Unemployment is rising due to COVID-19, and some of the top risk management firms in the industry have indicated that fraud will also quickly increase. While claims fraud, inflated repair invoices and other common scams are probably the first that come to mind, roadside assistance fraud is another issue to which insurers should pay attention. It’s more common that one might think.

Especially as insurers increasingly offer ecosystem services such as roadside assistance to strengthen customer loyalty and generate additional revenue, it’s important that they ensure their roadside assistance partners are taking measures to protect against fraud, which can range from customers abusing the aid to get free gas, to tow operators sending fraudulent invoices.

Here are some of the ways to protect against roadside assistance fraud:

Fast Payments Promote Trust

The adage, “An ounce of prevention is worth a pound of cure,” holds true in roadside assistance fraud. Instituting policies that reduce the incentive to commit fraud is far less painful than attempting to recover a loss, and one of these measures is to pay tow operators quickly. Especially in difficult times, those who issue payment within minutes instead of the standard Net-30 will foster loyalty that cuts down on fraud, especially while many companies are struggling to keep operations running.

Tow operators balk at complex billing that deducts difficult-to-understand fees from their payment. The fees create unpleasant surprises that can make the difference between a profit and a loss. So, make sure that roadside assistance partners offer clear and transparent billing.

Transparency in Invoicing

With fraud on the rise, be on the lookout for roadside vendors that will attempt to bill you for “ghost” services. One way to mitigate this type of fraud is by asking your roadside vendor to provide transparency into completed services, ideally in real time. Require your roadside vendor to provide an unfiltered view into jobs, as well as customer confirmation that the job was completed. This kind of transparency makes it far less likely that you’ll be inaccurately billed or overcharged. Plus, this level of transparency gives you a better view into the customer experience.

History tells us that, during times of high unemployment, we are likely to see more bad actors entering gig economy jobs. But fraud is often easily caught at the background check level, which can prevent bad actors from getting into the system in the first place. While it's easy to provide a false name, it’s more difficult to provide a false Social Security number and matching drivers license. So, it’s important to have transparency in how tow operators are onboarded into your roadside assistance partner’s network and the methods they use to verify the identity of each driver and the person's background. Ask about the types of checks they’re using to ensure identity verification, proper licensure and insurance compliance. Ideally, you want visibility all the way down to the driver level of who is servicing policyholders.

You need transparency because, while background checks have been an industry standard for years in roadside assistance, they may not be conducted at the appropriate level. For example, it’s common to accept a prior, third-party background check for a new contractor, a practice that leaves critical gaps in a contractor’s history and doesn’t necessarily report on charges or information relevant to the position. A “clear background check” usually does not tell you that the driver’s license is suspended, for instance.

Background checks should be run annually at a minimum, but there are now next-generation background check services that will run in the background to provide live monitoring of arrest feeds, county reports and other proprietary information sites. This kind of continuous monitoring can flag events that could signal trouble, providing the opportunity to prevent fraud before it occurs.

The Importance of Analytics

Some policy holders may look to their roadside policy to help get what they see as “free fuel” as many times as possible. It’s a common scam, where drivers purposely avoid filling up and, when they run out of fuel, call the roadside assistance service to get some for free.

This kind of fraud is most effectively detected through technology, specifically artificial intelligence, machine learning and analytics. Data analysis can identify previously overlooked trends to catch these kinds of issues and resolve them quickly. Insurers save money when machines and automation do the work instead of adding to headcount or finding problems only after the damage has been done.

Even as fraud is anticipated to increase, roadside assistance many times has been overlooked. Don’t settle for passive fraud detection. Demand transparency and encourage the use of technology to mitigate risk, which will both reinforce your reputation and drive your bottom line.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Andrea Hall is director of marketplace operations for HONK Technologies, a next-generation roadside assistance provider. She previously served as a senior claims analyst for litigation with AllState.

The plague that is coronavirus continues to threaten our way of life and our very existence.

And while we wait for our best scientists and Big Pharma to develop and deliver the vaccine we so desperately need to begin the return to some semblance of our prior lives, it is notable that finance and insurance – the nation’s third-largest industry – is coping better than most would have ever imagined, thanks to the technologies that have been gradually but surely emerging for at least the past two decades.

Now, with few if any acceptable choices, these technologies and the benefits they offer participants in the insurance ecosystem are being more eagerly embraced and adopted by insurers in the battle they are waging for their survival. Artificial intelligence, in all its manifestations, drives many solutions. It helps us transform the digital rivers of data flowing between us and our many connected devices and facilitates effective real-time decision making. As noted on April 30 by Microsoft CEO Satya Nadella, “We saw 2 years of digital transformation in two months.”

WFH (work from home) is a perfect example and, defined more broadly, encompasses video conferencing, distance learning, educational and training sessions and internal business communications platforms. Platforms such as Zoom and Slack are well-known solutions, but dozens of similar services have proliferated. Artificial intelligence powers all of them and allows for total individualization of communication preferences. Insurers have been able to leverage them in operations, and in a matter of just weeks have redeployed thousands of inside employees from corporate buildings to their own homes, hardly missing a beat. In many cases, customer experience has actually improved as distributed workflow algorithms ensure better matching of customer profiles with staff expertise and skill sets, while also reducing the associated potential risk of litigation.

The claims process has become another major beneficiary of artificial intelligence and other new technologies, including computer vision, machine learning, digital customer self-service and electronic claim payments. Contactless (or touchless) claims is now a reality, with some large insurers reporting up to 50% use of this method across all claims.

In a world where claims are submitted and paid without physical inspection and validation, fraudulent claims detection becomes an even higher priority, and here again solutions incorporating artificial intelligence, predictive analytics and computer vision are being deployed effectively. The recent partnership announced between Shift Technologies and Snapsheet is a perfect example, and there are many more in the works and underway.

Analytics also plays a critical role in streamlining claims settlement, which is recognized as a primary driver of customer loyalty and retention. This includes the current rapid adoption of digital claims payments, which speeds up the process while removing significant processing costs for carriers and getting money owed more quickly to customers; for many, cash flow has become more important than ever. The speedy settlement of claims has previously meant higher costs and a risk of overpayment, especially in high-volume catastrophes but by employing AI technologies these risks are now being mitigated.

Here is a partial list of the many additional ways in which AI and technology will play an increasingly critical role;

a solid working knowledge of AI and technology will become a prerequisite for even entry-level employees and most certainly for organizational advancement

the nature of risk has changed, and AI allows carriers to respond in real time (e.g., several large life insurers ceased issuing new policies on those over 75 almost immediately after COVID-19 altered mortality rate tables

data allows management to navigate change, and AI is an important tool in generating operational road maps

remote work forces present new management challenges in maintaining morale, motivation and corporate culture; AI enables automated monitoring and appropriate development and testing at the individual level

in a world of limited resources, partnerships will become more critical, and, for those that incorporate AI, relevant corporate expertise will be mandatory

continuous learning and technology development will help meet carriers’ long-term needs and goals

In an impressive example of the power and potential for technology in the insurance industry, conference production companies have quickly pivoted scheduled live events to virtual alternatives. (Insurance Nexus by Reuters Events has reimagined its “Insurance AI and Innovative Tech USA” conference scheduled for Chicago and is presenting it as a free, conference and meeting platform on May 27-28. The conference features over 30 speakers, 20 case studies, thought leadership discussions and fireside chats with key insurance decision makers, interactive sessions with live panels, Q&A and polls. A digital exhibition will feature over 20 solution providers and a one-on-one meeting service will connect participants sharing common interests. You can register here.)

As much as we all wish coronavirus had never happened, it has supercharged innovation in the insurance industry. Some changes are welcome, many of which are likely to be permanent, and which will benefit all stakeholders in this critically important industry.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Stephen Applebaum, managing partner, Insurance Solutions Group, is a subject matter expert and thought leader providing consulting, advisory, research and strategic M&A services to participants across the entire North American property/casualty insurance ecosystem.

The ability to micro-census – that is, to gather granular data about individual homes and businesses and use it to inform underwriting – will lead to the biggest changes in flood insurance since the launch of the National Flood Insurance Program (NFIP) in 1968.

Most visible among these changes will be the transformation of NFIP policies and the rise of private flood insurance, which micro-censusing makes possible (read: potentially profitable at scale) for the first time. Here, I’ll examine the rise of micro-censusing in insurance; its likely applications in the flood market; and the potential impact on NFIP and private products, the agents selling them; and the Americans they’ll protect.

