The nature and scale of the risk of future pandemics far outstrips the insurance industry’s capabilities, so any public-private partnership must make the most of them.

COVID-19 has revealed the expansive landscape of pandemic risk. The federal government has already committed $2.2 trillion to fund pandemic relief programs for individuals, businesses and state and local governments, just for 2020. Congress is currently debating whether to commit an additional $1 billion or $3 billion, with an outcome probably somewhere in between.

Meanwhile, policymakers, commercial interests and the insurance industry have been working through how to prepare for the risk of another pandemic in the years ahead. While they may argue about how much capital the insurance industry should be asked to put at risk against future pandemics (ranging from $0 to $50 billion), even the most aggressive proposals would transfer only about 1% of foreseeable losses to insurers.

Further, those proposals would direct all of the insurance industry’s pandemic risk capacity to take on “business interruption” losses. For example, the Pandemic Risk Insurance Act would give large corporations the tools to make up for lost profits and reduced executive compensation during a pandemic. The proposed Business Continuity and Protection Program, as well as Chubb’s Pandemic Business Interruption Program, would provide benefits similar to those recently paid out under the Paycheck Protection Program.

Without a doubt, the insurance industry’s role is severely constrained compared with the enormous scale of the pandemic risk. Accordingly, policymakers must thoughtfully position insurance industry capabilities where they can have the greatest impact for those individuals, state and local governments and businesses suffering financial loss during a pandemic.

The Pandemic Risk Landscape is an effort to provide policymakers and other stakeholders with a practical tool to assist them to consider the optimal positioning of the insurance industry’s capabilities within a public-private partnership. Equipped with a view of the full scale and range of exposures to financial loss confronting families, governments and businesses, policymakers may continue to conclude business interruption is the single best target of insurance industry resources within a public-private partnership. Or, they may find at least some of those limited resources should be allocated to other stakeholders and other exposures to loss.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Jason Schupp is the founder and managing member of the Centers for Better Insurance. CBI is an independent organization making available unbiased analysis and insights about key regulatory issues facing the industry for use by insurance professionals, regulators and policymakers.

We’re about five years into the insurtech boom, but we’re also in the middle of a pandemic. Excitement around emerging technology and startup innovation has taken a backseat as the insurance industry shifted its focus to COVID-19.

Yet startups have not failed as quickly as the industry might have predicted. It’s possible that some startups will begin to outrun their funding and close their doors in the next year or two. But for the time being, the insurtech market and funding remain relatively stable. What’s driving this?

COVID-19 and Insurtech Partnerships

The pandemic has altered insurers’ approach to insurtech investment. Insurers appear to be focused on tactical initiatives that can produce more immediate results. This contrasts with the R&D that was more prominent pre-pandemic.

Yet it turns out that startup activity and the global pandemic are not necessarily mutually exclusive. Insurer priorities most notably changed focus to cloud computing and digital strategy — with digital covering both external channels and internal workflows. Cloud and digital are two areas in which almost every insurtech excels and have led to additional opportunities in many cases. Insurers expect that these areas will continue to be prioritized even when the pandemic is over.

Lemonade’s IPO and What It Means for Insurtech

Lemonade’s IPO cemented one of the most notable insurtech players as a certified unicorn. IPOs validate the potential returns of insurtech and will help attract more investment dollars into the space, whether from venture capitalists or insurer investment arms. Few other startups have gained the investment attention that Lemonade has, but others — like life insurance startup Ethos or property insurer Hippo — have received funding over $100 million. Each of these startups’ successes helps attract dollars for the rest of the insurtech ecosystem.

Many insurtechs, especially startup MGAs, are exploring new revenue streams. For some, this means selling a wider variety of coverages directly online or embedding at different points of sale. Some MGAS are also moving to become full-stack carriers, like Buckle and Clearcover. Still other startup carriers, like Slice, Trov and Metromile, have gotten into the software business and are licensing their platforms out to other insurers.

Platform and analytics players are also finding success proving value to insurers in the current environment. Atidot, for example, partnered with Pacific Life to analyze product and pricing changes to help optimize market penetration for the insurer. In addition, Principal is licensing Human API’s medical records platform to circumvent paramedical exams for disability insurance during the pandemic.

Many startups have interesting ideas but haven’t thought through long-term financial or regulatory hurdles. The goal of many startups is to validate a business model first, then work out the details later. It’s possible that some startups will start to outrun their funding and eventually close their doors. But it will be interesting to see how insurtech evolves in a post-pandemic world, especially as new realities cause insurers to rethink processes that were manually intensive. For startups that can show value to insurers, this new normal may be an opportunity.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Insurers must quickly figure out what the world of work and home life will look like after the universe resets so they can start preparing their businesses.

Although the insurance industry seems to have aggressively and (mostly) successfully shifted toward digital interactions during the pandemic, an even trickier transition lies just ahead as part of what is being called "the Great Reset."

That transition to a post-pandemic world requires insurers to not just understand the internal workings at their companies, or even the new preferences of that fickle beast known as the customer; it means figuring out what the world of work and home life will look like after the universe resets, so insurers can revise products and revisit sales and marketing tactics. Maybe, for instance, some insurers will want to deemphasize small businesses, in general, as long as so many may go out of business and migrate toward "ghost kitchens" (which only offer takeout or delivery).

To try to help as we all sort through the complexity, I've pulled together the smartest thinking I can find on what comes after "the Great Reset." (Warning: McKinsey provides some serious pessimism at the end of what follows.)

