Few people today would argue about the value of data to an insurer, or the power and potential of analytics. Insurers have been leveraging data, business intelligence and, more recently, predictive analytics solutions to gain more insights and inform important business decisions. There is still much value in these areas, and there is still work to be done to modernize some of these capabilities and gain further benefits. Meanwhile, on the horizon and fast approaching is a new set of capabilities that will take analytics and the power they can bring to the next level. Artificial intelligence (especially machine learning), cognitive computing capabilities, new geospatial data and technologies and preventive analytics promise to yield differentiating capabilities to insurers bold enough to leverage them.

The challenge many have is sorting through all the potential capabilities in the data/analytics space and developing a strategy and plan that aligns to and supports their business strategy. Keeping track of the new developments and how they might be applied to specific business problems or opportunities is daunting. To aid insurers, SMA has recently updated our SMA Data and Analytics Spectrum. This framework has already been used by many as a way to understand what types of capabilities are needed to address specific types of business questions as well as to filter and assess tech solution providers.

The SMA Spectrum has five areas, and our research highlights the fact that the industry, in general, has made great progress in three of those areas but is lagging in the other two. The areas SMA terms Describe and Diagnose are the province of traditional BI, where insurers have much experience and, for the most part, have solid capabilities. The Predict area of the framework is where insurers have put a great deal of effort and investment over the past several years to build capabilities. Predictive analytics and models are becoming more widespread and more important in the industry today.

However, there is an area that SMA terms Discover, that enables companies to explore the WHY – using advanced tools to dig much deeper to gain a new awareness into the root causes of problems or the genesis of new opportunities. This is a nascent area with much potential for insurers looking to expand usage of text mining, image mining, speech analytics, scenario planning and other analytics tools. Finally, a new category of analytics is emerging in the SMA Spectrum that is called Prescribe. The notion of prescriptive analytics has been around for a while, but they are becoming practical now, and insurers are beginning to implement these capabilities. Real-time data from smart devices in conjunction with big data, machine learning and cognitive computing technologies are making it possible to recommend specific actions and, in some cases, automate the actions. Layer in geospatial analysis to provide context and new data and even more potential is there to predict, prescribe and even perform actions without human intervention.

The power of data and analytics is confirmed by the new organizational approaches being taken by insurers, new roles being established and investments in major initiatives to outgun competitors that are also seeking to gain advantage through data and analytics. You might think that the industry is reaching a peak in terms of the leverage from analytics, but with the rapidly evolving digital world and the new capabilities – you ain’t seen nothin’ yet!

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Mark Breading is a partner at Strategy Meets Action, a Resource Pro company that helps insurers develop and validate their IT strategies and plans, better understand how their investments measure up in today's highly competitive environment and gain clarity on solution options and vendor selection.

These days, all we hear is: Disrupt this, and disrupt that. I even saw a company on LinkedIn with a chief disruption officer. Really? Now that disruption appears to be the norm, what’s next, disrupt the disruption?

The term may have legitimate usage in some context, but insurance? The disruption is supposedly taking place in Silicon Valley, where IT firms are working on new insurance delivery, administration, marketing, and efficiency software models.

Okay, so we’re moving all of this transactional and administrative work into cloud-based digital environments, but where’s the disruption? Isn’t this just the natural progression from outdated systems technology to more current technology? Maybe people will transform the old agency management system into an app for your iPhone. That wouldn’t disrupt anything, but it would be cool.

A firm in Silicon Valley sponsored a conference called Insurance Disrupted 2016: Inside the Digital Tipping Point. Here is the link. (Note: The link says 2015, but it’s actually for the 2016 conference. Some tech genius didn’t remember which year it was, or was too busy playing foosball to change the link).

According to the website, one company “sees software as rewriting the insurance industry,” and others are working on “new insurance distribution plays…that will change the shape of insurance.” What could “rewriting the insurance industry" mean? And what is the “shape of insurance,” anyway?

Do you think any of these tech savants know the origins of insurance? A very brief tutorial: In about 1688, Edward Lloyd’s (London) coffee house began selling insurance against loss of ships and their cargo. This basic transaction hasn’t fundamentally changed in the last 329 years. Regardless of all of the current digital hoopla, this is exactly what we do today.

See also: Insurance Disruption? Evolution Is Better

Typical of Silicon Valley, the conference website promises something "insanely great," as if insurance isn’t 1,000 light years from anything remotely called insanely great. But that’s perfectly fine. Insurance is the second-oldest profession in the world, with a rich history and an economic mission second to none. It doesn’t need hyperbole to define its importance.

Here’s the thing about the Silicon Valley digital wonderfulness – it should enable disruption in the insurance business, not define it (or disrupt it). Technology’s role is not the be-all and end-all; it’s an important supporting player, as all technology has been since time immemorial. Advances in marketing and administration technology do not deserve to be called disruptive -- evolutionary, maybe, but not disruptive.

According to the "insanely great" website, insurance industry customer satisfaction is extremely low, but the reason has nothing to do with IT. It’s because we systematically devalue our product, reducing it to a nameless commodity, by constantly reminding our customers that its only value is a cheap premium. The irony is that this is what most insurers think creates value. Question for insurers: how cheap must insurance premiums be before the customer is satisfied?

Exhibit A: The Gecko

When the gecko tells us that in 15 minutes we can save 15% on our auto insurance, the product disappears. That which really matters — the insurance contract and service after a claim — become valueless and worthy of our contempt. The gecko doesn’t care, as its sole marketing strategy is low cost, not product value, and it serves its purpose.

Because the gecko’s relentless TV advertising disregards the value of products and services, it perpetuates the lie that the only way to evaluate an insurance product is by its cost. Many millions of consumers swallow this, hook, line and sinker, every year. No wonder customer satisfaction is so low — a mildly funny, smooth-talking gecko is telling us what’s really important, and it isn’t the quality of the product or the company selling it. It’s ironic because the gecko is owned by Berkshire Hathaway, which is renowned for its “value investing” approach to everything it does.

How Did We Get Here?

The simple answer is: We did it to ourselves. Imagine the “price is everything” mentality in contract law, which is similar to insurance. Contract lawyers sell their time and expertise, based on their knowledge of contracts. Insurers and insurance agents sell insurance contracts, and, by implication, their time and expertise.

A contract lawyer’s value has little to do with her hourly rate; it has to do with her ability to construct and interpret complex contracts. Insurers use many standard contracts, but each company has its own version of many others. Both the lawyer and the insurance company/agent owe a similar duty of care to customers. Why, then, is insurance sold like so many bags of potatoes, and contract law expertise is sold based on the value of the provider and the product?

Disrupting the Insurance Status Quo

Let’s completely rethink the way insurance is priced, and, in the process, create value for the product and the insurer. (Rates and rating formulae cannot be changed, but pricing can.) Can we design a paradigm that stresses value creation over chasing cheap premiums into the toilet?

Here are some ideas on how to really disrupt the insurance business:

Align product value with product cost, maybe using some of this new Silicon Valley software. Let’s create a value-based pricing scheme that recognizes that some coverages and features are more (or less) important to different customers. The current, cheap, premium-driven model obviates the need to differentiate product features and benefits.

Let’s better identify and allocate insurer capacity (capital) as a basis for competition. The insurance cycle is based on the amount of capital swimming around in the insurance markets. Let’s bring this dynamic down to the individual insurer level and use ROIC (return on invested capital) as part of the basis for pricing the product.

Let’s try to redefine insurance from a cheap-is-better necessary evil to an essential financial product, worthy of its cost. What we have now is the opposite: cost worthy of the product. When the cost is cheap, so follows the product, as we see in almost every other facet of economic life.

Finally, let’s educate our insurance sales forces to stress product value-for-the-money. The current insurance sales and delivery paradigm defies the old truism, that you get what you pay for, because the only value is a cheap premium, with the understanding that the product will be identical from every insurer regardless of the premium. (For some perverse reason, we must compare “apples to apples.” Why can’t we identify value differences and price them accordingly?)

