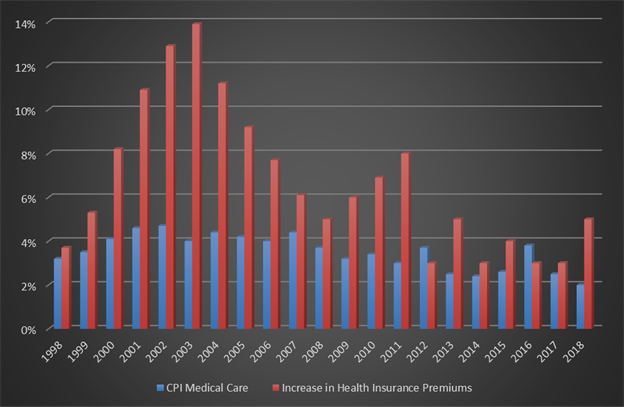

The chart below compares the government's Bureau of Labor Statistics' inflation calculations for Medical Care versus the Kaiser Family Foundation's research into how much insurance premiums have been increasing. The differences between the two calculations are huge. From 1998 - 2018, the government estimates that health costs have increased by only 107%, but for some reason insurance premiums have increased 288%. In fact, 288% is a material understatement, because that figure does not include the huge increases in deductibles.

One might say, "Well, this means the insurance companies are overcharging!" That is a possibility, but if the insurance commissioners of America are that bad at reviewing rate filings, which I doubt, then all the insurance commissioners and their staffs should be replaced ASAP. Another reason I don't think the difference can be accounted for by declaring insurance companies are grossly overcharging is that the ACA to some degree limits their profit margin, and a review of their financials finds profit margins that do not suggest massive overcharging.

Another perspective is that government-sponsored healthcare expenses do not increase nearly as much as the costs covered by insurance companies. Medical care is medical care, unless if under government programs patients get materially less care or the insurance companies subsidize government programs by overcharging everyone that buys their own insurance.

A third alternative is the Bureau of Labor Statistics' numbers are just plain wrong. I trust the Kaiser numbers because they are associated with Kaiser Permanente Insurance, so they know what premiums are being charged. Premiums are easier to verify, too.

In your day-to-day world, what difference does all this make? Maybe none except by adding to your humor or frustrations. Or, perhaps the difference adds to your conspiracy theories. In selling benefits, though, I think seeing the discrepancy helps the intelligent and educated producer sell and advise the educated and intelligent buyer. Understanding the true inflation of medical care will help people make better decisions.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Having spent seven years helping major insurers with digital transformation, I’ve seen the good, the bad and sometimes the downright ugly in practice.

The bad and the ugly include:

Digital "strategies" disconnected from the priorities of the business;

Inconsistent approaches across different parts of the insurer, confusing customers;

Gaps and overlaps in delivery, wasting both opportunities and resources;

Digital approached as a project rather than as a root-and-branch transformation; and

Lots of activity but little practical achievement.

All of these issues, and more, can be avoided by implementing a model for sustainable digital transformation.

I offer you my version of such a model, below.

1. The Customer

Ultimately, all premiums and other revenues flow from the customer, hence placing the customer at the center of the model. Without strong focus on the customer, the digital transformation won’t be sustainable.

For any digital initiative, the insurer therefore needs to ask what the impact will be on the customer and design or re-design accordingly.

That doesn’t mean that the customer should be the only focus. There’s still scope for using digital to reduce costs, increase efficiency and generate new revenue streams - just not at the expense of the customer.

2. Business Strategy

How the insurer seeks to serve the customer will be set out in the business strategy. This should therefore be the starting point for the insurer’s digital transformation.

To be sustainable, any digital strategy has to be rooted in the business strategy. To give but one example, digital claims would look very different in an insurer competing primarily on price than in an insurer competing primarily on personal service.

3. Digital Vision

The digital vision expresses how digital will help deliver the business strategy.

The vision can take many forms, such as narrative statements, depictions of the future state and key re-imagined customer journeys. But much more important than the format is that all key stakeholders must understand, buy into and be able to expound the digital vision.

The digital vision provides the glue for everything that follows.

Once all key stakeholders are aligned behind the vision, the next step is to drill it down to a level of detail that is deliverable. Again, the precise methods and tools for doing so can vary according to the particular needs of the insurer. But in my experience a focus on customer journeys or user stories is almost always a powerful component.

