When I was in high school, a friend of mine had a poster on his wall that read, "Just because you're paranoid doesn't mean they aren't out to get you."

That pretty well summarizes how the world of cybersecurity and insurance works. Companies may feel paranoid for looking over their shoulder all the time, expecting something back to happen, but we all know that there are plenty of bad guys out to find all the victims they can.

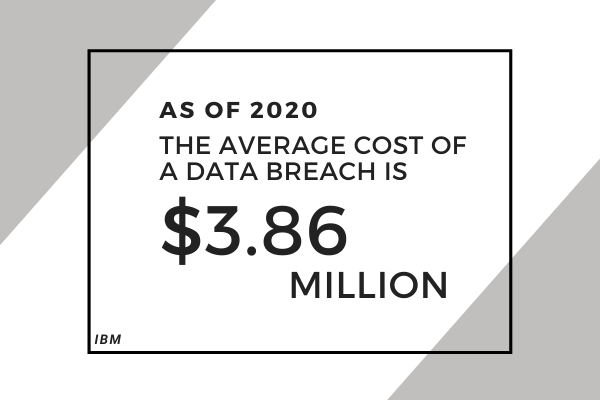

Ransomware, in particular, has become an enormous problem. A few years ago, hackers would make limited strikes and hit a few computers at a company, then demand $10,000 or maybe $20,000 to unlock them. Now, though, hackers have figured out ways to combine their specialized skills and make a much broader attack that includes finding and locking up the backup servers -- which means the hackers have pretty much shut a company down and can make any ransom demand they want. Demands of $500,000 or more are common, and some reach into the many millions of dollars.

Insurance is surely part of the solution for most companies, but paranoia plays a role, too. Companies need to spend much more time focusing on how to prevent the cyber attacks in the first place, and the best insurance companies are using their expertise to help clients with that effort. New tools and techniques offer considerable hope.

Within that effort at prevention, there is room for an awful lot more cooperation. Law enforcement can work with insurers and company clients to educate them on trends and offer advice, and insurers and their clients can work together to share information on vulnerabilities and on potential solutions. As long as the bad guys are working together, the good guys need to, too.

- Paul Carroll, ITL's Editor-in-Chief

WHAT TO WATCH

The Alarming Surge in Ransomware Attacks

Insurers can help clients protect themselves – but preventive approaches aren’t yet widely implemented, leaving the door open for unscrupulous hackers. Join Michael Palotay, Chief Underwriting Officer for Tokio Marine HCC - Cyber & Professional Lines, and Paul Carroll as they continue their discussion on ransomware, cyber attacks, and how businesses can protect themselves.

WHAT TO READ

CISOs, Risk Managers: Better Together

In most large firms, risk managers buy cyber insurance--but are rarely expert in network security and may not fully understand the risk profile.

Ransomware Grows More Pernicious

The emergence of the Maze variant creates a new threat, that stolen information will be released to the public on the internet.

How to Fight Rise in Cyber Criminals

IT security standards have sometimes been lowered or suspended for work at home in the pandemic, resulting in cyber security exposures.

New Enhancements for Cyber Coverage

Cyber insurance is probably the most rapidly evolving product on the market. Here are some of the newer enhancements.

How CAT Models Are Extending to Cyber

The approach to models used for natural catastrophes is being applied to cyber, leading to a quick maturation in understanding the risks.

How Machine Learning Halts Data Breaches

There are four main types of data breaches that advances in machine learning can help thwart.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Now, more than at any time in history, customers, insurance carriers and their distribution need nonstandard auto protection for drivers.

Although, in the past, some carriers have declined to cover higher-risk drivers, that could change, partly as a result of economic turmoil caused by the COVID-19 pandemic. Early in 2020, both the consulting firm McKinsey & Co. and the reinsurance broker BMS Group predicted the United States could see a surge in the market for nonstandard auto insurance.

In July 2020, Allstate Corp. announced it would buy nonstandard auto insurer National General Holdings Corp. for about $4 billion in cash, a deal that is set to be completed early this year. With National General reporting about $5.6 billion in gross written premiums in 2019 (with nonstandard auto policies accounting for 44% of that), Allstate is scaling up its auto insurance business at a time when the coronavirus has crushed traffic on roads and reduced claims. In September 2020, State Farm, America’s largest property and casualty insurance provider, announced it would buy nonstandard insurance provider Gainsco for about $400 million in cash, another deal expected to be completed early this year. It’s State Farm’s first acquisition of another insurance company in its 98-year history.

So why is a renewed focus on this type of insurance is important? Well, let's start with the most important part of the equation first: the customer.

The Customer

According to IBISWorld, the market size of the U.S. automobile insurance industry is estimated to be $311 billion in 2021. Estimates vary regarding the prevalence of nonstandard coverage; some experts say it makes up 20% of premiums for personal auto insurance, while others estimate it to be 30-40% of the auto insurance market.

Customers need nonstandard coverage availability and premiums to protect their families. One family member having driving issues (a DUI, multiple accidents, SR-22, being recently nonrenewed from a preferred policy and poor credit) shouldn’t knock out the entire family unit from getting the type of protection they need and from qualifying for a preferred policy/rate.

Today, the average household has multiple vehicles and multiple drivers. More than ever, people want a carrier and an advisor/firm to represent them on everything. They expect and demand a one-stop shop for all their insurance and financial needs. This includes, but is not limited to, providing protection even when the household account is not 100% a preferred risk.

Now let’s look at how a focus on the nonstandard market can benefit carriers.

The Carrier

Until recently, most of the largest carriers focused on the “preferred market.” A few of the leading carriers have had affiliate companies/brands to provide a nonstandard solution for their customers. Other preferred carriers dabbled in or tried to provide a “near-standard“ option, only to get clobbered in many instances.

Progressive and Geico are examples of companies embracing the nonstandard market with expertise pricing and are models of how to provide customers with a protection solution that is sustainable. However, most carriers are currently looking at strategic alliances or are purchasing existing nonstandard carriers as partners. The bottom line is that the customer has spoken, and companies need to provide a one-stop shopping experience going forward. Not providing such a solution opens the door to the competition.

