|

March ITL FOCUS: Predict & Prevent

ITL FOCUS is a monthly initiative featuring topics related to innovation in risk management and insurance.

Discover 'The Future of Risk™': Innovation, Tech, & Disruption Insights from Industry Leaders!

ITL FOCUS is a monthly initiative featuring topics related to innovation in risk management and insurance.

|

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Mobile-first solutions and visual AI are making processes faster and more accurate for insurers.

Mobile-first applications and strategies have become the go-to approach for delivering services, and they are making an impact in vehicle underwriting, transforming traditional workflows.

A mobile-first approach enables policyholders and insurers to speed the underwriting process significantly. Policyholders can submit important information directly through their mobile devices, eliminating the need for time-consuming physical inspections or lengthy back-and-forth communication.

But what's truly driving the mobile-first approach even further into the mainstream is the rise of artificial intelligence—particularly computer vision AI, or "visual intelligence." This technology is making it possible for insurers to assess, process, and price vehicle-related risks faster and from anywhere.

According to the Capgemini Research Institute's World Property and Casualty Insurance Report 2024, 42% of policyholders find current underwriting processes too complex and lengthy, highlighting the need for AI-driven improvements.

The combination of mobile and AI-powered technologies has the power to transform underwriting forever by prioritizing speed, accuracy, and customer satisfaction.

Powering a mobile-first underwriting approach with visual intelligence AI can mean serious advantages for insurers as it provides a way to analyze images or videos submitted by users remotely, with high accuracy. Visual intelligence AI can identify a vehicle's make, model, and condition, even spotting minor damage that a human inspector might miss. For insurers, this means faster decision-making and more accurate data, which means fairer and more reliable risk assessments.

Visual intelligence can also help reduce human error and subjectivity, which have long been challenges in vehicle underwriting. This is promising news for the 70% of insurance firms that reported inconsistent underwriting decisions as a prevailing issue in 2024.

See also: AI Revolutionizes Auto Insurance Via Real-Time Data

As AI and mobile-first technologies continue to advance together, it will only lead to smarter vehicle underwriting. According to Bain, insurers collect only about 60% of the data they need to underwrite a policy, highlighting the potential for more mobile data collection to improve this process.

After users submit vehicle details remotely via mobile devices, insurers can use visual intelligence AI to add a layer of more in-depth insights. This can help reduce manual underwriting processing times quite significantly, and lower overall operational costs.

More efficiency across the underwriting process benefits not only the underwriters but also end consumers, who experience quicker quotes and more transparency throughout the application process. The powerful combination of mobile and AI also means insurers can handle any surges in demand while maintaining accuracy and quality.

See also: AI and a Vision for Safer Roads

Shifting tedious underwriting processes to mobile-first can improve the customer experience overall. In fact, mobile-first practices aren't really an option any more but the standard for insurers striving to remain competitive.

The future of insurance lies not in replacing humans, but in elevating efficiency, precision, and a customer-first approach – a movement that will only continue as mobile and AI technologies advance.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Julio Pernía Aznar is CEO of Bdeo, a technology company that provides visual intelligence for motor vehicle and home insurers.

Specialty insurers must evolve beyond transactions to deliver personalized, digital-first coverage that meets modern consumer demands.

The insurance industry has long been defined by transactional relationships: customers purchase policies, pay their premiums, and file claims when necessary. While this model has sustained the industry for decades, it lacks the engagement and personalization that modern consumers expect.

Today, the rise of digital-first insurance providers and the increasing demand for tailored coverage require a transformation. Specialty insurers, in particular, have an opportunity to move beyond mere transactions and build customer-centric products that provide real value, trust, and engagement throughout the entire policy lifecycle.

Here's how specialty insurers like us at Roamly can shift from a transactional mindset and create products that foster long-term loyalty and enhance customer experiences.

The first step is to develop a deep understanding of who the customer is and what they truly need. Traditional insurers have historically relied on broad demographic and actuarial data to design policies, but today's consumers expect more than just a one-size-fits-all approach.

By leveraging data analytics, AI-driven insights, and customer feedback, specialty insurers can craft products that align with specific lifestyles. For example, at Roamly, we cater to digital nomads, RV, motorcycle, and boat owners, and travelers who need flexible, on-the-go coverage. Rather than simply offering a generic travel insurance policy, we integrate features that support their unique experiences—such as coverage for remote work setups or short-term rental insurance for RV owners.

Consumers today expect fast, intuitive, and digital-first insurance experiences. A customer-centric specialty insurance product should be easy to understand, purchase, and manage. This means moving away from cumbersome paperwork and opaque policy language and instead offering:

When customers feel that their insurer is accessible, transparent, and responsive, it generates trust and strengthens the relationship beyond just the moment of purchase.

Static, inflexible insurance policies often leave customers feeling underserved. Specialty insurers must design coverage that evolves alongside their customers' lifestyles and risk profiles.

For example, instead of offering a standard adventure travel insurance policy, insurers can provide dynamic coverage options that adjust based on:

This level of personalization ensures that customers feel seen and understood, which improves their overall experience.

Transformational insurance is about meeting customers where they are, rather than forcing them to seek out policies separately from their activities. Embedded insurance—integrating coverage directly into the purchasing experience of a product or service—has revolutionized the specialty insurance space.

For instance, Roamly partners with travel platforms to offer insurance at the moment of booking, ensuring customers have seamless access to coverage without extra steps. Whether it's integrating short-term rental insurance into an RV marketplace or providing travel medical insurance within a booking platform, embedding policies into existing workflows makes insurance feel like a natural, value-added component rather than an afterthought.

Beyond just offering financial protection, specialty insurers can help customers minimize risk. By using predictive analytics and AI, insurers can send real-time alerts about travel disruptions, weather hazards, or security threats based on a customer's itinerary.

Additionally, value-added services such as 24/7 concierge support, telemedicine access, or digital safety tools enhance the overall insurance experience. These measures transform the insurer from a reactive claims processor into a trusted partner that looks out for its customers.

Specialty insurers that focus on building long-term relationships, personalizing experiences, and embedding value into their products will not only retain customers but also differentiate themselves in an increasingly competitive market. As the industry continues to evolve, insurers that prioritize customer-centricity will be the ones that thrive.

The question for specialty insurers today isn't whether to evolve, but how quickly they can adapt to meet the changing expectations of modern consumers.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Brad Simmons is general manager at Roamly.

