Embracing a growth mindset and understanding how new disruptive technologies could change our industry are among the best strategies to prepare for the opportunities and challenges of the Fourth Industrial Revolution. I highlighted some of the new disruptive technologies in Part 1 and Part 2 of this blog series.

At Gen Re, we advise clients to routinely update their companies’ boards on how artificial intelligence (AI) advancements and collaborative robots are changing their clients’ industries and whether technology is replacing or complementing workplace activities.

What are some critical actions for evaluating AI and developing technologies?

1. Separate the hype from reality. The amount of information can be overwhelming for any CEO or board, so consider getting assistance from trusted advisers in tracking developments.

2. Focus on the core practices, processes, products and people at your customer organizations. Your policyholders’ employees can help you analyze which industries in their portfolio are most vulnerable to automation within the next five years. If a critical assessment reveals that a significant part is susceptible to obsolescence, examine whether product development, market expansion or new partnerships can provide a buffer for anticipated premium or market share loss.

3. Don’t overlook your own underwriting and claim operations. Can you use AI to improve your own underwriting results or identify creeping catastrophic claims? Having a work culture that encourages a growth mindset and embraces new technology is essential.

4. Critically track and examine the legal and regulatory issues that can slow the adoption of AI, robotics and automation. While AI technology continues moving forward, many legal and ethical questions surrounding this technology remain unanswered. Driverless technology provides one pressing example for insurers. As Warren Buffett commented at the 2017 Berkshire Hathaway annual meeting, “If driverless cars became pervasive, it would only be because they were safer,” which would mean that “the overall economic cost of auto-related losses had gone down and that would drive down the premiums" for insurance companies. We do not know when driverless technology will be widely adopted, but we know that now is the time to prepare for its impact on auto, umbrella and workers’ comp portfolios.

5. Don’t wait. It is not too soon to start the journey toward understanding the impact and possibilities of AI, robotics and automation. Ignoring the trend can be costly regardless of what lines of insurance you write.

Frank Bria is a senior vice president and treaty account executive for Treaty’s Regional & Specialty Cos., responsible for strategically growing and maintaining Gen Re’s relationships with senior management and executive boards of P/C insurers.

As the insurance industry continues down the path toward digital transformation, it is being inundated with data being generated by many different connected devices and systems. Enterprise data is growing so rapidly that analysts at IDC predict the worldwide volume of data will increase ten-fold to 163 zettabytes by 2025.

With the rise in volume and accessibility of data, comes an increased risk of data breaches. In the first half of 2019 alone, nearly 4,000 data breaches occurred, resulting in more than 4 billion records being compromised. On top of these challenges, insurers are also subject to an ever-changing list of complex regulatory requirements and industry standards meant to strengthen data security and consumer privacy. From the EU’s General Data Protection Regulation (GDPR) to the Payment Card Industry Data Security Standard (PCI DSS), the New York Department of Financial Services’ (NYDFS) Cybersecurity Regulation to the Insurance Data Security Model Law, insurers face a complex regulatory landscape.

Strategically moving some core business functions to the cloud can provide insurers with many benefits that can address these challenges head-on, including increased data security, business flexibility and scalability, better ease of compliance and reduced infrastructure and capital expenditure costs.

The insurance industry has been hesitant about cloud adoption, due in part to the widespread use of legacy technologies, a desire for single-handed control of data and the nature of being a highly regulated industry. Yet, when done right, moving key systems and IT functions to the cloud can benefit insurance firms in spades. Innovations in the cloud can make it easier for organizations to not only comply with industry standards but also better safeguard customer data, all while providing a great customer experience.

How the Cloud Can Help

According to Gartner, expenditures toward cloud-based enterprise IT offerings are increasing at almost triple the rate of spending on more traditional, non-cloud solutions. The firm also found that more than $1.3 trillion in IT spending will be affected, directly or indirectly, by the shift to the cloud by 2022. This trend underscores the many benefits that organizations are reaping from the shift to the cloud.

To realize these benefits, insurance organizations must start joining the pack and look to migrate key parts of their business and IT infrastructure to the cloud. For example, providers can strengthen data security and ease compliance with PCI DSS by moving their payments systems to the cloud. Because insurers process and store tremendous amounts of sensitive consumer data and personally identifiable information (PII) – like Social Security numbers, bank account numbers, dates of birth and payment card numbers – insurers are prime targets for hackers. Traditionally, when a customer calls an insurer to make a payment, the customer speaks with a service representative and reads payment card details aloud over the phone. Likewise, if the customer uses the website to make a payment, sensitive payment card information is collected via a web form or e-commerce platform integrated into the insurance company’s computer network. In both scenarios, as soon as the sensitive data enters the organization’s network infrastructure, the insurer is responsible – both from a compliance perspective and in terms of customer expectations – for protecting that data. By making the shift to a secure, cloud-based payments processing solution, organizations can keep sensitive payment card data out of their infrastructure completely, thus reducing the risk of a data breach and minimizing the scope of compliance for numerous regulations.

How Cloud-Hosted Payments Solutions Can Strengthen Data Security

Let’s say a customer chooses to call an insurer to make a payment. Cloud-based, dual-tone multi-frequency (DTMF) masking solutions, for example, allow callers to give their payment card data securely over the phone. The customer simply enters the card number directly into the telephone keypad. The DTMF tones of the telephone keypad are replaced with flat tones, making them indecipherable to an agent on the line or to a nefarious eavesdropper. Alternatively, the agent could send an SMS text message with a secure payment hyperlink to the caller’s mobile phone. The caller simply clicks on the hyperlink and enters payment information. In either scenario, the agent is able to stay on the line in full voice communication with the customer for the duration of the transaction, helping to troubleshoot, if necessary, and providing a frictionless and secure customer experience. Because a cloud-based payments solution sits between the telephony carrier and the contact center’s network, the payment card data is encrypted and securely routed directly to the payment service provider (PSP) for processing – keeping the sensitive data out of the organization’s network infrastructure completely.

Likewise, if a customer uses the insurer’s website to make a payment, cloud-based digital payments solutions can make the transaction more secure and provide a better customer experience, all while streamlining regulatory compliance. Say a customer is interacting with a customer service representative via web chat. When the customer wants to make a payment, the agent can send a secure payment hyperlink to the customer right in the chat window. The customer clicks on the link and is presented with a secure web form, where the customer can enter payment card information. Again, the sensitive payment data is routed directly to the PSP and never enters the insurer’s network.