Finally, let's look at how increasing the focus on nonstandard coverage can benefit distribution’s ability to provide unrivaled service.

Distribution

Whether advisors are employee-led or contractor-led, are brokers, firms, agents or team members, providing unrivaled service, advice and product solutions is the way forward. While there will always be an element of transactional sales, providing a meaningful and consistent customer experience is the winning strategy.

Most practitioners would not want to try to make a living on nonstandard auto only. But ignoring it altogether means a significant missed opportunity. The firm owners, brokers and agencies that have a laser focus on the economics business realize they must provide real solutions for all their clients, even in situations that are complex, difficult and risky.

Providing nonstandard service and solutions not only wins new business, it sustains relationships. And we all know great relationships lead to referrals and additional opportunities. Providing unrivaled service requires focus on factors other than just price. Offering nonstandard coverage when your competition does not is one way to leap ahead.

The nonstandard auto market has never been more important. It’s no longer a one-off. As our industry retools, nonstandard auto needs to be at the top of the list as we serve our customers.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

There is little doubt that the risk landscape has changed in the past few years. Natural catastrophes are increasing in number and severity, low probability risks are coming to fruition, higher probability risks (such as cyber) are looming larger and new risks are emerging. Here are some of the ways insurers can address the changing risk landscape.

From single-event scenarios to multiple-simultaneous-event scenarios

It has been common for insurers to test their solvency by creating several scenarios and estimating what each would do to capital levels. Typically, each scenario tested one variable at a time; for example, what would a 1-in-250-year event or an-XX basis point interest rate drop do to capital strength in a given year? However, as the risk landscape intensifies, single variable scenarios are no longer sufficient.

More robust and multi-event scenarios need to become the norm if the potential risk to capital is to be evaluated effectively. For example, what would the result be if 1-in-250-year event happened while equities plunged 35% in value? Or what would the effect be if two 1-in-250-year events occurred at the same time inflation rose by 40%? What would happen if three 1-in-150-year events happened in the same year? The macro-economic environment constantly changes, and individual company conditions are unique, so scenarios need to be tailored and updated as appropriate.

From virtually ignoring low probable risks to paying more attention to low probability risks

Scoring risks is done on the basis of both their potential impact (dollar impact to profits, revenues, expenses) and their probability of occurring (high medium, low). Other things may come into play, too, such as how imminent the risks are (one year away, three years away, more than three years away). This kind of scoring makes it possible for companies to decide which risks should get the most focus and resources in an effort to mitigate their impact. The problem has been that the impact of low probability risks is hard to quantify and is often underestimated. Additionally, the very fact that their likelihood is not high means these risks tend to be taken less seriously than perhaps they should be.

The current pandemic — with all its ripple effects — has shown that low probability/high impact risks can and do happen. Some insurers realized the loss potential if a virus became widespread and incorporated virus exclusions in various policies. This has served them well, because those with such exclusions are better protected against claims for coverage that was never intended.

Some low probability/high impact risks emanate from the broader environment and some come from a particular company’s business model or operations. In either case, the risks need to be properly vetted and commensurate mitigation plans need to be implemented.

From focusing on current risks to focusing on both current and emerging risk

That there are so many current risks insurers must attend to leads to emerging risks not being identified or being pushed to the back burner. Even though emerging risks can be hard to identify and assess and may not seem imminent, they should not be marginalized. Given the speed of change, these risks can emerge as full-blown risks sooner than might be anticipated. Significant ones can quickly cause serious consequences.

Any insurer ignoring emerging risk identification and mitigation is opening itself up to potential loss or impairment that could have been minimized or avoided. Some emerging risk categories are: AI; cyber; environmental, social and governance (ESG) developments; and new energy sources.

Insurers’ perception of themselves can be quite different from the way they are perceived by stakeholders outside the industry. And it is the external perception that forms the basis of an insurers’ reputation. Any one insurer may have a better or worse reputation than the universe of insurers, but all are affected to some extent by the umbrella perception.

Some of these negative aspects of insurers’ reputations stem from many retail buyers not always understanding the insurance mechanism and from thinking insurers make greater profits than they actually do. Some retail buyers would rather not buy insurance at all but are forced to by laws or lenders. Commercial buyers can find insurers slow, cumbersome and not very transparent.

In reality, insurers tend to be ethical in honoring their contractual obligations and are price competitive while also trying to improve processes and customer experience. This is largely true because insurers are heavily regulated, have publicly available ratings by rating agencies and exist in a competitive marketplace.

Despite this reality, a poor reputation contributes to low customer loyalty, fraudulent claims, extra scrutiny by third parties and other risks or threats. Now, insurers face more reputational risk than ever before as things like example, the legitimate, but unfortunate, denial of COVID-19 related business interruption claims has dented insurer reputations. How this will play out in the long run is unknown.

What this means in terms of insurers’ enterprise risk management (ERM) is that, when they look at their reputational risk picture, they need to assess the risks to their reputation from the outside in. They need to see how they appear in the eyes of customers, regulators and the community at large. Improvement can take the form of improved communication starting with clearer policy language but can move well beyond that to more frequent communication with customers, greater transparency and more responsible advertising.

All in all, insurers of all sizes need to take note of changes in the risk landscape and must continuously improve their ERM practices.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

She has written three books on ERM: Enterprise Risk Management – Straight To The Point,Enterprise Risk Management – Straight To The Value and Enterprise Risk Management – Straight Talk For Nonprofits, with co-author Al Decker. She is an active contributor to the Insurance Thought Leadership website and other industry publications. In addition, she has given presentations at RIMS, CPCU, PCI (now APCIA) and university events.