The Rise of Micro-Censusing and Its Applications in the Flood Market

In the last two decades, innovation in the insurance industry has been powered by better data. Data collection from smart devices is changing how health and auto insurers price policies, and data from services like Google Maps is changing how underwriters assess business insurance applications.

In homeowner’s insurance, providers are pulling publicly available, address-specific data – from roof type to proximity to a fire hydrant – and feeding it to algorithms to assess risks.

All of these can be considered examples of micro-censusing because they use data at the individual rather than demographic level to determine risk, which makes for much more accurate assessments.

Now that readily available tech makes micro-censusing possible and practical, it’s become wildly popular. With micro-census data, insurance providers can price policies more accurately and manage risk far better than was historically possible.

This is a boon for markets like flood, where existing risk models are often outdated. Micro-censusing makes it possible to assess risk on a property-by-property basis in something close to real time.

In practice, this means, for example, that the houses on the lower-lying part of a street, where water tends to pool during heavy rainstorms, could receive vastly different quotes from those at the top of a modest hill, where puddles typically don’t form. Homeowners at both locations would receive more precise quotes.

Risk Rating 2.0: How NFIP Is Leading the Way

FEMA is redesigning its flood insurance products, thanks in part to micro-censusing breakthroughs. In October 2021, the NFIP plans to roll out Risk Rating 2.0, an all-new rating methodology.

While not many details about Risk Rating 2.0 are public, the update is expected to change NFIP policies in a few fundamental ways.

First, micro-censusing capabilities are expected to introduce property-specific risk assessment capabilities, which will make way for flood insurance policies that are tailored to each household.

The new rating engine is also expected to help agents accurately price and sell policies. More rating clarity will help policyholders better understand their property’s flood risk and how that risk is captured in their cost of insurance.

Perhaps most importantly, NFIP’s rating characteristics under Risk Rating 2.0 include the cost to rebuild a home, which means that NFIP will aim to give more affordable quotes to owners of lower-value homes. In other words, the system will be able to provide fairer policies to all homeowners.

The Impact of Micro-Censusing on Private Insurance

In addition to changing the way the NFIP rates policies, micro-censusing technology is also drawing private insurers to enter the flood market. The new availability of data means they can now more confidently assess and underwrite risks around the country.

The implications of this are significant: With private insurers entering the market, there’s sure to be an increase in available products, which means greater opportunity for Americans to protect their homes and greater opportunity for agents to grow their books and better serve their customers.

Greater product availability will also put less strain on federal disaster funds. Today, 20% of all NFIP claims come from properties that aren’t in high-risk areas. Those properties receive a third of all federal disaster assistance for flooding, in part because they’re not required to carry flood insurance.

In other words, the impact of micro-censusing (and other technology) on flood insurance can’t really be overstated, especially in an era where FEMA’s official position is “anywhere it can rain, it can flood.”

Micro-Censusing Will Bring Macro Changes to America’s Flood Insurance

Today, the typical homeowner faces a 10% chance of fire loss over the course of a 30-year mortgage, but a 30% chance of flood loss. Still, 85% of homeowners have fire insurance and just 15% have flood insurance. These are clear indicators that flood insurance in America needs a makeover.

Micro-censusing has the power to spark dramatic change in the industry. The granular data it provides will lead to the entry of more private insurers and the improvement of NFIP policies, which will increase agents’ ability to find appropriate coverage for their customers. Overall, this will mean better flood protection for at-risk Americans.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Ralph Blust is the CEO of National Flood Services. National Flood Services uses technology to help insurance companies and agents manage flood programs, sell policies, process claims and create a better, more efficient experience for their customers.

As businesses around the country prepare to reopen, there is a concerted effort made to prioritize the safety of the workforce. Employers are also preparing to face more leaves of absence than ever as they account for employee childcare needs, at-risk groups with pre-existing conditions and possible employee COVID-19 cases. So, how do we approach reopening the economy with these concerns in mind? Furthermore, how does the workers’ compensation industry provide access to care for injured workers throughout this crisis and in the future?

Three industry experts joined us for our special edition Out Front Ideas COVID-19 Briefing Webinar Series to discuss access to care and the return to work during the COVID-19 crisis:

Jennifer Ryon – chief revenue officer, Prime Health Services

Leave of Absence and COVID-19

Sweeping changes to leave of absence laws are rapidly occurring at both the federal and state levels, helping employers adjust to the needs of their workforce. They are also expanding our industry’s terminology of “return to work,” as it applies to how employers are adapting their efforts through the pandemic.

The Families First Coronavirus Response Act (FFCRA) bill, introduced in mid-March, requires employers with 500 or fewer employees to provide their workforce with paid sick leave or expanded family and medical leave for specified reasons related to COVID-19. The bill requires up to 80 hours of paid sick leave at the employee’s regular rate of pay when an employee is in quarantine or experiencing COVID-19 symptoms and seeking a medical diagnosis. If an employee needs to take care of an individual subject to quarantine, or care for a child whose school or childcare provider is closed due to the pandemic, the employee is entitled to 80 hours of paid sick leave at two-thirds of the regular rate of pay. An additional 10 weeks of paid expanded family and medical leave at two-thirds the employee’s regular rate of pay must also be provided if an employee must care for a child whose school or childcare provider is closed due to reasons related to COVID-19. While the requirements only apply to businesses with fewer than 500 employees, the majority of businesses with more than 500 employees have instituted additional paid family leave or allowed their workforce to use their paid leave for COVID-19-related reasons.

Many state and statutory paid leave policies have extended rights that are similar to the coverage offered by the FFCRA. Some of the nuances of these extensions include additional unemployment benefits for individuals who have been furloughed or laid off. Some states also allow for accrued paid sick leave for employees and are allowing employees to use these benefits for reasons related to COVID-19. Employers need to understand that some of these state and federal changes may run concurrently with offerings from self-insured plans. Some policies have offset provisions that allow benefits like short-term disability or workers’ compensation to be offset by benefits offered at a state or federal level. For example, if an employee is taking leave to care for a child whose school is closed due to COVID-19 reasons, they would benefit from the FFCRA, but not be able to take advantage of short-term disability. Self-insured benefits should be used as supplemental coverage, instead of being used in addition to federal and state benefits, so the employee is receiving 100% of standard pay in total.

As businesses consider their reopening plans, they should consider three components: preparation, deployment and sustainability of employees’ return to work. These components should be guided by principles that include the safety of the employees, visitors and general public, compliance from public health organizations and government agencies, collaboration across the organization and agility that enables a swift response to changes that may occur. Many questions require answers for each component of the plan, including:

Preparation

Have you considered both community readiness and facility readiness?

If employees return to the office, can you ensure social distancing? Is it being enforced within the community?

Have you adjusted the footprint in your office to allow for safe social distancing? Is it possible while still maintaining productivity?

Do you have testing capabilities?

Will you require personal protective equipment (PPE) to be worn? Can employees buy their own, or will you supply items, like face masks, to your workforce?

Have you allowed for flexibility in the workforce, especially for groups more vulnerable to the illness, and employees needing to care for children?

Deployment

Are employees adapting to the changes, or do you see a decline in productivity?

Have employees made use of flexibility policies? Is there an increased demand for leave?

Do employees feel safe with the return to work, or is there significant apprehension?

Are you adapting to the needs of your workforce?

Are you enforcing the use of PPE? Are employees encouraging others to maintain safe social distancing?

Is testing working, or are you seeing a rise in employee transmissions?

Sustainability

Have you been able to phase more employees back into the physical workspace?

Are employees more productive than they were when working from home?

Do employees still feel comfortable coming into a physical workspace?

Is the community prepared for a possible second wave of the virus? Has a vaccine been established?

Are you able to pivot back to a work-from-home model if necessary?

Access to Care

With hospitals not offering elective surgeries due to the pandemic, we may be considering how our injured workers are getting the care they need. It is also important to consider how we are handling these changes operationally between employers and claims teams. Are we considering which patients are more at risk? Can we use analytics to understand which patients should be recovering? Are there significant milestones tracked in a patient’s recovery? What are the expectations of your claims teams? Through this crisis, it is crucial to take a personalized approach to understand both the functionality of the team and the injured worker within a claim.

Preferred provider organizations (PPO) work as a network for connecting workers’ compensation resources (hospitals, primary care specialists, occupational health, etc.). Some are providing their clients with a real-time listing of what providers are currently available, including operating hours and telehealth capabilities. While serving both the client (third-party administrator or carrier) and the provider, the challenge lies with how to provide better help to the client. TPAs and carriers are currently working with claims teams on their workflows to act as a liaison for communication between the payer, provider, employer and employee. This need for improved communication will increase as businesses around the country reopen and there is further demand to locate a provider.