The cumulative effect of these ideas, in my humble opinion, have the potential to be truly disruptive, as many thousands of insurance salespeople would have to abandon the “I (or the gecko) can save you 15%” mentality, which only serves to devalue the insurance product and, more importantly, devalue the person or company selling it. The ultimate goal of this initiative is for customers to acknowledge the premium, (cheap or otherwise), but also know what the premium is purchasing and why. In other words, where’s the beef?

See also: The 5 Charts on Insurance Disruption

Next time, I’ll rough out a new and, I think, disruptive, value-based pricing model. I may be just a lonely voice in the wilderness, but nothing ventured, nothing gained, right?

Note – the term “product value” as I use it here includes the cost of losses and all of the expenses necessary to support the insurer’s infrastructure and provide ancillary customer services such as adjusting claims, and loss control/prevention.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Donald Riggin is the president of the ART of Captives, a consultancy specializing in alternative risk financing techniques. He provides corporate and public sector clients with state-of-the-art risk financing advice and services.

Disruption is inevitable, and no organization is immune. Findings from McKinsey suggest that the current pace of disruption is happening 10 times faster than the Industrial Revolution, at 300 times the scale, and with 3,000 times the impact. This is an unprecedented opportunity for businesses to thrive, but at the same time an unprecedented threat to slower-moving organizations, which may end up allowing themselves – or their industry – to be disrupted.

“We are at the precipice of unbelievably powerful advancements driven by technology. We no longer have to ask if we can do it, but if we should do it, and, if we do, how do we do it responsibly,” says Eric Boyum, managing director, technology and communications industry, at Aon.

Embracing disruption – both managing it and anticipating it – is crucial for businesses to thrive during this change. But what constitutes disruption, and how does it differ from innovation? Putting the customer experience first and truly understanding audience needs is critical. From agility to forward-thinking industry trends, established organizations can learn from newcomers and help their teams innovate on behalf of customers – key to thriving amid change.

In Depth

Today, innovation and disruption confront many industries, driven by a host of entrepreneurial firms looking for opportunities to beat incumbents at their own game. The situation becomes even more interesting, however, when entrepreneurs are a leading force in creating a new game.

Boyum, who works with some of the world’s leading technology companies, offers a key distinction between innovation and disruption: “All those that participate in disruptive movements can be considered innovators – however, not all those that innovate are necessarily disruptors.”

Randy Nornes, executive vice president, Aon Risk Solutions, elaborates: “Disruption does not come from typical competitors,” where most companies traditionally focus their defensive efforts. Instead, disruptors often originate from outside the industry being disrupted – which means established players don’t recognize what’s happening until too late. The disruptor then captures and develops a market, eventually unseating incumbents.

See also: Key to Digitizing Customer Experience

When Apple released its first smartphone in 2007, it probably wasn’t looking to transform the transportation industry. But it turned out that putting a GPS unit in the pockets of billions of people across the world would crack open a whole universe of commercial applications inconceivable to the original inventors. Uber, the paradigmatic “disruptor,” was quick to see the opportunity.

Smartphone technology was available to everyone. Uber’s ability to capitalize on Apple’s innovation and aggressively outpace incumbents in the taxi industry through offering cheaper, more flexible rides, marked it out as a true disruptor. It is now the most valuable private company in the world.

Apple itself was, of course, also a disruptor. It jumped on the then-new technology of file-sharing with iTunes and disrupted (many would say fatally) the physical music retail industry. Spotify, in turn, disrupted iTunes by putting subscription streaming ahead of paid downloads.

It’s not just about innovating and making products better – it’s about anticipating consumer needs. This type of disruption often comes from new players, as opposed to traditional competitors. “The company that provides the most taxi rides does not own any taxis; the company that rents the most rooms does not own any rooms, and the company that distributes the most media does not generate any content,” Boyum says. “These companies are, of course, Uber, Airbnb and Facebook.” They got there not by being the best in their field at providing a certain product but by providing a completely new one.

Data for the People

“We’ve seen entire industries emerge because they promise something to the end-user: a better customer experience,” Nornes says. Uber could have made bigger, plusher taxis. Instead, it correctly saw that what travelers wanted out of their experience wasn’t necessarily luxury but affordability and convenience of a kind that traditional taxis had yet to provide.

Through a data-driven understanding of audience or a market, disruptors seek to prioritize customer experience and work to improve the status quo – often creating a new one. “A lot of sharing economy companies focused on technology and new ways of capturing data,” Nornes says. “In the transportation world, disruptors leveraged the GPS technology that’s inside a smartphone to create a superior service.” In turn, this data has been used in other ways to improve the ridesharing services. An Uber passenger can feed back data via ratings, which the company can then leverage to further optimize user experiences and create a model that is, to an extent, self-regulating.

This data-led process of transformation is set to intensify. By 2020, there could be 20 billion internet-of-things devices worldwide. Understanding the emergent narratives of consumer behavior that this enormous mine of data produces will be the first order of business for tomorrow’s would-be disruptors.

The Ripple Effects of Disruptive Innovation

“The most important lesson to learn is that disruption can happen to everyone – no one is immune,” Boyum says. This disruption can come in many forms, other than direct competition.

Nornes asks: “How do you deal with independent contractors? How will regulations evolve? What are the talent implications – do companies have the necessary disruptive talent to keep ahead of competitors?” Some of the more wide-reaching implications of disruption could include:

Insurance & Regulations: Businesses don’t operate in a vacuum – from insurance to regulations, they are governed by a complex network of secondary services, which will also have to adapt to disruption. Current insurance policies are built on certain assumptions about how customers engage with products or services. Initially, Uber struggled with getting its drivers insurance coverage, as providers had no products that accommodated the unique risks of non-employee drivers – of course, disruption here also means an opening of markets for new products.

There must also be responses to the shifting nature of work in the gig economy. Is an Uber driver a freelancer using an app, or should he be treated – and compensated – as a full employee?

Employment & Talent: Headlines proclaiming an unemployment doomsday at the hands of automation are abundant. Don MacPherson, partner, Global Engagement Practice at Aon Hewitt, frames this as a hiring and retention issue: “Are we still going to be able to bring people into this organization as we’re seen to be shedding jobs that are now obsolete?”

But, he explains, organizations should relish the opportunity to transform their talent and training strategies. Incumbents should look at what innovators are doing: What types of talent are they bringing on? How flexible is that talent? And, perhaps most importantly, are they fostering functions like R&D, which will allow them to leverage their disruptive capabilities in a competitive environment?

Societal Impact: Models that disrupt multiple industries, like the sharing economy, also have widespread societal implications. A firm like Airbnb disrupts far more than just hospitality incumbents. Homesharing can create incentives for more buy-to-rent activity, which causes distortions in rental markets as prices rise. This, in turn, can provoke regulatory responses from local governments – which affect the whole housing landscape, rather than just the operations of one company. And so they have, in Paris, San Francisco and New York.

The onus is on the disruptors to communicate the benefits they bring for all stakeholders. For instance, customers enjoy ridesharing because it’s more affordable and convenient, but reducing the number of cars on the road also helps fight pollution. Similarly, flat-sharing could emphasize the tourism revenue it generates.

See also: Smart Things and the Customer Experience Disrupting for Tomorrow

If companies can perform this balancing act – from embracing new technologies, models and services around consumer needs, to preparing for the unknowns that disruption can bring – then they can find huge success in the coming years.

“Disruption is the result of dramatic innovation. And whether business models rise and fall on this is not the point,” Nornes says. Disruption is a bigger trend than the fortunes of an individual company – it’s the rise of new ways, perhaps better ways – of doing things. By recognizing evolving customer needs and forcing new ways of thinking within an organization, companies and their leaders can make sure they are on the right side of history.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

As Guidewire's Chief Innovation Officer, Paul Mang supports senior executives of insurance organizations in refining their innovation strategies to achieve growth objectives. Mang also leads the analytics and data services go-to-market team to help clients leverage analytics to deliver greater value to policyholders.

