Diversity and inclusion (D&I) have been priorities for the insurance industry for years. However, there have been fundamental limitations on progress that have gone under-addressed. While the state of D&I in the insurance industry is stronger than ever, we limit the potential to advance these issues without having a meaningful, clear-eyed examination of a few basic issues.

Cultural Disconnect

Organizations are only as strong as their culture or brand. Prior to joining Zurich, I owned a consulting firm. As a consultant, I learned first-hand that no matter how great the marketing efforts might be, if a company culture or brand is lackluster there will be always be a fundamental disconnect with customers.

Company culture is one of the areas where we see more prominent diversity and inclusion issues plaguing the insurance industry. As a young woman, I had experiences in being heard, or unheard, that have shaped my perspective. While I believe there are opportunities to make a mark in the industry if you put the effort in, I also see barriers in corporations that don’t allow for people to be their authentic selves. Organizations that adhere to a rigid hierarchy, with leadership teams unable or unwilling to innovate, throw up roadblocks to D&I due to preconceived notions. These are the companies that fail to seek diversity of experience, culture, education, personality, perspective and thinking. These organizations rarely embrace authenticity in employees, seeking conformity instead. This approach limits worker experience and professional growth opportunities.

Successful company cultures are lived, as are toxic and limiting company cultures. Companies that are sincere about D&I have to live it.

COVID-19Side Effects

When the pandemic pushed the U.S. workforce to go remote, it became clear the virus was hitting the Black and Latinx communities more harshly. Access to high-speed internet, availability of space in the home for one or more remote workers and students, healthcare accessibility and urban food deserts, among other matters, were all existing obstacles. But, while not always apparent in the workplace, these issues became clear challenges for many workers and their employers after the pandemic shutdown.

As an industry focused on managing risk, we need to consider the risk of not properly supporting the communities we represent and their well-being. Our leaders, both in the insurance industry and beyond, must remember that not everyone is experiencing the events of 2020 equally. We may be “in this together,” but we are not in it together equally. Greater empathy is essential to greater diversity and inclusion.

It Starts at the Top

One of the clearest signs of the lack of progress on D&I issues in corporations is the lack of diverse talent at the leadership level. The standard response for most industries on this point is to note the lack of diverse talent available. This bias has been consistently used to justify a lack of executive team diversity. Another defensive argument is that companies work to ensure all employees have the same opportunities to advance their careers. This latter rationale has been used to justify maintaining the same systems and processes that have been in place at corporations for years. We may add employee resource groups, mentoring programs and programming, but the systems have not changed.

In my role focused on diversity, inclusion, equity and belonging at Zurich, I invite leaders to question these biases. What if there was ample, diverse, executive-level talent available? Would the company’s leadership look dramatically different? Would it be more diverse? Would the systems and processes currently in place to nurture and advance careers change if we proved not all employees have equal access to opportunity? If the answer is no, then we have to acknowledge our inherent biases and make changes.

These biases are overcome when leaders are open to and can rely on those around them to provide critical insight. Recruiting is one example. What efforts have their organizations made to find great talent? If the slate offered by recruiters is not diverse, do they push back and request a more diverse pool? Do they leverage their industry relationships to find that talent? Does the executive team hold leaders to account for seeking talent that mirrors the individuals and communities they serve?

Recruitment is just one priority. Expanding in-house talent is also essential. To complete my doctorate, I spent a lot of time researching what companies do to advance diverse people in their careers. Do diverse professionals have the same access? The same mentor opportunities? The same advocates? In my experience, the answer is often no.

This could be an affinity bias. We naturally want to help those who remind us of ourselves. We need to understand that some people advance in their careers, and some do not, precisely because of these biases. Insurance industry leaders need to face this difficult reality to create better opportunities for our diverse talent.

What Can Change?

One solution Zurich has embraced is called the Inclusion Cohort, a program we launched last year. It’s designed to better prepare diverse talent for potential leadership roles, offering them leadership assessments, identifying strengths and areas for development and providing them with mentors. Our priority was to build the cohort so members would have a sense of camaraderie and shared success. Today, more than half of the initial participants have been tapped for new responsibilities, with another earning a leadership position. Our goal is to scale similar programs across the company.

We are also working on extensive anti-racism programming for our executive and leadership teams to help them better understand diverse experiences, which helps build empathy and motivation to change.

These and other efforts are steps Zurich is taking to promote a more diverse industry future, and they are shareable.

Organizations like the Insurance Industry Charitable Foundation (IICF) have proved critical to highlighting the industry’s D&I efforts. Their meetings and events, like the upcoming virtual Inclusion in Insurance Forum, are instructive on the challenges commonly faced across the industry in building equity and belonging. These events allow individual organizations like ours to work together to share and adopt meaningful strategies.

Recognizing the role that culture, global events like the pandemic and leadership and its priorities have on diversity, inclusion, equity and belonging within the industry is the first step to meaningful change. That change can sometimes be slow in coming, but it does come. Now is our chance as an industry to step up and create the diverse and inclusive future we need.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Dr. Lauren Young is the director of diversity and inclusion for Zurich North America. Prior to working at Zurich, Dr. Young served as an organizational change consultant for 10 years with a variety of Fortune 500 corporations.

Over the last decade, businesses have placed tremendous focus on improving the safety of their products, their establishments and the services they provide to their customers. They have taken advantage of data, technology and enhanced risk management practices driving safety and quality. Yet we continue to see extreme verdicts, social inflation and “hell hole jurisdictions” in the liability arena. The question is, what more can be done?

In this paper, we will analyze the trends in liability and auto losses, both litigated and non-litigated, and provide guidance on tactics to manage those losses.

Key findings:

Nuclear verdicts continue to be a concern for the business and insurance community. Just one of these verdicts can have

a major impact on individual programs. Media coverage and advertisement of these verdicts may motivate increased litigation that, in turn, creates an increased burden on carriers and companies.

Litigation costs continue to rise.

There are more attorney-represented claims at first notice of loss.

The “social inflation” factor is real and is likely driving some of the increasing litigation cost.

Litigation avoidance practices will reduce liability claim costs and increase control over the litigation rate.

Plaintiffs’ bar has become increasingly coordinated in approach and strategy in tort suits. An awareness of how plaintiffs’ strategies have evolved is a critical part of defending any claim.

Advocacy and early intervention are important factors in mitigating the likelihood that claims could evolve into more expensive disputes.

Figure 1

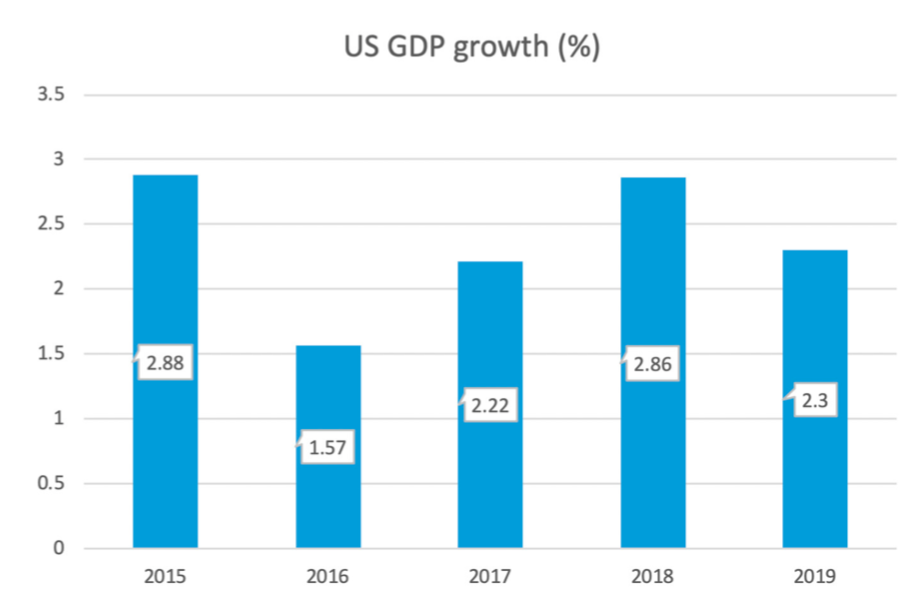

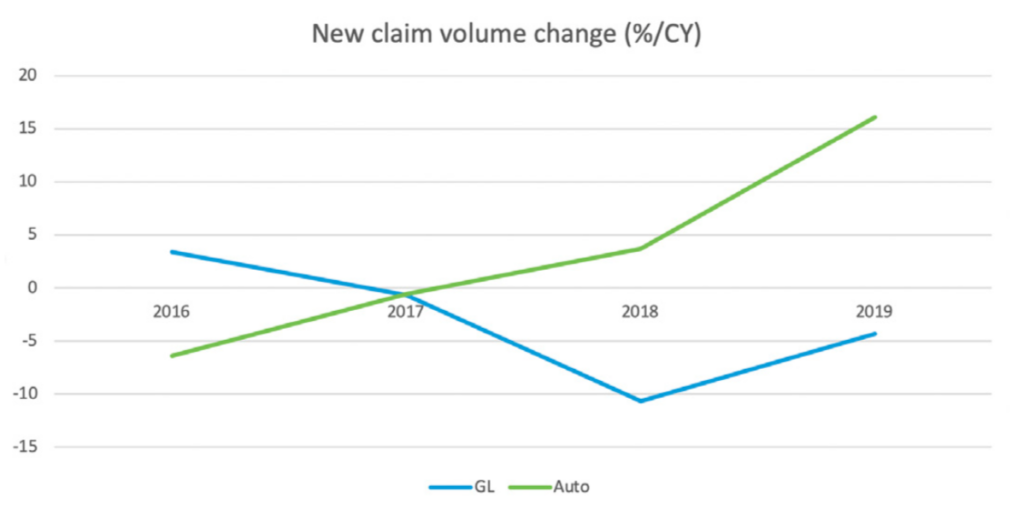

Despite GDP growth, we have seen an average decrease in general liability (GL) claims of 2.7% per year over the last five years (See figure 2). With the increased amount of transportation services (e.g., restaurant and retail delivery and ride-sharing services) and improvement in the economy, auto liability (AU) claims continue to increase in frequency. However, this increase is significantly less than the increase in related exposure growth.

Figure 2

Most liability and auto claims reach an amicable resolution without litigation or attorney involvement. When the parties cannot agree on resolution, the impact is substantial. The majority of the total paid for both GL and AU is attributable to disputed cases. In fact, 0.1% of all GL claims with total incurred losses over $500,000 make up 29% of total paid losses. For AU claims, 1% with values over $100,000 make up 60% of total paid losses. Clearly, even when litigation is a small fraction of the total claim volume, litigation and the largest value claims have a sizeable impact on ultimate values.

Given the impact that litigation and disputed claims have on results and incurred losses, the best outcomes for claims may be a case

of “timing is everything.” As claims mature through their life cycle, litigation rates increase. Several factors drive this result, including lack of communication, lack of understanding and poor resolution strategy. We will delve more into these drivers and the prevention and control tactics for litigation, later in this paper.

