Digitization and technology transformation are taking top priority for property and casualty insurers in 2021, a recent survey reveals. But while many insurers are meeting consumers’ demands for a more efficient and convenient experience, they may be leaving money on the table by failing to expand strategies to address B2B needs, including around digital payment.

Certainly, investing in infrastructures to support consumers’ desire for a more modern, retail-like experience is an important first step toward embracing the digital age. As COVID-19 accelerated the move toward contactless payment, leading insurers aren’t just going digital. They are also diversifying their payment offerings to include mobile and push-to-card payments.

Yet, many carriers stop there without considering the big-picture benefits of a more holistic strategy that incorporates digital B2B payment offerings. However, change is on the horizon: A recent Association of Financial Professionals (AFP) survey found that one-third of organizations primarily use electronic payment for B2B transactions, while 60% say they are very likely or somewhat likely to convert the majority of B2B payments from check to electronic. These findings suggest that both vendors and suppliers see the value of digital payment—and so, too, do the insurers that work with them.

B2B Digitization: Trends and Benefits

The advantages of B2C and B2B digital payment processes are similar, but the priorities are different. Both options create economies of scale by improving operational efficiencies and lowering costs associated with processing paper checks, and both lay the foundation for better consumer or client experiences.

Yet, while the need to respond to consumer demands has served as the primary driver for B2C digital payments in the insurance space, the AFP survey suggests that operational considerations are the drivers for B2B payment:

Nearly half of respondents point to the benefits of straight-through processing to accounts payable or accounts receivable and the general ledger.

Cost savings came in as the No. 2 priority for 45% of respondents, and both improved cash forecasting and speed to settlement tied for third at 42%.

While vendor relations ranked lower in priority, the potential to elevate partnerships certainly exists as digital adoption is typically a win-win administratively for both the insurer and third-party. For example, in the healthcare space, remittance data that is electronically linked to payment from insurers to providers is critical to easing the administrative tasks associated with payment reconciliation. Digital payment infrastructures exist that can support creation of the remittance data, creation of the payment, reconciliation of the payment and treasury management services. The impact: reduced potential for error, improved visibility and increased productivity.

The COVID-19 pandemic also upped the ante for B2B payment digitization. Faced with the need to quickly pivot to remote operations, insurers with electronic payment infrastructures already in place were at a distinct advantage. A Mastercard study suggests that COVID-19 became a significant force propelling adoption and use of B2B electronic funds transfer to address payment delays and improve security and transparency.

Holistically Addressing B2C and B2B Digital Payment

Automated clearinghouse (ACH) represents the entry point for many insurers taking the plunge into digital payment. It’s a good first step, but there are many reasons why a broader portfolio of options makes sense when considering B2B payments.

The insurance industry is heavily reliant on payment data. While ACH can address remote operations and speed of payment, it lacks the framework to support immediate visibility into remittance data. For this reason, electronic payment options such as virtual cards hold great promise for B2B.

Like ACH, virtual cards are efficient, cost-effective, secure payments and reduce administrative costs. For B2B transactions, these options require no enrollment or IT investment, and there are no complex remittance reports to reconcile. Characterized by a randomly generated card number, expiration date and security code, virtual cards are loaded with a specific payment tied directly to the payment request generated in the payer’s adjudication system. They also reduce administrative complexities and eliminate the need to share bank account information—and can be easily replaced if lost or stolen.

As a complement to ACH, solutions such as virtual cards and mobile payment options can work in tandem to improve payment to businesses while also addressing consumer preferences. In a recent Engine Insights/VPay survey, more than half of respondents said payment choice was important to the claim experience.

Time for a More Modern Approach

It’s a new year for growth and positioning in the insurance industry, and many lessons have been learned from 2020. As trends point to accelerated adoption of frictionless, contactless payment for consumers, vendors and service providers, the right digital payment strategy will give insurers a competitive advantage on many fronts. Forward-thinking insurers will consider how to holistically address digital payment strategies to support B2B and B2C.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Elisa Logan is vice president of marketing at Optum Financial. Logan’s focus is to provide strategic leadership and drive company growth. She brings over 25 years of B2B strategy and marketing experience to her role.

The pandemic has changed everything. Well, not everything… but it has changed many aspects of the lives of individuals and families and has had far-reaching effects on businesses in every industry. The patterns that represent the ebb and flow of daily life have been altered significantly. Where we work, travel, eat and buy are quite different than what they were in early 2020. This upheaval of society has important, long-term implications for the P&C insurance industry. Customers, risks, operations and the workforce all have undergone rapid transformations over the last year. This makes strategic planning a challenge for insurers.

As the new decade dawned in 2020, many insurers began thinking about what the world would be like in 2030 and, by extension, what it would mean for their business. Enter scenario planning.

Scenario planning is a time-tested tool in the strategic planning toolkit. SMA has been quite busy facilitating scenario planning sessions for insurers over the past couple of years. The beauty of scenario planning is that, even though the timeframe is often 10 years out, the result of the process is the identification of strategic actions that should be taken in the near term to position for the possible developments in the future. Before the pandemic, many were able to envision the state of their customers and their business model 10 years out. Even though there were many uncertainties, there was still a relatively clear line of sight to the future.

Although mid- to longer-term planning should never be based on straight line projections, they still form the basis from which various alternate future scenarios can be developed. Now, it is fashionable to say that 2025 is the new 2030. The predominant theme is that the pandemic, economic lockdowns and work-from-home mandates have accelerated digital transformation. There is no doubt this is true, but the reality is more nuanced than just an acceleration of trends in a straight-line manner. It is not just that the future we envisioned will arrive more quickly than we originally thought – it’s that the future will be different than we all thought it would be. In other words, the future isn’t what it used to be.

None of us can predict the future. But that makes scenario planning even more valuable. Evaluating different alternative futures in the context of the insurance enterprise stretches our thinking, opens up possibilities and identifies foundational capabilities that are required for success in any of the possible futures. Every dimension can be explored in a holistic way, looking at factors external to the insurer such as the industries and customers they serve, the potential changes to the landscape of risk, the nature of the workforce and the role of automation and advanced technologies. The whole value chain is in play – from how products are conceived and designed to how they are sold, priced and serviced – along with every part of the business that supports those activities.