Currently, she is an independent consultant on ERM, ESG and strategic planning. She was recently a senior adviser at Hanover Stone Solutions. She served as the chairwoman of the Spencer Educational Foundation from 2006-2010. From 1989 to 2006, she was with Zurich Insurance Group, where she held many positions both in the U.S. and in Switzerland, including: EVP corporate development, global head of investor relations, EVP compliance and governance and regional manager for North America. Her last position at Zurich was executive vice president and chief administrative officer for Zurich’s world-wide general insurance business ($36 Billion GWP), with responsibility for strategic planning and other areas. She began her insurance career at Crum & Forster Insurance.

She has served on numerous industry and academic boards. Among these are: NC State’s Poole School of Business’ Enterprise Risk Management’s Advisory Board, Illinois State University’s Katie School of Insurance, Spencer Educational Foundation. She won “The Editor’s Choice Award” from the Society of Financial Examiners in 2017 for her co-written articles on KRIs/KPIs and related subjects. She was named among the “Top 100 Insurance Women” by Business Insurance in 2000.

Six Things Newsletter | April 27, 2021

In this week's Six Things, Paul Carroll explains why the insurance industry should beware the grey swan. Plus, how social inflation affects liability costs; the future isn't what it used to be; a new environment for insurers; and more.

In this week's Six Things, Paul Carroll explains why the insurance industry should beware the grey swan. Plus, how social inflation affects liability costs; the future isn't what it used to be; a new environment for insurers; and more.

As the U.S. steadily emerges from the pandemic — and we all hold out hope for India — the temptation is to dismiss it as a one-off, a once-in-a-century health disaster, a black swan. But the pandemic is actually what’s coming to be known as a grey swan — something that, while rare, relates to a known problem and that can be planned for, if we come to grips with the cognitive biases that blur our ability to see them.

As we’ve learned the hard way over the past 20 years, there are a lot of grew swans out there, so we as an industry need to learn to prepare better for them, both for our own sakes and for those of our many clients... continue reading >

Join Michael Palotay, Chief Underwriting Officer for Tokio Marine HCC - Cyber & Professional Lines, and Paul Carroll as they continue their discussion on ransomware, cyber attacks, and how businesses can protect themselves.

Mark Twain reportedly once responded to a rumor of a serious illness by saying, "Rumors of my death have been greatly exaggerated." Insurance agents and brokers could have said the same thing over the past decade and will likely be parrying those rumors for years to come.

There’s no doubt that agents & brokers inhabit a world going digital and not every agent will migrate easily into the ever-more-digital world, but those who do will find the work more rewarding, both for themselves and for their ever-more-loyal clients.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

The words “platform” and “ecosystem” are trending and in danger of becoming overused and losing their true meaning, but when used in the proper context they are powerful and highly relevant. The insurance claims management process is a perfect use case for just how critical these structures can be in achieving transformation. And my latest endeavor with Claim Central Consolidated is an excellent example of a platform and ecosystem that enables carriers to make that happen.

The property claims process has historically been stubbornly long, complex and more costly than necessary. The factors contributing to these conditions include a disjointed overall workflow, which is a result of the many manual tasks, different staff and third-party skills required and the disparate, non-integrated systems needed to fully adjudicate and resolve the claim.

In simple terms, a platform is a group of technologies that are used as a base upon which other applications, processes or technologies are developed. The word "ecosystem" derives from the Greek words oikos meaning "home," and systema, or “system.” In the early 1990s (go, class of 1990), James F. Moore originated the strategic planning concept of a business ecosystem, now widely adopted in the insurtech community.

Using biological ecology as a metaphor, Moore revealed how today's business environment parallels the natural world and how, just like organisms in nature, companies must coexist and coevolve within their own business ecosystems. He identified radically new cooperative and competitive relationships and provided a comprehensive framework that businesses can use to enhance their own collaborations with their customers, suppliers, investors and communities. Who knew we would be applying this type of thinking to technology?

Platforms and Ecosystems for Insurance Claims

Powerful and exciting insurance industry ecosystems have emerged – made possible by digitization – and continue to evolve like living organisms, as connected sets and cluster ecosystems within the larger and broader ecosystem of services in a single integrated experience. Platforms enable and support ecosystems in that they connect offerings from cross-industry and inter-industry players in P&C, Life, Health and Accident.

Platforms and the ecosystems they support will increasingly enable insurers to turn strategic visions into realities. Today, insurers succeed by offering products. In the future, insurers will win by providing access to risk prevention and assistance services—and by offering the right product to the right customer at the right time.

Claim Central Consolidated

Many people have asked what I’ve been working on since exiting WeGoLook. I am thrilled to be spearheading the perfect example of the power and potential of a platform-based ecosystem within Claim Central Consolidated, a global leader in property and auto insurance claims technology, services , data and insights, and pioneers of digital claims fulfilment. Our market-leading technology solutions are completely transparent, simplifying the claims process and significantly improving policyholder service satisfaction on behalf of leading insurers across the globe.

Developed and proven in Australia, Claim Central recently expanded to the U.S. market, initially focusing on the property claims market with the successful rollout of TradesPlus – a network of over 40 trades types which are easily accessed within our Exchange. The Claim Central platform comprises three basic components offering a number of solutions and choices within many evolving cluster ecosystems embedded in our broader platform:

ClaimLogik Plus end-to-end claims lifecycle management platform, built with the vision of providing a single platform that connects all parties involved in resolving a claim, available in three purpose-built versions;

Growth Edition – best suited to smaller businesses such as 1099’s

Business Edition – best suited to SME scale insurers, IA firms or TPA’s;

Enterprise Edition – best suited to higher volume claims handling such as larger TPAs or carriers

TradesPlus+ Managed Repair

cloud-based platform connecting insurers directly with a pre-screened, on-demand marketplace of suppliers to carry out claim-related services and property repairs.

Insurers have direct access to suppliers including:

Contractors

Emergency Services

Inspectors

Adjusters

Experts

Housing

Virtual Inspections as a Service (VIaaS)

connects remote desktop assessors directly with policyholders to inspect and assess their claims using our live video streaming and collaboration platform LiveLogik

enables insurers to secure inspections and damage assessments without the risk, cost and time associated with deploying traditional field adjusting resources during the COVID-19 crisis.

