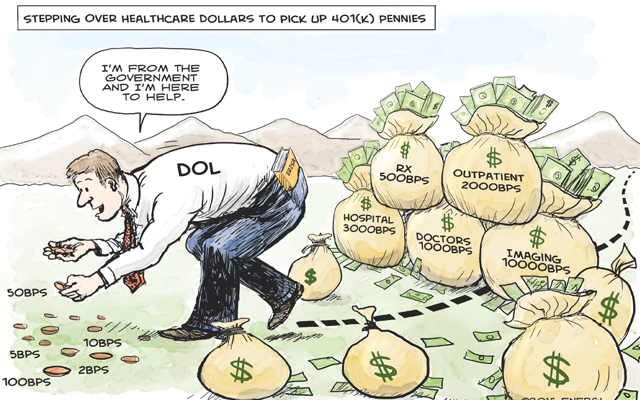

The U.S. Department of Labor (DOL) is determined to establish regulation over excessive loads and charges built into and sometimes hidden inside 401(k) plans. The costs are known as basis points, called "Bps" (Bips) in the industry, and they represent hundredths of a percent. For example, a load of 60 basis points equals 0.6%, and 100 basis points equals 1%. The DOL’s logic is that trustees and plan fiduciaries are too often oblivious to the excessive costs built into the plan and the resulting reduction in the investment performance for the plan participants.

But why are we being distracted about 401(k) pennies when the real culprits have created a healthcare system where hundreds and thousands of excessive cost "Bps" are annually overcharged to plan participants and employers?

Where is the outrage over the lack of transparency for disclosing fees, charges, expenses and loads built into the healthcare system and health plans offered to employers by insurance companies and HMOs?

Why is no one demanding accountability for massive claim payment errors, overcharges, hidden charges and compensation, excessive fees, hidden spread pricing or medical errors?

Health plan fiduciaries are typically oblivious to the true costs hidden inside their plans in the same way they don’t understand the all-in costs of their 401(k) plan. The major difference is that healthcare waste can easily be 10 times greater than the "Bps” being scrutinized inside 401(k) plans.

Imagine if the plan sponsor was held accountable to a fiduciary standard when managing the health plan. Ignorance is not a defense available to a fiduciary.

How will you change the way you manage healthcare when the DOL’s Employee Benefit Security Administration declares that health plans are subject to 408(b)(2) regulations?

Do you know what questions to ask? Here are a few to think about. See if you know the answers. If you don’t know the answers, then ask yourself, why not? Are you going to wait until regulations mandate that you act in a prudent manner in the best interest of the plan and the participants?

- What is the claims payment error rate by your insurance company, health maintenance organization (HMO) or third-party administrator (TPA)? What’s the impact when 3% to 10% of plan expenses are errors?

- How much does spread pricing by the pharmacy benefits manager (PBM) cost the health plan participant?

- Which physicians are the bad actors whose practice patterns are more than 300% outside established medical evidence protocols?

- Which hospitals charge 1000%-plus above Medicare payment rates?

- How much did iatrogenic disorders cost the plan?

- What percentage of readmissions were preventable?

- How much are labs, urgent care, MRIs and Emergency Departments upcoding and overcharging the health plan? What happens when you are accountable because your health plan and participants are paying four to 10 times more for the exact same services?