What will the world of 2025 or 2030 mean for your business? For that matter, how do you need to adjust your strategies and plans now and for 2022?

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Mark Breading is a partner at Strategy Meets Action, a Resource Pro company that helps insurers develop and validate their IT strategies and plans, better understand how their investments measure up in today's highly competitive environment and gain clarity on solution options and vendor selection.

Social inflation is a term you frequently hear in risk management these days. It refers to a public, anti-establishment sentiment that has a far-reaching impact on businesses and the insurance industry. Last year, Out Front Ideas with Kimberly and Mark discussed the impacts of social inflation with a panel of experts. Our guests were:

Mark Bennett, vice president of large casualty claims for Safety National

Oliver Krejs, partner for Taylor Anderson

Aref Jabbour, senior consultant for Trial Behavior Consulting

Andrew Pauley, government affairs counsel for the National Association of Mutual Insurance Companies (NAMIC)

Jury Trials

While only 5% of lawsuits result in a jury trial, knowing the potential outcome for a defendant shapes the future of underwriting and pricing risks in the industry. Because of the impact on rising costs, it is critical to explore what is causing the public to shift sympathy in support of the plaintiff.

Over the last five to six years, we have seen a steady increase in awards by juries. We have also witnessed an increase in the number of cases going to trial, especially in cases valued up to $1 million.

What is happening with liability juries to drive these large reports? One of our experts breaks down the major areas of concern.

The perception of the value of money has changed since the financial crisis. Juries believe that defendants can pay out larger sums of money to a plaintiff. Much of this is based around our daily exposure in the media to larger verdicts, desensitizing the public and making such verdicts appear more common and acceptable. Juries also believe defendants should pay even if there is substantial evidence they were not at fault, because the plaintiff deserves compensation.

Media outlets and social media are affecting public opinion.Anyone with a social media account can attest that ideas expressed there are more extreme and less filtered than what someone would be willing to say in person. These publicly expressed ideas become validated in people's minds, which are hard to change. For example, we are seeing an increase in jury awards against police officers, even in cases where the evidence supports that the officer acted appropriately. There is a true struggle to overcome these types of societal prejudices as media-based opinions become more prolific.

Bad Faith, Litigation Financing and Other Challenges

Expansion of bad faith claims, litigation financing and the statute of limitations also challenge insurers. One of our guests summarized these issues:

Bad Faith — The original intention of bad faith was to hold an insurer responsible when particularly egregious acts have been committed and when a worker has been intentionally put in harm’s way. However, some states have lowered the standards for claims. Insurers can get hit with punitive damages after one minor claim. Often, the claim can simply result from missing a statutory deadline, so no one was harmed, but the claim is used to punish the insurer. One of the most common effects of bad faith litigation is added costs to the system. Florida, for example, has long been known as one of the most challenging jurisdictions for insurers in the context of bad faith, and vehicle owners recently paid $1.2 billion in added costs based on outcomes of bad faith litigation.

Litigation Financing — This has become a regulatory vacuum where companies or individuals finance litigation in exchange for a percentage of the settlement/verdict. This results in longer litigation and more cases going to trial, and can also create a conflict of interest among parties. It creates a major concern for expansive litigation and furthers the need to investigate the motivations behind these cases. We see more instances of hedge funds getting involved simply because of the return on investment it provides them. These situations don’t always mean the plaintiff will be better off. For example, in one case in New York, the plaintiff was allowed to borrow $27,000, and the case settled five years later for $150,000. The lending company took $100,000, the attorneys took the rest, leaving $111 for the plaintiff.

Statute of Limitations — The guidelines for when a claim can be filed have been changing rapidly on a state-by-state basis due to loosening laws across the country. These changing laws significantly affect public entities, school districts or other institutions, specifically relating to the ability of a claim to be filed retroactively in a childhood sexual assault case or abuse claim. Some states have expanded the limitations beyond expiration dates, some allow for a period of discoverability and some allow for a lookback period. California, for example, passed a law allowing for a lookback period that extends the time a file can be claimed up to five years. The law has extended previous claims of viability from the age of 26 to the age of 40. However, the court’s interpretation will determine whether these claims can be filed based on current policies.

Litigation Solutions

Although we often cannot avoid litigation, there are measures we can use to prevent excessive jury awards. While none of these guarantee a favorable outcome, our guests suggest them as a general approach.

Change how cases are worked up from the beginning.A specific case that came out of Texas’ fifth circuit sought to change a law to closely mirror a direct action state like Louisiana, allowing the layers below an insurer to settle out and fund the case, leaving the excess carriers above them with the obligation to defend the case. Litigation changes like this will result in excess carriers having to completely adjust due to changing defense costs and exposures. Understanding how to educate the jury, providing expert testimony and getting all parties on the same page will need to be in the basic setup of a case.

Advocate for early intervention and get all parties on the same page. Before litigation begins, you should ask yourself what your discovery process looks like. Are you interviewing all potential witnesses and figuring out what the fact pattern may look like? Do you know the answers to questions that the jury may seek later on in trial? Do you have the facts that will allow you to empower the jury? Ensure that there is a consistent message and always take more of an anticipatory approach than a reactive one.

Educate the jury on what is reasonable and factual.Because of social inflation’s impact on a jury’s prejudice, it is imperative to empower jury members with facts and reason. For example, do you know what the jury views as a reasonable award that would properly compensate the injured? In hospital charges, billings are often inflated up to 300% to 600% higher than what the facilities regularly accept from insurance companies.

Tort reform is a key element in combatting these rising jury awards. Stakeholders need to educate legislators on the societal costs of these large awards. This is no easy path. Businesses need to get involved with state and local bar associations and work with PACs on legislative efforts.

The awards being seen today are from accidents that happened several years ago. That means the industry is probably looking at several more years of accident year combined ratios above 100% before rates are adequate for the reality of the exposures being faced.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Kimberly George is a senior vice president, senior healthcare adviser at Sedgwick. She will explore and work to improve Sedgwick’s understanding of how healthcare reform affects its business models and product and service offerings.