Regulators are assisting in healthcare needs through efforts to push telehealth legislation. With patients fearing possible exposure from in-office visits, demand for telehealth is increasing. Harvard reported a 60% drop in in-person visits, with a 10% increase in telehealth visits. Due to increased demand, some physicians have rushed to offer telehealth capabilities without understanding regulations first. States are addressing issues related to telehealth, such as limitations on prescriptions that can be prescribed over the phone and the scope of care being provided.

Provider Access

There are concerns about on-hold elective procedures because there are restrictions on which providers are allowed to operate and which patients they can see. Dentistry, for example, can only see patients with infections or pain, which may result in more expensive procedures in the long term. However, patients are missing wellness visits that are crucial to the recovery process. For instance, serious procedures like biopsies, removal and replacement of orthopedic devices or hardware and cast replacements may result in further long-term damage to the patient. There may be an increase in the expansion of benefits in the instances where an injured worker needed care but could not receive it.

With elective surgeries being canceled or postponed, providers are adjusting through reschedules based on pain levels and how likely a patient may be to resort to an emergency room visit. With a decline in patients, some private practices are being acquired and consolidated by larger healthcare systems. Some satellite physicians are being reassigned to hospitals to help with pandemic needs. With healthcare staff adjusting to current needs, it is vital to assess how quickly they can be reassigned back to their original roles when we return to a state of normalcy, and the demand for elective procedures increases.

Preparing Claims Teams

As we plan for the future beyond the pandemic, there is a need to address the impact on claims teams. They will need to know how to prioritize medical care for injured workers. Do they understand how social isolation has affected the injured worker? How has this crisis affected recovery and the injured worker’s level of functionality? Do you have tools at your disposal to suggest help for those affected more severely? Developing a communication plan for your claims teams and emphasizing data collection on current claims will create a more streamlined process while creating a better understanding of the patient population.

To listen to the full Out Front Ideas with Kimberly and Mark webinar on this topic, click here. Stay tuned for more from the Out Front Ideas COVID-19 Briefing Webinar Series, every Tuesday in April and May. View the full list of coming topics here.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Kimberly George is a senior vice president, senior healthcare adviser at Sedgwick. She will explore and work to improve Sedgwick’s understanding of how healthcare reform affects its business models and product and service offerings.

Mark Walls is the vice president, client engagement, at Safety National.

He is also the founder of the Work Comp Analysis Group on LinkedIn, which is the largest discussion community dedicated to workers' compensation issues.

Although the speed of recent changes for us all has been breathtaking, learning how to be productive when working from home is not new.

Given that so many leaders, perhaps including you, are suddenly facing the challenge of working from home as a new normal, it seems only fair to share what I've learned in the nearly six years since I launched this blog and my business.

I’ll start with the basics. What I’ve learned about creating and protecting a productive place to work in a home that you probably didn’t buy or furnish for this purpose. Let’s think about your working space and behavior.

1. Environment matters

Once you start to work for prolonged hours at home, you notice how different your environment is to the office. Noise, interruptions, distractions, discomfort or too much comfort – all can be issues.

Your working space

I can recall early on learning that just trying to use the dining room table was a bad idea. Too many distractions and through traffic. As we learned from Cal Newport in his book “Deep Work,“ it is vital to have a working space that is conducive to concentration and minimizes distraction.

My next location was working in one of my children’s old bedrooms (fortunately we’ve reached a life stage when they’ve all moved out). This was better, but still had the feel of a bedroom. A room designed for comfort and snoozing is not the visual cue you need when reading, writing, planning or making key decisions.

One advantage of working in an old bedroom is the simple device of a door that closes. This is important psychologically as well as physically. I encourage you to close the door and to tell others in your household that when the door is closed you shouldn’t be disturbed unless it’s urgent. Some fellow business owners I know even use a Do Not Disturb sign.

Transforming your home office

Over the years, I have gradually invested in transforming the space around me. Aspects that have helped (in creating a space that helps me focus and get more done) include:

Filing cabinets and bookshelves (less cognitive load if less cluttered)

In trays and a filing system for prioritization of printed material

A clear desk space, only containing what is needed for the current task

Notice boards with longer-term dashboards and reminders in sight

A wall planner with colored dots to help me see the year visually

Clear floor space for standing and pacing to think or take calls

Different people will find different aspects of my approach work for them. Having chatted to many others who work from home, I don’t believe there is one right answer. What matters is that you stay aware of when you are distracted or when tasks take longer than they could.

Be honest with yourself, and, where a more conducive environment would help improve your focus, take action. When you are going to be working in the same space for a long time, even small improvements can give you huge cumulative gains.

2. Habits and your routine matter

I’ve learned that I can’t rely on my motivation and consistency every day. It’s human nature that we have days when we feel ready to take on the world and others when we’d rather stay in bed. For me, it’s proved better to focus on developing routines and habits than to rely on motivational posters or "getting pumped" pep talks.

“Atomic Habits” by James Clear confirms much of why certain changes have worked well for me and others have not. That book will really help you develop good habits and stop bad ones.

Building on that habit of planning my day and prioritizing what matters most, for a few years I invested in Michael Hyatt’s Full Focus Planner. This did help establish a number of good habits for me, including getting clear on my "big three" each day and reviewing my week.

The concept of the big three is to review everything you’d like to get done and be forced to choose which three matter most. This means considering what impact completing those will achieve (so, important not just urgent). You commit before you start your day to the idea that, if they are all you get done today, it has been a success. It’s surprising how much this helps, especially for a natural self-critic like me. There are more "win days."

A weekly review

Weekly reviews are another habit that was driven by that planner, which for me is completed every Sunday. Taking time to review wins and distractions over the last seven days, as well as what I could do differently. The review also prompts you to think about all aspects of your life.

Since those years investing in the Full Focus Planner, I found it to be too expensive a subscription for the benefit. At present, I’ve replaced it with the Lux Productivity Planner (which covers six rather than three months) and am seeing the same benefits. You’ll note I’m sure that I’ve stayed with a paper-based planner. I encourage you to think about the benefit of doing the same. Not relying on solely digital systems can help you in a number of ways. For me it helps me step back and recall better.

Establishing routines that serve you

Finally, one other habit that I have learned along this journey is the importance of establishing a morning routine and an evening routine. This will differ for everyone but should include those things you want to do consistently (so need to make into unconscious habits). Repetition and environment are your friends again here, and I encourage you to practice defining these and honing them to work for you.

Checking with others and then going into "the office" to start work

Over time, I’ve also developed both "start of work" and "end of work" routines. These can help include aspects like managing your email, social media content, reminders/tasks and finance/CRM systems. They also help to act as behavioral bookends to my working day, making it easier for me to relax afterward.

3. Your whole self matters

It is easy to fall into the trap of only thinking about your mental activity as if you are a robot. But too much self-neglect has taught me that it is so important to think more holistically. If you are going to be sustainably productive, even in the medium term, you need to look after yourself.

Others are more qualified to talk on each of these topics than I am, but my own mistakes have taught me to take care of all these aspects:

My physical self (exercise, diet and hydration)

My emotional self (celebrate wins, interact with others, open up)

My spiritual self (take time to reflect on meaning in what I do)

My social self (keep in touch with others and not just by email)

Taking care of physical you

The first of these, taking care of your body, can also be helped by a few simple changes to how you work. Sadly, my morning routine does not now include sociable badminton, but for me still means running and yoga at home. I’ve shared before on some apps that help me.

In your home office, also beware of becoming so absorbed that you don’t notice how long you are sitting. It really is bad for your body and energy-sapping. I’ve shared before how much a standing desk helped mem and I’m still benefiting from that investment two years later. I also use my Apple Watch to prompt me to stand at least every hour (normally a prompt to leave my office to get a drink and chat with my wife).

So, I encourage you to watch out for becoming too sedentary. Of course, we should also turn to diet. Now, I would be a hypocrite if I tried to preach to others about diet – after all, I’m a middle-aged man who enjoys food and drink, which shows. But, suffice to say that I have discovered that more vegetarian meals do improve my energy levels.

The main lesson I’m learning is about hydration. So, my final tip for looking after the physical you is to always have a water bottle on your desk. If you feel hungry (a big potential bad habit when working at home), try drinking water, instead. If you feel tired, before you have yet another coffee try drinking water. Drinking water is really helping me as it becomes a habit.