What is critical is to ensure that all key stakeholders, across the insurer, are aligned behind this more detailed digital design as well as the higher-level vision - not least because trade-offs between different functions and business units are likely to be required.

If key stakeholder alignment isn’t achieved at this relatively early stage, the digital transformation is unlikely to be sustainable.

5. Digital Capabilities

Only now should the insurer ask what it needs to put in place to deliver its digital transformation - the digital capabilities required.

These can, and should, be wide-ranging, encompassing culture, people and processes as well as the requirements for new and improved technology.

The digital capabilities provide the bedrock for the digital transformation, and are likely to be fairly stable over time.

6. Road Map

Once the insurer knows What capabilities are required, the next step is to establish the How and the When. How will any required culture changes be made sustainable? Should new people be brought in, or can existing staff be re-trained? For technology capabilities, should the insurer buy on the open market, build unique capabilities in-house or rent from others in the increasingly abundant insurtech ecosystem?

More controversial is likely to be the When. By now, everyone should be excited about the digital transformation and be keen to get on with it. Unfortunately, not everyone can be first - so compromises and trade-offs will again be required. Otherwise, the digital transformation is liable to collapse in acrimony in its early stages - and never deliver in the first place, let alone be sustainable.

This is also the point at which the digital transformation’s relative priority against other strategic initiatives comes into play. Reaching alignment on the trade-offs between digital transformation and other critical programs will be essential to the sustainability of the digital transformation.

7. Delivery

And now the insurer merely(!) needs to deliver to the road map. As with any transformation program, this won’t be simple - but the same sorts of approaches, tools and techniques apply, so I won’t go into that further here.

8. Review

Many digital transformations end with delivery. But that’s a mistake. Because the world moves on, and the digital transformation of an insurer is rarely complete.

To ensure sustainability, it is also critical to implement a process of continuing review - seeking feedback from customers, assessing financial and other outcomes, considering potential improvements and translating what is learned into updated visions, designs, capabilities and road maps as appropriate.

Without this step, both the digital transformation and the insurer itself will stagnate - losing the benefit of all the hard work done to that point.

Surrounding steps two to eight in the model, you’ll see a ring titled "change management."

Having now read through those steps above, you’ll see why.

Multiple times I’ve used terms such as alignment, understanding and buy-in. And no digital transformation program will be sustainable without its key stakeholders acting in harmony to achieve common goals.

Key to sustainability, therefore, is the establishment and use of a high quality change management capability within the digital transformation program.

Finally, no insurer’s digital transformation program is likely to be sustainable without the underpinnings of good governance.

This includes multiple elements, but experience shows that the most important to get right are:

The RACI Matrix for Digital, showing exactly who is responsible and accountable for what, across the insurer’s functions, lines of business and transformation capabilities;

An accompanying target operating model; and

The processes and cadences for managing the digital transformation, at both the strategic (vision, capabilities, design, road map and review) and tactical (continuing program delivery) levels - including financial management.

* * *

None of the above is rocket science, yet to this day few insurers, globally, have implemented a truly sustainable digital transformation.

I hope that, by publishing this simple model, I am providing some help to those who find themselves struggling.

Most insurers won’t, of course, be starting from a blank sheet of paper, so the model will need refining to meet the particular needs of each insurer.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Although I often remind people that ITL isn't a news site, I'm going to make an exception here, because I want to be sure you saw the news about ITL that opens up major opportunities both for the website and for this Six Things newsletter.

And, yes, there is a connection to blockchain. Even if I'm indulging in some news, I still don't believe in clickbait.

The news is that The Institutes has bought the Insurance Thought Leadership brand and publishing assets, including this newsletter. (Press release here.) As a result, I will have access to a slew of thought-leading resources, including a number of publishing properties and events that The Institutes has acquired in recent months and years. Among them: the International Insurance Society, run by my old friend and colleague Mike Morrissey; Risk & Insurance; CLM, which helped launch TI's The Future of Risk conference last year; Claims Pages; and the Pacific Insurance Conference.

I'll also be able to draw on the various repositories and generators of knowledge at The Institutes. That begins with the group that prepares all the educational materials that TI provides as part of the designations it grants but also includes the Insurance Research Council, the Griffith Foundation and the RiskStream Collaborative.

I'm the newest of the newbies, and the integration of ITL with the mother ship is in its early stages, but expect to see thoughts and thinkers from these other TI assets start to show up in what we do at ITL, and perhaps to even see some migration from ITL into these other venues as we all work to improve the state of play in insurance.