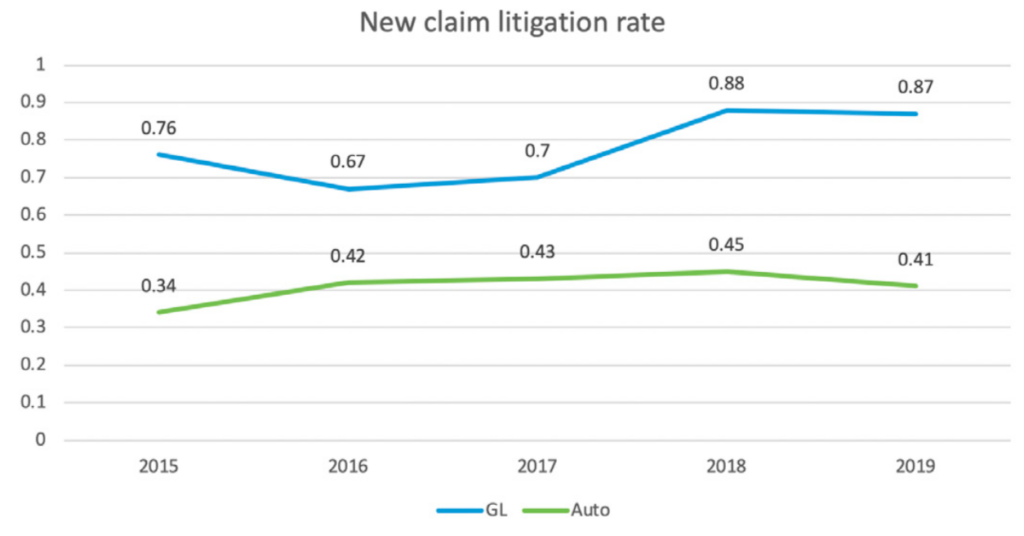

Litigation trend:

As a percentage of the whole, the litigation rate on new GL and AU claims is extremely low. (See figure 3).

Figure 3

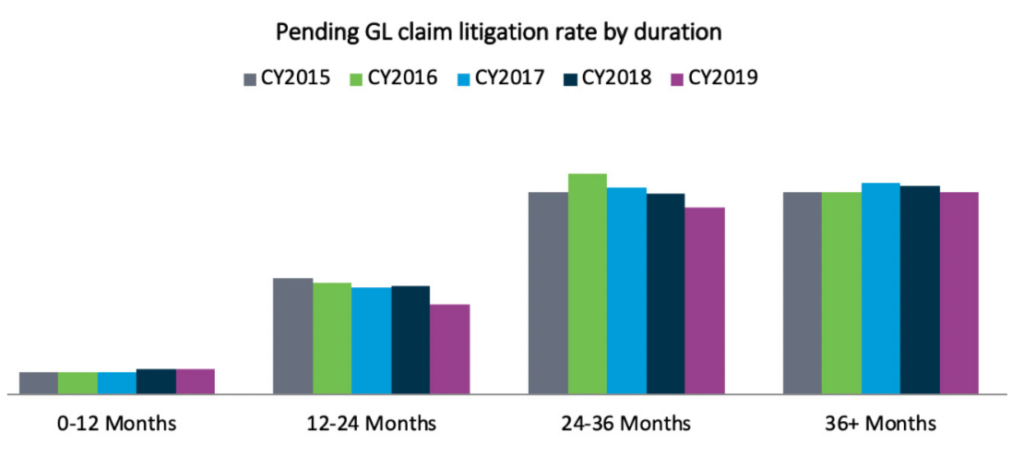

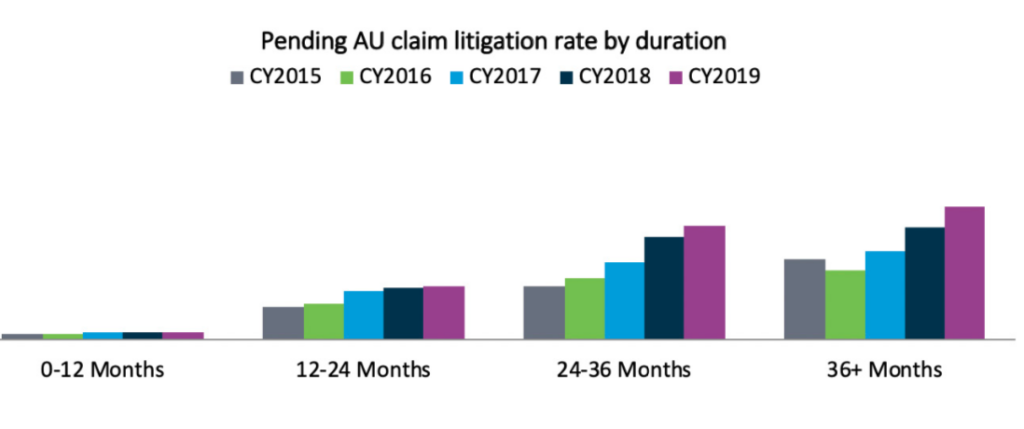

As expected, however, the litigation rate increases significantly with claims that remain open after the initial year. (See figures 4 and 5). Despite this, the percentage of litigated liability claims has been declining in the last three years. (See figure 4).

Figure 4Figure 5

As noted in figure 6, incoming litigation rates have remained flat

in the 0-12 month and 36-month development points while the 12-24 month and 24-36-month development points are seeing decreases. The two factors that favorably affected this include: the focus on resolving cases earlier in the life cycle; and the reduction in cases that continue in litigation past year three. Additionally, as already noted, there has been an increase in cases with attorney representation at first notice of loss. Although this has been viewed as a troubling trend, early attorney involvement can move cases to resolution earlier and makes access to information via discovery and negotiations quicker, resulting in faster evaluations and resolutions.

Figure 6

Perspectives on casualty litigation trends

In recent years, controlling the costs and outcomes of litigated cases, especially when left to juries to decide, has become increasingly challenging. At one end of the spectrum, the more egregious outcomes often referred to as “nuclear verdicts,” are commonly viewed as those cases with jury awards greater than $10 million. Another way to evaluate these cases is where the outcomes are “unexpected,” because the results were either not anticipated or considered a worst-case scenario. There are, of course, cases that have a true value of $10 million or more. But those are not the cases that are the focus of this discussion; it is the cases where a verdict is rendered far beyond what has been typical in similar circumstances.

Apart from large outlier cases, there are a growing number of cases that present unprecedented financial and reputational risk. And while these trial outcomes may be viewed as “affordable” to the defendants and insurers in specific cases, they are nonetheless often startling, considering their improbability.

In 2013, the insurance industry noticed a marked increase in auto loss frequency, which was especially concerning given that a 25-year decline in auto collision frequency was reversing. That 25-year trend was largely related to the increasing safety-related improvements in vehicle design. In subsequent industry studies, among 26 variables found to be correlated to the increase, the number of lawyers per million population was a significant variable. Since then and through 2019, plaintiffs’ lawyers continue to appear to be focusing on auto loss claims given the increased frequency. A detailed report by the Casualty Actuarial Society elaborates on this premise.

Industry-wide GL trends also reflect deteriorating conditions, with most GL costs attributable to litigated claims. It is noteworthy that, among four key drivers in a recent Milliman report on the GL line, two were related to litigation: litigation funding and the increase in jury award frequency and severity. The report noted that the ratio of non-economic to economic damages is increasing. In addition, Advisen maintains a large general and products liability loss dataset that reveals that plaintiffs’ attorneys have increasingly coordinated to create strategies that drive higher verdicts.

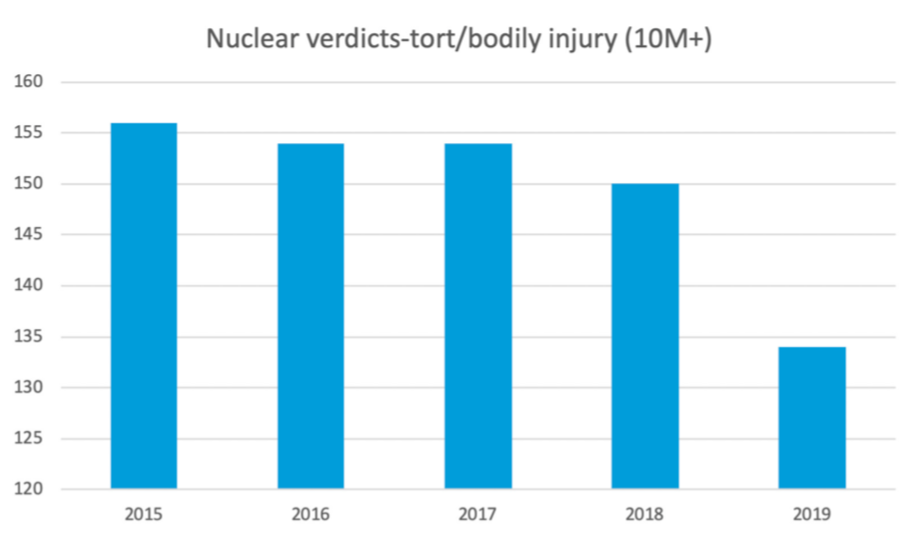

So how significant is the nuclear verdict risk? The chart below lays out the number of these verdicts for the past five years.

(See figure 7).

Figure 7

The total number of these verdicts has decreased over the past two years and is well below the five-year average. However, that decrease is countered by the increase in the value of those verdicts. According to one nationwide source of verdicts and settlements, for 2015, the largest verdict, in a wrongful death action in Florida, was over $844 million. By contrast, the largest verdict for 2019 was $8 billion for a Risperdal verdict against Johnson & Johnson in Pennsylvania (later reduced to $6.8 million). The next largest was for over $2 billion in a Roundup case (cancer allegedly caused by weed killer) in California.

So, the challenge with nuclear verdicts is not just about industry impact, but more about the impact an individual verdict can have on a business, insurer or individual. Additionally, the challenge is about the influence (including social inflation) these extreme awards have on other juries, who have become accustomed to hearing large award figures in the media and have had their perceptions changed.

Many verdicts are reduced after trial by a court or by the parties through settlement negotiations. In addition, some jurisdictions have punitive damage caps or non-economic damage caps that can also come into play in reducing jury awards. Regardless, when the judgments are reported, often by eye-catching media stories, the damage may be done. It is the rare case where a reduction in a jury award will be front-page news.

In the report from the Institute for Legal Reform titled “Costs and Compensation of the U.S. Tort System,” the authors found that total costs and compensation paid in the U.S. tort system were $429 billion, or 2.3% of U.S. gross domestic product (GDP). Of this amount, 57% went to plaintiffs, with the balance being the cost of litigation, insurance and other risk transfer costs

Of the $429 billion:

$250 billion (58%) is attributable to commercial and general liability exposures;

$160 billion (37%) to auto exposures; and,

$19 billion (4%) to medical malpractice litigation exposures.

Florida had the highest costs as a percentage of GDP (3.6%). When measured as the cost per household, the states with the highest costs (California, Florida, New York and New Jersey) were greater than $4,000 per household (versus $2,000 for the lowest-cost states).

The Institute for Legal Reform conducted a survey of over 1,300 general counsel/senior litigators, who ranked these elements as the most significant indicators of the litigation environment in states:

Enforcing meaningful venue requirements;

Overall treatment of tort and contract litigation;

Treatment of class action suits and mass tort claims;

Consolidation suits;

Damages arguments;

Proportional discovery;

Effective use of scientific and technical evidence;

Trial judges’ impartiality;

Trial judges’ competence;

Juries’ fairness; and,

Quality of appellate review.