That’s enough for now. In my following posts, I will share more on looking after the emotional, spiritual and social you. I’ll also share posts on recommended hardware, software and other equipment to help you be more productive at home.

Keep safe, and please keep in touch.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Paul Laughlin is the founder of Laughlin Consultancy, which helps companies generate sustainable value from their customer insight. This includes growing their bottom line, improving customer retention and demonstrating to regulators that they treat customers fairly.

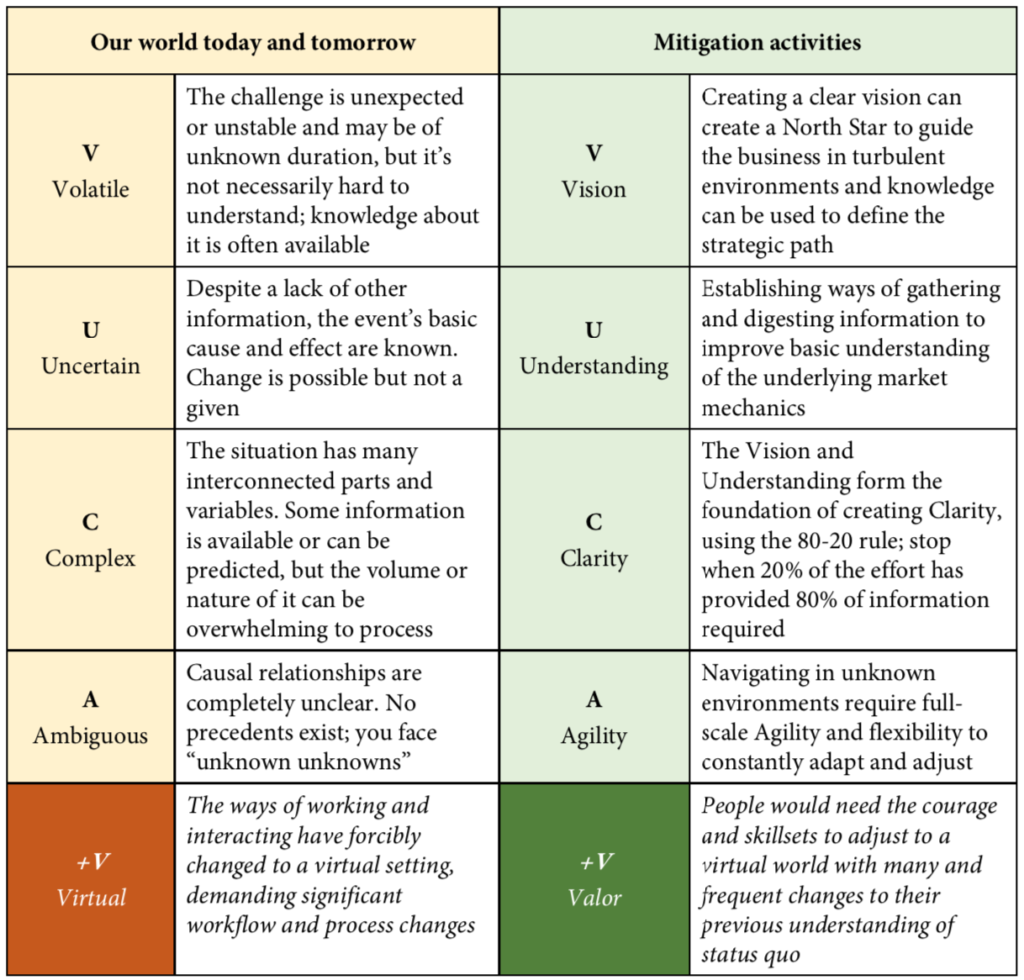

The term VUCA (volatile, uncertain, complex, ambiguous) was coined by the U.S. military as a reaction to an increasingly complex situation, with many frontiers and unknowns around the world.

For business, the pandemic crisis has taken the VUCA elements of the corporate environments to a whole new level and even suggests adding a V, for "virtual," as the world has gone virtual in literally weeks.

Introducing VUCA+V:

Source: Own development based on HBR (January-February 2014)

Successfully navigating the current VUCA+V environment, and preparing for the new normal bound to follow the end of the pandemic, require insurers to develop a wide range of new skill sets and rethink their operating models that up to now have been based on cumbersome processes, manual workflows and significant paperwork.

“It worked yesterday” does not mean it works today – or tomorrow.

Staying home, doing business, have forced us all to go digital. This has developed our virtual meeting skills, our online shopping savviness and our ability to handle our daily tasks and administration work online – we’re looking at a seismic shift of everyone’s readiness for digital products, services and ways of doing business.

The virtualization of the way we live, work, shop and interact directly affects the future demand for products and services, and people skills and competencies – we will see jobs, products and competencies becoming obsolete as the virtual ways no longer require them. As a result, companies and people will need to redefine who they are and what they offer.

The pandemic and lockdown have almost completely changed the playing field all over the world – and this means the players have to adapt if they want to stand a chance to win in the future game.

In a world they haven’t seen before, insurers must do what they haven’t done before if they want to stand a chance to succeed.

The world’s virtual habits have changed profoundly, so insurers must adapt to serving customers virtually. Now and post the pandemic.

The virtual insurer’s toolbox

Successfully competing in a new VUCA+V world requires insurers to develop a new set of tools and methods and apply them swiftly and thoroughly. Here’s a brief overview of some of the most essential:

Strategic savviness (Vision)

Artificial intelligence (Understanding and Clarity)

Organizational agility (Agility and Virtual)

Strategic savviness — Vision reduces volatility

Navigating through troubled waters requires a firm leadership team, constantly focusing on the company’s North Star – the strategic direction and goal. For a North Star to be effective, it must be specific, and reaching it must be realistic. It makes little sense to have a North Star set on conquering new markets if the insurer is struggling in the current one. The North Star therefore changes over time as the insurer progresses. The key to a successful use of this concept is to make sure everyone in the company is aware of the direction and believes in it.

Scenario-based ability to analyze and forecast market developments under various circumstances is another key element in creating a sustainable company, as this enables the insurer to prepare for the various outcomes and act swiftly when required.

Swift reaction requires a fast response mechanism, an "if this happens, then we do..." preparedness.

Deployment of artificial intelligence — Understanding and Clarity help navigate through Uncertainty and Complexity

Predictions of trigger events identified during the strategic scenario planning can be done by using artificial intelligence to constantly gather information and analyze the market developments, thereby enabling the insurer to act faster and with greater confidence.

To extend the insurer's ability to predict market changes, artificial intelligence can be expanded to create an early warning system (EWS), analyzing key financials from the insurer and comparing the trend in these with the trends found in the market.

A simple example could be monitoring the development of claims costs for car repairs and comparing this with macro-economic parameters (import index, exchange rates, etc.) to predict changes in, for example, spare parts prices and then cascade this down to expected development in claims costs and further into the underwriting models.

Advanced analytics will therefore be able to suggest corrective actions to keep the insurer solvent and on the right track earlier, as the AI will analyze large datasets constantly at a pace humans cannot keep up with.

This information could be directly used in advanced underwriting models that, if automated, would provide customers with immediate quotes and improve the customer experience and deliver on the here-and-now expectations in the new normal.

Organizational Agility — Agility and Valor improve adaptability to Ambiguous environments in a Virtual setting

It is imperative for insurers to keep agile and flexible not only during the pandemic but also after, as several aftershocks in the markets can be expected – we’re in a recession, and it will take time before the markets stabilize, if they ever do.

One thing is clear; once the markets have returned to a more stable state, we will be facing a new normal that everyone has to adapt and adjust to.

The two most significant factors that cripple insurers’ flexibility and ability to adjust quickly to internal and external events are fixed costs and workforce rigidity, with a certain amount of interdependence between these.

It is difficult to keep profitable in a market with very fluctuating demand and price indexes – to do so, the insurer must at a minimum be able to adjust the cost base to reflect the changes, and to do so immediately. It is of little help if it takes several quarters to adjust the cost base to changes that happen overnight.

The insurers therefore have to relook at fixed costs like rent and other long-term commitments, once being the permanent staff. It is advisable that the insurer offshores as much back office and operations as possible to enable faster adjustments to the cost base – this may come at an initial cost premium, but this will be more than offset by the increased ability to adjust expenses to market developments.

Incumbent insurers are organized in silos with a high degree of independence and little direct interaction. This provides a stable organization that works like a well-oiled machine in stable times.