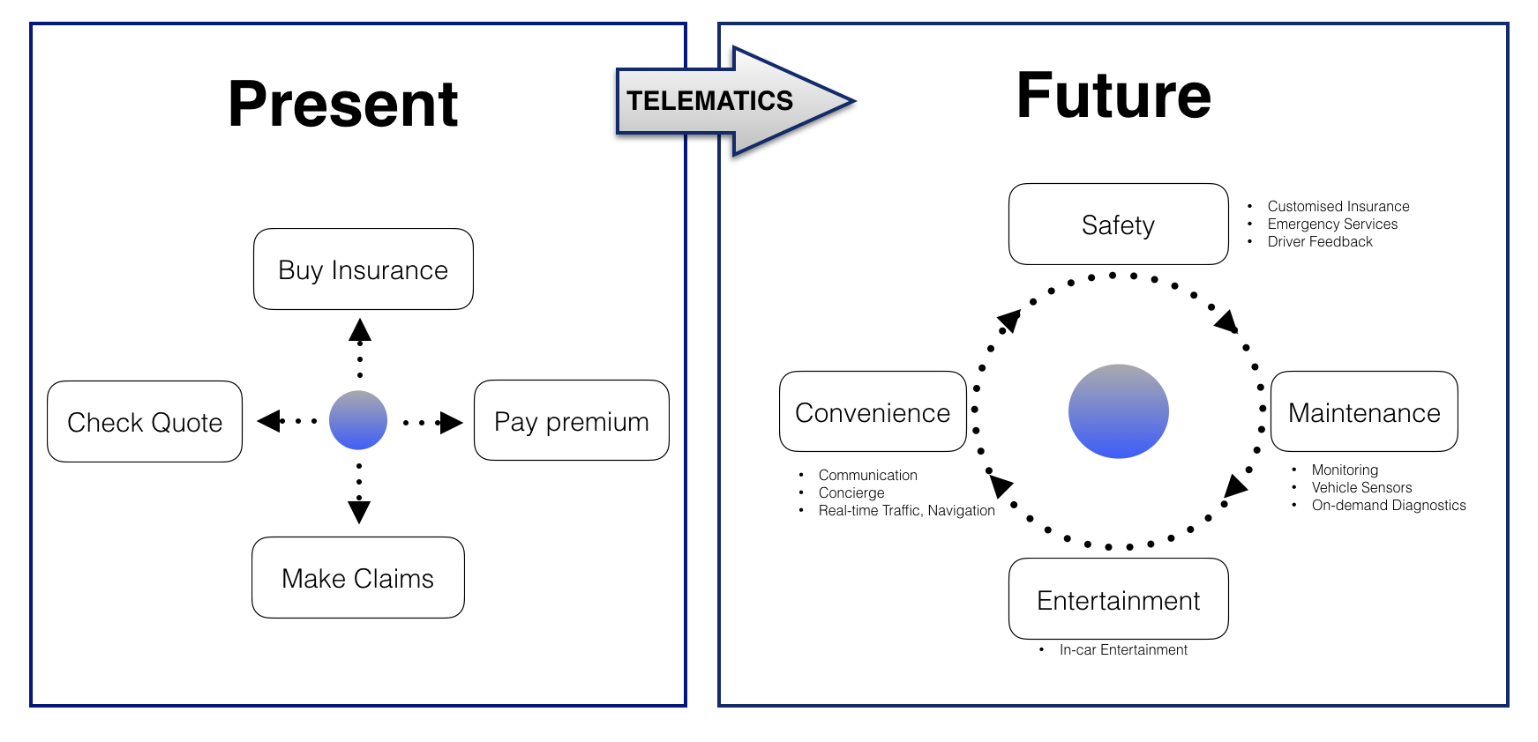

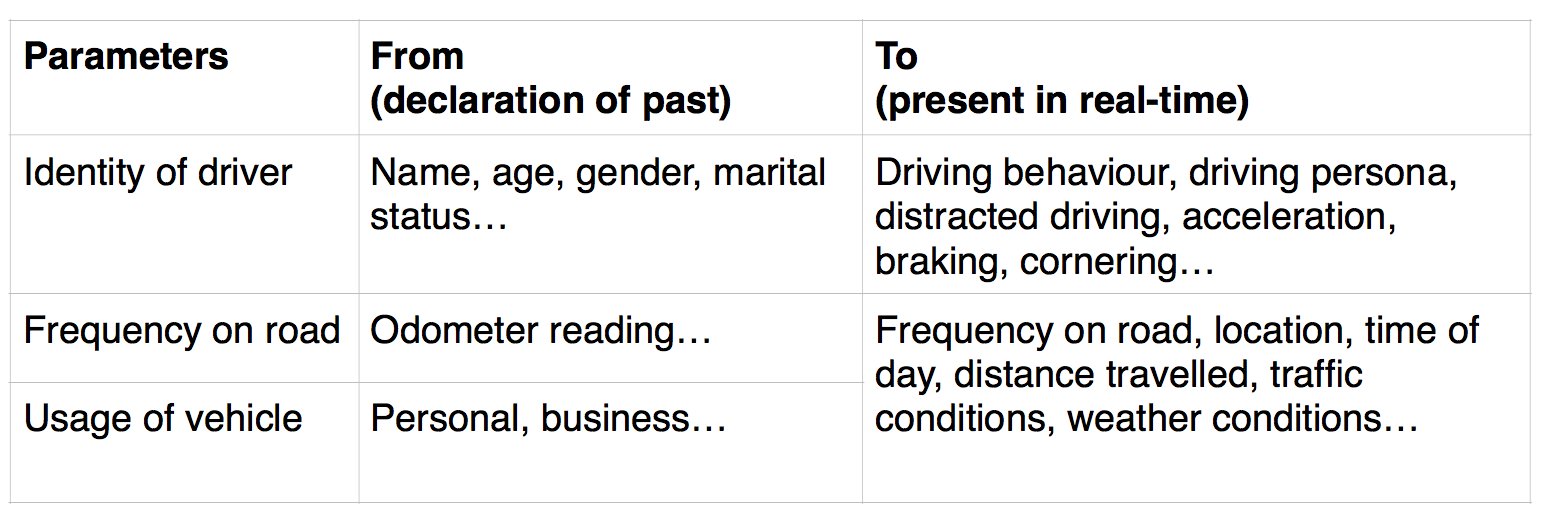

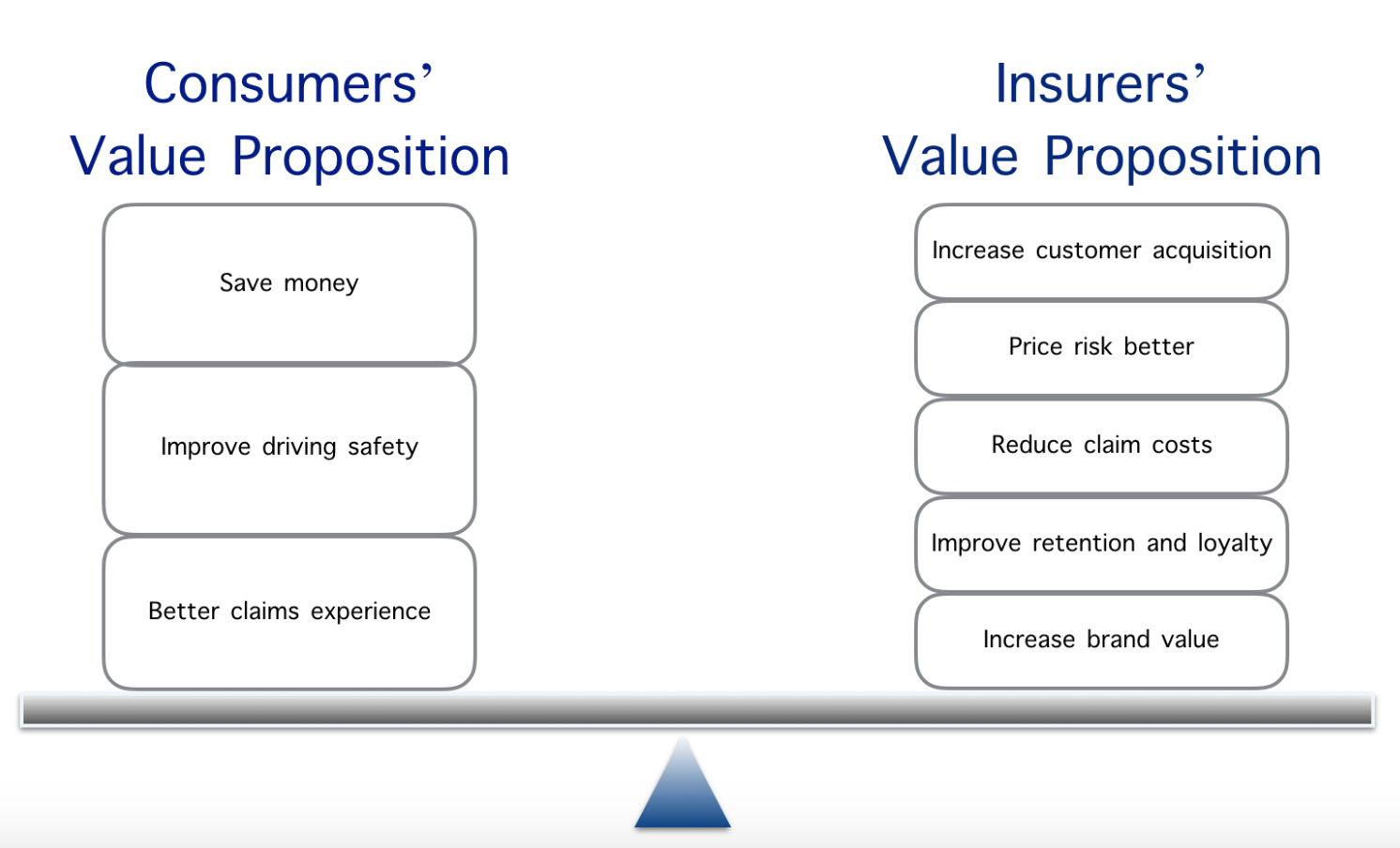

Telematics has the potential to dramatically alter the auto insurance industry, from personalized premiums based on individual driving data to automated emergency services and entertainment-based add-ons to more immediate and active management of claims.

Risk AssessmentValue Proposition

Telematics has much to offer both consumers and insurers.

Solution Analysis

Technology solutions available today are similar in terms of what is possible, but there is a difference in the manner that information is collected, delivered and used. When selecting the most appropriate technology solution and provider to partner with, I recommend the following considerations:

1. Telematics Model (PAYD, PHYD, CYD, Embedded):Several telematics models are emerging with varying levels of consumer interaction and integration.

Pay As You Drive (PAYD)is a mileage-based system that has been around for some time in varying forms. A device is installed in the car to validate when and where a car is driven. More advance systems are available now.

Pay How You Drive (PHYD) considers driving style and behavior in addition to collecting mileage and GPS data. The average driver has one accident every 10 to 12 years, but more common are unsafe driving maneuvers that increase the likelihood of an accident. An accelerometer used in the PHYD models can provide event information such as abrupt acceleration, deceleration, hard braking and sharp turning, which help us understand driving behavior and predict accident claims better.

Control Your Driving (CYD)goes to the next level. While PAYD and PHYD models are about collecting data rather than interacting with consumers, therefore passive in nature, CYD uses the data to provide constructive feedback to drivers through mobile or in-vehicle interfaces and potentially improves driving habits. There is sufficient evidence that driving behavior can be improved with feedback. The teen and elderly markets are niches for early adopters of this model.

Vehicles embedded with telematics devicesare the long-term aspirations of both automakers and insurers. These systems provide all-around safety and driving assistance. These systems usually include services such as adaptive cruise control, collision warning, lane assistance and blind-spot detection. This model is growing fast in the auto market, driven by the safety benefits of reduced driving risk. New technology can enable additional services and features like safety controls activated when poor road conditions are detected by the GPS. BMW’s connected drive is the first step in this direction. Mobileye is helping autonomous cars "see" via crowdsourcing; the company has outfitted 4,500 NYC Uber and Lyft cars with anti collision technology. Some analysts project that all major manufacturers will have embedded telematics solutions in their cars within the next five years.

See also: Game Changer for Auto Telematics 2. Data Protection (collection, use, disclosure and storage of personal information): Telematics generates big data. Therefore, the ownership, collection, use, disclosure and storage of data becomes crucial in gaining trust and loyalty.

Privacy:The success of other industries indicates that people are willing to trade some of their privacy in return for the right services, in the right time at the right place. That has proved true in social media, Uber, online credit card use and internet banking. When it comes to telematics, though, the stigma of insurance companies and the fear that data about driving behavior could be misused are causing concern. To overcome this hurdle, we must be as transparent as possible up front, offer the right amount of value-added services and carefully position the offering with the right messages to win over consumers. The telematics solution selected must provide a feasible program that gets appropriate access to driving patterns without seeking access to too much data. Aggregated driving scores, limitations on driving history and GPS use and specialized onboard data analysis functions could mitigate these concerns. As long as we know about driver safety and potential risks, we don’t need to dive deep into consumers' personal data.

