“When one thing is different, it is change; when everything is different, it is chaos!”

Yesterday, Corona was a beer. Today, Corona is still a beer but is also a disease, a pandemic. It is the reason I’m at home typing this article, and you’re at home reading it. If the Civil War was the defining event in our county in the 1800s, and the world wars, Korea and Vietnam were the defining global events of the 1900s, then corona – the virus, not the beer –will be the defining event of 2000-2020. If you consider worst-case scenarios, this coronavirus crisis may just be it.

I question whether the worst of these worst cases is not the disease but our reaction to the real and imagined threats. Time will tell.

For perspective, consider the following:

It was October 1962. I was a sophomore in high school. Coach Blanco was our teacher. He was sitting on his desk facing south. Tension was in the air because the U. S. Navy was going to confront the Soviet Union that day over its deployment of ballistic missiles in Cuba. In the previous weeks, we had prepared for such a contingency by practicing nuclear bomb drills – literally getting under our desks and covering our heads with our arms and hands.

Coach said, “Boys, if you see me get off this desk and crawl under it, you do the same because that means I’ve seen a mushroom cloud.” Nervous laughter followed. Thank God we never needed to act on his instructions.

Since that time, the U.S. has fumbled through the Vietnam conflict (which in retrospect should never have been fought) and avoided nuclear war. We finally declared victory in Vietnam and withdrew. Decades later, the Soviet Union collapsed, and the Berlin Wall came down. We have been blessed.

Shortly after the Cuban Missile Crisis and the assassination of John Kennedy (Nov. 22, 1963), Lyndon Baines Johnson became president. The Great Society followed, with a set of programs that aimed for the total elimination of poverty and racial injustice. Some progress was made, but real challenges remain.

Today, our country and the world are threatened by the coronavirus and the nearly complete shutdown of our malls, schools, Main streets, manufacturing, commerce and social lives. The U.S. has gone from a booming economy to an economy that has gone down in a boom.

I could go on, but I won’t. I’ll offer the following six questions for your consideration. Consider these strategic planning issues to be pondered as you plan your future, next week, next month and next year(s). Obviously, this is not an all-inclusive list.

Tomorrow - who will be your clients and prospects?

What will be their wants and needs that you are positioned to address?

Since the virus crisis eliminated “place” as part of the value provided by your office, will you compete as well in a virtual market as you did on your Main Street?

As technology and the growing Gen X, Gen Y and future generations become more enamored with each other, does human touch (like a good neighbor or your local agency) lose value?

As technology allows us to provide service that is fast, hot and cheap, will clients tolerate current commission levels, will coverages be quoted net of commissions or will commissions become negotiable?

What is your greatest nightmare about the agency business? Is it closer to or further from your horizon than it was on last New Year’s Eve?

After the assassination of JFK, the journalist Mary McGrory said, "We'll never laugh again," and Kennedy aide Daniel Patrick Moynihan famously replied, "Mary, we will laugh again. It's just that we will never be young again."

If I might be so presumptuous: After our coronavirus experience, we will laugh again, and the young will still be young, but we will never feel invincible again.

My friend Mark attributes his success to “waking up scared to death every morning!” Do you? Should you? Or will you remain in your comfort zone of yesterday, dumb, fat and happy?

Place your bets on tomorrow!

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Mike Manes was branded by Jack Burke as a “Cajun Philosopher.” He self-defines as a storyteller – “a guy with some brain tissue and much more scar tissue.” His organizational and life mantra is Carpe Mañana.

In 2008-09, during the height of the Great Recession – a time when the U.S. economy was in a meltdown and every auto manufacturer was seeing sales plummet – Hyundai Motors increased its market share by a remarkable 40%.

Understanding how Hyundai did it offers a valuable lesson to any company that’s trying to navigate a period of consumer crisis. Here’s how the story goes:

In October 2008, Wall Street and the banking sector began to implode, car sales fell precipitously and Hyundai sought an answer to a question that was vexing most auto industry executives during that dark time: Why weren’t people buying cars? Why weren’t they coming into showrooms? Why weren’t traditional car buying incentives (rebates and financing deals) – which were always effective in past economic slumps – driving foot traffic into the dealers?

To answer these questions, Hyundai executives did something extraordinary. They talked to their customers. Through those conversations, Hyundai was able to put its finger on exactly what was going on in consumers’ heads.

What Hyundai executives came to realize is that – even in the depths of a financial crisis – plenty of consumers were still interested in buying cars, and plenty of consumers still had the money to buy cars. But people were staying away from the dealer showrooms because they were afraid.

They were afraid that they’d buy the car, get laid off shortly thereafter and be saddled with car payments they couldn’t afford. (Remember, at this time in the U.S., the economy was shedding hundreds of thousands of jobs each month.)

With the benefit of hindsight, the fear might sound like common sense. Back then, however, the realization was an “Aha!” moment for executives, and it triggered an entirely new line of thinking at Hyundai around how to arrest, if not reverse, the sales decline.

The company shifted its focus from sales incentives to fear mitigation and tried to figure out how to eliminate (or at least alleviate) the emotionally charged worries that were keeping consumers away.

The answer lay in an entirely new offering that Hyundai rolled out in January 2009 and dubbed the “Job Loss Protection Program.” It was a guarantee whereby the automaker basically said to consumers: If you buy a car from us, and within one year you are laid off (for any reason at all), just bring the vehicle back and – no questions asked – we’ll forgive all remaining payments on the car.

This single tweak to their customer experience was a game changer. With the fear of job loss impacts removed from the purchase decision, consumers flocked to Hyundai dealers, boosting sales by double-digits, increasing market share by 40% and elevating the brand’s prominence in the marketplace to levels never before seen.

Hyundai weathered the Great Recession better than many other automakers. The approach the company used to accomplish that feat has clear relevance now, as both B2C and B2B companies navigate an even bigger consumer crisis triggered by the COVID-19 pandemic. To emulate Hyundai’s approach — so that you better engage your target market, as well as strengthen loyalty with existing customers — follow this three-part formula:

1. Look at the world from the customer’s perspective.

This is, of course, the golden rule of customer experience design. ts importance, however, is accentuated during challenging times, when customers are thinking and feeling in a way that’s very different from normal. Understanding those dynamics is critical to adjust your customer experience so it resonates even more strongly with your target clientele.

Doing this effectively requires truly immersing yourself in the customer’s perspective, which is not something that can be achieved solely through dry research surveys and satisfaction studies. In times of crisis, teasing out what’s on your customer’s mind requires getting close to them (physically or virtually), stepping into their shoes and seeing the world through their eyes.

Hyundai accomplished this by having in-depth conversations with sales prospects and customers. Other avenues for immersing yourself in the customer perspective include consulting with front-line employees (as they can tell you what they’re hearing from customers), as well as actually observing customers as they interact with your business (to spot existing pain points or new ways to better serve them). All of these insight-gathering techniques help reveal those not-yet-obvious consumer needs that fuel customer experience innovation.

2. Pay attention to emotional needs, not just rational ones.

In the two-year life of the Hyundai Job Loss Protection Program, only 350 cars were returned to the company – a minuscule percentage of overall sales, and a statistic that belies the impact the program had on the automaker’s brand recognition and business success.

The fact that so few cars were returned under the program, despite its tremendous popularity, suggests that consumers’ perceived risk of job loss (and the resulting impact on one’s ability to make car payments) was much greater than the actual risk of that outcome. What that really means is that the true value of the Protection Program was in its ability to satisfy consumers’ emotional needs, as opposed to rational ones.

That doesn’t make it any less of a beautiful solution to what consumers clearly viewed as a real problem. Indeed, the program underscores the importance of not just thinking in terms of rational, logical requirements that customers might have during times of crisis. It’s equally important to satisfy their emotional requirements, which in the case of Hyundai amounted to the mitigation of fear. For other businesses (or other types of crises), those emotional considerations might be addressed, for example, by giving customers peace of mind, by making them feel like they’re part of a community or by instilling in them a sense of pride or confidence.

Whatever the tactics, the key point is that in a crisis (as we’re experiencing with the COVID-19 pandemic), people are in a vulnerable, emotionally charged state. While creating emotionally resonant customer experiences is important at any time, it’s even more vital during difficult times, and presents a unique opportunity to create an indelible, positive impression on the people you serve.

3. Advocate for your customer in tangible ways.

Being an advocate for your customer means putting their interests ahead of yours. Importantly, it’s not about good annual report copy, website content or an advertising campaign that touts “putting your customers first.” It’s about showing customers that this company’s got your back, that we’re in your corner. It’s rare that people see companies do this, so, when it does happen, it creates a memorable peak in the customer experience that helps cultivate loyalty.

