When workers’ compensation was conceived over 100 years ago, it was designed to cover traumatic injuries in an industrial setting. As workers’ compensation evolved, that coverage expanded in many ways. It was recognized that there were certain diseases or conditions, like asbestosis and black lung disease, to which workers in certain occupations were exposed, and to which the general public was not similarly exposed. The cause of these occupational diseases was not a sudden traumatic exposure but instead resulted from exposure over time, and it often took several years before the disease manifested itself. The traditional workers’ compensation system was not set up for such conditions, so most states eventually passed occupational disease statutes as part of their workers’ compensation laws.

Infectious diseases were never considered occupational diseases. Still, most states will cover infectious diseases under workers’ compensation if the worker can show all of the following:

They contracted the disease.

They were exposed to the disease in the workplace.

Their risk of catching the disease at work is greater than the general public.

All of this leads us to the events of the last year with the COVID-19 pandemic. Although thousands of workers’ compensation claims were paid under the existing standard, several states passed presumption laws, assuming that workers in certain occupations contracted COVID-19 in the workplace. These presumptions changed the burden of proof for covered employees so that workers no longer had to prove they had a greater risk of catching the disease than the general public.

A troubling legislative trend is emerging in 2021, which takes this one step further. Several states are considering legislation or regulatory action that will classify COVID-19 as an occupational disease under their statutes. This consideration is alarming for many reasons.

First and foremost, COVID-19 is NOT an occupational disease. Millions of people worldwide contracted the disease, most of whom did not catch it in the workplace. An occupational disease, by definition, is particular to the risks of the occupation. That is not the case with COVID-19. Will this open the door for future infectious diseases to be covered under workers’ compensation? The flu of 1918 never went away; it lives on in a mutated form, necessitating annual vaccinations. The COVID-19 virus will likely undergo similar mutations, which could also necessitate annual vaccinations. Will all respiratory viruses be considered an occupational disease in the future?

Additionally, by making COVID-19 a named occupational disease, are policymakers not creating a de facto presumption that all COVID-19 is work-related? Policymakers seem to be using workers’ compensation to cover some of the pandemic costs, but workers’ compensation is not health insurance. There is no way for employers to run loss control against a global pandemic. There is no way for underwriters to assess the risks of a worldwide pandemic accurately.

If we continue to blur the lines between workers’ compensation and group health, where does this lead? Cancer and heart disease are already considered occupational diseases for specific occupations in certain states, as are hernias and bloodborne diseases. If workers’ compensation becomes responsible for common conditions that affect millions of people every year, it is no longer meeting its designed purpose. It is no longer a grand bargain for employers when they are being forced to pay claims under workers’ compensation that should be the healthcare system’s responsibility.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Mark Walls is the vice president, client engagement, at Safety National.

He is also the founder of the Work Comp Analysis Group on LinkedIn, which is the largest discussion community dedicated to workers' compensation issues.

On March 12, 1928, William Mulholland, Harvey Van Norman and Tony Harnischfeger hiked down the dry side of the newly filled St. Francis Dam in California, inspecting worrisome leaks. Mullholland was the mastermind behind Los Angeles’ new aqueduct — a 233-mile series of man-made rivers and reservoirs that would eventually bring much-needed water to the San Fernando Valley. Before he left that day, Mulholland reassured Harnischfeger that, even though the leaks needed to be fixed, they didn’t represent a serious structural danger. That evening, the dam gave way, and 400 people living below the dam, including Tony Harnischfeger, were washed down the valley. It was a tragedy that could have been avoided.

We still have preventable tragedies, such as breadth of the pandemic and the Beirut explosion, but we also have advanced science that can give us quick vaccines, improvements in cyber security, fewer auto accidents through safer vehicles and greater access to relevant data from health and wellness to weather and water leaks.

Those of us in insurance technology know how knowledge can help us take advantage of opportunities and avoid risks. At Majesco, to help us look ahead, we gather insurer viewpoints and assess strategic priorities. This year’s survey report, Strategic Priories 2021: The Insurance Industry Shift Hits Hyper-Acceleration for Digital Business Models, the first of two reports, is especially crucial to an understanding of priority shifts: how COVID-19 affected insurer priorities and how those who are accelerating key strategies are leaping forward.

In today’s blog, we’ll see that the COVID pandemic is not the only challenge insurers face. We’ll take a close look at what concerns insurers today.

Internal Challenges — Insurance Execs Share Their Views

Majesco surveyed insurance executives regarding these internal challenges:

Digital capabilities

Data security

Innovation

Legacy systems

Budget

Aligning IT and business strategies

Data and analytics capabilities

Talent (retention, availability)

Change management

Aging workforce/retirements

Post-COVID work environment

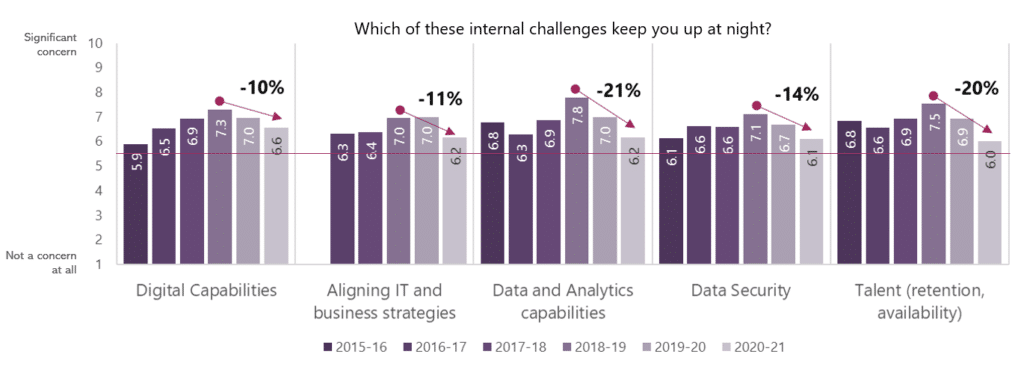

Of the 11 internal challenges in the survey, five show indications of becoming more the “norm” of doing business (Figure 1): Digital capabilities, Aligning IT and business strategies, Data and analytics capabilities, Data security and Talent (availability, retention). These challenges showed steady increases in concern over time but peaked in 2018-19 and have trended lower over the past two years. This trend likely suggests that companies have adapted to these norms through improved capabilities, adjusting expectations or increased confidence via the benefit of experience gained.

However, the question remains … Do these perceptions match reality? A few examples:

Many insurers embraced portals, but most of these do not deliver a next-gen, holistic digital experience that customers, employees and distribution partners want and expect and that is part of a digital maturity that is needed.

Insurers have made progress getting their internal data sources in order but still struggle to realize the benefits of a fully integrated data environment consisting of internal and new external structured and unstructured sources, with AI/ML-generated insights.