Storage:Dynamically generating data within an automobile or mobile phone creates challenges. The sheer amount of data generated makes it difficult, if not impossible, to store it within the automobile or mobile phone itself. Thus, decisions about what to store, and where, become very important. This issue is amplified by the privacy concern of data storage. In cases where certain pieces of data are not stored within the automobile or mobile phone, the retention aspect of privacy policies becomes important. Once the data is destroyed, there is no way to recover it. Moreover, unlike static data, which is collected only once by any interested party, dynamic data is collected repeatedly by a service provider to keep it up to date. Thus, there has to be a continuous transfer of dynamic data from many vehicles through the telematics service provider to application service providers. This requires an efficient and scalable evaluation of constraints in the privacy policies.

Security:The growth of e-commerce on the web has been limited by the reluctance of consumers to release personal information. 94% of web users decline to provide personal information to websites at one time or another when asked, and 40% who provide demographic data have gone to the trouble of fabricating it. If potential auto telematics users share the concerns of web users, then a large segment of the potential telematics market, perhaps as much as 50%, may be lost. There is significant potential for misuse of data collected. Consumers may substitute false data or hack into vehicle applications. Telematics service providers may sell consumer data to third parties without the permission of consumers. Therefore, telematics applications will be successful if providers know that the data they receive is accurate and if consumers know that their privacy is assured. Data protection must provide both privacy and security protection. Telematics solutions that can achieve that protection while enabling the sharing of data are the most viable options.

3. Ease of Installation (solution access): Complex installation processes (like blackbox installation) result in lack of interest and conversions from the traditional insurance model to the telematics model. AXA launched a mobile telematics solution in some of its international markets but was unsuccessful in acquiring a buy-in from consumers as the app had to be switched on before a drive. Such a solution leaves room for anti-selection and requires additional effort in the day-to-day lives of consumers. Even insurers like Progressive have only managed to convert approximately 20% of their book of business to the telematics model despite more than a decade of marketing initiatives and spending.

4. Ease of Use (interaction and feedback): The telematics solution selected must be intuitive and easy to use for both consumers and insurers. It should help us identify the risk (item that is insured), peril (anything that could cause damage — breakdown, weather conditions, fire, water, ice, road conditions, accident, etc.) and hazards (anything that increases the chances of peril — speeding, hard braking, driving behavior, etc.). The solution must be able to answer questions such as who is driving, how well the person is driving and how much is the car being driven. Mobile telematics solutions must be able to distinguish driving from walking, riding a bike or hopping on a train, bus or boat, for instance. The right solution will employ real-time data analytics and feedback to engage consumers, improve driving safety and facilitate better claims experience and meaningful dialogue with insurers.

