Through creative destruction, weak businesses shrink and stronger ones expand. The ripple effect of all that disruption often washes ashore at group long-term disability (LTD) insurers, where disability claim costs tend to increase during recessions -- new claim submissions rise while claim recoveries fall.

Sadly, studying the effect of past downturns on group LTD isn't entirely straightforward. Every economic decline comes with a unique context -- a tangle of related causes and effects, all of which can affect LTD claims in different ways. And because the economic shock of 2020 was created by a global pandemic and not a financial crash or inflation scare, COVID-19's implications are especially difficult to unwind.

Disability carriers still need to try.

Understanding the Three R's...

The three R's are a good place to start. I'm not referring to reading, writing and 'rithmetic but to the three rates that drive LTD experience: incidence rates (new claims), termination rates (closed claims) and interest rates. When it comes to these R's, carriers should avoid the temptation to look too intently at the past for clues to the future.

To understand why, consider the lessons of the Great Recession of 2008. This decline was caused by a financial contagion -- a liquidity crisis brought on by subprime lending. This led to a contraction in most sectors while the typically recession-resistant "HUGE" sectors (healthcare, utilities, government and education), in fact, grew. New claim submissions initially dipped as employees deferred claims in a bid to cling to employment or lost jobs too abruptly to file claims.

Eventually, however, new LTD claims rose and remained elevated for years before returning to pre-recession levels. Claim termination rates, too, deteriorated during the recession but rebounded quickly during the recovery. Lastly, an increase in asset defaults and lower portfolio yields strained the income statement of LTD insurers.

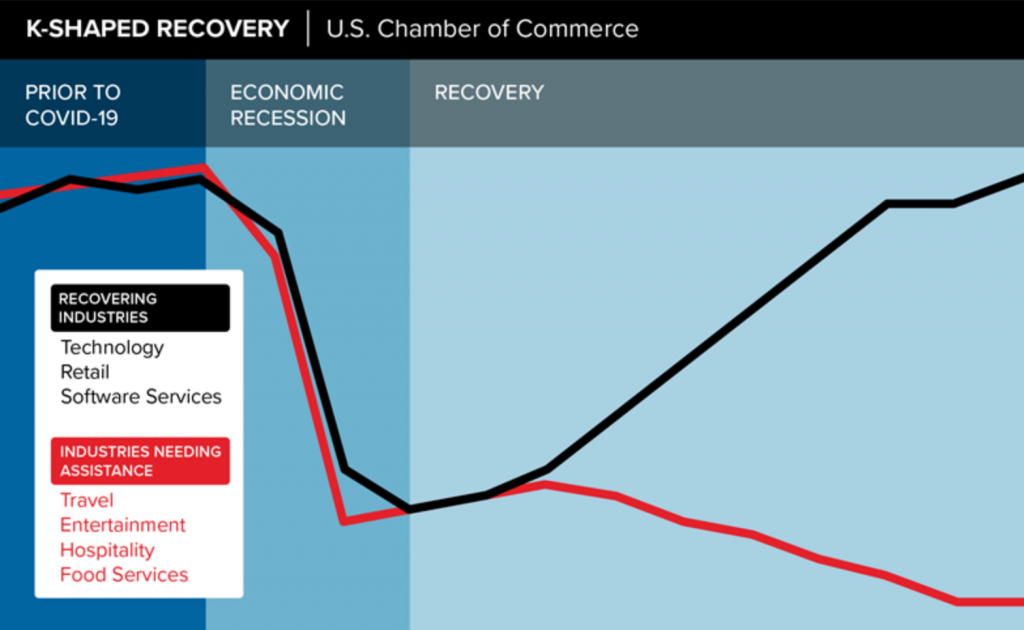

... and a K

But this is not 2008. Fast forward to today, and it's clear that, as former U.S. Federal Reserve Governor Kevin Warsh put it, "If you've seen one financial crisis, you've seen one financial crisis." Every recession is unique, and the pandemic-driven decline is particularly unprecedented. In fact, the form this recession may be taking has joined a growing alphabet soup of economic terms. Readers may be familiar with the optimistic V-shaped recovery pattern as well as the pessimistic L-shaped, with U- , W- , and Z-shapes falling somewhere in between. Economists are now introducing the notion that the post-pandemic recovery could look more K-shaped. Think of the vertical line of the K as the starting point from which different parts of the economy diverge: Some sectors grow while others decline. The market has been bullish on companies that support the "quarantine lifestyle" but was less kind to smaller companies as well as those situated in the travel and hospitality industries.