Which brings me to blockchain.

While I've seen great potential in the technology for years, I've been waiting to see it move beyond the theoretical and into the market, at least in significant tests. I haven't exactly been surprised as concerns have surfaced, in particular about the speed with which transactions can be processed on a blockchain, a means of keeping encrypted public records that can be updated and accessed by relevant actors and, at least in theory, can't be altered. Such concerns always seem to surface about technologies that promise such fundamental change—one of my favorite lines from Silicon Valley is, "Never confuse a clear view with a short distance."

So, I was intrigued at a planning meeting two weeks ago when the leaders of RiskStream said that, after a long gestation, they are about to take to market a real, live test of blockchain. (Here is a white paper they prepared.) Of the four use cases, the two that struck me as having the most immediate promise relate to first notice of loss and proof of insurance for drivers.

With blockchain, insurers will be able to populate an encrypted public record with up-to-the-moment information on whose auto insurance is current. A decryption key to the record can be provided via an app to anyone with the right to see that information, in particular a police officer or motorist/insurer involved in an accident with the person providing the proof of insurance. Blockchain thus provides a way to tie together insurers' disparate systems in real time, without potentially outdated paper cards, and should reduce the number of motorists who drive without insurance.

For first notice of loss, blockchain will provide a sort of spine to which the various aspects of the claims process can attach. To start, those elements will be the initial information gathering, including the conversations with those involved in an accident to gather their version of what happened. By creating a shared record for the insurers to access via decryption keys and then process via their own systems, RiskStream expects to reduce the number of calls between the companies, which can be numerous and time-consuming. Over time, RiskStream hopes to add elements to the blockchain, including dealings with collision-repair shops.

Don't expect miracles. I certainly don't. But at least blockchain and the market will start to meet each other. I'll be fascinated to see what happens—and I'll let you know what I learn.

Cheers,

Paul Carroll Editor-in-Chief

P.S. I'm sorry to no longer be working on a daily basis with the great cast of characters (and I do mean characters) who did so much to help with the publishing side of ITL before the acquisition by The Institutes. Looking at you, Dave Dias, Wayne Allen, Paul Winston, Guy Fraker and Joe Estes. Many will continue on with the other part of ITL, now known as IE Advisory, which will continue to counsel on innovation best practices, drawing on its database of insurtechs and other companies whose technologies could affect the course of our industry. I wish you guys all the best, and I'm sure we'll all see each other around the campfire.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

Today’s era of total mobility has seen insurance consumers increasingly demanding to receive customer service across a number of different channels – each driving an exponential increase in data volumes. Bombarding systems with queries and operational tasks like never before, this surge in traffic is taking its toll on insurers’ back-end systems. A new architecture, the digital integration hub, is rapidly coming into focus as the ideal solution to ensure that legacy back-end systems are not compromised while enabling U.S. insurers to digitalize their customer and intermediary interactions.

Rewind to just 10 years ago, and insurance providers in the U.S. comfortably relied on the telephone and e-mail. Since then, the pace of technological development has spelled out an ever-increasing number of touchpoints, creating pressure from consumers and intermediaries to deliver a better, faster, more intuitive user experience. In 2019, 23% of insurance executives said enhanced customer experience was their primary indicator of marketing success to support their acquisition and retention efforts (66%) and to increase personalization (60%). Customers expect that information should forever be at their fingertips, through an app or an instant messaging (IM) service. Modern consumers expect a seamless customer experience in which one conversation can be carried out, successively and simultaneously, across various platforms.

Intermediaries, brokers and direct insurers as well as a growing number of third parties are increasingly responding by striving to provide their consumers with information, modeling and fast processing of claims across different devices and channels. As a result, frequency and volume of system interactions across multiple channels are surging. More than ever, systems are being interrogated through a huge range of operations.

Risk arises because the data required to fulfill these queries is stored in back-end systems that also contain business-critical information such as customer data. These back-ends must be kept safe from third-party access – and third-party activity must not interfere with line-of-business systems by provoking unpredictable peaks in queries. Although new front ends have been designed to be remain independent from back-end legacy systems, the front ends often put pressure on the legacy systems, occupying machine time on low-value activity rather than core operations.