5. Accuracy (trust): Our business is built on trust. It is imperative that the telematics solution we implement helps build trust and value in the digital age. Data accuracy is crucial in acquiring a buy-in from consumers, assessing driving behavior, pricing and speed and quality of response during a breakdown or accident.

6. Notifications (auto alerts): Most fleet telematics solutions have failed to create value as the focus has been largely on collection of information alone. Such solutions require someone to run reports, analyze them and understand them before taking corrective actions. This results in delayed feedback to drivers and in most instances becomes reduced to just knowing where vehicles in a fleet are (dots on a map). Automatic notification and alerts facilitate information to be reviewed at the right time, in the right place and by the right person for improved service (safety, accident and roadside assistance) and quality of care.

7. Ease of support (cloud): Cloud-based telematics solutions facilitate the delivery of new or upgraded capabilities without stretching IT bandwidth and keep the total cost of data ownership low. This is imperative if we wish to own the data. If not, then partnering with a solution provider that can maintain and support the solution at scale in an economically viable manner is crucial.

Customer Engagement

Engaging customers to improve driving behavior calls for a change in human behavior.

Humans are not inspired to act on reason alone. You don't connect with your audience by using conventional rhetoric, which in the business world usually consists of a PowerPoint presentation in which you say "here is our company’s biggest challenge, and here’s what we need to do to prosper," while building your case through statistics, facts and quotes from authorities. The problem with rhetoric is two-fold. First, the people you are talking to have their own set of authorities, statistics and experiences, so, while you are trying to persuade them, they are arguing with you in their heads instead of being motivated to reach certain goals. Second, if you do succeed in persuading them, you’ve only done so at an intellectual level. That’s not good enough. The theory of rational action that claims human beings are abstract symbol manipulators much like computers that seek to maximize their self-interest has dominated most of the 20th century and is the foundation for major institutions, from stock markets to governments. Research in the last couple of years, though, has led to a profound shift in how we understand human thought and behavior.

Scientists have pieced together enough evidence to know that humans are embodied beings, which means we work the way we do because of the kinds of brains we have, the kinds of bodies we have and the typical experiences that pervade our evolutionary history. We know now how real human nature works (mostly). The big picture is that we are profoundly moral beings, and our behavior is shaped by value judgments, deeply held beliefs and assertions about right and wrong. We are profoundly social, and our behavior is influenced by the behavior of those around us through shared stories, common expectations and need for cooperation (and competition). We make decisions through context-based logic determined by how we understand the situations we find ourselves in and reason with our emotions. Try asking someone on a date without those subtle emotional cues of presence, enthusiasm and appeal.

I believe that something as simple as fun can influence human behavior for the better. In a series of experiments, Volkswagen tested this theory. Check it out…

The speed camera lottery

Can we get people to obey the speed limit by making it fun to do so? The winning idea was so good that Volkswagen, together with the Swedish National Society for road safety, actually made this innovative idea a reality in Stockholm.

Piano Stairs

Can we get more people to take the stairs instead of the escalators by making it fun to do so? Piano stairs created on Odenplan underground station in Stockholm have become a hit in cities worldwide from Milan to Santiago and more.

The way to persuading people and ultimately a much more powerful way is by uniting an idea with an emotion. It comes down to good design in our attempts to change human behaviour and will depend on our understanding of REAL human nature. Knowing where we went wrong in the past and what we know now is right, we can engage and design models to promote socially desirable outcomes like reduction in environmental impact and greater sensitivity to the needs of others.

See also: 5 Value Levers for Auto Telematics

Using the fun theory to improve driving behavior is a tested formula that has worked globally and one that I would recommend as a first step. Create a competition that is built off recognition and rewards good behavior. Huge, safe-driving campaigns could be turned into beautiful marketing messages that people would be proud to be a part of. The intelligence and data we collect could change the way we do business altogether.

Liberty Insurance: Drive Well from Michael Hanson on Vimeo.

Delivery

Inventing a future and testing ideas is not enough. To bring auto telematics solution to life, models need to change from actuarial to actuarial plus big data. Implementation will require collaboration between solution providers, underwriters, actuaries and product and marketing teams to create economically viable customer propositions, storytelling and messaging that connects with your audience and keeps their attention long enough to convert.

Scale

Companies like Uber and Lyft struggle with public perception and regulations globally. Partnering with them and creating compelling value propositions for their drivers presents an opportunity for efforts in auto telematics to scale quickly.

Conclusion

The winners will be early movers that capture the safest drivers, take advantage of pricing power and strengthen customer relationships while easing privacy concerns.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Shahzadi Jehangir is an innovation leader and expert in building trust and value in the digital age, creating scalable new businesses generating millions of dollars in revenue each year, with more than $10 million last year alone.

Senior management have to come to grips with the fact that digital transformation is not an event but rather the operating environment of 21st century business.

Like music, photos, TV, and data, once something becomes digital it becomes a consumable and moves from the domain of the specialized expert to a public commodity. As with Blockbuster, Borders, Capital Records and newspapers, businesses based on non-digital product are the hand-crafted hobbies of the 21st century. Craft markets will exist into the future, but they are generally not profitable and rather a labor of love.

Changing the way we work

Here’s the kicker. Digital transformation is now looking at not just the things we sell, which includes services, by the way, but how we do business. From crowd funding to network marketing to blockchain (how Bitcoin works), the basic principles of how we have traditionally gone about business are changing.

Crowd funding, where a population at large is directly involved in the creation of products, also has ramifications for invention and design. Brainstorming on steroids. Network marketing has wiped out traditional sales channels from cold calling and direct mail to bricks and mortar retailing. And blockchain has the capability to render capital-intensive industries obsolete. What Bitcoin did to money, people are now looking to use to undermine energy, insurance and infrastructure oligarchies. One day, blockchain may even be capable of fixing our political system.

See also: 4 Rules for Digital Transformation Understanding Digital Transformation

What really is digital transformation? Gartner, a leading authority on such things, defines digital transformation as “to leverage digital technologies that enable the innovation of their entire business or elements of their business and operating models.”

So innovating is not just what we do, but how we do it, our “operating models.” In my last article, “Misunderstanding Innovation,” I wrote on how innovation is not invention but rather the application of invention as a solution to a practical need. As such, innovation is the backbone of digital transformation, just as audit is to compliance or controls are to risk.

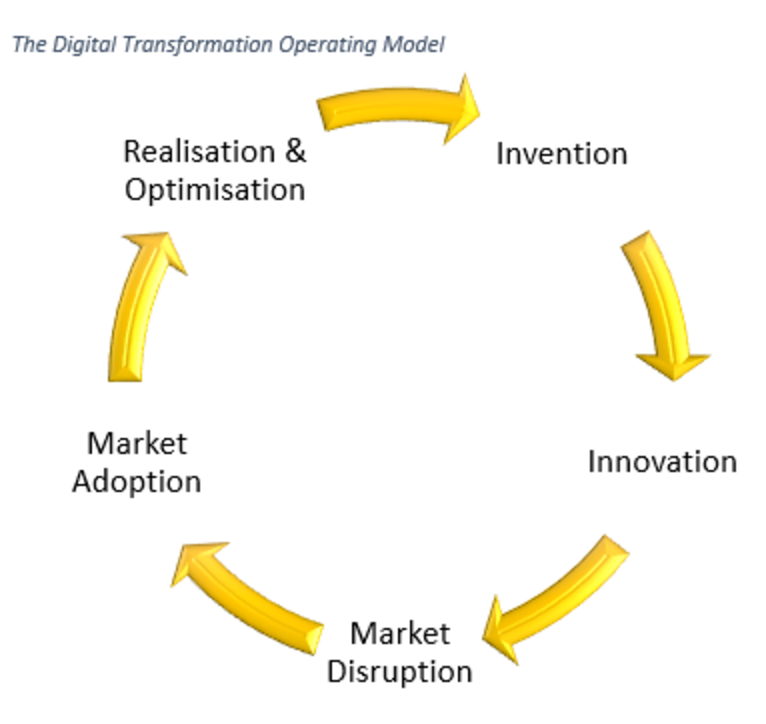

Digital Transformation as an Operating Model

Back to my opening statement that digital transformation should not be thought of as an event but rather an operating environment, just as industrialization in the 18th century was not a single event but a period of continual transformation. From the introduction of the weaving loom through production lines to mass production, the transformation fed change that has continued for 200 years.