Additional Analysis

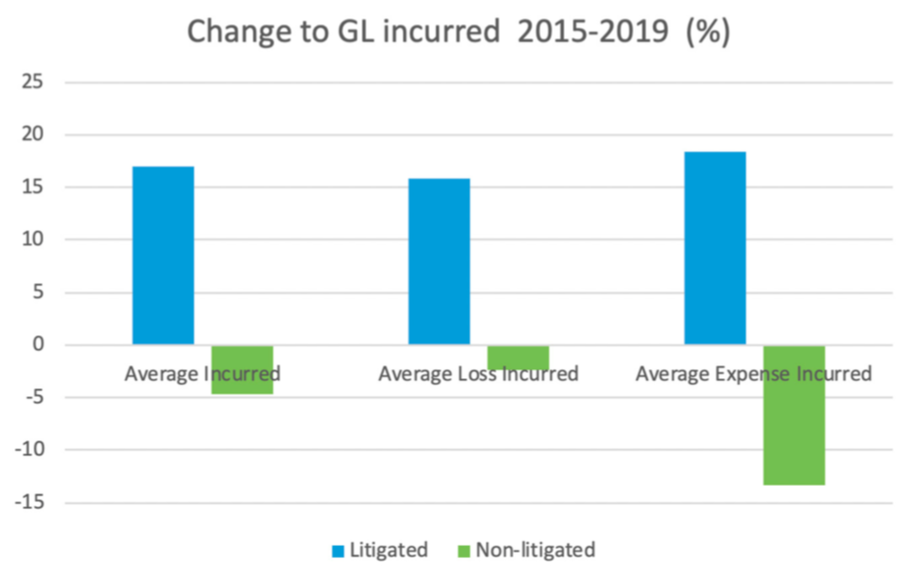

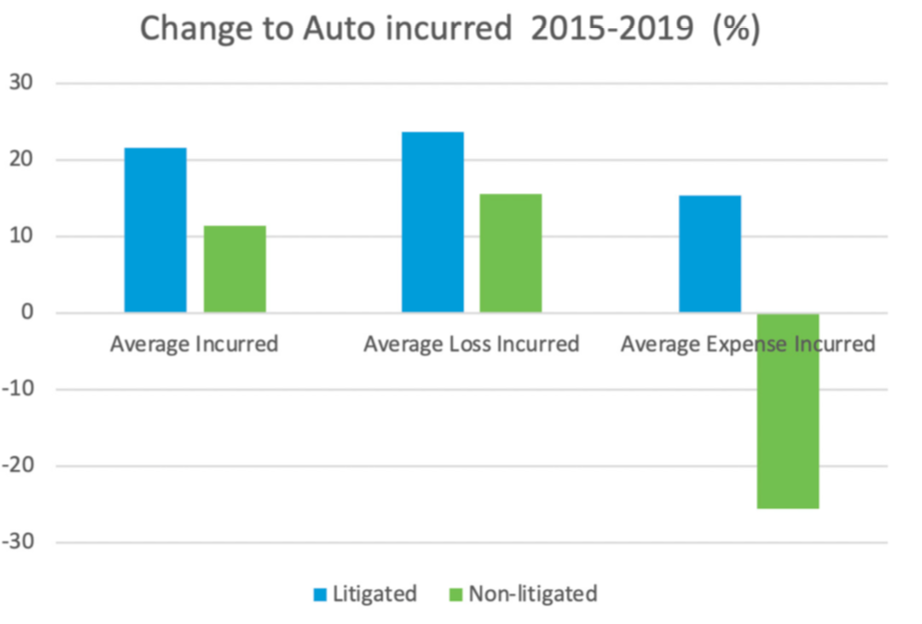

Not only are the loss cost and expense for litigated claims larger than non-litigated, as anticipated, the incurred amount for both damages and expense for litigated claims has been trending up for several years. This contrasts with the incurred trend for non-litigated claims, which has been on the decline in recent years for AU and GL. So, not only are litigated claims more expensive than non-litigated, they continue to get more expensive relative to incurred costs for non-litigated claims from previous years.

Figures 8 and 9 show increase in cost by % for each of the categories noted.

Figure 8Figure 9

Influences

Social inflation, nuclear verdicts, trucking accidents, “reptile brain” and litigation funding are among the more common topics frequently discussed as drivers of current litigation trends. Industry trends are notoriously difficult to predict, given the lack of broad, readily available and consistent data across various jurisdictions, industries, lines of business and carriers.

Without a doubt, litigation has a measurable impact on overall claim outcomes. As already noted, litigation rates generally increase the longer claims are open. Not only are litigated claims more expensive than non-litigated, they continue to get more expensive when measured by incurred costs compared with previous years. Additionally, the duration of both AU and GL litigated claims substantially exceeds non-litigated claims, including the likelihood of adverse reserve development over time for litigated claims. As a result, the industry focus on avoiding and mitigating litigation

is appropriate, particularly because the trend of costly litigation

is accelerating across calendar years. The largest verdicts and settlements continue to represent a small percentage of the total claim volume, yet they also continue to have a significant impact on overall results.

Companies have a number of tools they can use to control litigation and avoid high-liability verdicts. The focus should be on resolving claims at an earlier date, particularly in the first 12 months of a claim. The risk and cost of litigation both increase dramatically thereafter. Use predictive modeling to identify claims likely to become litigated and ensure an aggressive workflow to push for defense and resolution if appropriate. Recognition by claims professionals of the risks and red flags for outlier verdicts is critical to ensure that defense counsel is prepared to manage these risks and to move cases through trial when necessary.

Because nuclear verdicts are so few and can happen anywhere, the ability to predict them remains challenging. Thus, the focus should remain on sound litigation avoidance tactics, proven litigation management tools and strong preparation for trial.

Emerging tactics and best practices for litigation

There are a variety of factors, strategies and tactics that can affect the exposure to outsized or unexpected results in civil litigation, as well as improve the outcomes of more routine litigation.

Attorney selection — To have an effective settlement strategy, it is critical that counsel be willing and able to try cases. Use of data-based attorney scorecards and evaluations helps identify the best attorneys for various types of cases. Anecdotal opinions about counsel are not adequate for this challenging litigation environment—the data is critical to identifying the best counsel for each claim.

Leveraging artificial intelligence (AI) and predictive analytics — The best way to avoid the risk of nuclear verdicts is to avoid unnecessary litigation. Using data to identify claims likely to end up in litigation and to focus early on those claims for settlement is a key to reducing litigation costs and risk.

Attitudes toward corporations — One of the growing challenges with litigation is an increasingly negative perception of corporate defendants among some jurors. Millennials in particular are often identified as holding unfavorable views of these defendants. This must be accounted for not just in jury selection but throughout the life of the claim. Also, it is important at trial to ensure that corporate defendants have a “human face” either through witnesses or presence of a corporate representative throughout trial.

Mitigating the “reptile brain” tactic — There is debate among defense counsel about whether this is in fact a new or exceptional concern. It is not a new theory — but does seem to have the focus of at least some plaintiff attorneys. The tactic is really about fear and using it to create a reaction in the jury. Identifying those plaintiffs’ attorneys that are planning on using this approach (this will often be apparent from discovery) and planning accordingly is critical.

Mitigating anchoring tactics — “Anchoring” occurs when an individual depends on an initial piece of information to make subsequent judgments. This tactic can result in large awards based on a large damage number presented by plaintiff. It is worth considering whether it is appropriate for the defense to talk about the actual amount of damages at trial rather than try to defend against plaintiff’s number. This strategy is controversial, however, and it should be approached cautiously given the risk of a “split-the- difference” outcome.

Mitigating “third party funding” tactics — This is an increasing trend in litigation in the U.S. and seems to be exacerbating the trend of larger verdicts. Some jurisdictions and courts have begun to allow discovery into these funding relationships, and defense counsel should be exploring that thoroughly when allowed.

Case evaluation — One thing that seems to have clearly changed since the advent of the “social inflation” phenomenon is that the likelihood of a better outcome later in the life of a claim in terms of total cost has decreased. The days of a favorable settlement at the 11th hour seem to be the exception now. As a result, it is critical to have an early and thorough understanding of the case and its value.

Settlement approach — The obvious and effective way to manage litigation costs is to avoid them. As noted above, it is critical to be prepared to try cases. However, it is just as critical to identify and resolve the cases that should not or need not be tried. The key is not to change how you handle cases, but how you think about them and to create a cost/benefit analysis of trial. This requires not only an appropriate case evaluation but an honest evaluation of the related issues. Key questions should include:

How long does it take to get a trial date in the jurisdiction?

How long do trials typically last?

How much will trial itself cost?

What pre- or post-judgment interest might attach to a verdict that might be appealed?

What are the other costs to the defendant, including business interruption, reputation, etc.?

Win or lose, what is the likely cost of appeals or additional negotiations if needed?

Is it likely a party will continue to litigate after a verdict?

Will there likely be attempts to impose a cap on damages or have it removed?

The bottom line is that some cases are appropriate for trial, and some are not. With the risk of nuclear verdicts, some that seem to shock even seasoned litigators, until there’s a clear understanding of what verdicts are likely to go “nuclear” it is prudent to have a plan in place to limit litigation only to those claims that should be litigated to verdict.

To free time to focus litigation efforts on cases that will go to trial, claims teams must improve their ability to identify cases for resolution and resolve them at the appropriate time. A case that gets to the eve of trial and settles then with no change in evidence or information is an outcome that should be avoided. That is a case that could have settled earlier.

Identifying cases to resolve requires focus by claims professionals as well as the effective use of data, predictive modeling, attorney scorecards and other tools. Timing is critical; once a claim has gone into litigation, even if the ultimate settlement amount is the same, the overall cost will increase due to litigation and defense costs.

In those cases that do go into litigation, a litigation plan must be developed and provided. Claim teams must take a direct hand. The “litigation plan” obviously must incorporate counsel’s evaluation of the claim, steps to take in the litigation process and, just as critically, a “resolution plan” to make sure that the discussion gets redirected back to conclusion—whether the case ultimately is tried or settled.

Throughout the litigation, the discussion of the claim should always include the resolution plan for those cases that should or could resolve. The resolution plan must have concrete steps, and not just follow an automatic path without a clear plan tailored to each case.

Risks associated with GL and AU claims can be managed to allow for predictable outcomes, even in an environment with “social inflation,” “nuclear verdicts” and tough jurisdictions. Numerous resources, tools and best practices are available to ensure that a very small percentage of claims do not drive oversized verdicts while ensuring an appropriate approach to dispute resolution.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Christopher E. Mandel is senior vice president of strategic solutions for Sedgwick and director of the Sedgwick Institute. He pioneered the development of integrated risk management at USAA.

“We’ve seen two years’ worth of digital transformation in two months. From remote teamwork and learning, to sales and customer service, to critical cloud infrastructure and security—we are working alongside customers every day to help them adapt and stay open for business in a world of remote everything.” — Satya Nadella, CEO Microsoft

This statement was on April 30– just two months into COVID – and reflects the pace of change and acceleration of digital transformation across all industries, including insurance. The pace of change in insurance continues to gather speed and dominate C-level discussions and planning.

Today’s changes require insurers to gain clarity on how to succeed in the future of insurance. Future market leadership will be defined by a new digital foundation and business model that embraces customer, technology and market boundary changes with vision and energy. This year’s Strategic Priorities report found that forward-thinking leaders are digitally transforming their current business, while also disrupting it by building their business model for the future. The gap between Leaders, Followers and Laggards over the last year and the next three years is staggering:

In the past year, Laggards had a 41% gap to Leaders; and Followers, had a 15% gap to Leaders.

Over the next three years, the gap widens, with Laggards falling 62% behind Leaders and Followers trailing Leaders by 21%.

The era of succeeding as a “fast-follower” is long gone. Today’s Leaders are reallocating their investments into digital transformation that gives them a compelling, engaging, customer-centric approach that differentiates them.

How do your strategies align to what Leaders are doing? What specific plans can you take to improve your odds of success? How can you accelerate your digital transformation? These questions and more are what the just-announced strategic alliance between Majesco and KPMG are focused on: to provide a sustainable, risk-optimized route from strategy through execution.