However, the machine is rigid and not very ready for the process changes required to keep up with constant market fluctuations, and changes will not be carried out fast. This must change if the insurers are to stand a chance to survive – and thrive – in the new normal.

It goes without saying that the future insurer must digitize all processes and ways of working and become truly virtual. It’s not enough just to "add electricity" to existing processes, as this will just digitize the old – the insurers must redesign and digitize all processes to accommodate the demands for agility and flexibility.

Supporting – or enabling – the organizational changes must be done by a new way of thinking about technology – insurers cannot get rid of their aging legacy systems overnight, so it is necessary to explore ways of working with "two-speed" IT, building a flexible layer on top of the legacy systems.

This will provide the insurers with the needed agility to adjust processes and customer- facing applications at the speed needed to keep up with the changes in consumer behavior and expectations.

Implementing changes at the scale discussed here can almost be likened to establishing a brand-new insurer – it’s not a little task and must be carried out wholeheartedly and with absolute full and unanimous support from the entire management.

Initiatives like these – that are required – are board-level material, as they will require investments and many unpopular decisions to work. It usually takes a crisis before changes of this magnitude are approved and can be done.

Now is the time.

Stay safe and good luck.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

In 1970, economist Milton Friedman published an idea that has driven capitalism for the last half-century: The only responsibility of a corporation is to generate profits for shareholders.

That sole focus has produced distortions that have made many, including senior executives, increasingly uncomfortable and has led to an alternative formulation known as "stakeholder capitalism." The new formulation tries to deliver for customers, employees, suppliers and communities, as well as shareholders. A recent survey of Fortune 500 CEOs finds that stakeholder capitalism has gained major momentum, and I heartily recommend that the insurance industry lean into the concept both during the pandemic--when so many stakeholders are desperate for help--and beyond.

The Business Roundtable ratified the movement with a Statement on the Purpose of a Corporation last August that was signed by 181 CEOs. (Progressive Corp. CEO Tricia Griffith was listed prominently among the signatories.) This week, Fortune magazine reports that a survey of Fortune 500 CEOs found that only 4% disagreed with the new emphasis on stakeholders, vs. just shareholders, and that almost half felt that the pandemic will accelerate the move to stakeholder capitalism. (18% said the pandemic would slow the move.)

Alan Murray, president and CEO at Fortune, wrote: "The current pandemic is likely to widen the rifts that have plagued Western society in recent years—between knowledge workers and manual workers, the well-educated and the less-well-educated, top tier cities and the rest. Businesses will need to play a bigger role in healing those rifts, or risk losing their operating licenses."

While Friedman's dictum helped break up the old boys networks that let many weak CEOs hang on as long as they looked the part and didn't ruffle feathers, the discipline inherent in his prescription dissipated for, it seems to me, two main reasons.

First is stock options. They should be the right way to encourage senior executives to focus on benefiting shareholders: Deliver a higher stock price and reap huge rewards. But options have devolved into a "heads I win, tails I win" situation for CEOs. If the stock climbs, senior executives win. But even if the stock drops, boards often find ways to issue another slug of options at a lower price in the name of retaining talent.

Besides, it's become clear that stock options can drive short-term thinking that actually harms a company. How hard is it to cut costs to make sure you hit your number for the quarter--and leave it to the next guy to cover for the R&D that didn't happen?

It's also become clear that, while some CEOs make a huge difference, much of what happens to the stock price is out of the senior team's control. You can be the greatest oil company CEO in the world at the moment, and you're still getting hammered. How can anyone make money when prices have sometimes dipped into negative territory, meaning you're having to pay customers to take your product off your hands? But try to do badly these days as the head of a grocery chain.

A massive research project by McKinsey found that 55% of a company's performance is out of its control in anything like the short term--that 55% stems from a company's "endowment" (its size, debt load and historical R&D) and from the trends in its industry and the geographies where it operates. Even the 45% that can be influenced likely doesn't deliver sustained results for years. So, lots of the variation in year-over-year results that drives bonuses is noise, not a reflection of long-term success.

The second cause of distortion is compensation consultants. Again, the practice was instituted with the best of intentions. Companies would figure out what others were paying senior executives, then decide roughly where an executive fit among his or her peers and arrive at a fair compensation package. But what are the odds that a compensation consultant would rank the CEO in the bottom quartile? Don't you fire someone ranked that low? What are the odds that a CEO would even find himself or herself in the quartile second from the bottom? Yes, the consultant reports to the board, but everyone still wants to make nice with the CEO. So, as in Lake Wobegon, all the CEOs are above average. That means they deserve to be paid more than the average, which raises the average, which means the CEO deserves more, which raises the average--and on and on until we get to today's wild disparities between CEOs and front-line workers.

Stakeholder capitalism will, of course, have its own problems. While everyone seems to be laser-focused these days on the customer and while suppliers will likely be treated fine (they have leverage and can go elsewhere if not treated well), companies will have more trouble seeing communities and, yes, employees as true stakeholders.

Employees would seem to absolutely be stakeholders. Every presentation I used to see as a reporter at the Wall Street Journal would include a slide (often, it was the first slide) claiming that the company had the best people and talking about them as the competitive advantage. But employees are a cost, a huge cost, and every fiber in an executive's being wants to cut costs. So, employees, as a group at least, are paid as little as the company can get away with. Yes, every company needs to be competitive, but competition among businesses tends to drive toward lower costs, not toward higher pay and benefits.

Communities will also be tough. Every company should want to be a good citizen in the communities where it operates, and most try hard to be, but there are limits to what's possible. Companies need to have the flexibility to move resources around quickly, even though the communities that lose the people or the facility may be hurt. And how much compassion could, say, Kodak, show to its longtime headquarters of Rochester, NY, while in the throes of bankruptcy? Communities will often be an afterthought.

But the efforts toward stakeholder capitalism seem to me to be an important attempt to fix the distortions that have developed during the past half-century, especially during the pandemic and especially for the insurance industry.

In the pandemic, people are in a world of hurt, and they're going to remember the companies that treated them well. Just look at the disdain that people still have for the financial services executives who paid themselves big bonuses during the Great Recession, more than a decade ago, while laying off tens of thousands of employees and letting customers' mortgages foreclose. I said that every grocery chain CEO is killing it these days, but... the CEO of Kroger is catching all kinds of heat for preparing to let a "hero bonus" of $2 an hour expire for in-store workers while being in line to collect millions of dollars by hitting profit goals. The long-term benefits of caring for customers, employers, suppliers and communities, as well as shareholders, could be the legacy of this devastating stretch.

The need for insurers to care for all stakeholders seems especially strong, because that's the ethos for the whole industry. We can either define ourselves as truly focused on wellbeing, or we can be seen as merely offering lip service.

After saying as much six weeks ago, in talking about the moral imperative for the industry, and then warning two weeks ago that the industry might be losing the PR battle, I'm happy to say that the opportunity seems to still be wide open to lean into the stakeholder capitalism concept. Insurers, like Progressive, can even claim a leadership role. I hope we will.

Stay safe.

P.S. Here is an article that talks about some specific topics that we all should be addressing now, to use our short-term efforts on the pandemic to set us up for long-term success; the insurance industry could play a major role. I'm more than a bit biased--the article is written by my longtime colleague Chunka Mui, based on some work he and I have been doing together for the past few years, and I even get name-checked in there a couple of times--but I commend it to your attention. It's very smart.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

The COVID-19 pandemic has created not just a healthcare crisis but also a global recession, and a complete solution, including robust healthcare measures such as easily available testing, will take time to develop. So, insurers need to focus on both a short-term approach, where most employees remain physically isolated and work remotely, and on a longer-term approach, where there is considerable ambiguity on the scope and timing of an economic recovery.

Every insurer needs to urgently examine current business and IT processes carefully and modify these in a secure manner to adjust to this "new normal."

Internal Culture Remains a Priority

Irrespective of the fact that the end or near abolition of physical proximity will require new modes of work, one thing doesn’t change—the importance of providing protection to customers in a cost-effective, efficient and humane way. Everything else must flow around this cornerstone.

Every insurer, as part of its culture, needs to have already addressed these foundational aspects:

Focus on ensuring the health of employees, contractors and associates.

Define and implement operational business and IT preparedness.

Prepare and roll out service continuity and mitigation plans.

Execute a corporate messaging strategy.

Coping With Uncertainty

There are no historical parallels to the COVID-19 pandemic—the closest approximations are the 1918 flu pandemic, the 1930s Great Depression and the 2008 Great Recession; however, they are only indicative—not equivalent.

