The insurance industry is experiencing seismic shifts in day-to-day operations stemming from this invisible yet intensely disruptive contagion COVID-19, but early signs of longer-term trends are also starting to emerge. A few short weeks ago, who would have thought that human health/safety and operational resilience would become the top two drivers of digital transformation? This pandemic has redirected our focus right at the base of Maslow’s hierarchy of needs overnight.

Organizations are overhauling operations to ensure the safety of employees and customers while business continuity and contingency plans are being put in place to ensure acceptable service for customers in this new normal. Insurers are focusing on retaining cash reserves while balancing customer retention with rebates, due to sheer uncertainty of the recovery timeline. Eventually, the obstacles presented by COVID-19 are giving way to new growth opportunities.

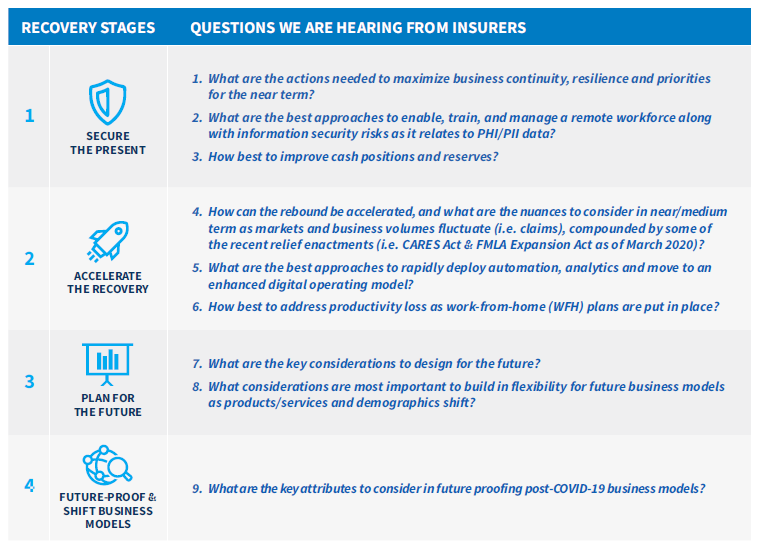

Based on our conversations with our insurance clients, some of the categorical questions being asked are represented in the table below. This paper addresses these key questions with a view to the “Future of Work” and key elements to consider in each of these stages.

Improving Resilience by Accelerating Digital With a Virtual Workforce

Moving not only in response to the present situation but also in preparation for the “Future of Work” will be the key differentiating factor between the leaders and laggards as the industry arrives at its new normal. The key areas that insurers are examining for current challenges and tomorrow’s opportunities fall into the following categories:

- Resilience for Near-Term Business Continuity: Insurers are embracing digital channels and have moved to makeshift, pseudo-digital business models essentially overnight to ensure business continuity. In the medium to long term, this will accelerate the digital transformation agenda as it offers intrinsically contactless business, reducing health risk and improved resilience -- in addition to typical transformation targets in growth, delivering customer experience cost-effectively and deploying/testing new products and services at lower costs. As reserves deplete and loss ratios are affected, insurers will soon prioritize these efforts to lower the cost of operations while improving resilience and addressing customer and employee health/safety.

- “Distance-Independent” and “Zero Paper” Business Models: In the near term, face-to-face meetings with agents and brokers to discuss policies or with adjusters to file a claim are extremely challenging. Customer journeys need to be modified to enable every step and interaction to happen anywhere and at any time. Paperless claims, data-driven underwriting and fully digital policy maintenance will be critical for longer-term growth and viability.

- Resilience in Workforce | Location Independence: We have witnessed a global shutdown in travel, businesses and borders to combat COVID-19. Some experts predict that, while many of these areas may relax these restrictions within a few months, the bans may need to go back in place if there is a resurgence in infections. Consequently underscoring the need to have a workforce – no matter whether these employees are nearshore, offshore or onshore – enabled and equipped to operate from anywhere.