Digital Maturity

Gartner’s Emerging Risks Monitor Report from earlier this year noted that “organizations are concerned about their ability to keep up with a rapidly changing business landscape, driven in part by concerns about their own organizations’ lagging and misconceived digitalization strategies.” This is a profound statement. Insurance still embraces decades of legacy business assumptions and technologies that are roadblocks on the path to digital maturity.

Why is this important? Because KPMG’s research, compiled from various studies, found that digitally mature organizations outperform less mature organizations. How? Digitally mature organizations had 25% higher revenue growth and 31% higher EBIDTA over the last three years, 11% higher Net Promoter Score and higher speed to market by 17 months! Digitally mature organizations not only operate more effectively, they are obsessed with their customers and with defining, unlocking and preserving value for both the customer and their business.

For too many insurers who lack digital maturity, this difference and the growing gap between Leaders and Followers and Laggards should be a strong motivator to move forward on the journey and get ahead of the curve … now.

Visionary leaders see the market, customer and technological trends as a many-fold opportunity for insurance — and are preparing to use new sources of data, reach new market segments, offer innovative products needed by customers, create exceptional customer experiences, leverage new channels and more. KPMG’s recent report, 2020 CEO Outlook, found that the top priorities were focused on: digitization of operations (74%); new digital business models (70%); the creation of a seamless experience (73%); and a new workforce model augmenting people with AI (66%).

Majesco’s research echoed a similar sentiment and indicated that leaders are moving forward with a cloud-based no-code/low-code platform using microservices and open APIs (64%); are envisioning and experimenting with new digital experiences (68%); and are focused on digital ecosystems and partnerships (45%) that will allow them to stay out ahead of the trend and the marketplace.

This is why Leaders are accelerating their digital journey across three key areas as depicted in Majesco’s Digital Maturity Model (below):

Digitize - Create Portals for Traditional Products & Channels for Digitization & Automation of Existing Processes

Innovate - Launch Innovative Products & Services to Transform to Digital Operating and Business Models

Insurers can start at any point on this maturity curve – from focusing on today’s business or by creating the business for the future. Regardless, having a single digital no-code/low-code platform with rich insurance content and a robust digital ecosystem of partners to enable this journey across a wide array of business scenarios is crucial for success.

But acceleration means traditional methods have to be adapted to meet the time pressures.

Digital Maturity — From Good to Great

The book by Jim Collins, "Good to Great," published nearly 20 years ago, is still so relevant in today’s digital age. While many different concepts were discussed in the book, the key to success was leadership. A key to that leadership is having the right people in the right positions to create an environment for success. They have a vision and goals for success and constantly review and act on data or results to “make it better.”

In today’s digital world that is about creating an environment that enables “test and learn” and innovation. And the theme is speed to market.

Companies that procrastinate are risking irrelevance, because, as the pace of change accelerates, their ability to adapt diminishes. This is why taking action now is crucial.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

Given the nature of insurance, and the possibilities that data analytics and technology offer, there should be little doubt that the industry is moving toward becoming a technology industry.

It is therefore only natural that insurers are looking for ways to reinvent themselves as technology companies, running corporate-wide digital transformation projects to ensure adjustment to the changing markets and secure a competitive position in the future.

This white paper demonstrates how insurtechs are important for the development of the industry but also underlines that insurtech does not address all challenges faced when creating a future successful insurer – insurtechs are digital instruments to be used in the transformation journey, but it’s still up to the incumbent to get the real transformation done.

This paper explores how to use insurtechs to address current incumbent pain points and what to look for before entering a partnership with insurtechs.

The Insurtech Landscape Mid-2020

Given the pace of the market development, it makes little sense to provide a fully updated and detailed state-of-insurtech – it does makes sense, however, to understand the underlying nature of the insurtech landscape to examine how insurtechs are entering and affecting the insurance industry.

This understanding will provide insurers with a future outlook and enable the development of adequate strategic responses – this will also help insurers to identify if and where insurtechs can fit into insurers' value chain.

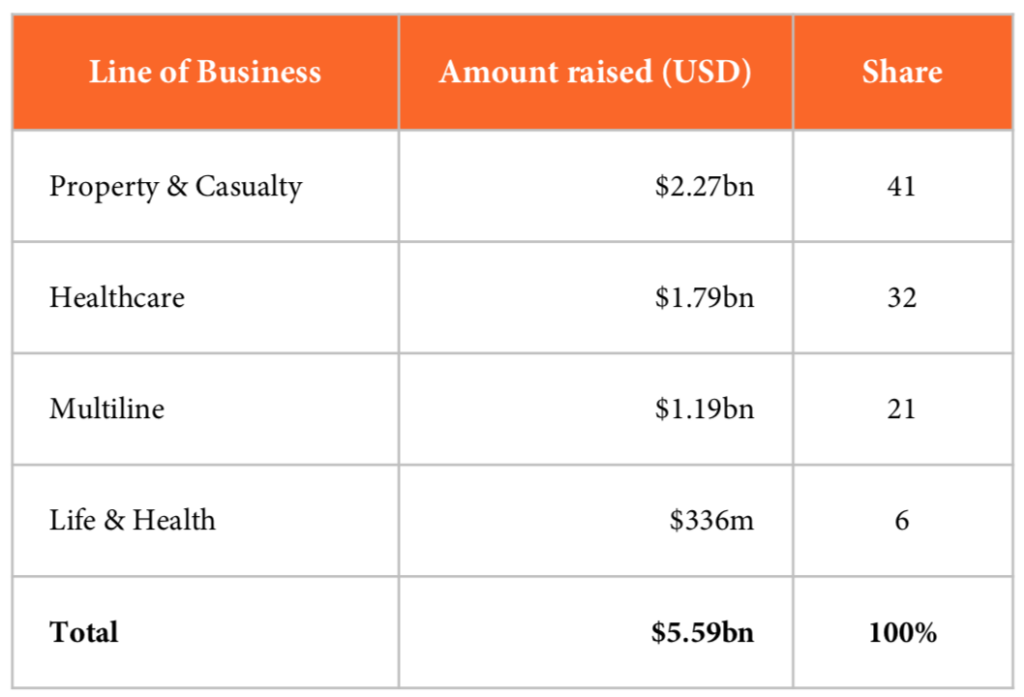

More than 75% of total dollar investments are invested in insurtechs offering products and services within distribution, and a total of 79% of all investments are in single-line insurtechs.

Table 1: 2019 total insurtech investments

Source: Coverager 2019 insurtech investments in review

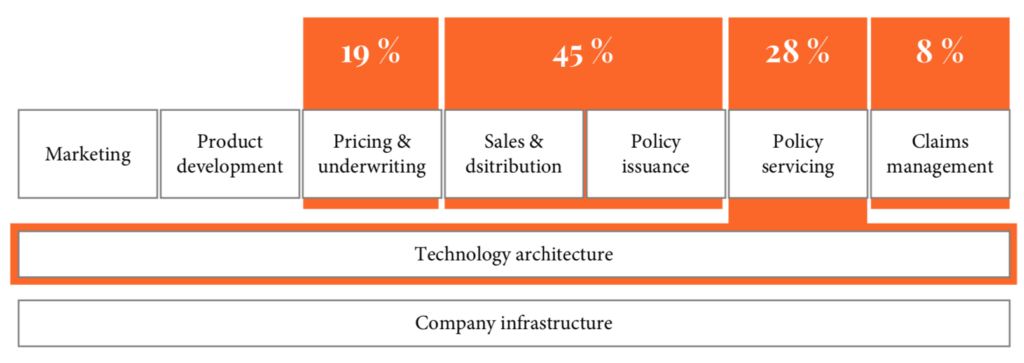

These two numbers, 75% of investments in products and services within distribution and 79% of all investments in single-line insurtechs, combined with insurtechs’ focus in the insurance value chain (see below) clearly show that insurtechs are focusing on specific areas of the total insurance value chain and not in creating new, full-fledged insurers.

The insurtechs seems to be zooming in on the areas that have the greatest business and growth potential and leaving out the less lucrative parts of the entire insurance value chain, which makes perfectly good business sense. You would only enter into industry areas with high inertia and potential for fast improvements.

Figure 1: Insurtech focus in the insurance value chain (Quarterly Insurtech Briefing January 2020)

Following the numbers from Figure 1, it appears that the structural issues impeding insurers to realize transformations at scale and speed are not addressed in particular by the insurtechs in the market.

Successful transformation of incumbent insurers requires more than a digital front end or various, isolated digital innovations – granted, it may add to the overall value provided to the customers or partners, but the underlying structural and process challenges still exist in the incumbents and still need to be redesigned for the insurer to reach the future virtual and digital state.

As shown later, some insurers are already partnering with insurtechs and benefiting from improved, isolated processes within distribution, sales, policy servicing and claims management, but very few – if any – have created a cohesive end-to-end experience for the customers and partners.

Partnering with an insurtech for a specific element of the value chain still leaves it with the incumbent insurer to realign, adjust and connect surrounding processes in an effort to create a complete customer-oriented solution.

Besides ensuring technical and operational integration, the incumbent should also carefully understand the cultural and organizational changes required when aligning and redesigning core processes.

In other words, and put provocatively, insurtechs are acting as digitally advanced middlemen or brokers – their disruption primarily lies within customer experience and service, while some leverage Internet of Things to refine pricing and improve service offering (health, home, car, travel).

Most insurtechs greatly rely on the backbone of the insurer – an important point to make and for incumbent insurers considering partnerships with insurtech to be aware about.

Successfully integrating with insurtechs

As mentioned, it does make good sense for incumbent insurers to look towards insurtechs for partnerships, as a partnership can fast-track the digital development process. Apart from being aware of the organizational changes required to make the partnership work, it is beneficial to create a gap analysis to evaluate existing competencies against competencies required to deliver on the insurer’s overall strategic direction and targets.

While looking at the elements in the value chain, and apart from identifying the gaps, noting down current pain points can detail the requirements for an insurtech partnership further.