We cannot predict with great accuracy the nature of either the slowdown or how the global economy will recover, so we must rely on flexibility and speed.

For example, while many respected analysts feel that specific lines of business such as auto insurance or commercial property insurance will recover quickly, a prolonged slowdown might lead many customers to renew with bare bones coverage, cutting premiums.

On the other hand, you have many U.S. states considering legislation to "retrofit" COVID-19 coverage into business interruption insurance, especially for small business owners in the hospitality industry.

Another uncertainty: How are continued social distancing demands going to impact the high-touch nature of high-value life insurance sales and underwriting?

The possible scenarios across various lines of business are too vast to even attempt to list here. The variety emphasizes that speed and flexibility are vital for insurers. Every insurance company will have to focus on being as digital as possible.

A clear understanding of the business value and ownership of data is a vital prerequisite for implementing a digital strategy. This understanding must extend not only to data that is created within the enterprise or via business partners but may also involve data that was typically under the purview of telecom providers and national governments—combined in what we can choose to call an "information mesh."

While every government will have differing notions of data privacy, an insurer will need to build a data infrastructure to reliably share appropriate information with the government in an efficient, unobtrusive manner. Witness the reality that the best COVID-19 pandemic control program in the world, Taiwan’s, was based on combining the national health insurance database with cell phone tracking data, etc.

While building such an information mesh, insurers will need to leverage technologies such as digital, cloud and automation in an agile manner—they should not lose sight of the fact that at its root this is all about people owning data and people deciding how to use it in a secure and efficient way.

Data and Technology Enablers

Data needs to be trusted to be consumed effectively by internal and external users across the banking, financial services and insurance enterprise, and data governance is the means to this end. The conventional data governance paradigm of managing data as an asset is failing due to the plethora of architectural data patterns. Instead, we recommend that data governance must embrace alternative paradigms. These paradigms can include a hub and spoke for gateways to trusted data or potable data, like a utility providing potable water, irrespective of the water source.

Architectural data patterns can include data lakes, data warehouses or marts, on-premise legacy systems, data in a public, hybrid or private cloud, streaming data, third-party data from commercial aggregators and public sources, click stream data, IoT data and much more.

The scale and complexity of data governance presupposes that human intelligence, collaboration and judgment be helped by advanced analytics, pattern matching and AI and ML techniques in the long run to achieve these ambitious goals.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Venugopal Shivram (Shiv) is a domain lead in the Technology Advisory Group within TCS' banking, financial services and insurance business unit. He has over 30 years of global experience in insurance and banking, focusing on consulting in analytics and big data.

With the official start of the 2020 Atlantic hurricane season just one month away, there has likely never been a more important one for the insurance industry. This is not just because most of the early-season guidance points to an above-average hurricane season, which could increase the chances of hurricane landfall along the U.S. coastline; but, because of COVID-19, if a hurricane makes landfall it comes with increasing pressures for the people affected and the stress on the insurance industry. With insurers already strained due to COVID-19, additional losses from a named storm could disrupt the industry.

By their very nature, hurricanes force people to gather close together in shelters and travel away from their places of residency during evacuations. This goes directly against what the Centers for Disease Control and Prevention (CDC) recommend for countering a Covid-19 outbreak. Think about when Hurricane Katrina hit New Orleans in 2005: Around 20,000 people took refuge in the Superdome. One building with 20,000 people can’t happen in the current environment. Additionally, we have all read that the elderly population is more susceptible to COVID-19 and that the CDC guidelines should be strictly followed for this demographic, but the elderly are even more at risk during a hurricane because COVID-19 complicates evacuation procedures that are already difficult for them.

COVID-19 is already placing unprecedented strain on disaster management, health and other systems; a hurricane will exacerbate that strain. With outbreaks across the entire nation, an area hit by a hurricane is less likely to get aid from other states or regions. Will power crews travel hundreds of miles to help restore power? The lack of quick response can further create problems with mold growth if the power is not restored fast enough. After a storm, sometimes as many as 10,000 volunteers come from all over to help with the recovery, but it might be hard finding volunteers amid the pandemic. How about claims adjusters and another insurance personal that need to inspect property damage? How about contractors getting into an area to put tarps on roofs and prevent further damage? The list is almost endless of how uncertainty increases.

This is why all eyes will be on any little disturbance that develops anywhere in the Atlantic Ocean this season.

Atlantic Hurricane Forecasts Are a Dime a Dozen

Do you know there are at least 26 different entities that forecast various aspects of the Atlantic hurricane season? You can track the majority of the early season predictions here: http://seasonalhurricanepredictions.org.

In meteorology forecasting class, one of the lessons that is taught is that the consensus forecast is a hard forecast to beat. Although early April hurricane season forecasts for activity have the least amount of overall reliability, when you get a great number of forecasts that agree that the overall activity will be above normal it should get the attention of the insurance industry.

All the forecasts speculate on the same general climate factors that are leading indicators to an active hurricane season. One is the El Niño-Southern Oscillation (ENSO). Currently, the majority of the global ENSO forecast models call for ENSO-neutral conditions during the peak of the Atlantic hurricane season for August-October. When ENSO is warmer than normal, it is called El Niño, and it typically reduces Atlantic hurricane activity via increased upper-level westerly winds in the Caribbean extending into the tropical Atlantic that shear apart storms as they are trying to form. This is not forecast to occur this year. There is some indication that late in the summer months a La Niña might develop, which would bring even less wind shear to the Caribbean and might lead to above normal activity. From 1995-2019, the non-El Niño seasonal mean Accumulated Cyclone Energy (ACE) index across the Atlantic Basin is 160 (104 is the 1981-2010 average), with those non-El Niño years having an average of 16 named storms, eight hurricanes and four major hurricanes across the basin. So this is a good place to start if one wants to make the argument for more favorable activity across the Atlantic basin.

Currently, the Pacific remains in a warm-neutral state following a weak Modoki El Niño event in early 2019. Indications are showing cooling waters below the surface and conducive low-level winds at the surface, suggesting a La Niña event will slowly take shape over the next 3-5 months. This favors a busy season, particularly from September onward.