Building Resilience in Operations and Business Models

Organizations are under stress, and so are employees and customers, due to the uncertainty of the recovery timeline. Some are saying the overall economic impact may be far greater than the recession in 2008. Insurers are beginning to realize the importance of digital as a way to enable resilience and are designing it into core operations, technology and the digital workforce while removing reliance on physical locations.

The illustration below depicts how to build resilience into every level of the business, including core operations and technology, the digital workforce and the physical workforce as new business models emerge. Agile, design thinking, cloud enablement and DevOps will also drive quicker iterations to target states; by definition, these will need to be short-run, multi-week/multi-month, not multi-year, initiatives.

Physical Workforce

- Remove paper and physical contact points internally and externally to deliver services. Deploy chat/digital channels for customer self-service.

- Achieve location-independence through WFH capabilities and reduce workloads by automating away low- and medium-complexity transactions.

- Enable better employee experience through rapidly deployable attended/unattended automation to boost employee productivity, offsetting any short-term, WFH-related productivity loss.

- Redeploy physical workforce to drive customer experience on high-complexity product innovation or high-impact planning and growth work.

See also: COVID-19’s Once-in-a-Lifetime Opportunity

Digital Workforce

- Encapsulate operations with digital capabilities for continuity and offset loss in productivity.

- Reduce people-dependent physical interactions and expensive voice and paper interactions while improving CX.

- Redeploy moderate- and high-complexity customer interactions for human agents.

- Accelerate self-service through chat and voice for low-touch flow transactions.

Core Technology and Operations Capabilities

- Resilience in core operations across essential customer touchpoint functions: claims, policy maintenance, underwriting and new business/onboarding (for new offerings post-recovery).

- Capacity to deal with spikes in volumes as markets head to a new equilibrium.

- Rapidly enabled remote employee hiring, onboarding, training capabilities and WFH operations monitoring.

Moving Forward

For the next three to six months, most companies will be operating to “keep the lights on,” with the focus on delivering essential services and maintaining operations. While this period will be fraught with tactical challenges, it will eventually end; when it does, businesses can look ahead to the future and the opportunities it presents.

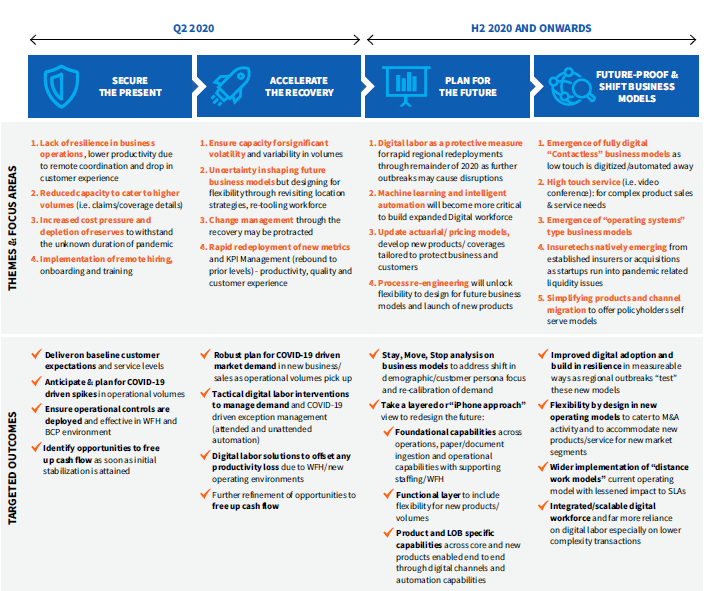

We have phased the coming months into stages to prioritize the recovery path and a way forward to the longer-term business model.

Figure 2 - Working through the stages of COVID-19 recovery

Stage 1 | Secure the present: This first phase will be spent protecting core operations and ensuring customer experiences aren’t disrupted across processes as volatility recedes and we head to the new equilibrium.

Question 1: What are the actions needed to maximize business continuity, resilience and priorities for the near term?

Digital and analytics will help address scale and volume variability while lowering operating costs, providing overall cost-per-claim improvement and enabling straight-through processing for low-complexity claims. Additionally, rapidly deployable attended automation can take care of many routine, repetitive tasks and drive efficiencies for underwriters and adjusters on their present-day desktops. For instance, this would include policy lookup, claim filing and data aggregation for underwriting and, consequently, free capacity to focus on complex cases requiring human intelligence and understanding.