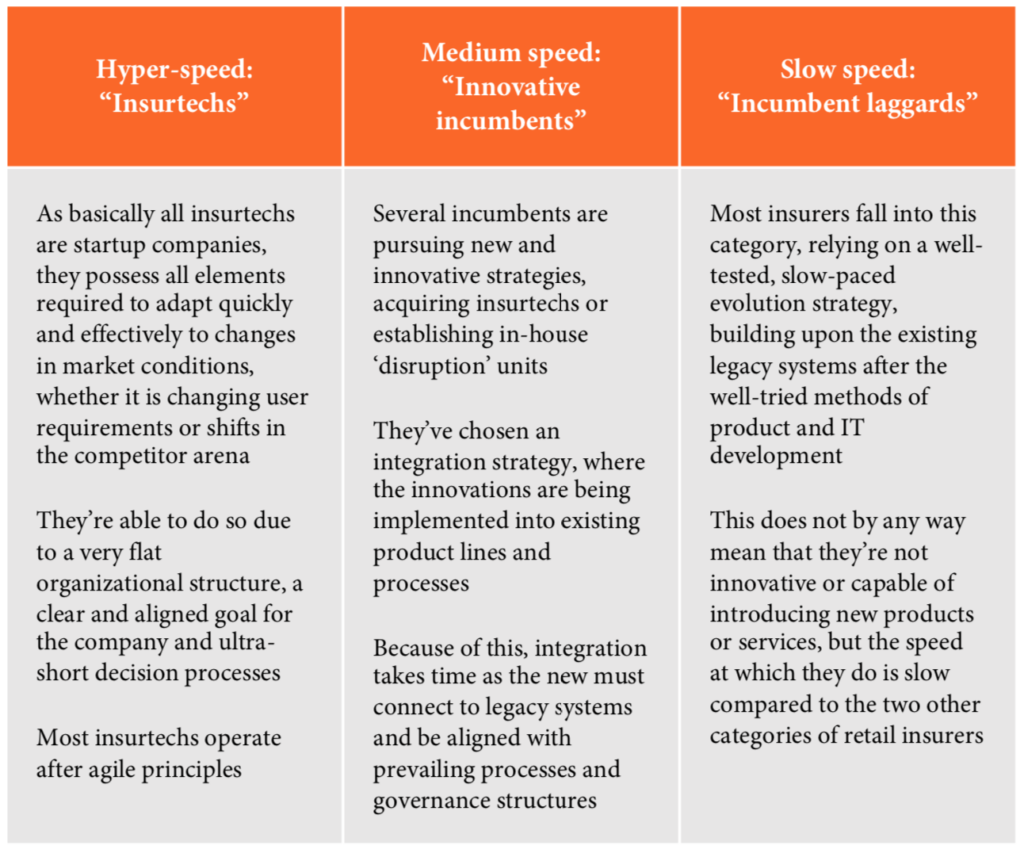

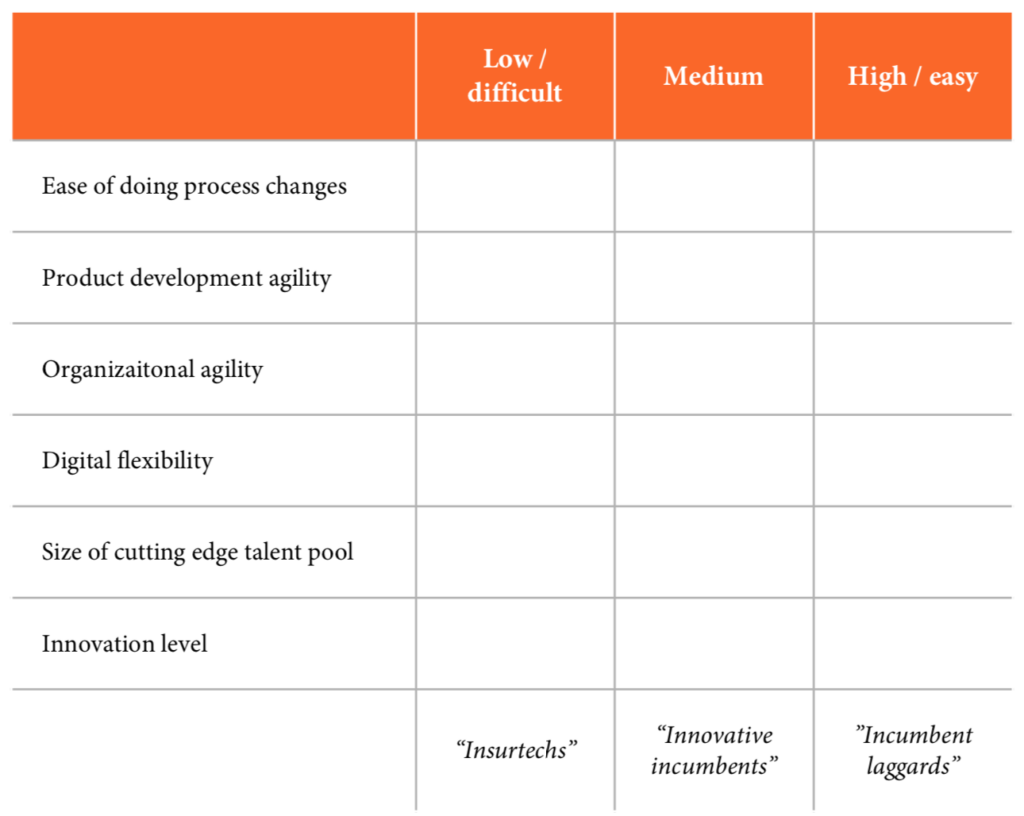

A starting exercise can be mapping the insurer against the "three-speed" insurer model to have a point of departure in defining the gaps and requirements for an insurtech partnership, followed by identification of current pain points throughout the value chain.

The three speeds of insurers

Insurers can broadly be divided into three different categories, reflecting their current digital strategy and ability to react fast to changes in the market from both users and competitors/partners.

Table 2: Insurers in the industry can be broadly divided into three different ‘speeds’

You can fill out Table 3 below to get an idea of how fast your insurer is capable of reacting to market changes.

Both internal factors as well as external factors are evaluated, as external factors play an important role in an insurer’s commercial success and viability.

Process changerefers to the ease of changing internal processes within the insurer, such as claims services, approval processes, etc. An important part of innovation in insurance is to offer a seamless and very fast experience for the users, which requires incumbent insurers to change their existing processes – this will not be a significant issue for insurtechs due to their startup nature and very quick decision processes.

Innovative incumbents acknowledge this need and change their internal procedures to accommodate this – but they are still far from the nimbleness and flexibility of the insurtechs because the innovative incumbents require the innovations to integrate with existing systems and processes.

The rationale behind product changes (agility) is similar to the process change described above but needs to be treated separately, as some products and services can be integrated at arm’s length and thus require less integration and internal adjustments to work.

Organizational agilityis the insurer’s ability to react on changes, internal as well as external, and is generally an indication of how fast the organization can get projects approved and begin implementing them. It’s also an indicator for how fast the projects can be implanted once approved.

Table 3: A simple framework to assess the insurer’s current level of development and transformation speed

The organizational agility depends on the formal hierarchical structure and numbers of approval nodes each change request must pass before finally being approved and ready to implement.

Insurtechs have a flat structure with very few formal approval nodes, which means they’re able to approve and begin implementation of changes almost immediately, where laggards are at the opposite end of the spectrum, being slowed down by a large number of approval nodes and long- lasting approval processes.

The innovative insurers are placed in between, again because they’ve realized the need for agility and adjusted internal structures and processes to accommodate this somewhat.

The level of an insurer’s digital flexibilityis based on how open and flexible the IT systems are, especially the customer facing systems.

The laggards are basing their development almost purely on legacy IT systems, which most often are inflexible monolithic structures, making it a long process to carry out changes, let alone introduce products and functionalities.

Innovative insurers have typically been through one or more digital transformation projects, making them far nimbler than laggards in terms of IT connectivity and development, but they still lag behind the insurtechs, who have full control of each and every bit in their digital control room.

It takes cutting-edge talentto drive innovation through, regardless of company and industry, and here again the insurtechs are in front, as they wouldn’t have been insurtechs if highly competent people hadn't gotten together to create the insurer.

Innovative incumbents are partly innovative and forward-reaching because they’ve managed to hire the right key talent to develop their new digital universe, but even the best talent is bogged down by the existing organizational structures and processes.

Even laggards with exceptional talent will find it difficult to perform due to the organizational structures and systems.

Given this, it’s unlikely that they’re able to attract the right talent and in the right numbers as the right talent is focused on deliveries, which is too complex in laggard insurance companies.

The presence of talent, and the insurer’s willingness to invest, is key to determine the insurer's level of innovation.

Laggards don’t possess the talent and cannot have an innovation strategy due to their choice on building evolutionary on existing IT systems, where innovative incumbents very much have an innovation strategy, as this is the basis for their future development.

The delivery on the innovation strategy is still not as fast as with the insurtechs for the same reasons.

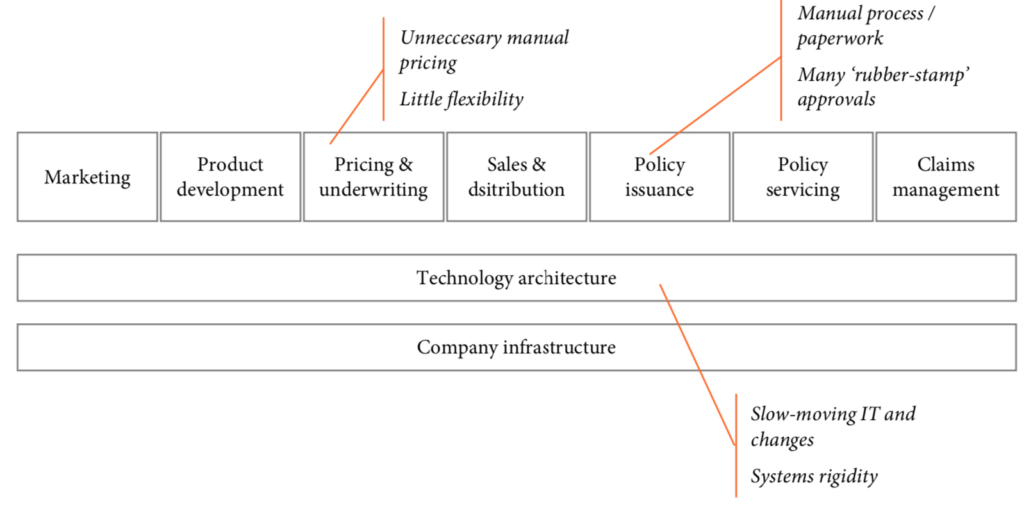

Mapping current pain points

A quick analysis of the insurer’s current speed and flexibility, combined with the identification of current pain points, sets the basis for understanding what kind of insurtech would add the most value in a partnership.

Pain points are generally specific processes or procedures that cause customers – or the organization – difficulties in getting their job done, whether it is buying a policy from the insurer, filing a claim or encountering bureaucratic red tape stopping marketing or sales processes required to keep – or establish – a competitive market position.

A fast and easy way to identify the pain points throughout the organization is to use the value chain and for each element to write down what is causing delays, inflexibility, challenges or downright customer issues.

Figure 2: Examples of mapping pain points to the elements in the insurance value chain

It is often a good idea to identify the pain points with colleagues to get a more accurate and unbiased view of the pains throughout the organization – done alone, the exercise can be biased toward specific areas that may not be representative for the organization.

These two small company analyses -- the speed of the insurer and current pain points -- provide a great starting point for understanding how insurtechs can help in the transformation of the insurer to a virtual and digital insurer. The next step is to search the marketplace for insurtech companies that offer products and services that match the insurer’s planned transformation journey.

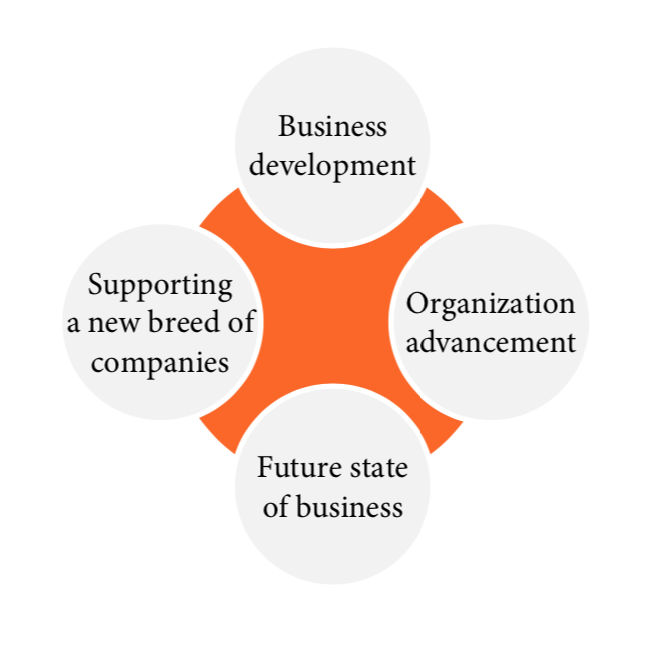

Benefits of partnering with insurtechs

It should already now be clear that partnering with insurtechs can make very good sense for the insurer to speed up and improve the digital transformation of the incumbent. There are at least four distinct advantages for insurers partnering with insurtechs.

