|

Six Things | December 14, 2021

A Wake-Up Call on Claims. Plus, employer trends shaping workplace; the future of the independent agent; what to understand about Gen Z; and more.

Discover 'The Future of Risk™': Innovation, Tech, & Disruption Insights from Industry Leaders!

A Wake-Up Call on Claims. Plus, employer trends shaping workplace; the future of the independent agent; what to understand about Gen Z; and more.

|

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

The future is going to include stronger insurer/distributor relationships. Agents want it. Insurers need it. Customers will benefit from it.

Well, now we know. Insurance’s direct sales didn’t drive the agency channel out of existence. It’s thriving. Customers still enjoy working with agents. Agents still enjoy working with customers and insurers. The greatest change brought about in the past few years is the steady retirement of Boomer agents and the increase in agency mergers and consolidations.

Insurers are now faced with the reality of competing for shelf space --- due to fewer agents, with a smaller crop of new agents to fill the void. Insurers are also faced with creating products and service processes that will fit the new generation of agents and the next generation of customers. Insurers need to become… digitally attractive. They need to fit with the flow. They need to bond with the agent.

It’s a two-way relationship. Independent agents crave great relationships with their insurers. A new Celent survey report, commissioned by Majesco, found that “those that make the placement decision (the leaders who choose the priority insurers for their agency) are very satisfied with the relationship with their current preferred insurer(s) — perhaps because…they are able to choose where to place the business and can choose to place it with the insurer they prefer.”

This is great news for insurers that work with independent agencies for both P&C and L&A. It means that, if they go through the hoops of creating a positive sales environment with processes that work and have reasonable pricing, agents will choose them, and the relationship will be the insurer’s to lose.

Inside the mind of the independent agent

Any insurer of nearly any type or size should be fascinated with the perspectives of independent agents. Because agents are still the largest channel for insurance sales, insurers need to keep tabs on what they are thinking and how they perceive insurers. Even for insurers with captive agents, agency service can be the make or break point of growth.

Majesco is interested in the agent and agency viewpoint, as well, so we regularly research all aspects of distribution management to keep our customers and partners ready for what’s to come. In August 2021, we asked Celent to execute a study on our behalf. Celent interviewed 231 captive agents, roughly split between one-third life agents, one-third P&C and one-third who carry a mix of both. The Celent report, Reshaping the Distributor Insurer Relationship, provides interesting insights … some of which will surprise you! We discuss the report results in a webinar that we encourage you to watch.

Today we’ll discuss a few of the agent insights in the Celent report across some very concrete details of the insurer/agent relationship.

Let’s listen to the agents and see what they have to say.

How does the agent like to communicate with the insurer?

Insurer/agent communication is complicated. Some tasks are straightforward. Others require nuanced communication. Some communication falls into the category of advice. Other communication requires equations, reports and varied presentation options. It shouldn’t be a surprise then that the question, “How do you prefer to communicate with your preferred insurer?” would need to be broken down into subsets.

When it comes to interaction preferences, Celent chose to solicit both the high-level view and to dig into interaction preferences across the varied functions of the broker/insurer relationship.

“The Silent Generation and Baby Boomers were more likely to prefer to use technology (for communication) than the younger generations," Celent found. "And surprisingly, almost 30% of Generation Z said they prefer to do everything via phone, email or in person rather than use technology alone to process business – the highest percentage across generations.”

Yes. You read that right. The older agents prefer to use technology to facilitate their communication, and the younger generations trend toward wanting to pick up the phone. Looking closer at the actual results, we see more of a middle road. Most agents prefer any and all forms of communication. In general, most agents like to use the technology to get started and then pick up the phone for confirmation or further discussion.

See also: Underwriting in the Digital Age

Digging a little deeper, we find out that younger agents are still in the learning cycle. They are most comfortable with a voice telling them something because it can be explained. As they mature in their positions, they will likely lean more on the efficiency of the technology and less on the expertise of the insurer on the other end of the line.

But, there’s another twist. Gen Z and millennials switch jobs and occupations more frequently than the Silent Generation, Boomers or even Generation X. Onboarding and educating agents needs to happen more quickly and with a more intuitive format. So, Celent’s suggestion is that insurers “can build additional tools, training and advice support into their portals.” They can build recommendation engines. They can consider gamification techniques for learning.

Are independent agents pleased with their preferred insurer?