In this article, the consulting firm lays out the broad parameters of what comes next for the economics of home life, including these predictions:

"A 12% drop in private consumption is anticipated in the United States over the next two years, with recovery to pre-crisis levels only by 2023–24.... The explosion of small brands, underway before the pandemic, has given way to a strong preference for global A-brands. After years of growth, out-of-home consumption has almost disappeared; many of us have stopped going to stores entirely....

"Zoom’s daily user base grew from ten million people to 200 million in three months.... At the same time, there has been an enormous rise in unemployment, which is expected to reach approximately 15% when 2020’s third-quarter results for the U.S. are complete."

Those predictions, if true, suggest not only that insurers will face headwinds with consumers because of a diminished appetite for spending but could also adjust policies and marketing/sales tactics to account for changes in how people use their homes and cars.

Of course, consumer buying behavior spills over into the businesses that serve them. Target, for instance, recently said that while it will hire 130,000 temp workers for the holiday season, the same number as last year, a far greater percentage will support e-commerce. Target, whose e-commerce sales tripled in the second quarter, says twice as many workers as last year will be assigned to help customers with onsite pickup of online orders; Target says that 90% of its online orders are now picked up at stores.

Small businesses have much bigger issues than big box retailers like Target do. How big? A recent headline in Crain's New York Business said of small businesses, "60% See Survival Past Six Months." That means, of course, that 40% don't see survival past six months, yet Crain's described the outlook as "Less Apocalyptic."

A new federal rescue package could throw a lifeline to small businesses, but I wouldn't want to have bet on anything getting through Congress until after the election settles which party has the upper hand -- perhaps until after a new Congress is seated in January.

The mix of businesses that are thriving will surely change, too, at least until a vaccine begins to kick in next summer or fall (the time frame that currently seems most likely, though hardly assured) and old habits can begin to reemerge. Movie theaters will have a hard go of it. Inside dining will, too, though those "ghost kitchens" seem to be doing a good business with takeout. Anything associated with tourism will stay muted. Visits to doctors' offices will remain far less frequent, while telehealth continues to take off. Cushman & Wakefield projects that the vacancy rate for commercial office space will rise from 11% pre-crisis to nearly 16% in the second quarter of 2022 and won't return to pre-crisis levels until 2025. And so on -- all kinds of habits are changing, and new ones are getting plenty of time to take hold.

There will be a good deal of variation by country in terms of what new habits form. McKinsey reports, for instance, that, while 60% of consumers in Italy have shopped online during the crisis, only 10% enjoyed the experience -- suggesting that the switch isn't permanent (or that online stores need to improve a bunch). New behaviors will also depend greatly on the sector involved. McKinsey again: "While use of e-pharmacies... has doubled or tripled in the U.S. over the course of the crisis, only 40% to 60% of consumers express an intent to continue using those services."

A wild card for all businesses is that the pandemic seems to have thrown brand loyalty out the window. McKinsey finds "an astonishing 75% of U.S. consumers trying a new shopping behavior in response to economic pressures, store closings and changing priorities. This general change in behavior has also been reflected in a shattering of brand loyalties, with 36% of consumers trying a new product brand and 25% incorporating a new private-label brand. Of consumers who have tried different brands, 73% intend to continue to incorporate the new brands into their routine.... The beneficiaries of this shift include big, trusted brands, which are seeing 50% growth during the crisis."

While the change in brand loyalty seems to apply mostly to retail products, I suspect that "the Great Reset" is making customers more open to changing insurance carriers and agents, too. You can either see that as a threat to your customer base or as an opportunity to poach from others.

The bad news -- and I warned there'd be bad news -- is that McKinsey projects in this article that the prospects for the entire insurance industry are under pressure.

I know far too much about this work because I was the ghost writer for "Strategy Beyond the Hockey Stick," the book that three of the article's authors published in 2018. The simple version of their warning goes like this:

A massive amount of analysis that they've done on the profitability of companies and of industries found that the results fit on a power curve: If your company or industry falls in the second, third of fourth quintiles, your results are pretty much the same as all the others in those quintiles. But, if you fall in the top quintile, well, lucky you. Your results are far, far better than those in the middle quintiles. Unfortunately, there's a tail, too; if you're in the bottom quintile, your results are far worse. And the McKinsey research for this recent article found that the pandemic is making the rich richer and the poor poorer. So, those industries in the bottom quintile, like insurance, have even more of a mountain to climb than they did before.

The good news is that the changing landscape creates opportunities for smart insurers. Life insurers have clear opportunities because COVID-19 has raised awareness. The trend toward telehealth offers big opportunities for not only health insurers but for those involved in workers' comp. And "the Great Reset" opens the way for all sorts of insurers if they adapt quickly to how consumers and businesses will operate.

Stay safe.

Paul

P.S. Here are the six articles I'd like to highlight from the past week:

Carroll spent 17 years at the Wall Street Journal as an editor and reporter; he was nominated twice for the Pulitzer Prize. He later was a finalist for a National Magazine Award.

It has been a long time since I took chemistry as a pre-med student in college – yes I was pre-med before switching to a math and computer science major! I loved science, and I remember the experience. I can’t recall many of the formulas or compounds. But I remember the labs – especially the all-night ones. I remember mixing chemicals, and I remember the role of the catalyst. No matter what you had in the tube or the beaker, we always had to watch out when we added the catalyst. It was the game changer. It was the one that could set the classroom on fire. The catalyst took all of the primary chemicals and created a quicker reaction. Poof.

A catalyst accelerates a chemical process without itself being affected. If you think about it, COVID-19 has acted as a sort of digital demand catalyst.

In an earlier blog, we talked about reading the signs of what is to come in the life insurance industry, and we talked about connecting the dots. If we look at the trends closely, we can make out a picture of where the life insurance industry seems to be headed. Too much is changing not to notice. COVID-19 has added an extra variable – a catalyst – that has accelerated and pushed insurance to the point of reaction.

