce) is proprietary to the BUCA. That’s laughable on its face, but most employers back down despite the absurdity of that claim. Clearly Bezos and Berkshire CEO Warren Buffett have shown they are long-term-oriented for strategic initiatives.

- BUCA fiduciary duty has trumped employer fiduciary duty: As a BUCA executive put it to me, “We (BUCA) are legally required to enable price gouging by hospitals.” I outlined the reasons why in Chapter 3 of my book, What You Don’t Know about the Pressures and Constraints Facing Insurance Executives Costs You Dearly. This dynamic is in direct conflict with employers' fiduciary duty as I outlined in Chapter 19 of my book, where I quoted a Big Four risk management practice leader, “ERISA Fiduciary Risk is the Largest Undisclosed Risk I’ve Seen in my Career.” There are two areas of legal jeopardy that are now snapping CEOs to attention. Chapter 7, Criminal Fraud is Much Bigger Than You Think, is just the tip of the iceberg on ERISA fiduciary risk, but it is so blatant that we’ve heard dozens of cases in the works triggered by the lack of oversight. An additional thread of fiduciary legal front is emerging -- activist shareholders are realizing how straightforward it is to slay the healthcare cost beast and improve earnings. Sadly, for many corporations, the only thing that spurs action is a legal target on their back. There is a simple calculator that translates removal of healthcare waste into market cap impact. Here's one example of something that has already happened: A multinational manufacturer simply implemented one proper musculoskeletal management program by having physical therapists working with employees and workplace ergonomics. This is translating into $2 billion of market cap impact (calculate savings times price-earnings multiple). One of the foremost experts in employer benefits, Brian Klepper, estimates that 2% of the entire U.S. economy is tied up in non-evidence-based, non-value-add musculoskeletal procedures. [See Chapter 12, Centers of Excellence a Golden Opportunity, for more]

- Coalitions co-opted: Too many business coalitions on health are supported by limited funding from employers, so they seek sponsorship from the very players whose business imperative is to redistribute money from employers to the healthcare industry incumbents. The people running these coalitions typically walk on eggshells trying to avoid offending their sponsors, and nothing substantive changes. Some have meaningful revenue streams from incumbents that largely perpetuate the status quo at a slightly better price.

- Threats of business reprisal: I’ve heard of many instances where a BUCA threatens an employer's revenue. BUCAs book lots of hotel rooms, buy lots of computer hardware, etc. Any effort to rein the BUCA in is fought furiously. Often the CEO of the employer isn’t even aware that it has happened. The risk-averse HR/benefits leader simply backs down out of fear there will be internal blowback for jeopardizing revenue, and the dysfunction persists. The message that CEOs implicitly or explicitly send to HR/benefits leaders is, “Keep our people happy and don’t get us sued.” In other words, a guarantee of risk aversion.

- Employer groups keep their “deals” proprietary: Classic short-term thinking. The employer may gain some short-term advantage and can claim a “win,” but the overall market they operate in remains unchanged. It is a key part of BUCAs’ divide-and-conquer strategy. Even a huge employer normally has a small usage share in a given market, so their impact is muted when the BUCA holds their deal terms proprietary rather than establish new market norms available to all employers.

- Lack of rethinking of healthcare payment and delivery: Most so-called innovation in healthcare is the equivalent of trying to optimize oil lamp technology to get better lighting in homes and cities. Or, putting recycling bins in a coal plant and calling it "green energy." The healthcare system has become a Gordian Knot designed by Rube Goldberg built up over the last 100 years. Those of us working on the Health Rosetta blueprint and Health 3.0 vision recognize that it is time for a reset. That approach has allowed smart employers to spend 20% to 40% less per capita with superior benefits and outcomes.

- Primary care ignored: As I pointed out in the open letter mentioned above, you can’t have a functioning healthcare system without proper primary care. Primary care has been brutally undermined. To the extent there has been focus on primary care, it has been to pile some niceties on top of a fundamentally flawed model. As one primary care innovator put it, putting wings on a car doesn’t make it an airplane. Having written the seminal paper (summary, detailed) on direct primary care (DPC) five years ago, I find it striking how few benefits professionals have heard of DPC, let alone adopted it. Value-based primary care couldn't be more different than the drive-by, hamster wheel primary care that has become the dysfunctional norm.

- Lack of supply chain mindset: Most employer-led efforts have not rolled up their sleeves because they are working on the mistaken assumption that healthcare is too complicated to tackle themselves. That is only true if you do not apply the proper resources. As a single company, Caterpillar applied a supply chain mindset (something Amazon has in spades) to their drug spending and fired middlemen who were not adding value. Seemingly every company says employees are their most important asset. Considering that health benefits are typically the second biggest cost after payroll, why wouldn’t a company want to ensure they get the greatest payback by carefully managing their healthcare supply chain? In Chapter 9, You Run a Health Care Business Whether You Like it or Not, I detailed how IBM’s mindset shift had the dual benefit of lower healthcare costs and a high-performance workforce.

- Lack of moral standing: Past employer efforts have not articulated a compelling reason that clearly benefits the best interests of the public and their employees. Rather, past initiatives were easy to perceive as antiseptic corporate blather meant to enhance their bottom line. Thus, it is easy to position the employer as the bad guy. For example, as I pointed out in my open letter to Bezos, Buffett and JP Morgan CEO Jamie Dimon, employers are the key enabler of the opioid crisis. Thus, it can’t be fixed without a major shift by employers (see Chapter 20, The Opioid Crisis: Employers Have the Antidote). Facing the largest public health crisis in 100 years, there is a moral imperative to address this situation. Taking leadership on this issue solves an internal issue (no doubt, ABC employees are afflicted with opioid overuse disorders at the same rate as the general public) while tackling a much broader societal issue.

"Your margin is my opportunity.” - Jeff Bezos