The impact of customer advocacy, however, is amplified during crises because of the vulnerable position in which many of your customers will find themselves. When you’re in a stressful situation, when you’re in a pit of despair due to tough circumstances, if someone extends a hand to help you get out of that quandary, it’s an engaging gesture for which you’ll be eternally grateful. That’s the power of advocacy in forging new customer relationships, as well as cementing existing ones.

The Hyundai Job Loss Protection Program transferred risk from the customer to the company. It was a tangible demonstration of advocacy by the automaker – a gesture of support and goodwill, even if it was grounded in a very business-focused desire to get consumers back into the showrooms. (No apologies for that are necessary, because the fact is, over the long-term, customer advocacy is simply good for business.)

In the current COVID-19 pandemic, you can spot those organizations that are employing Hyundai-like tactics. Instead of responding to the crisis by invoking platitudes in one of those “we’re here for you” broadcast e-mails, the smart organizations are being thoughtful. They’re thinking carefully about what people are going through, and they are making tangible changes to their customer experience as a result. Examples include:

Australian supermarket giant Woolworth’s, which in mid-March was among the first retail stores to establish dedicated shopping times for elderly and disabled customers. Their move was in response to panic buying by the general public, which left vulnerable populations struggling to get their basic necessities. Woolworth’s made it easier for them to do so.

American Family and Allstate insurance, which, within hours of one another, were the first U.S. auto insurers to announce they’d be refunding a portion of their policyholders’ insurance premiums. Both insurers noted that people were driving far less (due to stay-at-home orders), and this was a way to help ease some of the financial strain that their customers were experiencing.

Scholastic, which recognized the difficult task that teachers, parents and children faced as they moved to remote schooling. In response, the company curated an online library of virtual lesson plans to help instructors and caregivers minimize the disruption to kids’ education.

U-Haul, which saw an opportunity to help scores of college students who, on short notice, were instructed to vacate their dormitories as schools shut down to prevent the spread of COVID-19. The moving and storage company offered any college student in the U.S. and Canada 30 days of free storage while they figured out what to do with their belongings.

These are all examples of companies that carefully considered how the landscape in which they operated had changed, and how the lives of people in their communities had been altered. Were these firms being purely altruistic? Perhaps not, but that doesn’t diminish the significance of their actions.

These companies are, after all, for-profit entities. It’s okay if they aspire to earn a better brand reputation. It’s okay if they hope to attract some new customers via their actions. The point is, they’re doing it in a noble way, a way that genuinely aids people in the short term, even while potentially helping the company in the long term.

Their actions were guided not by what was legally required, not by what a regulator mandated and not even by what many of their customers (or non-customers) may have reasonably expected. Their actions were guided by what was fair, what was right and what served the best interests of consumers.

Critics might note that some of these firms’ customer experience enhancements were quickly copied by competitors. That’s true, but there is a first-mover advantage here. Those businesses that drive experience innovations (rather than follow them) tend to be viewed by consumers in a more positive light. (Hyundai’s 2009 Job Loss Protection Program was copied by other automakers within a few months, but none achieved the notoriety that Hyundai did.)

Furthermore, while a single, specific experience enhancement may be easy to copy, what’s much harder to replicate is the outside-in mode of thinking that customer experience leading firms possess. That’s where they derive long-term strategic advantage, because they’re the ones that are perpetually devising new and improved customer experiences that become a hallmark of their brand.

With every crisis comes opportunity. Not an opportunity to exploit a bad situation for business gain, but, rather, an opportunity to enrich the lives of those you serve by genuinely and selflessly helping them during a time of need. In a crisis, that’s how you cultivate customer loyalty, that’s how you generate positive word-of-mouth and that’s how you come out stronger on the other side.

Jon Picoult is the founder of Watermark Consulting, a customer experience advisory firm specializing in the financial services industry. Picoult has worked with thousands of executives, helping some of the world's foremost brands capitalize on the power of loyalty -- both in the marketplace and in the workplace.

During this pandemic, many workers (nurses, police, grocery store clerks, transit professionals, etc.) are considered essential, potentially putting them at heightened risk for contracting COVID-19. A key question, of course, is whether a worker who contracts COVID-19 is compensated under workers’ compensation for income loss and medical expenses.

Below are some frequently asked questions that get posed to me as president and CEO of the Workers Compensation Research Institute (WCRI). We’re an independent, not-for-profit research organization that provides high-quality, objective research and statistical information about public policy issues involving the various state workers' compensation insurance systems in the U.S.

Q1: Is COVID-19 covered under workers' compensation and, if not, why not?

A1: Historically, communicable diseases, like the flu, have generally not been covered. Workers’ compensation covers injuries and illnesses that arise out of and in the course of employment. It is generally difficult to establish work-relationship for a disease that could be contracted anywhere. Indeed, some states’ statutes bar compensation for communicable diseases. In the past few weeks, though, a number of states have taken steps to expand workers’ compensation coverage to include COVID-19 for certain groups of workers.

Q2: What is the course of action for states seeking to cover essential workers affected by COVID-19?

A2: Some states consider that their current laws, regulations and procedures are sufficient to provide compensation for workers who demonstrate that they contracted COVID-19 at work. Other states have changed their rules, either by executive order or legislation, to increase the likelihood that a worker who contracts COVID-19 may be eligible for workers’ compensation. The states vary in terms of the scope of workers covered and in terms of the burden of proof required by an ill worker to establish work-relatedness. A number of states’ laws and orders cover only first responders or healthcare workers. Others expand coverage to include other groups of workers deemed to be essential, e.g., grocery workers. In some states, the worker may be eligible for workers’ compensation if the worker can demonstrate that the illness was the result of his employment or occupation. In other states, for the workers covered, there is a presumption that their illness arose from work, though that presumption can be rebutted.

Q3: Is this the first time coverage has been expanded for conditions that may arise outside of work?

A3: No. For example, we have seen workers’ compensation coverage expanded to include those, particularly first responders, who witness a traumatic experience and as a result have post-traumatic stress disorder (PTSD) and can no longer perform their duties.

Q4: Is workers' compensation administered at the state or federal level?

A4: Individuals injured on the job while employed by private companies or state and local government agencies are covered by workers’ compensation programs administered by the states. The essential features of the states’ workers’ compensation systems are similar, but they may vary in terms of the compensability of some conditions, the amount of benefits paid and other features. Federal and some other workers are covered by four disability compensation programs administered by the U.S. Department of Labor.

Q5: What does workers' compensation cover, and are the benefits across the country the same?

A5: Workers’ compensation covers all medical benefits and wages lost while off work due to the injury. It covers the first dollar of medical care, and there are statutory formulas for the income benefits that replace lost wages. WCRI’s workers’ compensation laws reports are a great resource to identify the similarities and differences across workers’ compensation systems in U.S. states and Canadian provinces.

Q6: Is WCRI working on any research that will help us better understand the impact of COVID-19 on state workers’ compensation systems?

A6: WCRI has a wealth of studies that provide a pre-COVID baseline for evaluating the impact of the virus on workers’ compensation claims. This includes WCRI’s CompScope Benchmarks studies, which compare a range of workers’ compensation performance metrics across 18 states. In the future, we will evaluate the impact of the virus on the composition of claims and their costs, how the virus may have affected the delivery of care to workers and the impact of that on worker and claims outcomes, including duration of disability.

John W. Ruser is president and CEO of the Workers’ Compensation Research Institute (WCRI). The institute is an independent, not-for-profit research organization that provides high-quality, objective research and statistical information about public policy issues.

Sadly, the insurance-focused news outlets are starting to overflow with references to who is suing whom over certain types of coverage related to the COVID-19 pandemic. There is a growing regulatory and legislative outcry for the insurance industry to pay out in instances where there is no specified coverage or where coverage is actually excluded. Both business and personal lines customers do not fully understand where they are (and are not) covered. It is a pretty dismal picture, and it is going to take a long time to sort all this out. In the meantime, a growing trend provides a glimmer of hope in all this chaos – parametric insurance.

Parametric insurance covers a specific event that can trigger a claim payment based on metrics from a recognized source such as the Richter scale for earthquakes or the number of hours a plane is delayed. While parametric insurance isn’t new – it has been available in emerging nations over the years – usage has been limited and sporadic. During 2019, there were undoubtedly some launches of more mainstream products such as Swiss Re’s Quake Assist product and Sompo’s flood product. However, this month, there have been at least four notable launches or expansions:

AXA Climate – AXA partnered with Dutch satellite technology firm VanderSat to derive triggers linked to soil moisture levels, enabling drought-related parametric insurance. The same soil reading technology can determine excess moisture, as well, triggering payment in either direction.