No test scenarios could have accomplished what COVID has accomplished in seven short months. In fact, Microsoft CEO Satya Nadella stated in April, “We’ve seen two years’ worth of digital transformation in two months.” COVID has compressed time frames for digital utilization as it has ignited a rush for digital capabilities. It is speeding up a demographic and customer engagement shift. That is a catalyst!

We have not seen such a rapid shift like this in our lifetime, one that will demand core systems that will adapt to customer needs and behaviors – moving between jobs regularly, seeking on-demand offerings, looking for value-added services, buying benefits that can port to individual insurance and full digital engagement. These trends are tied to the new dominant insurance buyer of the digital era.

Who are the new dominant insurance buyers? How will they change the nature of insurance?

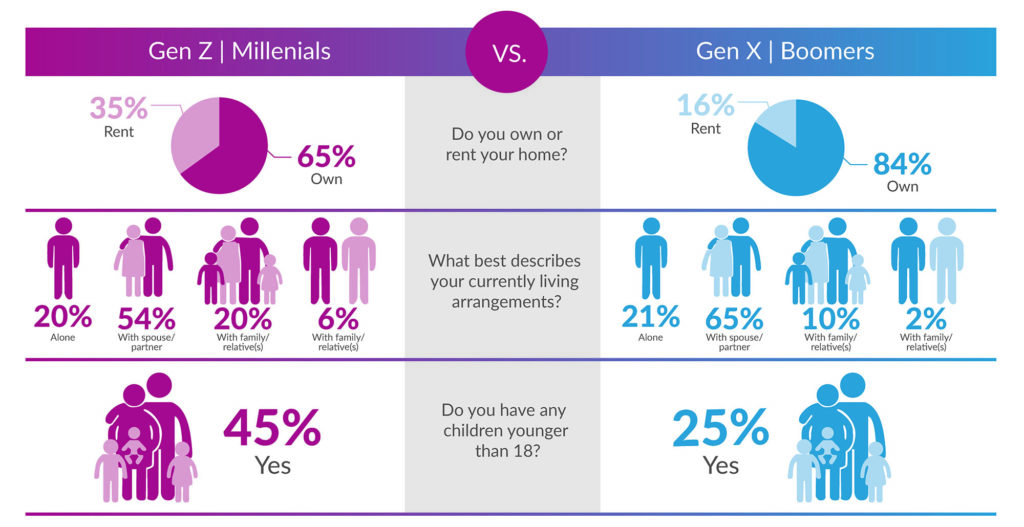

In Majesco’s latest thought-leadership report, Rethinking Life Insurance: From a Transaction to a Life, Health, Wealth and Wellness Customer Experience, we use our recent consumer survey to paint a picture of this dominant insurance buyer as we chart the similarities and differences between demographic groups. For the purposes of our reporting, we place the segments into two large “super segments.” Gen X and Boomers fit into one segment – the older generation that has been the foundation of growth for 50-plus years. And the younger segment -- Gen Z and millennials, who represent the next generation of buyers and who expect digital-first engagement, products and business models.

Some interesting insights regarding the younger generation set the stage for a different view on expectations and engagement. Currently, the younger generation rents at twice the rate of the older generation and is two times more likely to live with parents/family or friends/roommates, as seen in Figure 1. However, the younger generation is also 80% more likely to have children under 18 in their household. Yet, they represent a strong segment increasingly ready for insurance as they form new households and raise their families, replacing the older generation as the coveted insurance buying segment.

Figure 1: Demographic profiles of the generational super segments

These segments identify how insurance’s dominant buyers are changing, particularly their expectations, usage and perception of life insurance. The urgency of adapting to millennials and Gen Z is reaching a tipping point. Next year, millennials will overtake the older generation. And by 2025, the combined Gen Z and millennial generations will dominate the 30- to 60-year-old sweet spot for insurance — a complete flip in dominance in the next five years.

Insurers unprepared for this new dominant insurance buyer and their extremely different needs and behaviors will increasingly find they are no longer relevant.

As we have been pointing out recently in our webinars and blogs, insurance’s focal shift from transactions to experiences is going to result in a wide range of growth opportunities. The younger generation seems to understand the value of insurance and wants it. However, they expect something that is personalized to them. To get this, they are more willing to share personal data like health and exercise data (including in real time) to underwrite their policy. They want services. And they expect a seamless, digital process.

You may not realize it yet, but this is the generation we’ve all been waiting for! The only drawback is the lack of preparedness and the swiftness with which this is unfolding…now accelerated by COVID-19.

While L&A insurers needed to operationally improve prior to COVID-19, they are now more pressured to do so, both during and after the crisis. The pandemic is rapidly exposing less-than-desirable customer experiences, as insurers deal with paper-bound processes, non-digital post-service transactions, a rise in “fluidless” online life insurance purchases through new competitors and the need for extra caution due to fraud. At the same time, risks have emerged that demand new products such as “pay gap” for employees unable to work during a shutdown, various health products and simple life coverages – either as individual products or voluntary benefits.

To retain the customer and revenue, insurers must rethink their scope away from a life insurance transaction to a broader lifestyle experience across health, wealth and wellness that includes:

Insurance Product:Product (risk, services, experience) redefined but requires insurance to participate and play within ecosystems, rather than simply existing as a product unto itself.

Lifestyle - Health, Wealth and Wellness: A unified view to cover all aspects of life from health, wealth and wellness for banking, insurance, wellness activities, brokerage account 401K accounts and more, in a holistic way instead of separate transactions or policies for each.