In all the scenarios described above, both the insurance provider and the payment channel (telephone, SMS, the webchat solution, etc.) are kept out of the scope of compliance for GDPR, PCI DSS and other regulations. At the same time, these cloud-based digital payments technologies can relay real-time progress updates that inform the agent when the link has been opened, when payment information has been collected and whether the payment was approved by the PSP, providing the business with powerful insights into the status and success of collected payments.

By handling payments in the cloud, insurance providers can dramatically reduce the amount and types of sensitive data they process or store – making themselves less of a target for hackers and reducing the scope of compliance for numerous industry standards and regulations. Moreover, by moving their payments to the cloud, organizations can reduce costs by eliminating the capital expenditure related to hardware, and enable greater productivity across their IT teams by offloading the task of maintenance and updates to third-party service providers.

Additional Benefits of Moving to the Cloud

Cloud-based technologies offer unmatched flexibility, scalability and nimbleness compared with traditional, on-premises IT solutions. Here are just a few benefits of adopting a cloud-based solutions:

Greater Resiliency and Reliability – because many cloud solutions are able to accommodate thousands of customers at once, these platforms offer a greater level of reliability at a lower cost than insurers could typically afford independently.

Geo-redundancy – cloud-based payments solution providers have geo-redundant data centers, resulting in an additional level of backup in the rare case that the main payments system fails – a necessity for companies to consistently and reliably ensure customer satisfaction.

Scalability – cloud solutions enable organizations to quickly and easily scale up on-demand, without requiring additional investment in on-premises hardware.

Cost Control – tightly tied to flexible scaling options, cloud payments solutions often result in better cost control and allow organizations to take advantage of economies of scale, compared with investing in on-premises infrastructure. This ability to save on up-front hardware costs is especially important for fast-growing businesses.

Less Equipment – depending on the deployment option, firms can migrate their payments systems to the cloud and have little to no equipment to maintain, allowing their IT and infrastructure teams to focus on more strategic projects.

Quick and Easy Implementation – cloud implementations are typically faster and less complex to get up and running than on-premises deployment models.

Easier Software Updates and Bug Fixes – because cloud payments solutions are most often managed by service providers, insurance companies can relieve themselves of the burden of having to manually update software and patch bugs.

Security Comes First – Cloud or No Cloud

While the insurance industry has traditionally been hesitant to migrate important functions such as IT or payments systems to the cloud due to security concerns, it is important to remember that the challenge is not in the security of the cloud itself. In most cases, data breaches are the result of a user – not the cloud provider – that has failed to follow or enforce appropriate security policies and controls. As long as the organization enacts proper security policies and trains its employees on the importance of following them, it should have no worries about cloud solutions adding security risks.

That said, security should always be a top priority for companies, whether they are using on-premises or cloud-based solutions. It’s important to carefully select a provider that adheres to the highest security and compliance standards. When choosing among cloud-based payments solution providers, make sure they have achieved industry-accepted certifications like ISO 27001, PA DSS and PCI DSS Level 1 certification. (Here is a helpful guide that explains the different PCI compliance levels).

As insurance organizations struggle to keep pace with an increasingly dynamic business landscape, a deluge of sensitive customer data and ever-more-complex regulatory requirements, they will find that migrating their critical systems and functions to the cloud will provide the nimbleness and flexibility they need to remain competitive. Cloud payments solutions can help optimize costs and provide scalability, while enabling stronger security, easier compliance and a superior customer experience.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Gary Barnett, CEO, Semafone, is recognized worldwide as an authority on contact center and unified communications technologies and solutions. He has a proven track record for delivering outstanding leadership and stakeholder value throughout his 30-year career.

There’s a quote attributed to Henry Ford: “If I had asked people what they wanted, they would have said faster horses.” While Ford was speaking about cars, there is still a lesson for the insurance industry. In an increasingly digital world, agencies and the insured don’t need to continue trying to improve outdated coverage processes just because they’ve been a cornerstone of the industry for the last century or more. Obsolete but convenient practices are costing both parties time and money.

The “horses” of the insurance industry are the paper and PDF forms still used to this day as the main means to complete the insurance application and renewal process. Confusing forms can take weeks or months to pass between agents and the insured before finally being completed correctly, wasting valuable time. In the worst-case scenario, incorrect forms are sent to market, resulting in incorrect coverage for the insured.

Automation is the solution that the industry didn’t know it needed, but, for those who use it, there is no question of ever going back. With current technology, agents can provide their clients with digital forms that auto-populate duplicate answers, check in on the status of their client’s application and provide help, insight and advice in real time. Agents and the insured can become significantly more efficient.

Cost pressures will always be a factor for businesses across all industries, but long-term cost management is possible if insurance agencies reevaluate technological solutions in three simple areas:

1. Maintain Online Collaborative Systems

The current application and renewal process is unnecessarily complex and confusing. It includes dozens of forms and applications to manage, with many including repeat questions. Moving the renewal process into an easy-to-use online experience allows both agency staff and the insured to access information on their own, freeing up time to complete application and renewal forms at everyone’s convenience.

An easy, central location cuts back on either party having to track down tangible papers or multiple PDF file forms across email and envelopes. A one-stop shop that works both ways can allow clients to complete forms, share documents, update information and more. Information flows seamlessly to agents, who can interact in real time.

Having both the agent and the insured work together within the same hub to complete the renewal process eliminates the inefficient back-and-forth across meetings, emails and phone calls.

2. Use Digital Smart Forms

The current application and renewal process is plagued by mounds of paperwork that both the agent and insured must continually update and track. If one piece is missing, it’s time wasted for agency staff who must go back and forth with the client. This process leaves room for errors and omissions. Digital smart forms make all the hassle and lost time go away.

Smart forms and applications that live online include features such as automapping, which autopopulate common answers from one form to another. The need for insureds to constantly fill out the same data over and over again, from one year to the next, is eliminated. Smart online forms can also be customized by hiding certain questions that are not necessary for going to market, attaching comments within the forms to streamline communication and building in e-signatures to remove the need of printing, scanning, emailing and faxing.

Instead of a manual data swap susceptible to faulty procedures and a huge liability for mistakes, automation via smart forms provides a digital on-ramp that helps agencies achieve unparalleled workflow efficiencies and an exceptional customer experience.