Global Parametrics/Arbol – Global Parametrics, a parametric and index-based disaster risk transfer company, teamed up with Arbol, a technology-driven marketplace that uses blockchain and smart contracts to provide weather risk insurance coverage to smallholder coffee farmers in Costa Rica.

Parsyl – Parsyl Insurance launched a suite of connected cargo insurance solutions for perishable goods, called ColdCover. Parsyl’s quality-monitoring and risk management platform leverages smart sensors and data analytics to manage the supply chain as well as loss control. The featured product within the company’s new suite is called ColdCover Parametric, which includes customized quality triggers and payout levels.

Understory – Understory initially launched its Hail Safe product for auto dealerships this past November but rolled it out to a significant number of additional states in April. The product coverage is triggered through the use of Understory’s proprietary hail sensor. Understory partnered with international weather risk manager MSI GuaranteedWeather to bring the product to market.

These examples are stated simply for brevity. But the scenarios are not that simple. For example, the Global Parametrics and Arbol example also includes an ecosystem of related parties in the transaction. And Parsyl provides services and an extensive risk management system so that cargo and fleet owners can manage exposures. From an education perspective, it is worth getting further details on all four scenarios. However, for purposes of this blog, the particularly hopeful note is that all this has happened in one month – the cycle of innovation and response is speeding up.

Insurers and technology providers are coming together to find opportunities to create products that have specificity in terms of coverage and payment amounts. This is a very good thing! Insurers need to continue to seek opportunities to innovate in this area. Clearly, not all product lines are appropriate for parametric policies. However, in more instances than not, bringing sensors, aerial imagery, weather data and science to insurance products across all product segments can only help create transparency both in coverage creation and in loss settlement. This needs to be a goal for all insurers.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Karen Pauli is a former principal at SMA. She has comprehensive knowledge about how technology can drive improved results, innovation and transformation. She has worked with insurers and technology providers to reimagine processes and procedures to change business outcomes and support evolving business models.

Since starting the Out Front Ideas COVID-19 Briefing Webinar Series just a couple of weeks ago, we have been receiving questions from our listeners regarding COVID-19 and how it is changing the landscape of workers’ compensation. With daily changes in regulations occurring across the country, we wanted to answer the most pertinent questions affecting how we handle claims moving forward.

Three industry experts joined us for our special edition Out Front Ideas COVID-19 Briefing Webinar Series to answer audience questions regarding the impact of COVID-19 on workers’ compensation:

Max Koonce – chief claims officer, Sedgwick

Nina McIlree, MD – vice president, medical management, Zurich North America

Thomas Robinson – co-author, Larson’s Workers’ Compensation Law

What does the term "presumption" refer to in workers’ compensation law?

Presumptions are mechanisms in workers’ compensation law used to switch the burden of proof in claims. Instead of the injured worker needing to prove the injury occurred in the course and scope of their employment, these presumptions state that the illness or injury is presumed to have occurred while on the job. Some presumption laws were already in place, but mainly applied to firefighters and first responders who filed claims related to heart and lung diseases, and sometimes cancer where exposure could have occurred on the job.

In the instance of COVID-19, presumptions are changing on a state-by-state basis. Several states, through either legislation or executive orders, have enacted presumptions relating to COVID-19 occurring in first responders and healthcare workers. Illinois has embraced a presumption that covers all essential business employees who could be at risk of exposure, and other states are looking at similar legislation.

How do these presumptions define healthcare workers?

A big problem with these presumption orders is that they are often vague. Some define healthcare workers as those on the front lines treating infected patients. Other orders simply refer to “healthcare workers” and could apply to a wide variety of people employed in the healthcare system who may have no exposures to patients. Unfortunately, this lack of definition in new statutes is confusing.

Are presumptions rebuttable? Is it difficult for an employer to prove that an employee contracted COVID-19 somewhere other than the workplace?

While not impossible, it will be challenging, especially because the goal of presumption laws is to shift the burden of proof to the employer. However, if a fact finder can prove that exposure to the virus came from someone else (e.g., someone was showing symptoms in their household), the employer may be able to file a rebuttal.

How does the industry handle new COVID-19 claims?

At the foundation of workers’ compensation, we determine each claim based on the merit of each case. That said, are legislative changes in presumptions necessary for cases like healthcare employees who have faced exposure to multiple patients with the virus? Healthcare workers are typically at higher risk anyway, so we already see a higher frequency of claims from their industry.

The current crisis also changes the investigative process for claims examiners. Their process has become much more detailed for COVID-19 claims, including contact tracing and testing to prove positives. In all presumptions, there is more entitlement for specific groups of employees, which creates inequity in claims, when other employees may be just at as much at risk.

Are the testing and quarantining periods covered within a workers’ compensation claim?

This coverage varies by jurisdiction, but some have required this to be covered under workers’ compensation. Some jurisdictions require the testing and quarantine to be covered under workers’ compensation, even if the employee ultimately is shown not to have COVID-19.

What industries are filing COVID-19 claims?

Healthcare represents the highest percentage of claims, including food service within the healthcare industry. Public entities are also seeing a large number of claims due to first responders. Combined, these industries cover about 65% to 70% of COVID-19 claims. The rest of the claims are coming from essential industries, like grocery stores, where employees cannot practice shelter in place or social distancing. There were also a few early exposure claims from the transportation industry, like airlines, but, with travel regulations in place, those have now almost entirely dropped off.

What is an employer’s liability claim?

When workers’ compensation was initially crafted, employees gave up their right to civil litigation for workplace injuries in exchange for guaranteed no-fault benefits. Under this agreement, workers’ compensation is the “exclusive remedy” for employees who suffer a workplace injury. Employer’s liability is the potential exception to this exclusive remedy. Under very narrow circumstances, certain states allow an injured employee to pursue civil litigation, alleging that the actions of the employer created a situation where the injury was “substantially certain” to occur. In regards to COVID-19, there has been some litigation filed alleging the employer did not provide proper protective equipment and knew employees risked exposure.

If we release an injured worker for modified work, but work isn’t available because of current conditions, do examiners continue temporary transitional employment (TTE)?

Because every state has its own workers’ compensation laws, the answer varies. Some states will insist that benefits be continued for a light-duty release even when an employer has no control over whether a business is currently operating due to current regulations. With a full-duty release, when many businesses are closed currently, the employee would collect unemployment in lieu of workers’ compensation benefits. Continuation of healthcare benefits for injured employees is the most crucial consideration currently, so we can encourage a return to work when businesses do reopen.

Is workers’ compensation litigation continuing given the current crisis?

State agencies are trying to manage litigation in a few different ways. Some states are using virtual or telephonic processes to work through settlement hearings. Others are using an alternative notarization process, where you can see all members signing necessary documents. The remaining states are using limited staff to process documents needed for litigation to work through the process. There are state agency matrices designed to inform clients and examiners what methods they are using and whether they are currently operating. There is a prioritization of resolutions currently because the public is facing so many uncertainties in their daily lives.

When does an employer need to report a claim involving COVID-19 to its carrier or claims administrator?

The best practice is always to report it as you would with any other work-related illness. If an employee says he has been exposed to the virus on the job and wants to file a claim, file it. Consider the future of not filing a COVID-19 claim. For example, does it leave you responsible if you did not take the necessary steps to file a claim, and OSHA gets involved, or an employee decides to file a suit? What if the employee can prove she made a clear statement about being exposed to the virus while on the job?

To listen to the full Out Front Ideas with Kimberly and Mark webinar on this topic, click here. Stay tuned for more from the Out Front Ideas COVID-19 Briefing Webinar Series, every Tuesday in April. View the full list of coming topics here.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Mark Walls is the vice president, client engagement, at Safety National.

He is also the founder of the Work Comp Analysis Group on LinkedIn, which is the largest discussion community dedicated to workers' compensation issues.

Kimberly George is a senior vice president, senior healthcare adviser at Sedgwick. She will explore and work to improve Sedgwick’s understanding of how healthcare reform affects its business models and product and service offerings.

The Messaging Battle on COVID-19: Are Insurers Losing?

I worry that the insurance industry is losing the messaging battle on business interruption coverage for the coronavirus, and at a crucial time.

Many insurers have made grand, public gestures, returning some $10 billion of premiums to customers whose lives and businesses have been put on hold by the coronavirus, but I'm not sure customers have really noticed. I worry that the insurance industry is losing the messaging battle at a crucial time. We risk being relegated to the traditional role of the bad guy, hiding behind lawyers to deny any and all claims, at a time when we need to be helping customers as much as possible--and need to be seen doing that good work.