Insurers' current approach to assessing the risk from severe convective storms is fundamentally flawed. AI allows for key, property-specific insights.

The current approach to managing severe convective storm risk is fundamentally flawed. Most models in use today rely on stochastic methodologies designed to evaluate probable maximum loss scenarios but lack the precision to accurately assess average annual losses at the individual property level. This approach does not fully account for how hail damage accumulates over time on roofs. Just as a single cavity cannot be attributed solely to one candy bar, hail damage often results from cumulative effects rather than a single large hailstorm.

This leaves many carriers in a reactive posture, responding to events rather than anticipating them. For example, when a large hailstorm devastates a region, the typical response is to reassess rates across broad geographies—regions, territories, or ZIP codes. This reactive approach not only fails to address the underlying risk effectively but also triggers a cascade of negative consequences.

When the next storm inevitably hits, it targets a different set of properties, repeating the cycle. Losses continue to mount, good risks continue to leave, and carriers are left grappling with rising claims and deteriorating risk portfolios.

See also: Property Insurance Must Evolve for Climate Resilience

Some carriers have explored alternative measures, such as mandatory actual cash value (ACV) endorsements for roofs older than a certain age (e.g., 10 years) or exclusions for roof coverage on older properties. While these strategies may help curb immediate losses, they often lack the precision needed to differentiate between well-maintained and poorly maintained properties.

By treating all older roofs the same, regardless of their actual condition or risk profile, these blunt-instrument approaches drive away good risks—policyholders who maintain their properties but find themselves penalized nonetheless. Once again, carriers are left with the worst risks: poorly maintained roofs with limited coverage options elsewhere.

Fortunately, there is a more effective approach: Property-specific risk management. Advanced AI-powered models enable carriers to assess the unique risk profile of each structure, moving beyond proxies like roof age, material, and ZIP code. This approach considers critical factors such as:

AI-powered models uncover critical insights that traditional methods often overlook. For example, claims frequency for asphalt shingle roofs rises exponentially with age, while for metal roofs, the increase is more gradual before leveling off. Similarly, properties exposed to multiple hailstorms see claims frequency double with each event, up to a point where the effect saturates. These nuanced, non-linear relationships are invisible to traditional methods but can be precisely modeled using AI.

AI-powered risk assessment transforms how insurers evaluate hail damage risk by analyzing the interaction between the built environment and regional climatology. This approach moves beyond outdated methods that rely on broad groupings, such as ZIP codes and roof age, to assess risk. Instead, each property is evaluated based on its unique characteristics, enabling more accurate underwriting and pricing decisions.

Traditional models often fail to distinguish between good and bad risks within the same territory. AI-driven models, however, leverage vast amounts of property-level data to unlock a level of granularity that conventional methods simply can't achieve. By moving past broad categorizations, insurers can tailor their decisions to the specific attributes of each property, leading to a more precise, fair, and profitable approach to risk assessment.

The results speak for themselves: Insurers using AI-driven models are outperforming their peers, achieving over 60X lift in risk segmentation. This precision not only improves profitability and reduces loss ratios but also ensures fairer premiums for policyholders—delivering value across the entire insurance ecosystem.

See also: What Trump 2.0 Means for Climate Initiatives

The traditional methods of managing severe convective storm risk are no longer sufficient in an era of increasing storm frequency and severity. Reactive rate adjustments and blunt exclusions are short-term fixes that exacerbate long-term problems. By adopting property-specific risk models powered by AI, carriers can break free from the cycle of rising losses and adverse selection.

This approach doesn't just mitigate losses; it redefines the relationship between carriers and their policyholders. Policyholders with well-maintained properties are rewarded with fair and transparent rates, fostering loyalty and trust. Carriers can provide tailored recommendations, educating policyholders about property maintenance. This makes for a healthier risk pool while improving the overall customer experience.

The path forward is clear: By embracing property-specific, data-driven models, the insurance industry can break the cycle of severe convective storm losses, ensuring a more sustainable future for both carriers and their policyholders.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Kumar Dhuvur is the founder and head of product at ZestyAI, an AI-powered property and climate risk analytics platform.

He has led credit risk analytics teams at Capital One Bank and advised financial services institutions on risk management strategies while at McKinsey.

He holds an MBA from the Wharton School, University of Pennsylvania, and a B.S. in electrical engineering from IIT Madras.

Cyber threats lead aviation's top five risks for 2025, while workforce shortages and business interruption intensify challenges.

The annual Allianz Risk Barometer found that these are the top five risks for the year ahead, as voted for by a number of aviation sector experts around the world:

In fifth place, our respondents flagged the shortage of skilled workforce. While this actually represents a new entrant on the top five risks list, few will be surprised at its inclusion. An issue for the industry since before COVID-19, aviation continues to battle with labor force limitations, with demand far outstripping supply. The reasons include significant numbers of retirements during the pandemic; a lack of appeal in the profession; insufficient training capacity to meet demand in any event; and the cost of training being unaffordable (in the case of flight crew).

In a review of the position in April 2024, the Royal Aeronautical Society highlighted research suggesting that over the next 10 years 300,000 more pilots, 300,000 more maintenance engineers and 600,000 more cabin crew will be required. These targets are unlikely to be met. The shortage will affect everyone in the industry and will have the effect (as is almost always the case in a supply shortage) of pushing up costs via wages. This increase will force a market correction by making aviation jobs more appealing; however, it is not one market participants welcome. Unfortunately, this risk looks like it is here to stay.

In fourth, surprisingly down from No. 1 in 2024 is political risks and violence. Notwithstanding the fragile ceasefire in the Middle East, we remain in a world beset by conflict – from the war in Ukraine to civil wars in Myanmar and Sudan. Throw in stateless terror organizations looking to exploit the disenfranchised and marginalized, and it is not surprising that political risk and violence remains a key risk for aviation in 2025. Civil aviation authorities and airlines must constantly dance on a tightrope to balance their potential security risks against the demand for provision of safe, commercially viable air travel for a global population that still wants to travel in greater numbers than ever before. Evolving geopolitical situations, along with new methods of waging war, require constant attention.

In third place, aviation industry respondents are concerned about changes in legislation and regulation. This is a new entrant on the list this year and is related (among other things) to the evolving landscape of sustainability requirements. This is likely to become even more the case with the shift in the position of the U.S. in relation to the Paris Agreement and environmental, social, and governance (ESG) regulation.