3. Set Automated Reminders

Moving toward automation doesn’t necessarily mean applications and renewals are entirely hands-off. In fact, automation encourages opening communication channels between the agent and insured that would’ve been taken up by excessive administrative work. The insurer can provide notes, comments or tips within the application questions to help guide the insured through the process.

As application deadlines approach, it’s imperative to keep that communication open, especially by leveraging automated email reminders. Automated reminders can allow for a collaborative process while saving time. Such reminders can be sent at increasing intervals as the clock ticks down toward a deadline. Agents, instead of constantly drafting manual emails, have time to track follow-ups.

A digitally enhanced insurance agency takes a process dreaded by agents and clients and moves it into a modern landscape. If agency leaders take full advantage of automation technology, they can have a more effective agency.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

We're all swimming in a soup of information and speculation about the coronavirus, and I'd love to be able to say I have some startling insight that will clear everything right up. I don't, of course. But I do have two bits of historical perspective that might help to frame a part or two of the many issues before us.

First, from my days as a reporter, I learned the value of understanding precedent—the line at the Wall Street Journal was that "there are no new stories, just new reporters." The precedents here, as this Washington Post article ably describes, suggest that the coronavirus may be more like the H1N1 virus, which official statistics say killed 12,469 people in its first year in the U.S. in 2009-2010, and less like the 1918 Spanish flu, which killed 50 million worldwide. There's no guarantee, of course, but perhaps history can help us start to form expectations and to see what path we're headed down.

The second bit of perspective comes from a curious exposure to poker—both my brothers are former professional players, and I was hired by one of the top poker players in the world to help him write a book on how to apply poker thinking to everyday life. Although he eventually decided he didn't have enough insights to warrant a book, I've found some poker concepts to be quite useful over the years. So, I'll tell you what I think they say about the coronavirus. I'll then add some thoughts on applying poker principles to innovation; yes, the transition doesn't really work, but I figure I won't be returning to poker any time soon, and I've found the principles to be important.

Poker players don't just bet if they think they have a better-than-even chance of winning a hand. They calibrate their betting based on a concept called "pot odds." They estimate their chances of winning a hand and multiply it by the size of the pot to help decide how much they should bet: A 50% chance of winning $1,000 warrants a $500 bet, while a 20% chance would justify a $200 wager.

Although there are a lot more variables involved with the coronavirus, governments can still apply the "pot odds" concept. They would start with the health, economic and other risks posed by a virus that Bill Gates says is behaving like a once-in-a-century pathogen. They would then multiply that rough figure by their best estimate of the odds that it will come to pass. My suspicion is that the potential catastrophe is so great that even a slim chance of the worst-case scenario would justify more mobilization of resources than we've seen to date.

Poker pros would also remind you that the outcome doesn't determine what the right course of action was. You aren't a genius if you draw to an inside straight on the river (the fifth face-up card) in Texas Hold'em and beat a set (three of a kind). You're just lucky. The right bet is the right bet, and poker pros are very disciplined about evaluating themselves based on the odds, not the outcomes. So, when the time comes to allot blame for the spread of the coronavirus or to hand out credit for containment (here's hoping), the actual toll from the virus should be set aside. It's possible to do all the right things and still have a massive problem, just as it's possible to do all the wrong things and hit that straight on the river.

Now for the awkward transition to what poker says about innovation....

When I lived in Silicon Valley in the late '90s and early aughts, I was invited to play in the neighborhood game and didn't want to lose too much money to a bunch of smart, numbers types, so I called my younger brother right before leaving my house and said, "You have two minutes. Give me your best stuff." One pointer not only set me up for the game (I had one losing night through maybe a dozen evenings over two or three years) but showed me a mistake that I've seen companies make repeatedly.

My brother told me that most of the money in Texas Hold'em is lost before anyone sees any of the five community cards that are dealt face-up. Each player is dealt the two face-down cards, and the temptation with mediocre cards is to think, well, maybe this will grow into something, and it won't cost me THAT much to see the flop (the first three cards that are dealt face-up, for anyone to use). If you're ruthless about whether you bet your first two cards, my brother said, you'll avoid the slow bleeding of chips that affects so many players.

That sort of mistake shows up in innovation efforts all the time. Once a venture gets set up, it's very hard to kill—among other reasons, people typically view the end of a project as a failure, rather than as education that can define future efforts, and fear their careers will suffer. So, companies bleed money through ventures that everyone knows aren't going anywhere. Think of Iridium, the Motorola satellite phone project that invested billions of dollars in the hope that the technology would prove out and a reasonable business model found, then couldn't find a way to gracefully back away from its big bet. (Of course, the technology never did work as advertised, and having to charge more than $3 a minute for calls didn't allow for much of a business model.) Motorola was on top of its game in the '80s and '90s, known for its innovation, but even those guys fell for the "betting on the come" trap.

My next lesson in poker came a decade-plus ago, with the book flirtation with the famous poker player. (I'm pretty sure I signed a non-disclosure agreement, and I've never seen him publicly say anything about the project, so I won't identify him.) Even though the book never went anywhere, he exposed me to numerous concepts, including pot odds, and I began to see how companies get confused about probability.

Many companies start with the goal and work backward to the odds: "We need to generate this sort of bump in the stock price, so we need profit to climb X% this year and revenue to increase Y%. What can we do that gives us the best chance of hitting X and Y?" The problem is that the best chance isn't necessarily a good chance.

The backward approach can show up in any sort of strategy discussion but seems to be especially prevalent in decisions about innovation, particularly if the company is under some pressure. Having done a number of home remodels in my time, I used to think that the most expensive words in the English language were, "while we're at it...." But I've come to believe those are eclipsed by the CEO who says, "well, we have to do something."

Look at Sears, which, as it began closing stores by the dozens years ago, decided that it had to try something to break the cycle. It made a heavy investment in digital operations, including a loyalty program, even though Sears didn't have the right technology, the right technology people, the right customer base...pretty much the right anything. The digital/loyalty program may have been the best chance, but that chance was still maybe 10,000-to-one.

Yes, every company needs to be exploring digital possibilities, because there are opportunities out there, as well as threats that you'll want to spot as early as possible. But you can play lots more hands if you're willing to fold your losing cards quickly. In the process, you'll increase the odds that you'll spot opportunities that aren't just your best chance but that are real, live, good chances to cash in.

In the meantime, let's hope and pray that leaders around the world play their cards (our cards) perfectly as they deal with the coronavirus in the weeks and months to come.