Already, some politicians are trying to turn coronavirus into a sort of asbestos, making the insurance industry cover risks that it never signed up for. Yes, with SARS serving as a warning in the early 2000s, the insurance industry wrote policies in recent years that excluded pandemics, in a way that the industry never explicitly excluded asbestos, but public opinion is a funny thing: Groundswells can develop if they aren't headed off at the beginning. And politicians respond to groundswells. After all, it's people who vote, not corporations.

To try to figure out whether the industry had already lost the battle for public opinion, and what more the industry could be doing, I called an old colleague who has been doing PR for major insurance clients for decades. (We'll just call him Sam, because he wants his clients, not him, to be the story.) The good news is that he said the battle isn't lost yet. The bad news is that Sam thinks the industry needs to do a lot more to get the message out that it's living up to its responsibilities while helping clients however possible.

"A lot of people hate the insurance industry," Sam said. "Here's how they see us: Clients pay us a bunch of money, then they have an issue, file a claim, and the insurance company hires a lawyer to fight them--over a product they bought but never received."

He said it's crucial to keep hammering away at the message that insurance companies are in the business of paying claims. They wouldn't have any customers if they didn't pay claims.

"That message gets tricky, of course," Sam said, "because the customer hears, You pay lots of claims, just not mine...?"

Some industry leaders--including Evan Greenberg, CEO of Chubb, and John Neal, CEO of Lloyd's--have seemed to make headway with repeated assertions that the industry can't be saddled with risks it wasn't paid to take on and, in particular, that it simply isn't practical or fair to expect insurers to cover what amounts to the cost of a war.

Hitting those themes, a Washington Post columnist wrote, "While the businesses that are currently shuttered didn’t do anything wrong, neither did their insurers.... Since everyone is getting the benefit [from the shutdown], everyone should pay for it: through borrowing now and taxes later. Think of it as Americans belonging to one of the largest mutual insurers in the world: the United States of America, Ltd."

Sam said the industry doesn't do itself any favors with legislators or customers by referring to its capital as surplus or reserves. "Reserves? Surplus? Come and get it!" he said.

But he said the argument against raiding reserves is pretty straightforward: Claims for business interruption would be some $300 billion a month, for an industry with $800 billion in reserves--and, oh, by the way, that money isn't just sitting there; it's set aside to pay other claims that insurers already face. The industry wouldn't last long in the face of such claims.

Neal has said that just paying legitimate claims will already make COVID-19 the most expensive event in the history of insurance.

The fact that Marsh offered a pandemic policy two years ago and got no takers seems to resonate in conversations I have with folks outside the industry: It hardly seems fair to make insurers pay on policies that customers declined to buy.

But Sam said insurers need to get beyond the defensive. "Nobody reads the fine print until something goes wrong," Sam said, "and if you're spending all your time defending the exclusions in the fine print, then you won't be able to get the stink off you."

Going on offense means working--as publicly as possible--with governments to prepare for the next pandemic. contributing as much wisdom, technique and discipline as possible. That sort of work has already begun in the U.S., with what's being referred as PRIA (a pandemic version of the Terrorism Risk Insurance Act, or TRIA), and in Europe, with what's being called Pan Re.

Sam said that, while insurers need to stick with a hard no on business interruption claims under policies that were never designed to cover pandemics, they need to say yes in every possible way on service to customers in these difficult times.

"We have to cushion the blow as much as possible," Sam said.

When the industry does good things--and I see many--it also needs to toot its own horn more. Maybe the messages are getting lost in the shuffle because of everything else going on, but it seems to me that the industry could do a lot more to dramatize how it's helping clients. The world is hungry for good-news, human-interest stories these days. Yet a friend of mine told me that his auto insurer, one of the top five, didn't even notify him of a rebate on his premium.

"I saw the news about premium rebates, so I called my company," my friend said. "They told me, yes, we're rebating X dollars. I said, "That's great, but was I just supposed to notice on my statement, or were you ever going to tell me?'"

I suggest we tell people as often as they can stand to hear. So far, insurance commissioners seem to be siding with the carriers on business interruption policies, but lots of other forces are aligning against the industry. Consumer groups are complaining, and politicians are listening. Some civil authorities are using language in shutdown orders designed to trigger insurance coverage, and legislators in several states are considering forcing insurers to cover business interruption claims on the pandemic. Even the president said two weeks ago that insurers should cover many claims. The plaintiffs bar is, of course, ready, willing and able to help with such claims.

If Sam is right--and he's more optimistic than I am--then the industry has time to stand up for itself. But time is running short. If the tide turns, it will likely turn for good.

Stay safe.

Paul Carroll

Editor-in-Chief

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

ITL is planning to release a collection of on-demand videos which will focus on timely topics and consist of 4-6 webinars promoted and released over the course of 8 weeks.

With the world turned upside down by the pandemic, we're spending a lot of time thinking not only about how to navigate the choppy waters but also about what the world will look like for insurers and their customers once we finally (safely) reach the other side.

Fortunately, we don't have to do this thinking all on our own. We have access to most of the most innovative thinkers in the industry--after all, our very name is Insurance Thought Leadership--and to leaders in other industries, including in technology, who have a history of making the right call amid widespread confusion. Our old friend and colleague Alan Kay, the principal inventor of the personal computer, says that "the best way to predict the future is to invent it," and the leaders and thinkers we're talking to have a history of inventing the future.

In the coming days and weeks, we'll be drawing on these people heavily. In addition to our mainstay, publishing articles, we'll pull together podcast and webinar series that broadly describe what will likely be the New Normal, while diving into specific technologies that will likely drive the most change and into parts of the industry that will be most affected.

The topic we want to begin with is Risk Management, which has become particularly relevant during the COVID-19 pandemic.

After that, we plan to explore the topics you have told us are important, such as:

AI

Autonomous Vehicles

Blockchain

Connected Insurance

Cost-Cutting/Efficiency

Customer Experience

Cyber

Innovation

Workers Comp

Please let us know if you'd like to participate, whether by writing an article, by being an interview subject or by sponsoring a series and helping us get the word out as broadly as possible.

In the meantime, stay safe.

If you are interested in partnering with ITL on a topic that best showcases your brand , contact us at sponsorship@theinstitutes.org

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

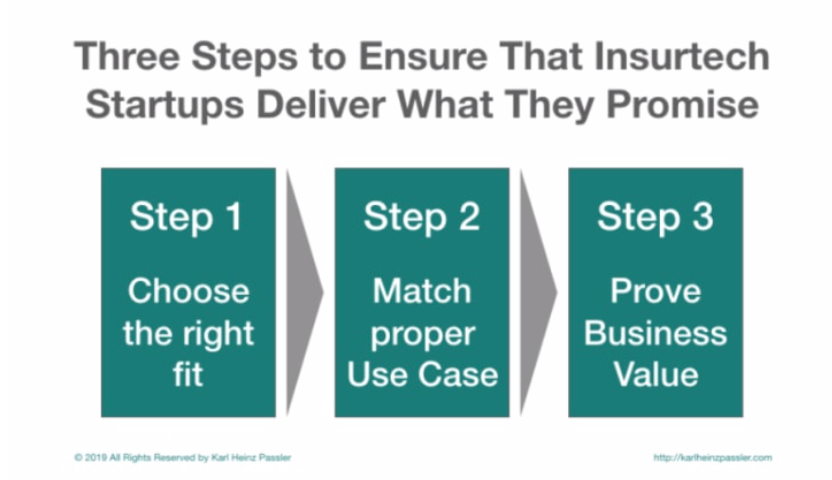

There are more than 1,000 insurtechs that can help established insurance organizations. Most of the startups look the same at first glance, but they are not all created equal. Apply this three-step process to ensure that startups deliver what they promise.

The Three Steps in a Video

This video lecture explains the three-step process in the context of "Separating the wheat from the chaff in relation to insurtechs." It contains examples that are briefly described in the following article.

Overview of the Three-Step Process

The three steps are:

Step one, focus your efforts and select startups with the right strategic and operational fit. Step two, take the skill of the startup, match it to corresponding activities and create a proper use case. And step three, prove the business value to your decision-makers before you invest more resources.