Global aviation companies are in the unenviable position of having to comply with both European standards still focused on Net Zero by 2050 and a U.S. government loosening requirements, at least in the short term. The implications of the European Union's Corporate Sustainability Reporting Directive (CSRD) are yet to be fully borne out. A regulatory framework to standardize sustainability reporting across industries, the CSRD is likely to add costs consequences for those needing to comply. With the complexity (and potential repercussions of misreporting) and a shifting regulatory landscape, it is therefore no surprise that such regulation is a key concern for those in the aviation sector.

See also: 5 Ways Drones Are Changing Insurance Claims

Just off the top spot, in second place, is business interruption – up from No. 5 a year ago. Linked to both the shortage of skilled labor and political instability, the fragility of aviation supply chains remains a significant concern for the industry. In something of a perfect storm, there have been both delays to new equipment delivery, but also problems with existing aircraft and engines requiring maintenance (and the potential grounding of aircraft as a result).

The International Air Transport Association (IATA) has reported that the average age of the global fleet has risen to a record 14.8 years (a significant increase from the 13.6 years average from 1990-2024), with a record backlog for new aircraft of 17,000 planes. These issues are having significant effect on operators who are forced to bear significant cost via expensive (hitherto unplanned) maintenance, rising lease costs due to aircraft shortage (IATA estimates 20% to 30% higher than 2019), scarcity of spare parts and increased operating costs as a result of operating older aircraft while awaiting new, more efficient equipment. This can also have repercussions in relation to sustainability plans and targets – older aircraft have higher emissions: IATA report that fuel efficiency was unchanged between 2023 and 2024, vs. a historic 1.5% to 2% improvement trend. The continued operation of older aircraft also has an effect further down the food chain – with smaller operators in developing markets also having to wait longer to upgrade their secondhand aircraft and the spares market affected by fewer older aircraft being stripped down. It is no surprise that this is such a concern for the aviation industry.

At No. 1, the risk most concerning the aviation industry in 2025 is cyber incidents. At No. 2 in 2024, the risk has made the jump to top position after a year with notable high-profile incidents such as the CrowdStrike outage in July, demonstrating the fragility of the global aviation industry's technological reliance.

See also: Cyber Incidents Top Global Business Risks in 2025

Perhaps the reason for cyber incidents' place at the summit can be put down to the truly enormous and varied threat such a term encompasses: Cybercrime, IT outages, malware/ransomware attacks, data breaches and the associated fines and penalties are all included. This is not to mention the potential for malicious acts from hostile operators on actual flight operations, such as GPS spoofing – a sophisticated attack that exploits weaknesses in an aircraft's navigation system and has become increasingly common in areas of geopolitical instability such as Eastern Europe and the Middle East.

All told, aviation companies have a lot to worry about. Aside from any business interruption and cost of remediation, there is the risk of reputational damage, litigation from consumers, regulatory action and fines and ransom requests.

As the aviation industry continues its digital transformation journey, through the further integration of artificial intelligence (AI) and a significant transition to cloud infrastructure, maintaining robust cyber security while continuing to innovate remains a critical challenge. It is therefore no wonder that cyber risk is at the forefront of the aviation industry's concerns for 2025.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Adam Tozzi is head of underwriting global tasks and processes (aviation) at Allianz Commercial.

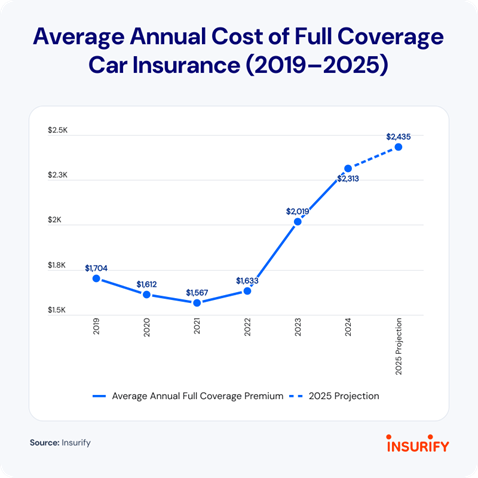

Car insurance rates have increased nationwide since 2022 as climate risks and EV adoption drive unprecedented cost increases.

Car insurance rates have been rising dramatically, with a 15% increase in 2024 alone. American drivers now pay an average of $2,313 annually for full coverage, with some states exceeding $3,000. Insurify projects that rates will increase another 5% in 2025, bringing the national average to $2,435. While the pace of increases has slowed, financial pressures remain significant for many drivers.

Rising vehicle repair costs, high-tech and electric vehicles (EVs), and climate risk are among the main causes of these increases. EV insurance costs surged 28% in 2024, twice as fast as for comparable gas-powered models, making them 23% more expensive to insure on average. Climate change has also played a role, as insurers factor in the growing financial impact of hurricanes, hailstorms and other severe weather. Additionally, state-specific regulations and market conditions have led to disproportionate increases in some states.

In regions prone to natural disasters, insurers are adjusting their pricing models to account for the heightened risk. States with high rates of uninsured motorists, frequent weather-related claims, or unique legal structures regarding liability often see steeper increases in insurance premiums.

See also: Are High Insurance Premiums Holding EVs Back?

The states experiencing the highest car insurance costs include Maryland ($4,060, up 53% in 2024), New York ($3,804, up 14% in 2024 and projected to rise a further 10% in 2025), and Florida ($3,166, with an expected 10% increase in 2025 due to climate risks and insurance fraud). Other states, such as Nevada and Georgia, are also seeing significant boosts, with projected increases of 8% in 2025.

Maryland now has the highest average full-coverage premium in the country, surpassing states such as Florida and Michigan, which have historically been at the top. This dramatic increase is due in part to new state legislation requiring insurers to provide enhanced underinsured motorist coverage and cover diminished value claims.

New York continues to be one of the most expensive states for car insurance due to high population density, frequent accidents and stringent coverage requirements. The state's no-fault insurance system has long contributed to higher rates. Florida faces similar issues, with a no-fault system that has led to a significant rise in fraudulent claims.