Services:Provide services such as wellness discounts, preferred access to gym memberships and access to online brokerage accounts that provide a powerful, single engagement, eliminating points of friction between the different participants of the ecosystem.

Continuous and Fluidless Underwriting:Constantly updating the risk profile of an individual or thing that changes the terms and pricing that are influenced by the continuous flow of data and use of the data to avoid fluid-based underwriting for a range of life insurance products.

Highly networked, data-driven business models are emerging, within and outside of insurance. They are redefining the customer journey, and the entire customer relationship, across a broader set of health, wealth and wellness options.

The viability of the insurance industry is vitally connected to demographic and market trends, customers’ expectations and their adoption of new technologies. The combination of these factors will pressure the insurance industry to develop products and services that are more affordable, tailored to very specific needs, digital-first, simpler and grounded in trust that not only protect lives but also enhance those lives across a wide array of areas beyond insurance, as reflected in Figure 2. They will also be looking for consolidation. “Can I meet more than one need with this one relationship?”

Customers will expect a different experience that brings solutions to all of these needs together.

Figure 2: Elements of a holistic lifestyle ecosystem

Protecting Themselves and Their Lifestyles

Numerous research studies, including our own primary consumer and SMB research, have highlighted customers’ view that insurance is complex and difficult and unpleasant to deal with. From the multi-page, fluid-oriented applications to the multi-page contracts full of confusing legal terms and exclusions and a variety of different riders, traditional broad policies exacerbate the problem. Understanding what is covered and how much can be like a maze, where the “truth” is difficult to determine, creating frustration and lack of trust.

In contrast, newer coverage options remove complexity, because they are simple, specific coverages for specific needs and time frames. Simplification of the life insurance process and policy has been a major focus of startups like Ladder Life, Haven Life, Bestow, Fabric, Health IQ and others – driving their growth and loyalty with customers. But simplification may also mean a broader approach.

As we mentioned in our recent blogs on mobility ecosystems, organizations are expanding their brands to offer simplicity through tools that meet multiple needs at once. With life insurers, this kind of ecosystem will begin to look much more like a comprehensive life, health and lifestyle management process. Insurance will always be a part of it. The experience created by the insurer, however, might look dramatically expanded and radically simplified. The result will be straightforward – insurers will be contributing, not just to the security of individuals and families, but to holistic life improvement.

Connecting to Better Life, Health and Wellness

Technologies like IoT and wearables have rapidly matured from emerging technologies over the past five years. Fitness trackers and other connected wearables are becoming important connections and hubs for new ecosystems that provide value-added services or insights for people to manage their health and wellness. A 2018 study commissioned by Vitality found that adults who used fitness trackers tied into a rewards scheme could add two years of life expectancy, on average.

Scientists and tech companies are realizing the potential of these devices beyond their original fitness tracker role to predict possible adverse health conditions, including COVID-19. In the 2020 Innovation in Insurance Awards sponsored by Efma and Accenture, a submission by PZU in Poland used a wearable device to measure oxygen and pulse in real time to reduce transfer infections of COVID to medical staff in hospitals.

Michael Snyder, chair of genetics at Stanford School of Medicine, noted that smartwatches and other similar connected devices make at least 250,000 individual measurements a day. This continuous stream of data, fed into powerful predictive algorithms, can be more effective than traditional methods at detecting health issues. For example, Scripps Research Institute found that changes in heart rate caused by an infection can get detected four days before a conventional temperature check detects a fever. Recognizing the health and wellness potential of these devices, Apple has been researching how its watch can be used to detect heart problems, and Fitbit is conducting 500 research studies on issues like cancer, diabetes and respiratory conditions.

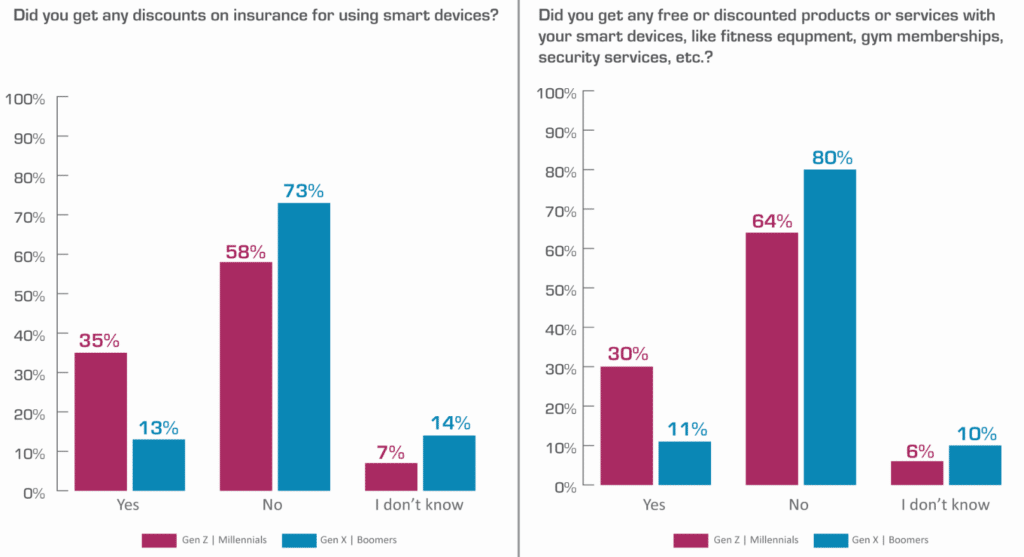

These innovations fit the younger generation. Gen Z and millennials who own a connected device are nearly three times more likely to say they received an insurance discount or free/discounted products or services as part of the device as reflected in Figure 3. Whether these discounts are real or perceived, it’s clear that the younger generation wants a stronger connection between these devices and related products and services – an example of ecosystem thinking. Just as these generations grew up with digital technology as a defining factor of their youth, ecosystem engagement is a defining influence on their behaviors and expectations (just look at Apple and Amazon engagement) as they become the dominant buyers of products and services to protect life, health and wealth.