Given increasingly severe data breaches, data security may be more of an illusion than reality for many critical industries like insurance and why the need for cyber insurance is so critical.

The reliance on an aging IT workforce to keep old legacy systems running should shift insurer priorities to rapid legacy transformation, including no code/low code capabilities.

Figure 1: Declining levels of concern about internal challenges

The challenges regarding Budget and Legacy systems remain steady, with above average concern in every survey. Budgets will likely always be a universal source of discomfort, but as companies begin to establish new operating models that have new cost structures and shift IT expenses from capital expenditures to operating expenditures, companies open up the opportunity to reallocate resources to new initiatives.

While many insurers have completed or begun legacy transformation projects, many of these are non-platform modern, on-premise implementations that are the “new legacy” systems and are now being replaced by next-gen, cloud-based digital insurance platforms. This next-gen platform has superior capabilities that meet the needs of today’s and tomorrow's insurance customers, including no code/low code capabilities.

Interestingly, four new internal challenges in this year’s results all garnered lower levels of concern: Innovation and Change management, Digital and Data/Analytics capabilities and IT-Business alignment. Low levels of concern over Aging workforce/retirements and post-COVID work environment align with the downward trend in concern over Talent (availability, retention). These could be blind spots for many companies, which we’ll discuss in a moment.

Talent and Retention — IT Crisis or Minor Business Conundrum?

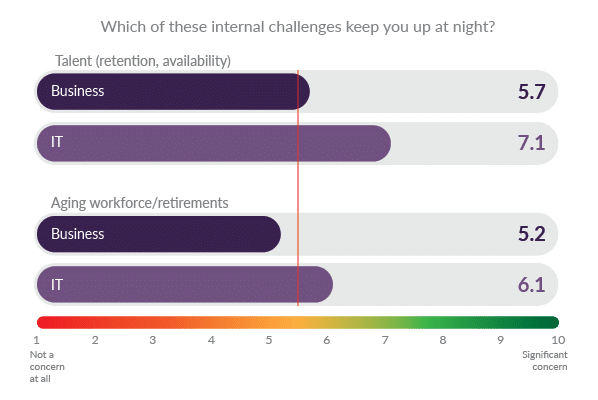

It is not surprising that IT executives are much more concerned about internal talent issues than their business counterparts, as seen in figure 2. Their 25% higher concern about the availability and retention of talent is driven by the fact that they face stiff competition with insurtech and Big Tech for employees with the skills needed to transform to digital-first insurers. Until they can achieve the transformation, however, IT needs to retain as much of its aging workforce as possible to maintain legacy systems and keep the current business running. This lack of alignment is problematic, meaning resources are allocated to business as usual rather than focused on creating the business needed for the future.

Figure 2: Levels of concern over talent issues, IT vs. Business

External Challenges — Insurance Execs Share Their Views

Majesco surveyed insurance executives regarding these external challenges:

Changing customer expectations

Emerging technologies

Regulatory requirements

COVID-19’s impact on target markets

Pace of change

Insurtech

Growing market availability of new/innovative insurance products

New competition from outside the insurance industry

New competition from inside the insurance industry

The rise of direct sales (B2C and B2B)

The rising cost of the agent channel

AM Best innovation score

This year, we see declining concern for several external challenges, including Changing customer expectations, Regulatory requirements, Pace of change and New competition from inside the insurance industry. It appears that insurers are feeling more confident in these areas, either through improved capabilities, adjusted expectations or experience (or a combination of these).

However, as with the internal challenges, is there a risk of being too comfortable, confident and complacent, particularly coming out of COVID? Andreessen Horowitz says that e-commerce increased more in the last six months than in the entire decade beforehand! Add to this the emerging customer experiences from fintech and retailers such as Sofi and Amazon that are creating experiences, rather than transactions. Majesco research indicates that customers are willing to share their data if it leads to more personalized products and pricing that fit their changing lifestyles and risks, like on-demand and embedded insurance.

In addition, concerns have been nearly flat or declined slightly in concern over Emerging technologies, New competition from insurtech, startups, MGAs and New competition from tech giants from outside the insurance industry. This last challenge issue is a concerning blind spot, as experimentation and market entries by players from outside the industry accelerates. Consider a few recent examples:

Intuit launches QuickBooks insurance and 401K services — QuickBooks customers can now protect their businesses with comprehensive insurance coverage and offer their employees a 401(k) benefit, traditionally offered only by large companies. This integration will enable QuickBooks users to seamlessly obtain a customized quote and easily purchase general liability, professional liability and workers' compensation coverage from Next Insurance with a few clicks of a button, directly from their QuickBooks account.

Petco launches insurance — In October, Petco announced the launch of Vital Care, a paid annual plan providing pet parents with a convenient, affordable way to meet their pets' routine wellness needs.

Walmart offers pet insurance and health insurance — In November, Walmart announced it added pet insurance as animal adoptions soar during the pandemic. The company is offering insurance through Petplan and connecting people to pet sitters or dog walkers through Rover. In July 2020, it was announced that Walmart was launching a health insurance arm — dubbed Walmart Insurance Services — to sell plans to consumers. Walmart's low prices and wide footprint could pose a threat to insurance startups — especially those firms breaking into the Medicare Advantage market.

Tesla insurance approved in Texas — In December 2020, the Texas Department of Insurance approved filings for insurance to be underwritten by a third-party Austin-based insurer and distributed by Tesla Insurance Services, which follows the company’s 2019 launch in California. Tesla’s Texas program uses driver behavior-based data collected by the vehicle as an input to determining at-fault collision rates. The program also covers cyber identity fraud expenses, electronic key replacement, loss or damage to the original wall charger and loss when the vehicle is being driven by autopilot.

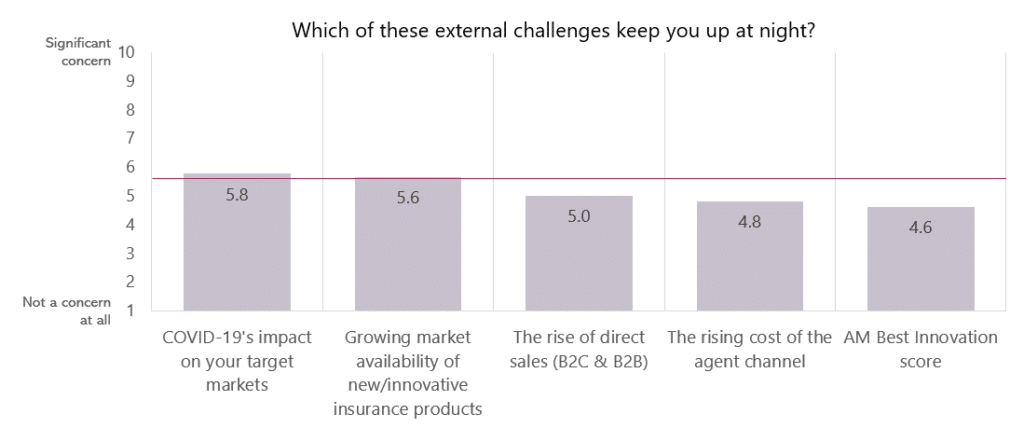

As industry and market trends evolve, so do the topics covered by our annual survey. We added five new external challenges this year. Although these don’t have historical results for trending, COVID’s Impact on Your Target Markets had the fourth-highest overall ranking among all 14 external challenges, reflecting the real uncertainty on the pandemic’s effect on the economic health of consumers and businesses, and the impact for insurance.