The Power and Potential of Ecosystems

McKinsey research found that ecosystems will generate $60 trillion by 2025 which will constitute 30 percent of global sales in that year. Consequently, many insurance executives are looking beyond industry borders to understand the growing opportunities and threats that come from new partners and competitors in the ecosystems relevant to them, from mobility to healthcare and beyond.

Platform businesses are the most efficient value creators, compared to other types of businesses, because they harness the power of distributed supply and network effects. The network effect is a phenomenon whereby increased numbers of people or participants improve the value of a product or service.

Purpose-Built Insurance Ecosystems

The P&C insurance industry has already developed ecosystems to support specific business functions, and continues to do so. Some of the earlier examples date back to 1980 when information providers developed platforms linking auto insurers to collision repair facilities for the purpose of streamlining the accident repair process. These ecosystems quickly expanded to include independent appraisers and adjusters, autoglass and car rental vendors, salvage pool and towing operators, parts providers and others. Today they are beginning to include telematics service providers and auto manufacturers and dealers.

New property claims ecosystems such as Claim Central have emerged to include a full suite of segment specific cluster ecosystems including contractors, inspection technology, digital payments and other service providers which enable insurers to resolve claims in hours instead of days or weeks. According to Paul Carroll, editor-in-chief of Insurance Thought Leadership, "Innovation will focus less on bells and whistles and more on improvements across entire processes and organizations. But incumbents must start preparing."

Look no further for a brilliant and powerful new ecosystem extension than the recent announcement that Credit Karma, a unit of Intuit, has partnered with Progressive Insurance to offer usage-based auto insurance to Credit Karma’s millions of financial service smartphone app members using its integration with DMVs to obtain instant driver and vehicle information.

“It is not a matter of if, but when the insurance industry will have to adopt an ecosystem approach. The industry is not immune to the changing demands of the market” - Dr. Geoffrey Parker, Professor of Engineering at Dartmouth College and a visiting scholar and Fellow at the MIT Initiative on the Digital Economy.

I feel blessed and excited to be a tiny part of it!

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Robin Roberson is the managing director of North America for Claim Central, a pioneer in claims fulfillment technology with an open two-sided ecosystem. As previous CEO and co-founder of WeGoLook, she grew the business to over 45,000 global independent contractors.

Commercial lines insurers have many options for distribution partners. The world of intermediaries is continuing to expand, with many new platforms to connect distributors to carriers. We are frequently being asked by insurers how many distribution platform partners an insurer should have and how to identify the ones that best align to their strategies. Often, the questions are framed as comparative raters, especially because the concept of comparative rating migrated from personal lines over into commercial. Most of the intermediary platforms provide rate-quote-bind capabilities along with the capability to compare rates and coverages across multiple carriers. But many of the platforms provide a richer set of capabilities to improve the entire process for the benefit of agencies, brokers, MGAs, carriers and others in the ecosystem.

In total, we count around 30 companies that focus on simple or moderate commercial lines risk, ranging from small commercial to mid/market and specialty lines. Prominent names include CoverHound, CoverWallet, Bold Penguin, Tarmika and Talage, plus incumbents like IVANS, Bolt and Appulate. (The world of placement and trading platforms for very complex risk is a whole different animal, but there are also a number of new players in that space.)

SMA’s recent research report, “Commercial Lines Distribution Platforms: Rapidly Evolving Options for Carriers,” provides insights into the growing stable of distribution platforms with significant capabilities for commercial lines. A companion report profiling each of the companies identified in this report is scheduled for release in May.

Let me now answer two of the most common questions we have been getting from insurers working on distribution strategies:

Question #1. How many distribution platform partners should we connect to?

Answer #1. It depends, but the answer is probably not just one.

Question #2. How should we select the best partners?

Answer #2. This should be based on a number of factors, including the lines covered, robustness of specific functional capabilities, platforms your agents are already connected to and the business model, among other factors.

Of course, there are many other considerations related to distribution strategies. Should we pursue a digital brand or direct strategy to move into new markets? Or even to compete in markets where we already have a presence? What enhanced tech capabilities should we be providing to our distributor community to attract more submissions that match our appetite? What are the best approaches to managing channel conflict? What are the best options to enable a true omni-channel environment?

The list could go on, but the main point is that distribution strategies in commercial lines are in play. Many companies are updating or rethinking their strategies to reach preferred segments and drive more profitable business.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Mark Breading is a partner at Strategy Meets Action, a Resource Pro company that helps insurers develop and validate their IT strategies and plans, better understand how their investments measure up in today's highly competitive environment and gain clarity on solution options and vendor selection.

Beware the Grey Swan

We as an industry need to learn to prepare better for grey swans -- rare but very possible events -- both for our own sakes and for our clients.

As the U.S. steadily emerges from the pandemic -- and we all hold out hope for India -- the temptation is to dismiss it as a one-off, a once-in-a-century health disaster, a black swan. But the pandemic is actually what's coming to be known as a grey swan -- something that, while rare, relates to a known problem and that can be planned for, if we come to grips with the cognitive biases that blur our ability to see them.

As we've learned the hard way over the past 20 years, there are a lot of grew swans out there, so we as an industry need to learn to prepare better for them, both for our own sakes and for those of our many clients.

This report from Aon on dealing with grey swans' effect on corporate reputations includes a daunting list of those that have been broadly ignored over the past two decades, starting with the 9/11 terrorist attacks -- which somehow caught the world by surprise even though Islamic terrorists were known to want to strike in the U.S., even though plots had been uncovered to hijack and crash planes into high-profile targets or blow them up and even though terrorists had attacked the World Trade Center itself and tried to make it collapse eight years earlier (right across the street from my office at the time).