Satisfaction varies widely. Agents who are empowered to place the business are most satisfied with their preferred insurers. (96% are very satisfied or somewhat satisfied.) But when the end customer is allowed to make the choice without agent involvement, only 84% of agents are very satisfied or somewhat satisfied. What will improve satisfaction throughout all groups is an overall increase in digital capabilities.

Which capabilities need to become digital?

Insurers have been investing in the future, many of them attempting to bring digital processes to the agency. Agents are expecting that these improvements will increase and cross all of their functions. For example, new business quoting is only considered by 40% of agents to happen digitally with their insurer. In the next three years, 59% of them expect to be able to quote using a digital process. License management would be an excellent place for insurers to grow their digital capabilities. Only 49% of agents seem to be using a digital process, yet 61% consider this to be an area their insurer should digitize in the next three years.

Agents are also ready for additional changes in policy inquiries. Though it’s a nice touch-base point with insurers, 60% of agents feel that they should be able to use more of a digital process in the next three years. Information on demand is an essential aspect for agents who need to win the business and keep the business.

Agency interaction is also variable based on P&C vs. life agents. The Celent report points out that their level of digitization isn’t equal:

“For property casualty agents, the five activities with the highest level of digital interactions today are getting reports, policy changes, renewals, compensation and commissions and policy inquiries. For life agents, the top five digital activities are getting reports, compensation and commissions, updating and managing licenses, policy changes and renewals. Property casualty agents are more likely to be handling policy transactions in a digital manner, and life agents are more likely to be handling agency management transactions in a digital manner.”

In all interactions, though, insurers are increasingly going to need to provide digital options.

Celent found: “Insurers need to be investing for the future. Agents have high expectations for increased digital interaction across all types of activities.”

How satisfied will agents be with insurers that make their lives easier?

It might be stereotyping, but if there is one thing that agents are good at it is thinking through a process and how to improve it. That’s the nature of selling. The person who sells has to think ahead for their clients, for their business and for themselves, tweaking pitches and processes to land the business and then keep it. This makes agents good at thinking ahead, envisioning and anticipating the outcomes of future scenarios.

For example, Celent asked agents about their preferences about policyholder self-service for certain tasks. The agents came back with more than data. They came back with insightful context regarding what should be allowed via self-service and what must be guarded for the security of the business. Celent also asked agents to look out into the future of their preferred insurer satisfaction. This is highly relevant to an insurer’s technology decisions, shedding light on the prioritization of service improvements over the next three years.

Celent said, “While agents don’t expect insurers to become significantly less effective, they do believe insurers will become more efficient. And although they expect more transactions to be automated, meaning less human interaction, they don’t foresee any negative impact on personal relationships.”

The larger the independent agency is, the more likely it is to view insurer technology as crucial.

Celent said: “Large agencies — those generating over $10 million of revenue annually — are 50% more likely to say they believe future investments will impact the insurers’ effectiveness in working with the agency. They also report an expectation that the personal relationship will improve, moving from 40% to 54%. Clearly, those insurers that expect to work with large agencies in the future will continue to face pressure to digitize their operations.”

See also: Building Your Digital Sales Arsenal

The case for catering to distributors

There are, of course, dozens of areas where insurers would be best-served to adapt now and reap the rewards later. Data makes its own case for a new approach among insurers. How can an insurer’s use of data dramatically improve the effectiveness of agents at the same time it reduces loss?

A great example would be the collection of agency data. Transactions tell stories. Is the customer at risk for shopping a policy around? Are they at risk for fraud? Customer touchpoints can potentially shed light on the past and the future. How closely aligned is the technology that resides in the insurer’s back office with the technology at the independent agent? Agents want technology that is easy to use. They want more help from insurers with their technologies. Is this desire a potential bridge into better use of transactional data?

What about communication channels?

Celent’s findings seem to indicate that insurers should be less concerned with pushing agents to use particular communication channels and instead prepare for the seamless use of all of them. Maybe this is the great takeaway:

The future of insurance is going to include stronger insurer/distributor relationships. Agents want it. Insurers need it. Customers will benefit from it.

Yet, many insurers aren’t ready to deliver on their part of the relationship. They need a fresh look at the benefits and the full opportunity. They need a road map on how to make the organization as attractive as possible to agents across most products and geographies.

In our next look at the Celent report, we’ll take a close look at insurer options. What is the best path forward for an insurer that is concerned about growing the business through agency partners? For another look at what drives agents and brokers, revisit my blog on “Consumer-Grade Digital Experiences for Agents and Brokers,” or view our webinar, "A New Digital Experience for Agents and Brokers."

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

Incumbent insurers and banks still seem in no rush to strengthen their currently weaker position to capture the value from Open Insurance.