Mark Walls is the vice president, client engagement, at Safety National.

He is also the founder of the Work Comp Analysis Group on LinkedIn, which is the largest discussion community dedicated to workers' compensation issues.

In this week's Six Things, Paul Carroll explores the implications of AI-based transcription on the issue of too many meetings. Plus, how insurers can step up on climate change; solving life insurance coverage gap; how AI is moving distribution forward; and more.

As the jury got set to begin deliberations in the trial of Derek Chauvin this week, the judge told them that they would have to rely on their notes from the three-week trial because no transcription of the testimony would be available. Someone tweeted that the lack of a transcript made perfect sense — if the year were 1821.

He has a point. Natural language processing has advanced so much that using artificial intelligence to produce an instant, highly accurate transcription has become trivial, The advancement has broad implications, ranging from the number of meetings that we’re all subjected to, to the interactions that agents and customer service reps have with clients... continue reading >

Join Michael Palotay, Chief Underwriting Officer for Tokio Marine HCC - Cyber & Professional Lines, and Paul Carroll as they continue their discussion on ransomware, cyber attacks, and how businesses can protect themselves.

Mark Twain reportedly once responded to a rumor of a serious illness by saying, "Rumors of my death have been greatly exaggerated." Insurance agents and brokers could have said the same thing over the past decade and will likely be parrying those rumors for years to come.

There’s no doubt that agents & brokers inhabit a world going digital and not every agent will migrate easily into the ever-more-digital world, but those who do will find the work more rewarding, both for themselves and for their ever-more-loyal clients.

Join Michael Palotay, Chief Underwriting Officer for Tokio Marine HCC - Cyber & Professional Lines, and Paul Carroll as they continue their discussion on ransomware, cyber attacks, and how businesses can protect themselves.

ITL is a leading platform for thought leaders in the insurance and risk management industries. Partner with ITL to create expert thought leadership content and promote it to our expert audience.

Sponsored Content

Custom Content

Display Advertising

Custom Webinars

Monthly Topic Sponsorships

ITL Partner Packages and more

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Finally, Fewer Meetings?

Using AI to produce an instant, highly accurate transcription of a recording has become trivial, The advancement has broad implications.

As the jury got set to begin deliberations in the trial of Derek Chauvin this week, the judge told them that they would have to rely on their notes from the three-week trial because no transcription of the testimony would be available. Someone tweeted that the lack of a transcript made perfect sense -- if the year were 1821.

He has a point. Natural language processing has advanced so much that using artificial intelligence to produce an instant, highly accurate transcription has become trivial, The advancement has broad implications, ranging from the number of meetings that we're all subjected to, to the interactions that agents and customer service reps have with clients.

Let's start with meetings. I hate most meetings. I was so disappointed to realize years ago that someone had written a book called "Death by Meeting," because I considered writing a book with that exact title.

But meetings are hard to stamp out. When a colleague and I facilitated a long-term strategy session for a major medical organization a few years ago, we asked for a list of things that the top team wanted to stop doing. Almost everyone said the organization held far too many meetings -- and recommended a long series of meetings to tackle the problem. (The CEO had quite the chuckle.)

Automatic transcriptions provide at least part of a solution. Many meetings are held just to distribute information -- even though the orthodoxy is that meetings should focus on making decisions. But transcriptions make distributing information trivial. Those not attending a meeting don't even have to watch or listen to a recording; they can just skim the transcript in a tiny fraction of the time. If they want to catch all the nuance, or if the transcript seems unclear, they can click on the links that the AI provides to that part of the recording and listen to or watch the actual session. (This article in Wired provides some detail on the advances. My favorite service is Otter.ai.)

No one has to take notes at a meeting any longer. Those wanting to forward details to their staffs can just highlight the important points, or, if some information or interactions are considered to be confidential, can simply cut and paste what they want to share from the transcript.

Many people who now feel their time is sucked away via meetings will be able to avoid them while not missing out on any of the information. The problem won't entirely go away, because many want to be included in meetings even if they don't want to actually attend -- status depends on being invited to certain meetings. But at least there's now more flexibility, and smart organizations will find ways to use the advances in transcription to free valuable time for executives and staff.

The capability should be cranked into the deliberations that companies are going through now as they consider how much work-from-home will be part of their future. We've all learned how to "attend" virtual meetings without being 100% present -- I've pretty much lived in gym shorts for 14 months now. Knowing that meetings can be automatically transcribed gives us a backstop so we can be productive during the times when our full attention isn't needed. Smart companies will note that the definition of a meeting has become fluid and will plan accordingly.

AI-based transcription won't just reduce the number attending meetings at senior levels of insurers but will also affect how agents and customer reps interact with clients. While it's long been easy to record conversations, the interactions are now searchable because they can be turned into text. That makes a huge difference.

I remember a colleague at the Wall Street Journal's nascent TV operation cataloguing video back in the early 1990s, trying to document all the key words and topics that might make the video of use years later. He was a bright fellow who went on to be CEO of a multibillion-dollar communications company, but he soon found that the work took too much time and yielded too little return. Today, he could search transcripts in seconds to see who was interviewed, what the person said, etc.

This searchability will increase accountability for anyone offering advice. That's not a huge issue at the moment, because it's largely those giving advice who are recording calls "for training purposes," but clients will increasingly record calls, too, and will have text that they can easily search and present as evidence if they feel they've been ill-used. Look at how seemingly every public interaction is caught on camera these days -- and recording audio is even simpler.

At the same time, agents and insurers are increasingly able to search transcripts to see what is puzzling clients, so they can smooth out kinks in the customer experience. Agents and insurers can also see what bigger issues might need to be addressed.

We don't live in 1821. It's 2021, and, after a year of COVID, we deserve all the breaks we can get.

I'll start us off by skipping four meetings this week.

Stay safe.

Paul

P.S. Here are the six articles I'd like to highlight from the past week:

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

It was 1999, and everything about business was changing. The internet was hot and growing! Ebay and Amazon launched within the previous four years. Napster debuted the peer-to-peer music file sharing network – the precursor to iTunes. E-business!