The dangers that a hurricane posed to the levees in New Orleans were well-known long before Hurricane Katrina devastated them. So were the perils of subprime mortgages -- a member of the Fed's board of governors saw the crisis coming so far ahead of time that he published an alarmist book in 2007 yet was largely ignored until after the Great Recession of 2008-9 began. The tsunami that caused the disaster at the Fukushima nuclear plant in 2011 was eminently foreseeable. And, of course, many had been predicting a pandemic for years before COVID-19 pretty much shut the world down starting last spring and killed millions -- Bill Gates even got most of the particulars of COVID right in a dire TED talk in 2015.

Why do we keep missing these grey swans?

Drawing on the seminal work of behavioral economist Daniel Kahneman, the Aon report lists six cognitive biases that cloud our judgment on risks more complicated than "white swans" -- which are common enough that we have clear data on them and routinely incorporate them in our risk management.

The biases are: the ambiguity effect (our minds don't like options with unknown probabilities); normalcy bias (we underestimate the likelihood and severity of disasters); optimism bias (we underestimate the probability of being affected directly); the ostrich effect (we ignore negative information to avoid the anxiety that comes with decision-making); herd instinct (we align with the behavior of a group to avoid conflict); and status quo bias (we prefer to keep doing what we're doing).

As the report explains, the ambiguity effect, normalcy bias and optimism bias "relate to our limitations as natural statisticians. We gravitate toward information that we can process and organize [while avoiding]... uncertain, ambiguous data.... To help us navigate through the storms of life, we tend to be optimistic about our chances. Despite knowing the health risks associated with smoking or obesity, for example, we believe that 'it won’t happen to me,' yet we buy lottery tickets equally believing that, 'it might be me!'"

The ostrich effect, herd instinct and status quo bias "relate to managing our emotional state. Evidence that conflicts with our rosy view of the world is uncomfortable and unpleasant.... It is easier to go along with the majority than stand one’s ground and cause waves."

So, how can we do better?

The report's conclusion: "Effective risk management strategies will acknowledge these flaws openly and institute measures to combat their most harmful effects."

It suggests considering, in particular, the possibility of "a large-scale cyber attack with physical consequences. Cyber physical risk is not new, but its threat is growing rapidly, as adoption of the Internet of Things (IoT) accelerates and increases the 'attack surface': the number of connected systems and devices through which an attacker can enter or extract data."

That kind of attack certainly seems plausible -- as the SolarWinds attack by Russia showed, nation-states have the ability to sabotage each others' infrastructure, such as electric grids, pretty much whenever they want.

The report adds: "We could turn our minds also to the 'green swan,' the term coined by the Bank for International Settlements to describe black swan events related to climate change." It's always hard to trace a disaster to climate change -- some will say the recent Texas freeze may stem from climate change's tendency to cause more extreme weather; some won't -- but the likelihood of green swans is certainly increasing.

One caution: I think the evaluation of disasters after the fact is often Monday morning quarterbacking: "It's obvious that we should have punted/shouldn't have punted," "should have passed/should have run," "should have seen that that player would be a star/a bust," etc. You can't just prepare for one grey swan and hope that's the one you should have headed off. You have to prepare for all the grey swans you can imagine -- you don't just fix the levees in New Orleans; you prepare for what hurricanes might do up and down the Gulf Coast.

That can be expensive. So, there has to be some real calculation involved based on the odds of an event, the likely cost of a disaster and the expense associated with avoiding all such problems -- and the nature of grey swans is that none of these figures are easily quantified.

All we really know for sure is that grey swans are occurring faster than we've expected and have been far costlier -- COVID-19 has cost trillions of dollars in the U.S. alone, and the devastation in terms of lives lost has been even greater. So, we'd do well to confront our biases and keep trying to make ever-more-realistic evaluations of the risks we're facing.

Stay safe.

Paul

P.S. Here are the six articles I'd like to highlight from the past week:

