When a person applies for a mortgage in the U.S., credit reports are pulled from all three bureaus -- Equifax, Experian and TransUnion. Why? Because a single bureau does not provide the whole story. When you’re lending hundreds of thousands or millions of dollars it makes sense to find out as much as you can about the people borrowing the money. The lender wants the whole story.

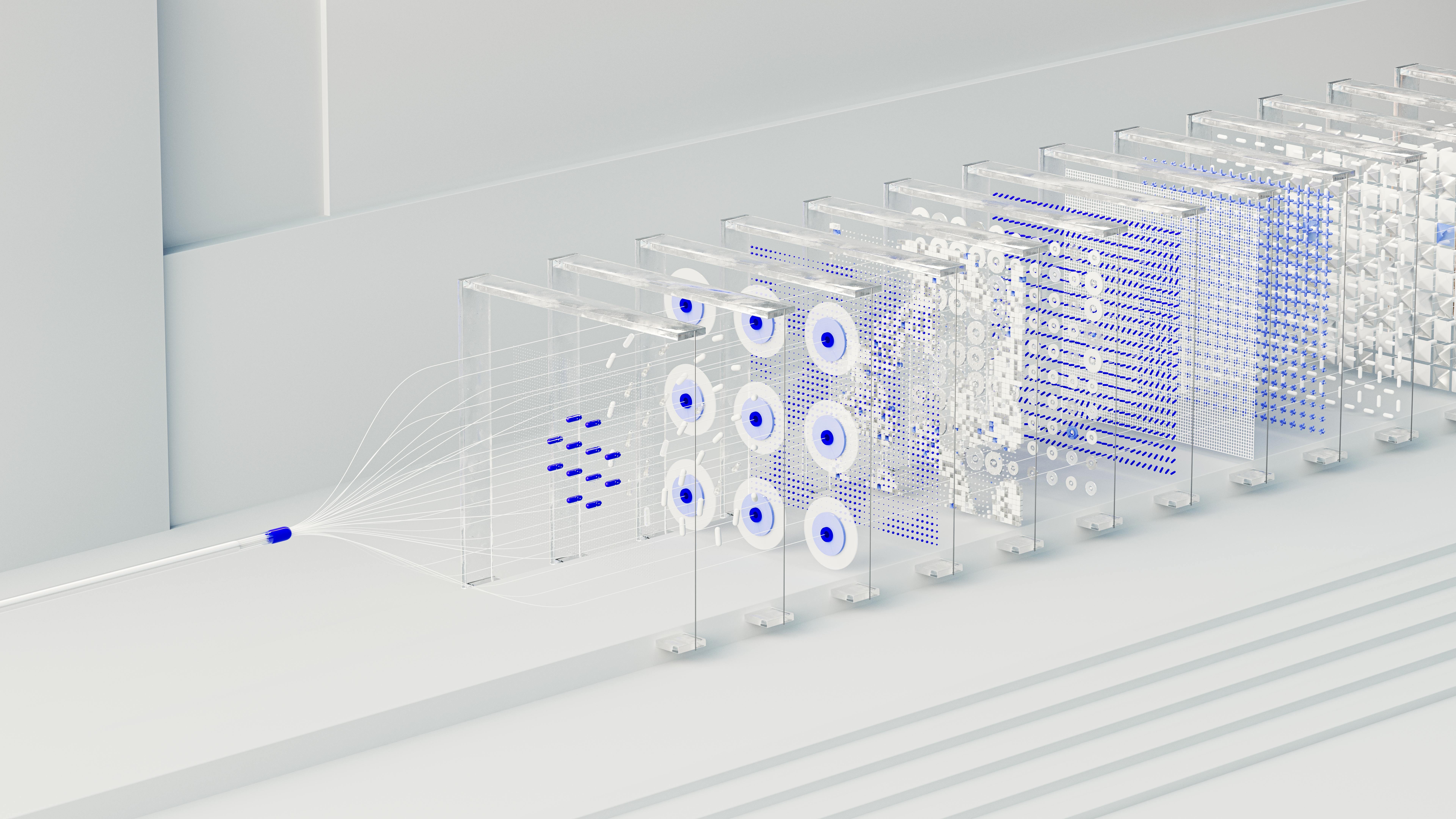

When you’re underwriting the property, doesn’t it make sense to get more than one perspective on its risk exposure? Everyone in the natural hazard risk exposure business collects different data, models that data differently, projects that data in different ways and scores the information uniquely. While most companies start with similar base data, how it gets treated from there varies greatly.

When it comes to hazard data there are also three primary providers, HazardHub, CoreLogic and Verisk. Each company has its team of hazard scientists and its own way of providing an answer to whatever risk underwriting and actuarial could be concerned with. While there are similarities in the answers provided, there are also enough differences -- usually in properties with questionable risk exposure -- that it makes sense to mitigate your risk by looking at multiple answers. Like the credit bureaus, each company provides a good picture of risk exposure, but, when you combine the data, you get as complete a picture as possible.

See also: Next Generation of Underwriting Is Here

Looking at risk data is becoming more commonplace for insurers. However, if you are looking at a single source of data, it is much more difficult to use hazard risk data to limit your risk and provide competitive advantage. Advances in technology (including HazardHub’s incredibly robust APIs) make it easier than ever to incorporate multi-sourced hazard data into your manual and automated underwriting processes.

As an insurer, your risk is enormous. Using hazard data -- especially multi-sourced hazard data -- provides you with a significantly more robust risk picture than a single source.

At HazardHub, we believe in the power of hazard information and the benefits of multi-sourcing. Through the end of July, we’ll append our hazard data onto a file of your choice absolutely free, to let you see for yourself the value of adding HazardHub data to your underwriting efforts.

For more information, please contact us.

The Next Step in Underwriting

Lenders draw data on individuals from all three credit bureaus. Why don't insurers do the same with the three sources of hazard data?