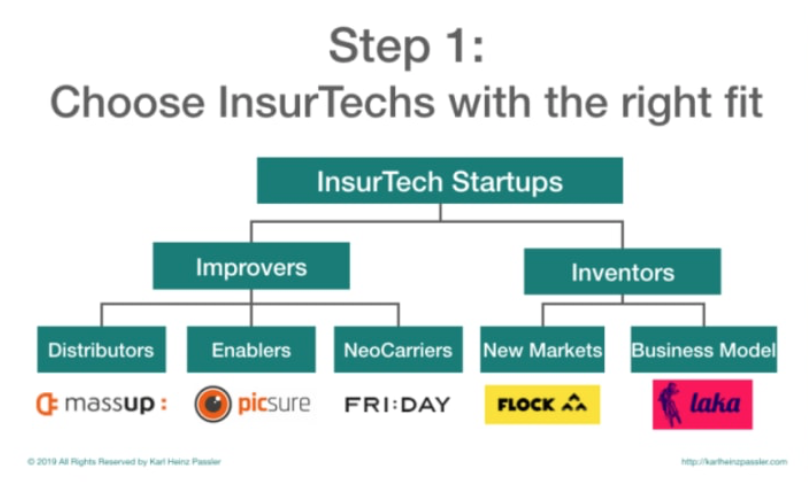

Step 1: Select Startups With the Right Fit

Start to focus your resources by dividing insurtech startups into the two groups of Improvers and Inventors. Improvers take the current insurance industry and apply state-of-the-art technology on top. In this way, they improve and digitize existing insurance processes and business models.

Divide Improvers further into three distinct types, based on their method of value creation. Distributors provide an excellent customer experience directly to policyholders. Enablers empower incumbent insurance providers to run digital services. NeoCarriers offer the full-stack of insurance activities to brokers, policyholders and incumbent risk carriers as a white-label solution.

If you begin the journey of improving your business with insurtech startups, I would pick one of these types. The low-hanging fruit would be Enablers and Distributors because they relate the most to what your organization is doing today. Pick one, two or three startups and start working with a dedicated team.

The second group is Inventors. They don’t accept how insurance is done today. Inventors question the underlying assumptions, reevaluate them and re-invent insurance propositions and business models, offering new ways to provide insurance services.

Based on the Improvers method of value creation, you can divide these insurtechs into two types. New Market Conquerers enter new markets like drone insurance (e.g. Flock), shared economy (e.g. Airbnb) and the gig economy (e.g. Uber). New Business Model Operators are the more interesting type but also harder to understand. They could disrupt the insurance industry, so you need to deploy people who are really at home in the insurance industry to understand what is going on there. One example is Laka, with its bike insurance.

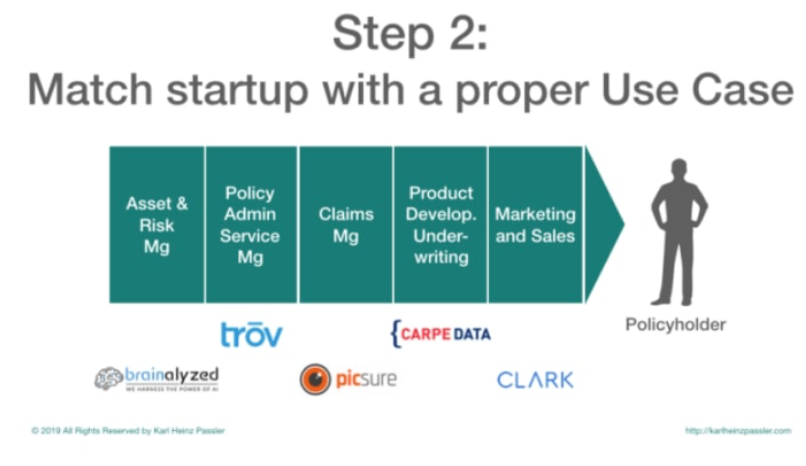

Step 2: Create a Proper Use Case

Take an insurtech with its capabilities, match it to the activities inside the insurance value chain and create a proper use case that will move the carrier's key performance indicators (KPIs) in the right direction.

Facilitate workshops with insurtechs to find out where you as an insurer can apply the new capabilities in your value chain. The value chain is a classic old school management insurtechs that documents the core activities that create value for the customer, our policyholder. This tool helps to identify suitable activities that are most likely to be located in the following departments: Asset and Risk Management, Policy Administration and Customer Service, Claims Management, Product Development and Underwriting and, of course, Marketing and Sales.

Start creating use cases in collaboration with the team of insurers and startups. A use case is the description of a workflow that creates additional value for the insurance company. After developing a series of use cases, select the most promising one and take the third step.

A startup can help detect fraud in images of claims by extracting data from images and giving insurers clues as to whether the image was manipulated after it was captured. If there are deviations from the policyholder's description (e.g. taken in Hamburg vs. Frankfurt), the insurer may have detected fraud. If the insurer does not have to pay, it reduces its loss ratio and thus increases its profit.

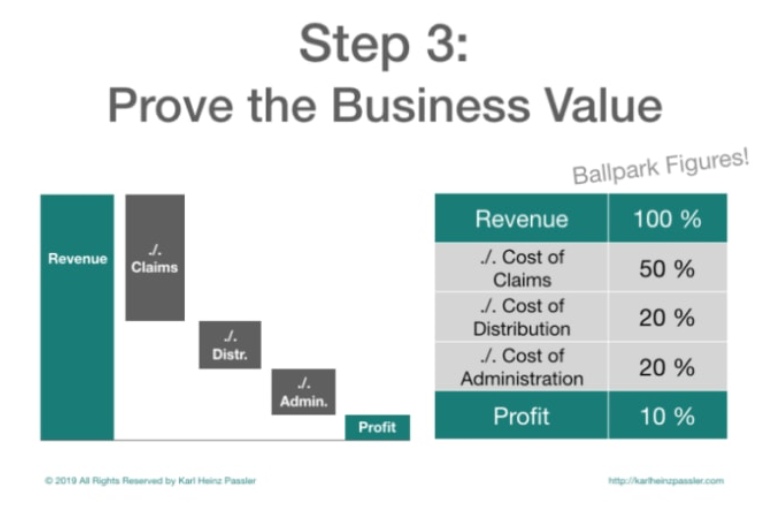

Step 3: Prove the Business Value

Prove the value of the use case before you begin to scale up. Use the value table with the five key figures on which carrier decisions are typically based. Deliver facts, not an opinion, to make the right investments.

Take the use case and execute a proof of concept (POC), do a prototype and test it. Experiment to create some real-world data. Take that data and put it into the value table with the five key figures insurance carriers decision-makers rely on. These are 1) Revenue 2) Cost of claims 3) Costs of Distribution 4) Costs of administration and 5) Profit. The calculation is as follows: Revenue minus Costs of Claims, minus Costs of Distribution, minus Costs of Administration equals Profit.

Enter your specific numbers from your test and analyze which of the KPIs will be influenced (at scale) by the use case you developed and tested. Calculate different scenarios and their results.

Another example: If you identify fraudsters and reduce your claims ratio by one percentage point (this makes your head of claims happy), you increase company profit by one percentage point (makes your CFO and CEO happy). At a premium of 1 billion euros, one percentage point corresponds to 10 million euros. All of us know that applying a "simple" image check doesn't cost 10 million euros. It is, therefore, a suspect for a proper use case to prove.

If you can prove the value of your use case with facts, it is easy to ask a decision-maker: We need more money because this use case brings the company more money than it costs.

Summary

By following this three-step process, innovators in insurance companies (and entrepreneurs in startups) can focus their efforts and only work with insurtech startups (vice versa with insurers) that have the right strategic and operational fit to help improve an organization.

Select the right partners and create proper use cases based on activities within the insurance value chain. Demonstrate the value of use cases through testing with POCs and prototypes. Then apply real-world data to the presented value table and analyze what will happen before scaling and investing more resources.

If you can prove the value of your use case with facts, you will be much more successful when asking your decision-makers for more money to invest and scale up.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Karl Heinz Passler is a product manager and a mentor for startup scouts at a pan-European insurance corporation. He is a co-author for "The Insurtech Book," which has been published by Wiley and has become an Amazon business bestseller.

There is a belief that business closure orders by civil authorities trigger civil authority coverage in business income insurance policies if the orders allege property damage of some kind. This is a misconception that is typical of generalizations about insurance contracts that come from the failure to actually read the policy language.

For example, most of the local and state governmental orders I’ve seen refer to property damage as a basis for mandatory business closures or operational changes. Here is one of the 18 “WHEREAS’s” in the City of Key West State of Local Emergency Directive 2020-03:

“WHEREAS, this order is given because of the propensity of the virus to spread person to person and because the virus physically is causing property damage due to its proclivity to attach to surfaces for prolonged periods of time;”

Dust has a proclivity to attach to surfaces, but does that result in “property damage” if I can remove it with a cloth? If I don’t vacuum my home for a month, have the floors been damaged? Admittedly, a virus can be more problematic than dust for most people, but does it actually cause damage by temporarily residing on the surface of property? These questions were addressed by the first and second articles I wrote about the COVID-19 pandemic. Yes, there is a temporary impairment of the use of the property but almost certainly no direct physical damage and likely no real damage at all.