Growing market availability of new/innovative insurance products ranked sixth, tied with insurtech, ranking higher than the challenges from new competition from inside and outside the industry, suggesting that incumbent insurers more strongly associate insurtech with these new offerings – again, another potential blind spot on new competition.

The remaining three new issues, rise of direct sales, rising cost of the agent channel and AM Best innovation score, had considerably lower ratings than all other external challenges. (See Figure 3.) Again, are these blind spots, or do insurers have a good handle on these challenges? With e-commerce rising across all industries and demographic shifts in channel preference, we expected higher ratings on these two channel challenges. With the lackluster results of AM Best’s first Innovation Assessment mentioned earlier, it is somewhat surprising that this issue came in dead last.

Figure 3: New external challenges added to the survey

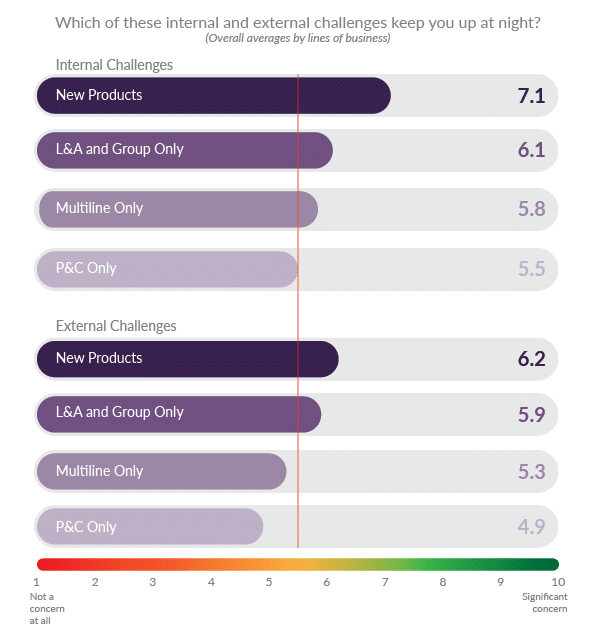

Key Differences Among Segments

Aggregating the ratings across all internal and external challenges highlights some key differences between direct written premium (DWP) tiers and line of business segments. The largest tier is much more concerned about internal challenges overall. This suggests that the complexity of the large organizations leads to a higher number of challenges that can be a hindrance to agility. Smaller companies should have an advantage here with less bureaucracy and complexity – but old systems could also be a hindrance negating this advantage. Replacing these systems with next-gen core platforms should now be of the utmost urgency.

Companies with new products are much more concerned about the internal and external challenges, as highlighted by the aggregated rating comparisons. (See Figure 4.) The L&A/Group Only segment is a close second on five of these. This makes sense when you consider that these companies are challenging the status quo with non-traditional products and blazing trails, which can exacerbate existing challenges (e.g. IT, talent, etc.) as well as bringing up brand new challenges.

Figure 4: Differences in aggregate levels of concern over internal and external challenges by lines of business

How does your opinion rank within these challenges? Can knowledge open your organization up to the opportunities in our midst?

Do you know what you don’t know?

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

Six Things Newsletter | March 23, 2021

In this week's Six Things, Paul Carroll thinks it may be time to start planning for a robust rebound in the U.S. economy. Plus, transforming auto claims appraisals; how to combat the surge in ransomware; analytics that lower spending on claims; and more.

In this week's Six Things, Paul Carroll thinks it may be time to start planning for a robust rebound in the U.S. economy. Plus, transforming auto claims appraisals; how to combat the surge in ransomware; analytics that lower spending on claims; and more.

In the first full week of spring, green shoots are starting to poke through the metaphorical ground in the U.S. economy, as well. It may be time to start planning for a robust rebound late this summer or in the fall, both in terms of what needs to happen as insurance employees increasingly return to the office and in terms of what will happen for clients’ and prospective clients’ businesses... continue reading >

Hear from industry experts as they discuss their approach to growing and expanding customer relationships with an integrated disability and absence management solution.

That was the dictum of the late, great Mel Bergstein, who way back in 1994 founded the pioneering digital strategy firm Diamond Management & Technology Consultants. (It became part of PwC in 2010.) I heard Mel’s line a lot, as a partner with Diamond from 1996 through 2003, and I think his are words to live by in the insurance industry these days.

Everyone seems to have gotten the memo about the need to digitize insurance and to explore innovative ideas, but the present typically creates a real drag that slows movement toward the future.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Airlines are rarely held up as models of customer experience (CX) excellence, but, in one important respect, the aviation industry actually deserves that recognition.

At many airlines, the traveler experience leaves a lot to be desired. People are subjected to a host of annoyances and indignities, from baggage charges to ticket change fees, from cramped seating to overbooking.

But one aspect of the airline customer experience is remarkably good, and consistently getting even better: the industry’s discipline in identifying and addressing the causes of accidents.

Say what you want about the awfulness of air travel, but it does have one undeniably redeeming quality: It’s really safe. While commercial airline accidents obviously garner a lot of media attention, they are extremely rare. Accounting for just 0.006 deaths per billion miles of travel, flying is the safest form of transportation out there, far safer than driving.

We were recently reminded of this, when a United Airlines plane suffered an engine failure moments after departing Denver International Airport. Pieces of the engine rained down on a Denver suburb. Fortunately, no one was hurt on the ground, nor on the plane, which quickly returned to the airport and made an emergency landing.

Within hours of the incident, the National Transportation Safety Board’s (NTSB) “Go Team” was mobilized, and it’s from their tireless work that all businesses can learn a valuable lesson.

Established in 1967, the NTSB is an independent government agency that investigates all civil aviation accidents, as well as major incidents involving other forms of transportation (such as train derailments).

The Go Team is a cornerstone of the NTSB’s investigative process. Ready to travel anywhere in the world at a moment’s notice, the team includes a variety of specialists – in aircraft structure, engines, hydraulic systems, crew performance and even air traffic control. They all descend on the accident site to piece together what happened and to determine what went wrong.