Minnesota saw the fastest-growing rates in 2024, with a 58% increase, followed by Maryland (53%) and California (48%). These increases were driven by severe storms, legislative changes and rising climate risks. Minnesota's increase is largely attributed to a string of severe hailstorms that resulted in costly vehicle damage.

Meanwhile, EV insurance costs remain a major factor in rising premiums. The Tesla Model 3 is the most expensive EV to insure, at $4,362 annually, which is 25% higher than a comparable Mercedes-Benz A-Class. Similarly, the Hyundai Ioniq 5 and Kia EV6 cost 41% and 32% more to insure than their gas-powered counterparts.

Climate-related damages are also driving up claims. Hurricanes Helene and Milton caused nearly $50 billion in insured losses in 2024, including 138,000 flooded vehicles. Hail damage claims have also risen sharply.

In states like California, insurers are grappling with the increasing risk of wildfires. South Carolina and Florida also face heightened risk due to hurricanes and flooding. In response, some insurers are limiting coverage options or withdrawing from high-risk markets altogether.

See also: 10 Most Expensive States for Car Insurance

To mitigate rising costs, drivers should compare rates across multiple insurers, consider telematics programs that track driving behavior for discounts, and bundle policies with home or renters insurance. Telematics programs can offer discounts of up to 30% for safe drivers who enroll.

With insurers stabilizing financially, there may be some moderation in rate increases, but affordability will remain a challenge for many. Drivers who shop around and leverage available discounts will be in a better position to manage rising costs.

While auto insurance rates are projected to rise at a slower pace in 2025, affordability remains a growing concern. With the cost of car ownership rising across the board—from vehicle prices to maintenance and fuel—many Americans are feeling the pressure.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Cassie Sheets is a data journalist at Insurify.

The insurance industry is shifting from traditional actuarial models to incorporate behavioral data in risk assessment practices. The implications are enormous.

The insurance industry has traditionally followed an actuarial model of valuation to assess, rate, and price the risks it insures. This process involves analyzing data related to variables that represent the risk attributes of an individual or property to predict the likelihood of a risk event occurring within the policy period.

However, the behavior of the insured—such as lifestyle habits, driving patterns, or how well someone maintains the safety of their home—has historically not been directly included in these calculations. Despite being significant causal factors in risk events, these behavioral aspects could not be incorporated due to the lack of appropriate technologies to source and analyze such data. Instead, insurers relied on retrospective analysis of risk events to identify parameters that could serve as reliable proxy predictors of behavior.

Over the past decade, several new technologies have emerged, triggering a data and information revolution that has enabled the insurance industry to source real-time risk data, including data related to customer behavior. Access to real-time behavioral data has led to a paradigm shift in how the insurance industry evaluates risk. The transition into a new era of behavioral insurance has just begun. These technologies are maturing, and the concept of monitoring behavior is gradually gaining market acceptance. Insurers are now experimenting with behavioral insurance products that integrate insights from real-time data, offering behavior-based adjustments to traditional actuarial valuations.

See also: Precision Underwriting Transforms Risk Assessment

Insurance is a contract that transfers risk from an individual to an insurance company in exchange for the payment of a premium. To quantify risk and calculate the premium amount, the insurance industry employs actuarial valuation, a method based on mathematical probability calculations. Insurers assess various variables—known as rating factors—related to personal, demographic, or asset characteristics, as well as transaction history, usage patterns, and claims history. These factors are used to create a risk snapshot at the start of the policy period. Using this snapshot, insurers aim to predict the distribution of risk throughout the duration of the contract.

Rating factors enable insurers to quantify risk more effectively by transforming unmanageable risks into manageable ones. For any given rating factor, good risks within a group (comprising individuals who share the same rating factor) offset the bad ones, and the actual loss of an individual is replaced by the average loss of the group. Insurers use multiple rating factors, ensuring that cross-subsidization occurs only after normalizing for other risk variables. However, the issue of cross-subsidization persists. As long as all possible rating factors have been identified or normalized, as the size of the risk factor group increases, the standard deviation of the group’s average loss approaches zero. This, in turn, enhances the accuracy of predictions about future outcomes.

However, if not all possible rating factors have been identified, we revert to a relative position. In such cases, the premium rate for any customer is based on the average risk across the insurer’s portfolio or class of business (the risk pool), adjusted for bonus-malus factors (relativities derived from the risk factors). The resulting premium is considered actuarially fair, as the individual is charged a premium commensurate with the expected claims under the policy. More sophisticated insurers may target profit and share of reinsurance costs as a function of claim volatility rather than average claims. In such scenarios, rating factors are regressed against claim volatility, but the underlying principle remains similar.

While actuarial valuation aims to statistically predict claim frequency, it has traditionally not accounted for risk behaviors that contribute to losses. Due to a lack of appropriate technologies and methods, insurers have historically been unable to monitor behaviors that directly influence risk and incorporate them into the initial risk snapshot. Behavioral assessment represented a soft underbelly of risk management, as it was inherently subjective and a continuous factor throughout the entire policy period. For insurers, information asymmetry remained a significant challenge, as they often had insufficient data about the insured individual or property to make accurate decisions. There are two types of asymmetric information: one related to hidden risk factors and the other related to risk actions.

In insurance, information asymmetry poses a significant challenge. It arises from the fact that insurers often lack sufficient knowledge about the insured individual or property to make accurate decisions. Information asymmetry related to hidden risk factors occurs when one party to the contract possesses knowledge about themselves that the other party does not. This leads to adverse selection, where higher-than-average risks are more likely to seek and obtain insurance coverage at standard or average rates. Insurers can mitigate this risk by analyzing more data from diverse sources or reactively by voiding the contract or imposing restrictive clauses if the deliberate suppression of material information is discovered later. Conversely, information asymmetry related to actions occurs when one party to the contract alters its behavior to the detriment of the other party. For example, if the insured fails to follow best practices for risk prevention or mitigation, the likelihood and severity of the risk increase. While the former type of asymmetry undermines insurers’ ability to accurately assess the risk of loss, the latter exacerbates it.

As behavior is an important constituent of information asymmetry, insurers depend either on disclosures made by customers or obtain information from other institutions and regulated bodies. Another way to uncover the mystery of behavior is to conduct a retrospective analysis of risk events to find data associations that could be treated as correlations and proxies for risky behavior. With the help of proxies, insurers have traditionally created generic a priori behavioral risk snapshots, such as assuming that young people are bad drivers or that highly educated professionals tend to be good drivers.