Senior management have to stop thinking of digital transformation as a passing fad, and embrace the fact that the world has changed. As in the 18th and 19th centuries, change will drive change, and as the management in those times developed process management models (see, PDCA is NOT Best Practice) to drive the development of automated production, so, too, managers now have to develop transformation models to take account that disruption and innovation will drive further disruption and innovation.

Transformation as a Lifestyle Choice

The fact that you have transformed your operation today is only a temporary reprieve. You need to redefine your business model to be an agile platform continually identifying and innovating to improve end-customer quality of life: That’s your customer’s customer.

Women as the Mothers of Innovation

The current beat-up of getting more women involved in STEM (science, technology, engineering, math) misses the understanding that innovation has at its root, a deep empathy for the quality of life of others. Developing and elevating women’s inherent intuition as to the plight of others will do more to foster innovation than a plethora of inventions. Hundreds of inventions never see the light of day, yet a handful of innovations have changed the world. Again, please re-read my previous article on Misunderstanding Innovation.

If Malcolm Turnbull truly wants Australia to develop an innovative culture, we should be promoting more people into psychology, sociology, anthropology and statistics. These are the strategic vocations of innovation, while STEM and invention are the tactical solutions. Yes, stats is math, but it allows us to understand bias as well as predictive analytics, which identifies and prioritizes targets for innovation.

See also: Why You Need a Digital Leader Where to From Here?

Accepting the need to transform your business model is in itself an inherent risk. Just as a window cleaner straps on a safety harness before scaling a building, so having an active risk and compliance system operational is a mandatory prerequisite before embarking on any transformation. You will need systems that alert you to emerging issues and to give you continual insight, throughout the transformation process, without the need to go and look for it. The business graveyard is as full of those who lost their footing on the way as those who did nothing. This is not a shameless plug for what I do but rather the reason I do it.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Greg Carroll is the founder and technical director, Fast Track Australia. Carroll has 30 years’ experience addressing risk management systems in life-and-death environments like the Australian Department of Defence and the Victorian Infectious Diseases Laboratories, among others.

With the imminent arrival of autonomous vehicles to the roads, many people have started worrying about the safety of this new technology, especially when an issue arises to do with choice.

In this piece, we'll delve into the issue of the "Trolley Problem" and how AVs will deal with this and whether all manufacturers have the same stance.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Helen Green writes about all things design and automotive market research. She specializes in infographics and articles that are both informative and fun to read.

In the U.S., the life insurance participation rate is in a steady decline, reaching new lows each year. This, coupled with insufficient savings, creates financial instability for millions. An early or unexpected death of a loved one creates a vacuum of loss, bills, debt and reduced income that is both devastating and unnecessary. Preventable poverty due to lack of savings and insurance is on the rise, even among the employed and financially thriving.

Analysts and industry leaders have tried to understand the motivations and aspirations of millennials who “believe they will live forever” or haven’t grown up and “live in their parents’ basements.” While psychological and lifestyle factors certainly contribute to empty savings accounts and a dearth of insurance policies, the truth is a far more mundane structural issue: no one is selling insurance to the younger generation.

The industry adage that life insurance is “sold, not bought,” is proving true through its decline. The historical insurance sales approach – an army of captive and independent insurance agents providing a consultative sale to customers—is becoming more and more ineffective over time. Today, only 26% of Americans own their own life policies. Why is that?

The average age of a life insurance agent in the U.S. is 59, and agents tend to sell within five years of their own age. This leaves the bulk of millennials and even Gen X potential customers without the advice, education and handholding that their insured predecessors have had. This gap leaves young families, who most desperately need the protection, underinsured and in a state of potential poverty if tragedy strikes.

This endemic crisis is evident on the memorial pages of GoFundMe, where one can scroll through page after page of “my brother-in-law suddenly passed away and the family needs help to pay for the funeral and provide for the family.” Successful campaigns raise as much as $50,000 – an amount woefully low for the future liabilities of family and future.

See also: Where Price-Focused Sales Are Heading

Younger customers have different needs and priorities than previous generations. They prefer to use technology to find the information they need about insurance and to buy a policy. Many younger customers are not sold on the need for life insurance; however, once educated on the benefits are likely to purchase a policy. In fact, 86% of Americans overestimate the cost of life insurance, some by as much as 300%. And among the insured in America, many are grossly underinsured, including the 32% who have less than $100,000 in coverage.

Insurance innovations

In the last 50 years, the way insurance companies do business has changed very slowly. Even in recent years, where other industries such as banking, payments and retail have had to shift their distribution models in major ways, insurance is still only dipping its toes in new sales models, even as their workforce careens toward retirement.

That said, there have been incredible leaps forward in making it easier for consumers to BUY insurance. Insurance companies are investing hundreds of millions in expanding products and services to make it easier for the interested buyer to make an informed purchase quickly, less intrusively and for the best price, all while retaining the financial viability that customers require.

Key investments in data and analysis gave birth to no-exam life insurance policies known as simplified issue insurance. These policies require no medical exam or blood test and are beginning to be offered at greater and greater face values.

This innovation is made possible through a massive data-sharing initiative between healthcare providers, insurers and governments. The data-sharing allows insurers to gather information to assess various risk factors for potential policyholders, even in the absence of the medical exams and blood tests that were once necessary.

Many insurance carriers have also pivoted their direct marketing focus to online sales and digital purchase and enabled a new generation of price comparison engines to ensure those in the market for a policy can easily buy it. Some of these shifts have created channel conflict with the declining direct salesforce, and that conflict often results in hamstrung marketing initiatives that attempt to satisfice amid this dialectic and strategic conflict.

These one-sided investments on the buy side of insurance primarily serve the needs of those who have already opted into the marketplace. But that leaves the question: Where is the real innovation that will close the insurance sales gap?

Closing the sales gap?

In a world where three in four Americans do not own life insurance and 50% of millennials would have an immediate financial need if something were to happen to the primary wage earner in their household, it is now a societal need to close this gap.

The insurance industry needs to look beyond its own agents. Consumers depend on many advisers for financial services, and the industry needs to engage those providers. Paving the way for broader licensing and reducing barriers erected to protect carriers (not the ones for protecting consumers) will help bring more educators and salespeople to the industry.

Insurance digital investments must do more than digitize the past. While making it possible to buy insurance online is an advance, it still resides in the Web 1.0 world of price-comparison and lead generation.

Break down barriers between insurance and adjacent industries. While it has always been true that the person who designs your estate plan is not the person who sells you the appropriate amount or insurance or defines your future investment needs, the consumer doesn’t want to find multiple vendors and convince them to work together. In a modern world, these artificially siloed industries should simply work together.

See also: How to Move to the Post-Digital Age?

It was through these observations with fellow World Economic Forum attendees that I saw the need to create the Tomorrow app. Using Tomorrow, families can set up a trust fund for free, including a free will and revocable living trust. In fact, it’s a social experience one does with family and friends who will take on roles such as guardian, executor and trustee. Then, with an understanding of one’s family and finances, Tomorrow educates its customers about their insurance gap, prices the policies that close that gap and brings customers to a policy application. Because Tomorrow leverages all of the data entered to create their trust funds, customers complete the application in three to five minutes, and the policy is added to their trust. For simplified issue policies, that is often the end of the customer’s work, and policies are issued in a matter of days.