Within a matter of days, the NTSB issues a preliminary report. (An official, final report can take months if not years to publish, depending on the complexity of the incident.)

But here’s the most important part: Based on its investigation, the NTSB releases safety recommendations, which can then be turned into “airworthiness directives” by the Federal Aviation Administration (FAA). Those directives, which can be issued on an emergency basis if necessary, establish legally enforceable rules that can dictate anything from aircraft design changes (which would be handled by the manufacturer) to maintenance procedure enhancements (which would be handled by the airline).

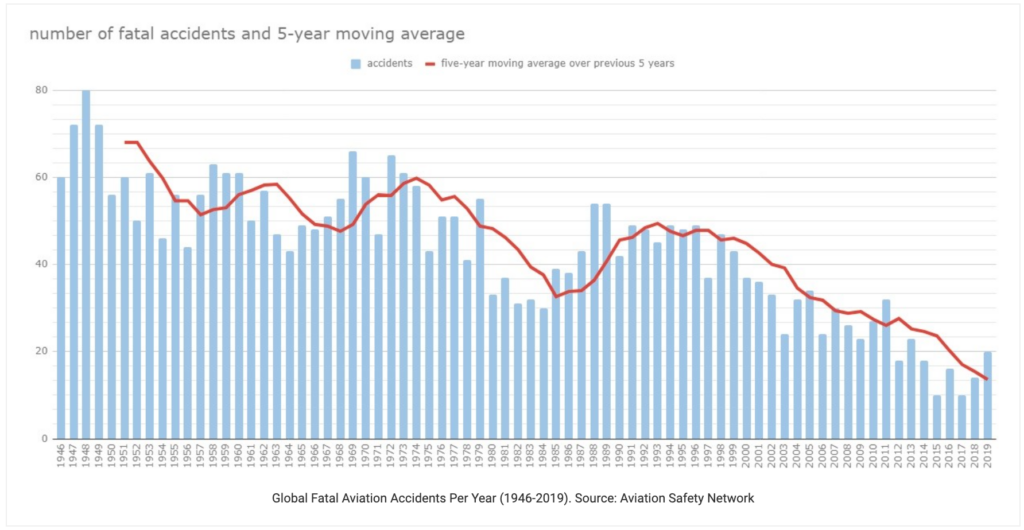

What does that disciplined process of investigating aviation accidents and addressing their root causes yield? Decades of consistent improvement in the civil aviation fatality rate, with the five-year moving average hitting an all-time low in 2019 (despite a marked increase in the number of flights).

Now, imagine if the above graph were charting the failure rate for your company’s customer experience, perhaps measured through product defects, complaints or some other indication of an experience gone wrong.

Because that’s really what the NTSB Go Team (and other countries’ aviation safety agencies) do. They root out the underlying cause of a failure in the experience. Granted, in the case of the NTSB, they’re looking at failures that can be grave, resulting in harm to dozens if not hundreds of passengers. But the value of the NTSB’s approach is applicable to any business, regardless of product or service sold.

Think of it this way: There are a finite number of reasons why an aircraft will suffer an operational failure. By rigorously investigating every failure, and directing aviation partners to pursue remedial action, the NTSB and FAA have gradually narrowed the list of potential failure points. Hence the remarkable and steady long-term decline in accident rates.

The same logic applies to your business. There are a finite number of reasons why your customer experience may fail, from a product design flaw to an outdated website link to an inaccurate instruction sheet. There may be a long list, but it is a finite list.

You would be remiss then, if you didn’t take the opportunity to investigate failures when they occur, pinpoint the root cause and address the underlying issue. Only by doing so can you start to check items off of that finite list and begin removing potential sources of experience failure from your customers’ lives.

To bring the NTSB’s proven approach to your organization, keep three things in mind:

Invest in investigation. When experience failures arise, people’s focus is (rightly) on solving the problem for the affected customer. Once that’s done, though, organizations just move on to the next task – answering the next call, resolving the next complaint, manufacturing the next widget. Resist that temptation. Culturally, people in your organization must understand that an essential part of experience recovery is asking yourself, “How did my customer even end up in this situation?”

Turn insights into action.It doesn’t help anyone if a field sales rep or a call center agent figures out the root cause of a customer experience failure, but then doesn’t have an outlet to communicate that to people who can do something about it. After all, the NTSB’s investigations would be pointless without their safety recommendations and the FAA’s associated airworthiness directives. Make sure there is a clear avenue for your staff to share their findings with those who can drive change, such as a manager or an internal CX improvement team.

Make it about progress, not punishment. Interestingly, conclusions from an NTSB investigation cannot be entered as evidence in a court of law. That is by design: The architects of the NTSB wanted the organization to be viewed as an independent party, focused on preventing future accidents, not facilitating litigation. In the business arena, staff need to be forthcoming to assist with root cause analysis. If they sense that the exercise is punitive, they’ll likely be reluctant to participate in a genuine way. Keep the exercise constructive, with an emphasis on continuous CX improvement.

Every company, even legendary ones, has to occasionally deal with customer experience failures. What separates the good from the great is how the organization approaches the resolution of those issues. Does it fix the problem for just one customer, or does it address the problem for all customers in the future. The NTSB has certainly demonstrated its proficiency in the latter approach, chipping away at root causes and turning air travel into the safest transportation experience on the planet.

So, the next time your organization encounters a customer experience failure, ask yourself, “Who’s on our Go Team?” Whether it’s a responsibility that lies with a dedicated unit, or an accountability that’s embedded in every staff member’s role – ensure this investigative work consistently gets done, because it’s that discipline that will keep your business flying higher.

A version of this article originally appeared on Forbes.com.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Jon Picoult is the founder of Watermark Consulting, a customer experience advisory firm specializing in the financial services industry. Picoult has worked with thousands of executives, helping some of the world's foremost brands capitalize on the power of loyalty -- both in the marketplace and in the workplace.

For those of us in insurance, the journey to digital transformation has felt slow, challenged by regulations, legacy systems and complex business functions that require sophisticated solutions.

The pandemic has been a wakeup call: Digital is no longer an accessory but a necessity for any business. Effective digital technology is essential to meeting our customer needs and providing them with protection, security and peace of mind. We are at a pivotal moment, where we must overcome the barriers to digitization.

No-code technology can play a key role. For decades, enterprises have relied on code to build and maintain software. But coding is extremely complex. It takes a long time to learn and master, and it’s time-consuming to write, update and maintain code. At the enterprise level, a reliance on code creates a system in which a select few who are responsible for building and maintaining software for the entire enterprise. This typically leads to high costs, slow timelines and sub-par outcomes.