New technologies and automation also pose great risk to existing infrastructures. For instance, new front-end development technologies such as single-page-web-application, html5, css3, angular, react and progressive eb apps (PWA) struggle to operate at the required speed and highlight the limitations of legacy systems. Additional data sources, from distributed ledger technology, big data, IoT, cloud computing, AI or biometric technology heighten the issue of handling growing data volumes.

So how can insurers leverage the powerful potential of application programming interfaces (APIs) without placing their back-end systems in jeopardy?

A new architecture centered on digital integration hubs has distinguished itself as a more efficient system and a means to overcome this challenge. In this new architecture, APIs read data extracted from a "data lake," which is perpetually updated in near-real time by the legacy systems rather calling data up from legacy systems directly. The opportunities to feed data into the data lake from other sources such as IoT is endless and presents a game changer for the industry.

When gathering data from legacy systems, traditional data management platforms tended to be based on a batch approach, which updated data in the data warehouse (DWH) on a daily basis rather than in the near-real time way offered by digital integration hubs and require hundreds of extraction and ETL procedures. While traditional DWHs can be useful for analytics and reporting, their more infrequent pulling of legacy data makes them unsuitable for customer-facing front ends. Reducing the complexity of the API service layers, digital integration hubs allow for historical and new real-time data to be fused into a single repository that APIs, rather than the back end, can interact with. During peak activity, the digital integration hub can handle the load and leave back-end systems unaffected.

Other advantages that come with digital integration hubs include their provision of 24/7 real-time data and intuitive Google-like search functions. Brokers can seamlessly access data through dashboards or "cockpits" that allow them to manage customer profiles based on a 360° view. Through system integration, flexible end-to-end solutions can help insurers to embark on their journey toward digitalization and meet customer expectations without putting their systems at risk. Insurers should embrace the opportunity to introduce a digital integration hub and connect legacy back-end system integration with new technology and data-sources.

Today, there are some vendors on the market that can provide one or two of the elements composing the solution, but end-to-end solutions offering all of the above benefits are much less common. Paying attention to the specific needs of the client, experienced consultants can be helpful in selecting and combining different options to fully realize the benefits offered by digitalization.

To find out more, download the latest whitepaper from Fincons Group here.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Giuliano Altamura is global financial services business unit general manager at Fincons Group, where he analyzes business activities that he has seen accelerated in the insurance sector and suggests solutions to help insurers are able to ride the digital wave.

Insurance systems need to talk to each other. They must be able to store, share, retrieve and use the same data. Data should flow unimpeded from the first collection of information, from a prospect or census, through underwriting to policy administration to claims. Failure to integrate data adds cost and complexity and introduces errors. These errors can slow everything down, potentially leading to loss of business in an increasingly competitive environment for employee and voluntary benefits.

Integration with many other systems is a must. Insurers often have a variety of best-of-breed systems: sales/underwriting, CRM, policy administration, claims, enrollment systems, risk and lead scores and self-built software. No one wants to re-enter data. Everyone requires an automated streamlined solution.

Systems today often still can’t use the same data for a variety of reasons.

Legacy systems for employee benefits may still be great workhorses, but they are less flexible. It takes extra work to get them to communicate with other systems. Insurers that have gone through a merger may have two sets of systems and often find their systems are incompatible. This means data must be re-entered multiple times.

Even if carriers decide to implement their own integration, the dynamic nature of the group insurance market can quickly make a recent system integration obsolete. For example, carriers may be forced to consider a new insurance product or to retrofit old ones to meet the market demands. Usually, such changes will trigger a cascade of updates for many, or sometimes all, integrated endpoints. Micro-services can alleviate this kind of problem. Breaking down software into smaller components can lead to better modularity, which in turn may reduce the implementation effort because smaller portions of the system have to be changed.

Sometimes even micro-services are not enough – many carriers have implemented complicated data pipelines with complex business logic. Changing or updating a single stage in this pipeline can thus have dramatic consequences on any downstream endpoint.

This is where an exchanger platform can be really helpful: Instead of software updates and changes in micro-service application programming interface (API), exchanger software lets carriers easily change or update the data structure that flows through the pipeline.

Exchanger software must be designed with compatibility in mind: both backward compatibility (compatible with data structures produced by any older version) as well as external compatibility.

Managing data flow is a growing priority for both IT and business users. And each of those groups of users has specific requirements and constraints. IT users are focused on data formats, data security and system performance, while business users are more focused on business rules and data validation.