Figure 3: Four major benefits for insurers by partnering with insurtechs

Business development

An obvious advantage of partnering with a tech- savvy professional is the opportunities it creates for new ways of selling existing products and introducing new products to the market.

However, as previously discussed, many insurtechs are building products and services that focus on optimizing existing business processes, including operational efficiency and claims costs savings (direct as well as indirect through reduction of operational expenses).

Business development can therefore be both in terms of increasing revenue through new sales channels or new products and in terms of improving business processes and hence reduce operating and claims costs.

Organizational advancement

It’s important again to underline that successful integration of an insurtech partner requires significant adjustments of the insurer’s organization to fully cater to new processes and products that are introduced through the partnership.

This is, of course, especially true when the insurtech’s product is focused on internal process development, where the full participation of the organization is required.

When done correctly, these organizational advancements will lead to a changed organization with a broader understanding and acceptance of new and more efficient ways of working.

Creating a future state of business

The organizational changes pave the way for creating a more advanced organization, capable of dealing with complex partnerships going forward.

This will not only benefit potential future insurtechs but also improve the way the incumbent insurers are handling their partnerships – the learnings from the insurtech partnership enable the insurer to revisit existing agreements with fresh eyes and new ideas on how to optimize for the future.

The insurtech partnership helps direct the attention on a future state, and a successful integration will instill a "can-do" attitude in the organization.

Working with insurtechs creates a source of continuous learning and organization development, enabling the insurer to stay competitive.

Supporting a new breed of companies

Apart from direct business and organizational benefits, partnering with insurtechs sends a strong message from the insurer to the market, a message of being at the forefront of the industry, which increases the insurer’s ability to attract talent, partners and customers.

Furthermore, the insurtech partnership actively supports the development of the next generation of insurers and partners, thereby supporting the development of the industry long into the future – the insurer leaves its mark on the industry.

Will all insurtechs do?

There are several areas the incumbent insurer should be aware of before venturing into a partnership with an insurtech.

The insurtech must be a real new technology service/product provider, and partnering with it should demonstrate a clear business leap for the insurer, as opposed to an incremental change.

Incremental changes and improvements are required and should be part of any company’s improvement programs, but to reap the full benefits, the insurtech must offer a truly innovative leap for the insurer.

Partnering with the insurtech should match the company’s current strategic direction – or actively be part of a new strategic direction set by the management. It makes little sense to spend time, money and organizational effort to partner with an insurtech if the partnership will not take the incumbent insurer a great step toward the set strategic targets.

Following the discussion on organizational learning and culture, it’s an extreme benefit if there’s a people/culture match even before the partnership is agreed upon.

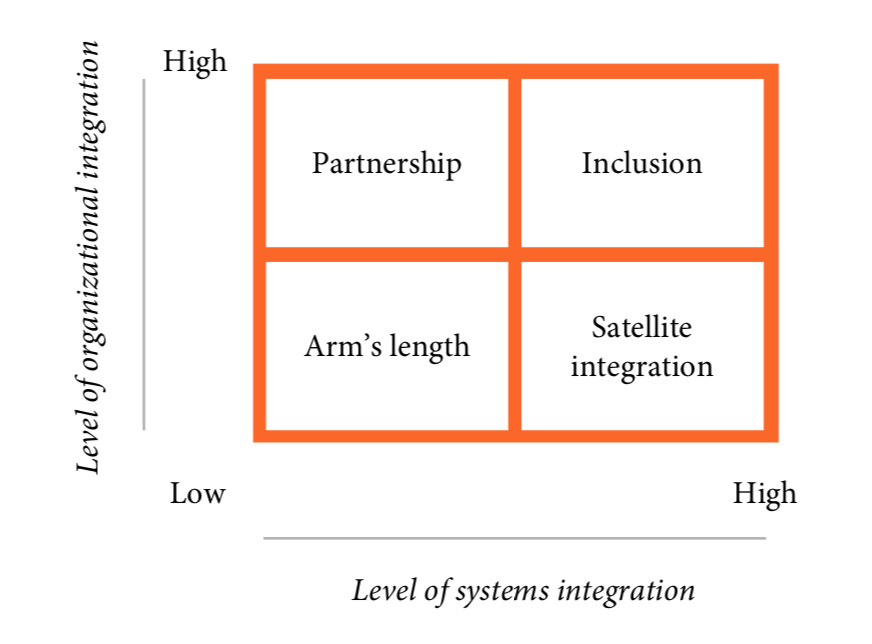

How to integrate: four basic ways

It’s imperative to understand that this is two very different worlds: an agile and very modern small-business environment and the more bureaucratic and institutionalized environment of the incumbent insurer. At some point, these must match to make the partnership a success, and positive vibes between the partners beforehand will ease this process.

There are different ways of considering structuring the partnership between the insurer and the insurtech, all of which have different advantages and disadvantages to consider – and to be aware of when the partnership hits the insurer’s organization.

Figure 4: Four different ways insurers can integrate or partner with insurtechs

Arm’s length

Partnering with an insurtech and managing the relationship at arm’s length makes it little more than an external distribution partner or an outsourced claims management function. It is very easy for the insurer to administer, as there will be minimal disturbance and interruption of the daily operations, processes and organization.

The arm’s length will have very limited transformation effect on the insurer.

Satellite integration

A high level of systems integration with little organizational integration is typical for insurtechs that connects to the insurer via APIs or using the insurer’s microservices for a specific set of transactions.

In this scenario, there will be little organizational red tape, but some IT challenges can be expected as the IT unit must work and integrate with the insurtech.

Partnership

Insurtech partnerships with little systems integration and high levels of organizational integration typically rely on the technology from the insurtech and require a high level of cooperation and coordination between the insurtech and the insurer – advanced use of artificial intelligence for underwriting or fraud detection could be examples of this, where the insurer in many cases only needs to export simple data sets for the insurtech’s solution to work with.

This can have quite a few organizational challenges as the incumbent organization can get the "not invented here" syndrome and feel the insurtech is coming and interfering with the daily work.

Inclusion

Integrating the insurtech into the insurer will most likely be the partnership model with the biggest return on investment, but at the same time this model poses the greatest challenges, as both systems and organizations must be included and aligned with each other.

It’s safe to say the most significant risk is a clash of cultures between a well-established, well-regulated, experienced incumbent insurer and a newly founded, agile, dynamic and "free-of-rules" insurtech.

Performance indicators – the cornerstone of success

The organizational and cultural strain caused by introducing external parties to the organization – or simply caused by digital change initiatives – can be somewhat reduced by creating a set of clearly articulated targets and goals for the company, the units, the teams and the individuals.

To be successful, the targets and goals must be connected, so the teams and units will be depending on each other to achieve them. This will initially force collaboration that, over time, if managed, will reduce the cultural tensions – working toward the same target is a strong motivator.

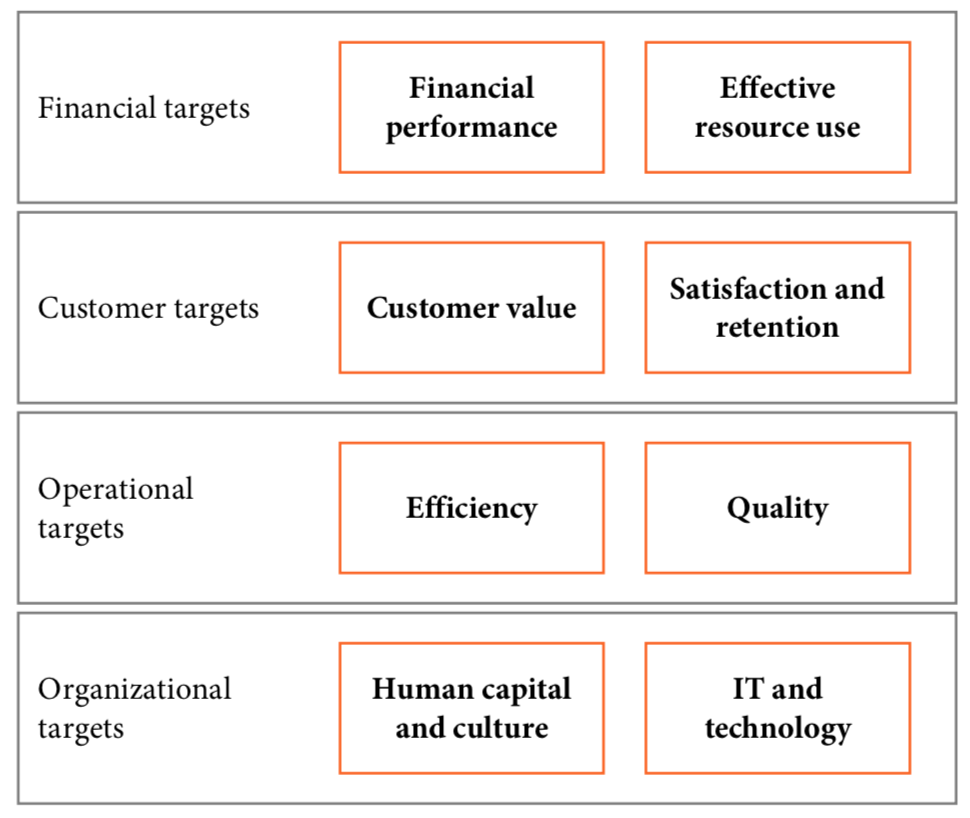

A fast way of setting up a framework for target and goal setting is to use the principles from the balanced scorecard, illustrated below.

Figure 5: The balanced scorecard high-level structure Source: Balanced Scorecard Institute

One of the major strengths of the balanced scorecard is that targets are set for the organization as a whole and then cascaded down to the business units, teams and individuals. This provides an overview of how each goal and target is supporting the organization in achieving the end targets.

Given the insurer already has a set of financial performance targets, the balanced scorecard is used to set underlying goals for the units working with the digital transformation and insurtech partnerships, all aiming at supporting the insurer in reaching the overall targets.

This approach can further be used to create business cases for investments and calculate return on investments, because of the specificity of the targets and goals required to create a successful balanced scorecard.

When setting the goals in the scorecard, it can be defined how investments help move the performance indicators toward the goals and therefore illustrate the value of the investment.

Final thoughts

Insurtechs are not the only answer to transforming incumbent insurers into virtual and digital insurers, but they may be able to play a very important role for the insurer in achieving the virtual vision.

When embarking on a continuous transformation journey, it is vital for insurers to keep the overall picture of the organization, its interdependencies, culture and modus operandi in mind.

For insurers to become agile, virtually and digitally competent organizations, they must ensure proper adjustment and development of the underlying key systems, which include organizational structure, management processes and culture.

Merely partnering with insurtechs or other companies does not make these challenges disappear, though – and conquering these challenges are key for future and sustainable success.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

“Social inflation” is considered one of the major emerging risks that the insurance industry must face. While people may misconstrue the term as relating to the rising impact of social media on online behavior of netizens, it has actually to do with increasingly hostile legal environment that insurance carriers are facing today. This manifests in the form of much larger verdicts, liberal treatment of claims by boards, more aggressive plaintiff bars, etc. This article explains the trend and describes measures that carriers can deploy to keep a check on increasing legal expenditure.