We’ve all seen this in action. A team comes up with a software idea or identifies a process that needs updating. The team brings the idea to developers (aka “coders”), who are already underwater with requests. The scope of the project is reduced, then takes 12 to 18 months to get off the ground. If requirements change, funding shifts or people change jobs, the project can fail entirely.

No-code fundamentally changes this. No-code is exactly what it sounds like -- a way to build software without using any code. No-code users build software using a visual interface that houses a library of configurable pre-built components. This approach expands the pool of people who can build software beyond those who can write code and frees developers to focus on truly complex problems. No-code allows companies to build complex, mission-critical applications faster, at a fraction of the cost and with fewer bugs.

No-code is a perfect fit for an industry like insurance, where a reliance on code has held us back from building and scaling the software we need to meet the moment. The potential use cases are vast. We already have great examples of how enterprise no-code is being used.

Digitizing business origination in life insurance

Traditionally, business origination processes have relied on paper processes or solutions built via coding. Multiple points of intake (e.g., paper, e-apps, digital) contribute to data inconsistencies, low adviser productivity and a sub-par customer experience.

A top 10 life insurance company used Unqork's no-code platform to digitize the business acquisition journey from end to end. Through a unified digital interface for advisers, customers and operations, the company streamlined policy administration and underwriting. Turnaround time for new business fell from over two months to less than 20 days on average. The company also reduced costs by 30% and enhanced the customer and adviser experience.

Digitizing onboarding of the plan sponsor and adviser

For most insurers, client onboarding is incredibly time-consuming and costly. High-touch and heavily reliant on pen and paper, traditional processes yield sub-par results and are often rife with data inconsistencies.

No-code can be used to create end-to-end, self-service solutions that automate sponsor, plan, servicing, pricing and adviser and third-party administrator (TPA) data capture. This digitized process allows for direct client outreach, integration with third-party data providers, due diligence assessment and seamless coordination across functions.

A top five insurer used Unqork’s platform to digitize plan sponsor and adviser onboarding, accelerating client onboarding times from four weeks to three hours, decreasing the cost of operations and technology ownership while increasing revenue potential and improving client relationship management.

Streamlining rate-quote-bind and policy administration

The policy administration process is notoriously inefficient. Insurers often rely on a number of different channels -- phone, web, agent, self-service -- and intake varies widely across channels. Agents often depend on the back office to receive an indicated rate and issue a policy, restricting agent productivity and delaying the rate-quote-bind process. Inefficient processes contribute to a significant administrative load and hurt the customer experience.

Enterprise grade no-code can be used to automate the intake, quote, bind and issue processes for no-touch and underwriter workflows. These systems are user-friendly and optimized for mobile, to ensure a positive customer, agent and underwriter experience.

A top insurer developed a policy administration system that allows agents to independently perform submission, quote, bind and issue processes. The paperless system was built in just six months, and the insurer experienced huge efficiency gains: more than 70% in quoting and more than 80% for binding and issuance.

--

We’re just starting to scratch the surface of what no-code can do for insurance. There are endless use cases across the industry -- with digital solutions for common, inefficient processes and bespoke applications for niche challenges. The potential is revolutionary: The industry can provide a better experience for carriers, agents and customers alike.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

In the first full week of spring, green shoots are starting to poke through the metaphorical ground in the U.S. economy, as well. It may be time to start planning for a robust rebound late this summer or in the fall, both in terms of what needs to happen as insurance employees increasingly return to the office and in terms of what will happen for clients' and prospective clients' businesses.

My optimism hinges, in particular, on a survey of chief financial officers that Deloitte released last week. While straws have been in the wind for weeks now as the vaccine rollout has accelerated in the U.S., I was struck that only 13% of CFOs considered the North American economy to be bad in the first quarter, down from 26% in the fourth quarter and 60% in the third. 29% said current conditions are good, up from 18% in the fourth quarter. (Only 7% consider the European economy good; 48% view it as bad, and 1% as very bad.)

We could still take a hit if capital markets reset -- 83% of CFOs consider equity markets overvalued. But 57% said they feel somewhat more optimistic about their company’s financial prospects, and 10% are significantly more optimistic. Only 3% are somewhat or significantly less optimistic.

In terms of when companies will return to normal operations -- whatever "normal" turns out to be -- 37% of CFOs say their company is already at or above its operating level before the pandemic. 16% of CFOs expect to hit that mark in the third quarter, and another 16% predict their companies will get there in the fourth quarter.

The new normal will likely include less travel: 73% expect travel expenses post-pandemic to be between 50% and 80% of where they were before. Just 12% see travel at 81% to 100% of pre-pandemic levels, and only 2% project an increase.

While the CFOs weren't asked about the likely working environment for their companies, in general, they provided some feedback on their function that may be instructive for others. Only 31% expect the majority of their finance staff to work four or more days on site post-pandemic; 45% expect the on-site work week to be three days.

When you step back and look at the implications for the insurance industry, I'd say that most clients, outside of those involved in business travel, will snap back -- as long as a company has managed to stay in business. The hunger is there -- literally -- for meals at restaurants and for other social outings. (The first thing I'm going to do when I get vaccinated is hop on a plane and fly to Pittsburgh to give my nearly 91-year-old mother a hug, having not seen her except on Zoom in 14 months.) Schools will reopen, and, while the lost year in the classroom will cause problems for a long time, the rhythms of life will return for parents with school-age kids.

But I'd guess that the office environment, both for the insurance industry and for clients, will take time to sort out. There were clearly lots of advantages to working from home -- I fill up my car about every six weeks -- but I miss the camaraderie, and academics argue that creativity drops when people and ideas don't bump into each other.

I'd guess that most businesses will more or less follow what the CFOs predicted, that people will come to the office three or four days a week -- perhaps coordinating so that members of a group are likely to see each other -- but will have much more freedom to keep doing those Zoom meetings. Perhaps keep an eye on Microsoft, which said this week that it is starting to call employees back to the office as it rolls out a hybrid model of work in the office and at home. A recent essay in Fortune offers advice on testing hybrid models -- mostly on mistakes to avoid. The author reports that employee time spent on collaboration declined to 27% in 2020 from 43% pre-pandemic and says that trend needs to be reversed for a host of reasons.

In any case, having to sort out a hybrid work environment is a nice problem to have after a year hunkered down. I'm just delighted to be finally feeling optimistic. See you soon, Mom.

Stay safe.

Paul

P.S. I was also struck by an article over the weekend in the Wall Street Journal about how Blackstone has shifted its investment focus from value-based investments to growth companies. If even Blackstone sees more opportunity in growth than in spotting undervalued companies and wringing inefficiencies out of them, that has to be a good sign, right?

I'd actually argue that it's a good sign for the economy but not for Blackstone. If it's switching from a tried-and-true formula that has the firm with more than $600 billion under management, then the firm is running out of opportunities to work its formula. You just don't stop minting money unless you have to.