These digital interventions lead to improved resilience and enable improved customer service, the most important aspect right now for insurers. Companies that fail to retain their current customer base will create post-COVID-19 drain on margins and cash reserves, especially if the recovery period is protracted. The good news is that, with relatively low-cost yet focused investments and interventions, the simpler transactions can rapidly be ramped onto digital channels, with the added benefit of making employees more productive in the WFH environment.

Question 2: What are the best approaches to enable, train and manage a remote workforce along with information security risk?

Remote hiring, onboarding and training with capabilities to coordinate and monitor WFH workforces are fast becoming new capabilities organizations are building out of necessity to react to near-term operational needs.

Clearly, information security is of critical importance. InfoSec controls span three areas across technical (e.g., encryption, multi-factor authentication), administrative (e.g., role-based security and credentials, data minimization/masking, read-only rights) and physical controls (e.g., supervisory and location-centric monitoring). Risk control self-assessments (RCSA) initiatives will need to be modified to ensure effectiveness of technical and administrative controls, while computer vision and initiatives emerge to augment physical controls.

Operational controls, key performance indicators (KPIs) and metrics are rapidly being updated to look at leading indicators to improve reaction time, exercise operational control on WFH workforces and ensure service continuity. Updated run-books, procedure guides and laptop-camera-enabled monitoring are all making their way into the WFH ecosystem.

Question 3: How best to improve cash positions and reserves?

Building a cash reserve and identifying opportunities for freeing cash flow to drive innovation will also become a parallel priority, as the timeline for recovery is unknown today.

L&A providers are preparing for larger claim payouts and potentially longer-duration disabilities, due to flexibility in parameters stemming from the COVID-19 stimulus package. In P&C, auto insurers have already declared refunds on the premium to control the cancellations due to non-payments. The industry anticipates a higher delinquency quotient, which will require ramping up billing and collections function to recapture potentially lost revenue. This will also create an opportunity for machine learning, analytics and automation-enabled tools to drive efficiencies in the collection function.

Apart from traditional approaches, high-impact, near-term digital interventions and no-code rapid deployments will also help free cash flow with relatively short paybacks. Success factors, however, will depend on focusing on multiple benefit areas and the ability to deploy robust solutions quickly where volume volatility exists. Additionally, service and capabilities are going to be more important than ever, particularly those that are low-effort yet data-driven and can accurately and quickly identify the right opportunities for digitization or automation.

Stage 2 | Accelerate the recovery: Once infections slow and countries begin lifting their stay-at-home orders, insurers can move from focusing on basic operational continuity to building more resilient business models. The focus will quickly move to getting back to normalcy.

Question 4: How can the rebound be accelerated, and what are the nuances to consider in near/medium-term business volumes that will fluctuate (i.e. claims), compounded by some of the relief enactments (e.g., CARES Act & FMLA Expansion Act as of March 2020)?

Digital tools previously seen as ways for cutting costs or increasing efficiency are now essential. They offer protection against similar events or regional COVID-19 outbreaks that could disrupt operations by reducing reliance on human labor through automation, analytics and machine learning. Initially, these efforts will focus on new business/onboarding, then underwriting when the time arrives for new policies to be written. Subsequently, they will help free capacity and mitigate operational, compliance and audit risks as regulatory parameters evolve and changes are made to COVID-19 relief acts throughout the recovery cycle.

Control room functions and tight controls on projected volumes will be essential to ensure scale up/down of digital and human labor to meet changing volume. As a result, digital and human workforces will need to be tightly integrated to enable stable operations and deal with volatility as the relief acts and market dynamics cycle through periods of volatility.

Question 5: What are the best approaches to deploy automation and move to a digital operating model?

The global nature of this crisis demonstrates the need for insurers to take a second look at their location strategy, re-tooling and re-engineering their workforce for maximum resilience. It’s not so much about whether employees are onshore or offshore – it’s about being able to sustain operations regardless of external circumstances. Enabling the remote workforce to be augmented through digital capabilities, whether attended or unattended automation, becomes a key consideration, as this will not only ensure consistently higher service quality but also reduce training needs as staff are hired.