In addition, if we’re being honest about these government-mandated business interruptions, we would admit that their purpose is to prevent or minimize the spread of disease from one person to another. Surface contamination is simply one means of this occurring. These orders really aren’t issued to prevent or minimize property damage because, realistically, there is no real property damage.

So, why do these orders include the “property damage” references? Legal gamesmanship. Well-intentioned, perhaps, but an attempt to affect insurance coverage based on a generalized comprehension of what is and isn’t covered under many, if not most, business income insurance forms. For example, following up on the Key West directive above, consider this excerpt from a local publication citing attorney Darren Horan:

“Both types of coverage – and people can have one, both or neither – but they both require physical damage to the property, which is why it was so important for the city to include specific language in its emergency declaration stating that the virus causes physical property damage. That can only help business owners with these types of coverage. Of course, it’s always a fight when dealing with insurance companies, but I’m glad Commissioner Clayton Lopez was at the meeting when I mentioned this needed language and brought it back to City Attorney Shawn Smith for inclusion in the city directive.”

Based on this narrative, the inclusion of a reference to property damage in the directive was to trigger insurance coverage, not because of any real or perceived property damage. In fact, there was no citation of any actual property damage. If anything, such orders are issued to PREVENT “property damage,” something that does little or nothing to actually trigger most business income coverage forms. For example, take this language from the Civil Authority Additional Coverage in the ISO CP 00 30 10 12 business income form:

"When a Covered Cause of Loss causes damage to property other than property at the described premises, we will pay for the actual loss of Business Income you sustain and necessary Extra Expense caused by action of civil authority that prohibits access to the described premises, provided that both of the following apply:

"Access to the area immediately surrounding the damaged property is prohibited by civil authority as a result of the damage, and the described premises are within that area but are not more than one mile from the damaged property."

Let’s parse this language phrase by phrase to illustrate why simply placing a “property damage” statement in a civil authority directive is almost certainly insufficient to trigger coverage.

“causes damage to property other than property at the described premises”

There is no allegation of any real, existing damage to any property. The policy language indicates that the viral contamination (IF a covered peril) must have actually caused damage to property. Directives like this are preventative, not remedial.

“that prohibits access to the described premises”

Nothing in this directive actually prohibits access to any premises. The directive prohibits conducting business as usual with the public. It does not forbid, for example, a property owner from physically accessing his building or business. In fact, for many businesses, they can continue operating in a modified way, such as a restaurant providing carryout or delivery of food. In situations like that, certainly the employees have access to the premises.

“Access to the area immediately surrounding the damaged property is prohibited by civil authority as a result of the damage”

There are three points to make about this last policy language excerpt:

First, there is no identification of any “damaged property.” Again, the directive is largely preventative.

Second, the directive doesn’t appear to prohibit access to the area. A business may be closed entirely to the public, but that doesn’t mean someone can’t walk or drive down the street immediately adjacent to the business. The reason for this reference to the surrounding area in the policy language is to express the intent of the coverage--for example, when a hurricane or tornado hits a neighborhood or business district, with extensive debris, downed power lines, etc., access is limited only to necessary emergency personnel. This coverage was never intended for an exposure like a viral pandemic that largely affects individual facilities and not widespread areas.

Third, if there was a prohibition against accessing the immediate area, it would have to be “as a result of the damage.” What damage? No actual damage is cited or known, much less proven, to exist.

The reason the “property damage” directive language doesn’t accomplish, in this example, what the attorney thought it did is because the basis for the language was a generalization of coverage and not what the cited policy language actually says. Unfortunately, the media, government officials, politicians and others pick up only on the generalization and not the actual contract language.

Game over.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

William C. Wilson, Jr., CPCU, ARM, AIM, AAM is the founder of Insurance Commentary.com. He retired in December 2016 from the Independent Insurance Agents & Brokers of America, where he served as associate vice president of education and research.

In their search to boost profits and reduce their loss ratio, property and casualty (P&C) insurance carriers often turn to improving a cast of “usual suspects”: sales, pricing, new product development and a host of operational areas from new business through subrogation. But the biggest area to target— the one with the largest, near-term upside potential—is claims processing. Every insurer wants to reduce operating costs, cut claims leakage and reduce claim severity.

But what’s the best approach?

That depends on whom you ask. Technology providers insist that bleeding-edge, massive new systems are the answer. Internal processing teams will push for more human resources—with more relevant experience and better training. Other executivess will tell you to focus on reducing claims fraud.

But if you ask The Lab, we will say that the best approach is to keep asking questions, because the answers will point you toward a massive payback—a windfall. For example, what is the “standard” P&C claims leakage ratio, i.e., the industry average benchmark? And what is the source for this leakage number? Probably, the answer you get on leakage ratio will fall in the 2% to 4% range. Press for the source. The likely answer will be vague and hard to pin down. It’s unlikely that the answer will be: “our routine analysis and measurement of our claims processing operations—at the individual adjuster level.”

Stated differently, the source is actually “conventional industry wisdom.” If so, you’ve stumbled into a diamond field of improvement opportunities. To scoop them up, all you need to do is upgrade your company’s ability to perceive and manage claims processing at an unprecedented level of granular detail.

It’s worth the heavy investment of initially tedious effort. That’s because actual claims leakage is typically several multiples of this conventional-wisdom average of 2% to 4%: The Lab routinely documents 20% to 30%, and even more. That means that the payoff for reducing leakage, even for smaller P&C insurers, can easily reach hundreds of millions of dollars—which drop straight to the bottom line.

No, customer experience isn’t devastated. That’s because other (completely satisfied) policyholders are having their claims paid by adjusters who follow the carrier’s guidelines. The lower-performing adjusters, on the other hand, are simply not following these guidelines, and carriers fail to practice the process-management discipline necessary to ensure that all adjusters adhere to the loss-payment rules and targets.

Now, if you ask The Lab precisely how to reduce your claims leakage and loss ratio, we will point to three underused tools, or improvement approaches, to help P&C insurers surmount this challenge and achieve breakthrough levels of benefits, specifically:

Knowledge work standardization (KWS)

Business intelligence (BI)

Robotic process automation (RPA)

While the second two—BI and RPA—require a nominal amount of technology, the first approach, standardization, not only paves the way for the other two but also requires no new technology whatsoever. Typically, Knowledge Work Standardization, or KWS, alone delivers labor savings in excess of 20%, easily self-funding its own implementation— and readily covering much of the BI and RPA improvement costs. Taken together, these three tools rapidly transform an insurer’s P&C claims-processing operation and upgrade its related management capability. This allows management to significantly reduce loss payments while simultaneously improving operating efficiency. The result is an increase in “operating leverage”: the capability of a business to grow revenue faster than costs.

Interestingly, these three tools, or improvement approaches, also deliver major benefits for customer experience, or CX, aiding in policyholder satisfaction and retention. Here’s how:

First, roughly half of the hundreds of operational improvements identified during business process documentation will also deliver a direct benefit to policyholders.

Second, the process documentation and data analysis help pinpoint the reasons that policyholders leave. The predictive models that result help reduce customer erosion.

Third, these documentation and analytical tasks also identify the most advantageous opportunities for cross-selling and upselling. In this article, we will cover these three tools/improvement approaches broadly, then we’ll drill down to explore their real- world application—and benefits—in P&C claims processing.

1: The Search for Standardization in P&C Insurance Operations

Standardization—the same innovation that gave rise to the modern factory system—is arguably the most overlooked improvement tool in insurance operations today. And it applies to everything: data, processes, work activities, instructions, you name it. In other words, variance is standardization’s costly, inefficient evil twin. Consider:

Insurance operations performance is typically reported

in the form of averages. These numbers are usually calculated for work teams or organizations. And this is also how supervisors approach their management task—by groups. Individuals’ performance is rarely measured, compared, benchmarked or managed.

Rules of thumb routinely apply. “Here’s how many claims an adjuster should be able to process in a given day or month.”

Industry lore trumps data-driven decision-making: “Claims processing is an art, not a science.” Or, even more dangerously: “Faster adjusters are the costliest ones, because they’ll always pay out too much.” (Spoiler alert: The opposite is true.)

Differences in details go unexploited: At one insurer, for example, The Lab discovered that five teams were processing claims—and each team used its own format and guidelines for notes. That single, simple issue confounded everyone downstream, as they struggled to reconcile who meant what.