Expertise in hyper-efficiency and in the sort of sophisticated financial tools that private equity uses don't relate much to success in spotting and nurturing high-growth companies, so I'll bet anybody a nickel that within a couple of years we'll see Blackstone retrench. But I don't have a stake in Blackstone, so I'm simply pleased that it and its hundreds of billions of investment dollars will chase growth and encourage everyone to innovate, at least for now.

P.P.S. Here are the six articles I'd like to highlight from the past week:

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

The pace of digital transformation is accelerating in many industries due to COVID-19, and nowhere is this more evident than in automotive insurance. At the start of the pandemic, carriers and collision repairers had to find new ways to minimize in-person interaction between employees and customers. This resulted in the rapid adoption of virtual, or photo-based, estimating and served as a tipping point for claims automation.

So how does this affect auto insurers? Although the pandemic has reinforced the benefits of virtualization, truly automated estimates — or touchless estimates — remain the ultimate goal. Achieving that goal, however, requires a technological evolution. Despite catalysts including business incentives, customer expectations and a global pandemic, the transition from onsite inspections to full automation will take time.

Common Misperceptions

To understand the progression of claims automation, it’s important to first address misperceptions about the current state of touchless estimates. The belief that, today, fully automated appraisals can be accurately produced without human intervention is fiction. In fact, it’s comparable to recent exaggerated assertions about the prowess of self-driving vehicles. While advancements in technology have led to increased automation, the need for human oversight and intervention remains critical. Additionally, the regulation and infrastructure required to support an automated end-to-end system are still evolving.

The Pursuit of Touchless Estimates

Insurance carriers are on a quest for touchless estimates to stay competitive and meet increasing consumer demands for better response times and self-service capabilities. After all, an automated appraisal process is expected to deliver:

Improved efficiency and appraiser productivity

Greater estimate consistency

Better cycle times over traditional methods

Higher customer satisfaction

For this automated process to be successful, though, insurers must consider their unique workflow requirements. Unlike field estimating — where a one=size-fits-all approach may work — a scalable, automated appraisal solution requires an open, flexible and cloud-based ecosystem that can integrate with other business applications. Open ecosystems let carriers streamline operations and leverage best-in-class technologies that reduce the reliance on human effort while they build out an automated claims experience.

Three trends — or levels of automation — have marked the evolution from onsite inspections to touchless claims. These levels are not sequential; rather, they are being developed and deployed in parallel as the artificial intelligence (AI) used to automate estimates becomes more mature.

Virtual (Photo-Based) Estimating

Virtual estimating demonstrates the power of using photo capture to produce accurate assessments. Images and videos are put at the center of the appraiser’s workflow. Despite its efficiency, virtual estimating is primarily driven by humans, not machines.

Vehicle owners start the claims process on their mobile devices and are guided through how to capture and share photos and video of damage.

AI is leveraged to organize and categorize the imported images as well as to detect and highlight the damaged sections of the vehicle.

Appraisers rely on an application with a 360-degree view of the damage to write an initial estimate as if they were physically at the vehicle instead of a remote location.

Before the pandemic began, virtual estimating was used for low-severity claims. However, it accounted for just 6% of all estimates written in the U.S. and 4% in Canada at the start of last year, according to Mitchell data. By April 2020, those percentages more than doubled.

Field appraisers can typically complete three to four onsite inspections per day when factoring in administrative tasks and travel time. Working from images, however, allows an appraiser to finish approximately 15 to 20 estimates per day.

Guided Estimating

Human-machine collaboration is the next step in the progression from handwritten to machine-written estimates. Appraisers are guided by the AI through each decision. The goal, of course, is to empower the appraiser while leveraging the AI for useful recommendations.

At this level of automation, the machine is becoming much more involved in the process. While appraisers ultimately remain in control, the information and decisions presented to them are delivered by AI with each sequential line of the estimate suggested for their consideration. Guided estimating extends beyond virtual estimating by:

Driving a set of AI predictions that recognize the damage to components

Transforming these predictions into repair line recommendations

Surfacing supporting evidence and empowering appraisers to make changes based on their own expertise

Delivering a continuous feedback loop that relies on appraisers’ decisions to educate the AI

Automated Estimating

Touchless estimating is the final level of automation. This fully automated process is powered by AI using vehicle and claims data to generate all operations, parts selections and pricing. Predominantly machine-driven, the process works by:

First capturing claim details and vehicle content, like virtual and guided estimating

Analyzing the information using computer vision and other machine-learning algorithms to translate it into component-level estimate lines

Pre-populating the entire estimate for review and approval by the appraiser

Additional data integration will help carriers further streamline the claims process beyond automating appraisals. For example, claims could be settled even faster by incorporating telematics incident reports, loan payoff amounts, titled/registered owner information and taxes and fees into the workflow. And LexisNexis Risk Solutions predicts that “by 2025, at least 40% of total loss claims will be settled within a couple of days instead of weeks.”

The transformation from field appraisals to touchless claims isn’t done in a vacuum or entirely by a machine. Appraisers are critical to developing and improving the process. If automation is introduced slowly, they can build their confidence in the AI while perfecting the results through continuing feedback. Creating an experience where the guidance is clear, actionable and transparent helps create trust between humans and machines.

Processes driven by human-machine collaboration take time, but they can lead to vast improvements in speed and accuracy. For auto insurance carriers, the time to act is now. After all, when it comes to meeting policyholder needs and staying competitive, the question isn’t whether to automate appraisals. It’s which partner has the experience and expertise to help you achieve your goals and support the evolution of your organization’s claims process.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Olivier Baudoux is senior vice president of global product strategy and artificial intelligence for Mitchell’s Auto Physical Damage division. He is a highly regarded technical leader and expert in artificial intelligence and automation.

The threat of a cyber-attack is far more dangerous now than it has been in the past, yet knowledge of the threat prevention systems necessary to protect oneself remain widely unknown.

Ransomware, in particular, has exploded as a problem. The frequency of such attacks is up almost 200% in the past two years. Severity is up, too — the average ransom demand has surged from roughly $10,000 to well north of $100,000. Combine those two issues, and ransomware is many times as big a problem for clients and insurers as it was two years ago.

Unless companies create more sophisticated protection systems, the problem will become even worse. Hackers are more astute, increasingly have access to inexpensive tools and have greatly expanded how and what they attack. There are even ransomware developers who sell or lease their ransomware, offering Ransomware-as-a-Service (RaaS).

In the past, attacks were relatively limited. When an employee clicked on an attachment that included a virus, the attack would encrypt the computer. There was minimal ability to spread to other computers, and individual computers were oftentimes backed up. This meant ransomware was frequently seen as just an inconvenience for a company and wasn’t as significant an issue for insurers as it is today.