Question 6: How best to address productivity loss?

A primary focus is on achieving location independence through WFH capabilities and reducing workloads by automating away low- and medium-complexity transactions. This includes enabling better employee experience through rapidly deployable attended/unattended automation to boost employee productivity and offset any short-term, WFH-related productivity loss.

Stage 3 | Plan for the future: Shifting from human-centered to digital processes can help companies be prepared for future surprises like the COVID-19 crisis. The key lesson learned is how we think about future models with resilience and flexibility designed in for future sudden shifts in the market.

Question 7: What are the key considerations to design for the future?

Machine learning and intelligent automation will be more important than ever in a post-coronavirus world for both employees and customers; these capabilities will provide customized experiences for a segment of one, tailored to that worker's or consumer’s preferences.

As the next normal settles in and is run for a sustained period, new challenges will emerge and will need to be addressed, especially for workforces in developing countries. One way to address this is to organize work into micro-teams (or pods) and ensure a hub-and-spoke model exists from function leaders through to individual staff. The intention is to drive collaboration and self-directed work reallocation at the micro-team level, when unforeseen circumstances affect a team member.

Question 8: What considerations are most important to build in flexibility for future business models as products/services and demographics shift?

The best way to explain this is to reimagine the future model the same way the larger internet natives have to build their platform business; essentially, to build a layered, or “iPhone,” view to redesigning for the future with:

(a) Foundational capabilities (i.e., physical hardware) across operations, paper/document ingestion, operational capabilities and supporting functions with staffing/WFH.

(b) Functional layer (i.e., operating system or iOS) to include digital capabilities and flexibility for new products/volumes across new business/underwriting, claims, policy maintenance and finance/compliance/audit functions, which are common and reusable to different products and lines of business (LOB).

(c) Product- and LOB-specific capabilities (i.e., apps on the iPhone) across core and specific new products enabled end to end through digital channels and automation capabilities. The goal is to flexibly and inexpensively add, delete and modify new products, such as credit insurance products, short-run coverage for specific regional risks products, parameter changes to categories of policies etc.

See also: COVID-19 Will Put ‘Tele’ in a Lot More Than ‘Medicine’

Stage 4 | Future-proof and shift business models: The problems insurers faced before COVID-19 may exist once the virus is no longer a pressing concern, but interventions of today should be thought through with the longer-term transformation in mind.

Question 9: Key attributes to consider in future proofing post-COVID-19 business models.

Organizations will look to redesign their business models to be more resilient against competitors now as well as pandemics or emerging regional risks.

This will give rise to “death of distance” or “physical contactless” business models, with ways of operating that can be done from any location. This includes offering products, services and delivery through fully digital channels. This will include providing straight-through underwriting for simple policies, and enabling customers to video conference with an agent for more complex or high-touch services.

Insurtechs, fintechs and other digital natives will exert competitive pressure on legacy insurance companies. Conversely, post-pandemic liquidity and access to private equity and venture capital will create interesting acquisition opportunities for insurers. Focused acquisitions may help leapfrog innovation in customer interaction and operational and distribution areas, but the key will be in the appropriate integration of these acquired capabilities at scale.

Conclusion: Digital as Key Enabler of Contactless, Distance-Independent and Resilient Business Models

COVID-19 has shown how situations can radically disrupt operations overnight. However, it’s also shown that people are equipped to adapt quickly and overcome global business challenges.

Insurers have a significant opportunity to thrive by building in resilience, rapidly deploying contactless business models, lowering reliance on physical locations and leveraging WFH capabilities. All of this needs to be executed with speed, agility and decisive action to assess, align and adapt quickly to the new reality.

Digital, automation, machine learning and analytics will enable future business models and have now become essential ingredients to long-term success, with a renewed focus on health/safety and resilience as well as customer experience and efficiency. However, the right digital capabilities must be applied to produce well-defined and achievable outcomes and are as important in “accelerating the recovery” as they are to designing the “business models of the future.”