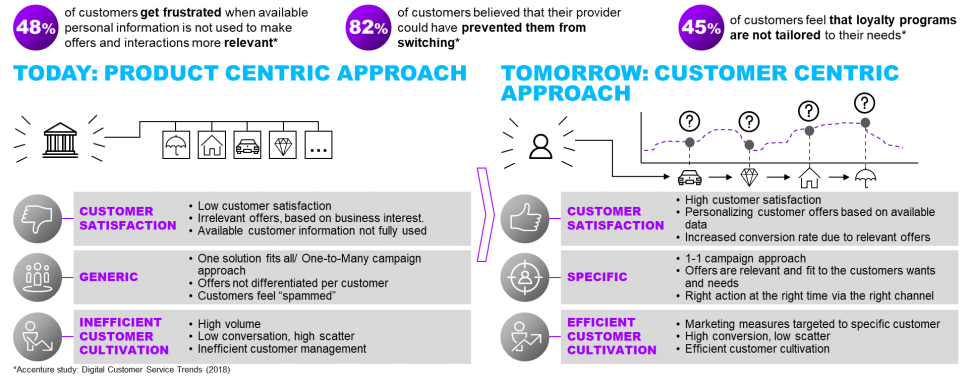

In a rapidly changing industry, some P&C insurers are pulling ahead of their competitors by focusing on customer satisfaction and retention.

“The insurance industry as we know it is at the edge of a new business environment,” says

Michael Costonis , head of Accenture’s global insurance practice. “Breaking away from the pack and capturing new revenue opportunities requires a shift in business mindset – a shift from product-focused to customer-focused.”

Customers want extra benefits, and one way to provide them is to offer value-added services. Travel companies and other insurance branches are already exploring the benefits of value-added services for retaining customers, as

Jamie Biesiada at Travel Weekly points out. Because P&C insurers have been slower to adopt this strategy, however, many opportunities for capitalizing on this strategy remain.

Here, we look at some of the most popular value-added services in P&C insurance, which of these services focus on building loyalty and how to create the right service offerings or packages to encourage your customers to stay with your company in the long term.

Value-Added Services: The State of the Industry

For many years, P&C insurers have struggled with the challenge of selling a product that is substantially similar to their competitors’ products. “Because customers don’t discern much difference between insurers, companies end up competing largely on price,” write Bain & Co. partners

Henrik Naujoks, Harshveer Singh and Darci Darnell . A downward spiral occurs, in which costs and profits are cut and customers jump ship the moment they see the same coverage for a few dollars less.

See also: How to Build Customer Loyalty in Insurance

When insurers compete on price, customers do what

Brandon Carter at Access calls the services shuffle: quitting or threatening to quit their insurance providers to access the same price-lean deals that new customers receive. “My goal is to pay less in a system that actually punishes people for being loyal customers,” Carter explains. Focusing on cost decimates loyalty. Focusing on value can boost it.

Yet insurance companies aren’t making value-added services their first choice when it comes to customer retention

Tom Super, director of the P&C insurance practice at J.D. Power, adds that many P&C insurers are turning to digital tools to court customers, particularly in the auto insurance business.

But digital technology is only a tool. The insurers that will stay ahead of their competitors in the race for customer retention and loyalty are the ones that best leverage that tool to provide the value customers want, says

Mikaela Parrick at Brown & Joseph.

Which Value-Added Services Boost Customer Loyalty?

Value-added services provide an extra benefit that enhances the core product or service. This additional service may be offered at little or no cost for the customer, yet it may make both the customer’s and the insurer’s work easier.

Connecting experience-based services to the product and brand can be a powerful way to encourage loyalty, adds

Roman Martynenko , the founder and global executive vice president at Astound Commerce. While this approach is most commonly seen in retail, P&C insurers can adapt it to their needs. A top-of-the-line mobile app or a personalized starter kit featuring smart tools for each customer’s home can make customers feel like they’re part of a family.

Unique, innovative or specially tailored value-added services can also help encourage loyalty and boost customer interest by becoming a cornerstone of an insurance company’s brand.

Value-added services don’t have to be expensive or complex, suggests

Mike McGee of Investment Insurance Consultants. For instance, a disaster preparation email sent at the start of tornado or hurricane season can help customers take loss-prevention steps, address safety and feel supported by their insurer, at very little cost to the insurance company.