In the last few decades, conventional insurance practices such as the law of large numbers, rating factor normalization, and premium cross-subsidization have been challenged by three forces: traditional rating factors being seen as discriminatory, the changing preferences of new demographic generations, and emergent technologies.

Perceived Discrimination: Over the years, some rating factors—both causal and correlative—have started being considered spurious, illegal, or unfair. With many countries enacting anti-discrimination legislation, the insurance industry started invoking the principle of actuarial fairness to legitimize its actuarial valuation methods and risk selection practices. The industry drew a distinction between fair and unfair forms of discrimination and insisted that fair discrimination is necessary to differentiate between good and bad risks and to avoid adverse selection. The industry’s rallying point has been that the core principle of actuarial fairness would be endangered if the sector was not granted exclusive exemptions from such equity legislation. Despite this, some rating factors have been called out for having a discriminatory effect against specific social groups, resulting in their usage being restricted. This has weakened insurers' ability to infer what was happening within the behavioral black box.

Changing Preferences of New Customers: Customers from the new generations have a different view on risk and premium cross-subsidization. They prefer the personalization of insurance coverage and services and intend to pay only for the exact risk they represent, rather than cross-subsidizing the higher risk of other customers. Customers who exhibit prudence and sound judgement in their behavior want their good actions to be acknowledged and rewarded by the insurance company in the form of appropriate premium discounts. They are keen to avoid paying for the imprudence of other customers.

Emergent Technologies: Data-driven technologies such as telematics, wearable health trackers, home sensors, smartphone sensors, big data, and predictive modelling are now allowing insurers to obtain even more granular and nuanced behavioral data, enabling them to determine actual causal risk factors and the costs of covering the risks with greater accuracy. New customers also support the concept of continuously sharing their behavioral data in exchange for rewards that recognize their acts of prudence and sound judgment.

The ability to track at-source risk data and customer behavior in real time removes the veil of information asymmetry and effectively transforms risk management in the insurance industry. Insurers can now distil clear insights into the dynamic behavioral elements, allowing them to sketch and continuously refine the causal behavioral graph throughout the contract period. The concept of insurance is shifting from hindsight-based risk profiling to foresight-based risk assessment. This introduces a new narrative for insurance, moving away from a valuation modelled on behavioral proxies to one based on causal behavioral values. As a result, primary driver parents who let their younger children drive their car can no longer hide behind traditional rating factors.

See also: The Cognitive Biases Hurting Risk Management

Behavioral insurance is characterized by insurance products that incorporate approaches for continuously tracking risk data and making behavioral interventions based on risk insights. It leads to the charging of tailor-made, personalized premiums based on monitoring the customer's behavior. By pinning the responsibility for some hazards and risks directly on the insured, behavioral insurance creates a new narrative for the industry. Behavioral insurance is in its early stages of growth and adoption, and the insurance industry is beginning to pivot towards a new approach. To start, the industry is experimenting with monitoring some well-established behavioral variables that are causative of risk but previously could not be measured earlier. Currently, the popularity of behavioral insurance is more in motor, followed by life and health, and relatively less in home insurance. The behavioral variables monitored range from to good driving-related parameters in auto insurance, healthy lifestyle activities in life and health insurance, and proper home maintenance in home insurance.

In life and health insurance, lifestyle behaviors such as exercising, food habits, and periodic health checks are monitored to promote healthy living. In auto insurance, in addition to conventional risk parameters, various aspects of driving behavior are tracked. These include vehicle speed to assess speeding events and compliance with speed limits, acceleration and braking patterns to detect aggressive driving behaviors such as rapid acceleration or harsh braking, as well as unsafe cornering and sharp turns. Monitoring behavioral data helps insurers identify key causal predictors of risk and intervene to encourage rightful behavior. Behavioral interventions take the form of rewards, such as premium discounts and coupons for redemption, or punitive actions, such as rate hikes and penalties.

From a risk pricing perspective, insurers are yet to explore the integration of causal behavioral data into their core risk valuation models. Conventional actuarial valuation of risk still dominates the core. Rate-making is still based on traditional variables that are either independent of behavior or account for conventional proxies. Currently, behavior valuation functions as a wrapper around the values calculated through actuarial valuation and fairness. Behavioral data is converted into a behavior score, whose impact on risk is defined in quantitative terms. These bonus-malus charges are applied to the actuarial premium depending on the behavior score.

Existing insurance contracts are predominantly rigid and inflexible. Once fixed, premiums are either changed at the beginning of a new contract period in short-term contracts or remain unchanged in long-term contracts. Behavioral insurance is attempting to change this paradigm by introducing interim and periodic checkpoints in long-term contracts to review behavior for potential revisions to the premium and/or policy conditions. In the case of short-term contracts, even bad behavior that does not cause a risk event or result in a loss, as well as non-adherence to healthy behavioral protocols, is penalized due to the probable increase in risk profile. By tracking behavioral variations, insurers can capture incidents of morale hazard and prevent claim leakages by denying compensation for claims caused by imprudent behavior. Behavioral insurance promises to reduce risk through new processes, most of which are automated with the help of data and algorithms designed to steer individual behavior in the direction of maximum profitability.

Behavior valuation is seen as a solution to address the challenges posed by perceived discrimination in the use of certain predictor variables within the actuarial valuation method. The behavior of an individual, despite all other influencing factors, is presumed to be a conscious choice made by the individual and therefore controllable. This hypothesis posits that rather than being typecast based on a vague generalization, individuals are fully responsible for the type of risk category they represent. Hence, behavior valuation based on behavioral variables is perceived as fair and is not considered discriminatory, as it is based neither on proxies nor on statistical generalizations. Measuring behavioral data and assessing behavioral interventions help insurers organically distinguish prudent customers from imprudent ones.

There are lower-hanging fruits in the rating factor universe that insurers may want to consider before turning to behavioral factors. For example, detailed flood hazard mapping has had a greater impact than behavioral pricing over the last five to 10 years, and gene microarrays are expected to have a much greater impact over the next 10 to 20 years than the differential between one’s "vitality age" and actual age ever will. That said, every little piece of information helps, so there is still room for behavioral pricing, but we also need to consider other challenges.