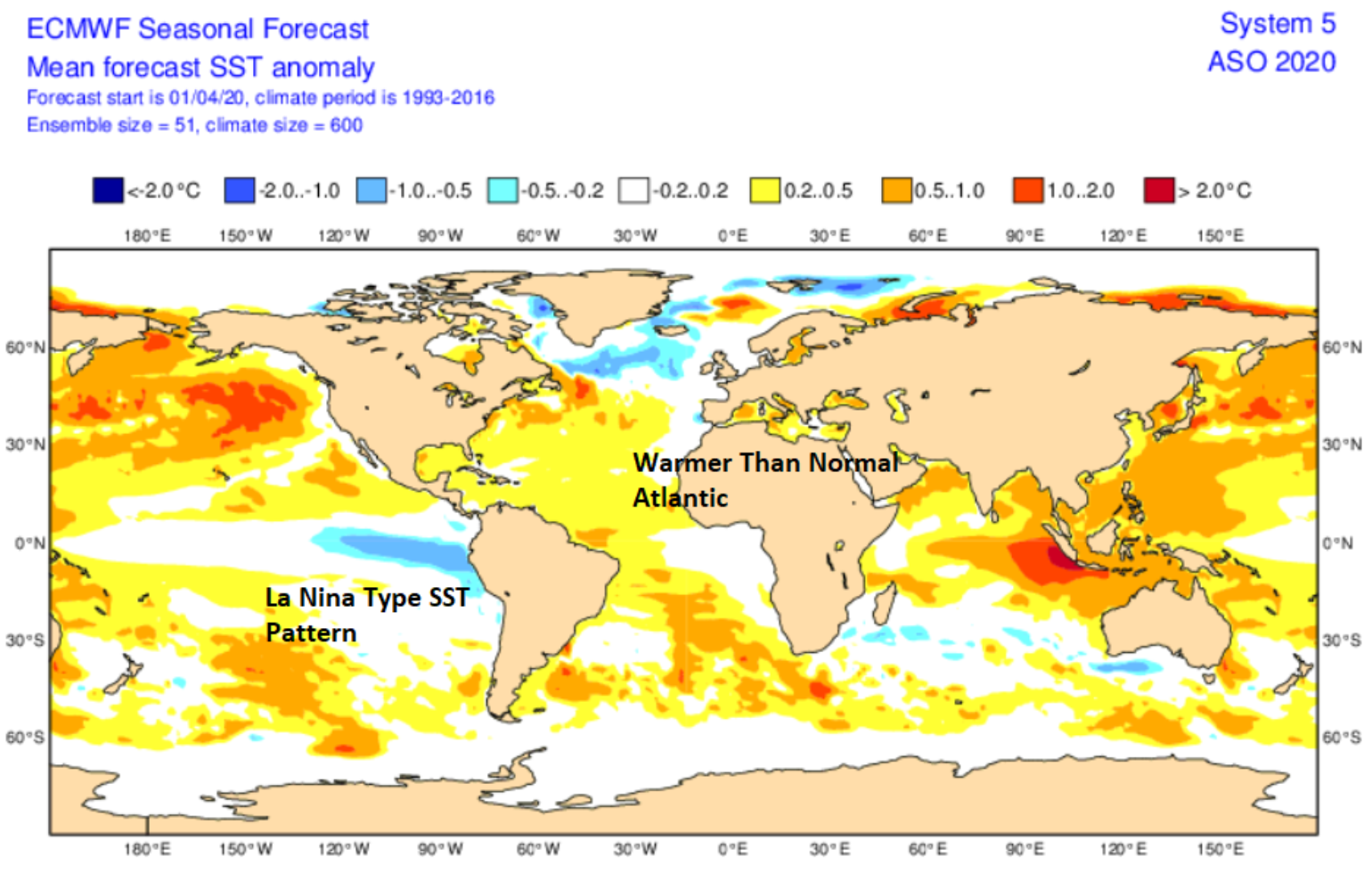

The other major climate forcer leading to an above-normal forecast is the Atlantic Sea Surface Temperature (SST), which is unusually warm at this time. This early-season warmth in the Main Development Region (MDR) has a strong relationship to an active hurricane season as a catalyst to tropical waves that move off Africa.

Historically, warmer than normal sea surface temperatures in the eastern Atlantic correlate with more active Atlantic #hurricane season. Currently, most of the eastern Atlantic is warmer than normal, except for north of 45°N. pic.twitter.com/SAkM5DX7VS

While these warm SSTs could change before the summer, the fact that the air temperatures over the area will only get warmer will likely limit any cooling of the current SST. Together with the increased probability of La Niña, the Atlantic SST signals elevated chances of a busy Atlantic hurricane season.

Much of the Atlantic's waters are already warmer than average as of the end of April. The fact that the SST is already this warm and forecasted to stay above normal suggest a more active than normal named storm season. Above is the ECMWF August September October SST anomaly forecast.

If you haven’t noticed, there has been plenty of severe weather in the Southeast U.S. over the last month or so. Part of the blame of these severe weather outbreaks can also be put on the warmer than normal SST in the Gulf of Mexico feeding moisture into the Southeast as mid-latitude low-pressure systems pull moisture up from the Gulf of Mexico, where water temperatures are one to three degrees above normal. There is no relationship between April Gulf SST and annual hurricane activity, mainly because Gulf of Mexico conditions can change quickly over a given season with weather pattern shifts. However, if such anomalies persist into July, the temperature could be deeply unsettling.

A wildcard to the season could be how much dry air rolls off the coast of Africa with tropical waves. There have been seasons where all the major climate forcers looked to align, but named storms need the precise set of ingredients to come together to make for a super active year, and dry air can be a wildcard; too much dry air aloft can inhibit named storm development.

Landfall Analogs

Many of the seasonal hurricane forecasts shy away from the most important factor for the insurance industry, which is overall landfall activity. After all, the Atlantic basin can be very active, but if no hurricanes make landfall the impact on the insurance industry is irrelevant. By looking at current oceanic and atmospheric conditions that are similar to conditions now and that might be expected during the peak of the hurricane season, analog years can provide useful clues as to what type of landfall activity might occur for the 2020 Atlantic Hurricane season. The years that seem to be most common are 1960, 1995, 1998, 2007, 2010 and 2013.

The analog years suggest a clustering of a pattern that would point to named storm activity along the central Gulf Coast and the Outer Banks. There is also a cluster of activity north of Puerto Rico and in the western Caribbean. In general, the analogs point to years with named storm landfall activity, so landfalling named storms should be expected from Texas to Maine, with the most focus on the regions mentioned above.

By now, the insurance industry understands that often tropical named storm activity comes in waves, which is largely a result of the passage of the Madden–Julian Oscillation (MJO) or large scale Convectively Coupled Kelvin Wave (CCKW). As we approach the start of the Atlantic hurricane season, the insurance industry can start to get a sense of when the Atlantic basin might experience some activity. The latest forecast guidance suggests that the first such wave of activity might occur around May 11, with another coming shortly after the start of the Atlantic Hurricane season. Given that the last five hurricane seasons have produced at least one named storm before June 1, it wouldn't surprise me if this year tried to follow suit given the warm SST in the Gulf of Mexico. Often, early season development occurs with storm activity off the Carolina coastline. These types of early systems tend to meander or make landfall along the North Carolina to northeast Florida coastline. But another area ripe for early season activity this year could be in the Gulf of Mexico.

Summary

The season looks to be active with a higher probability of named storm landfalls along the Gulf Coast or Outer Banks, NC, raising many questions about the possible effects on the insurance industry.

As the BMS Property Practice pointed out, if there is a heightened risk along the U.S. coastline would the authorities even allow non-permanent residents into the area to reach a second home if their primary residence is out of state?

Who is going to take steps to limit damage? How will storm response hamper recovery efforts in terms of volunteers or field adjusters? If hotels are not operating, where do people go, where do adjusters stay?

Maybe this is the year that insurtech solutions help the insurance industry respond to a natural disaster in new ways. No matter how you look at it, we are entering uncharted territory this hurricane season.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Andrew Siffert is vice president and senior meteorologist within BMS Re U.S. catastrophe analytics team. He works closely with clients to help them manage their weather-related risks through catastrophe response, catastrophe modeling, product development and scientific research and education.

The outbreak of the novel coronavirus (COVID-19) and the shelter-in-place response has wounded the US economy. Business and consumer-oriented economic indicators show the extent of the damage thus far, but economic data released in spring/summer months are likely to demonstrate further deterioration. The P&C insurance industry has not been immune to the economic fallout. The downturn is likely to strain underwriting profits, and the decline in interest rates and financial markets will undoubtedly impact net investment yields, which will exacerbate the industry-wide profitability efforts. The P&C insurance industry should expect differing impacts dependent on the insurance line. The line by line policy and loss impacts are studied within this article. Going forward, it is anticipated the pandemic response and economic downturn may expedite technological change and adoption, as industry players seek to maximize operational efficiency in a new world.

The Economic Downturn

The emergence of the pandemic has wreaked havoc on consumer activity, business activity and governments. Declines in manufacturing, residential housing, trade, business formation, and retail/food sales have all shown up in April’s economic indicators. These numbers are likely to worsen with May releases.

Figure 1:

Economic Indicators released in April indicated a sharp decline in residential and business activity.

The decline in residential and business activity underscored by worsening economic indicators (shown above) forced businesses to reevaluate their operations. Many have cut costs, including staff. This process has resulted in an unprecedented spike in unemployment claims.

Figure 2:

Unemployment claims spiked in April 2020

The recent spike in unemployment is extremely alarming, and despite efforts by government and the Federal Reserve to provide temporary backstops, the impact is already showing up in lower frequency economic indicators, such as Gross Domestic Product (GDP). In the first quarter of 2020, GDP was estimated to have declined by 4.8%. Interestingly, a significant piece of this decline was a contraction in healthcare. The “flattening of the curve” was a mantra aimed at ensuring protection of the healthcare industry during the global pandemic, but an associated decline in elective procedures has resulted in significant losses for many hospitals.

Figure 3:

While the GDP decline was worse than initial estimates and undoubtedly indicates the start of a severe recession, it came in below the measure hit in Q4 2008 when GDP declined 8.4%. It is expected that the 2020 downturn will worsen significantly when 2nd quarter GDP is released in the summer. Some are estimating a 40% fall in GDP in Q2, hinting at an economic depression. Hopefully, that will be avoided.

Impact on the Overall P&C Insurance Industry

The P&C insurance industry is not insulated from the economic fallout. The impact on business activity is expected to be felt in commercial lines and the effects on residential activity and general consumer activity are expected to show up in personal lines. The effects are expected to impact the P&C combined ratio through changes to premiums, losses and expenses.