Fast Company magazine was putting out 300-page monthly issues that covered the most innovative companies and people imaginable. Every time you turned a corner, you found a Starbucks that you hadn’t seen before. Apple had just created berry-colored, egg-shaped computers called iMacs. The economy was hot. IT departments were busy with Y2K preparations. The future was coming fast and furious! Could life get any better?

With all of the optimism for the future in the air, the time was ripe for people to “discover their working selves.” Two Gallup researchers, Marcus Buckingham and Curt Coffman, wrote a managerial book, "First, Break All the Rules," that had us thinking about how to do things differently using our individual strengths. They used interviews with over 80,000 employees to identify practical insights regarding managers. Some of the insights for individuals and managers are highly relevant when carried to insurers and systems. For example, in their chapter on "How to Manage Around a Weakness," they discuss how managers can devise a support system that keeps an individual’s strengths operational while rendering their weaknesses irrelevant. The exact same principles can be applied to insurers that find themselves with weaknesses that seem to be rendering their strengths ineffective. There are support systems that can make those weaknesses irrelevant.

In a 2001 follow-up book, "Now, Discover Your Strengths," Buckingham and former Gallup chair Donald O. Clifton built on that idea by helping individuals identify their strengths so that they could focus on what they do well. This concept also works well in the macro sense for insurers. How well an insurer knows its strengths and weaknesses will determine its ability to aggressively make the right strategic and operational moves.

If we think about what has transpired the last 12 months during the COVID-19 crisis, we see a pattern emerge that is crucial for insurers to re-visit.

There is great opportunity in the COVID and post-COVID economy.

Insurers need to know their organizations well enough to know whether they are prepared to take advantage of the opportunities. Insurers need to know which strengths and talents they are missing and which ones they have firmly in hand.

They need to focus on their strengths while they seek assistance from others to shore up weaknesses.

They need metrics. They need to pursue continuous evaluation of where they are against competitors because that landscape is constantly shifting. They need to know: “Are we Leaders, Followers or Laggards?” They need to use that position, no matter what it is, as inspiration to move forward.

For the past five years, Majesco has been helping insurers look in the mirror and to gauge their efforts in light of the marketplace shifts and trends and other insurance organizations. In what ways are these companies leading? Are they doing enough to be considered Leaders? Are they Followers, still in the race, and trying to close the gap? Are they, perhaps, Laggards…desperately needing to look in the mirror and reconsider their activities in light of their strengths and weaknesses?

This year’s comparison and analysis has been tinged with the presence of COVID-19. How are companies reacting? Has it modified their plans? Majesco’s latest thought-leadership report, Strategic Priorities 2021: Despite Challenges, Leaders Widen the Gap, sheds light on how COVID-19 has hurt and helped insurers and their plans for the future. We’ll share some key insights from Majesco’s report below.

We have seen the significant impact of the COVID crisis on the growth and strategic activities last year for all three segments; even the Leaders were not immune. But what distinguishes Leaders from the others is how much better they were prepared and responded to the crisis. Our research suggests the pandemic could be an inflection point that redefines every company in the industry – by pushing Laggards into further irrelevance, testing Followers to recommit to a new digital future, and providing Leaders a springboard to accelerate innovation, competitive differentiation and growth.

Leaders are able to take advantage of the unique conditions of the crisis that can create the springboard which sparks innovation. A recent article in MIT Sloan Management Review helps explain these unique conditions, highlighting “five interdependent conditions that characterize a crisis and boost innovation.”

A crisis provides a sudden and real sense of urgency.

Organizations can drop all other priorities and focus on a single challenge, reallocating resources as needed.

Teams come together to solve the problem with a greater diversity of perspectives.

The importance of finding a solution legitimizes what would otherwise constitute waste, allowing for more experimentation and learning.

Because the crisis is only temporary, the organization can commit to a highly intense effort over a short time.

Leaders are undoubtedly viewing these conditions as an opportunity to seize a competitive advantage, which is reflected in their stronger optimism for the future compared with Followers and Laggards.

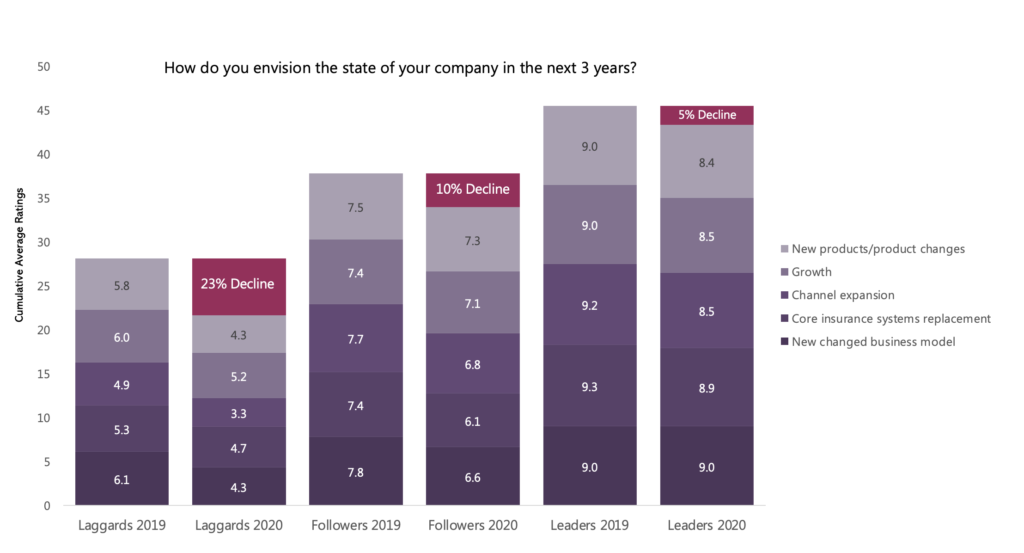

When assessing the outlook over the next three years, the impact of COVID is clear, as seen in Figure 1. Both Laggards and Followers have the same level of decreased optimism for the future as they had in the assessment of their companies’ growth and strategic activities in 2020 vs. 2019. However, Laggards also had nearly a 25% decline in their outlook for both last year and the next three years whereas Followers, while less, still showed smaller declines of 10% in both.