Here are some signs of the phenomenon:

A major P&C insurer anticipates $40 million in quarterly legal costs for property losses alone

There is a 94% increase in assignment of benefit (AOB) lawsuits in the state of Florida in the last five years

An increased probability of "nuclear verdicts" (> $10 million) is a real trend. In 2018 alone, the top 100 verdicts ranged from $22 million to $4.6 billion

Here are some factors driving the trend:

Litigation Funding: Propelled by easy capital availability, a new class of plaintiff attorney funding model has emerged in the last 10 years. Essentially, this model provides funding for legal expenses to plaintiff attorneys in exchange for a portion of the judgment or settlement. The model is good in the sense that it levels the playing field against large, well-funded corporations, but the unintended consequences (for insurance companies) is an exponential increase in attorney representation and pursuit of aggressive legal strategies. Approximately $9 billion has been committed to this "industry."

Rising anger against big corporations: The very premise of the big corporation versus the individual scenario is driven by anger. The perception among the consumers and the jurors is that a corporation has only one goal: profit. Stagnation of incomes/wages is another contributing factor to this mindset. Big businesses in America like to talk about the good jobs they provide, but median salaries in the U.S. have been flat for decades. This is not because of a failure of workers to become more productive; there were gains in productivity, but they did not go to workers. Gains mostly flowed to the organizations and their shareholders, including executives who received sizable stock-based compensation. Hourly compensation for workers remained practically flat.

Large verdicts being driven by general social pessimism and jury sentiments: New and interesting patterns are being observed in jury behavior, especially in personal injury and liability claims. Emotion and trust play a big role in how a jury rules. Some of the key reasons behind these large verdicts are: jurors’ distrust in big corporations and their lawyers; jurors paying less attention to lengthy testimonies and complex explanations; impact of social media on how millennial jurors view the court system; impact of emotional stories on how a jury thinks; and the “what if it were me?” attitude influencing how jurors approach justice.

Leaving aside the financial burden from social inflation, which is quite significant on its own, increased litigation also affects carriers in other ways. There can be inaccuracies in reserving, which is based on counsel's estimates of litigation spending. There can be negative press and poor customer engagement/satisfaction. And claims can increase in complexity, delaying settlement. .

Many insurers are either in the early stages of dealing with social inflation or are not moving as fast as they'd like on the problem. The most common reasons include:

Claim handling practices are often inadequately data-driven

There is limited ability to foresee litigation

There is lack of trust in analytical models

The company takes a semi-reactive approach for claim settlement and negotiations

Assignments are inefficient, either to claim handlers or attorneys

What can insurers do to manage this growing challenge?

Enter machine learning and artificial intelligence

Use of analytics from first notification of loss (FNOL) until the claim is paid is now a norm rather than a competitive edge. All large carriers invest heavily in use cases such as fraud detection, severity-based claim assignment, automatic loss estimation, recovery optimization, etc. However, given the complex nature of how litigated claims are handled, only a few top U.S. carriers are able to weave these capabilities effectively into business processes. Insurance carriers that successfully use analytics to drive business process change in claims litigation will stay ahead of this massive threat.

There are two unmistakable trends that carriers need to leverage:

Aggressive use of information sitting in claims and policy systems (structured attributes, adjuster notes) to develop signals around plaintiff attorney behavior. These signals then need to be deployed within claims operations to encourage early case assessment and litigation prevention.

Use of increasingly clean and comprehensive sources of external litigation information (from state courts, where most insurance litigation lies) to inform your litigation strategy. This includes past verdicts information by venues, judges, attorney firms, case types, etc. A thoughtful use of this information can help claims adjusters and defense attorneys devise the litigation strategy to avoid worst outcomes. There are multiple firms providing research tools that are based on these. Our recommendation, however, is for carriers to ingest the information, merge it with internal claims data and develop models and tools providing a comprehensive view

How carriers can leverage this trend

Carriers can use predictive and descriptive analytics solutions in claims management to mitigate the problem. At a high level, such solutions can lower ballooning legal costs by avoiding litigation and optimizing litigation strategy. Both these approaches call for incorporating advanced analytics processes and models at the key steps of the claim settlement process. This includes:

Advanced analytics and machine learning models to predict and avoid litigation and post-suit strategy formulation

Natural language processing (NLP) to leverage unstructured data and extract additional insights

External data ingestion to augment internal data and enhance model accuracy

Enhanced data management capabilities

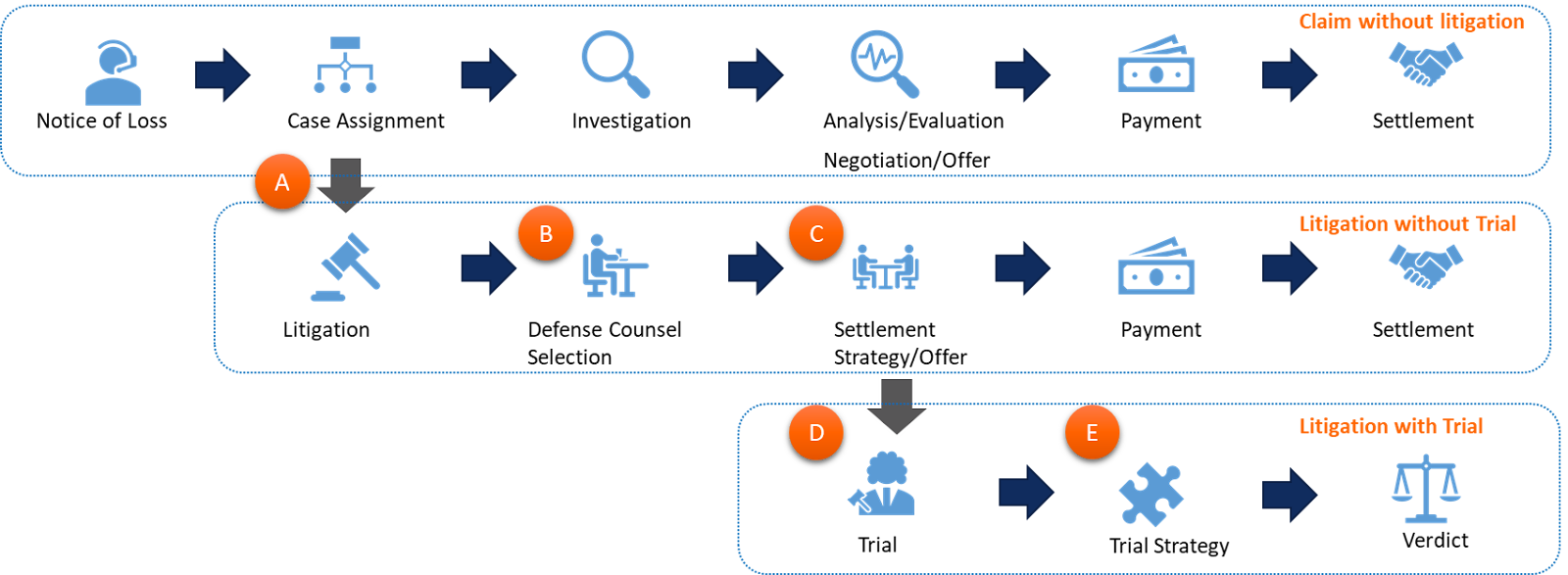

Any insurance claims raised can result into any of the three possible outcomes: claims without litigation, claims that involve litigation without trial and claims that involve litigation with trial. With the help of the aforementioned technologies, carriers can engineer the following mechanisms in the claims management process (Figure 1) to optimize the legal expenditure for a given product:

A - Prediction of litigation likelihood

B1 - Defense counsel selection

B2 - Law firm benchmarking

C1 - Attorney insights

C2 – Prediction of settlement failure

D - Legal activity duration, legal expense prediction

Claims data within insurance companies is being increasingly seen as a key asset, not a byproduct of the claims process. However, the path to using internal and external sources of data to drive business outcomes is long and arduous. It is becoming increasingly important for carriers to incorporate insurance analytics processes geared toward optimizing legal spending. To achieve this, insurers require a combination of capabilities to these engagements, i.e. ability to handle big data, ability to develop advanced analytics solutions and knowledge of "what, why and how to deploy" in claims business processes.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

When will the COVID-19 pandemic end? Will it end? P&C insurance, like all other business sectors, is faced with a time of unprecedented uncertainty. There are always multiple external factors to consider when developing strategies and adjusting plans. Now, layer into the traditional elements all the fallout from the pandemic, restrictions on economic activity, work-from-home, virtual schooling, social unrest and political/legislative uncertainties. How are all of these developments affecting P&C insurer technology strategies and plans?

SMA has been tracking changes to budgets and plans since the pandemic hit the U.S. hard in early 2020 via Market Pulse Surveys and our work with insurers. This blog summarizes some of the big themes regarding overall tech plans and digital transformation.

In the spring and moving into summer, personal lines insurers were aggressively revising tech plans. Most navigated the transition to #WFM smoothly and experienced lower claims due to changing patterns. Even with large rebates to policyholders and auto premiums down slightly, the financial picture looked positive for personal lines companies. As a result, many were accelerating their overall tech spending and digital transformation projects.

Commercial lines companies were faced with different circumstances during that time frame. Pandemic-related claims were rising, and riots across the U.S. generated a whole new set of claims. Many commercial lines companies were setting aside large reserves in anticipation of more difficult financial times ahead. As a result, tech budgets and plans were mixed for commercial lines companies. A quarter of the companies were slowing down or retrenching, while others reshaped their plans without changing budget levels. A small portion were even accelerating plans.

Fast forward to September and a look at fourth quarter plans. In some ways, the plans for personal and commercial insurers have flipped. Personal lines companies have moderated their plans, while commercial lines are now speeding up. Digital transformation is still a big driver of activity for personal lines, and a quarter of the respondents continue to accelerate their plans. However, there is a decline in the number of companies that are accelerating overall tech spending. Meanwhile, fewer commercial lines companies are pausing projects or cutting back budgets. As the industry settles in for the long haul, there seems to be a balancing out of plans for the remainder of the year.

An early glimpse into 2021 is fascinating. As insurers look to the future, there is a realization that digital transformation needs to be at the forefront of their strategies. Plans and budgets are just being developed now, but it appears as though there may be significant increases in overall tech spending and a rapid acceleration of digital transformation plans for both personal and commercial lines insurers.

Most recognize that the world will not be reverting to the way it was pre-COVID-19. Many things have forever changed and shifted to digital/virtual modes. Self-service capabilities will continue to be a focus. And the movement toward higher levels of straight-through-processing for both underwriting and claims will be accelerated. At the same time, insurers are positioning to lower infrastructure costs by reducing or repurposing physical locations, cutting back on employee and vendor travel expenses, shifting more to e-delivery instead of printing and mailing documents and more.

The industry is certain to experience more unexpected shocks along the way as industries and society adapt to events and movements born out of the global COVID-19 crisis and significant shifts in the economy, demographics, politics and other external factors. It will be a wild ride, but insurers are pushing the envelope on digital transformation to become more agile and responsive to changes during this volatile time.

Mark Breading is a partner at Strategy Meets Action, a Resource Pro company that helps insurers develop and validate their IT strategies and plans, better understand how their investments measure up in today's highly competitive environment and gain clarity on solution options and vendor selection.