Figure 3: Discounts and benefits bundled with smart devices

But the use of these devices is not just for wearables; it extends to home IoT as well, offering an opportunity to create a bridge from P&C and home security into home health and wellness. As health awareness technologies arise, IoT home devices can add value to those who choose to age in place, creating an all-in-one connected home and health offering.

So, if we follow the digital thread properly, the same capabilities that are desired by the younger generation are going to be used to assist the older generations with their health, security and lifestyle during retirement. With more than 10,000 Baby Boomers retiring each day, this is a huge market opportunity. Life insurance’s “new occupation” may be far broader and far more helpful than insurers had ever imagined. In targeting millennials, insurers may find themselves better prepared to meet the needs of all generations.

The Mood to Move

Motivation is the key to insurance sales. Is the new dominant generation motivated to seek life insurance, and are our sales processes advanced enough to capture them at the point of need?

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

In this age of disruption, all those organizations that spent many years and lots of cash to dig beautiful trenches for their useless Three Lines of Defense are being seriously damaged. These organizations are now left needing even more effort, to fill up their trenches and get out on the battlefield of real business.

R.I.P., Three Lines of Defense model (the three being: operational managers; risk managers and compliance functions; and internal auditors). Your creators saw a tiny speck of light, but millions are left without defense, and the trenches are in shambles. Sadly, your ghost will haunt many for a long time. They still have three lines, but these are now so blurred that organizations must be extremely careful not to kill their own front-line fighters, a situation much worse than running around in the old trenches.

The model turned to a story of failed backward innovation -- making something useless even more useless…… and that in the middle of the age of disruption.

As Michael Volkov recently said: “The IIA’s revised model [for the Three Lines of Defense] should be ignored and relegated to the ash heap of bad ideas.”

The elephant in the room is actually a grey rhino, not a black swan; it is time for risk practitioners to learn the lessons. Time to wake up to the reality that an outdated risk management process of steps to Identify, Analyze, Evaluate, Treat and Monitor the Risk, together with beautifully crafted RAG reports linked to a bunch of risk-mitigating responses, are of no use, and that following any standard or framework contributes nothing to the actual management of risk. The effective management of risk depends on the risk management skills of the front line and the decisions made by them in every situation of risk that they encounter.

It is time for auditors to get away from the management of risk, far away -- and to stay away. By the time anything gets to their line, it is too late anyway; all they can do is to issue a finding, implying that they “found” something. I have never seen an auditor resuscitate a dead business. Lately, we see more cases where they actually contributed to the death of organizations through a lack of diligence and susceptibility to corruption.

What a pity that the hours of heated, heat map-driven debates in the risk committee meetings on whether something should have been red, amber or green at the end of last month (or, even worse, last quarter); came to .....nothing!

The dominant personalities glaring at risk reports created from historic data, with their thinking clouded by unconscious biases, also made the syndication of decisions in these meetings so much more difficult. The hear no evil, see no evil, do no evil committee members who were mostly dedicated to their mobile phones during these debates are still going with the flow. Just like dead fish.

We also learned that "tested" business continuity plans are of very little value; no disaster will follow your plan. Success lies in the way each and every employee will respond to the situation of risk on D-day.

It is time for risk practitioners to grab the bull by the horns and learn this elephant-size lesson that the only way forward is building an effective risk culture and teaching everyone in the company radical risk management skills.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Horst Simon has been in commercial banking and the risk management consultancy industries for four decades. Since 2010 he is a risk management consultant and trainer and was associated with leading global players in the field of risk management consultancy and training as well as business process outsourcing.

Six Things Newsletter | September Wrap Up

September Highlights: 3 big opportunities from AI and ML; the future isn't just for insurtech; creating the future of distribution; and more.

In2Risk 2020 is a can’t-miss insurance industry event focusing on a diverse range of emerging issues and educational topics. Interactive, career-ready, forward-looking, plus the joy of Conferment.

The 2020 Global Insurance Forum is going virtual this fall! Join global insurance executives, regulators, academics and policy makers from all sectors of the industry for a complimentary two-day virtual forum on October 13-14.

California, the bellwether for so many things in the U.S., is in the lead on this insurance issue, with its wildfires showing how very complicated it will be.

IN the Know is your podcast connection to the top innovators, strategists, storytellers, thought leaders, movers, shakers, and go-getters in the risk management and insurance community.

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Six Things Newsletter | September 22, 2020

In this week's Six Things, ITL's Paul Carroll asks for some respect for insurance innovators. Plus, digital future of insurance emerges; AI in commercial underwriting; selling where life happens; how to minimize flood losses; and more.

In this week's Six Things, ITL's Paul Carroll asks for some respect for insurance innovators. Plus, digital future of insurance emerges; AI in commercial underwriting; selling where life happens; how to minimize flood losses; and more.

The insurance industry is pretty good at beating itself up for not innovating faster — and many analysts and customers are all too happy to join in — so it was a welcome surprise to see an article last week in the New York Times that enthusiastically described a nearly frictionless future for auto claims.

The article quotes an executive as saying, “In the near future,… we’re going to take the [auto claims] process from days or weeks to minutes.”