Sales innovation is the way forward

McKinsey estimated in 2015 that 20% of insurance agents in the U.S. would retire by 2018, leaving a talent gap in an industry that already has a worker shortage. This is significant on its own, but, considering that current insurance agents fail to reach the under-40 set, more than ever the industry desperately needs disruptive changes.

The only way forward is innovation in insurance sales through breaking down barriers, investing in modern digital approaches and looking beyond the insurance industry.

The article was originally published here.`

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Dave Hanley is CEO of fintech startup Tomorrow. Previously, Hanley founded Banyan Branch, a social media marketing agency acquired by Deloitte Digital, and was vice president of marketing at Shelfari, the social network for book readers. He helped grow it to more than 2 million members in 18 months before Amazon acquired it.

If insurtech disruptors have one thing going for them, it’s their digital savvy.

They have made it as easy for consumers to research, quote and buy coverage online as it is to make a retail purchase through e-commerce channels. “It took me 60 seconds to buy a policy,” a customer of one disruptor said.

Still, insurtech disruptors have a lot to learn about the industry, and some leading incumbents could be the ones to teach them.

The Disruptor’s Downward Spiral

To understand this better, let’s follow Judy, a quintessential customer as she excitedly makes the decision to purchase insurance from a typical disruptor.

First, she enters the site. It’s sleek and beautiful, and everything is easy to locate. Within seconds, she has selected the option to get a quote for her auto insurance, has entered her information and received a price she can live with. Hooray! But wait. Where is the coverage for her home, motorcycle and pet?

She searches the site but can’t find other insurance products. She clicks the help button, but all she can do is send an email with her question. Where is the personal touch? And how will she contact someone later when she has a question about her coverage or, worse, a claim?

See also: What’s Your Game Plan for Insurtech? The Lessons

The first thing disruptors need to learn is that the quick, convenient online service they are peddling is only the baseline model of what consumers expect from their carriers. Comments from other customers echo Judy’s feelings about the personal touch: “They do not have a phone number, so you are stuck dealing with bots and sending messages through their app.”

Hmmmm. Sounds like someone needs an agent.

Greg Hoeg, vice president of U.S. insurance operations at J.D. Power, concurs, “While many consumers want to shop online, they often still want to talk to someone when they buy their insurance to make sure they are getting the right coverage or have questions about their policy answered.”

J.D. Power also confirms the importance of digital channels in the buying process, reporting that incumbents with leading digital capabilities also lead in premium growth. And this is where incumbents come in to teach the disruptors a thing or two.

Following a Better Example

Top digital insurers are setting the best example of how to thrive in the changing market. They have continuously improved their capabilities to meet consumer demands for online buying and product choice and have empowered agents with top-grade digital tools.

Here is what Judy’s purchasing journey looks like with a traditional insurer imbued with the right digital capabilities and product selection:

Judy enters the site and begins the application process. After providing a few bits of personal data, a smart application process begins to draw information from verified third-party sources, auto-filling her application along the way.

Throughout the process, she is asked if she would like to add other types of coverage she is eligible for, such as home, jewelry or pet insurance. She clicks "yes" and is soon provided with quotes on multiple options. She has a question about one of the offerings, so she dials the number prominently displayed at the top of the screen.

Soon, she is talking with an agent who answers her questions and, without having to gather more information, quickly and seamlessly binds and issues all of the coverage types she wants to buy, in a single transaction.

Experiences like these are not the future of insurance. The capabilities exist today, without making extensive changes to current systems. A top-five insurer is already setting the example. It now meet the needs of 95% of current and future customers contacting the agency and has doubled year-over year growth through direct and agent channels.

Insurers like these have a message for insurtech disruptors and incumbents alike. It’s time to implement digital solutions and start meeting consumer needs for channel and product choice.

See also: Insurtech Checklist: 10 Differentiators To learn more about outcompeting in a changing industry, download our thought leadership piece, The Changing P&C Insurance Industry: What’s It Costing You?

Get Involved

Our authors are what set Insurance Thought Leadership apart.

It is projected that, by the year 2020, there will be 7 million drones in the U.S. alone. Most consumers buy drones for recreational use, but businesses have begun to use drones, as well. Drones are used by photographers to obtain better camera angles, by farmers for crop surveillance and by media outlets for coverage of newsworthy events. Amazon has even launched Amazon Prime Air, which uses drones to get shipments to customers in 30 minutes or less.

A similarly important shift is the rise of the gig economy, in which 55 million Americans offer their services and assets — homes, cars, labor — to earn supplemental or full-time income. Recently, these two phenomena have intersected. Drone use, in combination with the gig economy, will significantly improve various aspects of the insurance supply chain.

See also: Gig Economy: Newest Tool for Insurance Insurance and Drones

Drones can help the insurance industry by improving data quality, providing unprecedented views, ensuring safety and increasing the speed at which claims can be resolved. These new realities are incredibly important for the insurance sector.

By flying drones over damaged houses or other properties, operators can acquire high-quality video footage that accelerates and improves claims resolution processes. Drone footage can immediately be sent back to carriers for analysis.

Drones can significantly reduce the risks associated with field inspections. By leveraging drones, insurance adjusters can avoid climbing ladders and even setting foot in damaged buildings. Operators can remain safely on the ground and fly their drones over damaged property or disaster areas.

Insurance and the Gig Economy

Insurance carriers are already able to tap into the power of gig economy platforms to complete any number of tasks. At WeGoLook, for instance, we connect a network of 30,000 gig workers with insurance carriers across North America. At the swipe of a smartphone, a Looker can be dispatched to conduct a damage assessment, asset verification, scene inspection, document retrieval or any number of other tasks or processes. The gig economy not only offers insurers the ability to fulfill these needs affordably and at scale, but it can also help to accommodate workload surges brought on when natural disasters strike.

Bringing It All Together

Gig economy platforms are now beginning to offer drone services. These services combine the power of drone technology with the convenience and accessibility of gig solutions, making drones more accessible than ever for insurers.

Gig workers who own drones can be dispatched by insurers to conduct a variety of tasks. An insurer could hire its own drone workforce, but this would be time-consuming and expensive. Gig platforms allow insurers to completely outsource drone operation and training that would otherwise require significant upfront investment. Further, insurers don’t need to worry about how to train operators, conduct maintenance or insure against unintended damages.

The gig economy’s on-demand model can be tapped at any moment. This efficiency, combined with the use of drones, is vastly improving the time to process insurance claims.

WeGoLook’s COO, Kenneth Knoll, provides an example of this type of efficiency: “We recently received an assignment that involved capturing aerial imagery of a commercial location where an injury occurred and details were needed as part of the case. As opposed to photos from the ground, the aerial imagery was much more effective to illustrate the exact conditions of the scene in question. Plus, our drone footage was delivered to the carrier within 24 hours, thanks to the efficiency of our on-demand workforce.”

Given all the benefits of drone technology and the increasing availability of drone services via gig economy platforms, there’s a good chance that a drone will be involved in your next insurance claim. Insurance professionals and customers can look forward to better data, faster resolution times and safer inspections.

See also: What Gig Economy Means for Insurers Final Thoughts

Roughly 34% of the U.S. workforce currently participates in the gig economy in some way. When you combine these numbers with 7 million drones that will be owned by Americans by 2020, this creates the potential for a vast network of drone pilots working in a freelance capacity.

These freelance drone pilots can be helpful for insurance companies, insurance policyholders and gig economy companies that crowdsource and connect them with jobs. There’s no doubt that drones, in combination with the gig economy, will bring significant benefits for the insurance industry.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Robin Roberson is the managing director of North America for Claim Central, a pioneer in claims fulfillment technology with an open two-sided ecosystem. As previous CEO and co-founder of WeGoLook, she grew the business to over 45,000 global independent contractors.

According to the World Health Organization, mental health is described as: “a state of well-being in which every individual realizes his or her own potential, can cope with the normal stress of life, can work productively and fruitfully and is able to make a contribution to his or her community.” But the World Health Organization’s definition applies only to part of the population.