Each of these aspects must be configurable in the exchanger platform. One particular characteristic of integration systems for group insurance systems is the size of data that often flows between endpoints. For very large groups with a complex insurance product structure, the amount of exchanged data is very large. For this reason, the exchanger software can operate in both synchronous and asynchronous mode with built-in protection against system overload. Data flowing through the transformation pipe can be formatted in either XML or JSON and can be restricted to certain users, based on their authorization level.

The exchanger platform offers a powerful tool to build more specialized applications that fit more specific needs. Many carriers are now embracing cloud solutions like Salesforce or Amazon Web Services (AWS). Although in the long run this reduces IT operating costs, it still requires integrations with existing systems that are not yet deployed in cloud-like policy administration, claims, payroll and archive.

For all these endpoints, insurance carriers should now be able to use one of the many connectors built on top of the exchanger platform. Connectors are specialized applications ready to be deployed and integrated with a specific endpoint. For example, the Salesforce connector allows bi-directional communications with Salesforce cloud applications. Salesforce users can leverage a Salesforce connector to initiate "ratable quotes" and receive final rates whenever these are made available by the carrier rating system.

Data-exchange standards should encompass data aggregation, format and translation and frequency of delivery.

Without standards, chaos can develop, and costs can ratchet up. Unfortunately, data-exchange standards have not become universal. Industry groups such as LIMRA, CLIEDIS and ACORD are trying.

One encouraging sign of progress: In 2019, LIMRA launched the prototype of the LIMRA Workplace Benefits Electronic Data Exchange Standards. This is something we look forward to seeing develop as we enter the next decade.

Cristian Marcov is technical architect at Global IQX, a leading software provider of web-based sales and service solutions to employee benefits insurers.

Recent developments in robotics and artificial intelligence have changed the playing field for automated technologies. (Here is an earlier blog on the topic.) Historically, automation was beyond the reach of small and medium-sized companies. Robotics were costly, required highly sophisticated programming expertise, took months to integrate and could only perform single, discrete tasks.

In 2012, the advent of artificial intelligence (AI) was a game changer. AI brought collaborative robots to the market -- robots that see and feel like humans, learn (including integrating new data sets and information) and perform multiple tasks. These collaborative robots are also more cost-effective and easier to integrate, making them available and attractive to small and medium-sized businesses.

AI and robotics are now transforming many traditional labor-intensive industries, such as farming, construction, factories and fast food. While Amazon continues to be a global leader in leveraging AI and smart robots, there are plenty of examples of smaller businesses across the country embracing these new automated technologies.

Agricultural farms are using automated tractors and drones to help with growing their crops. Construction firms are purchasing automated brick-laying machines (to lay 3,500 bricks per day). Restaurant owners are investing in new automated machines that can store, prep and cook fast food in a highly controlled environment without any human intervention.

If the adoption of these new automated machines continues, there will be fewer jobs and payrolls in these industries. Over time, the job and payroll loss will affect insurance carriers that specialize in writing workers compensation insurance for these industries.

Historically, technology’s disruption was limited to blue-collar workers; however, AI technology now has its sights set on white-collar workers, including insurance underwriters, claims executives and legal professionals. The insurance industry, which has not been easy to disrupt, is primed for transformations due to developments in AI and automation.

Two years ago, Cambridge University predicted that insurance underwriters were vulnerable to automation. Since that time, we have seen a greater demand among U.S. carriers to invest in new AI technologies that allow them to automate the underwriting and settlement of claims for small commercial insureds. Given the shortage of new talent available to fill expected insurance and claims executives retirements, coupled with new AI technologies, we expect this trend to accelerate.

Developments in AI and automation are already changing the U.S. legal profession, one of the most regulated and specialized professions in the U.S. -- McKinsey estimates that 22% of lawyers' and 35% of paralegal tasks can be automated today. A recent HBO documentary, “The Future of Work,” supports this prediction. It highlighted how LawGeex, a new AI-driven computer software, performed against skilled corporate lawyers on a common task -- analyzing complex legal documents. LawGeex proved its ability to review and interpret the documents, identify potential legal issues and provide substantive advice to a client in half the time -- and with much greater accuracy -- than the corporate lawyer.

While LawGeex and other AI technologies will not displace lawyers in the short term, it will exert pressure on lawyers to shift their time to more highly skilled work - such as negotiating and deal structuring - and away from research, writing and reviewing documents. The result could significantly change law firm practices and economics.