When’s the last time you saw such a glowing statement about insurers in a national, non-insurance publication? Doesn’t it feel good?... continue reading >

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

Across commercial insurance, from auto liability to workers’ compensation, claims that involve a bodily injury tend to follow a common life cycle from the moment a claim is opened until the date it is resolved. As claims evolve through stages in this journey, a growing set of data gets added to the claim file, pulled from bills, notes, images, payments and other files. For complex claims, the journey can extend for years and involve updates and files from adjusters, nurse case managers, providers, attorneys and others. When AI is added, the data in this journey becomes visible, forming a more predictable trajectory that enables adjusters and supervisors to effectively manage the claim, reduce costs and enable better outcomes for all involved.

Traditionally, much of this data is not fully used, either stored beyond the reach of claims teams or overlooked by busy adjusters just trying to stay on top of their caseload. But now, image and language processing can aggregate and organize that data, and machine learning can be applied to generate insights and predictions about the likelihood of future events. All of that gives adjusters a powerful new tool to help claimants get back to health faster — and reduce costs for all parties involved.

To see the potential, let’s look at how a claim in a specific line of commercial insurance — workers’ comp — evolves today. A person gets hurt on the job, and the employer files a claim. A claims adjuster collects notes from the worker and employer and keeps track of progress as the claimant visits a doctor. The worker gets additional treatment over time, which is also documented, and then goes back to work if all goes well; if it doesn’t, the claimant may enlist a lawyer, which extends the life cycle many months or more. Much of the data collected is never analyzed, and often only a fraction is reviewed. Even if they had the time, adjusters would struggle to draw connections between all of the disparate data.

This is how things have worked for decades, but they haven’t actually worked, at least not to their potential. Claim costs have risen due to using reactive rather than proactive management and tools, allowing 28% of claims to drive 80% of claim costs.

To make the mountains of information that accompany a claim more useful, artificial intelligence (AI) is slowly being introduced into the claim’s journey, starting with predictions that are most critical, such as claim costs or attorney involvement. But AI is still very new to insurance, and today’s claims teams are only scratching the surface on how it can be applied for the betterment of all constituents.

AI in action

Let’s take a look at how AI can reshape the journey of a claim. In this new vision, the pivotal points in the claim life cycle remain the same, but, with data science mixed in, the journey becomes smarter and more efficient. A simplified flow may run as follows:

Intake and Phase I predictions

This is the area where several vital applications of data science emerge. Phase I also sets the stage for each subsequent phase.

A claim is opened, and all of the initial details on a worker’s injury are placed in a cloud-based system. As such, relevant case details are accessible to analysis; no one needs to go digging through case files manually or waiting for hard copy images to arrive. With advances in AI, asynchronous data sources, such as notes and images, are incorporated so that the system can understand and use them to establish trends and make connections.

Using data science, predictive algorithms assess not only the data collected on the claimant, but also can compare it to all of the data available in the system on other claims — which translates to a repository of millions of data points. This enables systems to do things like assign claimants to available providers who are believed to be the best-equipped to treat them and flag cases that might warrant extra care.

With relevant information available at claims adjusters’ fingertips, AI systems eliminate significant amounts of time spent by adjusters working on each claim. For example, the potential for the claims rep to simply direct a claimant to a provider she knows — whether or not it is the right provider for the case — dramatically decreases if there is an algorithm that looks for available specialists within a 30-mile radius of the claimant, who have a track record of positive outcomes and who are in-network and available. That information allows the rep to instantly choose the best provider for the job. This is particularly important today, given the limitations on care access imposed by COVID-19 and the new types of cases that are appearing in claims. Even veteran adjusters can’t rely on their same roster of thoroughly vetted providers; they need a system that can identify new possibilities that will deliver desired outcomes.

Well-trained machine learning can identify potential markers for problems within a claim based on data from thousands of other claims. With intelligence, systems can flag these cases for adjusters with recommended actions (again, based on data) so that adjusters can intervene early. Remember that stat about how 28% of claims result in 80% of claim costs? Early intervention can diminish this issue and save companies millions of dollars a year by being active about these claims; AI-based systems make this remarkably fast and easy to do.

In each of these cases, the adjuster is saved from countless hours of research that can never be as complete as what a machine can turn out in only seconds. As a result, the adjuster has more time to devote to the cases that matter most. She can also handle a greater number of cases to help more people more quickly.

Care delivery and Phase II predictions

In the next phase, the claimant goes on to receive additional care, and data related to the claim is continuously monitored. Algorithms can flag coding errors that prove costly throughout the life of a claim or look for signs of provider fraud. A wide range of claimant sentiment signals can also be triggered by the continuous data feed, including potential return to work concerns, comments that often lead to litigation, and treatment concerns with the primary doctor. The signals are time-stamped, and together they form milestones in the claim’s journey. The sequence of adjuster contacts and recommended actions can also be plotted.

If all goes well, and no flags emerge during the care delivery phase, the claimant heals and returns to work. The claim is resolved efficiently. In some cases, though, the claimant may pursue litigation, which can add thousands of dollars and several months to the life of each claim.

Litigation and Phase III predictions

Claimants might involve attorneys soon after filing a claim or much later. In either situation, attorney involvement represents a whole new phase.

With the right algorithm and the means to pull data, AI systems can identify the best attorneys for a case based on outcomes. The systems can also pull and analyze key settlement data so that organizations can make the right decision about whether to settle and when. As a result, cases are resolved as quickly as possible, and claims are closed more efficiently than ever before.

Conclusion

While this is only a snapshot of how AI can be applied today, it illustrates how having actionable, contextual information in your hands at the time you need it, particularly early in the claim’s life cycle, enables claims to be handled efficiently, resulting in better care for claimants, lower costs for organizations and fewer frustrations and manual tasks for adjusters.