Cheers,

Paul Carroll Editor-in-Chief

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

There seem to be infinite possibilities for insurance brokers to grow these days. Here are a few tried-and-true strategies that brokers can take full advantage of in 2020 to stay relevant and elevate themselves to strategic advisers.

Expand your product and services portfolio

Brokers need to challenge the idea of being specialists, especially because monoline insurance selling is not as prominent as it once was. It will pay off to operate as a generalist with a vast knowledge of multiple available coverages and services rather than focusing on a singular, niche area. Indeed, expanding their portfolio can help brokers manage clients’ entire risk profile, reach new segments of potential clients and elevate them from simply a vendor to a strategic adviser. For example, a broker with clients in healthcare, an industry with acute cyber concerns, might expand his or her portfolio to offer cyber insurance.

Get out of the Stone Age

In today’s digital world, clients are accustomed to having service at the touch of a button, and brokers must adapt. Implementing technology that boosts efficiency, enables customers to manage their own products and expedites all processes has become a must as clients no longer have patience to work with businesses unwilling to make such changes, regardless of coverage options.

Evaluating where strategic investments can be made specific to their business, such as adopting a new agency management system, using data and analytics, white labeling or partnering on risk engineering services, can also fuel growth. For example, using a system like CoverWallet to rate, quote and bind smaller accounts, frees up agents’ time to focus on larger accounts with more revenue potential. Or agents can tap digital partners like IVANS to identify emerging markets faster, which leads to quicker growth.

Be comfortable with a “blank piece of paper” mindset

Every successful broker has a growth mindset. Although it can be uncomfortable, a great way to grow can start from a “blank piece of paper” mindset. That is, moving away from the “business as usual” mentality and just saying “yes” can lead to unimaginable possibilities and new ideas regarding the evolving service, technology and customer experiences. For example, insurtech companies are super comfortable with a blank piece of paper – it allows them to think, design, build and test new ideas in a fast environment.

Straying away from the idea of perfectionism can lead to meeting new people, creating long-term goals and working on projects you hadn’t considered before. Being willing to start from scratch and think outside the box allows brokers to learn about the field in new ways. The ability to adapt to overcome challenges and a willingness to embrace the unknown are essential skills for successful brokers. A way to work on honing this skill is by looking for new strategies to adopt that allow you to stay up to date on current trends in the field, and maintaining an optimistic mindset. Long-term strategies can come from not being afraid to start at the end of something and working backward toward your goal instead of trying to fix what might be broken.

Have a referral strategy

Putting a referral strategy in place can help brokers capitalize on growth opportunities. Failing to take this step is essentially leaving money on the table. It’s important to set goals before crafting and implementing a strategy. From there, brokers can make it a habit to think about who they can tap for a referral two or three times a week, and then bring the referral to life. These efforts will add up over time with persistence, gratitude and creativity.

Referrals are a major business builder and money maker for brokers. When trusted clients, friends, family and colleagues recommend a broker’s services to others it can quickly translate into a new customer. However, brokers can’t rely solely on word-of-mouth referrals. To break free of the referral rut, brokers should leverage both social networking and traditional, in-person networking to organically grow their business, strengthen relationships and reach new audiences.

Strategic partnerships can allow brokers to push their capabilities to the next level and expand into new areas of insurance. There are three main potential partnerships for brokers to explore: agent aggregators, merger or acquisitions and gaining access to an online marketplace. Agent aggregators offer immediate expansion and resources. Mergers or acquisition can prove successful when two firms specialize in the same niche area or have symbiotic offerings. Lastly, gaining access to an online marketplace is an increasingly common option with the evolution of insurtech.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

It is impossible to discuss business models without considering moats. The word "moat" is used to describe a firm’s (actually, a firm’s business model's) competitive advantage. Both startups and incumbents need a defensible moat.

It is terribly au courant to discuss moats, specifically for startups (and even more for insurance startups), as if the essence of a moat is the technology or technology applications a startup insurance firm uses to get and keep customers.

But there are more attributes beyond technology or technology applications that can make up a moat. The 10 attributes, including technology applications. that I have listed below is only a partial set. (Please note that "Cost (Low or High)" means only one or the other for a specific product or business unit. I realize that the same firm can employ both low cost and high cost depending on the product, solution or market segment.)

It is entirely possible – and, I believe, desirable – for a firm to create a moat that is built on two or more attributes.

Moat mortality

“Guests, like fish, begin to smell after three days.” Benjamin Franklin

Regardless of which attribute or combination of attributes a firm uses to create a moat, a key question arises: What is the quality of the moat? That is, how fleeting is the defensibility of the moat? What might cause the moat to dry up? Will a firm’s moat last more than three days?

Includes business model expansion components, although they are not shown

Moats will dry up. The attributes of a moat will age, wither and die. The mortality of a moat depends on a host of factors, including:

emerging technologies and their applications

changing customer needs, expectations or demands

staff reductions

damage to the firm’s brand/reputation

labor shortages

changing economic policies (at local, state or federal levels)

external shocks (natural, man-made) to supply chains

? (you can fill in the ? here).

Regarding the first mortality factor (emerging technologies and their applications), we had an Arthur D. Little Center for Research and Development focused on banks, capital markets and insurance when I worked there as an insurance management consultant in the financial services practice. The center’s objective was to provide clients with a temporary window of competitive advantage through the use of technology.

We stressed to our clients that we were providing only a temporary competitive advantage because technology applications can be easily copied, newer applications based on the same technology can emerge and new applications from new technologies will arise quickly. To restate our position in the terms of this post: The mortality of a moat depending entirely or almost entirely on the applications of technology is extremely high.

Simply put: Relying on technology (or a technology application) for a sustainable competitive advantage is a fool’s errand.

Expanded insurance business model with selected key forces

At this point, I’ll turn "home" to the insurance industry, where I have spent my entire 40-plus-year career (with the exceptions of serving in the U.S. Army, going to graduate school and working as a "guest visitor" at Bell Labs on the Star Wars initiative).

Below, I illustrate an expanded insurance business model including selected key forces acting on an insurance company and its business model. This expanded insurance business model applies to both incumbent and startup insurance firms.

One way to consider an insurance business model (or a business model for firms in other industries) is that it sits in the middle of a communications web sending out and receiving signals from one or more of the forces shown in the visual. These forces act not just on the expanded insurance business model but also on the insurance firm’s moat (whatever the depth of the moat is at any given time).