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

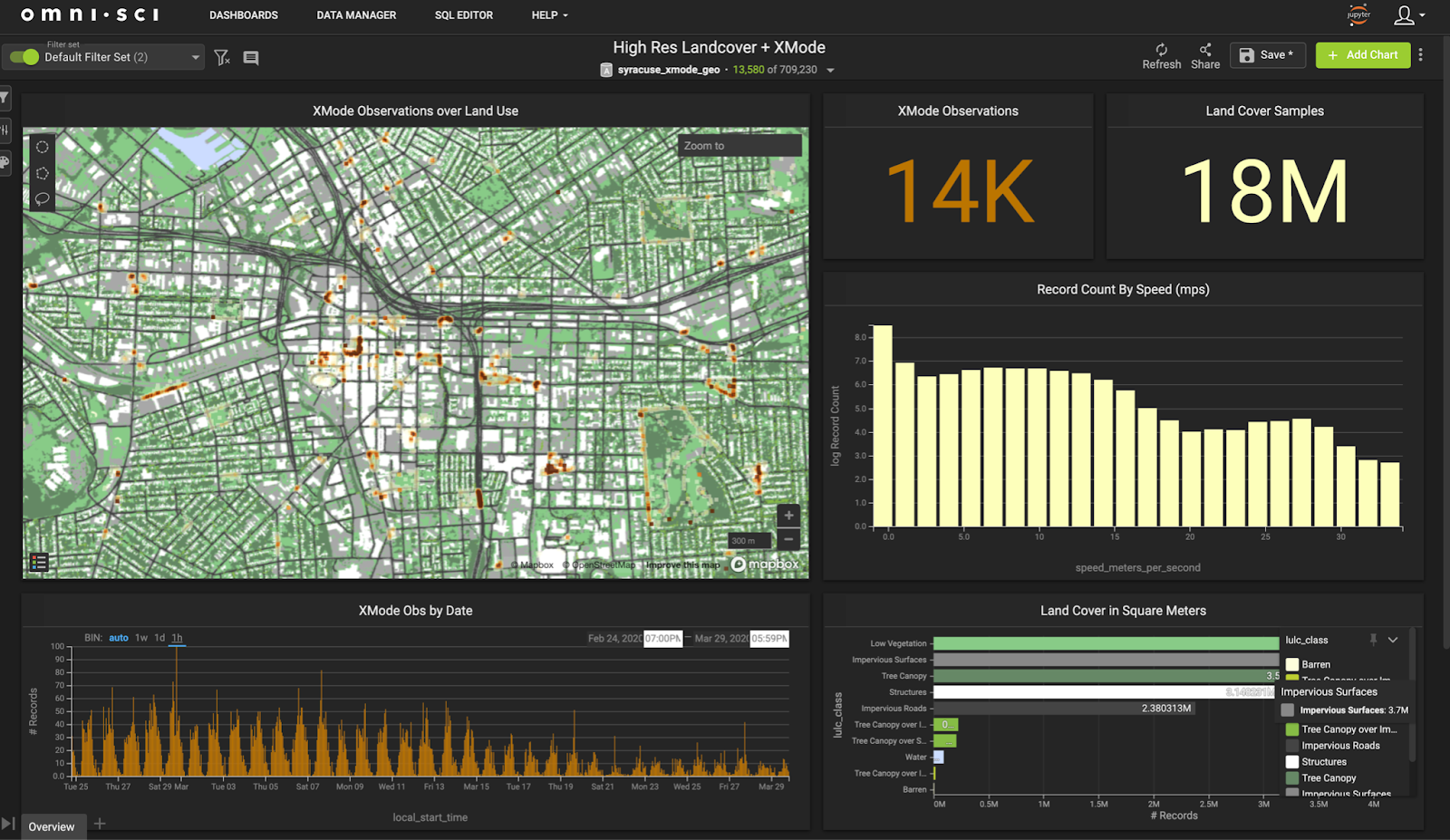

Figure 1: Granular GPS data combined with Machine Learning-derived 1m landcover allows transportation planners unprecedented insights into travel behavior (data courtesy of Xmode & Microsoft).

Knowledge is power. With the information now available at the fingertips of planners, traffic engineers and public safety professionals, more powerful methods are on the horizon to keep drivers, passengers, pedestrians, bicyclists and others safe.

If the insurance industry exploits this new trove of knowledge, the result can be fewer accidents, further declines in injuries and fatalities and a reduction in liability for everyone.

This new era in data-driven solutions can’t come fast enough. Globally, approximately 1.4 million people die in road crashes every year, or more than 3,700 each day, according to the Association for Safe International Road Travel. The Insurance Information Institute reports that speed-related crashes cost Americans $40.4 billion every year. Meanwhile, distracted driving continues to be a growing issue; in the latest Traffic Safety Culture Index report from AAA’s Foundation for Traffic Safety, more than half of drivers (52%) admitted driving while talking on a handheld cellphone at least once within the prior 30 days.

Traffic modeling used by departments of transportation is brittle and in need of updating. COVID-19 has contributed to this issue by forcing driving habits that will likely remain permanent. Commuting patterns and volumes have changed—and, with fewer cars, higher traffic speeds occur. On the urban planning side, concepts like parklets and bicycle lanes are taking hold; yet planners often work with 30-year-old data, along with parameters that are woefully behind the times.

A New Era in Data Analytics

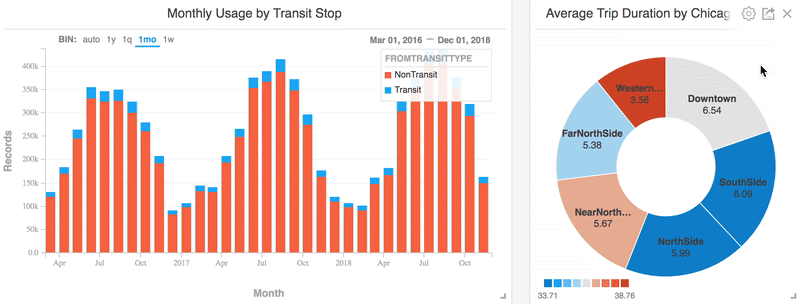

Figure 2: Bike sharing in Chicago and its relationship to public transit by neighborhood. Granular data allows transit planners to understand how new travel modes combine with existing ones.

Using data to increase vehicular and pedestrian safety is nothing new—but historically it’s had limitations. Traditionally, roadway data has been heavily aggregated from a limited number of sources. Road counters, for example, would give professionals traffic counts that amounted to a snapshot in time.

Geospatial data, by contrast, adds multiple dimensions to the art of ensuring safer roads, safer pedestrians and safer drivers. The most important change is that experts are now able to do analytics on disaggregated, granular data. Geospatial researchers are able to collect billions of records every month—not only traffic data but road conditions, event activity, accidents, weather, even what happens to vehicles as they move across networks. The science provides continuous, systematic visibility of factors over time and space.

By isolating, combining and cross-analyzing such massive datasets over time, researchers can investigate factors that play important roles. Police officers, for example, write reports hours after an accident has occurred, making accounts of road conditions at the time of the accident subjective. Through the use of continuous weather tracking, it’s now possible to roll back the data and pinpoint the impact of precipitation, fog, etc. to the very moment of collision.

Technology is making it possible to improve traffic safety in ways unimaginable just a few short years ago. Accelerated geospatial analytics allows analysts and planners to ask questions, and draw conclusions, from billions of lines of data, receiving those answers in milliseconds. This transformative capability lets professionals plot and visualize results, even for small or isolated areas.

Today, it’s practical to see how traffic is not only behaving in a single area, but also at the impact of different modes. Planners can investigate pedestrian activity, weather and other variables. If accident data causes engineers to look at a particular intersection, they can see the activity patterns around that intersection by time of day, day of week, holidays, commuting periods, even after a football game or other surge event.

The real-time component of geospatial analytics can be a game changer. Instant data, viewable nearly as soon as it’s collected, helps public safety departments plan their responses. In Austin, Texas, police, safety and repair crews were pre-positioned before a recent major rainstorm; the real-time analysis of changing flood patterns based on elevations, storm mitigation infrastructure, etc., was intersected with roadway maps to minimize accidents and damage. When public safety departments have knowledge of the street-to-street impact on traffic during sporting events, concerts, even public demonstrations or protests, the benefits to pedestrian and traveler safety can be remarkable.