As the world of claims continues to evolve, this technology will become even more important, driving insights and breakthroughs. Increasingly, AI produces results that empower organizations to adapt faster and more responsively. It’s exciting to think about where it will go next.

Ji Li, Ph.D., data science director at Clara Analytics, has leadership responsibility for organizing and directing the Clara data science team in building optimized machine learning solutions, creating artificial intelligence applications and driving innovation.

Blockchain can be used in different domains, such as fintech, healthcare, manufacturing, tourism, real estate and government. It removes intermediaries from many business workflows. This helps organizations optimize costs and gain additional competitive advantages. Let’s go through blockchain use cases beyond bitcoin.

Blockchain-based supply chains

In a traditional seafood supply chain, for example, it is hard to trace illegal practices and product mislabeling. There are too many parties involved, with incomplete transparency about their actions.

Food safety and quality issues lead to parties mistrusting each other, which adds to the industry’s economic instability. Sustainability is also a growing problem, because more customers demand to know where their food comes from.

To solve these problems, blockchain consultants suggest implementing the combination of IoT and blockchain. The IoT part consists in tagging seafood items with sensors that gather and translate their location data in real time. Recorded on a blockchain, this data becomes available to all members of that blockchain, allowing them to track the food origin.

Thanks to blockchain, the supply chain can become transparent and trustworthy. It can also become faster and cheaper because of the automation of product location and status updates.

The same approach can be followed with other highly regulated products (such as pharmaceuticals) or high-value resources (such as gemstones and precious metals).

Everledger, a startup that recently secured $20 million in funding, created a blockchain use case in which each asset is assigned a digital fingerprint and tracked throughout the supply chain. This system provides all stakeholders with an immutable, forgery-proof record of each product’s origin.

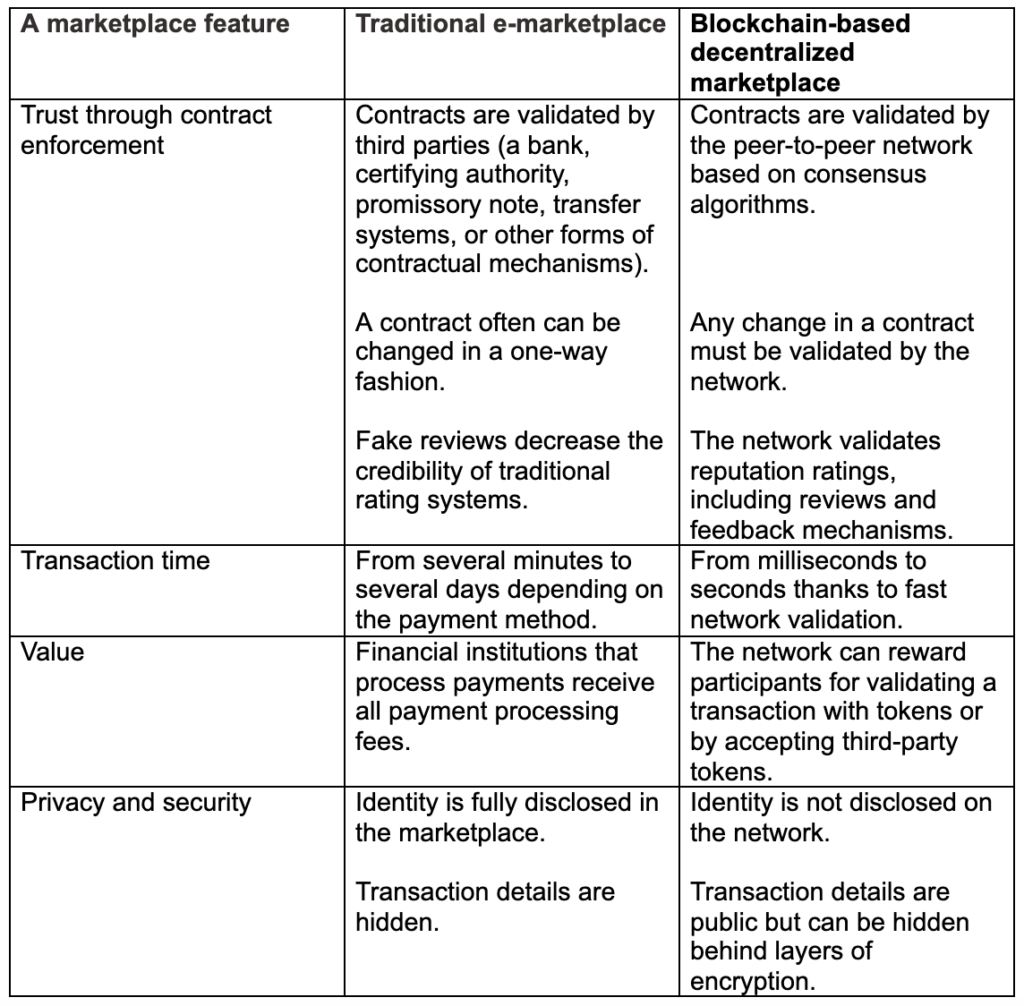

Distributed autonomous marketplaces

One of the main advantages of blockchain is its decentralized structure. That’s why in the future some blockchain applications may well underpin autonomous distributed marketplaces regulated by their users rather than corporations.

Let’s consider the possibilities blockchain can bring to marketplace management. In the table below, there are marketplace aspects that a blockchain model would redefine:

An example of a blockchain-based marketplace is Australian startup CanYa. The company tries to differentiate itself from the competition by offering more transparency and trust. CanYa’s founders guarantee that paying clients will be satisfied with the quality of provided services, while service providers will be paid in full and on time. All this is achieved thanks to blockchain.