Leaders, on the other hand, show much more optimism. Despite a 5% decline in their future expectations compared with last year’s survey, this is less than half of the 12% decline in their assessment of their companies’ performance in 2020 vs 2019.

Figure 1: COVID-19’s impact on outlooks for company growth and strategic activities over the next three years

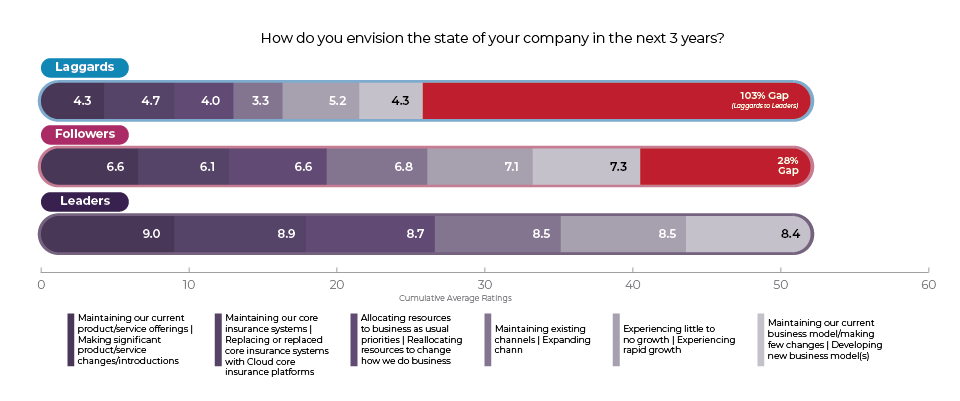

The most compelling result was astaggering, game-changing 103% gap between Leaders and Laggards in how they envision their companies over the next three years, a significant increase from the alarming 64% gap on their assessment of the past year (Figure 2).

While less, Followers’ 28% gap does not bode well for their future and contradicts earlier evidence suggesting they are keeping pace with the Leaders. While initial appearances may have been encouraging, digging deeper highlights that the breadth and impact of what Followers are doing is not enough for the future. The gap is slowly growing, and with another crisis it could substantially affect their future. Given that we have seen multiple major events or crises nearly every four or five years over the last two decades that have accelerated change – dot.com, 9/11, 2008 financial crisis, emergence of insurtech and COVID – the likelihood is great!

Figure 2: Gaps between Leaders, Followers and Laggards in assessments of company growth and strategic activities over the next three years

Even more discouraging for these two segments is the continued growth in the gaps with Leaders in their optimism for the future. This is especially alarming for the Laggards, whose gap swelled by nearly 40 percentage points.

Followers and Laggards must remember that every challenge has an opportunity or solution, some of which are incredible and give hope for an exciting, new future. They just need to plan for and execute on these to create an optimistic future.

Mirror, Mirror on the Wall

Instead of asking the famous quote by the evil queen in Snow White - “Mirror, mirror, on the wall — who's the fairest of them all?” … insurers should ask themselves “Mirror, mirror on the wall – am I a Leader, Follower or Laggard?”

This is where Majesco’s high-level analysis is meant to help answer that question. The most important analysis happens at the individual insurer level. Some form of introspection and analysis must occur within each insurer to confirm their locations within the realm of Leaders, Followers and Laggards. For a quick review, assess your own company against these definitions, below.

The Leaders: Companies that understand the market dynamics and have rapidly moved to planning and execution across most of the key areas. They are focused on a two-speed strategy by investing in modernizing and optimizing today’s business, while also investing in the future business nearly equally. They are or have moved from legacy or non-platform core to cloud platform core solutions, leveraging an array of platform, digital and emerging technologies to elevate customer experiences, launch products, expand channels and embrace ecosystems to transform the business.

The Followers: Companies that understand the market dynamics but are not moving as quickly or broadly into the various areas for planning and execution. They are solidly focused on modernizing and optimizing today’s business, but less so than Leaders on the future business. While they are relatively close in many areas to Leaders, the pace of execution when looking out three years is not the same, meaning that the gap will steadily increase. Because of this, Followers may not recognize the danger in the gap until it is too late.

The Laggards: These are companies that generally understand the market dynamics but are clearly stuck in the past and have failed to rapidly move to planning and execution across the array of strategic areas. They are not moving to new cloud platform solutions, or incorporating platform and emerging technologies. They are keeping their business solely focused on the current business model, which lacks the level of automation, digital capabilities, and more, needed to meet the rising demands of a new generation of buyers. If not already there, they are approaching a downward spiral of relevance that will be nearly impossible to reverse.

Because Leaders are so far ahead, their investment will be substantially less than Followers or Laggards that have waited, hesitated or just moved too slowly. Playing catchup is expensive – both in outlay of resources and in lost opportunities. The key is to confirm where you are, then never lose focus on it. Your organization deserves to know where it stands.

Fast-Tracking Transformations That Play to Your Strengths

The significant gaps between Leaders versus Followers and Laggards are becoming so great that there is a danger of Followers constantly trying to play catchup rather than their own game to win, and for Laggards entering an accelerating downward spiral. If you are still relying on the past and pre-digital age, pre-pandemic business models, now is the time to reevaluate.

It is time for bold moves. It’s time to skip some of the traditional steps involved in transformation and pull in support systems that will help your organization play to its strengths. It’s time to ask the hard questions to the Mirror on the Wall!

Begin by assessing where you are in the Knowing-Doing Gaps, from our Strategic Priorities research, that defines Leaders that are accelerating digital transformation with resilient digital business models. Rethink and reprioritize your strategies to take advantage of the shift and opportunities unfolding. And execute on these priorities with a sense of focus and urgency.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

Traditional IPOs give private firms months (if not years) to prepare for the governance requirements of being a public company — including adjusting compensation plans, hiring independent directors and establishing charters and bylaws, for example. The explosion of special purchase acquisition companies (popularly known as SPACs) in the market highlights one of the things “reverse merger” deals don’t have — time. There are often just weeks between when an investor approaches a target company with a letter of intent and when a contract is signed, formally taking the firm public.