The cost of collecting and processing real-time behavioral data is still relatively high compared with the potential reduction in cross-subsidization. Hence, the premium savings offered by insurers have been marginal. This, in turn, influences customers' willingness to change their behavior, which reduces with the offered premium savings. For instance, avoiding driving because it is raining may reduce claims, but the payoff may not be significant enough to justify the inconvenience. In comparison, consumers can obtain greater behavioral and financial payoffs elsewhere—for example, by using their washing machine at night due to smart meter-based electricity pricing.

The prospect of having granular risk data could improve risk prediction, thus enabling risk pricing that is more closely commensurate with the expected risk. The development of behavioral-based rates can be seen as a shift toward personalization. Behavioral-based personalization may result in greater premium variability or instability for customers, potentially reducing the appeal of insurance. Adding further complexity and uncertainty to a product that is already complex and primarily sold on the basis of certainty may not be such a great idea.

The monitoring of behavior invariably leads to the possibility of behavioral steering for the betterment of the risk profile. Conventional triggers for behavioral steering are explicit rewards or punishments. Over the years, the subject of behavioral economics and the subtle art of behavioral nudging have gained mainstream adoption. Insurers should be aware that any practice of data-driven design to manipulate behavior is unethical. They must adopt a cautious and well-thought-through approach in developing behavioral-based insurance models. They should always remember that the customer’s consent to share personal data is not an acceptance of being deceived or a justification for being placed in a panopticon.

Paradoxically, behavioral monitoring may provide insurance companies with more information than even the customers themselves may know. It may not only reveal what the customer consciously hides (suppression or misrepresentation) but also what the customer is not even aware of.

In the context of the Johari Window, a visual representation created by psychologists Joseph Luft and Harrington Ingham, the former falls in the hidden area (known to the self but unknown to others), while the latter falls in the blind area (unknown to the self but known to others). While insurers have the legal right to protect their interests by acting on the hidden area findings, it could become a legal and ethical challenge to penalize customers based on blind area findings that they are unaware of themselves. Insurers must follow the principle of utmost good faith to work on expanding the size of the open area. Before they initiate any punitive or curative actions based on those findings, insurers must openly disclose both the hidden and blind area findings and the consequent actions to the customers. Insurers should establish standards regarding the behavioral variables that are monitored and measured, how they are processed, the insights derived, and the consequent action pathways.

Given the continuous flow of behavioral data and the need for real-time processing, analysis of the data is only possible through automated decision-making systems. These systems can identify non-linear patterns within causal behavior to classify it as good or bad. It is well known that big data significantly influences causality analysis, making proxy and spurious correlations appear more authentic. This can engineer discrimination based on new behavioral proxy traits that are hard to detect. While this may or may not act against specific social groups, it would still be considered a bad faith practice. It must be borne in mind that the primary purpose of behavioral insurance is to remove proxies and replace them with causative variables while monitoring how risk progresses during the contract period. The subjective nature of behavior should not lead to the creation of a new black box—one that is even darker and system-generated.

The advent of behavioral insurance has raised concerns about the future role of insurance. Unlike traditional insurance, where information asymmetry drives the risk of adverse selection, behavioral insurance could usher in a new era of favorable or propitious selection. This could occur either because individuals with risky behaviors opt out of insurance or because insurers choose not to cover them. As a result, insurance becomes an unforgiving instrument, accessible only to favorable risk pools. This favoritism could, in turn, lead to a reduced need for insurance. An important factor that sustains the demand for insurance is the inherent unpredictability of human behavior and the range of risks it can trigger. If individuals’ behaviors are uniformly conditioned into an optimal state through behavior-steering, the scope of insurance may diminish. Ultimately, the need for insurance could be restricted to fortuitous losses, such as those associated with mortality or morbidity (life and health) or natural catastrophes (auto and home).

The spread of behavioral insurance is still in its early stages, primarily driven by wellness-based models in life insurance, telematics-driven usage-based insurance, manage-how-you-drive models in auto insurance, and sensor-based home insurance. Behavioral insurance offers several key advantages. First, it encourages the insured to adopt healthier practices, thereby reducing the frequency and severity of preventable risks. Second, behavior-steering fosters continuous engagement between insurers and policyholders, shifting the narrative of insurance from a low-touch to a high-touch model. Third, real-time behavior tracking helps mitigate moral hazard and adverse selection, reducing instances of insurance fraud. Finally, behavioral data enables insurers to build healthier risk pools and refine risk management strategies.

The foundation of behavioral insurance relies on customers sharing their personal data, making data privacy a critical concern. The core tenet of data privacy is an individual’s right to determine when, how, to what extent, with whom, and for what purpose their data is shared. Behavior monitoring involves multiple technology players across the data value chain, each contributing to data collection, processing, and analysis. Ensuring data privacy is a collective responsibility that requires robust legislation, governance structures, and regulatory oversight.

As behavioral insurance matures, core risk valuation will integrate both conventional statistical data and real-time behavioral insights. Currently used behavioral proxies will be replaced by truly causative variables, leading to greater accuracy. In traditional models, a customer’s transition between statistical risk segments is gradual and structured. In contrast, behavioral traits are highly dynamic, introducing greater volatility in risk segmentation. Consequently, a customer’s risk profile at any given time becomes a complex interplay of actuarial and behavioral risk scores, necessitating a more adaptive risk assessment approach.

In the future, behavioral insurance could expand to incorporate a broader set of behavior rating factors, behavioral patterns, and complex interactions with conventional risk variables to better establish causal associations. Additionally, longitudinal analysis will enable insurers to determine optimal feedback and reward mechanisms that effectively guide behavior in the desired direction. This evolution will lead to comprehensive behavioral response models, complementing the existing proactive approaches. The insured's responsiveness to preventive alerts and action reminders could emerge as a key causative behavioral predictor of risk. Repeated inaction or inappropriate responses to actionable alerts may be classified as high-risk behavior, influencing risk assessment and pricing.

That said, behavioral insurance could still fall by the wayside, overwhelmed by the many challenges it faces. Even if it manages to overcome them, it may do so too late. It’s not far-fetched to imagine a future where insurance premiums are driven less by individual behavior and more by unpredictable, chaotic—even apocalyptic—weather events. At that point, it won’t matter whether you did your star jumps this morning or diligently monitored visitor arrivals through your Google Nest doorbell—especially when a tropical cyclone is pounding on your door, despite the fact you don’t even live in the tropics!