Given a K-shaped recovery scenario, group LTD carriers may ask themselves how much of the business mix is in the upper versus the lower arm of the K. If most of a block is focused on high technology and well-capitalized firms, it makes little sense to adopt overly conservative underwriting or pricing adjustments. But it may be prudent to keep a more watchful eye on business blocks with significant exposure to "lower arm" economic sectors.

See also: 9 Months on: COVID and Workers’ Comp

Recession-resistant sectors are not necessarily pandemic-resistant.

This new K shape is already challenging long-held expectations about which industries represent good disability risks. The previous notion that certain industries are resilient in recessions is now being turned on its head. That's because recession-resistant sectors are not necessarily pandemic-resistant. For example, unemployment rates during the 2020 COVID-19 pandemic followed a pattern never seen before, sharply spiking during spring lockdowns -- and causing job losses in every single sector of the economy.

Morbidity Bersus Mortality

It is easy to see the effects of this pandemic on group life insurance: COVID-19 has a direct and immediate impact on mortality rates. However, the effects on group LTD are much more opaque, as the morbidity impact is largely indirect and delayed. Mortality risk and morbidity risk may have polar-opposite reactions to COVID-19, both in terms of timing and direct linkage, but that is not to say that the financial impact will be wildly different. There are many "pandemic headwinds" facing group LTD carriers, and it's just a matter of time before these trends crystallize.

For example, the pandemic has strained hospital systems worldwide, leading to deferred preventative care and interrupted treatments that could result not only in a wave of deferred claims, but also sicker insured individuals. Prolonged lockdowns, reports of rising burnout levels among essential workers, particularly in healthcare, and the long-term loss of employment will likely contribute to additional mental and nervous claims. In addition, some survivors of COVID-19 -- even those who had mild versions of the disease -- continue to report a debilitating constellation of symptoms long after their initial recovery. Called post-COVID-19 syndrome or "long COVID-19," this condition has generated growing concern among public health providers and disability insurers and is being researched. In RGA-led industry surveys, many disability carrier participants report significant concern over the pandemic's potential to reduce recovery and return-to-work rates among the long-term disabled.

And while much about the first pandemic recession is new, one fact remains the same in every downturn: The longer economic problems persist, the greater the risk that long-term disability claims experience will worsen.

Keeping Perspective

While these headwinds are troubling, it is important to keep risks in perspective. For example, not all deferred healthcare signals an increased risk of short- or long-term disability claims. Also, mental health is fluid, and sources such as the mental health index Total Brain show that if the conditions contributing to symptoms of depression and anxiety are relieved -- such as through the end of a pandemic or recession -- the additional likelihood of psychiatric disability claims is mitigated. This is good news in light of the current thinking from economists that the recession may technically already be over and the recovery begun. If so, the recession would be the shortest in U.S. history.

Similarly, elimination periods (EP) should mitigate much of the direct effect of the pandemic on disability claims as a 90-180 EP usually lasts longer than a coronavirus case. Even a diagnosis of long-COVID-19 may not necessarily result in long-term disability. The "long" in long-COVID-19 is in comparison with a typical flu duration of three to four weeks, not the "long" that we infer with long-term disability claims. While most long-COVID-19 cases at present have durations measured in months, it is also too early to truly understand the long-term health consequences of this disease. Said differently, a tidal wave of COVID-19 LTD claims does not appear to be on the horizon, but continuing research points to a few ripples headed our way.

Pressures brought by the pandemic also have led to some unexpected positive developments. Recovery from some disabilities may be made easier by work-from-home measures, just as lockdowns led to faster consumer acceptance of wellness and digital health technologies. Telehealth, for example, has proven to be a very viable and cost-effective alternative to in-person doctor visits. Public health mandates like social distancing and mask-wearing also appear to be suppressing the spread of other infectious diseases such as the seasonal flu. The blisteringly fast pace of COVID-19 vaccine development has opened our eyes to what is possible in virology and paved the way for faster advances in vaccine science.

See also: What Digital Can Do for Disability Claims

The discovery and rollout of vaccines offer hope that an end to the pandemic portion of the crisis is near, but the effects of this recession on disability claims may linger.