Partnering with other companies can boost loyalty for both organizations while providing value-added services that attract customers, digital transformation executive

Fuad Butt says on the IBM insurance industry blog. For instance, working with telecommunications providers to offer reduced-rate packages can help both companies succeed.

A highly specific partnership that uses existing technology to add value for both customers and companies is the recently announced alliance between Hyundai Motor America and data analytics firm Verisk.

“Hyundai customers will have access to their portable Verisk driving score, which can lead to discount offers on UBI programs and support driver feedback that helps improve their driving,” says

Manish Mehrotra , director of digital business planning and connected operations for Hyundai Motor America. A similar arrangement through an auto insurer can help both insurers and drivers have access to more information to improve safety and make better choices.

Choosing and Implementing Value-Added Services in P&C Insurance

The changing landscape of insurance offers one significant advantage to companies seeking to improve their value-added services: access to data about why customers remain loyal.

“The connections that enable excellent customer experiences aren’t always easy to make,” says

Chris Hall of Pitney-Bowes. Siloing fragments customer information, leaving staff without a complete picture of each customer. This fragmentation makes it difficult to determine which value-added services will actually pique customers’ interest.

If data access is an issue, start by de-siloing information to get a better sense of each customer. Then, find the services that best support your organization’s key differences from your competitors.

Kirk Ford , compliance and T&C manager at RWA Business, suggests first considering how you’d like your clients and customers to perceive your brand in relation to competitors. Balance your differences against your similarities so that customers see they’ll receive all the services they need, but with the value-added extras that make their relationship with this particular insurance company meaningful.

See also: The Future of P&C Distribution

However your insurance organization chooses to add value, resist the urge to announce it to customers merely as being higher-quality. “It doesn’t matter whether or not a company can pull off quality or exceptional service because quality and customer service rarely are differentiating strategies,” adds

Mac McIntire , president of the Innovative Management Group.

Instead,

Ryan Hanley formerly of Agency Nation, now at

Bold Penguin, recommends finding ways your value-added services can improve customer lives. When customers feel a sense of shared values, they’re more likely to stick with their insurance company, rather than risk their luck with a company that may not share those values—even if the prices are lower.

One way to connect with customer values is to change your company’s language surrounding insurance. “If you can sell insurance and not talk about insurance, it’s a win-win,” says

Rusty Sproat , founder of Figo Pet Insurance. He notes that many customers find insurance language obscure and frustrating. That’s why Sproat’s company focuses on providing quality information on pet care and health, switching the conversation to insurance only when necessary to complete a transaction.

Finally, don’t shy away from technology—but use it as a tool rather than a cure-all. Smart home sensors, telemetrics for vehicles and other tech tools are increasingly common in U.S. households, plus they can greatly improve the customer experience, says

Ramaswamy Tanjore at Mindtree. Consider the best ways to manage telemetric or other data, as well as how to position these tools to best showcase their value to loyal customers.

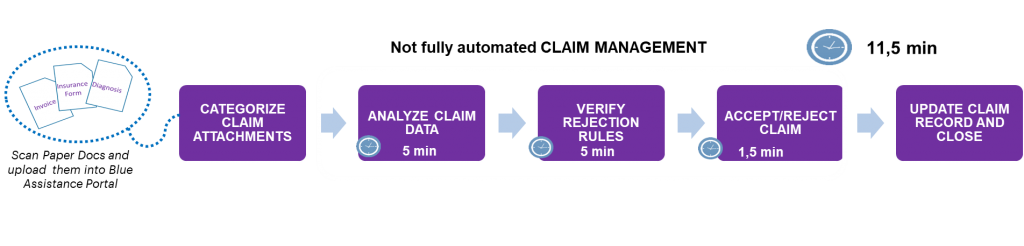

With our machine learning solution in place, a fully automated process was enabled and took only three minutes to do the same amount of work. This represents a 74% reduction in the claims settlement time.

Furthermore, the machine learning technology applied was able to process health claims with 80% accuracy. The other 20% are incorrectly processed owing to spelling errors or database limitations. However, machine learning technologies are able to store and recall those errors for more accurate claims processing in the future.