Reference

Barry, L., & Charpentier, A. (2020). Personalization as a promise: Can Big Data change the practice of insurance? Big Data & Society, 7(1), 205395172093514. https://doi.org/10.1177/2053951720935143

Cevolini, A., & Esposito, E. (2020). From pool to profile: Social consequences of algorithmic prediction in insurance. Big Data & Society, 7(2), 205395172093922. https://doi.org/10.1177/2053951720939228

Jeanningros, H., & McFall, L. (2020). The value of sharing: Branding and behaviour in a life and health insurance company. Big Data & Society, 7(2), 205395172095035. https://doi.org/10.1177/2053951720950350

McFall, L., Meyers, G., & Hoyweghen, I. V. (2020). Editorial: The personalisation of insurance: Data, behaviour and innovation. Big Data & Society, 7(2), 205395172097370. https://doi.org/10.1177/2053951720973707

Meyers, G., & Van Hoyweghen, I. (2017). Enacting Actuarial Fairness in Insurance: From Fair Discrimination to Behaviour-based Fairness. Science as Culture, 27(4), 413–438. https://doi.org/10.1080/09505431.2017.1398223

Minty, D. (2020, May 13). Are loss prevention initiatives just trojan horses for data harvesting? Ethics and Insurance. https://www.ethicsandinsurance.info/loss-prevention/

Minty, D. (2020, April 29). Behavioural fairness is a serious risk to the future of insurance. Ethics and Insurance. https://www.ethicsandinsurance.info/behavioural-fairness/

Tanninen, M., Lehtonen, T., & Ruckenstein, M. (2022). Trouble with autonomy in behavioural insurance. The British Journal of Sociology, 73(4), 786–798. https://doi.org/10.1111/1468-4446.12960

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Srivathsan Karanai Margan works as an insurance domain consultant at Tata Consultancy Services.

Chris Logan is an actuary, risk analyst and internal auditor based in New Zealand. He doesn’t want to be nudged by any corporate, so he keeps (behavioral) data sharing to a minimum.

Alcohol's cancer risks have moved into the public spotlight, creating an opportunity for life insurers to educate policyholders.

The headlines were everywhere:

"Surgeon General's report warns even moderate alcohol use increases cancer risk." --Tallahassee Democrat.

"Moderate drinking raises cancer risks while offering few benefits." --The New York Times.

"US surgeon general sounds alarm about link between alcohol and cancer." --CNN.

Those in the insurance and reinsurance industries calmly sipped their coffee and said some version of, "This is news?"

As he prepared to leave office after serving for presidents Obama, Trump, and Biden, U.S. Surgeon General Dr. Vivek Murthy issued a report titled, "Alcohol and Cancer Risk." The 22-page general advisory identified alcohol consumption as a leading preventable cause of cancer, stating that 741,300 cancer cases worldwide were attributable to alcohol in 2020. A quarter of those cases afflicted people who consumed two or fewer drinks per day.

Even more alarming to some, that percentage did not vary significantly as consumption increased. Just more than 28% of cases were linked to those who consumed around two to four drinks a day. Roughly 21% affected those who consumed four to six, and 26% for those with six or more. The report considered one drink comparable to a five-ounce glass of wine, a 12-ounce beer, or 1.5 ounces of liquor.

In concluding his report, Murthy called for warning labels to be placed on alcoholic beverage containers similar to those on cigarette packs.

See also: Data Science Is Transforming Public Health

Whether such labels are appropriate is a matter for politicians and regulators to decide. For insurers, alcohol's link to cancer is nothing new. The connection has been well established through multiple studies dating back to the 1980s and long factored into insurance risk assessment.

The headline-grabbing message that sparked so much public attention has been understood in the life insurance industry for decades: There is no completely safe level of alcohol consumption. Cancer is just one of the danger areas, layered on top of increased risk of liver disease and accidental death.

Alcohol consumption trails only tobacco and obesity as a leading preventable cause of cancer in the U.S. Research has demonstrated a causal relationship between alcohol use and an increased risk for seven types of cancer – breast, colorectum, esophagus, liver, mouth, throat, and voice box. And, as the surgeon general correctly points out, that risk starts increasing for some of those cancers – such as breast, mouth, and throat – with as little as one drink a day or less.

Scientifically, the call for warning labels makes sense. Alcohol metabolism occurs mainly in the liver and produces acetaldehyde, a metabolite from ethanol that can cause DNA damage that ultimately leads to cancer development. The International Agency for Research on Cancer (IARC) classifies alcoholic beverages, ethanol in alcoholic beverages, and acetaldehyde as carcinogenic to humans (Group 1).

The recent headlines led many who have heard from their doctors for years that a nightly glass of red wine might actually be good for them to scratch their heads. Then again, there was a time when doctors (not to mention the beloved children's cartoon Flintstone characters) endorsed cigarettes on television commercials.

While tobacco's link to cancer has been the subject of massive awareness campaigns for decades, alcohol's connection has largely flown under the public radar. In fact, only 45% of Americans surveyed in 2019 by the American Institute of Cancer Research said they believed alcohol causes cancer. More than 40% believed smoking was a major cause of cancer – in 1966. That number rose to 71% by 2001. While the percentage today varies depending on the type of cancer, a National Institutes of Health study found 97% of U.S. adults believe smoking causes lung cancer.

See also: Digital Health Services Create Liability Gaps

That discrepancy – more than 97% for smoking's link to lung cancer compared with just 45% for alcohol's connection to cancer overall – justifies the surgeon general's warning. But Dr. Murthy is ringing a bell the insurance industry has been sounding for years.

That said, this added attention presents life and health insurers – along with all those in the health and wellness space – a timely opportunity to reinforce that there is no completely safe level of alcohol consumption. As insurers continue to account for alcohol use in risk assessment, they can also take steps to educate consumers about its contributing role to a variety of cancers and other conditions, further establishing themselves as policyholders' wellness partners.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Dr. Adela Osman is vice president, head of global medical for RGA.

She also serves as co-editor of ReFlections, RGA’s global medical newsletter.

Dr. Valerie Kaufman is senior vice president and chief medical director, leading the U.S. medical team that implements RGA’s medical underwriting philosophy and strategy.

As hybrid work becomes permanent, traditional warranty management faces new challenges that require innovative tech solutions.