Insurance startups: a new species in the insurance ecosystem?

No.

Insurance startups are not a new species in the insurance ecosystem.

Insurance startups encompass new: insurance carriers, broking firms, managing general agencies (MGAs) and claim firms (to list only a few). These types of firms already exist in the insurance ecosystem.

The reality is that the essence of the value proposition must be the same for startups as it is for incumbent insurers: mitigate or manage risk (for a specific set of exposures) in a profitable manner that complies with insurance regulations. Insurance startups, to be successful, have to find a way to offer their value proposition in a manner that incumbent insurers cannot copy or don’t want to copy, at least in the near term.

(Relying on investor funds to paper over a startup’s losses is a myopic – and dangerous – approach to bringing an insurance firm to market. Eventually, financial reality will drop as sharply as a guillotine’s blade. And, if incumbent insurers don’t want to copy what one or more startups are doing, could it be that the incumbent insurers’ actuaries realize that the startups' offering will result in unacceptable levels of profitability or even losses?)

Giving credit where credit is due

To give credit where credit is due, I realize that insurance startups do use new(er) technology applications such as advanced analytics (i.e. forms of AI including algorithms/models, big data, cognitive computing or machine learning). This use of technology applications does give the insurance startups a degree of time to capture customers. But let’s get real: The insurance startups have not reached into a parallel universe and pulled out technology applications that incumbent insurers can’t copy and bring to market. There is no sustainable competitive advantage here.

To repeat myself, using technology (or technology applications) for a sustainable competitive advantage is a fool’s errand (however much money investors have plowed into the startup or however much enthusiasm the startup’s owners/management shout out to the world.)

Insurance startups have entered the insurance ecosystem by brokering transportation network companies' (TNC) insurance coverage, or insurance for telematics/usage-based insurance or insurance for specific items in a person’s home for a specific period.

Niches … all niches. I’ll agree that insurance startups creating their initial book of business on one or more niches is clever. But niches do not a robust moat make. I can see the moat vaporizing now.

Important questions incumbent insurers should ask concerning insurance startups

Incumbent insurers fully realize there are many hundreds of startup insurance firms in play or emerging around the world. There are quite a few "pump-and-dump" conferences that are filled with enthusiastic investors and entrepreneurs bringing the startup insurance firms to the insurance marketplace. A seemingly never-ending waterfall of digital ink promoting the startups and simultaneously scolding the incumbents (for not partnering or acquiring the startups) continues to fill all variety of insurance media.

Nevertheless, incumbent insurers are partnering with (or acquiring) some of the startup insurance firms or wondering if they should. However, I recommend that, before actually completing a (partnership or acquisition) transaction with a startup insurance firm, there are several important questions that incumbent insurers should consider asking the startup:

What is the startup insurance firm’s business model?

What best describes each part of the expanded business model?

What is the level of money invested in the startup (and from what sources and what from what rounds of investment)?

What is the number of customers that are on their books (not planned, not in the pipeline, not hoped for)?

What exactly is the startup firm’s profit formula?

What are the startup firm’s resources?

What are the startup firm’s processes, activities within each process, technology applications supporting each activity and technologies enabling each technology application?

What parts of the insurance market, whether existing or niche or new (niche could equal new), is the startup striving to serve?

What is the startup insurance firm’s moat?

What one attribute, if there is only one, does the startup firm’s moat most depend on?

What is the mortality of the startup firm’s moat?

Which moat attributes will dry up quicker than the other attributes?

How, if at all, will that be a problem for the incumbent insurer?

What parts of the incumbent’s business model will the startup’s business model:

strengthen (by bringing in new customers in the same markets the incumbent already is in, for example)

expand (by reaching new markets the incumbent is not in or does not plan to be in for some time?

offer new products/services the incumbent is currently not providing?

offer new technology applications, new skills/talent, new distribution channels that the incumbent is intrigued or interested in but has not yet decided to obtain itself for whatever reasons?

weaken, and for what reasons?

Whether partnering with the startup or acquiring the startup, what are the issues with integrating procedures, technology applications, staff and culture between the incumbent and the startup?

Is the investment (of money, people, skills, procedures, technology applications), whether in partnering with a startup or acquiring a startup, financially acceptable to the incumbent? If yes, at what time scale (immediately, short term or longer term, whatever these terms mean to the incumbent insurer) is the transaction acceptable to the incumbent?

Final comments

I’ve never shied away from my opinion that 99.99%-plus of the insurance startups are born to be devoured. Obviously, new insurance companies emerge in the insurance ecosystem, but it takes a great deal of time. Insurance is not a commodity, and that is a hurdle to succeeding in the marketplace. Another hurdle is that insurance regulations exist for a very strong reason: Insurance is all about helping people (and businesses) manage the risks to their lives, health, property, actions/behaviors and income streams. Insurance is not a "game" in which corners can be cut.

For me, the startup insurance firms’ business models and moats cry out for extinction.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Barry Rabkin is a technology-focused insurance industry analyst. His research focuses on areas where current and emerging technology affects insurance commerce, markets, customers and channels. He has been involved with the insurance industry for more than 35 years.

This is the latest post in our series on building a new MGA program. The first three steps and an introduction can be found here.

Technology can make or break a program business strategy. As we’ve covered in previous posts, distressed classes only remain distressed for so long until that market need is met. Agencies need a way to bring products to market quickly, or risk losing valuable potential business. Technology is key, but only if you choose your system wisely.