A combined ratio above 100 indicates the industry is paying out more money in claims then it is making from policies. Due to effects on policies and losses the industry should expect an increase in the combined ratio. Adding to industry stress, net investment yields are likely to decline as well. The industry typically invests very conservatively, so interest rates are a good measure to track as a proxy. Recently the Federal Reserve responded to the emerging economic crisis by expanding the money supply and reducing the federal funds’ interest rate to near zero (again). The decline in P&C investment yields related to lower interest rates will constrain P&C insurance profitability further. The duration of ZIRP (zero-interest rate policy) will specifically impact areas of insurance with longer time horizons.

Figure 4:

The industry-wide P&C combined ratio is expected to increase while interest rates (and investment yields) fall.

Which Areas (in P&C Insurance) are Expected to Be Most Severely Impacted?

While the magnitude of the impact on the P&C insurance industry combined ratio remains to be seen, the economic decline associated with sheltering in place from COVID-19 is bound to weigh on P&C insurance. There will undoubtedly be changes in the demand for insurance and the new environment will lead to alterations in insurance claims and losses. Down the road, this may also lead to changes in regulation and could even generate new business models.

Given the nature of the pandemic, it is challenging to predict all implications for insurance. A recent survey from PwC, for example, explored some potential areas of concern with finance leaders related to COVID-19 and found the following concerns rose to the top.

Figure 5:

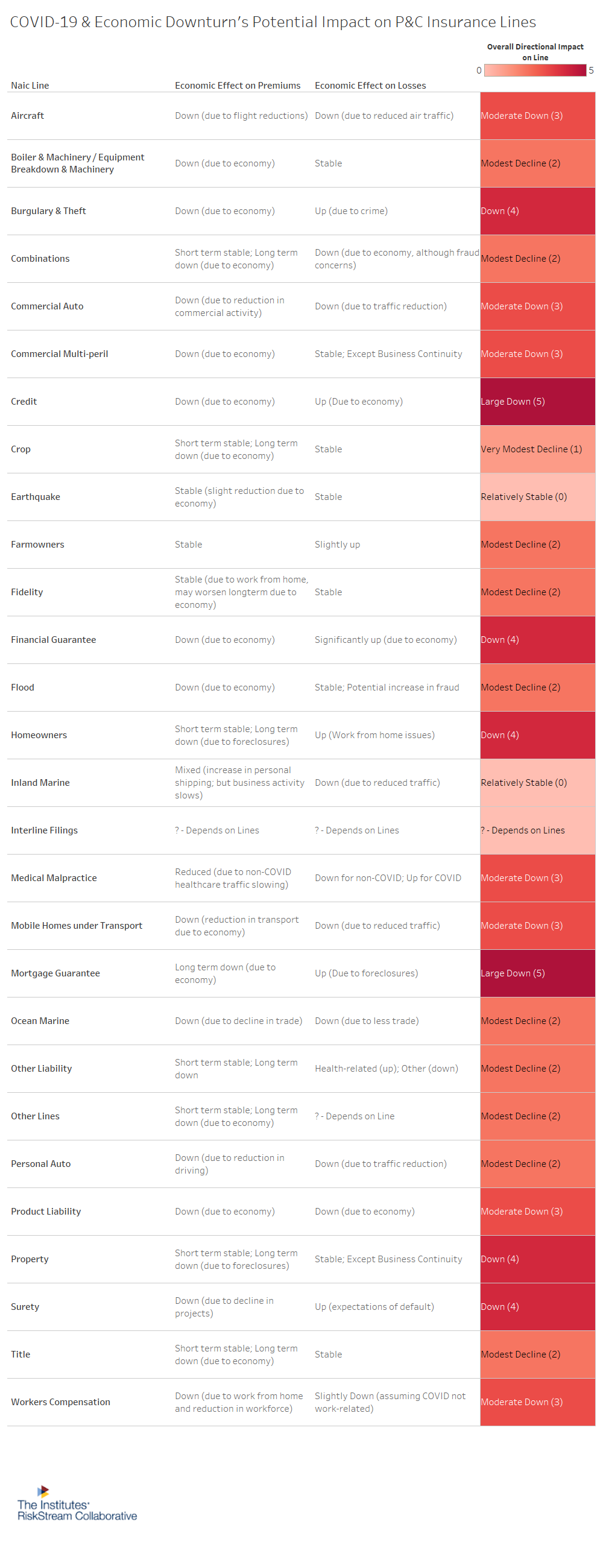

These themes are also relevant for leadership within the P&C insurance sector. The entire insurance value chain — from policies, pricing and distribution; to underwriting and risk management; to claims and servicing; to finance, payments and accounting — will be impacted in some manner. The industry will have to navigate operational pressures as more employees work-from-home, while simultaneously finding ways to optimize profit as general business activity pulls back and the economy contracts. If premiums decline or losses spike, insurers will need to find ways to cut costs. Yet, each line of insurance will experience policy and loss effects differently. Figure 6 analyzes the directional impact to each line of P&C insurance.

Figure 6:

Premiums are likely to contract across a variety of lines of insurance as the economy weighs on new exposures and causes early policy cancellations. General auto and air traffic will decline as more people stay home. The uptick in unemployment (shown in Figure 2) will undoubtedly show up in reduced premiums for personal auto, aircraft and commercial auto. The reduction in in workforce along with movement to new work-from-home environment may also result in businesses cutting workers compensation policies. COVID-19 and associated isolation policies impacted global trade (Figure 1) and business projects, which will reduce policies for various lines like ocean marine and surety. Areas related to housing, like homeowners or mortgage guarantee, may have some short-term stability, but long-term risk as foreclosures spike. Cost cutting, particularly within small business, is expected to constrain property premiums as many businesses consolidate. Finally, medical malpractice may see a reduction in policies particularly if the non-COVID healthcare slowdown (shown in Figure 3) continues and more hospitals cut back on elective procedures and associated expenses.

As shown in Figure 6, claim losses are also expected to vary by line. Reduced business and personal activity is expected to lower losses in a variety of lines, including auto, airlines and ocean marine. Credit, mortgage guarantee and surety losses are expected to increase as the economic downturn causes capital challenges and project cessations. Homeowners may see a slight uptick in losses as more residential activity takes place at home, due to school cancellations and work-from-home policies, thereby increasing risk.

Business interruption coverage, which can be included in property coverage (for example), is an area of question. This coverage indemnifies companies for lost profits for nonexcluded risks, yet outbreaks of disease are generally excluded. Certain policies include coverage for “interruption by communicable disease.” Even with this language included, some policies still exclude contamination due to a pathogenic organism, bacteria, virus or disease. There are a lot of elements to consider with this issue. Therefore, it is likely there will be challenges and litigation related to business interruption.

Why the Pandemic May Be a Catalyst for Tech-Adoption in Insurance

The P&C insurance industry was thrust into a new business environment due to the global pandemic. Within a week a relatively manual industry, which relies heavily on face-to-face interaction, showed an impressive ability to adjust and leverage technology to continue to provide products and services. While some firms within the insurance industry had already made strides in tech-related innovation and automation prior to the pandemic, the industry as a whole has been somewhat reluctant to adopt emerging technologies. On the surface, it may seem unlikely that the efforts over the past few months may have lasting impacts and change tech-adoption rates within the industry. Digging deeper, the pandemic and the associated economic fallout may windup being the key catalyst for widespread tech-adoption within insurance.

Prior to the pandemic the stage for large-scale technological adoption within insurance was already set. While the economic downturn will lower the quantity of available start-ups and InsurTechs, the quality and adoption rates associated with InsurTech may increase. In addition, the count of internal projects for brokers, carriers and reinsurers leveraging new technologies has been rising over the past few years. Industry organizations had already understood the importance of innovation, yet had less reason to trigger production usage. Some forward-looking credit agencies understood the industry-wide hesitancy and have created scores for innovation. AM Best released its innovation score methodology in March, 2020. They explain that these company-specific innovation efforts (or lack thereof) are likely to have a long-term impact on an insurer’s financial strength. Put differently, in order to profit maximize, insurers need to innovate. In this new world, they need to do so now.

While innovation can include elements outside of technology, much of it is directly related to technology. A notable constraint to technological adoption within insurance has been lack of customer adoption. Telematics, for example, has been around for an extended period of time, but never experienced robust demand. It’s possible the pandemic could change this. In an environment where miles driven has collapsed and more customers are now unemployed, Telematics and Usage-Based-Insurance (UBI) may provide angles for auto insurers to maximize retention of policyholders. The cost-benefit for consumers to exchange private information for a reduced rate is likely to be changing as well.