At any given time, one in five American adults suffers with a mental health condition that affects their daily lives. Stress, anxiety and depression are among the most prevalent for injured workers. Left untreated, they can render a seemingly straightforward claim nearly unmanageable, resulting in poor outcomes and exorbitant costs.

Increasingly, many in our industry are recognizing the need to do all we can to address this critical issue. We must openly discuss and gain a deep understanding of a subject that, until now, has been taboo.

Four prominent workers’ compensation experts helped us advance the conversation on mental health in the workers’ compensation system during a recent webinar. They were:

Bryon Bass, Senior Vice President for Disability, Absence and Compliance at Sedgwick

Denise Zoe Algire, Director of Managed Care and Disability for Albertsons Companies

Maggie Alvarez-Miller, Director of Business and Product Development at Aptus Risk Solutions

Brian Downs, Vice President of Quality and Provider Relations at the Workers’ Compensation Trust

Why It Matters

Mental health conditions are the most expensive health challenges in the nation, behind cancer and heart disease. They are the leading cause of disabilities in high-income countries, accounting for one third of new disability claims in Western countries. These claims are growing 10% annually.

In addition to the direct costs to employers are indirect expenses, such as lost productivity, absenteeism and presenteeism. Combined with substance abuse, mental health disorders cost employers between $80 billion and $100 billion in these indirect costs.

In the workers’ compensation system, mental health conditions have a significant impact on claim duration. As we heard from our speakers, these workers typically have poor coping skills and rely on treating physicians to help them find the pain generator, leading to overuse of treatments and medications.

See also: Top 10 Ways to Nurture Mental Health

More than 50% of injured workers experience clinically related depressive symptoms at some point, especially during the first month after the injury. In addition to the injured worker himself, family members are three times more likely to be hospitalized three months after the person’s injury. Many speculate that the distraction of a family member leads the injured worker to engage in unsafe behaviors.

Mental health problems can affect any employee at any time, and the reasons they develop are varied. Genetics, adverse childhood experiences and environmental stimuli may be the cause.

The stress of having an occupational injury can be a trigger for anxiety or depression. These issues can develop unexpectedly and typically result in a creeping catastrophic claim.

One of our speakers relayed the story of a claim that seemed on track for an easy resolution, only to go off the rails a year after the injury. The injured worker in this case was a counselor who had lost an eye after being stabbed with a pen by a client. Despite his physical recovery, the injured worker began to struggle emotionally when he finally realized that for the rest of his life he would be blind in one eye. Because his mental health concerns were raised one year after the injury, there were some questions about whether he might be trying to game the system.

Such stories are more commonplace than many realize. They point out the importance of staying in constant contact with the injured worker to detect risk factors for mental health challenges.

Challenges

Mental health conditions — also called biopsychosocial or behavioral health — often surprise the person himself. Depression can develop over time, and the person is not clued in until he finds himself struggling. As one speaker explained, the once clear and distinct lines of coping, confidence and perspective start to become blurred.

In a workers’ compensation claim, it can become the elephant in the room that nobody wants to touch, talk about or address. Organizations willing to look at and address these issues can see quicker recoveries. But there are several obstacles to be overcome.

Stigma is one of the biggest challenges. People who realize they have a problem are often hesitant to come forward, fearing negative reactions from their co-workers and others.

Depictions of people suffering from behavioral health issues in mass media are often negative, but are believed by the general public. Many people incorrectly think mental health conditions render a person incompetent and dangerous; that all such conditions are alike and severe; and that treatment causes more harm than good.

As we learned in the webinar, treatment does work, and many people with mental health conditions do recover and lead healthy, productive lives. Avoiding the use of negative words or actions can help erase the stigma.

Cultural differences also affect the ability to identify and address mental health challenges. The perception of pain varies among cultures, for example. In the Hispanic community, the culture mandates being stoic and often avoiding medications that could help.

Perceptions of medical providers or employers as authority figures can deter recovery. Family dynamics can play a role, as some cultures rely on all family members to participate when an injured worker is recovering. Claims professionals and nurses need training to understand the cultural issues that may be at play in a claim, so they do not miss the opportunity to help the injured worker.

Another hurdle to addressing psychosocial issues in the workers’ compensation system is the focus on compliance, regulations and legal management. We are concerned about timelines and documentation, sometimes to the extent that we don’t think about potential mental health challenges, even when there is clearly a non-medical problem.

Claims professionals are taught to get each claim to resolution as quickly and easily as possible. Medical providers — especially specialists — are accustomed to working from tests and images within their own worlds, not on feelings and emotional well-being. Mental health issues, when they are present, do not jump off the page. It takes understanding and processes, which have not been the norm in the industry.

Another challenge is that the number of behavioral health specialists in the country is low, especially in the workers’ compensation system. Projections suggest that the demand will exceed the supply of such providers in the next decade. Our speakers explained that, with time and commitment, organizations can persuade these specialists to become involved.

Jurisdictions vary in terms of how or whether they allow mental health-related claims to be covered by workers’ compensation. Some states allow for physical/mental claims, where the injury is said to cause a mental health condition — such as depression.

Less common are mental/physical claims, where a mental stimulus leads to an injury. An example is workplace stress related to a heart attack.

See also: New Approach to Mental Health

“Mental/mental claims” mean a mental stimulus causes a mental injury. Even among states that allow for these claims, there is wide variation. The decision typically hinges on whether an "unusual and extraordinary" incident occurred that resulted in a mental disability. A number of states have or are considering coverage for post-traumatic stress among first responders. The issue is controversial, as some argue that the nature of the job is, itself, unusual and extraordinary and that these workers should not be given benefits. Others say extreme situations, such as a school shooting, are unusual enough to warrant coverage.

What Can Employers Do

Despite the challenges, there are actions employers and payers are successfully taking to identify and address psychosocial conditions.

For example, Albertsons has a pilot program to identify and intervene with injured workers at risk of mental health issues that is showing promise. The workers are told about a voluntary, confidential pain screening questionnaire. Those who score high (i.e., are more at risk for delayed recoveries) are asked to participate in a cognitive behavioral health coaching program.

A team approach is used, with the claims examiner, nurse, treating physician and treating psychologist involved. The focus is on recovery and skill acquisition. A letter and packet of information is given to the treating physician by a nurse who educates the physician about the program. The physician is then asked to refer the injured worker to the program, to reduce suspicion and demonstrate the physician’s support.

Training and educating claims professionals is a tactic some organizations are taking to better address psychosocial issues among injured workers. The Connecticut-based Workers’ Compensation Trust also holds educational sessions for its staff with nationally known experts as speakers. Articles and newsletters are sent to members to solicit their help in identifying at-risk injured workers.

Continuing communication injured workers is vital. Asking how they are doing, whether they have spoken to their employer, when they see themselves returning to work reveal underlying psychosocial issues. Nurse case managers can also be a great source of information and intervention with at-risk injured workers.

Changing the workplace culture is something many employers and other organizations can do. Our environments highly influence our mental health. With the increased stress to be more productive and do more with less, it is important for employers to make their workplaces as stress free as possible.

Providing the resources to allow employees to do their jobs and feel valued within the organization helps create a sense of control, empowerment and belonging. Helping workers balance their work loads and lives also creates a more supportive environment, as does providing a safe and appealing work space. And being willing to openly discuss and provide support for those with mental health conditions can ensure workers get the treatment they need as soon as possible.

As one speaker said, “By offering support from the employer, we can reduce the duration and severity of mental health issues and enhance recovery. Realize employees with good mental health will perform better.”

To listen to the full webinar on this topic, click here.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Kimberly George is a senior vice president, senior healthcare adviser at Sedgwick. She will explore and work to improve Sedgwick’s understanding of how healthcare reform affects its business models and product and service offerings.

Mark Walls is the vice president, client engagement, at Safety National.

He is also the founder of the Work Comp Analysis Group on LinkedIn, which is the largest discussion community dedicated to workers' compensation issues.