This accelerated timetable to go public is what makes SPACs attractive to many investors and founders. But a short timeframe also forces the target company to act quickly, ensuring compensation plans meet the evolving needs of the firm and that governance processes are addressed following the acquisition.

In this article, we’ll explore the biggest compensation and governance issues private firms should address and then plan for when approached by a SPAC investor.

Adjust Compensation Plans Before a Deal Is Signed

When a firm is approached by a SPAC investor, the business should ensure its compensation plans are in order and make any necessary adjustments before signing a letter of intent for a deal. Once the letter is signed, the investor will need to be involved in approving changes, which can complicate the process.

In a traditional IPO planning scenario, we recommend leaders establish or review their guiding compensation philosophy, what they can afford on cash and equity programs, internal pay equity and pay for performance alignment. There’s little time for that kind of deeper analysis on a SPAC deal, however. The target company needs to be pragmatic and look at what changes to executive compensation and equity incentive plans can be done immediately.

Here is a checklist of items to tackle first and quickly to ensure your compensation programs are ready for when the acquisition is complete, and the firm is public:

Update broad-based and executive peer groups. Peer groups will shift from pre-IPO and private companies to public firms of similar size and industry or to where the firm is competing for talent. Keep in mind that the COVID-19 pandemic has accelerated the number of employees working remotely, effectively widening talent pools. Smaller, private firms are more likely to hire from local talent pools but that will likely change as a business grows — therefore, new peer groups may need to include businesses outside of the local market or industry.

Revisit current and future change-in-control provisions.Many incentive plans include CIC provisions for more traditional transactions and don’t apply to SPAC deals. First, determine whether your incentive plans need to specify SPAC deals more explicitly. Then, update CIC plans for when the company is public. It’s in stakeholders’ interests that key executives have reasonable employment protections that allow them to focus on executing strategy and driving performance.

Update parameters for equity incentive plans. Determine the ideal number of shares to authorize given what’s already outstanding and the company’s future headcount growth needs. We typically recommend a plan include an annual evergreen feature because they allow for an automatic, formulaic increase in plan reserves, typically at the start of each new plan year. Absent such a provision, increases in plan reserves after an IPO require shareholder approval via a proxy vote. Firms will also need to consider whether outstanding equity will be converted, cashed out or canceled upon completion of the acquisition.

Retain key talent through the close of the deal. Cash compensation and unvested shares should be market competitive to retain key talent through the transaction. The uncertainty surrounding SPAC deals can present a flight risk for employees.

Decide whether to introduce an employee stock purchase plan (ESPP). ESPPs can add a lot of employee value with minimal cost and are more widespread depending on company industry and size. To learn more abouot ESPPs, please see our article on plan prevalence here and plan design here.

Integrating the Board and Setting Up Director Pay

A SPAC acquisition is complicated and requires effective communication between the business leaders and the boards of both the SPAC and the target acquisition. Furthermore, the founders and board members of the target firm often stay at least for a certain period after the acquisition is complete. Therefore, it’s important for the combined team to build a positive relationship from the start.

Board members won’t typically receive compensation until the deal is complete and the company goes public. Instead of receiving cash compensation, SPAC board members receive pre-IPO founder shares of the SPAC. The founder shares for the SPAC investors are converted into common shares on the first public day of trading in a ratio of 1:4.

Once the SPAC is taken public, we advise the board to meet with external advisers to determine the market rate for board compensation based on the firm size and industry. As with many governance issues, director compensation has received extra scrutiny from investors in recent years and newly public companies need to establish fair pay plans that aren’t deemed excessive by proxy advisory firms and institutional investors. The largest proxy advisory firm, Institutional Shareholder Services (ISS), deems director pay excessive if it is within the top 2% to 3% of companies in the same sector and index.

Addressing Governance Processes Once Public

With investors increasingly scrutinizing the governance policies of public companies, including those that are newly public, going through a SPAC means your company will need to act quickly on governance issues.

Consider that, a few years ago, ISS began recommending investors vote against or withhold votes from the entire board of a newly public company (except new nominees to be considered on a case-by-case basis) if the board adopts bylaws or charter provisions that allow for what ISS deems egregious governance policies. These include supermajority vote requirements, a classified board structure and a multi-class capital structure.

There are numerous actions that pre-IPO firms should take early on. SPAC investors typically don’t have a lot of experience with public company governance requirements, so business leaders will rely heavily on the expertise of external advisers and the newly formed board of directors.

The first steps should include recruiting independent board members from diverse backgrounds (e.g., gender, race, ethnicity, work experience). From there, establishing independent committees and charters and then developing an annual independent board evaluation process to provide insight into performance are key. Once those processes are established, companies need to develop a plan of disclosing their governance policies to stakeholders. While certain public disclosure is required (e.g., director bios, their independence, committees and charters), the level of detail can vary, and many institutional investors are expecting more robust disclosure than has been standard. As part of this, showcasing an awareness of environmental, social and governance issues (ESG) in public disclosures can also help to position a newly public company favorably relative to investors, customers and employees.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

We are past the first anniversary of the start of the COVID-19 pandemic. While it’s an event many of us never expected to see, it is a reality that is informing an array of operational, financial and structural decisions inside the insurance industry. These changes will likely be with us long after the dust settles and the post-pandemic normal becomes the de facto operating model.

The pandemic has wrought a catastrophic human toll. However, there have been some silver linings in terms of things like the rapid acceleration of digital and virtual capabilities that allow customers, employers and employees to rethink the once seemingly unchangeable operating rules. Our collective eyes have been opened to an array of new possibilities that will likely inform hybrid models for as far into the future as we can see.

Another set of changes rippling through the insurance industry relates to the financial pressures that carriers are facing. Some of this has been created by persistently low interest rates. Long-term demographic shifts and changes in customer preferences are also having a profound impact on what carriers need to bring to market to remain both relevant and competitive.

Industry Evolution

This confluence suggests some notable “sea change” events in the future for life insurers in particular. For one thing, long-standing expense challenges have become clearer and more urgent. Investment income has masked this for perhaps as much as 25 years. No more. New products generally have less fixed cost covering capability than old, in-force blocks, so the natural changes in generations of policies create their own form of expense pressure.