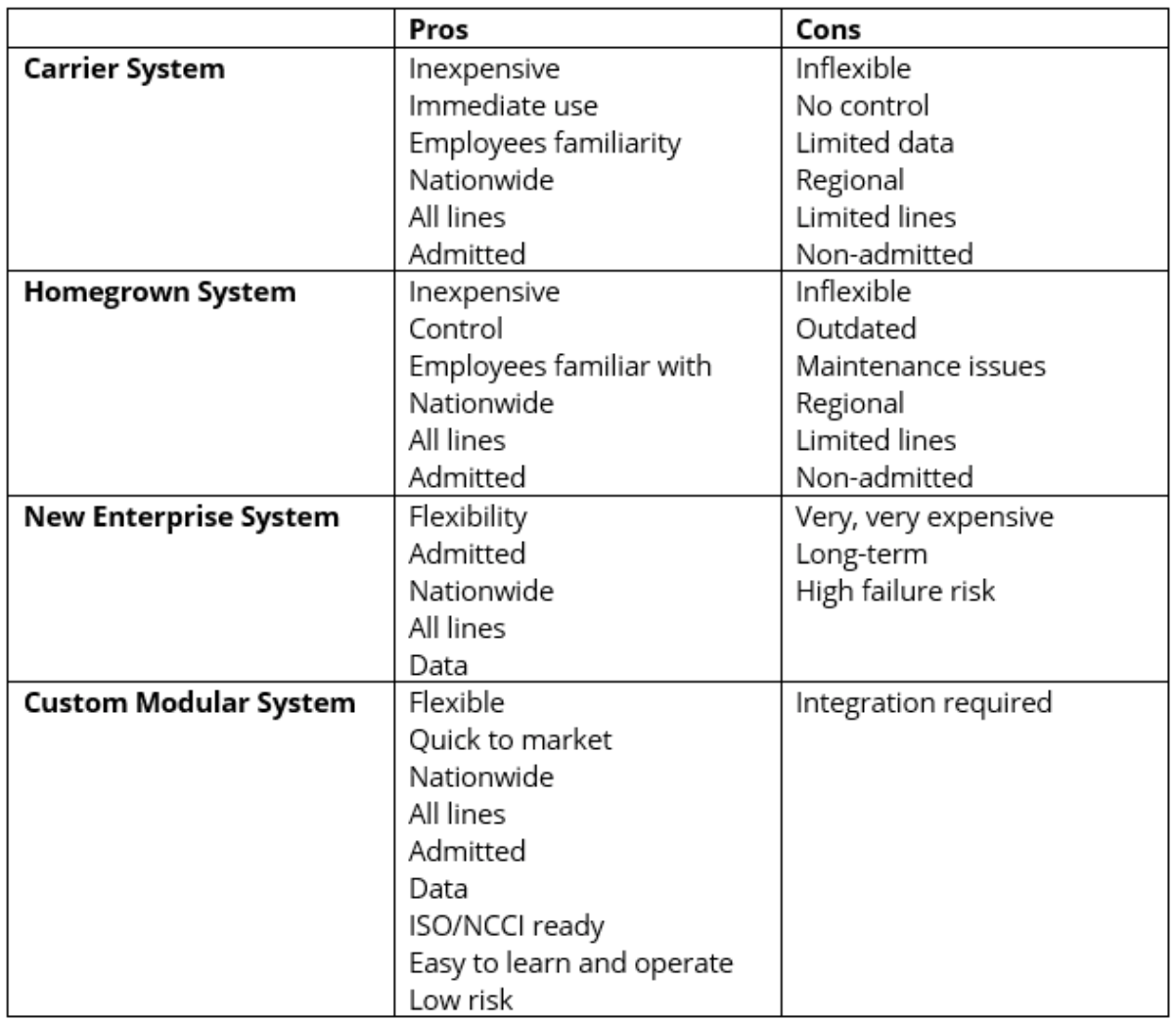

There are four options available when creating a program. You may use the insurance carrier’s system, homegrown software, a new enterprise rollout or a custom modular ISO/NCCI-ready system. Each has its pros and cons. The following is a summary:

As you can tell from the above analysis, the custom modular system is the best fit for programs. Let’s look at the characteristics of a new MGA program and how they match up with this option.

Most programs today are written on an admitted basis. You therefore need a system that supports bureau content like ISO and NCCI. It should provide the latest rules, rates and forms and regular, accurate bureau content updates to remain in compliance.

New programs are typically available in all 50 states. You may start off selling regionally, but you’ll need the ability to move quickly into all 50 states when you’re ready to expand. If your system doesn’t give you this flexibility, you’ll end up losing valuable market share in states you can’t enter fast enough.

It is typical for a program writer to provide one-stop shopping for the industry it targets. Loyal agents prefer this because it is easy to access all that is needed for an account in one spot. So, you need a system that supports all or most business lines, including BOP and worker’s compensation.

A custom product is key for success in the specialty insurance marketplace. But you shouldn’t need to reinvent the wheel every time you create a program. Typically, 80% of the product can be straight ISO or NCCI and 20% customized. For the 80%, you need an ISO- or NCCI-supported product. For the 20%, you need a system that makes it easy to build customizations, such as endorsements, forms and rating equations.

Program opportunities don’t last long. If you spot one, chances are one of your competitors has seen it, too. A system that supports programs needs to be implemented quickly – ready to write business in all 50 states in as little as 90 days. A large, enterprise-based system will simply take too long to implement; by the time it’s in production, it may be too late.

Your program system should also be modular. You should be able to implement or change the functionality you need with no effect on the rest of your programs.

You also want a system that is easy to understand and quick to learn. Underwriting and rating staff are expensive and hard to find, so you will most likely draw on existing staff for your new program. Your system should have a short learning curve that makes it easy for new users to come up to speed, and your vendor should provide adequate on-site training when you need it.

Your program solution should easily integrate with other systems and components in your insurance environment, like agency management systems, underwriting workflow solutions and billing. Your technology provider should have proven APIs to make this connectivity seamless, fast and cost-effective.

Your system should come at a cost that aligns with the scale of your business. You’ve done your homework, but new programs still come with a level of uncertainty. You want a price based on premium volume, not a large, fixed upfront cost.

Make sure that your technology provider has robust reporting capabilities and that program data is easily accessible. Big data is the name of the game today. The more data you have at your fingertips, the better you can demonstrate to your carrier partner your ability to identify and react to trends in the market.

A final critical characteristic is the need for a well-established tech firm with a superior track record. Your vendor should have adequate resources to deliver what it promises, and a management team that supports a long-term approach to your success.

There is a lot to consider when approaching the technology challenges of program business, and picking the right partner can mean the difference between business growth and stagnation. When it comes to program business, technology can deliver a critical competitive advantage.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

CJ Lotter is the director of engagement management at Instec. He spent nine years as chief research and business development officer at the U.S. programs division of Willis Towers Watson.

Workers’ compensation systems have been a central and meaningful part of our social safety net for over 100 years. This longevity was accomplished despite social and economic change and technology revolutions, through wartime and peacetime, economic crises, etc. Two features have been central to this enviable record of continuity. The first is a fundamental and enduring premise that workers’ compensation systems should provide a fair balance between (1) adequate income benefits and timely medical care for injured workers in their time of need and (2) an affordable cost to employers, which must compete in an increasingly global marketplace. The second feature is a robust, albeit imperfect, process for redressing significant imbalances that inevitably occur from time to time.