Accelerated analytics also helps with forecasting. Trends in bike sharing is one way to gain a better understanding of how to redo a street. This kind of insight into shifting transportation modes, particularly in urban areas, can be a major help to planners who have to think not in terms of months or even years, but decades.

New analytics platforms with accelerated processing capabilities make it possible to achieve all these benefits, all within the same tool. Moreover, there are few barriers to adoption. Advanced geospatial platforms are based on GIS (graphic information system) standards, making it easy for conventionally-trained GIS pros to quickly get up to speed. On the hardware side, advanced processing capabilities may be needed, but that can be acquired as a cloud-based service at reasonable cost.

Cooperation Is Increasing

Scores of organizations and industry partners are working together to make the most of the revolution in geospatial data. The Safe Streets Initiative, among others, is helping to change the way professionals understand the human behavioral aspects of traffic management.

It used to be taken for granted that the safest way to plan roadways was to make everything straight, with wide rights-of-way and huge clearances. Today, planners know that such approaches cause people to race through an area, making travel more dangerous instead of safer. Street design, too, takes into account a great deal of contextual information about street surfaces, pedestrian movement, retail density and patterns, as well as alternative modes such as electric scooters. What works on one block may be counterproductive two blocks away — something that the human element often makes clear.

Another issue is the evolving nature of transportation. The rise of ride-sharing is causing planners to look for ways to support stops to pick up passengers without affecting safety. Electric cars, scooters and bikes are affecting design guidelines, as well, making standards from just a few years ago obsolete.

Perhaps most important to geospatial analytics is the way data partners are coming together. Participation varies widely and often involves negotiation, but many partners are stepping up their game. Electric scooter data, for instance, is widely available, and electric bike sharing businesses usually include data sharing in their agreements with municipalities.

A key benefit — yet in some respects, a drawback — of all this granular data is the massive datasets. Uber releases Transportation Analysis Zone (TAZ) data from its operations, which is immensely useful for broad-scale transportation planning, but the benefits of TAZ are less useful for design work because there can be a huge diversity of conditions within one TAZ. As a result, there is opportunity for new methods of identifying analysis units; real-time GPS telemetry might reveal large numbers of pedestrians and cars mixing in an area along with electric scooters, indicating the need for specific planning solutions.

Need for Carrier Involvement

There is a role for the insurance industry in advancing geospatial analytics. Carriers should consider doing some active data-sharing pilot projects that allow experts to not only get hands-on experience but also evaluate how systems work together. Best practices are still emerging, including how insurance data can integrate with other sources. Determining how those combinations can be analyzed in real time is something new for practitioners to consider.

Many concepts can be applied to these integrated datasets. Cohort analysis, a common technique that allows data about specific groups to be tracked through time, is nonetheless rarely used in transportation planning. This is a huge opportunity, as is the use of machine learning and artificial intelligence to identify present and future trends in cross-referenced data.

Pilot projects can be done in an agile manner, flexibly and at low-cost. Insurance companies should find ways to empower internal teams and departments to investigate and find new solutions that will benefit policyholders, safety professionals, transportation providers and the general public.

When public and private entities combine forces to improve society, good things typically result — and transportation safety is no exception. From improving traffic safety in an urban corridor and accommodating new forms of travel, to lowering instances of distracted driving and reducing fatalities, data sharing is a pathway to new insights and better solutions.

There is a fundamental need to update the cadence and the granularity of the most basic data about travel behavior, in all its forms. Geospatial analytics can be the engine that drives this new capability. Knowledge is power — and with the power of geospatial capabilities behind their design, our streets and highways can be safer and more intelligently designed than ever before.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Mike Flaxman, PhD., is the spatial data science practice lead at OmniSci. An expert with more than two decades of experience in the field of spatial environmental planning, Flaxman has founded or co-founded several spatial planning firms.

Environmental, social and governance (ESG) is a philosophy, not a catchphrase. A principle for the good of expanding principal, ESG is a chance for the insurance industry to do well by doing good. This chance is real, measurable and beneficial. This chance is, in other words, not chancy.

This chance is a matter of reducing risk, not increasing it; of insuring financial security, not issuing assurances in lieu of guaranteeing them; of building assets, not buying losing properties. Seizing this chance should be a priority for every insurer.

About financial security, about the chance for the insurance industry to make this concept a reality, about the chance for insurers to offer security without the double-dealing that plagues the securities industry, about the chance to free Main Street from the speculation and volatility of Wall Street, I write of what I know. That is to say, I believe in ESG because I refuse to do business without it.

Where environmentalism is unimportant, pollution is common. Where social activism is unacceptable, pollution of the soul is certain. Where governance is unachievable, pollution of society—wholesale corruption—is unavoidable.

These conditions are not, however, exclusive to Wall Street.

Just as the forces of nature carry contaminants from one place to another, just as what is tolerable in one place is toxic to another, just as what is commonplace on Wall Street is cancerous to Main Street, the only way to prevent a catastrophe is to redirect those forces that threaten the insurance industry; to force the winds to change course without harming individuals or institutions.

ESG is, then, a policy from which policies—insurance policies—follow.

Demand for these policies is substantial, which means insurance advisers can be true to their profession, advising clients on how to transform values into valuable commodities.

Advice starts with education, where insurers invest in themselves and their clients.

The ROI goes beyond the issuance and signing of policies, because the greatest return is an audiovisual experience. An experience of sound and sight, where truth resounds without interference and righteousness flows without interruption. An experience that echoes throughout the insurance industry, attracting admirers across the nation.

ESG’s timeliness does not detract from the qualities that make it timeless, as if environmentalism is ephemeral or social concern is seasonal, as if governance is a fad rather than a fundamental basis for freedom and private property.

The insurance industry has a responsibility to support ESG, inspiring others to do the same. Truth governs this responsibility, regardless of how popular environmental, social and governance is; regardless of how newsworthy this responsibility is; regardless of how much more remunerative this responsibility is than all other things.