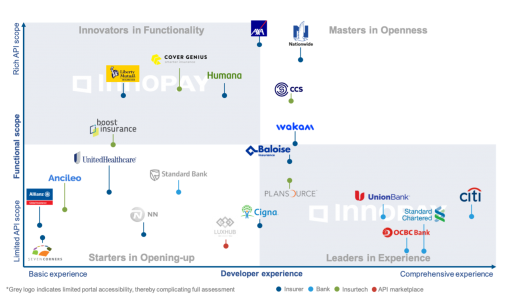

Open insurance continues to be the next game changer in insurance. The second edition of the INNOPAY Open Insurance Monitor, which keeps track of how the global Open Insurance landscape is evolving, reveals a rise in the number of insurtech players that are providing access by connecting insurers with digital ecosystems. Meanwhile, one application programming interface (API) marketplace has become the first in incorporating Open Insurance services in its digital offering. Based on our analysis of the findings, we can conclude that the traditional industry players – incumbent insurers and banks – still seem in no rush to strengthen their currently weaker position to capture the value from Open Insurance.

The Global Open Insurance Trend Is Expanding, Albeit Slowly

The updated edition of the Open Insurance Monitor includes several new players with insurance API propositions, both insurtechs and Open Insurance marketplaces. We can draw the following three key insights from the latest Open Insurance Monitor:

1. Insurtechs are entering the game

Most of the new entrants in this edition of the Open Insurance Monitor are insurtech players. They all offer "insurance as a service" that facilitates integration between insurers and third-party sales channels, with the developer portal environment as part of the offering. However, there is significant variation in the amount of functionality they offer, the level of developer experience and how they position themselves.

Boost and Ancileo, both located on the left of the spectrum, have a relatively small API scope focused on quotation, purchase and insurance policy modification. Although their developer experience is also relatively limited, they make up for it with clear API documentation that contains the necessary components for adequate interpretation and usage of the APIs. Meanwhile, Plansource offers benefits APIs as part of its complete HR solution to provide employing organizations a direct connection with insurance carriers for employees to have a seamless benefits shopping experience. The APIs include services for plan subscription and retrieval of relevant coverage data.

Another notable insurtech is Dutch-based CCS, which positions itself solidly on both axes. CCS has a wide API scope that covers multiple components of the insurance value chain, plus it acts as an API marketplace for its customers. Its developer experience is more advanced than its insurtech peers. For example, CCS offers proper developer usability features such as automatic onboarding, software development kits (SDKs) and app management and analytics functionality.

2. API marketplaces as a one-stop shop for insurance services

API marketplaces offer a variety of different API services from different providers, thus functioning as a one-stop shop for organizations that are looking to strengthen their capabilities through external APIs. The marketplace serves as a single integration layer, thereby reducing the implementation hassle.

LUXHUB is the first to integrate insurance services into its marketplace environment. It recently announced a new partnership with Baloise to provide mortgage insurance quotations directly to banks. As part of this new partnership, LUXHUB now publishes quotation and subscription request APIs on its portal. Although Baloise already had its own developer portal in place aimed at retail insurance, this partnership enables Baloise to directly integrate with core banking systems via the LUXHUB marketplace.

3. Existing players are not yet shifting focus

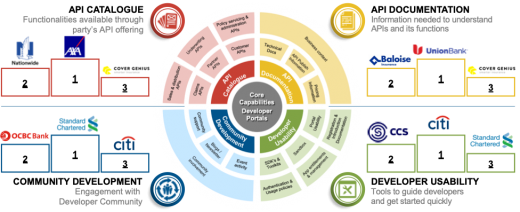

As highlighted in the first edition of the Open Insurance Monitor, insurers appear to be focused mostly on establishing their API portfolio, with their top priority being API documentation to allow developers to understand and use their APIs properly. There is little to suggest that insurers are shifting their focus toward other developer portal capabilities, while some extension of the API portfolio can be witnessed. For example, Nationwide has added several new API functionalities, including within its life domain, thereby moving closer to AXA as a functional innovator.

The same holds true for banks, whose superior developer experience is a result of their earlier Open Banking efforts. Their insurance-related API scope remains limited, but a few of them are improving their developer experience. For instance, Citibank has strengthened its developer usability with analytics and group role functionalities within app management and has enhanced community development by showcasing partner projects for inspiration. Meanwhile, Standard Chartered has launched an academy via its developer portal, where developers can improve their knowledge and skills on topics such as cloud transformation, APIs and emerging technologies. This feature is unique in both the Open Banking and Open Insurance space.