Demographic shifts are also in play. During this decade, the youngest Baby Boomer will reach retirement eligibility. We are but months away from the oldest millennial reaching 40 years old. The shifts in product demands are palpable, and a strategy that suggests millennials will turn into Boomers, aside from the graying hair, appears flawed. Perhaps fatally so.

All this is now playing out in carrier decisions about future business models. One interesting example is that publicly traded companies are under pressure to consider fundamental changes in their strategies, moving away from retail businesses with long-liability-tail products and toward more fee-based and institutional models. MetLife recently completed an exit that included individual life, annuity and P/C operations. Prudential announced that it is considering an array of options, including a possible sale of its core L/A business. Principal has a study of the future of the L/A business underway, driven in part by activist minority investors.

At the same time, mutual carriers (e.g., MassMutual, Northwestern Mutual) seem to be doubling down on the long-liability-tail retail businesses, perhaps a recognition that this is most possible when the prospect of quarterly earnings calls is not an imminent challenge.

The spate of M&A witnessed over the past few years shows no signs of abating. This is likely a reflection of the need to generate scale in core businesses, a recognition that organic growth can be difficult in economic downturns, as well as the realization of the need to see if smaller units are really businesses, distinct from “corporate hobbies.”

The challenges, and opportunities, for carrier IT organizations are real. Clarity on the business direction for a company, agility to respond quickly to new priorities, flexibility to ramp resources up (or down) depending on circumstances, and the ability to tie IT investments more closely to the internal business cycles of an organization will be key. Business as usual is likely to take on a different meaning in the future, a reality compounded by the ever-shortening useful life of technology.

We would have arrived here with or without the pandemic, but COVID-19 has accelerated the moment of reckoning. Developing an overarching IT strategy to address both the technology and human capital needs to support this could be key to how successful CIOs and their teams are at delivering successes, building on their effective responses to the pandemic’s arrival. It turns out that was the start, rather than an end, of a story.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Rob McIsaac is a senior vice president of research and consulting at Novarica, with expertise in IT leadership and transformation as well as technology and business strategy for life, annuities, wealth management and banking.

“Culture is the soul of the organization — the beliefs and values, and how they are manifested. I think of the structure as the skeleton, and the process as the flesh and blood. And culture is the soul that holds the thing together and gives it life force.” - Henry Mintzberg

The prevailing risk culture within an organization can make it significantly better or worse at managing these risks. It also significantly affects the organizational capability to take strategic risk decisions and deliver on performance promises. Risk culture arises from the repeated behaviors of the employees of the organization. These behaviors are shaped by the underlying values, beliefs and attitudes of individuals, which are partly inherent; and by the existing corporate culture in the organization.

Now that risk practitioners are finally catching on to risk culture and risk culture building; way after my first article on people risk in GARP Risk review back in 2004, we suddenly find a whole bunch of risk culture “experts” talking absolute garbage when it comes to the doing this thing.

Let us thus get the basics right:

Basics No 1: Governance Structure:

Firstly, the reporting line for the head of risk/chief risk officer is directly to the board. If you run your business by committees, that would be the chairperson of the board risk committee; if not, it should be a non-executive director who knows something about the management of risk.

Secondly, do not appoint your risk champions; select them from volunteers.

Basics No 2: The Definitions:

Before you formulate your own understanding, use these definitions:

“Risk culture is the system of values and behaviors present in an organization that shapes risk decisions of management and employees. One element of risk culture is a common understanding of an organization and its business purpose” --NC State ERM Initiative

“Risk culture is a term describing the values, beliefs, knowledge, attitudes and understanding about risk shared by a group of people with a common purpose” --Institute of Risk Management

Risk culture building is the training of mind, of heart and of personal character to respond effectively to any situation of risk and take the right decision to mitigate, control or optimize risk to the advantage of the organization.

Basics No 3: The Levels of Maturity:

Level 1: In a bad risk culture, people do not care and will not do the right things regardless of risk policies, procedures and controls. Generally reflecting an environment of risks managed in silos, people are always “firefighting” with no clear risk owners, no real communication and weak accountability.

Level 2: In a typical risk culture, people tend to care more and will do the right things when risk policies, procedures and controls are in place. Risk owners are clearly defined and roles and commitments are understood, but effective awareness is still lacking.

Level 3: In a good risk culture, people care and will do the right things even when risk policies, procedures and controls are not in place. At this level, there are integrated risk management teams with standardized roles and clear accountabilities, normally controlled by a central function that coordinates all activities.

Level 4: In an effective risk culture, people care enough to think about the risks associated with their jobs before they make decisions on a daily basis. Strong cross-functional teamwork and employees who apply sound judgment in the management of risk. A small central risk management advisory team that understands the enterprise fully supports the business at all levels. Organizations at this level are well-prepared for crisis management.

Level 5: In the ultimate risk culture, every person acts as a risk manager and will constantly evaluate, control and optimize risks to make informed decisions and build sustainable competitive advantage for the organization. At this level, organizational and individual performance measures are fully aligned and risk-sensitive. Every employee is a risk manager, and knowledge and skills are upgraded continuously. Such an organization is agile and designed to adapt to changes.

Basics No 4: Assessing the Current Level of Maturity and Building Action Plans:

To start risk culture building, an organization first needs to get an accurate picture of the current level of risk culture maturity in the organization. Various attempts have been made to do this, and most revert to some kind of questionnaire or checklist approach linked to a scoring sheet that is eventually tabulated to quantify an overall score, which is linked to a perceived level of maturity.

In some instances, organizations call in consultants who also conduct interviews. The outcomes are then debated and agreed upon by consensus with the client. These processes can easily be manipulated to support the perception of those in charge and also fail to identify specific weaknesses to support targeted action plans.

A full risk culture maturity assessment must cover the following operational areas associated with the effective management of risk:

Policies

Processes

People and Organizational Design

Reporting

Management and Control

You have two options:

A manual process: (offered as part of the formal Risk Culture Workshop training)

An on-line assessment tool: In an attempt to improve the accuracy of these kinds of assessments, a leading U.K. consultancy developed and launched an on-line assessment tool that is now commercially available.