Have you considered how robots, AI and automation will change the workplaces of your insureds - and your own company? Stay tuned for my next blog, “Navigating the Fourth Industrial Revolution,” for ideas on how to navigate AI and developing technologies.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Frank Bria is a senior vice president and treaty account executive for Treaty’s Regional & Specialty Cos., responsible for strategically growing and maintaining Gen Re’s relationships with senior management and executive boards of P/C insurers.

Net Promoter Score has its fair share of critics, but they often overlook one of the metric’s greatest benefits: its ability to define corporate culture.

“Net Promoter Score” sure has its share of detractors these days. But those critiquing the measure are overlooking one of its greatest (if not widely discussed) benefits.

Net Promoter Score (NPS for short) was conceived by Fred Reichheld (a Bain & Co. consultant) and introduced to the world in 2003 via his seminal Harvard Business Review article, “The One Number You Need To Grow.”

NPS was heralded by Reichheld and his colleagues as the quintessential metric for gauging customer loyalty across many industries. It was a simple measure yet demonstrated a strong correlation with repeat purchases and referrals and, consequently, business growth.

In recent years, Net Promoter’s popularity has surged, becoming one of the most widely used customer experience measures, used by small businesses and billion-dollar corporations alike.

The “likelihood to recommend” question that’s at the heart of Net Promoter is a now ubiquitous query in customer surveys, and one with which most all consumers are familiar (even if they’ve never heard of NPS).

Net Promoter’s nomenclature – its “Promoter/Passive/Detractor” shorthand for characterizing customer loyalty levels – has become standard vocabulary in the halls of many organizations, not to mention annual reports and earnings presentations.

With greater adoption, however, has come greater scrutiny of Net Promoter. This was perhaps best illustrated by a decidedly mixed review of the measure in a recent Wall Street Journal article (“The Dubious Management Fad Sweeping Corporate America”).

No performance metric is perfect, Net Promoter included. Many critiques of the measure, however, target weaknesses that relate less to the metric itself and more to how organizations have chosen to (incorrectly) implement it.

[If you’re interested in Net Promoter implementation, read this post for 10 Tips to help ensure success.]

But what gets lost in the maelstrom of Net Promoter critiques is the business philosophy Reichheld has long cited as the inspiration behind the metric: the idea that excellence in business comes from “enriching the lives we touch,” be it customers, colleagues, employees or any other stakeholder.

The structure of the Net Promoter scale, and the methodology used to calculate the NPS score, perfectly reflect that philosophy. The goal is not to satisfy those with whom you interact (“Passives” in Net Promoter nomenclature). The goal is to impress them – to create a “Promoter” by delivering an interaction so intensely positive that it all but guarantees people will want to come back for more (and tell others about the experience).

How exactly does one do that? How does one foster such a positive reaction that cultivates intense loyalty?

You guessed it – by enriching the lives of the people with whom you interact. By shaping every interaction, inside or outside the workplace, so people feel better after they’ve encountered you, as compared with before.

This is the true value of properly implemented Net Promoter programs (and one that so many critics – and even some adopters – of NPS overlook). It’s the behavioral guidance that the measure provides. It’s the picture it paints of what “right” looks like. It’s the motivation it delivers to go the extra mile.

The sheer power of that aspect of Net Promoter became clear to me years ago, thanks to a personal lesson delivered by none other than Fred Reichheld himself.

It was 2008, and I was preparing to launch what would become Watermark Consulting, the customer experience (CX) advisory firm I lead today. In an effort to better understand the market for CX consulting services (and whether there was a place for a new entrant), I did what any good entrepreneur does – I networked. I reached out to key people in the industry, seeking their advice and counsel, hoping to learn from those who had tread the path before me.

Most of the people I reached out to never responded (giving me a master class in e-Snubbing). Among the few who did reply was the most renowned luminary whom I had the audacity to contact: Fred Reichheld.

I had divined Reichheld’s Bain & Co. e-mail address, as any good sleuth would, and within 24 hours of my sending him a message, up came his response in my in-box. He hadn’t delegated the reply to someone else; it was clear he had personally written it. He appreciated my inquiry and wrote a couple of paragraphs with suggestions for me – advice that was genuinely helpful.

Here was this celebrity in the study of customer loyalty, a man famous around the world for his thought leadership, and yet he took the time to personally and thoughtfully respond to a message from me – a nobody.

