Open insurance continues to be the next game changer in insurance. The second edition of the INNOPAY Open Insurance Monitor, which keeps track of how the global Open Insurance landscape is evolving, reveals a rise in the number of insurtech players that are providing access by connecting insurers with digital ecosystems. Meanwhile, one application programming interface (API) marketplace has become the first in incorporating Open Insurance services in its digital offering. Based on our analysis of the findings, we can conclude that the traditional industry players – incumbent insurers and banks – still seem in no rush to strengthen their currently weaker position to capture the value from Open Insurance.

The Global Open Insurance Trend Is Expanding, Albeit Slowly

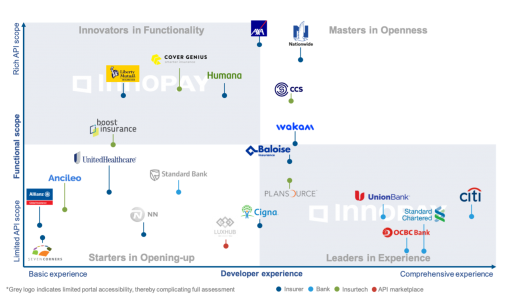

The updated edition of the Open Insurance Monitor includes several new players with insurance API propositions, both insurtechs and Open Insurance marketplaces. We can draw the following three key insights from the latest Open Insurance Monitor:

1. Insurtechs are entering the game

Most of the new entrants in this edition of the Open Insurance Monitor are insurtech players. They all offer "insurance as a service" that facilitates integration between insurers and third-party sales channels, with the developer portal environment as part of the offering. However, there is significant variation in the amount of functionality they offer, the level of developer experience and how they position themselves.

Boost and Ancileo, both located on the left of the spectrum, have a relatively small API scope focused on quotation, purchase and insurance policy modification. Although their developer experience is also relatively limited, they make up for it with clear API documentation that contains the necessary components for adequate interpretation and usage of the APIs. Meanwhile, Plansource offers benefits APIs as part of its complete HR solution to provide employing organizations a direct connection with insurance carriers for employees to have a seamless benefits shopping experience. The APIs include services for plan subscription and retrieval of relevant coverage data.

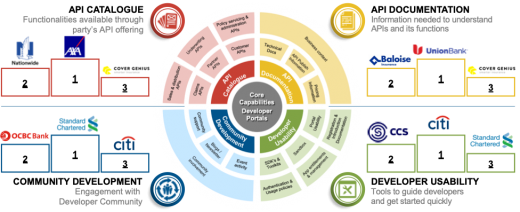

Another notable insurtech is Dutch-based CCS, which positions itself solidly on both axes. CCS has a wide API scope that covers multiple components of the insurance value chain, plus it acts as an API marketplace for its customers. Its developer experience is more advanced than its insurtech peers. For example, CCS offers proper developer usability features such as automatic onboarding, software development kits (SDKs) and app management and analytics functionality.

2. API marketplaces as a one-stop shop for insurance services

API marketplaces offer a variety of different API services from different providers, thus functioning as a one-stop shop for organizations that are looking to strengthen their capabilities through external APIs. The marketplace serves as a single integration layer, thereby reducing the implementation hassle.

LUXHUB is the first to integrate insurance services into its marketplace environment. It recently announced a new partnership with Baloise to provide mortgage insurance quotations directly to banks. As part of this new partnership, LUXHUB now publishes quotation and subscription request APIs on its portal. Although Baloise already had its own developer portal in place aimed at retail insurance, this partnership enables Baloise to directly integrate with core banking systems via the LUXHUB marketplace.

3. Existing players are not yet shifting focus

As highlighted in the first edition of the Open Insurance Monitor, insurers appear to be focused mostly on establishing their API portfolio, with their top priority being API documentation to allow developers to understand and use their APIs properly. There is little to suggest that insurers are shifting their focus toward other developer portal capabilities, while some extension of the API portfolio can be witnessed. For example, Nationwide has added several new API functionalities, including within its life domain, thereby moving closer to AXA as a functional innovator.

The same holds true for banks, whose superior developer experience is a result of their earlier Open Banking efforts. Their insurance-related API scope remains limited, but a few of them are improving their developer experience. For instance, Citibank has strengthened its developer usability with analytics and group role functionalities within app management and has enhanced community development by showcasing partner projects for inspiration. Meanwhile, Standard Chartered has launched an academy via its developer portal, where developers can improve their knowledge and skills on topics such as cloud transformation, APIs and emerging technologies. This feature is unique in both the Open Banking and Open Insurance space.

See also: Why Open Insurance Is the Future

Insurers Need to Start Deciding how to Compete Against or Benefit From Tech Players

The INNOPAY Open Insurance Monitor demonstrates that Open Insurance has been progressing slowly, but the presence of insurtech and API marketplaces in the Open Insurance space seems to suggest that the pace is accelerating. This presents incumbents with a choice: Fight the competition, team up with these tech-savvy new entrants or attempt a combination of the two. The "no regrets" move for insurers (and banks) would be to extend their own API portfolio and develop the necessary Open Insurance capabilities themselves. This would pave the way for an innovation platform that enables partnerships to be leveraged at scale. Insurtechs can play a role, for instance by providing direct access to a vast amount of different digital ecosystems for (white-label) product distribution. Because a wait-and-see approach is clearly no option, insurers need to carefully weigh up their choices and make the right decisions to safeguard their future position.