Building an effective risk culture requires aligning the structured approach in the innovation framework and the four-pillar risk culture building approach with the organization’s vision and purpose to be the most trusted and inspiring connector of positive change. This must be done within the context of the existing corporate culture, driven by the organization’s strategic objectives, with the outcome to realize the key benefits of risk culture building and create sustainable competitive advantage through the optimization of the management of risk within the organization.

Building an effective risk culture is much more than changing your organizational culture in line with your vision, mission, corporate values and risk appetite—you must factor in the interests of competing national cultures, sub-cultures, Maslow’s theory on individual self-actualization and the informal groups in the company. The interactions among these are not predictable, and variables cannot accurately be isolated.

An effective risk culture is not a matter of risk assessment or level of compliance; it is a matter of individual ownership of risk and personal “conviction” -- a state of mind where human beings own the risks and the process of managing those risks through making well-informed risk decisions because they want to, not because they have to. Companies drive value through optimizing risk management rather than a culture of compliance where people will do only what is required.

Basics No 6: The Four Pillars

Think differently

Get the whole picture

Build a risk nervous system

Make every employee a risk manager

Each of these pillars represents a structured approach to address the underlying mindsets and behavioral aspects of organization and individuals to influence their attitudes and responses to risk in the context of the organizational demographics and their education, experiences, circumstances, attitudes, beliefs, emotions, social status and other factors and filters.

Basics No 7: The “Do Not Even Think About It” List:

You can NEVER build an effective risk culture if you use the old Three Lines of Defense model or the (even worse) new Three Lines model

If you are promoting a “culture of compliance,” do not waste money attempting to build an effective risk culture

Building an effective risk culture is not a “project"; the work never stops

Even a bad risk culture can be strong, so stop talking about a strong risk culture as a good thing

If you are not going to link risk culture to the performance management of each employee, at all levels, forget about it

You can follow any risk management framework or standard to the last letter and still be useless at the actual management of risk... just because of culture

You can be a brilliant chief risk officer in one company and a total failure in the next... just because of culture.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Horst Simon has been in commercial banking and the risk management consultancy industries for four decades. Since 2010 he is a risk management consultant and trainer and was associated with leading global players in the field of risk management consultancy and training as well as business process outsourcing.

Our learnings fall into five broad areas. Whether you are an insurance carrier, BGA, FMO, insurance agency or producer, these lessons are key for the decade ahead.

Millennials are starving for life and annuity digital sales

Millennials are using Robinhood, Acorns, Betterment and other fintech apps daily and are conditioned to expect a similar digital experience in the workplace, including an advanced digital sales toolset for life, long-term care and annuities.

A consistent refrain that we hear from advisers is: “I am tired of trying to explain life and annuity products using PowerPoints and PDF brochures. Every other financial services experience is application-based. Even my 401K experience is interactive now.”

Millennials demand that there be a more visual, interactive and intuitive way to sell life and annuity products that matches their every-day fintech experiences.

Financial advisers expect a “digital experience,” and greater life and annuity adoption depends on it

Financial advisers today have already completed the shift to digital financial planning platforms. Whether it is EnvestNet Money Guide Pro (MGP), eMoney, RightCapital, AssetMap or RetireUp, the financial planning experience today is managed through a fintech platform. These platforms have simplified the discussion and engagement between the financial adviser and the client, making it easier to understand financial options and their benefits for the overall financial plan.

This is the expectation – digital, visual, interactive and easy to understand.

If life and annuity carriers and distributors want to return to growth – and increase sales within advisory channels – they will have to “speak the language” of the market, selling and servicing products through modern digital delivery.

Experience is everything

The adage, “Experience is everything,” has become, “Digital experience is everything.”

We increasingly talk about the paramount importance of the customer experience (CX) and the user experience (UX). Each sits at the forefront of organizational strategy and service delivery. And nearly every financial services product class has already shifted onto this agenda. Even cars are now designed and ordered through an online digital experience.

Unfortunately for the life and annuity sector, the sales experience remains entrenched in a legacy model – static, 45-page PDF illustrations; long PowerPoint decks; and traditional, print-oriented “brochureware.”

Without modernizing the pre-sale to in-force digital customer engagement (for a world where “experience is everything”), the life and annuity sector stands little hope of returning to sustainable long-term growth.

The chief learning from over a million digital sales presentations?

A legacy sales experience today undercuts the sales effectiveness of wholesalers, advisers and agents and ultimately reduces closing rate and top-line sales numbers across the P&L.

RIAs, BGAs, financial advisers and insurance producers are “de-localizing”

One little-noted potential long-term outcome of COVID-19 and the transformation shift to remote work is the “de-localization” of RIAs, BGAs, financial services firms and financial professionals.

Historically, financial services firms have focused their services on a local market or region, so they could meet and serve their clients, face to face, at the office or in the home. COVID-19, however, broke this model.

First, the permanent shift to virtual client engagement (e.g. via Zoom or Microsoft Teams) has proven that the face-to-face relationship can be retained even when in-person meetings cannot.

Second, the growing relocation of individuals over the past year has meant that many financial professionals are having to virtually follow clients to retain them. Finally, as firms have gotten smarter about lead and client acquisition driven by data, the opportunity of digitally targeting new clients -- at a micro-individual level -- in new cities or regions has become a reality.

What might this trend lead to over the long term?

It is possible that the trend may spark a new era of innovation in the advisory space, as “niche specialists” are able to digitally scale their service proposition.

Transformation of the wholesaler model is well underway

Wholesaler demand for digital sales enablement and marketing tools is growing by the day.

What digital sales enablement capabilities are wholesalers crying out for?

In our experience, this has been concentrated around three critical areas:

Digital, interactive product analysis tools that support virtual sales engagements

Modern platform-based product training, education and marketing experiences

Real-time data insight to drive case and account follow-up

While the digital hybridization of the adviser-client discussion has already been underway for several years, the wholesaling shift is just now taking off.

If you are a life and annuity carrier or distributor, start now. Not only will your GenX (age up to 55) and millennial (age up to 40) wholesalers double their sales effectiveness, they will also personally thank you, as will the advisers you serve.

Get Involved

Our authors are what set Insurance Thought Leadership apart.