See also: Why Open Insurance Is the Future

Insurers Need to Start Deciding how to Compete Against or Benefit From Tech Players

The INNOPAY Open Insurance Monitor demonstrates that Open Insurance has been progressing slowly, but the presence of insurtech and API marketplaces in the Open Insurance space seems to suggest that the pace is accelerating. This presents incumbents with a choice: Fight the competition, team up with these tech-savvy new entrants or attempt a combination of the two. The "no regrets" move for insurers (and banks) would be to extend their own API portfolio and develop the necessary Open Insurance capabilities themselves. This would pave the way for an innovation platform that enables partnerships to be leveraged at scale. Insurtechs can play a role, for instance by providing direct access to a vast amount of different digital ecosystems for (white-label) product distribution. Because a wait-and-see approach is clearly no option, insurers need to carefully weigh up their choices and make the right decisions to safeguard their future position.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

"The industry is lagging far behind financial services and utilities providers when it comes to the digital customer experience," J.D. Power finds.

Digitizing the claims process has been one of the shining examples of innovation in insurance -- or so it seemed. But J.D. Power threw some cold water on that notion in a report released last week.

"The industry is lagging far behind financial services and utilities providers when it comes to the digital customer experience," according to the J.D. Power 2021 U.S. Claims Digital Experience Study. "Adoption remains stubbornly low. During the course of this year, just 40% of claimants interacted with an estimator via digital channels and only 47% made a claim via a website."

Martin Ellingsworth, executive managing director of P&C insurance intelligence at the market research firm (and a longtime contributor to ITL), said that "the insurance claims process has not really evolved beyond the launch of digital photo estimation three years ago.”

He said the heavy investments that insurers are making in straight-through processing will enable more adoption of digital claims management, "but, right now, there is still a great deal of room for improvement."

For me, the key finding of the U.S. Claims Digital Experience Study, now in its second year, was that telephone calls still dominate in the estimator phase and lower customer satisfaction.

"Just 40% of claimants interact with their claim estimator via digital channels, while 49% interact with their claim estimator via phone," the report said. "The average overall customer satisfaction score among those claimants who use the phone is 861 (on a 1,000-point scale), lower than in any other interaction channel. Use of video chat with an estimator is associated with the highest level of overall satisfaction (882), yet it is experienced by just 26% of claimants."

The report also found that "digital claims management tools are hitting their key performance indicators for the estimation process just 35% of the time" and that, not surprisingly, Boomers use digital claims tools less than Gen Y and Gen Z do and are, thus, less satisfied with the claims process.

You can certainly take a glass-half-full approach to the J.D. Power report and argue that having 40% of claimants interacting digitally with an estimator marks a sharp improvement over, say, five years ago, and I'm inclined to sympathize with insurers trying to make the transition.

But I share the J.D. Power report because it's worth reminding ourselves from time to time just how far we still have to go. We can't be congratulating ourselves just yet, especially when other industries keep driving digital adoption and setting an example that insurance customers demand that we follow.

Cheers,

Paul

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Paul Carroll is the editor-in-chief of Insurance Thought Leadership.

He is also co-author of A Brief History of a Perfect Future: Inventing the Future We Can Proudly Leave Our Kids by 2050 and Billion Dollar Lessons: What You Can Learn From the Most Inexcusable Business Failures of the Last 25 Years and the author of a best-seller on IBM, published in 1993.

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

Generation Z's appetite for personalized, digital-first experiences can unlock new revenue opportunities, both now and in the future.

Generation Z, or “Zoomers,” the cohort born between the late '90s and early 2010s, is widely known as the first “digital native” generation. They are also the least likely to purchase any form of insurance. Insurers should understand the unique coverage needs of Zoomers and how they interact with corporate brands to maximize long-term revenue growth and customer retention.

Zoomers don’t buy a lot of insurance. They typically do not own homes, have dependents or own vehicles, and they are generally in good health. Many already have some coverage from a family member’s policy anyway.

Same Products, New Value Proposition

Nevertheless, older Zoomers in or entering adulthood do need various types of insurance -- it may just look a little different. It’s the industry’s job to help these young people understand the benefits of coverage. Their appetite for personalized, digital-first experiences can unlock new revenue opportunities, both now and in the future.

Let’s take life insurance as an example. Most Zoomers skip life insurance because they don’t have dependents, making it difficult to justify the cost of the policy. But what if we presented an alternative value proposition?