Why on earth would he choose to do that (especially considering I was shunned by so many CX experts who were far less eminent than Reichheld)? It’s because he was walking the Net Promoter talk, trying to enrich the lives of everyone with whom he interacted.

From that day on, I became a “Promoter” of Fred Reichheld – a raving fan, if you will. I’ve never met the man, I’ve never communicated with him since. But what stands out in my memory is the simple kindness that he demonstrated in responding to my inquiry and sharing some helpful advice. The interaction was, in a word, enriching.

As Reichheld, the father of NPS, demonstrated so convincingly to me, this is the true value of Net Promoter, and it’s something that gets overshadowed by the endless debates over the accuracy, relevance and predictive power of the measure.

Net Promoter is about orienting an entire organization (and individual behaviors) around the noblest of purposes: to enrich the lives of the people around you.

Who can possibly find fault with that?

You can find this article originally published here.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Jon Picoult is the founder of Watermark Consulting, a customer experience advisory firm specializing in the financial services industry. Picoult has worked with thousands of executives, helping some of the world's foremost brands capitalize on the power of loyalty -- both in the marketplace and in the workplace.

The most essential things are not always the essentials people have or know they need to buy.

Life insurance is one such thing not enough people have, given that the lives and livelihoods of many depend on the security that insurers can provide.

To provide for the survivors, to care for a man’s widow and his orphan, is not an act of charity but a declaration of independence; that the living will have the liberty to protect themselves from poverty; that they will have the means to live without fear of eviction or exile; that they will have the freedom to pursue happiness.

To make these promises a reality—to ensure that people have all the insurance they need—requires insurers to better express the urgency of financial safety.

“Insurers need to remind people about the safety life insurance offers. Whether they issue reminders for the second or third time, or for the first time in a long time, what they tell people must be clear and compelling. Anything short of that standard is a loss for everyone.”

As a scientist, I can speak to Albanese’s point about clarity of communication. I do speak to his point, in my own way, whenever I speak to nonscientists about biology or chemistry; which is to say I speak to persuade, I speak to inform, too, so I can get people to join my efforts or support my work.

Before they send a reminder to current or potential clients, insurers need to remind themselves of the importance of clarity of speech.

If people do not know why they need life insurance, if they do not comprehend the value of comprehensive coverage, if they do not know what they should know, then insurers have a duty to explain themselves.

Insurers have a duty to educate us about life insurance. That duty starts with a campaign that has a clear message and a consistent theme, so there is no confusion among those who see or hear the message, so the right people—those who need life insurance—get the point and spread the word, so people may buy all the life insurance they need.

This campaign must include traditional media and social media, because people receive messages through multiple outlets. We send and receive messages by email, voicemail, text, video and chat.

The conversations we have, the news we share, the comments we post and the posts we publish—all of these things have the power to influence how we act.

If life insurance is to be a topic of conversation, if we are to talk about this subject among our friends and family, if we are to do more than talk, then insurers must campaign to earn our trust.

Transparency is a good way to earn that trust.

Free of ambiguity and devoid of the slightest uncertainty, insurers can improve the world by proving to consumers that life insurance is a necessity.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

The past decade’s low growth rates, lack of trust in institutions and declining policy sales are forcing insurers to redefine their value propositions to stay relevant for new generations of consumers. Optimizing costs while investing in the right technologies and talent are also top agenda items. The willingness to take bold action will separate the leaders from the laggards. It will also enable some insurers to convert significant opportunity today into significant value tomorrow.

The unique mix of risk and opportunity is at the heart of the annual EY US and Americas Insurance Outlook. The report represents EY’s perspectives on the issues shaping the US and Americas insurance industry in the near term (next 3-5 years).

A complex environment and challenging fundamentals

The insurance industry is still feeling the effects of a low-growth decade. Economic inequality coupled with lack of trust in institutions is driving more lawsuits, larger jury awards and broader definitions of corporate negligence. For insurers, that translates to more claims, higher loss ratios and the need to raise premiums. It’s not surprising, then, that the number of policies sold has fallen.

Rising expectations for better customer experiences

Consumers expect intuitive, personalized experiences. But many insurers are still playing catch-up compared with digital leaders. Innovative firms will develop full customer lifecycle journeys by incorporating better data and richer insights and applying lessons learned from the most successful tech companies.