What does change look like? When systems stray significantly out of balance, legislators and regulators are mobilized by injured stakeholders to change the laws and regulations to move systems back toward that fundamental balance. Note that the direction is “toward” a better balance — not to some specific “ideal” definition of balance. In this context, “balance” has always been and necessarily remains an amorphous concept. Sometimes, the reform process falls short, and other times it overshoots. Having a reform process that generally moves the systems in the direction of improved balance has been one key to workers’ compensation systems’ successful adaptation to many twists and turns over the course of a century.

A few examples illustrate this. In the early 1970s, the benefits paid to workers were inadequate, according to a report by a national commission appointed by President Nixon. In the ensuing decade, legislatures in many states increased statutory benefit levels. By the late 1980s, the pendulum had swung in the opposite direction. Claims costs were rising at unsustainable double-digit rates; many elected and appointed insurance regulators were unwilling to pass these large cost increases on to their employer constituents; and the availability and affordability of workers’ compensation insurance became a serious concern. Over the next decade, many state legislatures addressed key cost drivers, deregulated insurance prices and created competitive state insurance funds as both the insurers of last resort and as competitors to private sector insurers. Claims costs were reduced, insurance was more affordable for employers and insurance markets were stabilized.

This book examines these questions:

Is there a plausible scenario in which many state workers’ compensation systems become seriously out of balance in 2030? And where the workers’ compensation reform process is unable to restore a reasonable balance?

If so, what will be the likely causes of the imbalance? Why will the workers’ compensation reform process be unlikely to deliver effective solutions?

What might replace state workers’ compensation systems?

When the balance in workers’ compensation systems is disturbed, the causes fall into either of two broad categories: developments outside of the workers’ compensation systems or developments within the systems. Internally generated imbalances typically involve the workers’ compensation statutes and regulations, as well as the incentives and behaviors of the system stakeholders and their agents and vendors. Externally generated imbalances result from forces like structural changes in the economy, societal norms and values, federal government actions separate from workers’ compensation or developments in the larger healthcare system.

Internally generated system imbalances are not unusual. In the past decade, several groups have raised concerns about the performance of state workers’ compensation systems. Some expressed concerns that too many state systems were not serving injured workers adequately. Other groups maintained that the systems were unnecessarily costly for employers and that alternatives may provide better benefits for workers at lower costs to employers.

In the wake of these critiques of state workers’ compensation systems, two groups convened “national conversations” among stakeholders from diverse perspectives. These conversations discussed the strengths and limitations in current state systems (IAIABC, n.d.; 2016 Workers’ Compensation Summit, 2016). Examples of the issues they suggested that should be addressed include:

Reducing the complexity of workers’ compensation systems (both groups)

Increasing the consistency/uniformity of state programs to reduce expenses (IAIABC)

Emphasizing a focus on worker outcomes—e.g., return to work and medical recovery (both groups)

Reducing the reliance on adversarial processes (both groups)

These are examples of issues that are typically resolved by incremental changes to the features of existing systems—as has been done in the past. Hence the historic change process has opportunities to address these concerns and improve system balance where needed.

The developments discussed in this book are different from these. They originate outside of the workers’ compensation systems. Because of this, they are much less amenable to solutions developed by the workers’ compensation reform process.

Scenario for the 2030s

Workers’ compensation costs triple since 2016, with no real change in benefits to injured workers. Both employers and worker advocates agree that the systems are seriously out of balance. Despite multiple attempts at workers’ compensation legislative and regulatory reforms, too many larger workers’ compensation systems remain badly out of balance.

What are the drivers of this scenario?

Demographic Change

Baby Boomers exit the workforce at an accelerating pace, creating historic labor shortages. During labor shortages, employers lower hiring standards. Labor turnover also increases. The shortages extend to healthcare providers, delaying care for injured workers. Claim frequency increases, and disability lengthens.

Restrictive immigration policies and practices worsen the labor shortages, magnifying the effects of the shortages on workers’ compensation systems. Automation mitigates the labor shortages but not nearly by what one might expect from reading the headlines about automation “destroying” large numbers of jobs.

Healthcare Reform

Accelerating growth of high deductibles in nonoccupational health insurance policies leads more insured workers to shift soft tissue injury cases to the free care alternative—workers’ compensation.

As Congress and the administration repeal and weaken key elements of the Affordable Care Act (ACA), more workers lose their health insurance— particularly those covered by Medicaid and nongroup policies. These workers will look for ways to continue coverage for many conditions. For soft tissue conditions, the free care alternative offered by workers’ compensation will be attractive. As the number of uninsured climbs, the number of cases shifted to workers’ compensation will increase.

Fee-for-service contracts are being replaced by payment models where provider organizations assume financial risk if costs exceed targets. These contracts cover most of the care paid by commercial insurers, Medicare and Medicaid. Workers’ compensation remains fee-for-service. Providers increasingly shift soft tissue injury cases to workers’ compensation to earn the fee-for-service payments, while not counting the costs of care for these cases against the performance contracts with the other payers. Workers’ compensation claims increase.

SSDI Solvency

Congress addresses the solvency crisis in the Social Security Disability Insurance (SSDI) program by abolishing reverse offsets. Moreover, new SSDI set-asides, akin to the Medicare set-asides, are mandated for workers’ compensation indemnity benefits. Workers’ compensation costs increase, as do the expenses involved in resolving claims.

Together, these developments raise workers’ compensation costs significantly—plausibly triple the level of 2016. Both claim frequency and cost per claim see large increases. The large increase in claim frequency is surprising because it is a stark contrast to the falling claim rates that we have come to expect over the previous several decades.

Workers’ compensation systems are seriously out of balance—costs to employers triple but benefits to injured workers have no real increase. In the past, the reform process would have moved the systems back toward balance. Yet this does not occur. Because the large cost increases arise from causes outside of the workers’ compensation systems, the typical workers’ compensation reform process has limited success in restoring balance in the systems.

Other developments outside of workers’ compensation systems also converge to create historic urgency (1) for both historic tax increases and spending cuts in virtually all government programs and (2) to improve the competitiveness of American businesses. This urgency pervades most public policy and strategic business decisions—including the search for solutions to what becomes known as the Workers’ Compensation Problem.