Life insurance marketing often focuses on financial protection for a traditional family structure. A socially conscious twenty-year-old is far more likely to purchase a life insurance policy if it is marketed as an inexpensive and customizable way to support a particular cause and leave a legacy.

Some innovative carriers are even marketing life insurance as a way to buy a tattoo for a friend, pay for an environmentally conscious funeral or send a friend or family member on a trip to Europe. In this way, life insurance is positioned as an act of love. Most importantly, the customer feels like he is in control.

Personalized messaging, at different points of life, is key to filling generational gaps in coverage. By crafting an alternative value proposition, insurers can turn Generation Z into their most valued customers.

Generation Z’s Unique Characteristics Spell Opportunities to Deliver Personalized Experiences

Between growing up amid the Great Recession and experiencing the COVID-19 pandemic in late childhood or early adulthood, Generation Z’s confidence in life planning and financial security has been shaken. Indeed, workers under age 25 were 93% more likely than workers over 35 to be laid off during the pandemic, contributing to lost insurance coverage.

As a result of these experiences and their ability to easily find information online, Generation Z is highly price-sensitive. 60% of Zoomers said price was the biggest factor when choosing which brand to buy from. Young people today are savvy consumers -- comparing prices, identifying discounts and reading reviews.

“They don’t want to pay full price for anything,” says Jason Dorsey, a Gen Z consultant and researcher.

The implications for insurance are clear: Insurers that offer both lower prices and price transparency will attract post-millennials.

“Offer lower prices” is easier said than done and has been a priority long before Generation Z. Instead, where insurers can really shine is in offering the right product at the right time to the right user.

For example, Generation Z is the most likely to celebrate their pets’ birthdays (81% do, according to a recent survey!) and treat them like a member of the family. How likely might they be to purchase pet insurance from an insurer that offers discounts and rewards on their furry friend’s birthday?

With the recent turmoil in the job market, many Zoomers are turning to gig work full-time. The growth of the gig economy means health, dental and life coverage traditionally offered through employer plans must be provided differently. Gig workers often seek untraditional terms for the insurance products they purchase, in some cases day-to-day or gig-to-gig.

While Gen Z is highly price-sensitive, this is balanced by their increased comfort with sharing personal data in exchange for discounts and personalized policies. This opens up a massive window of opportunity for insurers to deliver personalized experiences to this demographic.

Insurers that can provide on-demand, flexible coverage of key products, with simple self-service options and real-time quoting will find great success serving this underserved market.

Nudging the Health-Conscious Generation

Generation Z is the perfect consumer for life and health insurers. According to a UNiDAYS survey:

Insurers that leverage health and activity data to offer rewards and discounts can expect a high level of engagement from Generation Z. This generation embraces relevant technology and prioritizes their physical and mental health.

Wearables, like the popular Fitbit or Apple Watch, can help customers track various health indicators such as physical activity, heart health, sleep and nutrition. Insurers can then leverage this data to send coaching triggers via a digital assistant to encourage healthy behavior based on customer goals through personalized multichannel notifications via mobile, web, email, etc.

This technique is called nudging. Nudging is a behavioral science approach that uses subtle interventions to help users make better decisions while respecting their freedom of choice.

Using the same platform, insurers can offer timely discounts, recommend additional coverage and suggest more personalized policies based on the customer’s unique characteristics identified through health and behavior tracking.

Sun Life’s digital assistant, Ella, gave clients 15 million nudges in 2020, leading to an 83% increase in additional coverage purchased. Carriers that adopt nudging and behavioral analytics will maximize customer engagement and increase revenue.

Maximizing Digital Engagement Among Gen Z Consumers

Gen Z is known to be less likely to display brand loyalty, meaning they will happily switch from one insurer to another that offers lower prices. However, Gen Z is more likely than previous generations to be enthusiastic about a brand, engaging via digital channels and providing valuable insight into the marketplace.

Recent research from IBM shows that, if given the opportunity, 44% of Gen Z would submit ideas for product design and 36% would create digital content for the brand. When they share opinions online, they offer 2X more positive feedback than complaints. Gen Z, due to their digital literacy and shopping habits, are also highly influential in family spending.

While the benefits are clear, they come with high expectations. Post-millennials will switch insurance providers in a heartbeat if they are not provided with an always-on customer experience on their preferred platform.

See also: How to Market to Different Generations

When shopping for insurance online, Zoomers will compare multiple options by “parallel browsing” (having multiple tabs open at once). Insurers must adapt to this behavior by encouraging the user to remain on their website or app. Aside from the price itself, Zoomers reward clarity of information (i.e., “apples to apples”) and instant quoting that simplifies their research.