Shifting demographics

Though populations are not changing in the Americas as dramatically as in other parts of the globe, insurers are still susceptible to large-scale socioeconomic change. Mass retirements are looming. And insurers can’t take for granted that younger generations will automatically purchase conventional insurance products – particularly as they delay traditional milestones like marriage and home ownership.

Low interest rates remain a big challenge, especially for life insurers. Flat productivity, low inflation and low savings propensity are also dragging down the industry’s prospects. New value propositions, such as those related to financial wellness, and a shift toward fee-based products are two ways insurers should respond.

A looming recession

The current fear of recession and lack of overall macroeconomic confidence threaten the recent run of successful results. A slowdown will affect life insurers as ROI dries up and consumer saving falls. Non-life insurers will be hit as government and private spending drops, affecting trade, consumption and overall economic activity.

Scarce talent

Both life and non-life insurers need more “digital people” – that is, those who know how to use advanced technology. Forward-looking executives recognize that the right talent and skills are necessary to generate strong returns on investments in technology and transformation.

Insurers have understandably focused on upgrading technology in response to continuing margin pressures. But, technology is just one variable in the equation for successful long-term change.

A more holistic approach incorporates talent and cultural factors, as well as the emphasis on product innovation and new business models. Tomorrow’s market leaders will be technology-enabled, data-driven and operationally efficient – but also people-powered and purpose-led, with strong cultures that are adaptive, engaged and capable of rapid change.

AI-based technologies reached a new level of adoption in 2019 as businesses learned more about what exactly AI could do for them. 2020 promises to be even more exciting, with AI systems continuing to mature and companies extending usage and applications to address highly specialized needs. In the year ahead, organizations will be empowered to allocate resources even more wisely while achieving greater efficiency.

Here are my top predictions for AI in 2020:

AI Adopted More as an Assistant Than a Replacement

There has been some cross-industry concern that, as AI continues to improve, its resulting applications will take over human jobs and displace workers. Certainly, AI is being leveraged in new and interesting ways, but, rather than replace the human workforce with machines, AI-based technologies instead will become humans’ assistant.

AI and machine learning can analyze thousands of data points in seconds to yield insights that humans never could achieve alone. These insights will be used to make human decision-making easier and alleviate workers’ most mundane, time-consuming tasks so that they can concentrate on higher-order problems that don’t fit neatly into algorithms. Look for AI-based technologies to be applied strategically this year to help employees become more efficient and valuable in their roles.

Transfer Learning Becomes More Prevalent

Transfer learning, in which machine learning algorithms improve based on exposure to other algorithms, will become a more widely used technique in 2020. To date, it has been leveraged primarily with image processing, but we will see transfer learning applied to areas like text mining continue to improve.

The benefit of transfer learning is that a wider range of industries will be able to use AI to create highly specific applications based on small data. As less data is required, organizations can create state-of-the-art solutions that are faster, more accurate and better tailored to their specific needs.

The Cloud of the Black Box Continues to Lift

For a long time, AI has suffered from a lack of transparency. With machines developing more self-learning capabilities, developers might not know exactly why a machine learning system arrived at certain conclusions. When processes are hidden, behaviors can give pause to users who wonder if they should trust data generated by such a system. To combat this problem, more interpretable models are coming to the forefront.

In 2020, the differences between data explainability, traceability and determinism will become realized in AI. What is needed at which circumstances will also be clarified. As computing elements make complex predictions more understandable, solutions can be created that help explain those predictions. By removing the mystery of the black box, organizations can refine or expand queries to deliver more valuable information.

Traditionally, machine learning models have not been straightforward to deploy for data scientists and engineers. This will change this year as AI is delivered more like a service. AI models will be executed in cheaper, easier ways in the cloud.

This is a significant development on multiple fronts. By shifting to serverless deployment in the cloud, a machine learning model does not consume the same amount of computing resources as on a server. This results in a much different level of efficiency. This in and of itself will make AI as a service more popular. Moving AI to the cloud also improves the delivery model. Instead of coming in the form of a very heavy solution, an API can be created and shared.

These are just some ideas of where AI could go soon. AI and machine learning are advancing at a rapid pace, and companies are both eager and nervous to pull the trigger on new solutions. But the current momentum behind AI will continue to drive innovation, and organizations will evolve as they reap the benefits of machine learning systems.

Ji Li, Ph.D., data science director at Clara Analytics, has leadership responsibility for organizing and directing the Clara data science team in building optimized machine learning solutions, creating artificial intelligence applications and driving innovation.