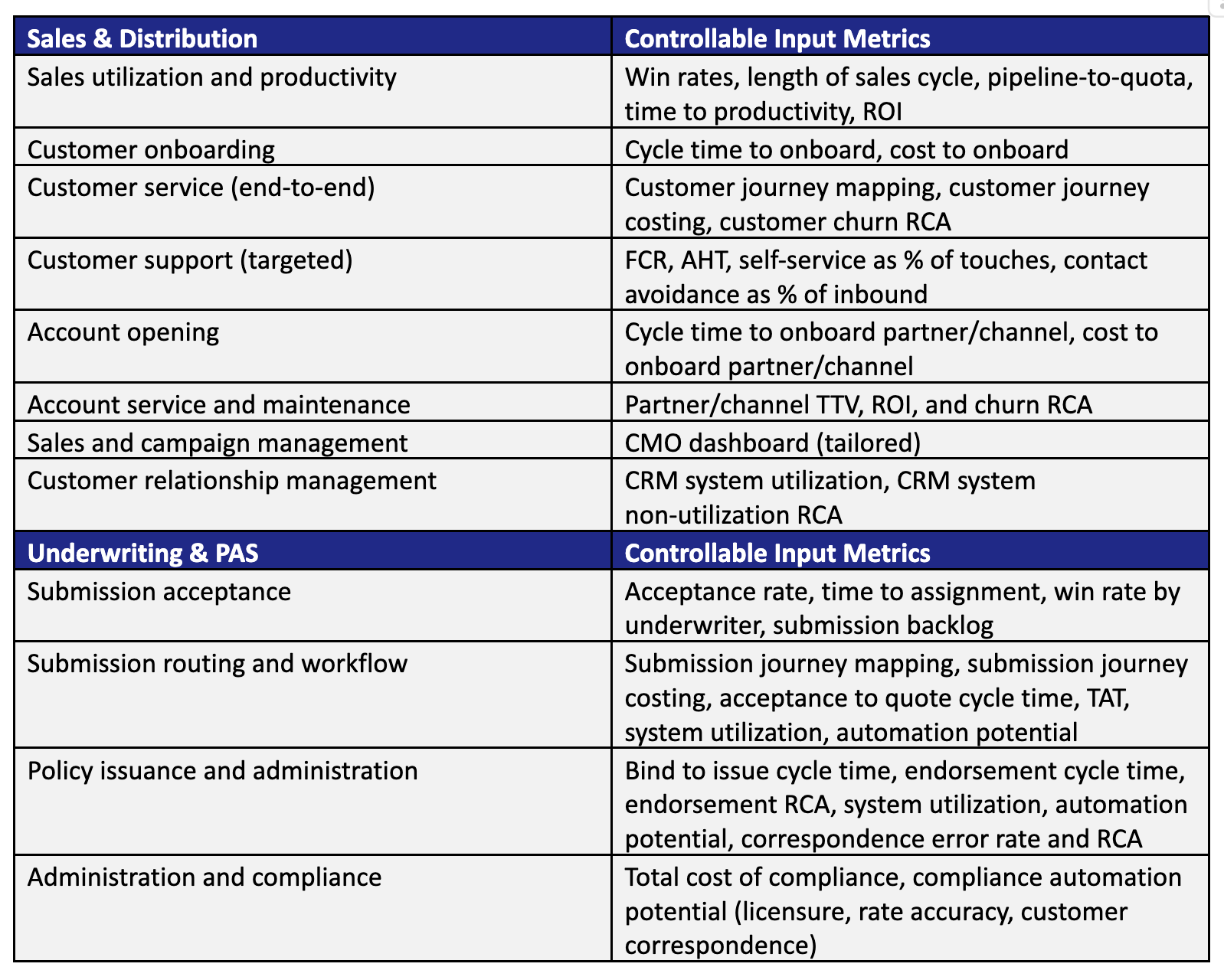

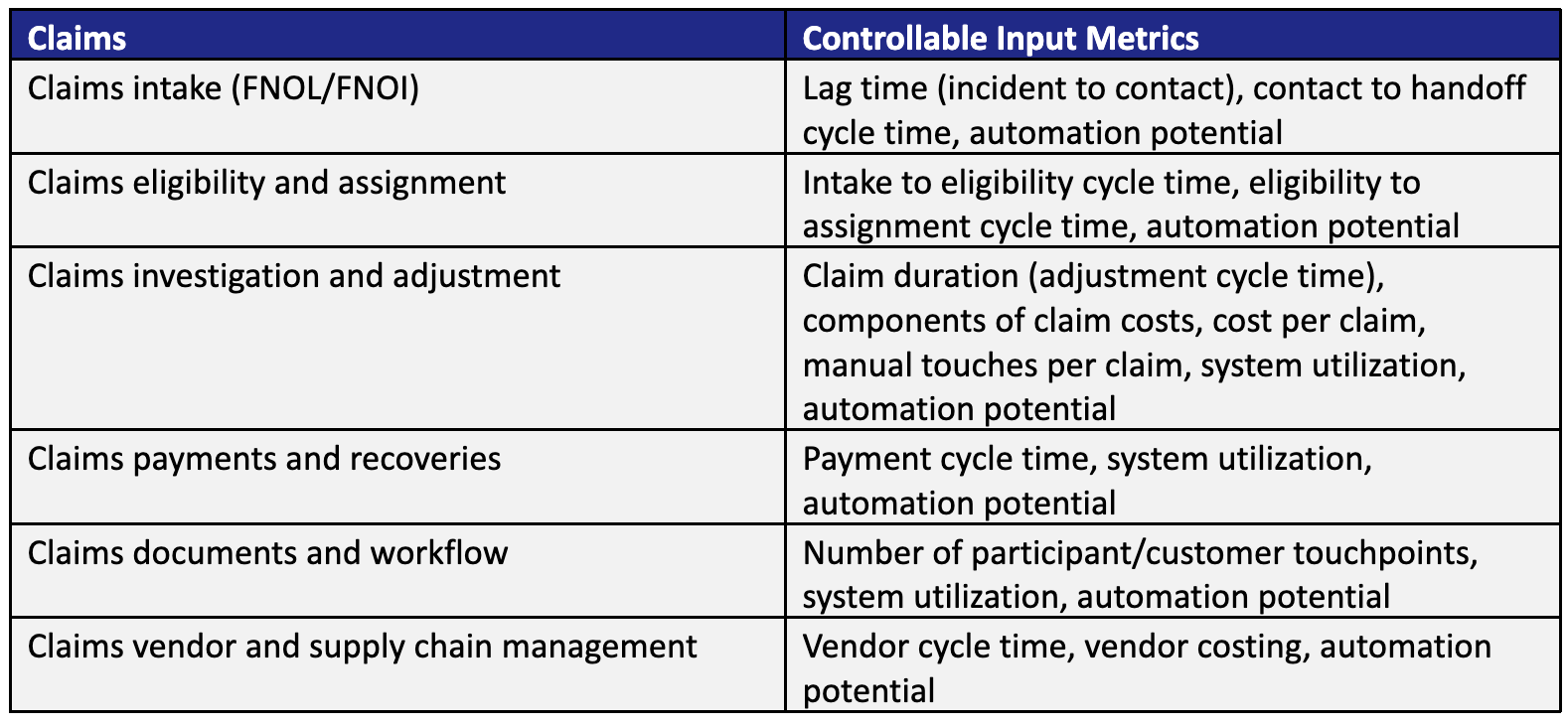

Fifteen years ago, I was working for a company with offices in California, New York, and London. I was at a conference in the U.S. My wife was back in London, with our three young children while overseeing the renovations of our 300-year-old house.

While I was away, the kitchen ceiling collapsed, bringing down with it an old water tank and soaking everything in dirty water. The au pair quit the same day. I hadn’t been in touch for 48 hours. My wife didn’t even know where I was staying.

So she sent an email to Matthew Grant – expressing some frustration that I hadn’t called and needing sympathy for the troubles at home. An hour or so later, she received a response:

“I’m sorry but I don’t know who you are.”

She saw red.