A recent Gen Re survey of Zoomers in Germany found that most respondents found insurance to generally be “non-transparent, difficult to comprehend and untrustworthy.” This generation is not easily swayed by polished marketing campaigns. Instead, they seek authenticity and integrity.

Insurers should also structure their digital presence to “coach” users through the insurance purchasing process, articulating why each step is necessary. One recent survey shows that many Zoomers do not have life insurance because it seems too complicated. Trends such as accelerated underwriting (AUW) and digital assistants can drastically improve the customer experience and speed the purchasing process.

Of course, a great mobile-first experience is essential. Zoomers are on their phones day and night!

The Window of Opportunity Is Open

There is no one-size-fits-all solution to engaging Generation Z. It’s actually the opposite: Post-millennials expect an always-on, personalized digital experience from the brands they interact with.

To be successful, insurers should be prepared to engage with Gen Z across multiple digital channels, offer more flexible policies and articulate a value proposition that is aligned with this generation’s appetite for risk, their increased social consciousness and their hunger for transparency and authenticity.

As Gen Z matures, they will establish their tastes and preferences as consumers. Insurers that prioritize the needs of this generation will not only establish themselves as trusted insurers to an aging Gen Z in the future but will be even more influential to older generations today.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Stephen Boucher is an account executive at Global IQX, the leading provider of AI-driven sales and underwriting solutions for the group insurance industry in the U.S. and Canada. He writes about emerging technologies, digital transformation and artificial intelligence.

In this whitepaper, we explore how conversational AI can create a better customer experience, improve agent productivity, reduce contact center traffic, and more.

Companies worldwide will spend more than $400 billion on call centers in 2022, and insurance companies will be among the big spenders – all to deliver an experience to customers that no one would consider optimal.

Customers are frustrated at all the forms they need to fill out as they deal with insurers and all the paper they need to shuttle around. They bristle when they deal with one part of the company and then find they have to start over when dealing with another, or when they get one sort of communication from, say, an agent that feels and sounds very different from what they hear and receive from a rep in a call center.

Fortunately, a form of artificial intelligence known as conversational AI is allowing companies to greatly improve the customer experience while slashing costs.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Creative Virtual is a conversational AI leader recognized in the industry for our nearly two decades of experience and unmatched expertise. Our innovative V-Person™ virtual agent, chatbot, and live chat solutions bring together humans and AI to deliver seamless, personalized, and scalable digital support for customers, employees, and contact center agents. Leading global organizations rely on our award-winning technology and expert consultation to improve their support experience, reduce costs, increase sales, and build brand loyalty. Our global team and extensive partner network support installs around the world in over 37 languages, providing both localized collaboration and international insights.

The COVID-19 pandemic changed how we sell insurance and rewrote the role of the independent agent forever.

COVID-19 changed how we sell insurance and rewrote the role of the independent agent forever.

Many agencies took significant time to adapt to the pandemic and ran into challenges from communication to management -- especially because many weren't built to support remote work. The challenges manifested in many ways, such as not having a web-based phone system (which makes remote work more accessible) and feeling the agency needed to have employees in the office for customers paying with checks and cash. The challenges resulted in lost production, leading to lost revenue -- and sometimes lost jobs.

The solution was clear. It was time to embrace disruption and innovate. Clearcover surveyed about 500 independent insurance agents and brokers in 2021, and 89% said they made significant changes to their businesses to weather the pandemic.

Insurance agencies that embraced digital innovation and those that reevaluated how to work with independent agents are seeing success. Agencies that had already embraced digital processes, such as customer e-signatures and customer text messaging capabilities, described being forced out of their offices as a "natural transition they had accidentally been preparing for."

The agencies that weren't so prepared brought determination and flexibility to the table. Several start-up agencies told us the pandemic accelerated their business. Because they were new, their systems and book of business were, too. They could easily pick up digital processes and take advantage of a fresh group of prospects that were now looking for a digital agency to help them with their insurance needs during the pandemic. Many had not yet established a physical location and decided to permanently work as a virtual agency instead of incurring the cost of rent for office space. Funds could instead be used to purchase digital leads, boost website and social media presence or hire additional staff.

See also: When Captive Agents Go Independent

Moving forward

Overall, agents reported that the pandemic doubled down on insurance customers' demand for more digital tools, which means independent agents can continue to navigate the disruption successfully by partnering with a digital-first carrier like Clearcover. Those that are successful are also requesting digital marketing solutions (e-flyers, social media content, etc.) to help support customer acquisition.