Now, attackers use their initial entry into a computer as the starting point to work their way into a potentially huge network. The hackers lay traps and can generally find how and where the system’s sensitive information and backup server are located. With this information, the hacker can ensure that paying the ransom is the only way for a company to recover. An attack is often so devastating that the hackers can — and will — ask for exorbitant ransoms.

Tools for hackers are now inexpensive on the dark web, and hacker groups often coordinate. Perhaps one individual finds some credentials that allow a path into a system but isn’t sure how to exploit it. The person might sell the credentials on the dark web or hire some hacker known to be especially good at exploring and exploiting that kind of system; this is RaaS.

While some industries were considered to be relatively low-risk, that’s no longer the case. For instance, a few years ago, manufacturers were considered a target class for cyber insurance carriers because they were unlikely to store personal information, like credit card records. But now, they’re getting hit the hardest: Manufacturers are typically large companies with underdeveloped cyber security capabilities. Hackers would use this to their advantage and exploit these companies, which weren’t prepared for the onslaught of ransomware attacks.

Within the Tokio Marine HCC – Cyber & Professional Lines Group, we’ve been working with thousands of policyholders to better prepare them for attacks, and people understand the problem conceptually. Cyber is a serious consideration at the executive level and mandatory for business continuity and disaster recovery planning. The recent SolarWinds attack has reminded us all that even the best-protected government and business systems are vulnerable.

Based on simulations of attacks, we know that approximately 30% of those who receive a phishing email will click on a link that infects their system. Thorough training of staff on awareness and best practices reduces the number who fall for a phishing attack. With proper training, we've seen a reduction in exposure, whereby only 10% of employees fall for the trick when a hacker attacks; but that can still be enough for a catastrophe to happen, like the SolarWinds incident.

Training should be mandatory, but it shouldn’t be the only layer of defense for the network. Perimeter defense, secure backups and patch management are all critical. At present, Tokio Marine HCC provides a vulnerability scanning service for policyholders, which provides insights on vulnerable points of entry for hackers, including security vulnerabilities in policyholders' perimeter and out-of-date software, to help the insured avoid becoming a victim.

To combat weak passwords, many companies are starting to require multi-factor authentication to safeguard access to their system. A person must use an alternate means to authenticate themselves through a code texted to a smartphone, provide biometric evidence of their identity through something such as an iris scan or verify their identity via another secondary means. This dramatically reduces the risk that a compromised password leads to a devastating attack.

Companies are moving toward a “zero trust” model to protect their systems. The idea behind this emerging model is to have virtual “hall monitors” to challenge every actor in the system and force that actor to revalidate itself before going into an additional "room." In the past, companies would use a firewall to keep hackers out, but once hackers get past the wall they virtually have access to any "hall" in the network.

Companies should also be thinking about their outsourcing arrangements. Outsourcing can be cost-efficient, but if you have a 1,000-person company and only have three full-time people in IT, you’re likely to be using outside contractors. Issues may arise with disagreements regarding who is responsible patching systems or monitoring the network for suspicious activity. Furthermore, Managed Service Providers (MSPs) are being targeted by hackers and, if the hackers gain unauthorized access, are being used to launch ransomware attacks against their clients.

At Tokio Marine HCC – Cyber & Professional Lines Group, we apply our expertise and use our scale to make deals on behalf of clients to create a package of security services from leading providers. These packages involve, for instance, CrowdStrike, which provides endpoint detection security; Cisco’s Duo, a leading service provider of multi-factor authentication; and many others. We provide the bundling of these services at a discount off the market price, as well as with a discount on premiums, because, based on our data, we’re confident that our clients are less vulnerable with solutions such as these.

However achieved, reducing vulnerability helps both our company and our clients. We view this as a mutual relationship. If we can keep our claims costs as low as possible, our premiums can be as low as possible. However, it is critical for our insureds to focus on cyber security, so they are not an easy target for hackers. Whether a company has insurance or not, an attack is hugely disruptive, and, although we can transfer some of the financial costs, we can’t transfer everything. For instance, companies oftentimes still have to deal with being shut down for a stretch of time, while they hopefully recover their data and ramp back up.

Minimizing exposure to an attack is possible, but a company must invest in layers of network defenses, training and maintenance to stay ahead. Having the right insurance policy can protect you from the financial burden, but the reputational harm or missed opportunities that result from a cyber-attack can be very costly.

If you are unable to reduce your vulnerability, the problem could spiral out of control. Insurers will need to keep raising rates rapidly or will simply drop out of the market — supply is already dwindling. Clients may find rates so high that they will self-insure — at great risk.

At Tokio Marine HCC – Cyber & Professional Lines Group, we’re committed to the market, and demand for the insurance has never been greater. Our focus is staying on top of loss trends so we can help our clients continue to reduce risks and keep the problem manageable for all.

For more information about the Cyber & Professional Lines Group, please visit www.tmhcc.com/pro

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Although insurers have readily adopted technologies to serve their customers, they’ve been less enthusiastic about using the same technologies to support their employees. Perhaps that’s one reason only 4% of millennials in 2018 showed an interest in working in insurance and 28% of financial services employees expected to leave their employers within five years.

To remedy this talent problem, there’s been a call for insurance companies to adjust their organizational structures, give young talent greater flexibility and improve their work cultures. If collective calls for change were the push, then the pandemic was the shove. Practically overnight, insurance companies had to adopt tech solutions for their employees and agents to maintain business continuity without being in the office or visiting prospects and clients. One recent survey reports that 60% of insurance professionals who responded have been working from home 100% of the time during the pandemic.

It’s clear that the insurance industry may not return to “normal” for the foreseeable future. When the first wave of the pandemic hit, companies learned to use tech to facilitate business. Now, the challenge will be adopting tools and practices that balance the best of technology without losing the one-to-one connectivity that’s the industry’s lifeblood.

Social Media and the Future of Work for Insurance Companies

The insurance industry’s evolution may have been slow until recently, but the industry hasn’t been stagnant. Most companies have shifted toward providing more customer-centric experiences.

Some have leveraged artificial intelligence to deploy more personalized services, such as using chatbots to answer inquiries or process claims. These solutions can serve as a framework for using even more advanced technologies. For instance, casualty companies are using IoT-connected sensors, real-time satellite information and unmanned aerial vehicles to assess accidents and natural disasters with unprecedented speed and efficiency.

No matter how useful these solutions may be, however, they cannot replace the human connection, an essential element in insurance. In my view, success with technology starts with taking the authenticity of relationships to digital channels, social media being chief among them. Here’s why:

1. Social media helps maintain smooth, consistent communication.

Communication skills have always separated the underperformers from the superstars, and, in insurance, effective and proactive customer communication is king. In fact, a survey from Collinson showed that two-thirds of customers want further communication from their insurance providers, and three-quarters would like to receive product and benefits recommendations. Yet most insurance companies reach out only for transactional matters like policy updates (67%) and renewal notices (79%).