Hybrid work is no longer a temporary response to global disruptions. It is a permanent means of doing business. In fact, according to recent data, more than 50% of employees as of 2024 now work in a hybrid setting.

While remote and hybrid work models offer numerous advantages, such as flexibility, they have also exposed critical inefficiencies in managing and securing distributed technology assets and traditional warranty management systems. Issues arise particularly in ensuring seamless device support, minimizing downtime, and optimizing IT costs. As companies equip employees with laptops, tablets and other devices to work from multiple locations, businesses must rethink their approach and leverage technological innovations to ensure warranties become a strategic asset rather than a liability.

See also: Overcoming the Talent Crisis in Underwriting

In a centralized office setup, warranty management was straightforward. Employees could submit claims, IT teams could oversee repairs, and companies had greater control over the lifecycle of their technology assets. However, hybrid work environments have created hurdles, such as:

With devices spread across multiple locations, tracking warranty coverage and eligibility has become more complex.

Employees working remotely often face longer wait times and logistical challenges when submitting claims.

Many businesses miss covered repairs simply due to poor tracking or lack of real-time insight.

IT teams must coordinate repairs and replacements across a dispersed workforce, leading to inefficiencies and increased costs.

To overcome these challenges, organizations must use technology to streamline processes, reduce operational friction and maximize asset value. Here's how emerging innovations are reshaping warranty management in the hybrid work era:

Technology is automating claim submissions, approvals and tracking. Automated warranty management platforms can:

Cloud technology allows companies to monitor warranty status and claims processing for all distributed IT assets. With real-time visibility, organizations can:

Predictive analytics leverage historical data and algorithms to anticipate device failures and track historical warranty claims. This innovation allows businesses to:

Seamless integration between warranty management platforms and IT asset management systems ensures that warranty data is incorporated into IT lifecycle planning. This integration helps businesses:

See also: 3 Steps to Weather the Coming Labor Crunch

By modernizing warranty management with technology-driven solutions, organizations can unlock key benefits:

As businesses continue evolving in the hybrid era, tech-enabled warranty management will become a non-negotiable necessity. Companies that invest in automated, and cloud-integrated solutions will streamline operations, gaining an edge in workforce productivity and IT cost efficiency.

The hybrid work model is here to stay, and so is the need for smart, technology-driven warranty solutions. Organizations that embrace these innovations today will be better prepared for the future of work—where efficiency, security and adaptability are paramount.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Brett Lassig is president of Get Cover, an insurtech offering digital-first warranties and service contracts.

He has more than 25 years of experience in the extended warranty and insurance services industries.

Digital health services expose providers to new liability risks while many remain unaware of available coverage solutions.

Digital health services, including telemedicine and telehealth, have become an integral part of patient care, enhancing access and efficiency. Not surprisingly, with these advancements come risks concerning patient diagnosis, treatment and data privacy. While many risks found with in-person care settings apply, virtual care settings expose healthcare providers to additional liabilities, such as allegations of violating the standard of care, navigating multi-jurisdictional regulations and technology failures.

In a virtual setting, poor technical quality could impair communication between a provider and patient. If a third-party telehealth platform fails, both the platform provider and the healthcare provider using it may face liability claims.

According to QBE's Digital Health Insurance Report, which surveyed insurance brokers specializing in healthcare liability, 63% reported that their health care clients are either extremely or very concerned about digital health risks. These risks include inadequate care (cited by 44% of respondents), technology and product errors (41%), and cybersecurity breaches (38%).

Despite the availability of customized coverage, 30% of healthcare clients were unaware additional coverage existed and thus did not purchase it, brokers reported. Consequently, more than eight in 10 brokers (84%) are concerned that some clients may be operating their business without the appropriate coverage for digital health services. This could stem from various factors, such as changes in a client's business model or an expansion of their geographic footprint to provide services in different states. Meanwhile, claims related to digital health services have risen over the last year, with 60% of brokers noting an increase.

Given the increase in claims filed, deeper engagement between brokers, carriers and clients is needed. The survey findings highlight the importance of raising awareness about the inherent risks of digital health services and educating health care providers about potential liability coverage gaps. 50% of brokers say their clients are interested in more information when informed that they may need to update their policies, and 27% say their clients want to purchase additional coverage.

See also: Digital Benefits Tools Drive Employee Wellness

As the landscape of healthcare evolves with increasing digital service integration, insurance providers are adapting with innovative coverage options. Some insurers offer branded digital health packages, while others adapt traditional coverage to include digital settings. A notable strategy is the hybrid approach, which combines traditional coverage models with flexible, tailored solutions for digital health.

This hybrid strategy starts with a professional liability basis applicable to both brick-and-mortar and digital operations. Insurers then augment this with additional coverages on an a la carte basis, facilitating seamless integration and reducing the need for policy rewrites as operations evolve. This model is advantageous as healthcare entities increasingly navigate between physical and digital realms, offering a comprehensive package that covers all liabilities thoroughly.

A key benefit of the hybrid approach is its ability to bridge gaps introduced by traditional insurance silos. For instance, while cyber policies might focus on financial loss, the healthcare professional liability aspect concentrates on bodily injury. This model aims to cover bodily injuries resulting from cyber and technology incidents—risks that might be overlooked in less integrated approaches. By coordinating coverage across different types of risks with a single carrier, or at least explicitly acknowledging expressed coverage for these risks, the hybrid approach minimizes uncertainties and disputes when claims arise, leading to better outcomes for all parties involved.

See also: Data Science Is Transforming Public Health

Despite these advancements, a significant gap remains in the awareness and adoption of comprehensive digital health coverage. Currently, brokers report that among the healthcare professional coverage of their clients, only 51% of the policies include expressed coverage for digital health services. However, with the growing recognition of digital health risks and the expanding scope of these services, a substantial increase in demand for tailored insurance solutions is anticipated.

As understanding of digital health risks improves and scope of these services expands, 68% of brokers anticipate an increase in demand for digital health services coverage. In this ever-evolving risk landscape, it is imperative for brokers and carriers to collaborate more effectively with clients in crafting optimal insurance solutions. This process begins by educating clients on the potential risks associated with digital health services and clearly explaining the various types of available insurance coverage.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

|

Partner with us

We’d love to talk to you about how we can improve your marketing ROI.

|

Drew Fekete is assistant vice president, underwriting – miscellaneous medical, for QBE North America.