The most successful agents will be the ones thinking about "what's next." They're the ones who share an exciting new initiative they are launching in their agency when we check in with them. For some, it's a social media play, hiring additional staff or finding new ways to engage with traditional lead channels in a more digital manner -- for example, creating a digital referral program with mortgage lenders or maintaining networking relationships via virtual coffee meetups.

The most successful agents stay engaged. They continue engaging with our sales managers digitally, whether on the phone or through our virtual consultations or our agent chat support team. They use digital resources to understand their business results and stay updated on product enhancements. As COVID-19 continues to shape our industry, these two things are clear: Innovation is driving success, and the agents who innovate to create exceptional service are invaluable.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Kaitlyn Taylor is the director of agency accounts at Clearcover, the tech-driven car insurance company. She currently oversees the distribution through Clearcover's growing independent agency channel.

You may be setting the bar too high for third parties. You may be insisting on "one-size-fits-all." You're surely doing too much manual work.

Third-party insurance verification ensures a vendor or a business partner’s insurer can actually pay for losses or damages. Contracts obligate business partners to maintain some level of coverage, but enterprises have to verify that third parties carry at least enough to protect them from exposure.

Verification is a slow, painful, complicated back-and-forth process that mostly produces marginal results, and some of the enterprises we've talked to say it's just not worth the hassle of chasing down every single one of their partners to verify their insurance.

Here are three common mistakes that enterprises make that cause unnecessary friction and frustration with their third-party insurance verification program.

1. You’re Setting the Bar Too High

From a compliance standpoint, enterprises feel more protected when their legal or risk management team(s) set third-party insurance requirements, but these professionals often err on the side of extreme caution. In doing so, they end up making it nearly impossible for most third parties to comply with their standards.

A research report by Evident found that, for the average enterprise, 75% of third parties -- including vendors, suppliers, franchisees and other partners -- fail to meet contractual insurance requirements. Our data shows that 4% of the third parties that were non-compliant had decided they no longer wanted to meet the company’s insurance requirements for one reason or another. More often than not, compliance would have cost more than they’d actually make from doing business.

There should, ideally, be a trade-off between compliance and coverage. If an enterprise is experiencing lower-than-average compliance rates and losing interest from desirable third-party partners, the enterprise needs to take a long, hard look at their requirements.

Businesses need to strike the right balance between adequate coverage and ability to demonstrate compliance to develop criteria that incorporate not only legal and insurance needs but also business operations. The goal for most risk managers or GRC program operators is to achieve close to 100% compliance, but if the actual figure is closer to 25% (as our data suggests) then there needs to be a right-sizing of insurance requirements.

Start by assessing your partner portfolio and their respective coverages to identify the highest risks, then review any rules or coverage amounts that usually result in an exception request, as these are good indicators of areas where third party partners get stuck in the verification process.

2. You’re Taking a 'One-Size-Fits-All' Approach

Businesses have different expectations for third-party partners, so supplier risk profiles will naturally vary. There’s a strong need to accommodate this variance by instituting a unique set of insurance requirements for each supplier category, but, in most cases, risk managers avoid going this route because they’re worried about adding more manual tasks to their daily operations.

Most corporate risk managers have just one or two blanketed sets of insurance requirements for all of their third parties, which means they’re already using excessive manual intervention because they’re constantly making exceptions and overrides so that their preferred suppliers can continue to participate in their network.

Evident’s average customer has roughly 23 sets of third-party insurance compliance criteria, but some of our customers, like grocery store chains and supply chain businesses, have more than 50 sets of compliance criteria. And it makes sense – you wouldn’t want your IT firm to prove they meet the same set of insurance requirements as your office snack vendor.

A recent study indicated that 42% of businesses are still assessing their third parties using spreadsheet-based questionnaires, and 65% of these respondents are either unsatisfied with this approach or neutral about it. Automated technology solutions offer a robust alternative to accommodating third-party risk variants that’s both safer and easier than using spreadsheets.

See also: Navigating the Future of Risk Management

3. You’re Doing Too Much Manual Work

The burden of tracking down certificates of insurance (COIs) from vendors, suppliers, business applicants, franchisees and other third-party partners typically falls on the risk management team, and, while the goal is a 100% response rate on COI requests, the actual response rate is more like 30% to 40%. Of those who do respond to requests, the ones that are able to demonstrate compliance with the company’s insurance requirements make up an even smaller percentage.