“NIGO” prevails. The sheer opportunity cost of things like forms and fields submitted “not in good order,” or NIGO, can be staggering—often with tens of millions of dollars in unrecouped revenue flying just below executives’ radar.

2: Applying Business Intelligence, or BI, to Insurance Operations

Modern BI applications derive their power from their ability to create a clear picture from crushingly vast quantities of seemingly incompatible data. The best BI dashboards visualize this data as insightful, inarguable business-decision information, updated in real time. They let users zoom out or drill down easily; just think of Google maps. You can click from a state, to a city, to a house, then back up to a continent, using either a graphical map format or 3-D satellite photo.

Then why aren’t insurers routinely harnessing this power? Most already own one or more BI applications, yet they’re not delivering that critical Google-maps-style visualization and navigation capability.

This lack can be traced to two, intertwined obstacles: business data and business processes. Each requires its own, tediously mundane, routinely overlooked and massively valuable, non-technology solution: standardization.

Business datais already well defined—but it’s defined almost exclusively in IT terms. Think of the latitude/longitude coordinates on Google maps; do you ever actually use those? These existing IT definitions are difficult, if not impossible, to reliably link to business operations and thus produce useful, navigable business information.

The Lab solves this problem by mapping existing “core systems” data points to products, employees, transactions, cycle times, organizational groups and more. The solution requires standardizing the company organization chart, product names, error definitions and similar non-technology items. This is a tediously mundane task.

Technology can’t do this. But people can, in a few weeks if they have the right templates and experience.

Business processesare also already defined—but with wildly inconsistent scope. For example, the IT definition typically involves a “nano-scale” process—like a currency conversion or invoice reconciliation. Business definitions represent the polar opposite: global scale. Think of “order-to-cash” or “procure-to-pay.” All parties involved—throughout business and IT—thus talk past each other, assuming that everyone is on the same page. Worst of all, almost no business processes are documented. They exist informally as “tribal knowledge.”

The Lab solves this disconnect by mapping business processes, end-to-end at the same “activity” level of detail that manufacturers have perfected over the past century. Each activity is about two minutes in average duration. The range for all activities is wide but easily manageable: from a few seconds to five minutes. Over the past 25 years, The Lab has process-mapped every aspect of P&C insurance operations—and we’ve kept templates of every detail for these highly similar processes. Consequently, we can (and routinely do) map business processes remotely, via web conference... around the world!

Rigorously defining, standardizing, and linking business data and business processes underpins the best BI dashboards, delivering the Google-maps-style navigation that execs crave. This is how it's possible to build astonishingly insightful BI dashboards that help make claims leakage losses apparent to our clients.

3: Robotic Process Automation, or RPA: A Powerful New Tool for P&C Carriers

Robotic process automation, or RPA, is simply software— offered by companies such as Automation Anywhere, Blue Prism, and UiPath—which can “sit at a computer” and mimic the actions of a human worker, such as clicking on windows, selecting text or data, copying and pasting and switching between applications. If you’ve ever seen an Excel macro at work, then you can appreciate RPA; it simply handles more chores and more systems. And it isn’t limited to a single application, like Excel. It is as free to navigate the IT ecosystem as any employee.

RPA “robots” are thus ideally suited for mundane yet important repetitious tasks that highly paid P&C knowledge workers hate to do. Better yet, robots work far faster than people, without getting tired, taking breaks or making mistakes. This frees up human workers for higher-value activities.

RPA also confers customer experience, or CX, benefits. With faster operations, customers enjoy the Amazon-style responsiveness they’ve come to expect from all businesses. On-hold times are reduced, claims get processed faster and the entire company appears more responsive.

Beyond the dual opportunities of knowledge-worker labor savings and CX lift, RPA holds the power to disrupt entire industries. Deployed creatively in massive waves, it can deliver windfall profits on a scale not even imagined by its purveyors.

Yet, today, most insurance companies’ RPA efforts, if any, are stalled at the very beginning; recent surveys indicate that internal teams hit a 10-bot barrier and struggle to find more opportunities, or “use cases.” That’s because the underlying processes to be automated are never made “robot-friendly” in the first place. So there needs to be scrutiny of the different activities—and the elimination of all of the wasteful ones that hide in plain sight, such as rework, return of NIGO input, and so on.

How to Overcome the 10-Bot Barrier in P&C Claims Processing

First, set expectations to focus on incremental automation with bots. No, you’re not going to replace an entire adjuster with a bot. But, yes, you will be able to quickly use a bot to call a manager’s attention to a high-payback intervention in the P&C claims-adjusting process. Examples:

Managers look for inactivity on open claims: If a claim is open with no activity in the last 10 days, that’s a red flag. But many claims are overlooked. A bot can call these out promptly.

Full-replacement cost, instead of partial replacement cost, is a major cause of overpayment that is most prevalent in roofing, flooring and cabinetry replacements. Bots can track payments and send management alerts based on line-of-coverage and even more granular detail. Roofing examples include: replacement, whole slope vs. whole roof; and number of roof squares replaced.

Audits are conducted on claims to improve quality and consistency—and to reduce overpayment. However, these are done on a very limited sample and only after claims have been paid and closed. Based on learnings from past audits, bots can alert management when certain claims- processing failures happen on a live basis. Managers can intervene... before payment.

Standardization (KWS), BI, & RPA: Focusing on P&C Claims Processing

All three of the above tools, or improvement approaches for P&C carriers—standardization or KWS; business intelligence, or BI; and robotic process automation, or RPA—can be readily applied to claims operations. Indeed, they seem to be custom- made for it.

Standardization

Consider the following story, created from a mashup of different P&C insurance carrier clients of The Lab:

This “insurer” had plenty of claims data to share with The Lab; in fact, theirs was better than most. But that’s not saying too much: While 40% of the data was usable and comprehensible, the other 60% wasn’t. (Remember: This is better than most P&C insurers.)

Data was reported weekly, and sometimes daily, on an organization-wide basis. Here’s what they had data to report on:

Overall averages of claims processed, based on total headcount.

Average losses paid per claim.

That said, the company never tracked the performance of individual claims processors. They were all effectively “self- managed,” following their own individual procedures. There were no standard, activity-level instructions and guidelines, set by management, for quantifying targets for time, productivity or effectiveness. There were, on the other hand, vague, directional methods, many in the form of undocumented “tribal knowledge” and “rules of thumb.” The claims processors simply managed their own workdays, tasks and goals—similar to Victorian-era artisans, prior to the advent of the factory system.

When pressed, the company defended its choice to not track individual performance. The two reasons it gave would come back to bite the managers:

They were confident that individual performance, if measured, would only vary by about 5% to 10%, maybe 15% at most.

They were equally confident that imposing time and productivity quotas on processors would increase loss severity. In other words, they were completely sure that faster claims processing equates to overpayment of claims.

However, their very own data contradicted both of these notions—in a huge way:

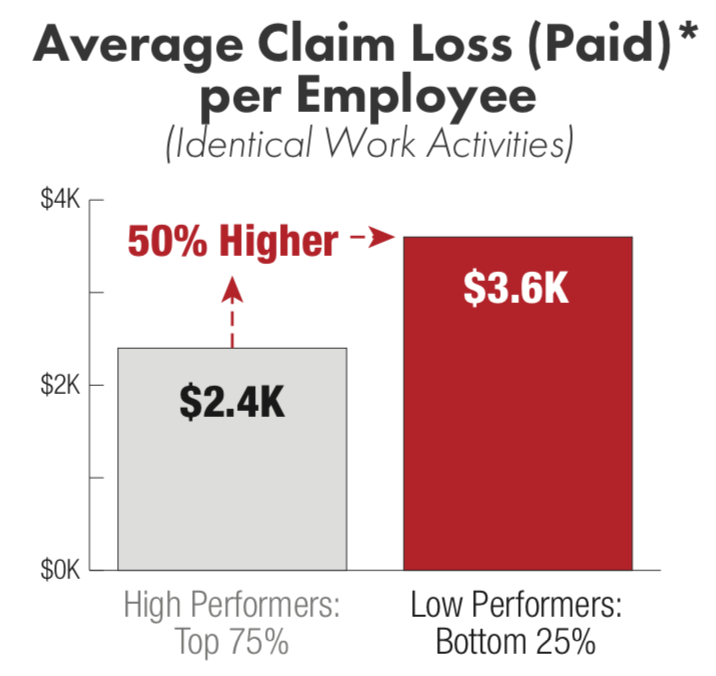

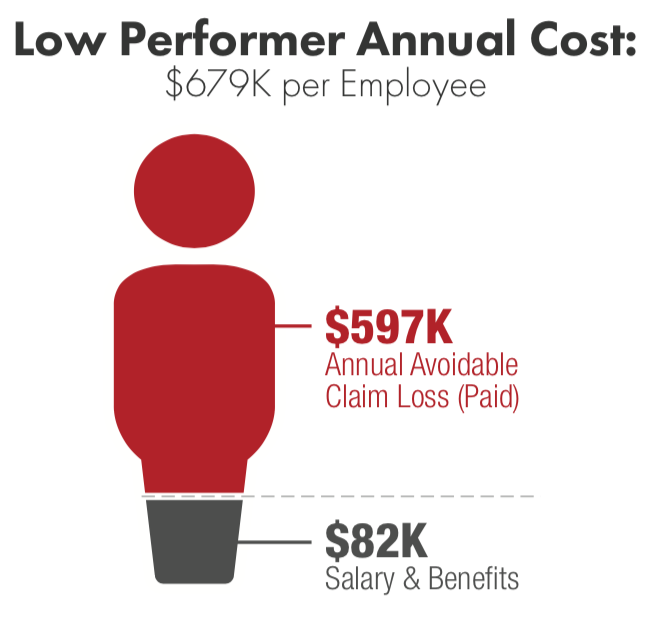

First, the “long tail” of claims processors revealed a 250% variance between the top and bottom quartiles of individual performers—that’s 15 to 50 times higher than what management believed to be the case. In other words, the top three quartiles were out-processing the bottom quartile so much that there was no hope of the bottom quartile catching up—even getting close to the average. Put another way: Reducing this variance alone would yield a 25% capacity gain—an operating expense savings. And it could be accomplished by the top performers’ simply processing just one more claim per day—an increase they’d barely even notice.

Second—and just as important—the data revealed that the slower performers actually overpaid each claim by an average of 50%, an amount that totaled in the scores of millions, swamping the amount spent to pay their salaries. This carrier was thus getting the worst of both worlds with its lowest performers: They were slower, and vastly more costly. Not only that, they dragged down the average performance figures (not to mention morale) of the faster, leaner producers.

The impact from these revelations equated to losses measured in hundreds of millions of dollars. Incidentally, the story above is not rare; rather, it’s typical. As we’d mentioned, it’s based on a mashup of several insurance carriers.

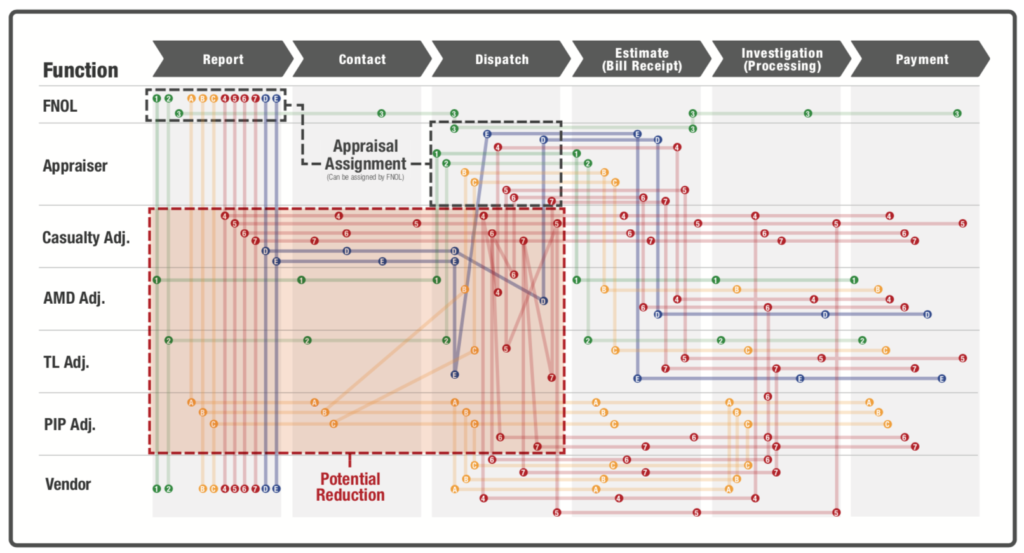

Here’s one other standardization eye-opener. The claims process itself was rife with rework, turnaround, pushback and error correction. As a claim made its way through reporting, contact, dispatch, estimating, investigation and finally payment, it bounced and backtracked between the FNOL (first notice of loss) team, the appraiser, the casualty adjuster and so on. When presented with this “subway map” of the as-is process, the insurer’s executive sponsors were aghast:

Fortunately, the “spaghetti mess” can be cleaned up, even without new technology.

Business Intelligence (BI)

The Lab often encounters P&C insurance companies that invest heavily in systems such as Oracle Business Intelligence or Microsoft Power BI yet struggle to get value from these advanced analytics platforms.

Many of the issues stem from failing to “complete the final mile” when it comes to data definitions and hierarchies; that is, companies aren't reconciling the IT-defined data elements with their own business-defined operations characteristics. This problem can often be traced to a disconnect between business leaders and IT organizations.

An IT person could—and often does—assemble and manage business intelligence for business units. But the person needs to understand the business so well that the person could confidently select which data to use and aggregate so that the final KPI (key performance indicator) in the resulting dashboard represents reality. And even if the person managed to create a BI picture of perfect “reality,” there’s no guarantee that the business would accept it. Let’s be frank: Creating useful BI and related analytics is a towering challenge. It’s overwhelming not only to IT; most businesspeople lack both the documentation and the comprehensive perspective to pull it off. So, the status quo continues: The “business language” experts will talk with the “IT language” experts, and the business executives will still lack the Google-maps insights they seek.

Another BI stumbling block is the “false precision” of too much data and too many categories. Consider the automotive insurer with “claims types gone wild”—such as “Accident: Right front fender,” and “Accident: Left front fender,” and so on. The Lab’s BI dashboards will often reveal to claims executives that 20% of the claims types represent 80% of the volume—another valuable, “long-tail” insight.

Robotic Process Automation (RBA)

As noted earlier, operational issues and customer-experience or CX challenges are typically two sides of the same coin. Often, both can be addressed by robots.

For example, consider the policyholder who calls the FNOL contact center and validates info. Then the person is handed off to another rep, who must re-validate the info. And then another. And another.

That’s not just an operational mess. It’s also creates a clear and present danger of losing that customer, hiding in plain sight.

While robots can speed repetitive chores, they can’t fix the underlying business processes (remember that FNOL spaghetti map, above?). Fortunately, Knowledge Work Standardization can. And once it does, the robotic possibilities are practically limitless: They span everything from sales prospecting to renewal notices to premiums/commissions reconciliation.

You saw how RPA bot deployments augmented the work of claims-processing managers. The next step is to augment the hands-on work of rank-and-file adjusters. Again, don’t try to replace the entire job position. Instead, augment the processor’s activities. In particular, hand off the adjuster’s mind-numbingly repetitive activities to the bot. This will allow the adjuster more time and thought—not to mention accountability—for complying with the policy’s payment guidelines.

For P&C claims, there are numerous opportunities to “park a bot” on top of routine, repetitive, knowledge-worker activity. Think of these as admin-assistant bots for adjusters. Here are two of many examples:

The “pre-adjudication assistant” bot. Adjusters spend lots of time sorting out “unstructured” information at the receipt of the FNOL. For example, they read descriptions of damage that arrive in free text data fields, then they standardize it and proceed to adjudication activities such as looking up coverages and setting reserves for the claim, prior to contacting the insured. Most, if not all, of these activities can be performed by RPA bots—but only if the inbound information is standardized. The Lab has used its KWS methods to create drop-down menus for this data and make it RPA-friendly. This standardization can be done incrementally, enabling bots to prep claims for adjusters: They look up coverage limits, set reserves and prep for the adjuster’s call to the insured.

The “customer contact assistant” bot. Adjusters, and others in the contact center, spend a great deal of avoidable and inefficient effort communicating with policyholders regarding their claims: advising status, notifying for damage inspections, obtaining corrections to initial NIGO information and more. Simply contacting customers can be a tedious, time-consuming and inefficient process; bots can help. They can be configured to send notifications to customers, preempting calls to the contact center. Bots can also initiate “text-call-text” notifications to customers’ cell phones. Here’s how it works: Bots, at the push of a button by the adjuster, send a text to the customer. The text may notify the customer to expect a call from the adjuster—avoiding call screening. The adjuster calls and gets through. Afterward, the bot sends a confirmation of the issue or next step.

Make the Move Toward Improved Insurance Operations & Reduced Loss Ratio