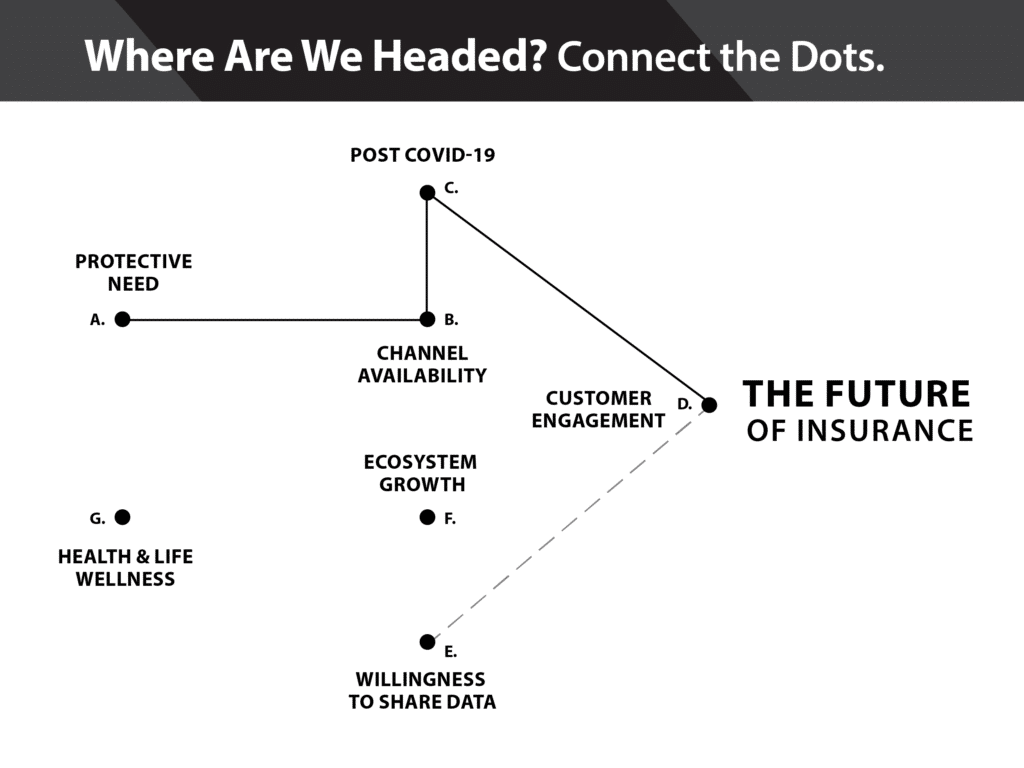

When executives are looking at future business scenarios, they are often called upon to “connect the dots.” If we draw a line from A to B to C to D, what kind of future scenario emerges? In which direction are the dots pointing?

Sometimes the lines are fuzzy. The dots don’t quite line up. The possible futures are too many to count. The next steps are nearly invisible. In fact, coming out of COVID-19, some industries, such as the food industry, real estate, automotive manufacturing and travel, are going to be faced with some, “So, what’s next?” moments. The train of progress might be leaving the station, but it’s anyone’s guess which platform you use to hop on board.

This is not the case with life insurance. Though the numbers of policies sold may vary and the types of life products may have some new wrinkles, if we connect the trends and dots today, we get an excellent picture of tomorrow. We know where this train is headed. We also know that your ticket to get on the train will be the launch of a new life business model.

We surveyed consumers asking them a range of questions related to health, wealth, wellness and life insurance. The survey results highlight a rapid shift, particularly by millennials and Gen Z, to wanting a lifestyle experience across life, health, wealth and wellness, rather than just a life insurance transaction.

Majesco’s survey sheds important light on several of the dots that can help insurers connect today’s strategies to tomorrow’s futures.

Life insurance – from boom to bust

On the eve of the Great Depression, there were more than 120 million life insurance policies, the equivalent of one policy for every man, woman and child living in the U.S. Once again, following World War II, the economic boom in the U.S. fueled a rise in life insurance ownership; by the mid-1970s, 72% of adults and 90% of households with two parents owned life insurance.

Fast forward to today, and only 54% of American adults own life insurance, according to a recent LIMRA report. That is down nine percentage points from 2011. Only 34% of Millennials own individual life policies.

Over the course of a century, life insurance went from a boom to a bust. What went wrong?

Growth and viability of the life insurance industry is vitally connected to the major trends redefining insurance, including demographic and market trends, customers’ expectations and their adoption of new technologies. Insurers’ long-held business assumptions and operating models were built to support “traditional” insurance approaches for products, channels, pricing and customer engagement, and this has not dramatically changed since the early 18th century when the first product mortality tables and structures were introduced. Innovative products like variable life, critical illness or long-term care still followed a similar business foundation.

However, today’s customers are increasingly digitally adept, with higher expectations, different needs and a demand for better experiences that are not met with the “traditional” insurance approach. Unless insurers develop a new approach, they will be unable to capture customers within the millennial and Gen Z segment, right as those customers become the dominant buyers beginning next year.

This new generation is not satisfied with traditional insurance processes, products and business models. They have grown up in a digital world. They expect and demand digital capabilities. Encouragingly, there are opportunities for growth and glimmers of revival of life insurance ownership on the horizon – but with a focus on engaging customers differently…and digitally.

Forbes recently reported that, starting January 2020, online life insurance sales increased 30% to 50% for companies with speedy apps that used data/algorithm-driven underwriting, particularly for those 45 and under, the prime growth market of millennials and Gen Z. In contrast, agent-driven sales were down by up to 50%. The COVID-19 crisis is accelerating the online competition started by new players such as Fabric, Ladder Life and Haven Life.

A recent Nielsen survey found that by mid-March, when COVID-19 reached critical concern, there was a significant increase in online shopping and that 25% expected this to continue post-COVID-19.

The COVID-19 crisis has contributed to a digital wildfire that has exposed less than desirable customer experiences due to manual, paper-bound processes and non-digital transactions. Multiple trends are pushing life insurance out onto a digital limb.

Once again, the life insurance industry is faced with an opportunity for growth and capturing a new generation of customers. But, to do so, insurers must adapt their business approach to meet a vastly different set of needs and expectations.

Generational views on life insurance are shifting to a holistic perspective encompassing health, wealth and wellness. Majesco’s research identified key differences between millennials and Gen Z versus Gen X and Boomers. Some of the highlights include:

Life insurance value is trending upward.Millennials and Gen Z believe life insurance is more important – 79% as compared with 60% for Gen X and Boomers. The younger customers also have a larger array of reasons why life insurance is important, many of which are based on new behaviors and needs.

Millennials and Gen Z are very willing to share personal data if they benefit from it. Millennials and Gen Z are willing to share their personal information and data 25% to 39% more than the older generations.

Millennials and Gen Z want more than a transaction – they want to manage their life more holistically. Millennials and Gen Z outpace Gen X and Boomers in wanting access to all health, wealth and wellness areas by 17% to 33% or more. The younger generation seeks information and advice for a variety of areas: health, financial planning, legal, tax, mortgage loads, bank balances, etc.

Younger generations want access to their information. They want information on their policies, medical records, fitness data and household purchases. There is strong interest in possible value-added services.

Millennials and Gen Z will use a wider and larger number of channels. This includes traditional agents as well as those they have existing relationships and loyalty with, including Big Tech like Amazon, Apple and Google.

This new era of life insurance is so much different than even just a few years ago. It will pressure insurers to develop products and services that are more affordable, digital-first, simpler, tailored to very specific needs and grounded in trust. Customer will want new, digital products like on-demand, single-item and embedded coverages and value-added services, that are bundled in a way to help customers manage their lives.

Life insurers must reimagine the scope of what they will offer to customers. They must think of a compelling customer experience that is wrapped around a risk product and of value-added services that are part of a broader health, wealth and wellness ecosystem.

The status quo is no longer an option

We see the impact of the status quo with the 50-year-long decline in life insurance ownership. In this new decade, a new life insurance opportunity exists for those who will participate in a broader health, wealth and wellness ecosystem and the growing insurable opportunities… offering a new boom era for life insurance.

Capturing the boom — turning a transaction into an experience

The success of life insurance, in part, depends on the longevity of the human body. We predict longevity and use our mortality numbers to gain the ratios we need to keep our business healthy. In the new realm of life insurance, that formula is backward. Start with the human body. Make it healthier. Improve our systems of health data and find out that people are sick before their sickness becomes an issue. Help them improve their wellness as a part of their natural lifestyle. Add lifestyle and financial benefits to the customer experience. Add years to lives. Improve mortality, lives, finances, satisfaction and security.

The 2020 LIMRA study picks up on the idea of the better life/health relationship within the life insurance industry.

“This personal health push provides an opportunity for the life insurance industry. What if life insurers — typically focused on mortality — could “flip the frame” to disease prevention and longevity? What if they became partners in the effort to live the longest, healthiest life possible?"

To retain the customer and revenue, insurers must rethink their scope away from a life insurance transaction to a broader lifestyle experience across health, wealth and wellness.

Highly networked, data-driven, value-added business models are emerging, within and outside of insurance. They are redefining the customer journey, and the entire customer relationship, across a broader set of health, wealth and wellness options across insurance and financial services.

Get Involved

Our authors are what set Insurance Thought Leadership apart.

Denise Garth is senior vice president, strategic marketing, responsible for leading marketing, industry relations and innovation in support of Majesco's client-centric strategy.

Six Things Newsletter | October 6, 2020

In this week's Six Things, Paul Carroll catches a glimpse of the future of insurtech. Plus, why haven't more startups failed; COVID, and how to pivot to innovation; 6 cybersecurity threats for insurers; and more.

In this week's Six Things, Paul Carroll catches a glimpse of the future of insurtech. Plus, why haven't more startups failed; COVID, and how to pivot to innovation; 6 cybersecurity threats for insurers; and more.

Today’s announcement that Bold Penguin is acquiring RiskGenius marks a milestone in the maturation of the insurtech movement. I’ve known Chris Cheatham, the co-founder and CEO of RiskGenius, for years and have closely followed the developments of what I have often described as my favorite insurtech. So, under embargo, I chatted with Chris to ask him to summarize how he surfed the first wave of insurtech so successfully and where he sees the movement going from here.

The deal feels to me like maturity because it exemplifies how insurtech has moved past some early ideas (e.g., that a Big Tech company like Amazon or Google would invade insurance and lay waste) and some early models (such as peer-to-peer provision of insurance coverage) that have yet to pan out. Instead, the Bold Penguin acquisition of RiskGenius exemplifies what I suspect will be the dominant model for some time: one where a company acquires a smaller firm for a particular skill or technology and incorporates it into the acquirer’s products and services... continue reading >

Insurance Thought Leadership (ITL) delivers engaging, informative articles from our global network of thought leaders and decision makers. Their insights are transforming the insurance and risk management marketplace through knowledge sharing, big ideas on a wide variety of topics, and lessons learned through real-life applications of innovative technology.

We also connect our network of authors and readers in ways that help them uncover opportunities and that lead to innovation and strategic advantage.

In most insurance companies, it is time to take out the 2020 budget and see where line items need to move for next year. Did the claims organization meet objectives? If not, what adjustments need to be made? What technology partners were aligned with the organization at the beginning of the year? And how do those initiatives need to be moved forward?

It sounds like a reasonable place to kick off from, right? Actually, the answer is probably “no.” If 2020 claims plans are the baseline for 2021, I conjecture that this is the wrong place to start.

SMA’s recently released report, Claims Transformation Reset: The Impact of COVID-19, lays out the case for why claims transformation and claims operations have a new performance baseline because of COVID-19. In most cases, many things changed, such as work-from-home (WFH) practices and interactions with customers that are no longer being done face-to-face. The pandemic’s impact is generally part of everyone’s view, but it is still evolving daily.

It is vital for claims executives to reassess other external forces affecting claims operations to effectively plan for 2021, not the least of which are workforce evolution trends and the rapidly changing digital connected world. Much has happened in these two areas, as well as three others outlined in the report. The environment that existed when 2020 plans were developed has dramatically changed.