ESG is crucial to establishing and maintaining trust.

ESG is also crucial to increasing trust, so the insurance industry can serve clients by protecting them.

ESG is a cause that demands our interest, defines our interests and determines the interest we earn.

A cause this great deserves an industry—the insurance industry—with a commitment to greatness.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Jason G. Mandel has spent over 25 years at the intersection of Wall Street and the insurance industry. Mandel founded ESG Insurance Solutions (www.esginsurancesolutions.com) in 2020 to help better integrate these two, often conflicting worlds Having a strong belief in ESG concepts (Environmental, Social and Governance), Mandel found a way of incorporating his beliefs in his business.

Representing only insurance carriers and products that he believes offer compelling risk management solutions and maintaining business practices that he can support, Mandel has led the industry in this ESG initiative. ESG Insurance Solutions serves some of the wealthiest families internationally, and their business entities, by providing asset protection, advanced tax minimization vehicles, principal protected tax-free income structures, employee retention strategies, key person coverage and tax-free enhanced retirement plans for their essential employees.

Over a year since the first shut down, and the windy road to a pre-pandemic world remains bumpy. For employers, this means responding to yet another COVID-19 occupational health concern arising from long-haul COVID-19 symptoms. These symptoms manifest in tens of thousands of individuals who survived the fight against COVID-19, only to be faced with lingering effects and symptoms, despite negative COVID-19 test results. In the medical field, this condition is called Post-Acute Sequelae of SARS-CoV-2 or PASC, also known as long-COVID-19 or long-haul COVID-19.

The Centers for Disease Control and Prevention (CDC) describes these symptoms as those that persist more than four weeks after first being infected with the virus that causes COVID-19. Long-haul symptoms include ongoing fatigue, “brain fog,” difficulty sleeping, loss of smell and taste, joint pain, shortness of breath, and coughing per the American Medical Association. These symptoms may also include palpitations, headaches, dizziness, muscle pain, anxiety, and depression.

The reason why some suffer these symptoms while others don’t remains unknown. In February 2021, the National Institutes of Health announced a $1.15 billion initiative to support research into the causes and ultimately the prevention and treatment of long-haul COVID-19. So while symptoms vary and long-hauler research is developing, the result on employers and the returning workforce remains considerable

Long-haul symptoms are surprisingly common. Surveys cited by the CDC - in a January 2021 Clinical Outreach and Communication Activity webinar - reflect the following:

35 to 54% of people with mild acute COVID-19 had persistent long-COVID-19 symptoms after two to four months.

50 to 76% of people reported new symptoms they had not experienced during the acute illness, and some had reappearance of symptoms that had resolved.

9% described their long-term symptoms as severe.

These statistics mean that the return to work process will be anything but simple. Employees afflicted with long-haul symptoms may require long-term disability benefits. Or, they may only be able to return in a part-time capacity or require modified work; and for those infected at work? If they have a previously accepted workers’ compensation claim, the virus becomes the mechanism of injury, rather than the injury itself, with secondary symptoms that arise from the original incident, like most other industrial claims. In these cases, the challenge for employees will be proving that the symptoms are related to the original COVID-19 infection.

But what happens when a workers’’ compensation claim wasn’t filed when the employee first tested positive? If the original COVID-19 symptoms were mild, for instance, it’s quite possible that an employee never filed a claim form – and since long-haul symptoms can arise months later, claim forms may be filed months after a positive test. Investigating these claims will prove much more challenging as contract tracing requires the employee’s recollection of activities engaged in months and months prior – which provides even harder for long-haulers with neurological symptoms and/or brain fog. Deciding to accept such claims then will depend on conducting late-stage investigation and may depend, in part, on whether one of the rebuttable presumptions applies to the original date of injury, all of which puts further pressures on California’s already stretched businesses.

In fact, the Workers’ Compensation Insurance Rating Bureau has estimated that California’s presumptions could cost workers’ compensation payers between $600 million and $2 billion, even though the typical COVID-19 claim costs less than $3,500.00, with the healthcare industries being hardest hit as 42.3% of all COVID-19 claims arise from this sector.

Another likely effect of late reporting will be the potential retroactive impact on Labor Code section 3212.88’s “outbreak” provision. The provision requires employers to keep track of all COVID-19 cases and report the highest number of employees who reported to work at the employee's specific place of employment in the 45 days preceding the last day the employee (who reports COVID-19 infection) worked at each specific place of employment. This is for the purpose of calculating “outbreaks” to determine if a rebuttable presumption applies. However, if a claim is reported months later and retroactively creates an “outbreak,” the impact could be staggering, particularly on previously filed claims which may not have qualified for the presumption based on the originally reported numbers.

When litigation arises, all parties will be challenged because of limited case precedent as long-haul symptoms arise well after the infection/diagnosis. Lyme disease and asbestos exposure cases, for instance, may prove useful but will not be definitive. Medical evidence will be absolutely necessary in any disputed case to tie the symptoms to the infection.

When these claims are first reported, a thorough medical history should be taken and special consideration should be given to occupational medicine or primary care treatment to manage the claim. Eventually and depending on the symptoms, a referral to internal medicine, cardiology, and/or pulmonary specialists may be made. Keeping the claim on track from the outset will be especially important for carriers and employers.

There is some reason, however, for cautious optimism as some long-haul symptoms are improved by vaccination; with 30-40% of long-haul sufferers noting some improvement post-vaccination, per Aikiko Iwaskio, a Yale immunologist . As COVID-19 vaccine distribution continues nationwide and overall infection rates drop, the number of long-haul sufferers will ideally decrease as well.

All in all, employers and carriers must tread lightly, as accepting a COVID-19 claim can have a significant impact, beyond the initial care and recovery. Handling these claims with watchfulness and caution from the very beginning is vital. Getting a thorough medical history and conducting as much investigation at the start remains key as well.

Get Involved

Our authors are what set Insurance Thought Leadership apart.