Case study 2: AI-powered automation of automobile claims processing

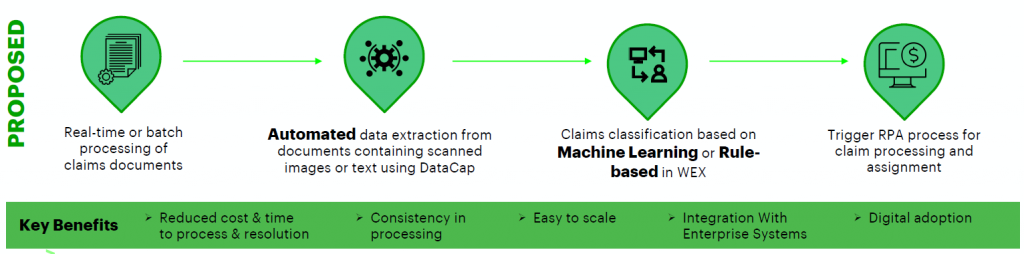

Accenture was recently part of a major client initiative to identify technologies and partner for an AI-driven automation journey. We proposed and built a solution to automate processes to extract and classify data from commercial automobile claims PDF documents.

The client faced many challenges, including having fewer than 400 records to classify 55 unique cases, and these records were mismatched and labeled inconsistently. The client also received scanned images containing text, owing to the redaction process followed to ensure data privacy.

We developed an on-premise solution using a combination of IBM offerings and open-source technologies that enabled a detailed analysis of training data. The solution also helped the client to identify quality and sparse/skew data and to test various approaches to maximize performance.

In the end, a blind data set of 207 claims documents was processed within a four-hour assessment window, and we were able to process claims PDF documents with scanned images as well as text, including several formats and layouts not part of training data.

See also: How to Use AI, Starting With Distribution

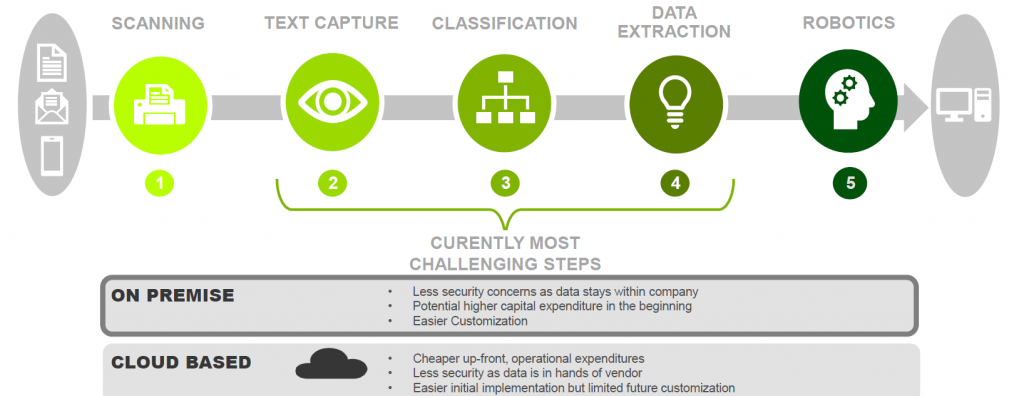

We identified several pain points in the current claims management process:

With our machine learning solution in place, a fully automated process was enabled and took only three minutes to do the same amount of work. This represents a 74% reduction in the claims settlement time.

Furthermore, the machine learning technology applied was able to process health claims with 80% accuracy. The other 20% are incorrectly processed owing to spelling errors or database limitations. However, machine learning technologies are able to store and recall those errors for more accurate claims processing in the future.

Case study 2: AI-powered automation of automobile claims processing

Accenture was recently part of a major client initiative to identify technologies and partner for an AI-driven automation journey. We proposed and built a solution to automate processes to extract and classify data from commercial automobile claims PDF documents.

The client faced many challenges, including having fewer than 400 records to classify 55 unique cases, and these records were mismatched and labeled inconsistently. The client also received scanned images containing text, owing to the redaction process followed to ensure data privacy.

We developed an on-premise solution using a combination of IBM offerings and open-source technologies that enabled a detailed analysis of training data. The solution also helped the client to identify quality and sparse/skew data and to test various approaches to maximize performance.

In the end, a blind data set of 207 claims documents was processed within a four-hour assessment window, and we were able to process claims PDF documents with scanned images as well as text, including several formats and layouts not part of training data.

See also: How to Use AI, Starting With Distribution

We identified several pain points in the current claims management process:

In the next post, I’ll look at how AI-related technology can be used to improve customer services and policy administration. Get in touch to find out how you can use AI in the entire insurance value chain, or download the How to boost your AIQ report.

In the next post, I’ll look at how AI-related technology can be used to improve customer services and policy administration. Get in touch to find out how you can use AI in the entire insurance value chain, or download the How to boost your AIQ report.