The tech industry has mastered digital communication because tech companies have always sold products and services to customers remotely. Now, it’s time for the insurance industry to adopt a similar communication style, and social media is the medium of choice. This is especially true now that American adults are using social media more frequently. Insurance companies must prioritize consistent, engaging social media communication with prospects and customers to future-proof their businesses.

While a permanently digital workforce might not suit insurance companies as well, there is still a lesson to be learned: The impacts of the pandemic have launched us into a lasting transition to the future of work. As agents turn to social media as a new way to connect with their customer base without the opportunity to meet face-to-face, they’re discovering that no other marketing channel can come close to replicating the two-way dialogue of face-to-face conversations. The benefit of connecting with customers from anywhere at any time won’t be lost once agents can meet with clients in person again. Social media outreach and engagement should continue alongside traditional communication tactics as an efficient way to form connections.

3. Social media amplifies the voice of your best brand ambassadors.

Tech companies have understood for years that people trust other humans over brands and companies. It’s no wonder tech influencers on social media can gain millions of followers. Insurance companies should take note and put real people behind the face of the brand to build trust.

An insurance carrier’s agents have, arguably, the most intimate knowledge of the company’s culture, service offerings and customer needs, so the marketing team would be wise to tap this organic source of advocacy. Empower agents to use social media on behalf of the brand, whether that means posting branded content to humanize the brand, sharing educational articles for customers and prospects or simply answering questions and concerns directly.

Don’t forget to arm them with the right tools and content to represent your brand properly. As digital natives enter the industry, they’ll want access to resources to help them succeed and organizations that will offer egalitarian structures. Social selling gives each agent a voice and flattens the organizational structure. However, as agents have greater geographic flexibility, it’s important to manage social media activity for compliance and brand continuity.

Insurance companies rely on genuine connections and risk management expertise daily, but the workforce won’t be back in the office anytime soon. With digital transformation already underway in the industry and the astronomical growth of social media use among adults, it’ll be easier for them to find their footing in the future of work.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Gregory Bailey is president and CPO at Denim Social. He was licensed to sell insurance at the age of 20, continued as an agent in the industry for the next nine years and then stepped into the corporate world of insurance.

When there’s a leak under your sink, do you let it keep dripping or call a plumber? Sounds like a simple question with an obvious answer. But what if you don’t know you have a leak? You’ve gotten used to a high water bill and less water pressure without even realizing how much you could be saving if you found the leak and fixed it.

This scenario isn’t unlike an issue many of today’s insurance carriers are experiencing called “premium leakage.” Inefficiencies, inaccuracies and risky processes due to the use of legacy systems cause carriers to unknowingly “leak” premium they should be collecting. Fortunately, eliminating premium leakage is simply a matter of looking under the kitchen sink to find the source and taking the necessary steps to stop it.

Where Legacy Systems Fall Short

The systems we now consider to be “legacy” (i.e. Excel, COBOL or VB6) have been relied on by insurance carriers for decades. For many carriers, these systems are seen as tried and true. Having accepted legacy systems as a way of life, carriers can have trouble noticing their shortcomings.

But as we look beneath the surface, we can see that legacy systems are causing some of the major pain points insurance carriers face:

Multi-entry

Siloed workflows

Inaccurate data

Manual errors

Slow turnaround times

Redundant processes

These pain points are due to legacy systems’ inability to share data seamlessly across the organization, integrate both internally and with ecosystem solutions and automate rules and regulations.

The Real Cost of Legacy Systems

Legacy systems aren’t just painful, they’re costly. A recent FINEOS study shows that an estimated 5% to 10% of insurance premiums vanish every year due to the inefficiencies caused by legacy systems. Premium leakage comes from multiple areas within an insurance carrier’s operations. However, a few spots are notorious for leaking valuable premium:

Case Setup Inaccuracies

A top culprit for premium leakage occurs when setting up and installing a new employer group on multiple systems that are not integrated. This process requires massive amounts of work-arounds and inevitably results in data inaccuracies across systems. Roughly 5% of annual premium can be lost just in this one area.

This notorious source of premium leakage can make or break a carrier’s year. Whether the carrier or the employer is responsible for managing eligibility and enrollment, relying on legacy systems or repurposed solutions (i.e. using a P&C system for anything in the life, accident and health market and vice versa) means the carrier is ill-equipped to properly manage enrollment and claims eligibility. This results in millions of dollars lost that otherwise could fund additional staff, capital investments or strategic initiatives.

What Carriers Can Do to Fight Premium Leakage

The solution to eliminating premium leakage is the same as the solution to better mobility and flexibility: strengthening your core. Because legacy systems and custom solutions are inherently prone to premium leakage, carriers must rethink their core system solutions to combat it.

So, what do these stronger core systems look like? They’re modern and integrated and allow data to flow freely between the carrier and the employer. They’re also purpose-built for the market they serve, enabling the insurance carrier to be a reliable source of truth for current plan and policy information, as well as member data for the employer.

With stronger core systems in place, the premium calculations for both the employer and the carrier are based on the same source of truth. Further, when an employee is enrolling for coverage the benefits and provisions are accurate and truly reflect what is eligible. This turns into accurate premium being billed to the insured and, most importantly, the right benefits being paid when they are needed. The result is zero premium leakage, and money back toward the insurance carrier’s bottom line.

The Customer Experience Goes Beyond the Monetary Benefits

While monetary recoupment is an exciting reason to tackle premium leakage, there are also customer satisfaction benefits of upgrading from legacy systems. Modern core systems make processes more efficient and yield faster turnaround times on claims for the employee. As most claims are filed in times of serious illness/injury or bereavement, a quickly processed claim can significantly improve a customer’s experience during a difficult time.

Additionally, the insurance carrier must meet the insured or enrollee where they are. To accomplish that objective, the digital experience offered must come with the same accessibility and ease experienced in most apps available to the insured. Carriers can’t offer a superior customer experience digitally when their technology backbone is made up of older legacy systems that are unable to support APIs or integration. They need modern systems that come equipped with APIs and the data structure to support the insured at all points of the policy lifecycle.

Premium leakage can be eliminated when carriers decide it’s time to look under the kitchen sink, see the source of the leak for themselves and call in the plumber. In this case, the plumber comes in the form of a modern, SaaS-based core system. By addressing the costly inefficiencies caused by legacy systems, insurance carriers can keep the full measure of their projected premiums in their pocket while also providing a superior customer experience.

Get Involved

Our authors are what set Insurance Thought Leadership apart.