The startup also launched iOS and Android apps processing both fiat cash and peer-to-peer cryptocurrency payments. Their own cryptocurrency—CanYaCoin—is created to be at the center of the platform. It is designed into the innovative hedged escrow contracts that combat the notorious instability of cryptocurrencies.

Origami Network takes a different approach by offering developers a platform where they can create their own peer-to-peer marketplaces. Origami developed a set of blockchain-based standards and protocols, which businesses can use to create their own online decentralized shopping platforms and enjoy all the perks of the distributed ledger technology.

The emerging smart marketplaces prove that blockchain use cases are not just limited to technological advancements but will also most definitely bring socioeconomic change through decentralized autonomous organizations, much like the internet did.

If we fantasize a bit and extend what startup SimplyVital Health is doing with its ConnectingCare platform for tracking post-discharge patient care, similar advancement can be made in the field of tracking customer care and the quality of after-services using IoT data on blockchain. This way, you don’t have to worry about an employee forgetting about a tweet or a message from a disgruntled client.

Similarly, music and photography publishing is moving to blockchain, with products like Ujo Music that allow users to protect all rights to their creations by simply publishing them, without the notorious intermediaries. It’s safe to say the same is possible for tracking all types of intellectual property and payments to creative professionals to secure their rights.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Ivan Kot is a senior manager at Itransition, focusing on business development in verticals such as e-commerce and business automation and on cutting-edge tools such as blockchain.

During this time of teams being physically apart, it is easy for leaders to avoid difficult conversations.

Empathy and compassion matter from leaders at this time, but you will not be serving your team if you use those as an excuse to avoid all criticism or challenging feedback.

For that reason, I am hearing from a number of my clients, who value some help on having more challenging conversations, and am pleased to share another book recommendation. This review covers a book that I have found provides a very useful model.

In her popular book, “Radical Candor,“ Kim Scott shares a model developed during her work at Google and Apple, as well as coaching CEOs in a number of successful startups.

It’s an easy read (though will provide you with plenty of challenge to put the theory into action). In this review, let me walk you through the key concepts and recommended steps (while still recommending that you buy the book).

Radical Candor: the central model of the book

At the heart of this book is the model that Kim presents to help define the term radical candor.

This term and its relevance to having difficult conversations is defined by considering two dimension in a 2×2 matrix. On the horizontal axis, you have the need for challenge directly (rather than avoiding saying anything, or moaning to others, at the other extreme). On the vertical axis, you have the need to care personally (rather than attack verbally just to win, at the other extreme).

The model:

Radical Candor 4 quadrant model (from Kim Scott)

I hope you can see that this definition of challenging conversations that can help (the radical candor quadrant) is useful in avoiding common mistakes. Kim emphasizes that radical candor is not brutal honesty or obnoxious aggression, as distinguished above.

However, Kim also (rightly in my view) highlights that a more common misstep is to back off a challenge that is needed for fear of hurting someone’s feelings or in response to emotion. That pitfall is defined as ruinous empathy above and is a mistake I’ve made in the past.

Start by learning to take it yourself

Moving on to putting that model into practice, this book recommends first experiencing being the recipient of criticism. In other words, solicit candid feedback.

It sounds easy, doesn’t it? Yet, most bosses will acknowledge that they rarely hear critical feedback from their peers or team that will help them improve. Unless we have the emotional intelligence aid of learning to experience receiving this, we are unlikely to be suitably nuanced in communicating it to others.

This book tackles the challenge head-on, with another model to guide you in requesting criticism. Kim proposes the following steps:

Ask a go-to-question

Embrace the discomfort

Listen with the intent to understand, not respond

Reward the candor

As an executive coach myself, I can see so much coaching wisdom in each of these steps: practicing asking open questions that cannot be answered superficially, getting comfortable with silence, silencing your inner defenses and offering appreciation even if it hurt.

Readers could learn so much from this book, even if they only became skilled at putting this part into action.

Praising can be difficult, too

When hearing the common term, difficult conversations, it is tempting to always think of giving or receiving criticism. But delivering praise can be hard, too.

As Kim highlights, it is easy to remain so high-level in praise that it does not help the hearer and comes across as insincere -- just saying that.

This book has a framework to help you provide more effective praise. It uses the acronym of COR:

Context: What is the context for your feedback?

Observation: Describe what the person did or said.

Result: What is the positive consequence that is most meaningful to you and them?

Such a simple formulation, but following that guidance can make such a difference in communicating praise that people take on board.

The book does go on to what readers probably expected guidance about: how to challenge someone, or communicate criticism in a way that is helpful. That balance is described in Kim’s initial model, of challenging directly while also caring personally.

Here, too, Kim provides a model/framework/acronym. It is labeled as HIP, but really it’s the slightly more clunky HHIIPP:

Humble: realize it is only your perspective

Helpful: make sure your goal is to help the person

Immediate: provide as close as possible to the event

in Person: where possible, meet in person

Private: find a private place away from others

not about Personality: Be specific and focus on behavior, not motive

Once again a helpful guide in a book packed with practical suggestions and examples from the rough and tumble of office life.

Are you having difficult conversations?

I hope that book review encourages you to both read this book and put this advice into practice.

Do you agree that difficult conversations are being neglected? Have you ever been trained how to do this well? How are you managing to still have these types of conversations when working from home?

I look forward to hearing your experience and advice.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Paul Laughlin is the founder of Laughlin Consultancy, which helps companies generate sustainable value from their customer insight. This includes growing their bottom line, improving customer retention and demonstrating to regulators that they treat customers fairly.