These external developments include:

Widespread Fiscal Distress at All Levels of Government andMillennial Voters Come of Age Politically

We begin the repayment of the massive governmental debt and unfunded liabilities accumulated under the Baby Boom generation. This severely limits governments’ ability to maintain many current programs. Privatization and consolidation of government services increase.

Because of the inherited public debt, millennials face the prospect of taxes doubling and historic cuts in government programs. Millennial elected officials and voters abandon many of the government budgeting norms and processes that had been used to kick the hard decisions down the road (from Boomers to millennials). Rather, they begin to make hard decisions on government spending to mitigate the impending tax increases. Given the debt that they inherited, millennials are unwilling to incur unnecessary public debt or additional unfunded liabilities that would burden future generations.

Globalization Pressures Intensify

U.S. employers face intensifying globalization pressures, driven by broadening diffusion of telecommunications technologies, especially in a handful of under- the-radar African and Asian economies that account for half of the world’s population growth. As competitors arise in emerging economies, U.S. firms are required to more often choose between aggressively reducing production costs of U.S.-made goods and services, moving production to lower-cost nations and losing business to foreign competitors.

The processes for improving public programs, including workers’ compensation, become increasingly sclerotic. Pragmatic problem-solving and compromise- based solutions become the exception, rather than the rule, in both legislative and executive branches at the federal and state levels. Too often, pragmatic problem-solving is replaced by all-or-nothing processes driven by ideology, camouflaged self-interest, electoral tactics and fake “facts.” This makes it more difficult to move the now out-of-balance workers’ compensation system toward a better balance.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Dr. Richard A. Victor is a senior fellow with the Sedgwick Institute. He is the former president and CEO of the Workers Compensation Research Institute (WCRI), an independent, not-for-profit research organization that he founded.

Consider this column a sequel to my piece about life insurance. Consider the connection between promoting a policy and selling a product, because what my previous column mentions, that insurers need to better explain what they mean, has greater meaning—right now. Because my own review of how insurers advertise suggests that their advertising does not work.

The same is true of individual agents: that they are indistinguishable, that they look alike, despite their differences in appearance, that they look like a collective smile with a caption underneath; a grin with generic copy in which the words are true but the message is irrelevant.

Do not, however, blame agents for how their marketing looks. Their response is reasonable, their reaction predictable, their return on investment picayune.

David Albanese of Ameraquest Financial Group, whom I quote in my previous column, says insurers have to invest in marketing with a force equal to what they spend creating or issuing new policies.

“Formulas work for actuaries, not sales, because marketing is not a science. The art of communication requires practice or: There can be no trials without errors and no experiments without failures. The goal is to encourage creativity over conformity, so agents can personalize their services and better serve their clients.”

Concerning Albanese’s point about marketing not being a science—amen. Amen to the fact that there is no test that will yield the same results, sparing agents from the training necessary to lead and the skills leaders need to communicate.

I understand the appeal of science because I am a scientist. But I also know that the attempt to make the unscientific scientific is both wrong, intellectually, and wrongheaded, financially.

The financial costs can be ruinous to morale, too, because when a formula does not work, when the elegance of an equation does not equate to the complex and sometimes inelegant ways in which people behave, when things fall apart—when all of these things happen at once, agents can lose confidence in themselves. Their loss can cause them to look for another line of work.

Consider the consequences of this scenario to the public.

If the most capable agents believe they are incapable of marketing their best products, if they decide to leave the insurance industry altogether, then the public will not enjoy the advice of the industry’s brightest stars and most brilliant agents.

We cannot afford this situation to go from a possible outcome to a probable or inevitable disaster.

Yes—marketing matters enough for us to care about the fate of the insurance industry. It matters enough for us to do all we can, for as many as we can, so most agents can acquire the know-how and the can-do spirit that is integral to successful marketing.

With the discipline of a professional, and the will of a competitor, an insurance agent can become a good if not great marketer.

With time, the results will be conclusive, the reviews consistent, the recognition clear.

With time, agents can excel at marketing.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

The insurtech movement has been underway for the better part of a decade. Now that we have entered the 2020s, it might be worth exploring what could be on the horizon for insurtech over the next 10 years.

Insurtech has evolved from its origins in the early part of the last decade (as an offshoot of the fintech movement) and quickly gained momentum over the last few years to experience a strong close in 2019. Along the way, there were rumors of its demise – maybe it was a wish made by those hoping insurtech would just go away and stop creating competition or driving the need to innovate. Along the way, there was also plenty of hype. Some even predicted massive disruption and the decline of the incumbents. But, as is often the case, the truth falls somewhere in the middle.

Viewing a snapshot of 2019 as the culmination of the first decade of insurtech is very informative. SMA’s recent research report, “Insurtech and Transformational Tech: Highlights and Insights for 2H19,” does just that. The second half of 2019, in particular, demonstrates how strong the movement is at this stage in its evolution. The number of deals is up. The funding for the second half of 2019 (and the full year) is up. Even more important is the fact that late-stage funding is dominating, signaling that insurtech winners are growing and likely here for the long term. In fact, there were eight P&C insurtech funding events in 2019 for $100 million or more.

So, what is ahead for the next decade? There may still be some that are rooting for insurtech to fizzle, or at least to have a smaller impact than expected. However, most are embracing insurtechs as an important part of the insurance ecosystem with roles as catalysts for innovation and change. With that background in mind, here are my top predictions for insurtech in the 2020s:

By 2030, we will see multiple insurtechs with over $1 billion per year in revenue.

The term "insurtech" will fade by mid-decade, but the impact of the movement will be lasting.

The next three to five years will see a flurry of M&A activity in the space.

Insurtech funding over the next five years will be greater than the prior 10 years combined.

Insurtech distributors will gain significant market share in personal lines, but agents/brokers will still dominate in commercial lines overall.

Insurtechs will play a major role in reshaping ecosystems for connected vehicles and smart homes, but the true revolutionary change in these areas will occur in the 2030s.

Depending on your viewpoint, these predictions might be bold. Or they might just be common sense. Prognostications of this sort are always difficult, especially looking out 10 years and especially while the world and the industry are in the midst of transformation. Therefore, you can feel free to disagree and come up with your own predictions for insurtech. But do check back in with me in 10 years to see if these predictions were fulfilled or if insurtech and the industry have gone in different directions.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Mark Breading is a partner at Strategy Meets Action, a Resource Pro company that helps insurers develop and validate their IT strategies and plans, better understand how their investments measure up in today's highly competitive environment and gain clarity on solution options and vendor selection.