Even if a risk management team obtains a COI, they’re either manually reviewing it themselves or hiring someone else to do it. Either way, it’s an error-prone and inefficient process. It’s also only half the battle, because simply having the COIs on file is not enough to avoid liability. Risk, legal and compliance teams also need to continuously verify that the COIs they’ve collected are valid, up to date and authoritative.

Enterprises are spending too much time and money on manual processes to verify third-party insurance. The insurance industry isn't well-known for its quick adoption of cutting-edge technology, but COIs aren’t going away anytime soon, and we need to have a combination of processes that aren’t clunky and outdated so they can meet today's business needs. Risk managers that let COI tracking technology do the heavy lifting have a lot more time to spend examining and improving the insurance programs that they’ve been hired to manage.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

David Thomas is the CEO and founder of Evident. He is a cybersecurity entrepreneur and industry expert, having held leadership roles at market pioneers Motorola, AirDefense, VeriSign and SecureIT.

While digitizing has improved customer experience, sped service and cut costs, it also opened opportunities for bad actors to commit fraud.

Insurers have offered some level of digital capabilities for sales and service for years, but customers’ and distributors’ adoption has been slow. When the COVID-19 pandemic emerged, carriers had to evolve their digital offerings seemingly overnight. While this shift to digital improved customer experience, sped up service and policy issuance and cut costs, it also opened up opportunities for bad actors to commit financial and identity fraud.

Strong digital capabilities mean insurers also need strong identity verification and fraud mitigation capabilities. The best way to keep the security up to date is to think of it as a continuous process, with regular evaluation of the defenses and enhancements or deployment of new solutions when necessary.

The Rise of Digital Interactions

Insurance customers, like those in other financial areas, are at risk of identity theft. In most cases, this happens through a large-scale data breach, but it may also occur when a family member fraudulently purchases a policy, for example. As more interactions occur digitally, the number of fraud instances rises.

Aite-Novarica Group research shows that more than 75% of carriers across life, personal and small commercial lines of business saw more digital activity from customers for both underwriting and claims in 2020. Underwriting data submission is seeing online activity grow significantly. For half of insurers, the rate of digital data submission grew by 50% or more from the year before.

Other drivers of higher digital activity for life insurers include the adoption of electronic health records for use in underwriting, changing the way agents and customers interact. In personal lines, inspections can be conducted virtually, and artificial intelligence can help assess property or vehicle damage and move the claims process along independently.

This higher rate of digital transactions is expected to continue, bringing in a new era for insurance carriers. While this shift is largely due to the pandemic, it’s also related to consumer preferences. Younger purchasers are increasingly buying goods and services across industries online, and older customers have familiarized themselves with these methods more during the pandemic.

See also: Innovation in Fraud-Detection Systems

Emerging Risks

While digital interactions improve the customer experience, they also make carriers and policyholders vulnerable to a new level of risk. Sixty-seven percent of insurers noted that they have seen a higher level of fraudulent activity as a result of their increased digital traffic. Fraud has increased nearly evenly in three main areas: the point of application, the point of account access and the point of payment.

Account takeover is of high concern for life insurers; the lack of advanced identity security available at call centers serves as an opportunity for those looking to commit fraud. They might call saying they forgot their policy number, then answer security questions with stolen personal data and reset the account password to take over the account fully. Property/casualty insurers have noted a rise in claims fraud through illegally obtained policies.

Multilayered Approach to Minimize Customer Friction

Insurers should ensure their fraud mitigation and identify verification processes provide a smooth customer experience while also protecting all stakeholders from advanced fraud tactics like synthetic identities and stolen personal information. This should involve a multilayered approach that spans both functional areas and capabilities, assessing gaps and strengths. A multilayered approach requires merging data from all available sources, combining fraud solutions and increasing security controls based on specific user information. Multifactor authentication, digital fraud risk scores and link analysis can all help insurers address fraud risk. No single technology will detect and prevent all fraud, but, rather, a combination of solutions and coordination across functional areas will bolster defense throughout the policy life cycle.

To learn more about how insurers are combatting the increased fraud activity emerging with digital capabilities, read Aite-Novarica Group’s full report Insurance Fraud: Rethinking Approaches in the Digital Age.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Manoj Upreti is a strategic adviser at Aite-Novarica Group. He has 15 years of experience in product development, market research and digital transformations in the life insurance, annuity and retirement industries.

IoT comes into focus. Plus, dramatic shift in underwriting ahead; premature failure in CPVC pipes; 5 trends to watch in commercial auto; and more.

|

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.