How dare I pretend not to know her because I was at work and she was having a hard time? She shot back a response:

“You B@st@rd, how dare you ignore me just because I’m having bad day. Who do you think you are?”

A few minutes later, she got a reply

“No, I really don’t know who you are. I am not your husband. But I do hope you sort out your troubles.”

She looked at the email address she had used. She had indeed sent her original email to Matthew Grant at Hotmail. Just not to the right Hotmail address.

We laugh about it now, but we both learned something about communication that day.

See also: Life Insurers' Communication Problem

Don’t be a stranger…

I was reminded of the comment, “I don’t know who you are,” when looking this week at the backlog of all the people who have asked to connect to me on LinkedIn.

I have a something of a love/hate relationship with LinkedIn.

We use it a lot at InsTech for sharing information about what we are doing and what our clients and members are up to. It’s a great way to share longer-form articles, event information, and links to our podcast episodes.

But none of us can control what the LinkedIn algorithm does with its content. Despite being selective about whom I open up my network to, I still get too much irrelevant information in my feed. And I get a lot of strangers asking to connect.

LinkedIn favors people from our connections when it shows us content, so one way to manage the quality of what we see is being thoughtful about whom we agree to connect with.

I also still believe in the original concept of LinkedIn, that connections are people in your network whom you know and whom you have a connection with in the real world outside of the platform.

I realize this may be more of a personal pet peeve, but I suspect I am not alone. Some people value the quantity of their connections on LinkedIn in the same way others value the size of their bank accounts. I’m not judging that approach if it works for you. For me, personally, I have a bias toward the quality of my connections.

I tend to get four types of people asking to connect. You probably do, too:

Type One – People I know. A pleasure to be connected, thank you.

Type Two – People I don’t know but who send a message explaining why they want to connect. I almost always respond to those and accept.

Type Three – People from companies that are already clients or who are likely to be buyers or users of our services, or the services of our clients and members. If you work for an insurer or a large technology company, or are an existing client, or perspective client, we need more people like you in our network. Thank you.

Type Four – People I don’t know and whose employers I don’t know. These people offer no message or explanation about why they want to contact. If I don’t know you, how do I know how I can I help you, or what I have I done that brought you to me? Sorry, but that will be a “decline.”

See also: 3 Steps for Insurers to Keep the Human Touch

Managing the communication overload

We are overwhelmed with the need to communicate today. Sometimes we spend too much time in “receive” mode and neglect the effort we spend in “transmit” mode. We respond to what is present, not what is important. We can write quickly, but we suffer regret slowly.

Can I offer some advice that might help make sure you are not the stranger and may reduce the likelihood of a small communication catastrophe?

Lesson One: Double check the email address before you send.

It’s too easy to send an email to the wrong person. I suspect you have done it more than once. I have. Most email tools use text prediction to complete the email address you start with. There are lots of Matthews out there. Are you sure you have the right one?

Lesson Two: Never say anything in an email you write that you wouldn’t want the person you are writing about to read.

Assume that any email you write about someone will be sent to that person. Because that will happen one day. It’s Murphy’s Law. If something can go wrong, it will. Harsh words said in haste can’t be taken back, and they are really hard to recover from.

Lesson Three: Who are you? Introduce yourself when requesting a connection on LinkedIn.

If you want to get someone’s attention on LinkedIn, take the time to say hello and introduce yourself. Tell them what they have done that has caught your attention. Don’t make the first contact be a pitch to sell something.

Lesson Four: If you travel and have someone waiting at home, check in every single day.

A phone call is best. Otherwise a text, WhatsApp, or email at least shows you remember them. It’s not every day something troubling happens, but each day does have something worth sharing, the good and the bad. These are the small parts of our day that may be forgotten or seem not important 24 hours later but which form the broader tapestry of how we experience our lives. That daily contact is part of the vital glue that holds us together.

I am still married to Mrs Grant. Occasionally, the other Matthew Grant does still get emails. I’m assured the offer to book flights to go on holiday in Bermuda that he received was entirely accidental.

Four suggestions. Take them or leave them. If you have read this far, then this is one communication that has succeeded. That’s good enough for me.